Chapter 9

2

Plant Plant AssetsAssets

Natural Resources

Natural Natural ResourcesResources

Intangible Intangible AssetsAssets

DepreciationDepreciation DepletionDepletionDepletion AmortizationAmortization

Copyright (c) 2009 Prentice Hall. All rights reserved.

� Held for use in business� Full cost includes several expenditures� Last several years� Can be sold or traded in

Copyright (c) 2009 Prentice Hall. All rights reserved. 3

Measure the cost of a plant asset

Copyright (c) 2009 Prentice Hall. All rights reserved. 5

The Cost PrincipleThe Cost Principle

Copyright (c) 2009 Prentice Hall. All rights reserved. 6

� NOT depreciated� What costs would be included in Land?

Copyright (c) 2009 Prentice Hall. All rights reserved. 7

� Subject to depreciation

Copyright (c) 2009 Prentice Hall. All rights reserved. 8

� What does the cost include?

9Copyright (c) 2009 Prentice Hall. All rights reserved.

� What does cost include?

10Copyright (c) 2009 Prentice Hall. All rights reserved.

� Purchase price (less any discounts)� Shipping charges� Costs to assemble

11Copyright (c) 2009 Prentice Hall. All rights reserved.

� Company purchases a group of plant assets for a single price

� Assign cost to individual assets based on relative sales values

12Copyright (c) 2009 Prentice Hall. All rights reserved.

Copyright (c) 2009 Prentice Hall. All rights reserved. 13

Fair value Percent Allocated cost

Land $75,000 50% $70,000

Building $60,000 40% $56,000

Equipment $15,000 10% $14,000

Total $150,000 100% $140,000

Capital expenditures Expenses

� Debited to an asset account

� Debited to an expense account

Copyright (c) 2009 Prentice Hall. All rights reserved. 14

� If a capital expenditure is incorrectly recorded as an expense:

Copyright (c) 2009 Prentice Hall. All rights reserved. 15

Account for depreciation

� Allocation of a plant asset’s cost to expense over its useful life

� Matches expense against revenue generated using the asset

17Copyright (c) 2009 Prentice Hall. All rights reserved.

� Wear and tear from us� Physical factors� Obsolescence

Copyright (c) 2009 Prentice Hall. All rights reserved. 18

Copyright (c) 2009 Prentice Hall. All rights reserved. 19

� Cost� Estimated useful life� Estimated residual value

Copyright (c) 2009 Prentice Hall. All rights reserved. 20

21Copyright (c) 2009 Prentice Hall. All rights reserved. 22Copyright (c) 2009 Prentice Hall. All rights reserved.

(Cost – residual value)1

Life

Depreciation expense

#12

23Copyright (c) 2009 Prentice Hall. All rights reserved.

