REVISED BALANCESHEET AS PER SCHEDULE VI

INTRODUCTION Schedule VI to the Companies Act, 1956 (‘the Act’)

provides the format in which companies registered under the Act prepare and present their financial statements

As per notification dated 28th March, 2011 by Ministry of Corporate Affairs, the revised Schedule VI is applicable to balance sheet & profit & loss account to be prepared for the financial year commencing on or from 01st April 2011

GENERAL INSTRUCTIONS Compliance with the Act and/or Accounting Standards: Where compliance with the requirements of the Act

including Accounting Standards as applicable to the companies require any change in treatment or disclosure the said changes can be made.

Disclosures are required by the Companies Act shall be made in the notes to accounts

Additional disclosures specified in the Accounting Standards shall be made in the notes to accounts or by way of additional.

Notes to accounts shall contain information in addition to that presented in the Financial Statements and shall provide where required

a) narrative descriptions or disaggregation's of items recognized in those statements.

b) information about items that do not qualify for recognition in those statements.

Presentation of figures:– Where Turnover:

o < Rs. 100 crores = Figures to be in nearest hundreds, thousands, lakhs or millions or decimals thereof.

o > Rs. 100 crores = Figures to be in nearest lakhs or millions or decimals thereof.

Once a unit of measurement is used, it should be used uniformly in the Financial Statements

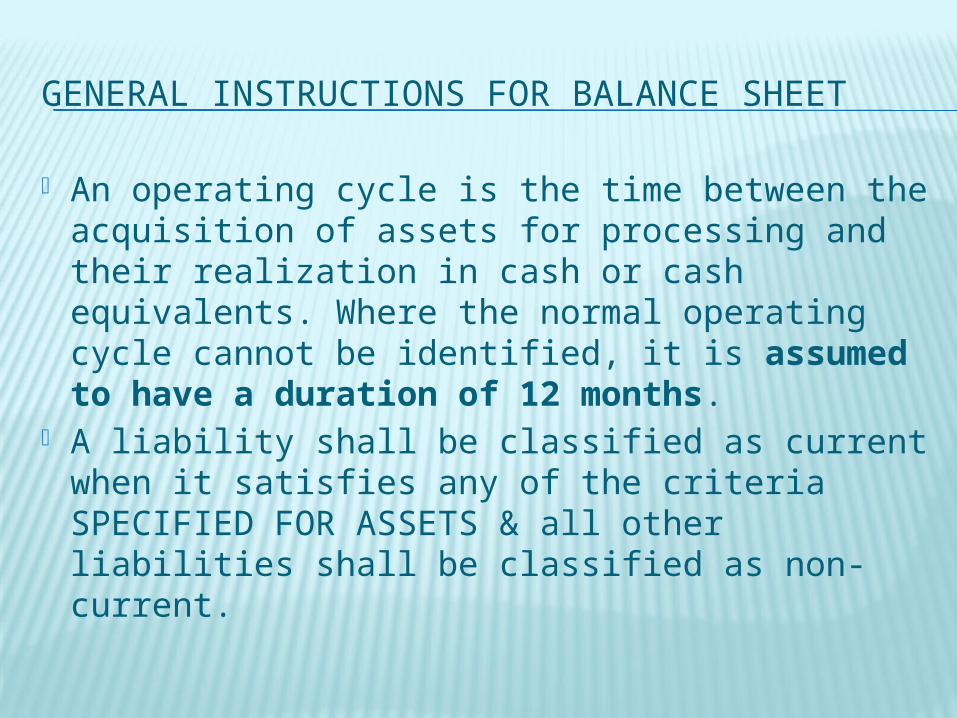

GENERAL INSTRUCTIONS FOR BALANCE SHEET

An operating cycle is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. Where the normal operating cycle cannot be identified, it is assumed to have a duration of 12 months.

A liability shall be classified as current when it satisfies any of the criteria SPECIFIED FOR ASSETS & all other liabilities shall be classified as non-current.

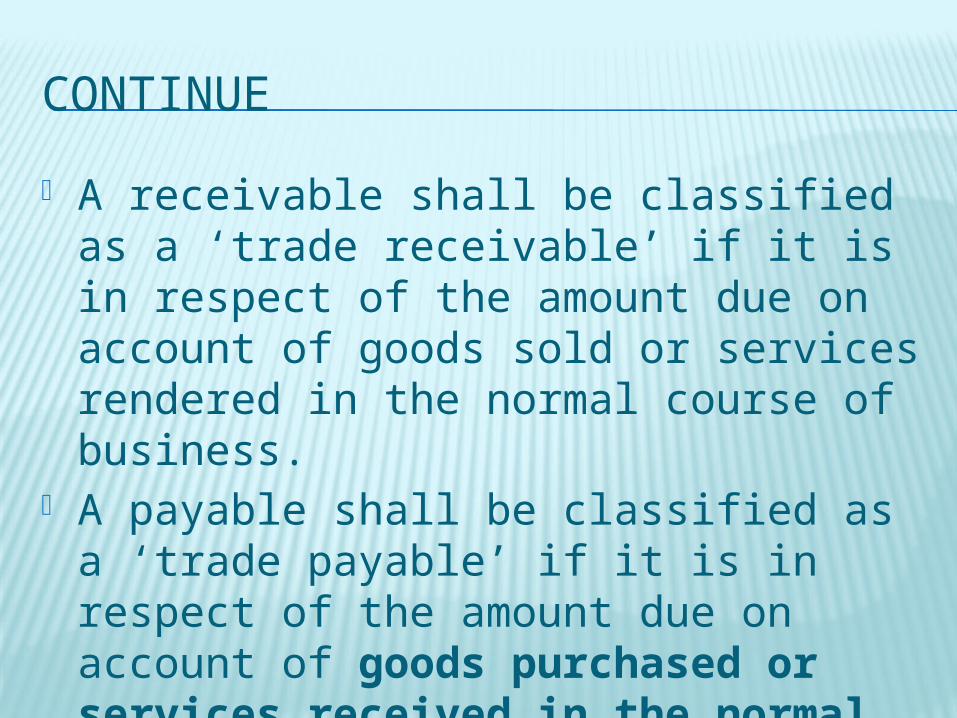

CONTINUE

A receivable shall be classified as a ‘trade receivable’ if it is in respect of the amount due on account of goods sold or services rendered in the normal course of business.

