(1)

Industry & Competitive AnalysisIndustry & Competitive Analysis - Automotive Industry - - Automotive Industry -

Group 4Danny Dharmawan Kosasih

Ratih DamayantiWidyarini Utami

(2)

Presentation Flow

Introduction

Structure – Market structure.– Car Categories– Herfindahl-Hirschman index (HII)– Government Policies & Environment Issues

Conduct– Porter’s Five Forces

Performance– Sales– Profitability

Competitive Strategy– Business Strategy Recommendation

(3)

IntroductionIntroduction

(4)

ASEAN Car Market

• Biggest World Car Makers: Toyota, Mitsubishi, Suzuki, General Motor and Ford have been expanding to Asia region

• They place production bases in ASEAN countries – for efficiency and marketing deeds

• Japanese Car dominates ASEAN market

• New contenders: China and Malaysia

• AFTA sharpened automotive competition in ASEAN – in 2003

(5)

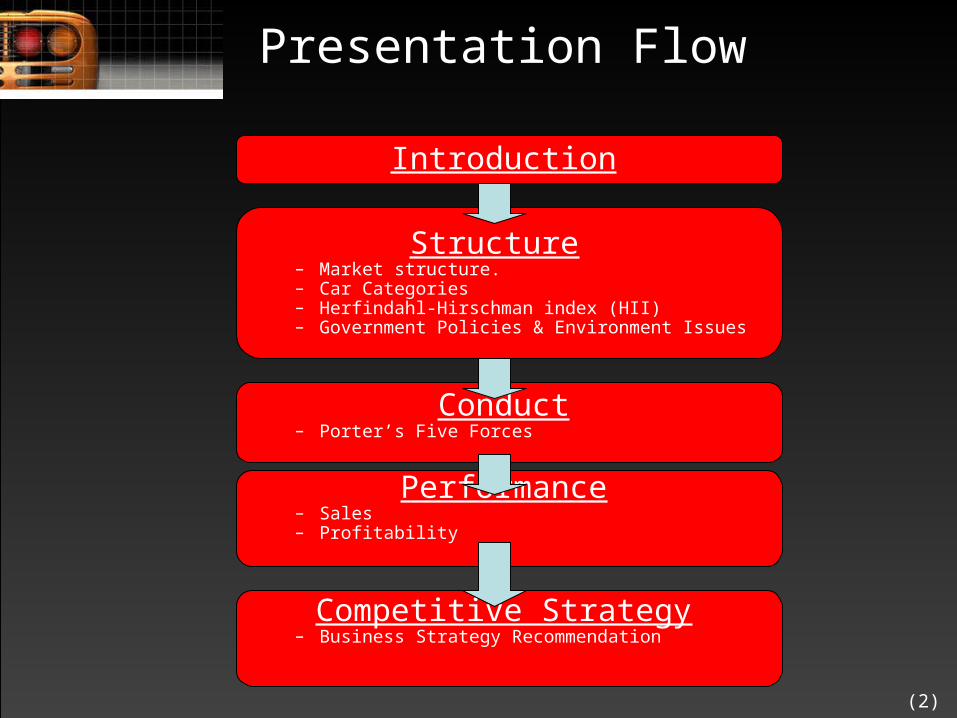

Indonesia: Where are we standing?

• 4 wheelers population in Indonesia per 2005 = 14.471.750* or increased by 325% in the past 10 years

• Indonesia is becoming production centre

• ATPMs in Indonesia now only hold distribution

• While manufacturing trend are operated by foreign car makers: i.e. Toyota and Suzuki

• No clear policy to protect domestic competition

• Next question, where are we heading to?

* Source: Direktorat Samapta Polri/ GIAMM – notes: not included Ranmor ABRI and diplomatic corps - 2005

(6)

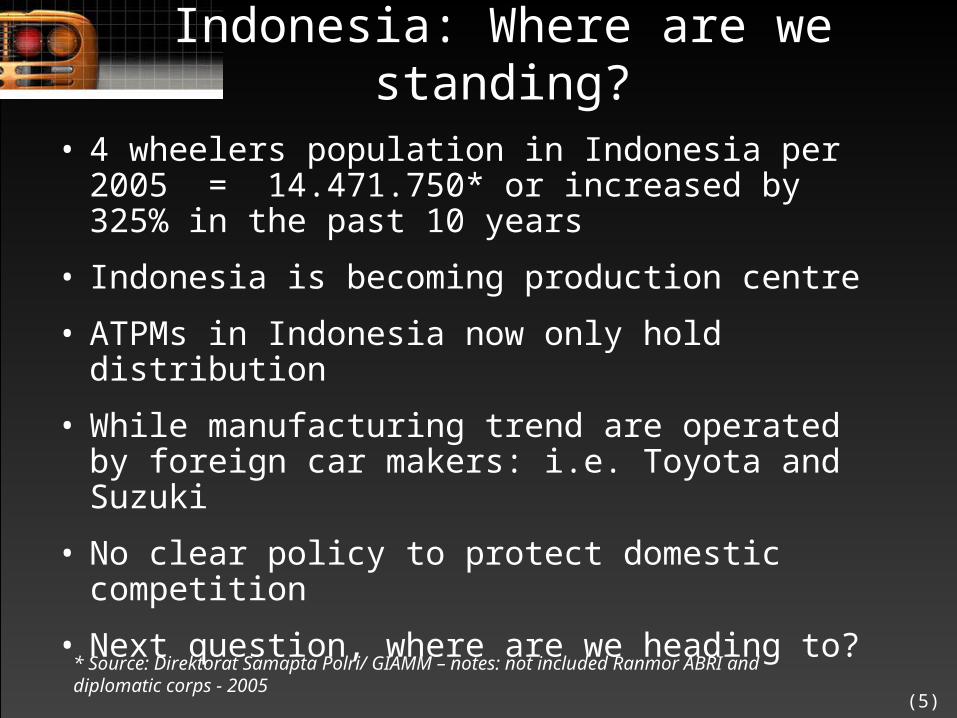

Indonesia: 2010 Vision

• Automotive industry is one of accelerator industries to achieve 7% economic growth

– Textile, Shoes & apparels

– Electronics and its components

– Automotive and its components

– Shipping & docks

Source: Visi 2030 & Roadmap 2010 Industri Nasional – KADIN 2007

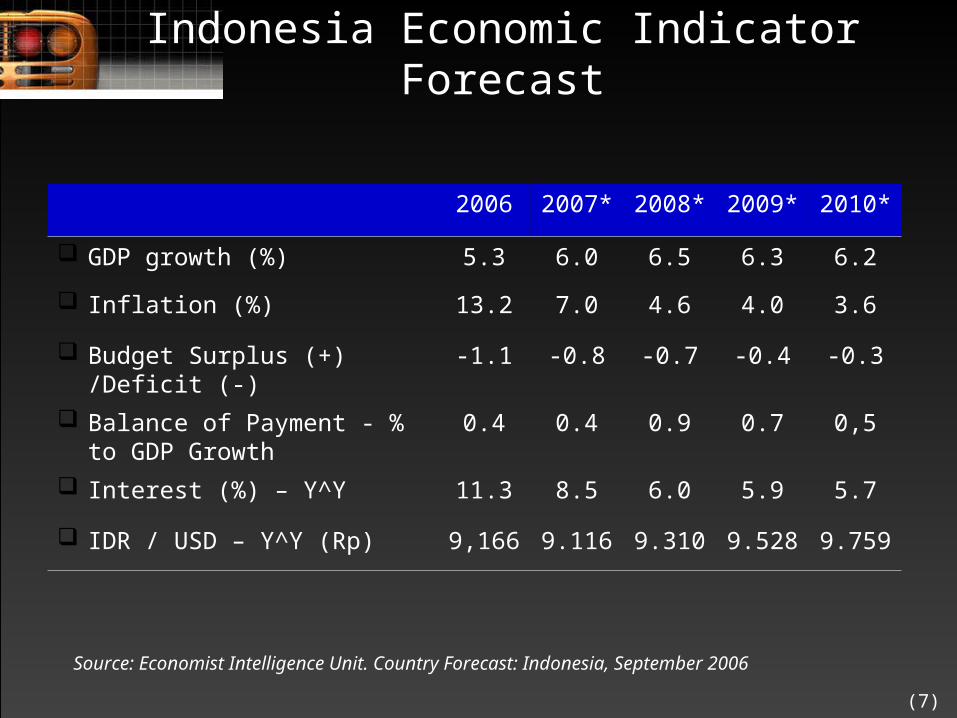

(7)

Indonesia Economic Indicator Forecast

2006 2007* 2008* 2009* 2010*

GDP growth (%) 5.3 6.0 6.5 6.3 6.2

Inflation (%) 13.2 7.0 4.6 4.0 3.6

Budget Surplus (+) /Deficit (-) -1.1 -0.8 -0.7 -0.4 -0.3

Balance of Payment - % to GDP Growth

0.4 0.4 0.9 0.7 0,5

Interest (%) – Y^Y 11.3 8.5 6.0 5.9 5.7

IDR / USD – Y^Y (Rp) 9,166 9.116 9.310 9.528 9.759

Source: Economist Intelligence Unit. Country Forecast: Indonesia, September 2006

(8)

IIMS 15th

19 - 28 July ‘07

(9)

StructureStructure

(10)

Market Structure: Monopolistic Competition

• Astra International (AI) & Indomobil Niaga International are two largest automotive companies in the country having affiliation with a number of foreign principals.

• They become agents for the Indonesian market.