CostAccumulated depreciation

Book value

Copyright (c) 2009 Prentice Hall. All rights reserved. 24

Depreciation expense =Depreciation per unit x activity during the period

Depreciation expense =Depreciation per unit x activity during the period

Depreciation per unit =

(Cost – Residual value) x

Depreciation per unit =

(Cost – Residual value) x1

Life in units

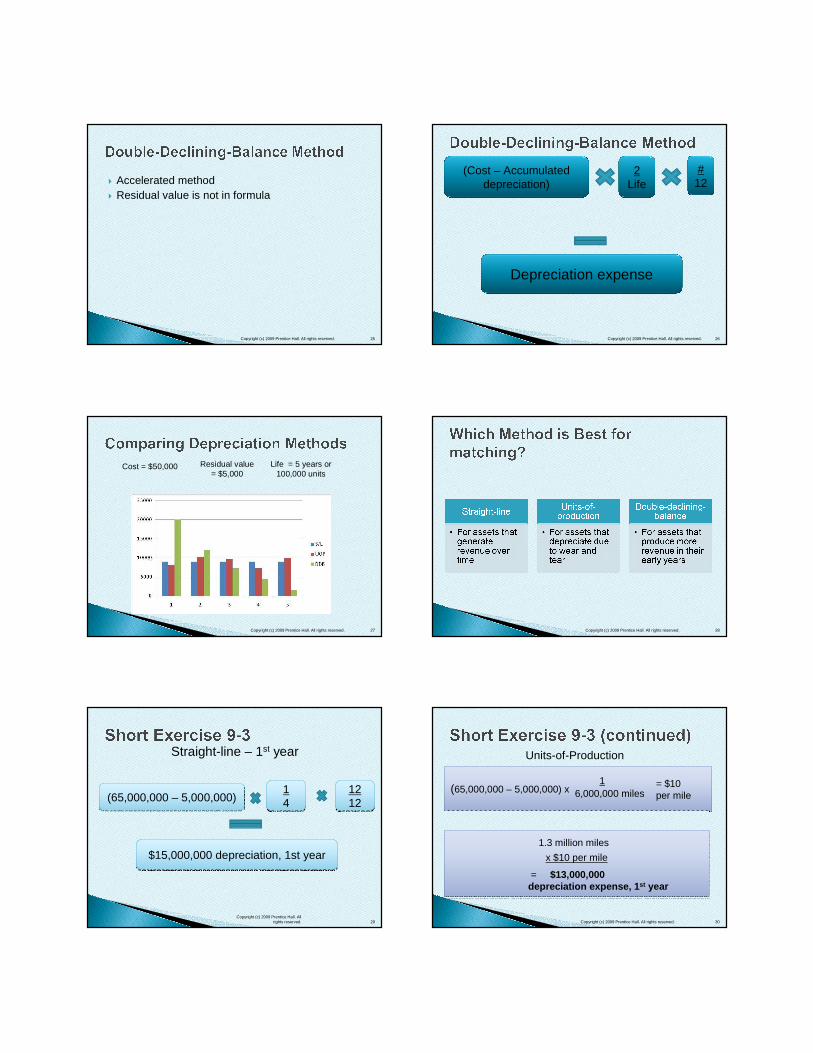

� Accelerated method� Residual value is not in formula

25Copyright (c) 2009 Prentice Hall. All rights reserved. 26Copyright (c) 2009 Prentice Hall. All rights reserved.

(Cost – Accumulated depreciation)

#12

Depreciation expense

2Life

Copyright (c) 2009 Prentice Hall. All rights reserved. 27

Cost = $50,000 Life = 5 years or 100,000 units

Residual value = $5,000

Copyright (c) 2009 Prentice Hall. All rights reserved. 28

Copyright (c) 2009 Prentice Hall. All rights reserved. 29

(65,000,000 – 5,000,000)(65,000,000 – 5,000,000)

Straight-line – 1st year

1414

$15,000,000 depreciation, 1st year$15,000,000 depreciation, 1st year

12121212

30

(65,000,000 – 5,000,000) x(65,000,000 – 5,000,000) x

Copyright (c) 2009 Prentice Hall. All rights reserved.

1

Units-of-Production

6,000,000 miles= $10 per mile

x $10 per mile

1.3 million miles

= $13,000,000 depreciation expense, 1st year

31Copyright (c) 2009 Prentice Hall. All rights reserved.