A payable shall be classified as a ‘trade payable’ if it is in respect of the amount due on account of goods purchased or services received in the normal course of business.

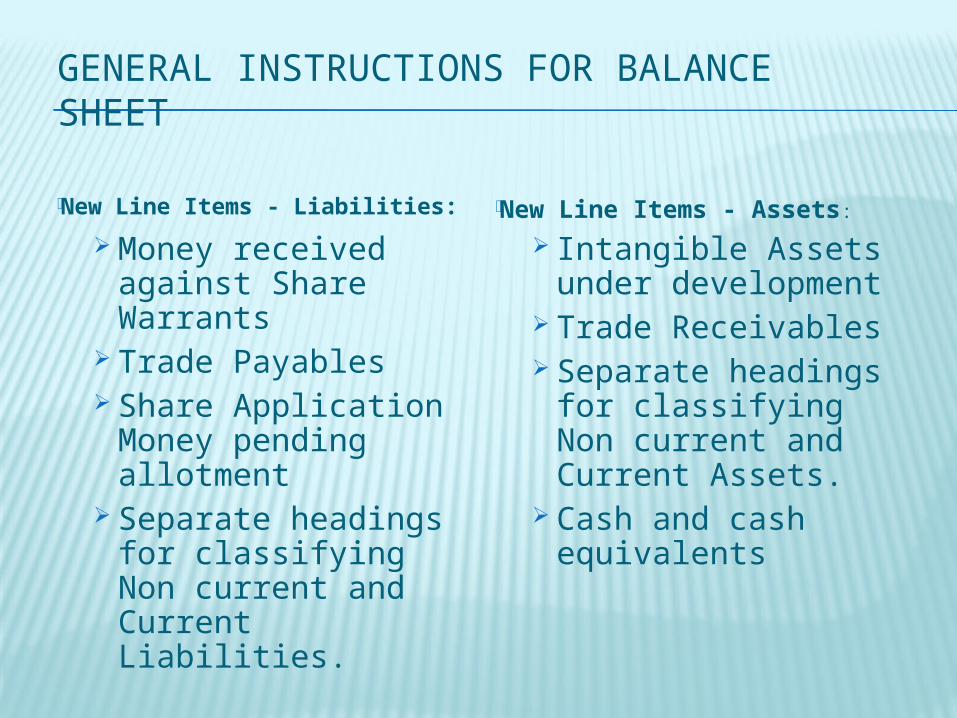

GENERAL INSTRUCTIONS FOR BALANCE SHEET

New Line Items - Liabilities: Money received

against Share Warrants

Trade Payables Share Application

Money pending allotment

Separate headings for classifying Non current and Current Liabilities.

New Line Items - Assets:

Intangible Assets under development

Trade Receivables Separate headings

for classifying Non current and Current Assets.