Vs

(11)

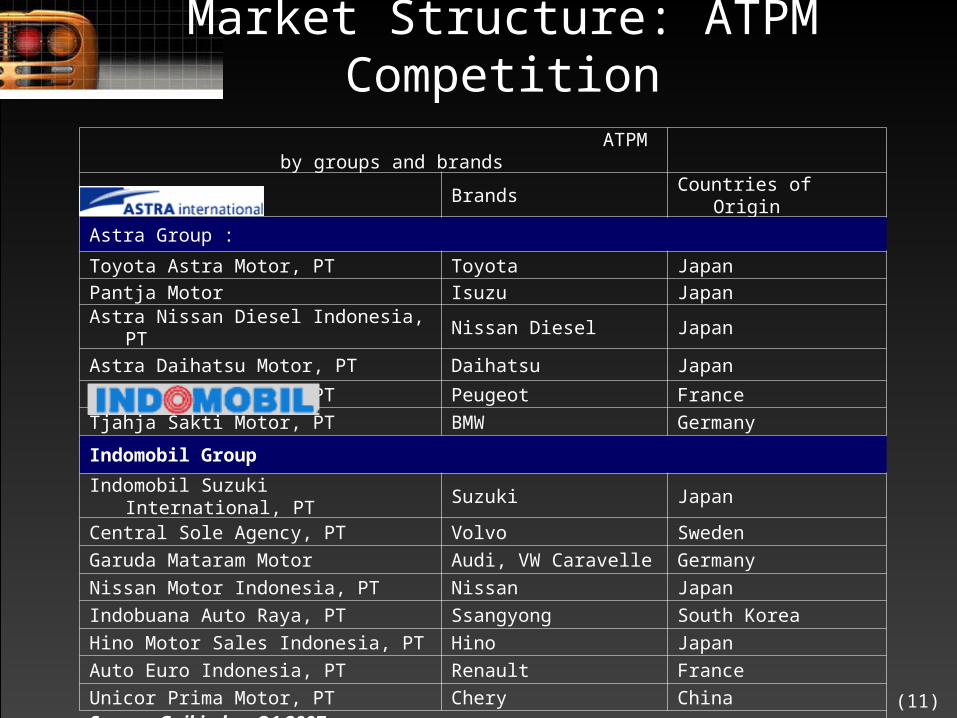

Market Structure: ATPM Competition

ATPM by groups and brands

Name of company Brands Countries of Origin

Astra Group :

Toyota Astra Motor, PT Toyota Japan

Pantja Motor Isuzu Japan

Astra Nissan Diesel Indonesia, PT Nissan Diesel Japan

Astra Daihatsu Motor, PT Daihatsu Japan

Astra France Motor, PT Peugeot France

Tjahja Sakti Motor, PT BMW Germany

Indomobil Group

Indomobil Suzuki International, PT Suzuki Japan

Central Sole Agency, PT Volvo Sweden

Garuda Mataram Motor Audi, VW Caravelle Germany

Nissan Motor Indonesia, PT Nissan Japan

Indobuana Auto Raya, PT Ssangyong South Korea

Hino Motor Sales Indonesia, PT Hino Japan

Auto Euro Indonesia, PT Renault France

Unicor Prima Motor, PT Chery ChinaSource: Gaikindo – Q1 2007

(12)

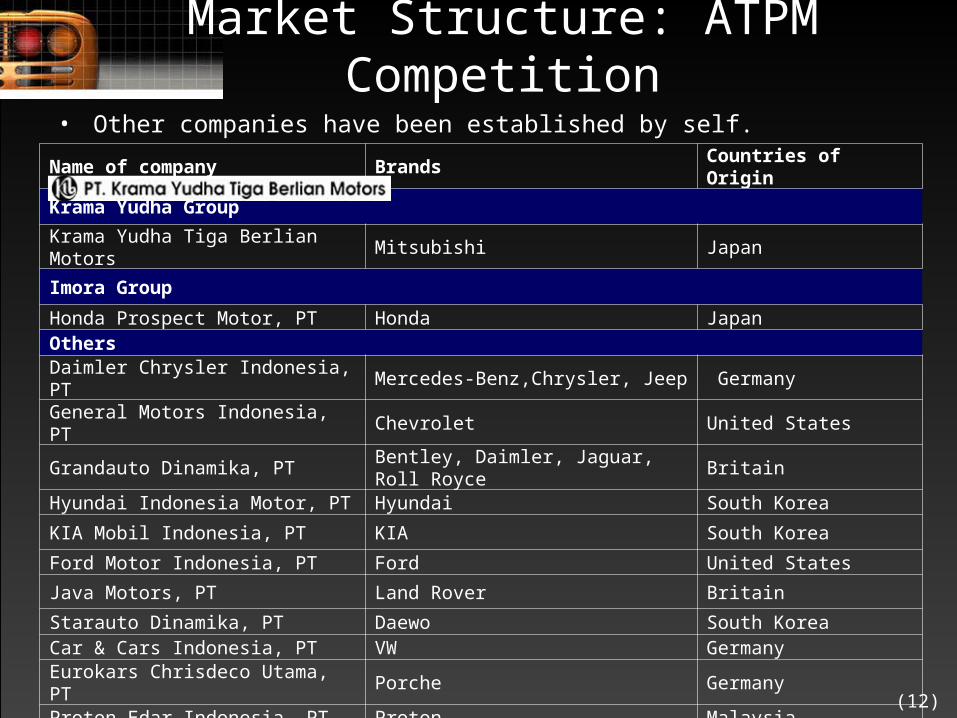

• Other companies have been established by self.

Market Structure: ATPM Competition

Name of company Brands Countries of Origin

Krama Yudha Group

Krama Yudha Tiga Berlian Motors Mitsubishi Japan

Imora Group

Honda Prospect Motor, PT Honda JapanOthers

Daimler Chrysler Indonesia, PT Mercedes-Benz,Chrysler, Jeep Germany

General Motors Indonesia, PT Chevrolet United States

Grandauto Dinamika, PT Bentley, Daimler, Jaguar, Roll Royce Britain

Hyundai Indonesia Motor, PT Hyundai South Korea

KIA Mobil Indonesia, PT KIA South Korea

Ford Motor Indonesia, PT Ford United States

Java Motors, PT Land Rover Britain

Starauto Dinamika, PT Daewo South KoreaCar & Cars Indonesia, PT VW GermanyEurokars Chrisdeco Utama, PT Porche GermanyProton Edar Indonesia, PT Proton MalaysiaTC Subaru, PT Subaru JapanMazda Motor Indonesia, PT Mazda JapanSource : Gaikindo – Q1 2007

(13)

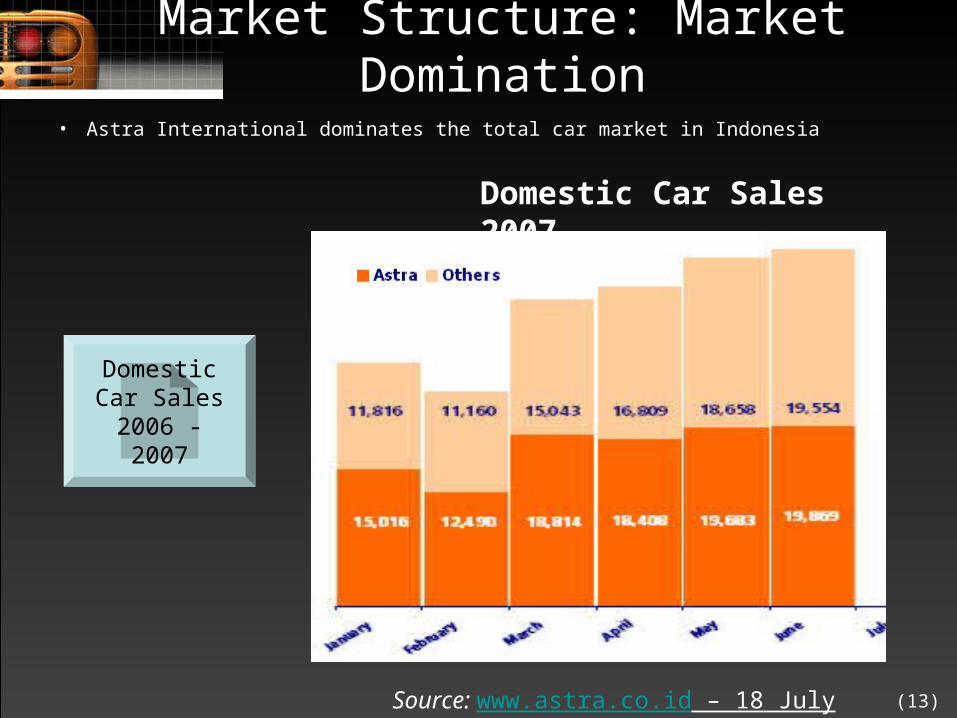

Market Structure: Market Domination

• Astra International dominates the total car market in Indonesia

Domestic Car Sales 2007

Domestic Car Sales 2006 -

2007

Source: www.astra.co.id – 18 July 2007

(14)

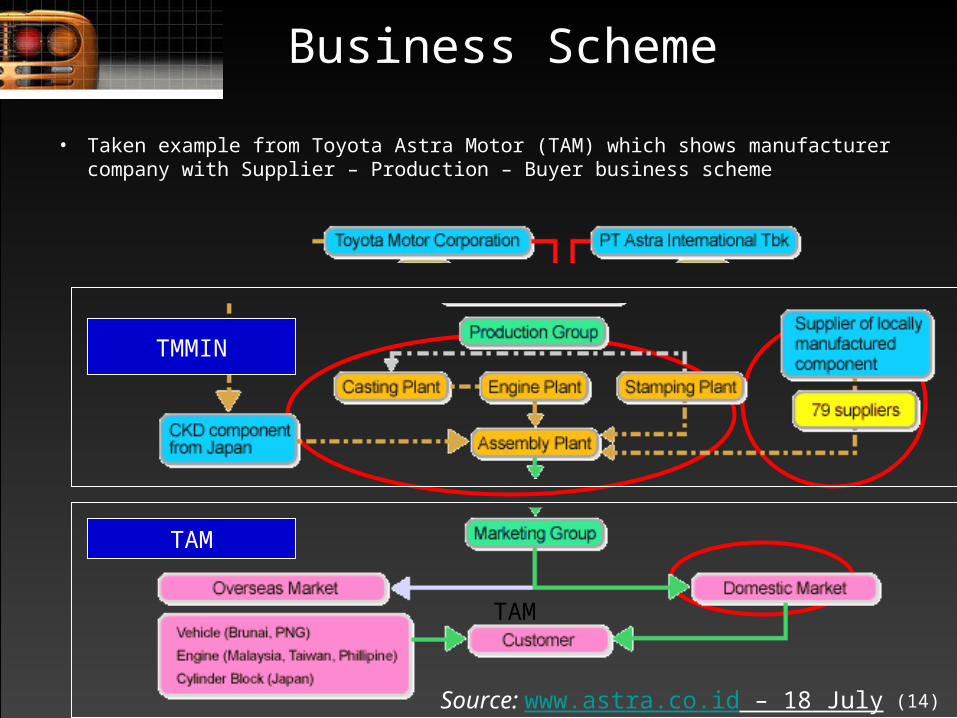

Business Scheme

• Taken example from Toyota Astra Motor (TAM) which shows manufacturer company with Supplier – Production – Buyer business scheme

TMMIN

TAM

TMMIN

Source: www.astra.co.id – 18 July 2007

TAM

(15)