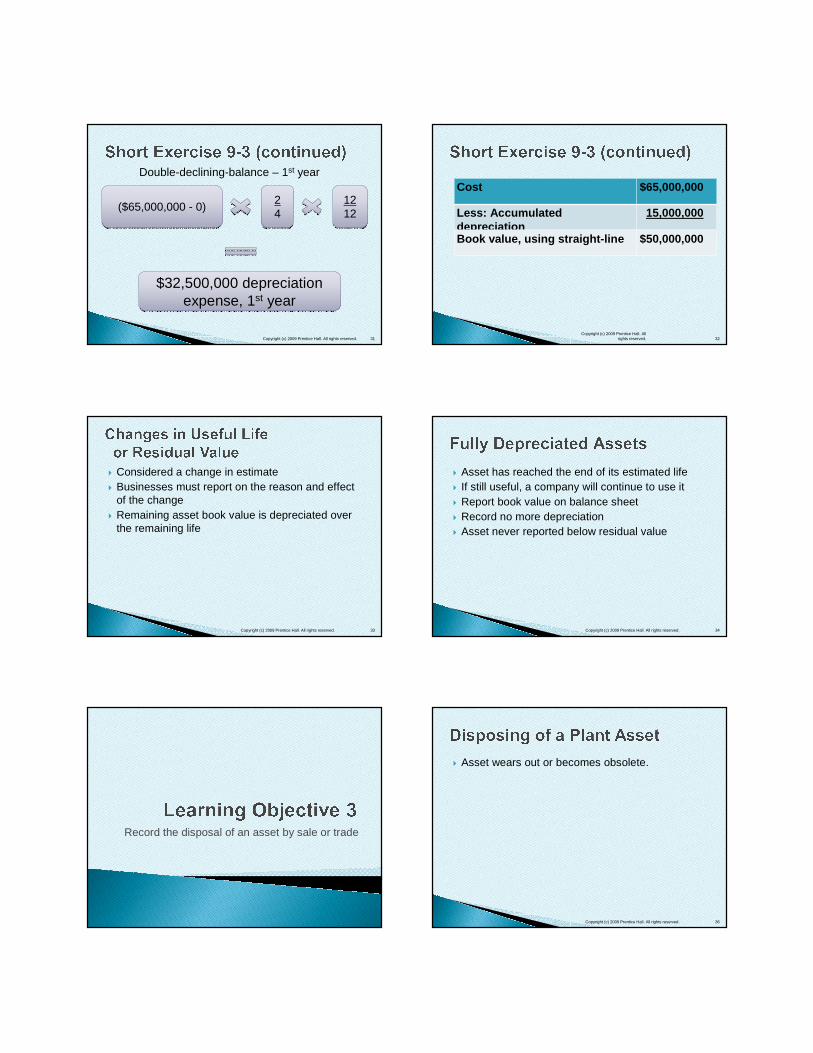

($65,000,000 - 0)($65,000,000 - 0) 12121212

$32,500,000 depreciation expense, 1st year

$32,500,000 depreciation expense, 1st year

Double-declining-balance – 1st year

2424

Copyright (c) 2009 Prentice Hall. All rights reserved. 32

Cost $65,000,000

Less: Accumulated depreciation

15,000,000

Book value, using straight-line $50,000,000

� Considered a change in estimate� Businesses must report on the reason and effect

of the change� Remaining asset book value is depreciated over

the remaining life

Copyright (c) 2009 Prentice Hall. All rights reserved. 33

� Asset has reached the end of its estimated life� If still useful, a company will continue to use it� Report book value on balance sheet� Record no more depreciation� Asset never reported below residual value

34Copyright (c) 2009 Prentice Hall. All rights reserved.

Record the disposal of an asset by sale or trade

� Asset wears out or becomes obsolete.