Cash and cash equivalents

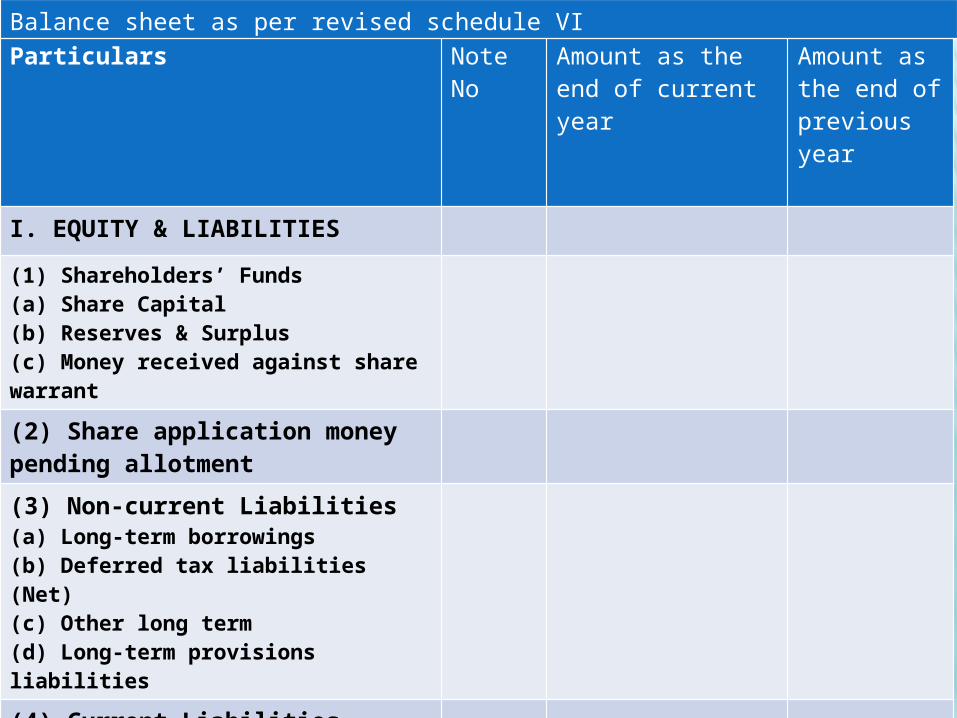

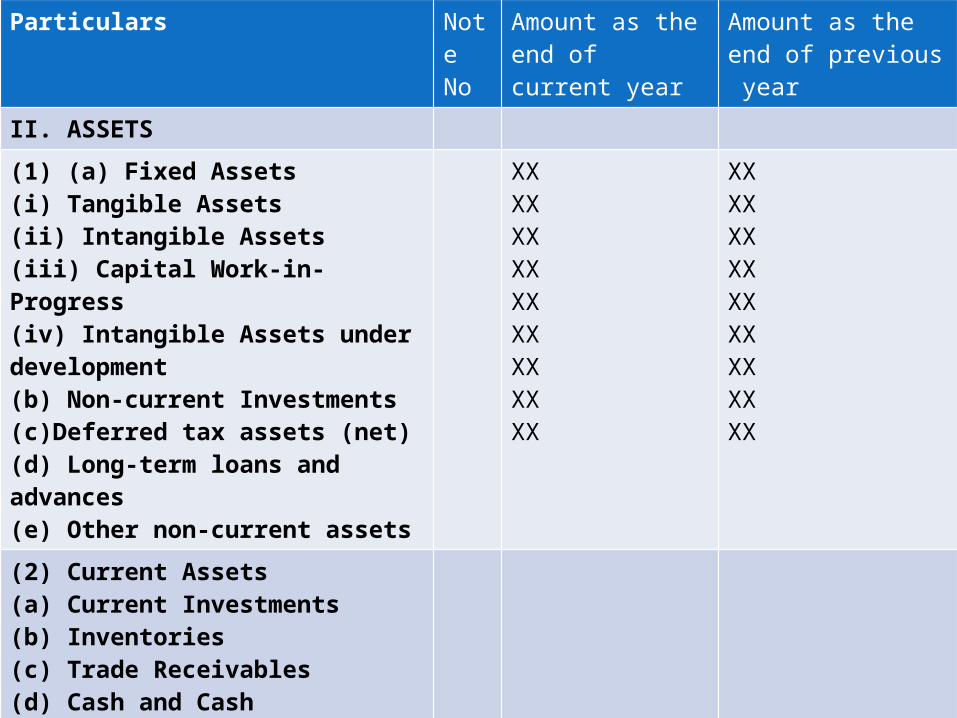

Particulars Note No

Amount as the end of current year

Amount as the end of previous year

I. EQUITY & LIABILITIES

(1) Shareholders’ Funds(a) Share Capital(b) Reserves & Surplus(c) Money received against share warrant

(2) Share application moneypending allotment

(3) Non-current Liabilities(a) Long-term borrowings(b) Deferred tax liabilities (Net)(c) Other long term(d) Long-term provisions liabilities

(4) Current Liabilities(a) Short-term borrowings(b) Trade payables(c) Other current liabilities(d) Short-term provisions

TOTAL

Balance sheet as per revised schedule VI

Particulars Note No

Amount as the end of current year

Amount as the end of previous year

II. ASSETS

(1) (a) Fixed Assets(i) Tangible Assets(ii) Intangible Assets(iii) Capital Work-in-Progress(iv) Intangible Assets under development(b) Non-current Investments(c)Deferred tax assets (net)(d) Long-term loans and advances(e) Other non-current assets

XX XXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXX

(2) Current Assets(a) Current Investments(b) Inventories(c) Trade Receivables(d) Cash and Cash equivalents(e) Short-term loans and advances(f) Other current assets

Total

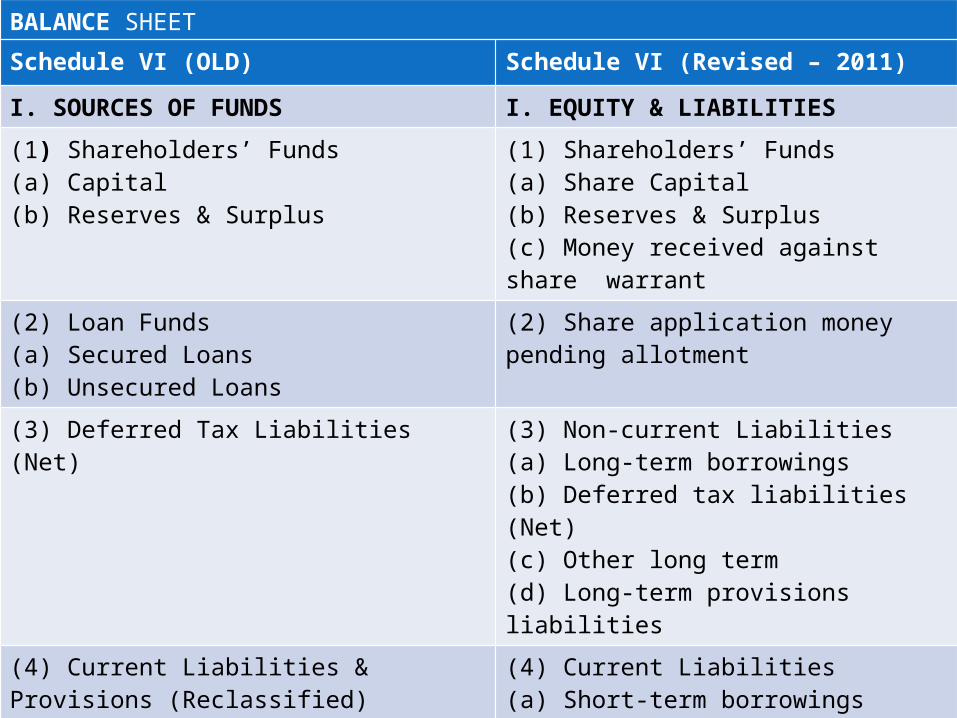

BALANCE SHEET

Schedule VI (OLD) Schedule VI (Revised – 2011)

I. SOURCES OF FUNDS I. EQUITY & LIABILITIES

(1) Shareholders’ Funds(a) Capital(b) Reserves & Surplus

(1) Shareholders’ Funds(a) Share Capital(b) Reserves & Surplus(c) Money received against share warrant

(2) Loan Funds(a) Secured Loans(b) Unsecured Loans

(2) Share application moneypending allotment

(3) Deferred Tax Liabilities(Net)

(3) Non-current Liabilities(a) Long-term borrowings(b) Deferred tax liabilities (Net)(c) Other long term(d) Long-term provisions liabilities