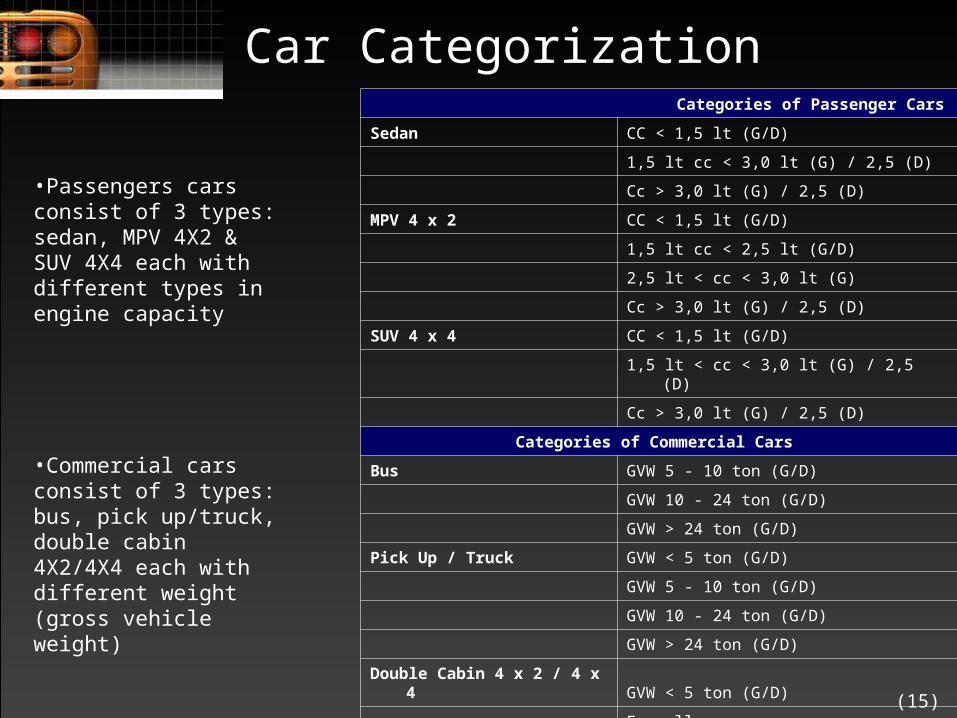

Categories of Passenger Cars

Sedan CC < 1,5 lt (G/D)

1,5 lt cc < 3,0 lt (G) / 2,5 (D)

Cc > 3,0 lt (G) / 2,5 (D)

MPV 4 x 2 CC < 1,5 lt (G/D)

1,5 lt cc < 2,5 lt (G/D)

2,5 lt < cc < 3,0 lt (G)

Cc > 3,0 lt (G) / 2,5 (D)

SUV 4 x 4 CC < 1,5 lt (G/D)

1,5 lt < cc < 3,0 lt (G) / 2,5 (D)

Cc > 3,0 lt (G) / 2,5 (D)

Categories of Commercial Cars

Bus GVW 5 - 10 ton (G/D)

GVW 10 - 24 ton (G/D)

GVW > 24 ton (G/D)

Pick Up / Truck GVW < 5 ton (G/D)

GVW 5 - 10 ton (G/D)

GVW 10 - 24 ton (G/D)

GVW > 24 ton (G/D)

Double Cabin 4 x 2 / 4 x 4 GVW < 5 ton (G/D)

For all cc

Source: Gaikindo – Q1 2007

•Passengers cars consist of 3 types: sedan, MPV 4X2 & SUV 4X4 each with different types in engine capacity

•Commercial cars consist of 3 types: bus, pick up/truck, double cabin 4X2/4X4 each with different weight (gross vehicle weight)

Car Categorization

(16)

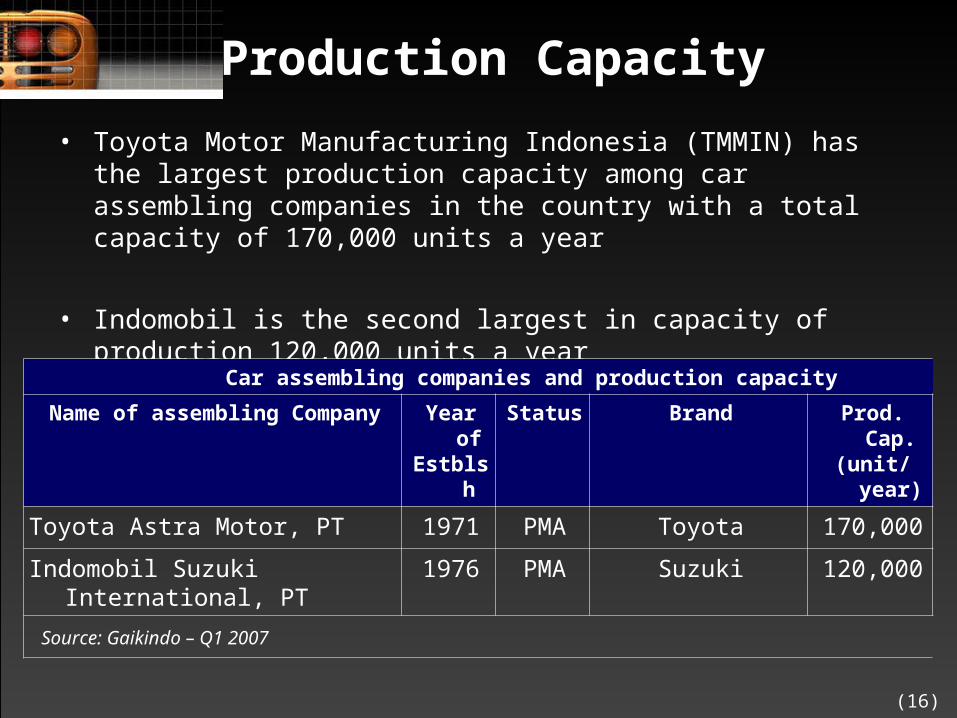

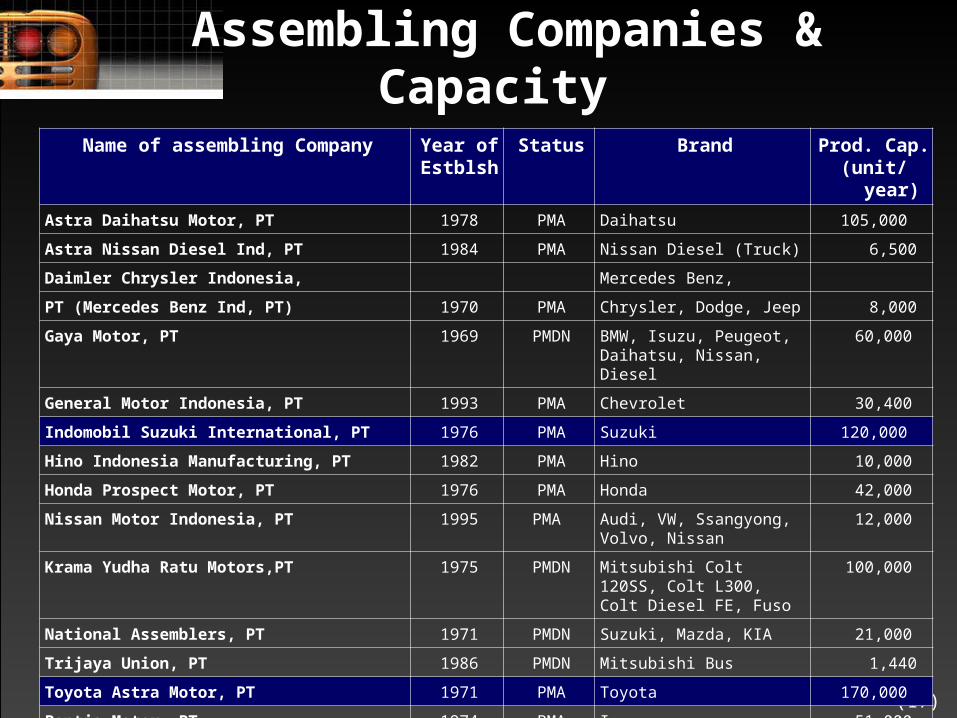

Production Capacity

• Toyota Motor Manufacturing Indonesia (TMMIN) has the largest production capacity among car assembling companies in the country with a total capacity of 170,000 units a year

• Indomobil is the second largest in capacity of production 120,000 units a year

Car assembling companies and production capacity

Name of assembling Company Year ofEstblsh

Status Brand Prod. Cap.(unit/year)

Toyota Astra Motor, PT 1971 PMA Toyota 170,000

Indomobil Suzuki International, PT 1976 PMA Suzuki 120,000

Source: Gaikindo – Q1 2007

(17)

Name of assembling Company Year ofEstblsh

Status Brand Prod. Cap.(unit/year)

Astra Daihatsu Motor, PT 1978 PMA Daihatsu 105,000

Astra Nissan Diesel Ind, PT 1984 PMA Nissan Diesel (Truck) 6,500

Daimler Chrysler Indonesia, Mercedes Benz,

PT (Mercedes Benz Ind, PT) 1970 PMA Chrysler, Dodge, Jeep 8,000

Gaya Motor, PT 1969 PMDN BMW, Isuzu, Peugeot, Daihatsu, Nissan, Diesel

60,000

General Motor Indonesia, PT 1993 PMA Chevrolet 30,400

Indomobil Suzuki International, PT 1976 PMA Suzuki 120,000

Hino Indonesia Manufacturing, PT 1982 PMA Hino 10,000

Honda Prospect Motor, PT 1976 PMA Honda 42,000

Nissan Motor Indonesia, PT 1995 PMA Audi, VW, Ssangyong, Volvo, Nissan

12,000

Krama Yudha Ratu Motors,PT 1975 PMDN Mitsubishi Colt 120SS, Colt L300, Colt Diesel FE, Fuso

100,000

National Assemblers, PT 1971 PMDN Suzuki, Mazda, KIA 21,000

Trijaya Union, PT 1986 PMDN Mitsubishi Bus 1,440

Toyota Astra Motor, PT 1971 PMA Toyota 170,000

Pantja Motor, PT 1974 PMA Isuzu 51,000

Source: Gaikindo – Q1 2007

Assembling Companies & Capacity

(18)

Largest Brands Sales in Indonesia 2005-2006

Ranks Year 2005 Year 2006

Brand/model Units % Brand/model Units %

1 Toyota Kijang 93,114 17,4 Toyota Avanza 52,260 16,4

2 Toyota Avanza 54,893 10,3 Toyota Kijang 46,565 14,6

3 Suzuki Carry/ Futura 47,896 9,9 Daihatsu Xenia 23,555 7,4

4 Mitsubishi Colt

Diesel FE

35,470 6,6 Suzuki Carry/ Futura 23,301 7,3

5 Honda Jazz 32,241 6,0 Mitsubishi Colt

Diesel FE

21,740 6,8

6 Suzuki APV 27,882 5,2 Honda Jazz 18,581 5,8

7 Daihatsu Xenia 27,505 5,2 Toyota Dyna 13,479 4,2

8 Mitsubishi T-120 SS 22,187 4,2 Suzuki APV 12,283 3,9

9 Mitsubishi L 300 19,431 3,6 Isuzu Panther 11,615 3,6

10 Isuzu Panther 18,846 3,5 Mitsubishi L 300 10,722 3,4

Sub total 379,465

71,1 Sub total 234,101 73,4

Total Domestic sales 533,917

100 Total Domestic Sales 318,904 100Source: Gaikindo – 2007

(19)