Copyright (c) 2009 Prentice Hall. All rights reserved. 36

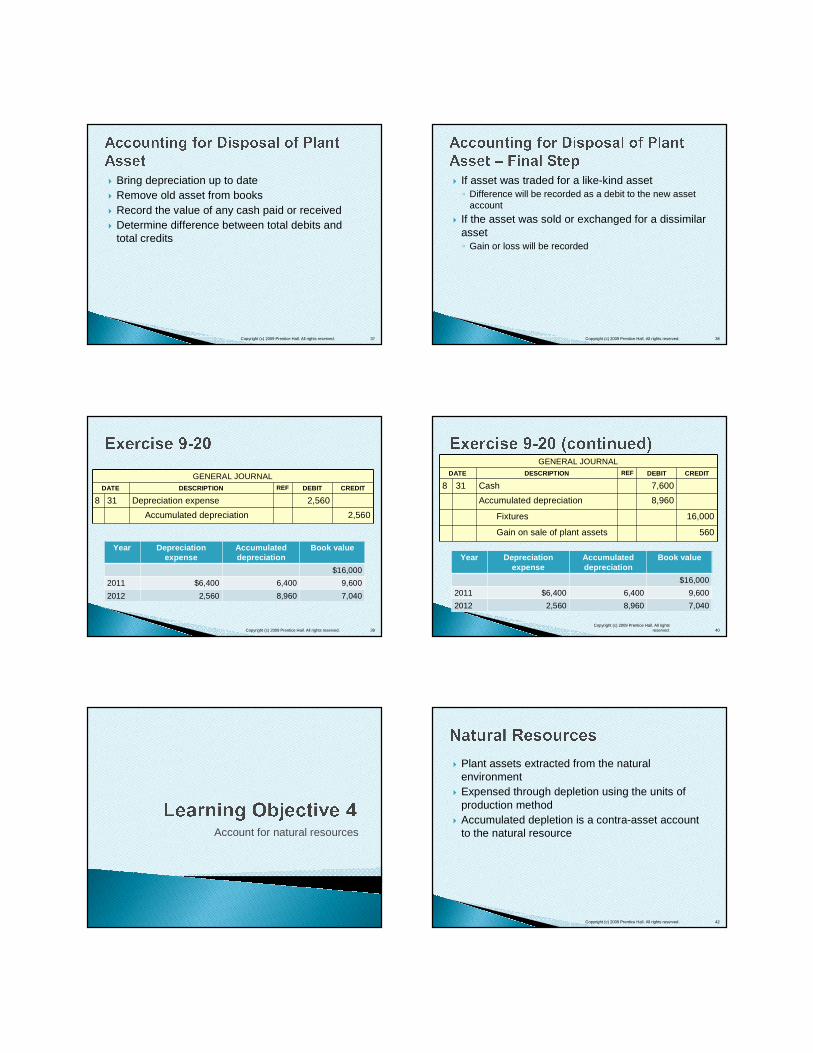

� Bring depreciation up to date� Remove old asset from books� Record the value of any cash paid or received� Determine difference between total debits and

total credits

37Copyright (c) 2009 Prentice Hall. All rights reserved.

� If asset was traded for a like-kind asset◦ Difference will be recorded as a debit to the new asset

account

� If the asset was sold or exchanged for a dissimilar asset◦ Gain or loss will be recorded

Copyright (c) 2009 Prentice Hall. All rights reserved. 38

Copyright (c) 2009 Prentice Hall. All rights reserved. 39

GENERAL JOURNALDATE DESCRIPTION REF DEBIT CREDIT

8 31 Depreciation expense 2,560

Accumulated depreciation 2,560

Year Depreciation expense

Accumulated depreciation

Book value

$16,000

2011 $6,400 6,400 9,600

2012 2,560 8,960 7,040

Copyright (c) 2009 Prentice Hall. All rights reserved. 40

GENERAL JOURNALDATE DESCRIPTION REF DEBIT CREDIT

8 31 Cash 7,600

Accumulated depreciation 8,960

Fixtures 16,000

Gain on sale of plant assets 560

Year Depreciation expense

Accumulated depreciation

Book value

$16,000

2011 $6,400 6,400 9,600

2012 2,560 8,960 7,040

Account for natural resources

� Plant assets extracted from the natural environment

� Expensed through depletion using the units of production method

� Accumulated depletion is a contra-asset account to the natural resource

42Copyright (c) 2009 Prentice Hall. All rights reserved.