(4) Current Liabilities &Provisions (Reclassified)(a) Liabilities(b) Provisions

(4) Current Liabilities(a) Short-term borrowings(b) Trade payables(c) Other current liabilities(d) Short-term provisions

TOTAL TOTAL

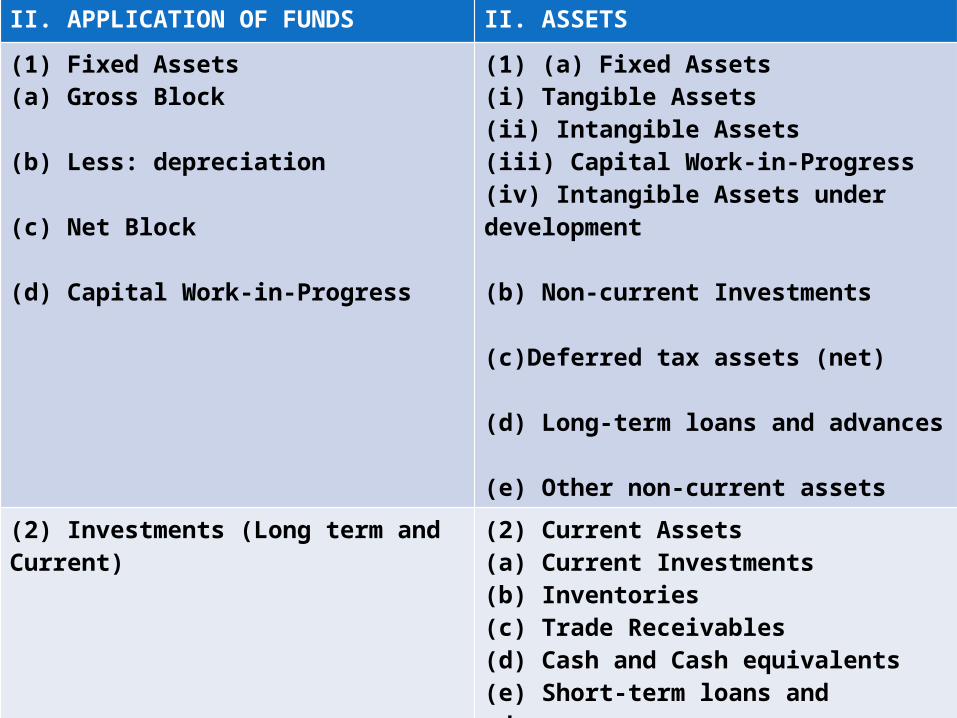

II. APPLICATION OF FUNDS II. ASSETS

(1) Fixed Assets(a) Gross Block

(b) Less: depreciation

(c) Net Block

(d) Capital Work-in-Progress

(1) (a) Fixed Assets(i) Tangible Assets(ii) Intangible Assets(iii) Capital Work-in-Progress(iv) Intangible Assets under development

(b) Non-current Investments

(c)Deferred tax assets (net)

(d) Long-term loans and advances

(e) Other non-current assets

(2) Investments (Long term andCurrent)

(2) Current Assets(a) Current Investments(b) Inventories(c) Trade Receivables(d) Cash and Cash equivalents(e) Short-term loans and advances(f) Other current assets

(3) Deferred Tax Assets (Net)

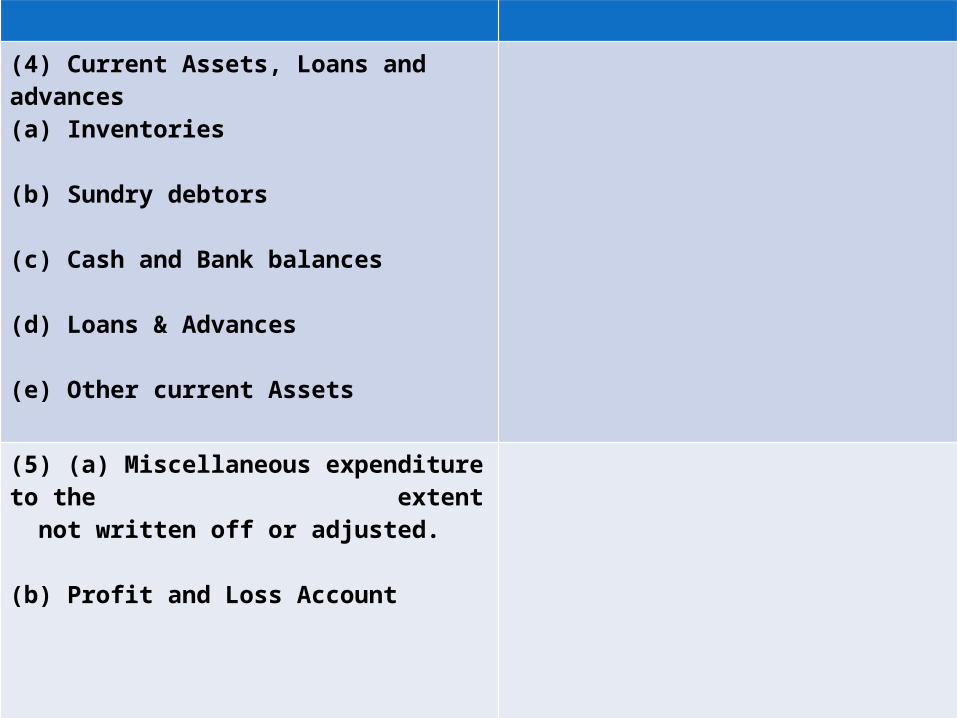

(4) Current Assets, Loans and advances(a) Inventories

(b) Sundry debtors

(c) Cash and Bank balances

(d) Loans & Advances

(e) Other current Assets

(5) (a) Miscellaneous expenditure to the extent not written off or adjusted.