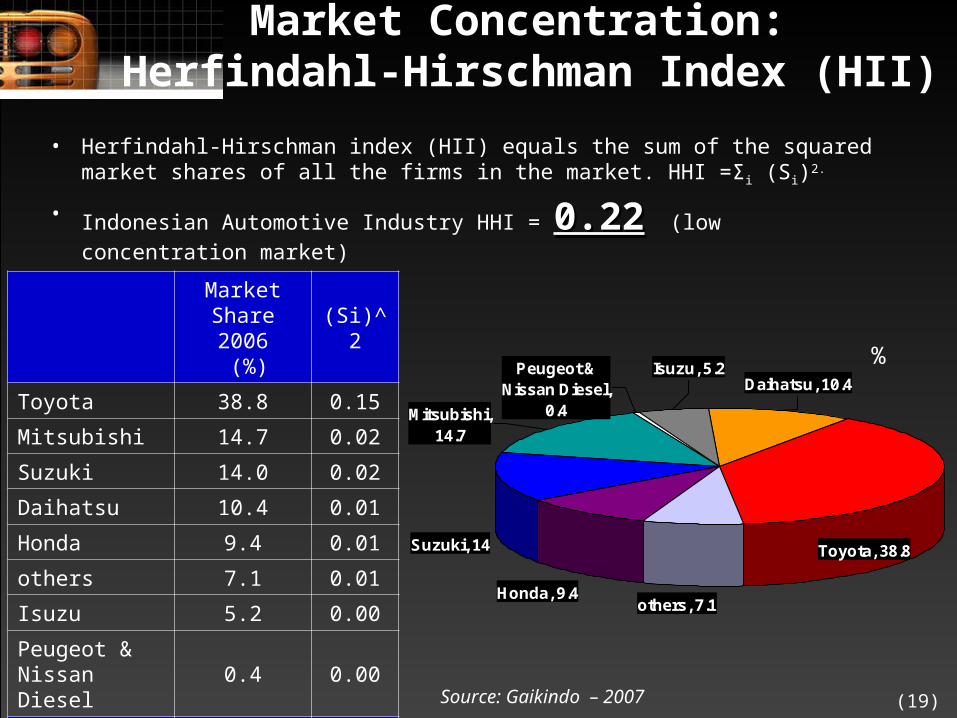

Market Concentration: Herfindahl-Hirschman Index (HII)

• Herfindahl-Hirschman index (HII) equals the sum of the squared market shares of all the firms in the market. HHI =Σi (Si)2.

• Indonesian Automotive Industry HHI = 0.220.22 (low concentration market)

Honda, 9.4

Suzuki, 14

others, 7.1

Toyota, 38.8

Daihatsu, 10.4

Mitsubishi, 14.7

Peugeot & Nissan Diesel,

0.4

Isuzu, 5.2 %

Market

Share 2006 (%)

(Si)^2

Toyota 38.8 0.15

Mitsubishi 14.7 0.02

Suzuki 14.0 0.02

Daihatsu 10.4 0.01

Honda 9.4 0.01

others 7.1 0.01

Isuzu 5.2 0.00

Peugeot & Nissan Diesel

0.4 0.00

Total 100 0.22 Source: Gaikindo – 2007

(20)

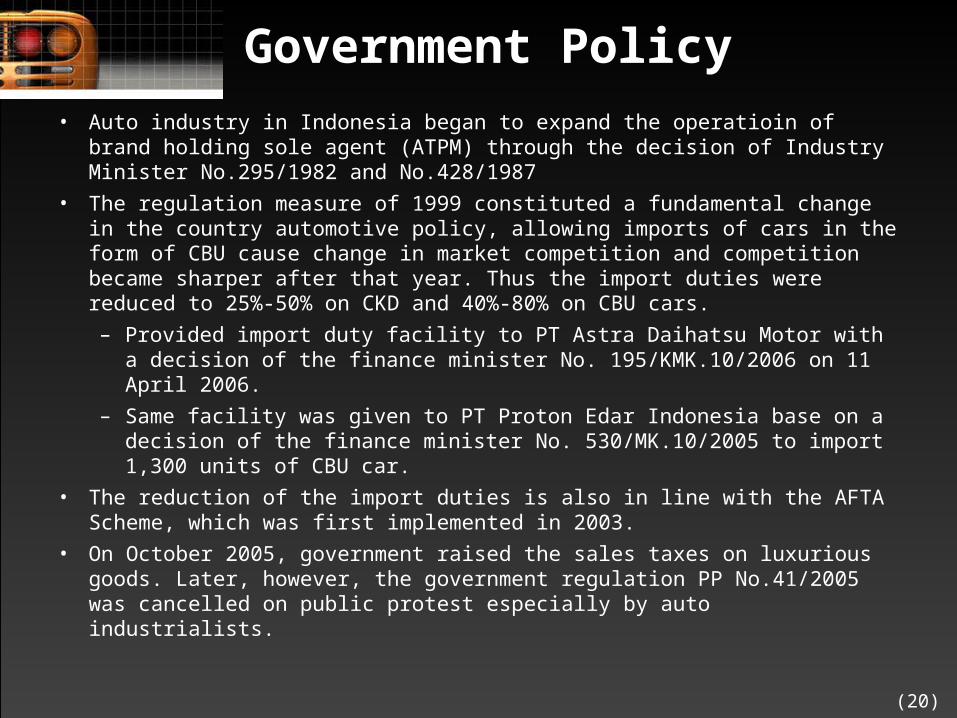

Government Policy

• Auto industry in Indonesia began to expand the operatioin of brand holding sole agent (ATPM) through the decision of Industry Minister No.295/1982 and No.428/1987

• The regulation measure of 1999 constituted a fundamental change in the country automotive policy, allowing imports of cars in the form of CBU cause change in market competition and competition became sharper after that year. Thus the import duties were reduced to 25%-50% on CKD and 40%-80% on CBU cars.

– Provided import duty facility to PT Astra Daihatsu Motor with a decision of the finance minister No. 195/KMK.10/2006 on 11 April 2006.

– Same facility was given to PT Proton Edar Indonesia base on a decision of the finance minister No. 530/MK.10/2005 to import 1,300 units of CBU car.

• The reduction of the import duties is also in line with the AFTA Scheme, which was first implemented in 2003.

• On October 2005, government raised the sales taxes on luxurious goods. Later, however, the government regulation PP No.41/2005 was cancelled on public protest especially by auto industrialists.

(21)

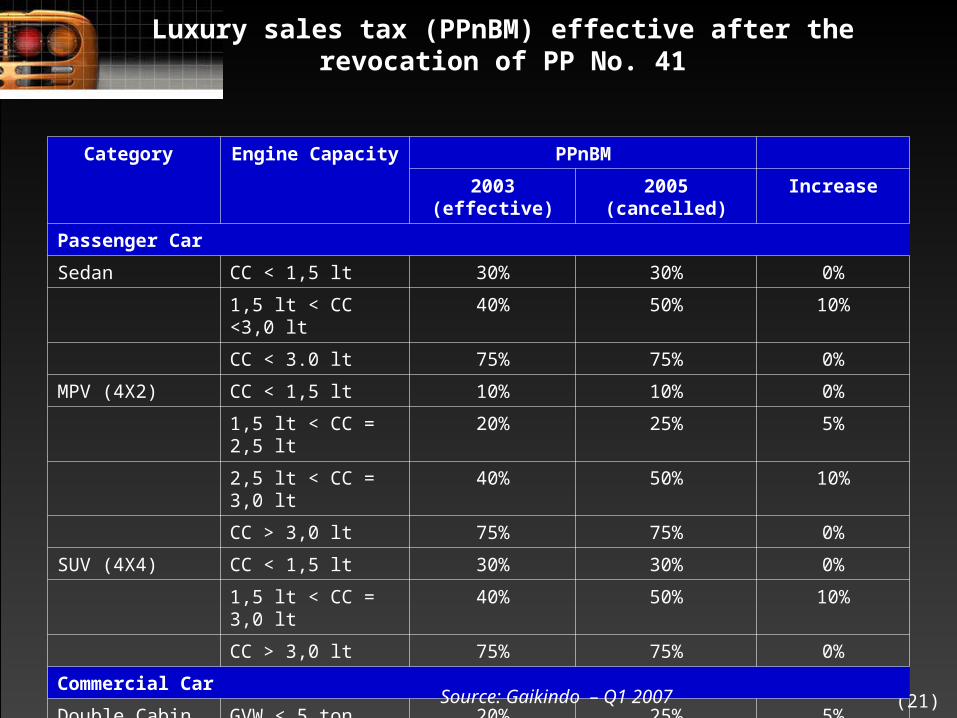

Luxury sales tax (PPnBM) effective after the revocation of PP No. 41

Category Engine Capacity PPnBM

2003 (effective) 2005 (cancelled) Increase

Passenger Car

Sedan CC < 1,5 lt 30% 30% 0%

1,5 lt < CC <3,0 lt 40% 50% 10%

CC < 3.0 lt 75% 75% 0%

MPV (4X2) CC < 1,5 lt 10% 10% 0%

1,5 lt < CC = 2,5 lt 20% 25% 5%

2,5 lt < CC = 3,0 lt 40% 50% 10%

CC > 3,0 lt 75% 75% 0%

SUV (4X4) CC < 1,5 lt 30% 30% 0%

1,5 lt < CC = 3,0 lt 40% 50% 10%

CC > 3,0 lt 75% 75% 0%

Commercial Car

Double Cabin 4X2/4X4

GVW < 5 ton

Double Cabin, All CC

20% 25% 5%

Source: Gaikindo – Q1 2007

(22)