Copyright (c) 2009 Prentice Hall. All rights reserved. 43

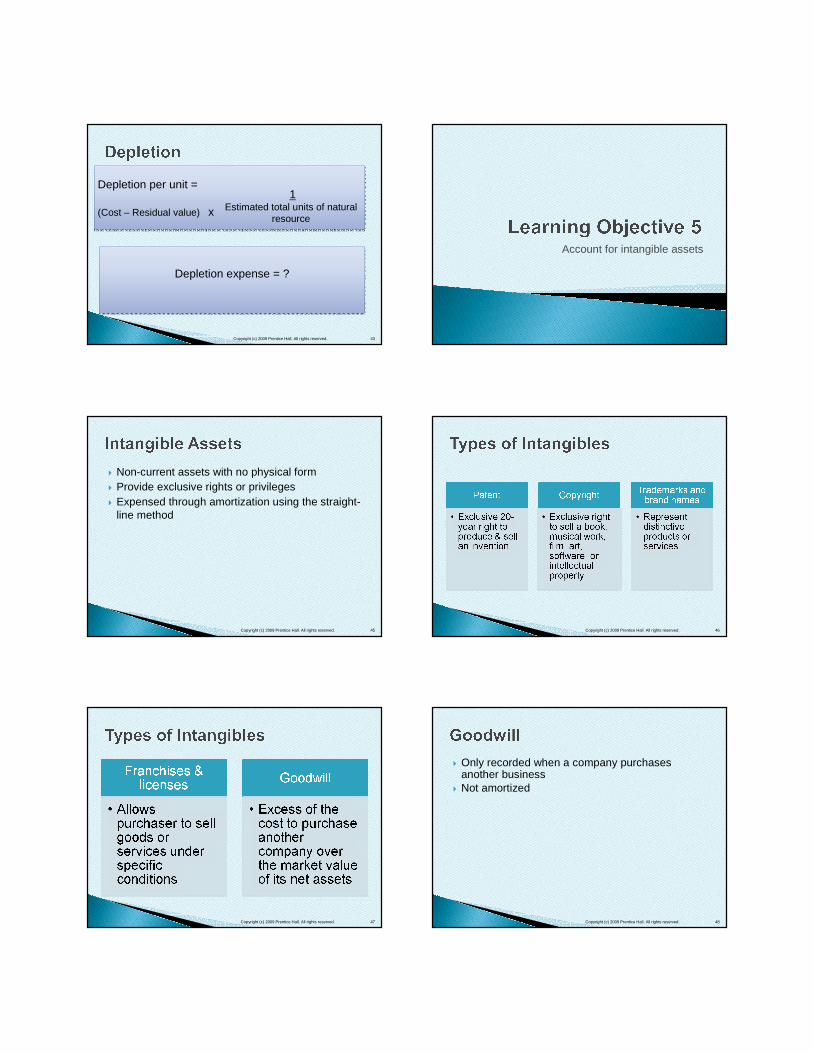

Depletion expense = ?Depletion expense = ?

Depletion per unit =

(Cost – Residual value) x

Depletion per unit =

(Cost – Residual value) x

1Estimated total units of natural

resource

Account for intangible assets

� Non-current assets with no physical form� Provide exclusive rights or privileges� Expensed through amortization using the straight-

line method

45Copyright (c) 2009 Prentice Hall. All rights reserved. Copyright (c) 2009 Prentice Hall. All rights reserved. 46

Copyright (c) 2009 Prentice Hall. All rights reserved. 47

� Only recorded when a company purchases another business

� Not amortized

48Copyright (c) 2009 Prentice Hall. All rights reserved.

� Important to several industries, such as pharmaceutical companies

� Not an intangible

49Copyright (c) 2009 Prentice Hall. All rights reserved.

Describe ethical issues related to plant assets

Capitalize� Results in higher

asset value and larger net income

� If cost provides a future benefit, then capitalize

Expense� Results in lower net

income◦ Less taxes

� If cost does not provide a future benefit, then expense

Copyright (c) 2009 Prentice Hall. All rights reserved. 51

![INTANGIBLE VALUE –FACT OR FICTION - AI Home | … · [IAS 38.8] 3. INTANGIBLE VALUE –FACT OR FICTION ... 2.36 INTANGIBLE PROPERTY (INTANGIBLE ASSETS): Non-physical assets, …](https://static.cupdf.com/doc/110x72/5af0812f7f8b9ac2468e1bc2/intangible-value-fact-or-fiction-ai-home-ias-388-3-intangible-value.jpg)