(b) Profit and Loss Account

TOTAL TOTAL

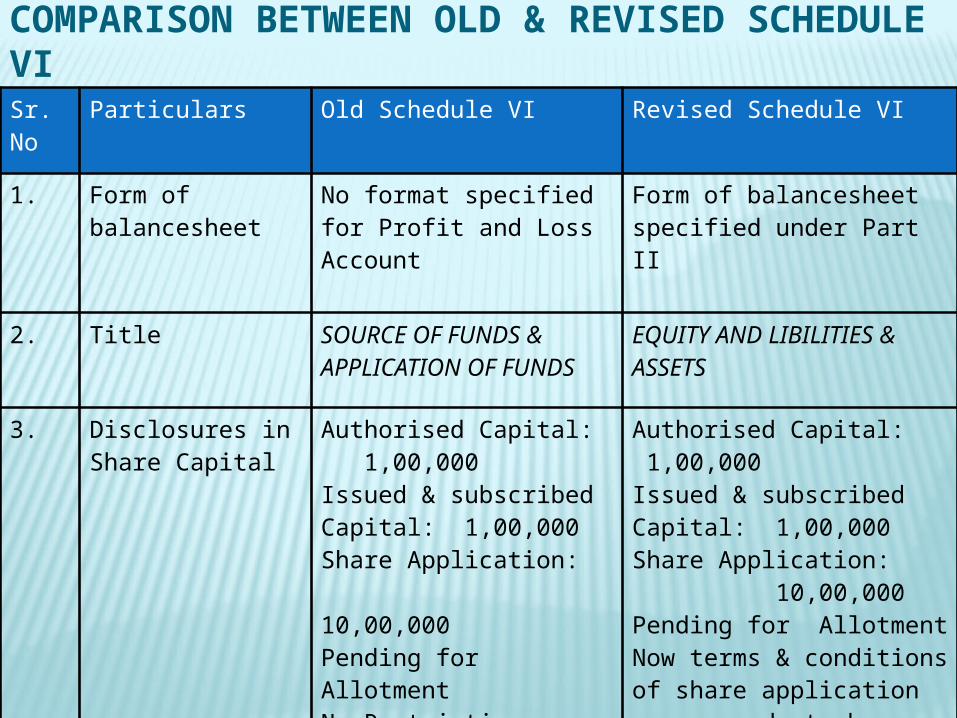

COMPARISON BETWEEN OLD & REVISED SCHEDULE VISr. No

Particulars Old Schedule VI Revised Schedule VI

1. Form of balancesheet No format specified for Profit and Loss Account

Form of balancesheet specified under Part II

2. Title SOURCE OF FUNDS & APPLICATION OF FUNDS

EQUITY AND LIBILITIES & ASSETS

3. Disclosures in Share Capital

Authorised Capital: 1,00,000Issued & subscribed Capital: 1,00,000Share Application: 10,00,000Pending for AllotmentNo Restriction

Authorised Capital: 1,00,000Issued & subscribed Capital: 1,00,000Share Application: 10,00,000Pending for AllotmentNow terms & conditions of share application money needs to be disclosed as if sufficient balance of Authorised capital is not available.

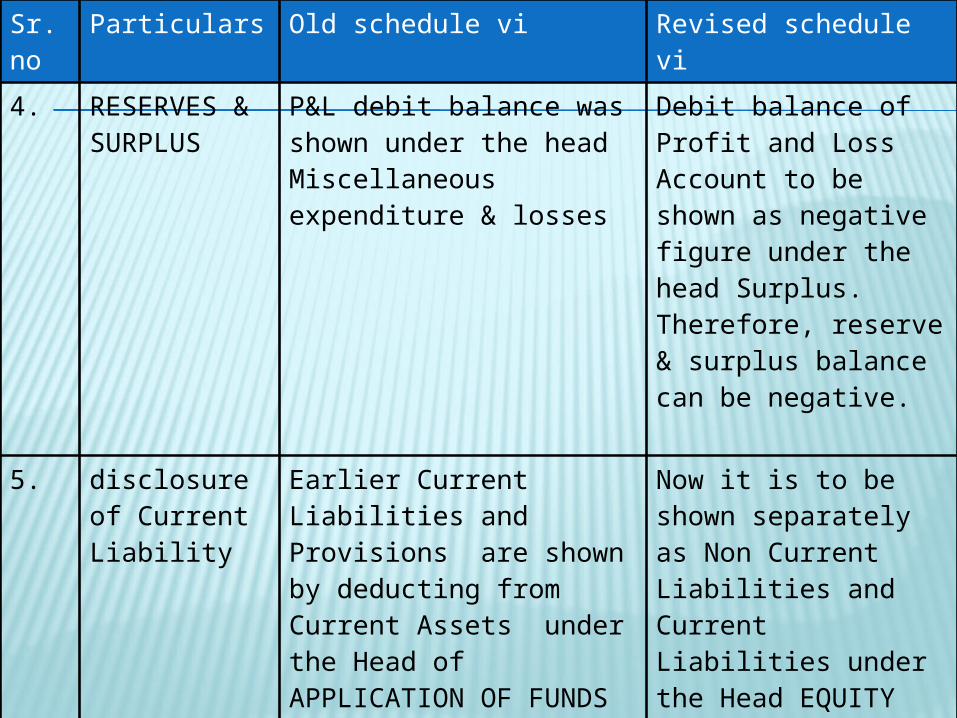

Sr.no Particulars Old schedule vi Revised schedule vi

4. RESERVES & SURPLUS

P&L debit balance was shown under the head Miscellaneous expenditure & losses

Debit balance of Profit and Loss Account to be shown as negative figure under the head Surplus. Therefore, reserve & surplus balance can be negative.