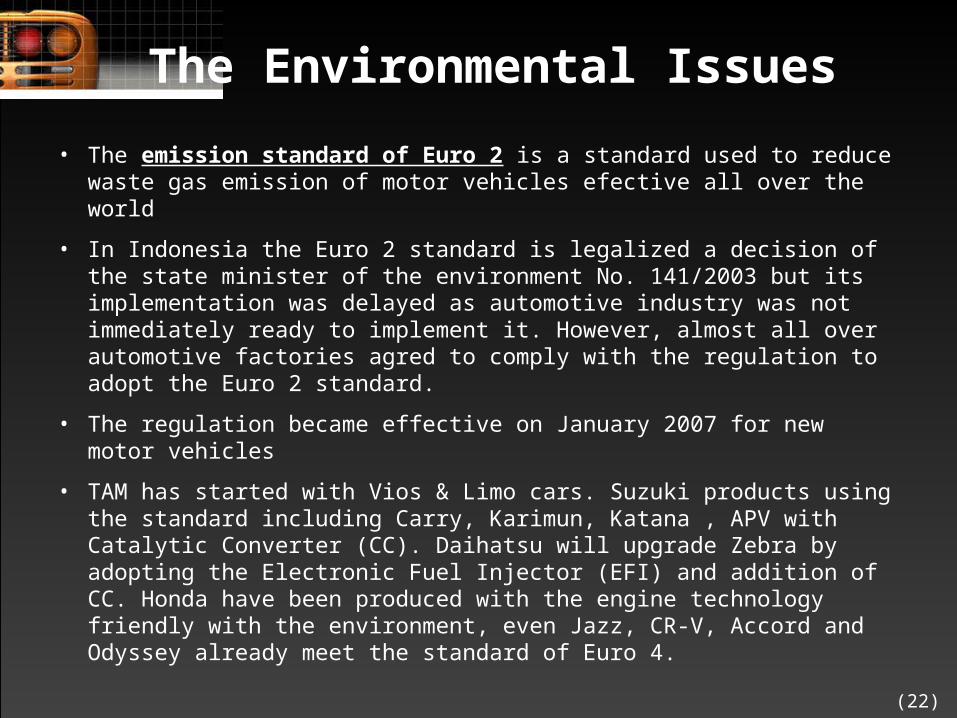

The Environmental Issues

• The emission standard of Euro 2 is a standard used to reduce waste gas emission of motor vehicles efective all over the world

• In Indonesia the Euro 2 standard is legalized a decision of the state minister of the environment No. 141/2003 but its implementation was delayed as automotive industry was not immediately ready to implement it. However, almost all over automotive factories agred to comply with the regulation to adopt the Euro 2 standard.

• The regulation became effective on January 2007 for new motor vehicles

• TAM has started with Vios & Limo cars. Suzuki products using the standard including Carry, Karimun, Katana , APV with Catalytic Converter (CC). Daihatsu will upgrade Zebra by adopting the Electronic Fuel Injector (EFI) and addition of CC. Honda have been produced with the engine technology friendly with the environment, even Jazz, CR-V, Accord and Odyssey already meet the standard of Euro 4.

(23)

ConductConduct

(24)

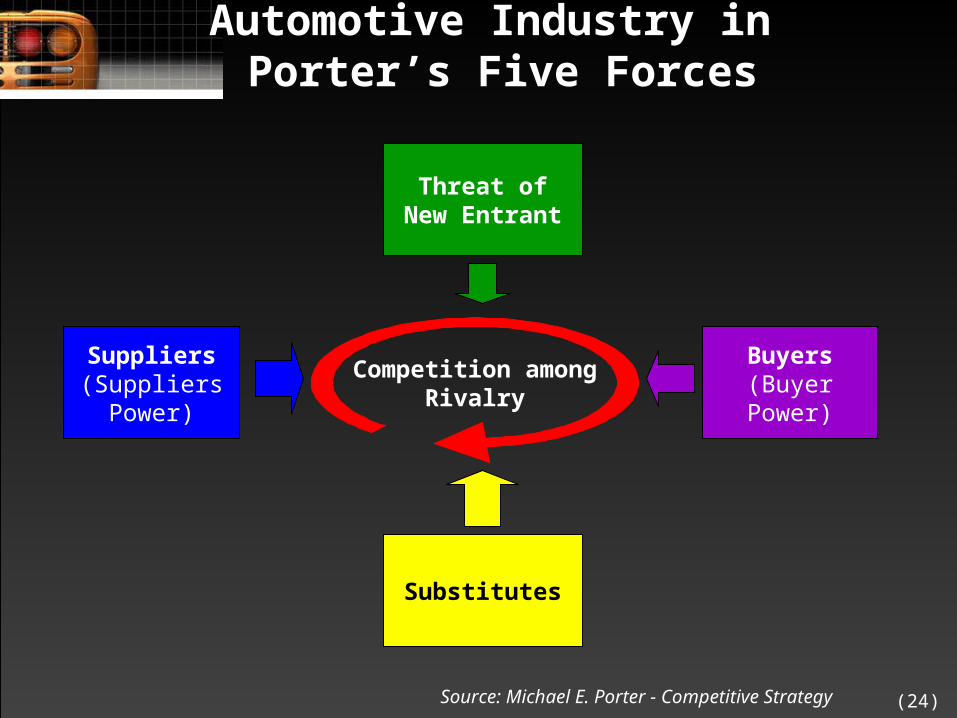

Automotive Industry in Porter’s Five Forces

Competition among Rivalry

Buyers(Buyer Power)

Suppliers(Suppliers

Power)

Threat of New Entrant

Substitutes

Source: Michael E. Porter - Competitive Strategy

(25)

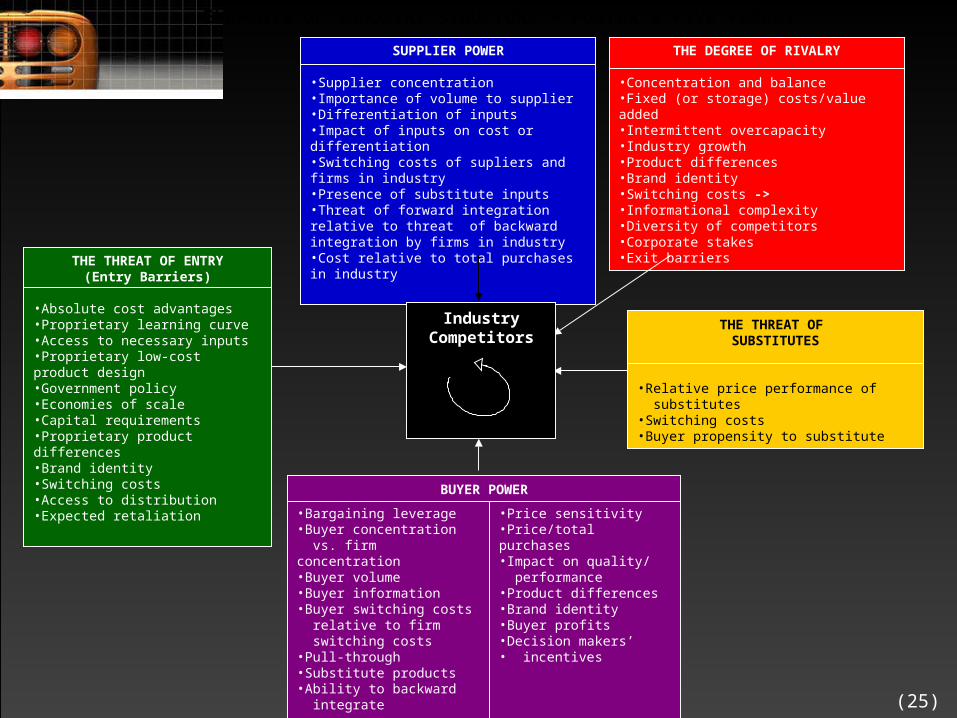

SUPPLIER POWER

•Supplier concentration•Importance of volume to supplier•Differentiation of inputs•Impact of inputs on cost or differentiation•Switching costs of supliers and firms in industry•Presence of substitute inputs•Threat of forward integration relative to threat of backward integration by firms in industry•Cost relative to total purchases in industry

THE DEGREE OF RIVALRY

•Concentration and balance•Fixed (or storage) costs/value added•Intermittent overcapacity•Industry growth•Product differences•Brand identity•Switching costs ->•Informational complexity•Diversity of competitors•Corporate stakes•Exit barriers

THE THREAT OF ENTRY(Entry Barriers)

•Absolute cost advantages•Proprietary learning curve•Access to necessary inputs•Proprietary low-cost product design•Government policy•Economies of scale•Capital requirements•Proprietary product differences•Brand identity•Switching costs•Access to distribution•Expected retaliation

•Bargaining leverage•Buyer concentration vs. firm concentration•Buyer volume•Buyer information•Buyer switching costs relative to firm switching costs•Pull-through•Substitute products•Ability to backward integrate

•Price sensitivity•Price/total purchases •Impact on quality/ performance•Product differences •Brand identity•Buyer profits•Decision makers’• incentives

BUYER POWER

THE THREAT OF SUBSTITUTES

•Relative price performance of substitutes•Switching costs•Buyer propensity to substitute

ELEMENTS OF INDUSTRY STRUCTURE – PORTER’S FIVE FORCES

Industry Competitors

(26)

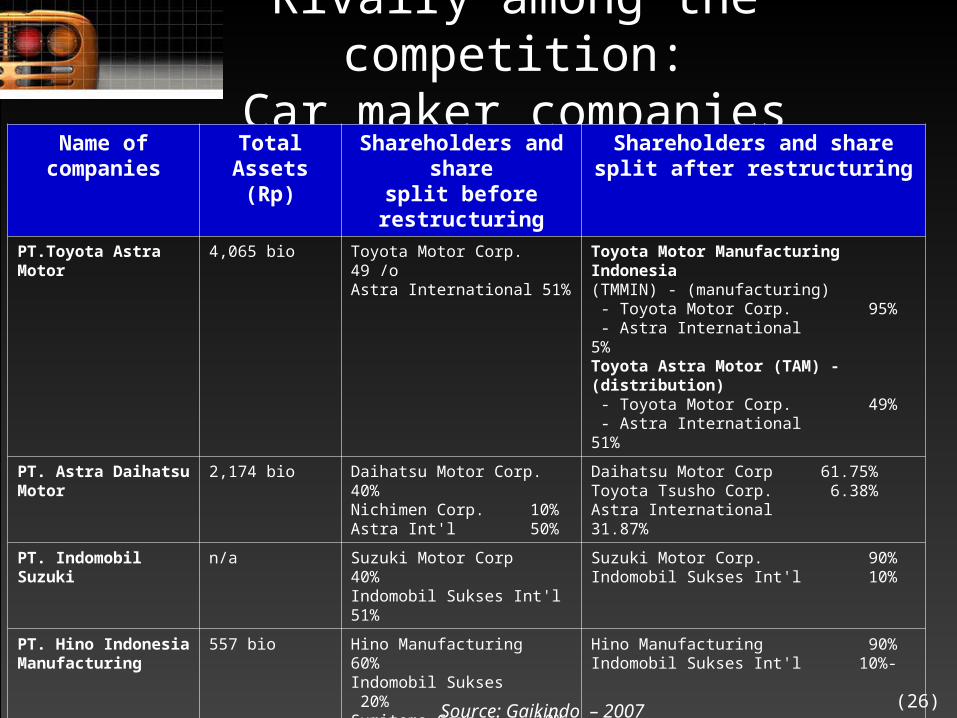

Rivalry among the competition:Car maker companies

Name of companies

Total Assets

(Rp)