5. disclosure of Current Liability

Earlier Current Liabilities and Provisions are shown by deducting from Current Assets under the Head of APPLICATION OF FUNDS

Now it is to be shown separately as Non Current Liabilities and Current Liabilities under the Head EQUITY AND LIBILITIES

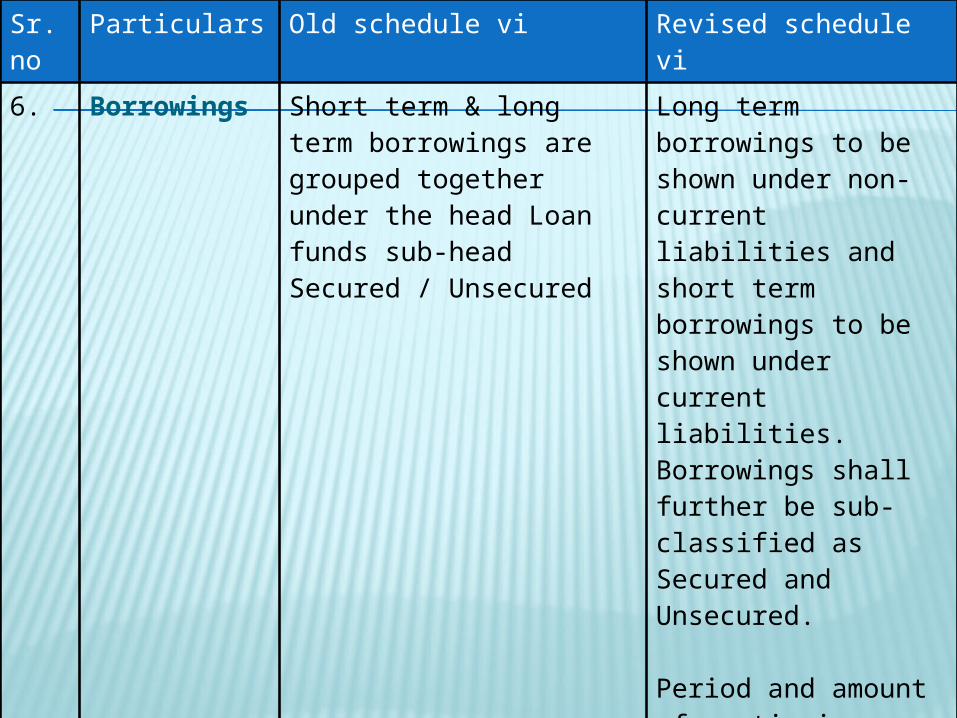

Sr.no Particulars Old schedule vi Revised schedule vi

6. Borrowings Short term & long term borrowings are grouped together under the head Loan funds sub-head Secured / Unsecured

Long term borrowings to be shown under non-current liabilities and short term borrowings to be shown under current liabilities. Borrowings shall further be sub- classified as Secured and Unsecured.

Period and amount of continuing default as on the balance sheet date in repayment of loans and interest to be separately specified

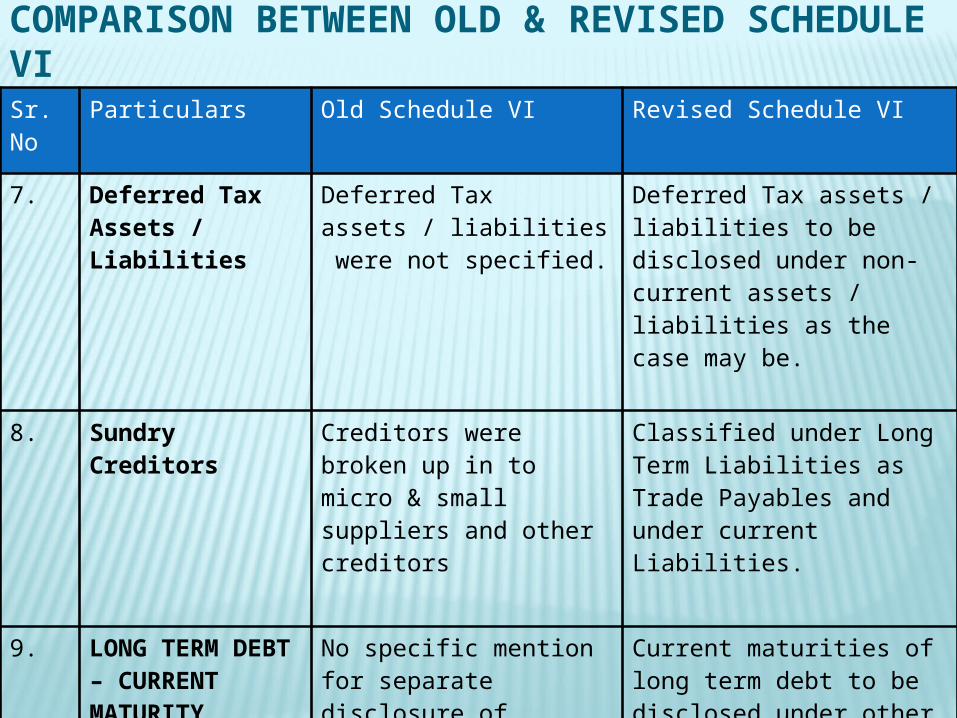

COMPARISON BETWEEN OLD & REVISED SCHEDULE VISr. No

Particulars Old Schedule VI Revised Schedule VI

7. Deferred Tax Assets / Liabilities

Deferred Tax assets / liabilities were not specified.

Deferred Tax assets / liabilities to be disclosed under non-current assets / liabilities as the case may be.

8. Sundry Creditors Creditors were broken up in to micro & small suppliers and other creditors

Classified under Long Term Liabilities as Trade Payables and under current Liabilities.