Shareholders and share

split before restructuring

Shareholders and sharesplit after restructuring

PT.Toyota Astra Motor 4,065 bio Toyota Motor Corp. 49 /oAstra International 51%

Toyota Motor Manufacturing Indonesia(TMMIN) - (manufacturing) - Toyota Motor Corp. 95% - Astra International 5%Toyota Astra Motor (TAM) - (distribution) - Toyota Motor Corp. 49% - Astra International 51%

PT. Astra DaihatsuMotor

2,174 bio Daihatsu Motor Corp. 40%Nichimen Corp. 10%Astra Int'l 50%

Daihatsu Motor Corp 61.75% Toyota Tsusho Corp. 6.38% Astra International 31.87%

PT. Indomobil Suzuki n/a Suzuki Motor Corp 40%Indomobil Sukses Int'l 51%

Suzuki Motor Corp. 90%Indomobil Sukses Int'l 10%

PT. Hino IndonesiaManufacturing

557 bio Hino Manufacturing 60%Indomobil Sukses 20%Sumitomo Corp. 10%

Hino Manufacturing 90%Indomobil Sukses Int'l 10%-

PT. Tjahja Sakti Motor n/a BMW AG 50%Astra International 50%

PT. Tjahja Sakti Motor (manufacturing) - Astra International 100%PT BMW Indonesia (Sales / Distribution) - BMW AG 100%

PT. Honda ProspectMotor

1,602 bio Honda Motor Co. Ltd 49%Honda Prospect Motor 51 %

Honda Motor Co. Ltd 51%Honda Prospect Motor 49%

Source: Gaikindo – 2007

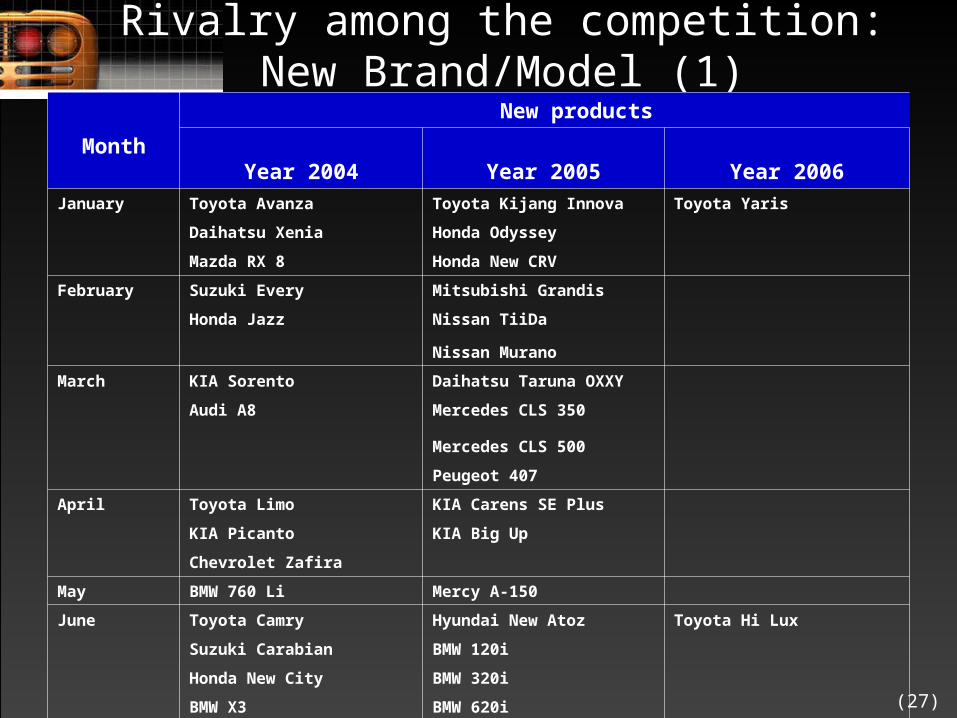

(27)

Rivalry among the competition:New Brand/Model (1)

Month

New products

Year 2004 Year 2005 Year 2006

January Toyota Avanza Toyota Kijang Innova Toyota Yaris

Daihatsu Xenia Honda Odyssey

Mazda RX 8 Honda New CRV

February Suzuki Every Mitsubishi Grandis

Honda Jazz Nissan TiiDa

Nissan Murano

March KIA Sorento Daihatsu Taruna OXXY

Audi A8 Mercedes CLS 350

Mercedes CLS 500

Peugeot 407

April Toyota Limo KIA Carens SE Plus

KIA Picanto KIA Big Up

Chevrolet Zafira

May BMW 760 Li Mercy A-150

June Toyota Camry Hyundai New Atoz Toyota Hi Lux

Suzuki Carabian BMW 120i

Honda New City BMW 320i

BMW X3 BMW 620i

BMW 740i

(28)

Month

New products

Year 2004 Year 2005 Year 2006

July Nissan New Cedric Toyota Fortuner Suzuki Grand Vitara

Chevrolet Aveo Hyundai Tucson Hyundai Azera

Renault Megane Nissan X-Trail STT

August Suzuki APV Mitsubishi Maven Toyota Avanza VVTi

Daihatsu New Zebra BMW 523 Daihatsu Xenia VVTi

Daihatsu New Taruna BMW 750 Li Chevrolet Kalos

Nissan New Serena Peugeot 407 2,9 Nissan Latio

Chevrolet Spark Mercedes R350L

VW New Caravelle

September Toyota Kijang Innova Suzuki Swift Chery QQ

Nissan Teana Ford Focus

Ford Ranger DC KIA Pride

October VW Touareg Mercedes C230

Mercedes C280

Mercedes E280

Mercedes B170

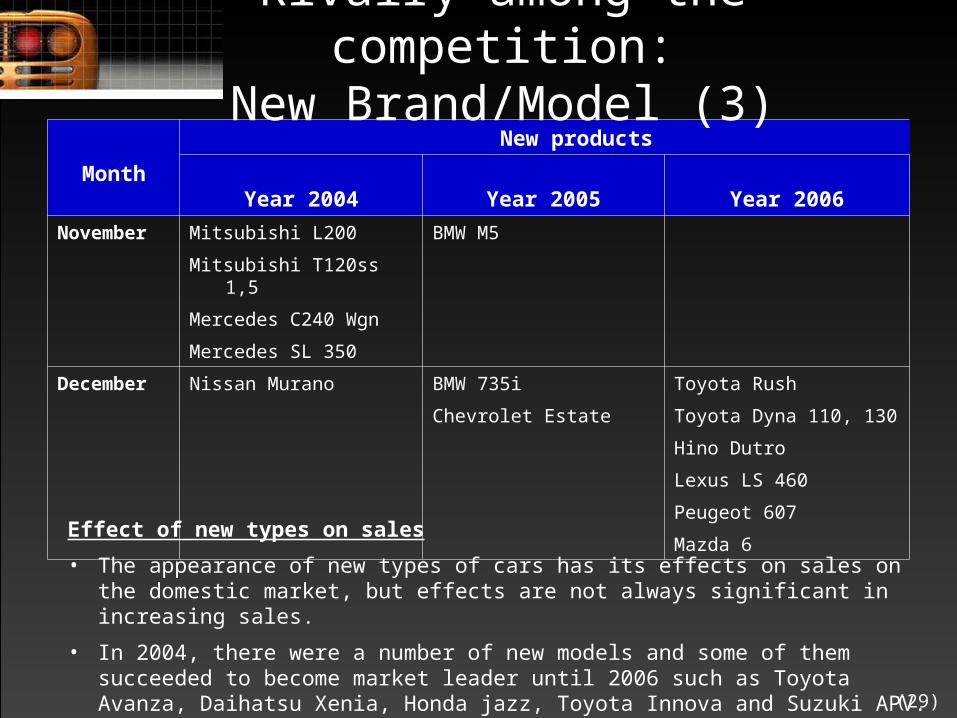

Rivalry among the competition:New Brand/Model (2)

(29)

Month

New products

Year 2004 Year 2005 Year 2006

November Mitsubishi L200 BMW M5

Mitsubishi T120ss 1,5

Mercedes C240 Wgn

Mercedes SL 350

December Nissan Murano BMW 735i Toyota Rush

Chevrolet Estate Toyota Dyna 110, 130

Hino Dutro

Lexus LS 460

Peugeot 607

Mazda 6

Rivalry among the competition:New Brand/Model (3)

Effect of new types on sales

• The appearance of new types of cars has its effects on sales on the domestic market, but effects are not always significant in increasing sales.

• In 2004, there were a number of new models and some of them succeeded to become market leader until 2006 such as Toyota Avanza, Daihatsu Xenia, Honda jazz, Toyota Innova and Suzuki APV.