9. LONG TERM DEBT – CURRENT MATURITY

No specific mention for separate disclosure of Current maturities of long term debt

Current maturities of long term debt to be disclosed under other current liabilities

COMPARISON BETWEEN OLD & REVISED SCHEDULE VISr. No

Particulars Old Schedule VI Revised Schedule VI

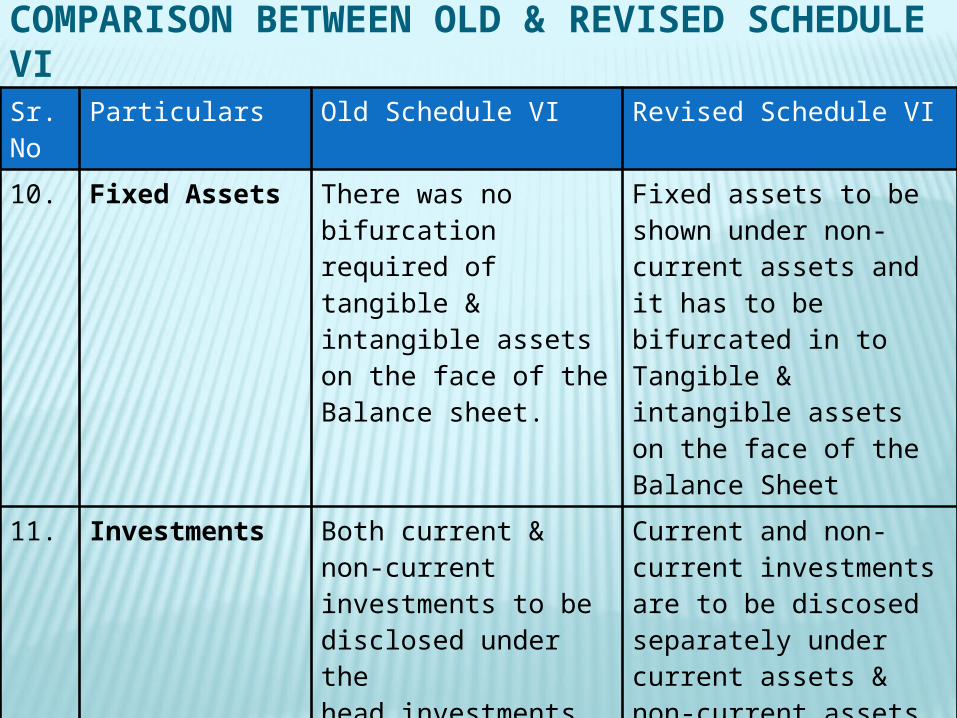

10. Fixed Assets There was no bifurcation required of tangible & intangible assets on the face of the Balance sheet.

Fixed assets to be shown under non-current assets and it has to be bifurcated in to Tangible & intangible assets on the face of the Balance Sheet

11. Investments Both current & non-current investments to be disclosed under the head investments

Current and non-current investments are to be discosed separately under current assets & non-current assets respectively

12 Deposits Lease deposits are part of loans & advances

Lease deposits to be disclosed as long term loans & advances under the head non-current assets

COMPARISON BETWEEN OLD & REVISED SCHEDULE VISr. No

Particulars Old Schedule VI Revised Schedule VI

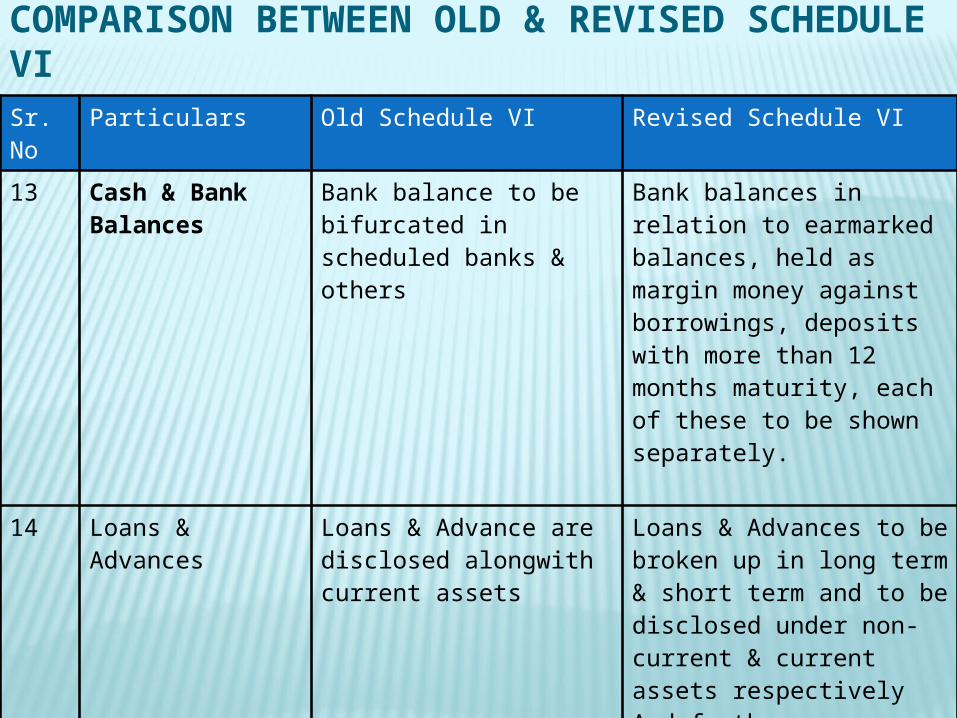

13 Cash & Bank Balances

Bank balance to be bifurcated in scheduled banks & others

Bank balances in relation to earmarked balances, held as margin money against borrowings, deposits with more than 12 months maturity, each of these to be shown separately.

14 Loans & Advances Loans & Advance are disclosed alongwith current assets

Loans & Advances to be broken up in long term & short term and to be disclosed under non-current & current assets respectivelyAnd further bifurcation with capital advances security deposits etc.

COMPARISON BETWEEN OLD & REVISED SCHEDULE VISr. No

Particulars Old Schedule VI Revised Schedule VI

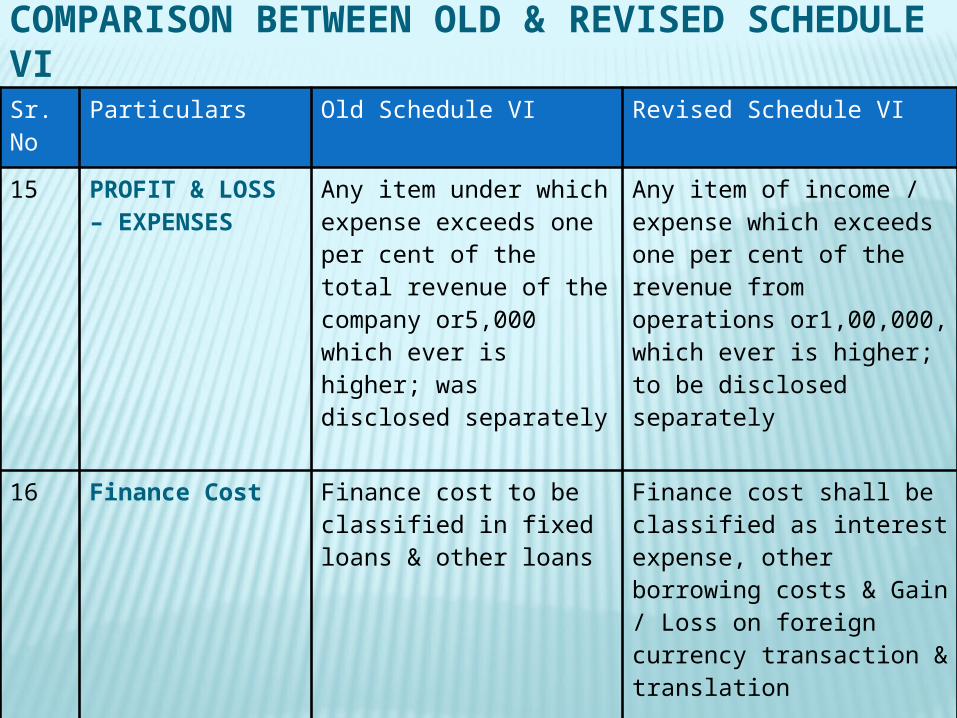

15 PROFIT & LOSS – EXPENSES

Any item under which expense exceeds one per cent of the total revenue of the company or5,000 which ever is higher; was disclosed separately

Any item of income / expense which exceeds one per cent of the revenue from operations or1,00,000, which ever is higher; to be disclosed separately

16 Finance Cost Finance cost to be classified in fixed loans & other loans

Finance cost shall be classified as interest expense, other borrowing costs & Gain / Loss on foreign currency transaction & translation

COMPARISON BETWEEN OLD & REVISED SCHEDULE VISr. No

Particulars Old Schedule VI Revised Schedule VI

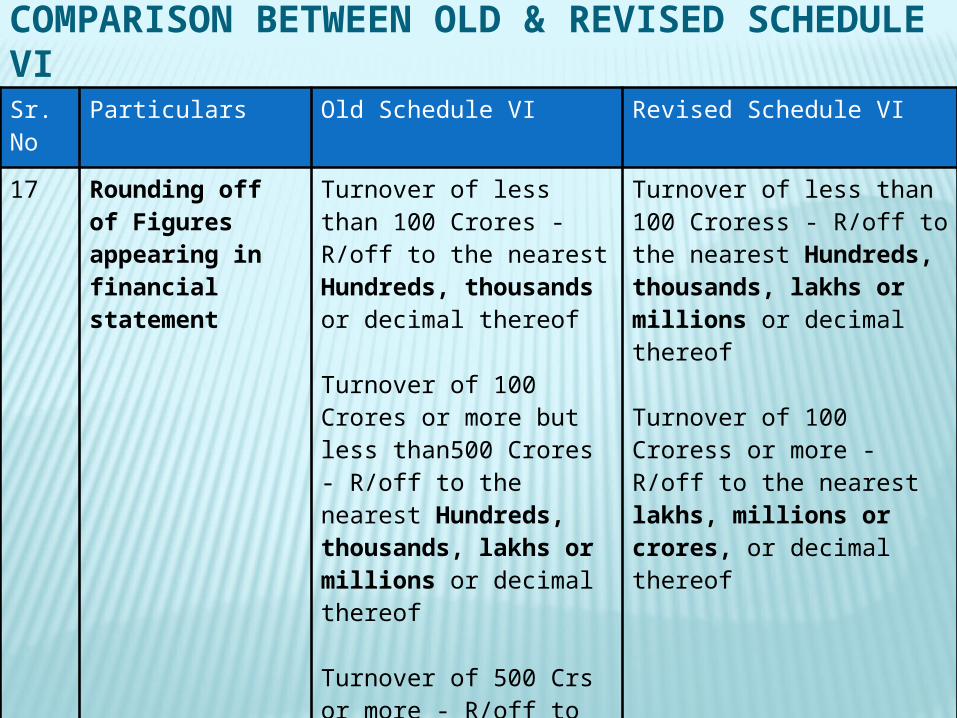

17 Rounding off of Figures appearing in financial statement

Turnover of less than 100 Crores - R/off to the nearest Hundreds, thousands or decimal thereof

Turnover of 100 Crores or more but less than500 Crores - R/off to the nearest Hundreds, thousands, lakhs or millions or decimal thereof

Turnover of 500 Crs or more - R/off to the nearest Hundreds, thousands, lakhs, millions or crores, or decimal thereof

Turnover of less than 100 Croress - R/off to the nearest Hundreds, thousands, lakhs or millions or decimal thereof

Turnover of 100 Croress or more - R/off to the nearest lakhs, millions or crores, or decimal thereof

COMPARISON BETWEEN OLD & REVISED SCHEDULE VI

Sr. No

Particulars Old Schedule VI Revised Schedule VI

18 Purchases The purchase made and the opening & closing stock, giving break up in respect of each class of goods traded in by the company and indicating the quantities thereof.

Goods traded in by the company to be disclosed in broad heads in notes. Disclosure of quantitative details of goods is diluted

![ppt [final]](https://static.cupdf.com/doc/110x72/557211a2497959fc0b8f45c0/ppt-final-55c1eb754e129.jpg)