(30)

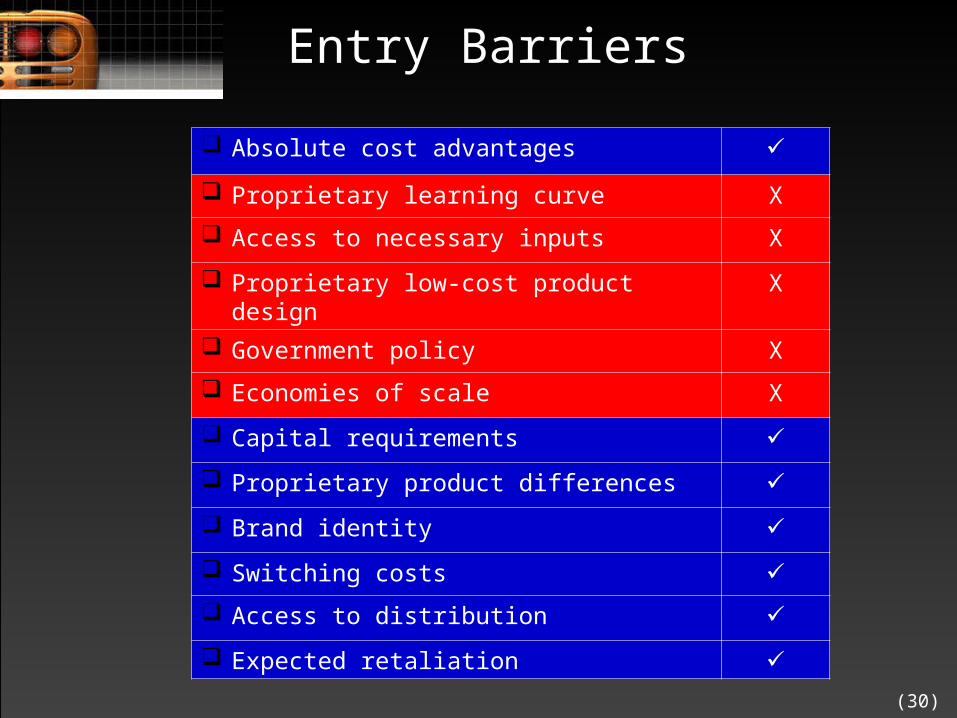

Entry Barriers

Absolute cost advantages

Proprietary learning curve X

Access to necessary inputs X

Proprietary low-cost product design X

Government policy X

Economies of scale X

Capital requirements

Proprietary product differences

Brand identity

Switching costs

Access to distribution

Expected retaliation

(31)

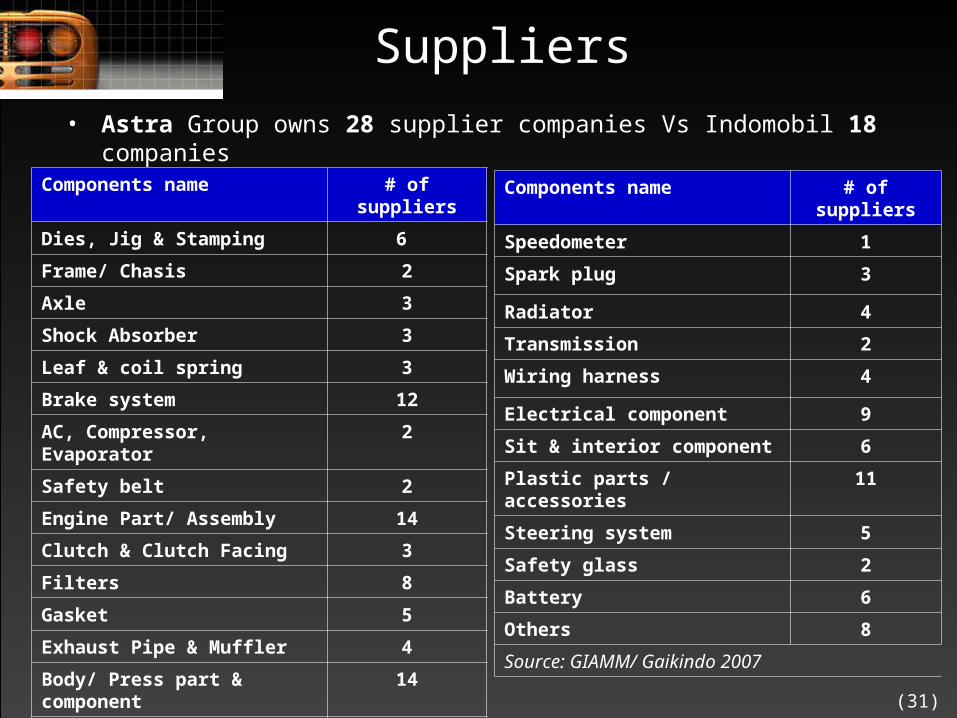

Suppliers

Components name # of suppliers

Dies, Jig & Stamping 6

Frame/ Chasis 2

Axle 3

Shock Absorber 3

Leaf & coil spring 3

Brake system 12

AC, Compressor, Evaporator 2

Safety belt 2

Engine Part/ Assembly 14

Clutch & Clutch Facing 3

Filters 8

Gasket 5

Exhaust Pipe & Muffler 4

Body/ Press part & component 14

Rubber parts 8

Wheel Rim / Alloy 6

Components name # of suppliers

Speedometer 1

Spark plug 3

Radiator 4

Transmission 2

Wiring harness 4

Electrical component 9

Sit & interior component 6

Plastic parts / accessories 11

Steering system 5

Safety glass 2

Battery 6

Others 8

Source: GIAMM/ Gaikindo 2007

• Astra Group owns 28 supplier companies Vs Indomobil 18 companies

(32)

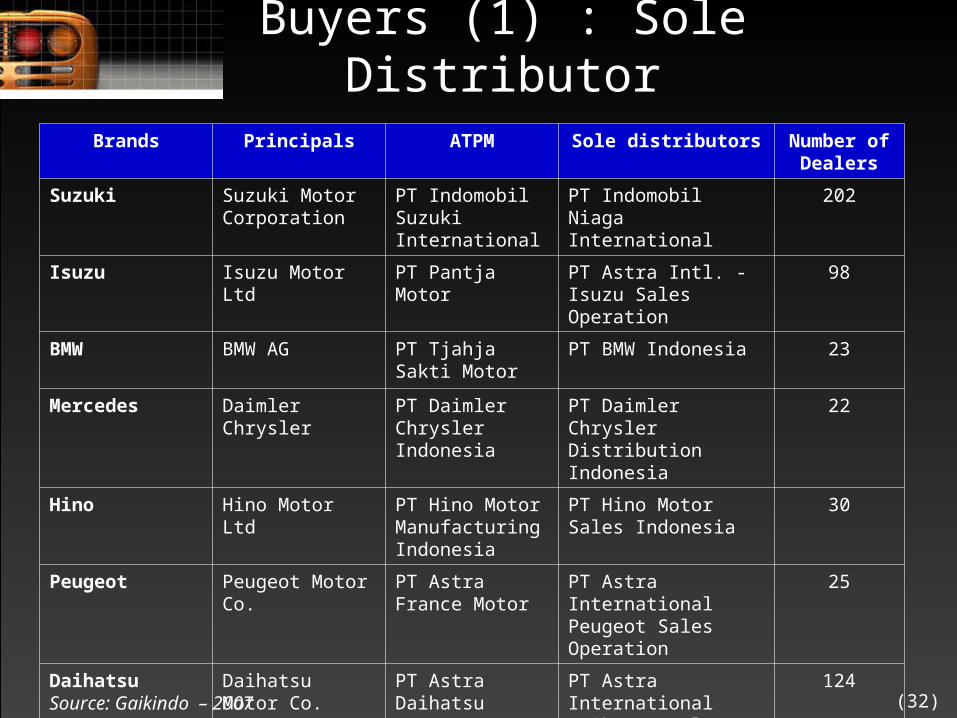

Buyers (1) : Sole Distributor

Brands Principals ATPM Sole distributors Number of Dealers

Suzuki Suzuki Motor Corporation

PT Indomobil Suzuki International

PT Indomobil Niaga International

202

Isuzu Isuzu Motor Ltd PT Pantja Motor PT Astra Intl. - Isuzu Sales Operation

98

BMW BMW AG PT Tjahja Sakti Motor

PT BMW Indonesia 23

Mercedes Daimler Chrysler PT Daimler Chrysler Indonesia

PT Daimler Chrysler Distribution Indonesia

22

Hino Hino Motor Ltd PT Hino Motor Manufacturing Indonesia

PT Hino Motor Sales Indonesia

30

Peugeot Peugeot Motor Co.

PT Astra France Motor

PT Astra International Peugeot Sales Operation

25

Daihatsu Daihatsu Motor Co.

PT Astra Daihatsu Motor

PT Astra International Daihatsu Sales Operation

124

Source: Gaikindo – 2007

(33)

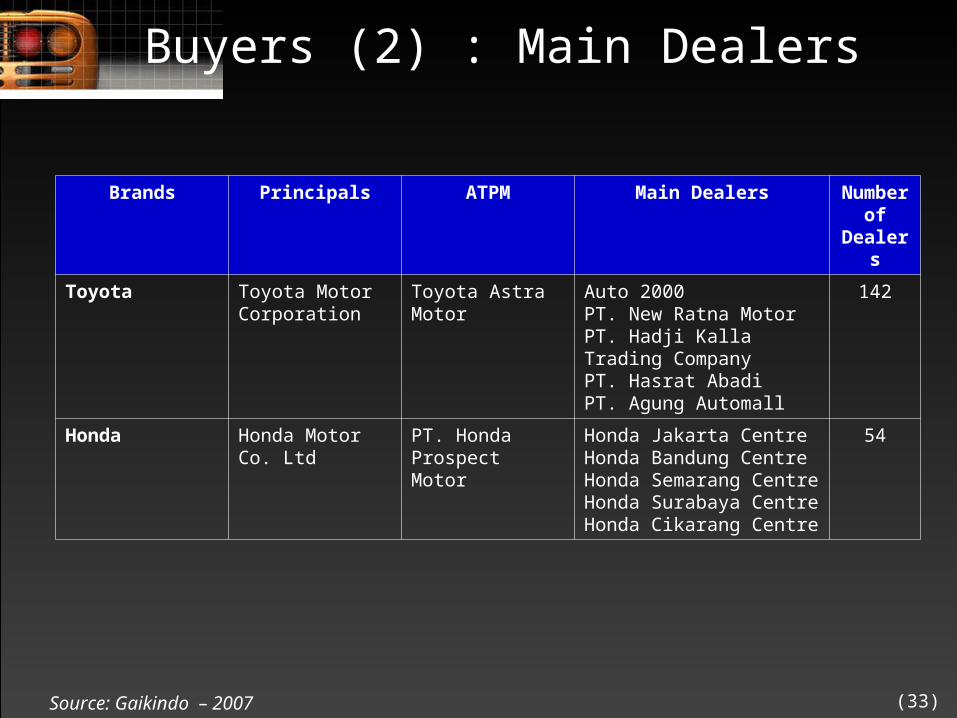

Buyers (2) : Main Dealers

Brands Principals ATPM Main Dealers Number of

Dealers

Toyota Toyota Motor Corporation

Toyota Astra Motor

Auto 2000PT. New Ratna MotorPT. Hadji Kalla Trading CompanyPT. Hasrat AbadiPT. Agung Automall

142

Honda Honda Motor Co. Ltd

PT. Honda Prospect Motor

Honda Jakarta CentreHonda Bandung CentreHonda Semarang CentreHonda Surabaya CentreHonda Cikarang Centre

54

Source: Gaikindo – 2007

(34)

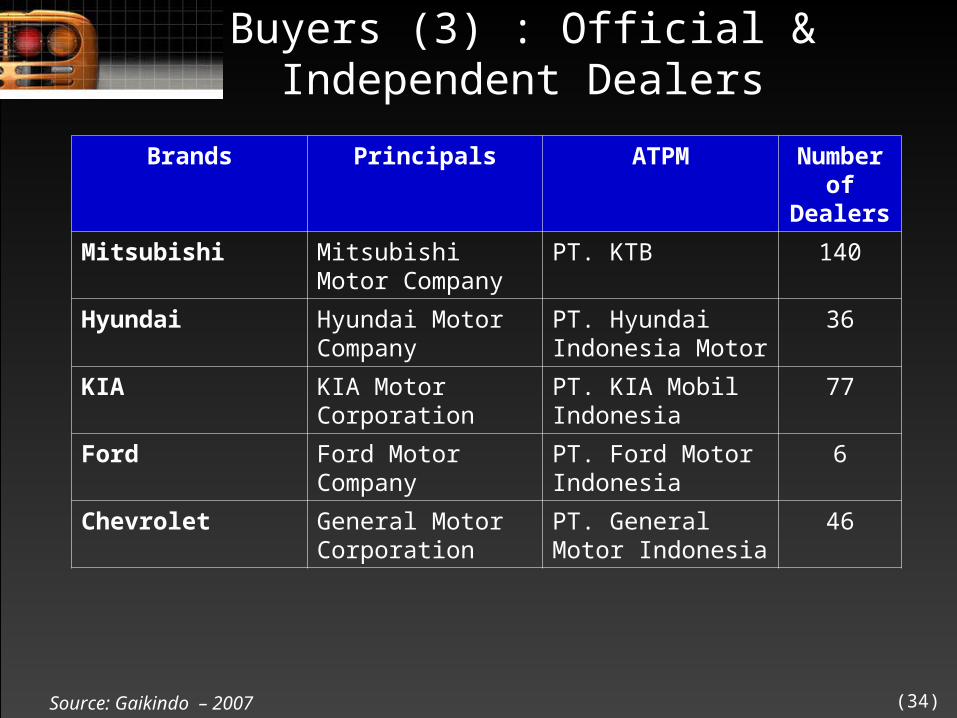

Buyers (3) : Official & Independent Dealers

Brands Principals ATPM Number of

Dealers

Mitsubishi Mitsubishi Motor Company

PT. KTB 140

Hyundai Hyundai Motor Company

PT. Hyundai Indonesia Motor

36

KIA KIA Motor Corporation

PT. KIA Mobil Indonesia

77

Ford Ford Motor Company

PT. Ford Motor Indonesia

6

Chevrolet General Motor Corporation

PT. General Motor Indonesia

46

Source: Gaikindo – 2007

(35)

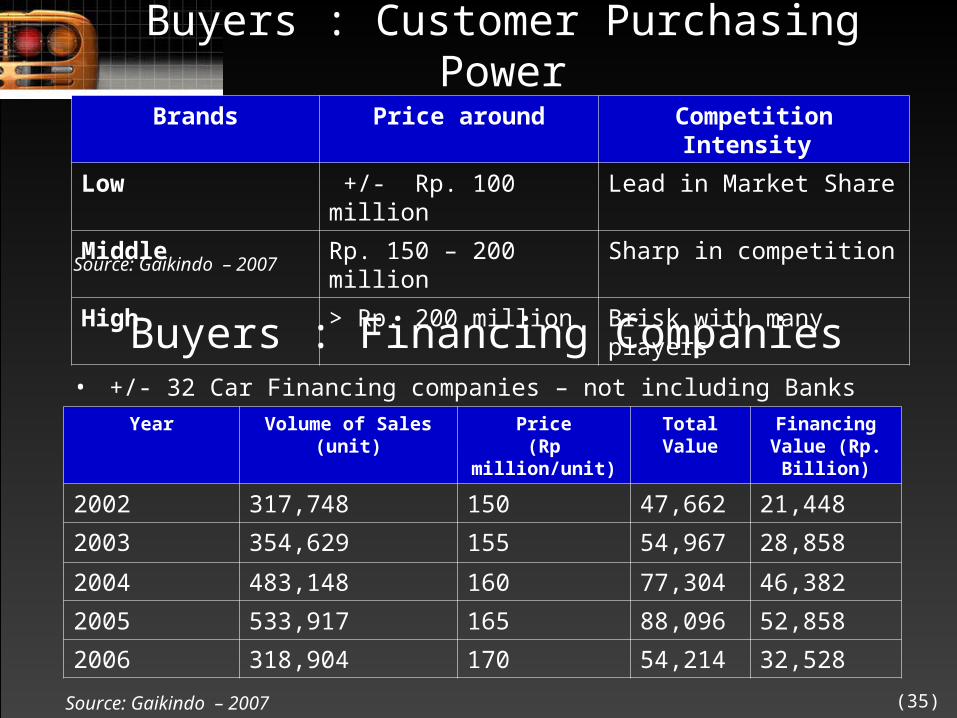

Buyers : Customer Purchasing Power

Brands Price around Competition Intensity

Low +/- Rp. 100 million Lead in Market Share

Middle Rp. 150 – 200 million Sharp in competition

High > Rp. 200 million Brisk with many playersSource: Gaikindo – 2007

Buyers : Financing Companies

Year Volume of Sales (unit) Price(Rp million/unit)

Total Value Financing Value (Rp.

Billion)

2002 317,748 150 47,662 21,448

2003 354,629 155 54,967 28,858

2004 483,148 160 77,304 46,382

2005 533,917 165 88,096 52,858

2006 318,904 170 54,214 32,528

Source: Gaikindo – 2007

• +/- 32 Car Financing companies – not including Banks

(36)

New Entrant – Threat From Chinese Car

(37)

Substitute

• 2 Wheelers – population in 2005 = 33.193.076*

• Mass / Public Transportation

* Source: Direktorat Samapta Polri/ GIAMM – notes: not included Ranmor, ABRI and diplomatic corps - 2005

(38)

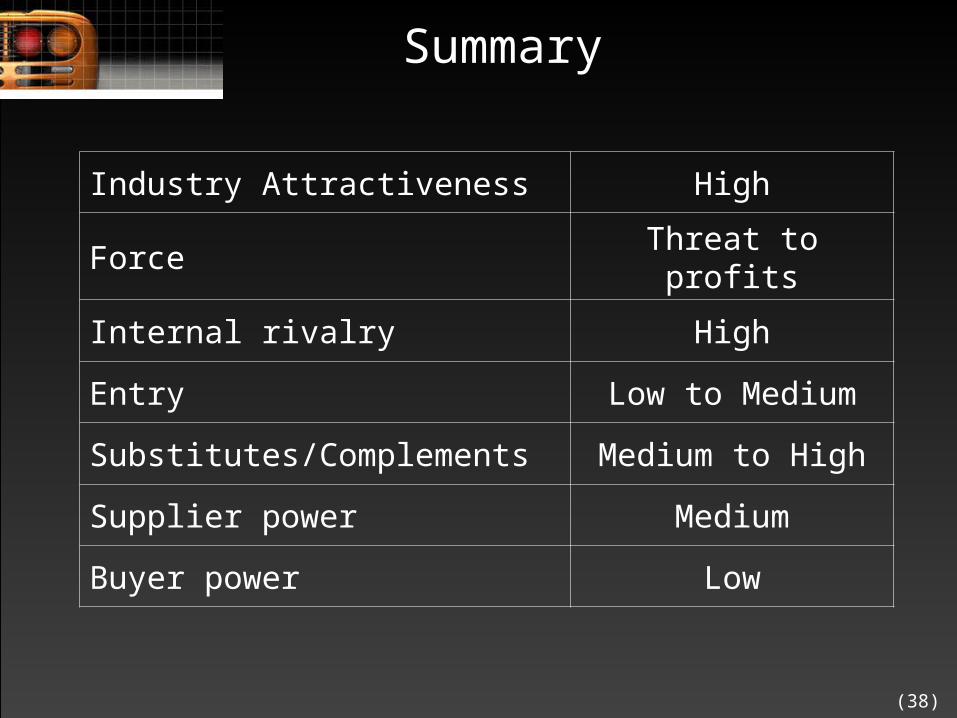

Summary

Industry Attractiveness High

Force Threat to profits

Internal rivalry High

Entry Low to Medium

Substitutes/Complements Medium to High

Supplier power Medium

Buyer power Low

(39)

PerformancePerformance

(40)

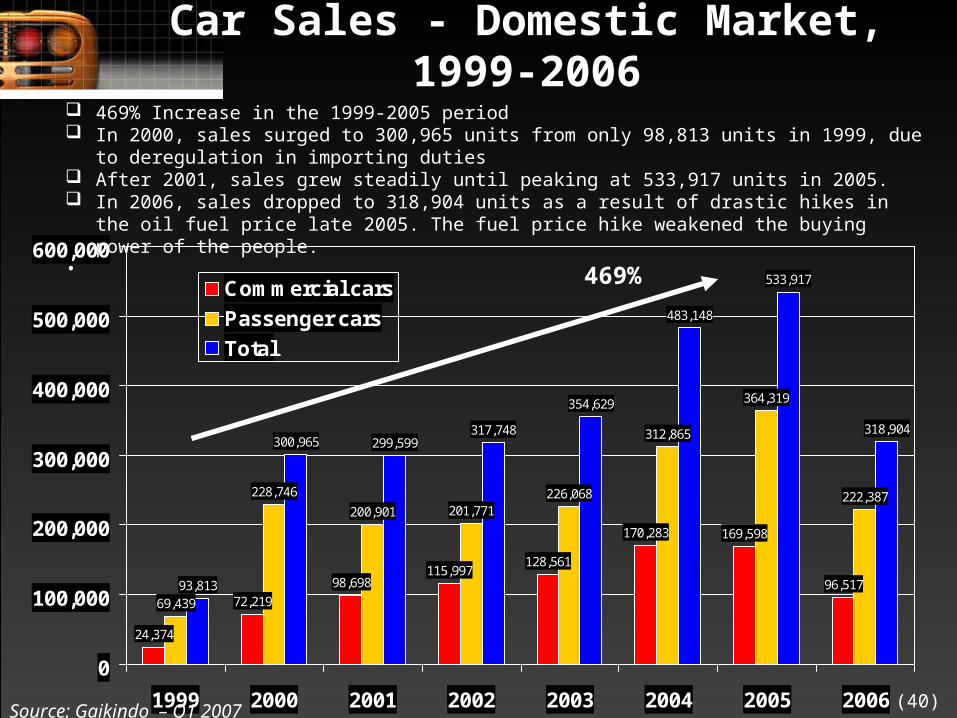

Car Sales - Domestic Market, 1999-2006

24,374

72,219

98,698115,997

128,561

170,283 169,598

96,517

69,439

228,746

200,901 201,771226,068

312,865

364,319

222,387

93,813

300,965 299,599317,748

354,629

483,148

533,917

318,904

0

100,000

200,000

300,000

400,000

500,000

600,000

1999 2000 2001 2002 2003 2004 2005 2006

Commercial cars

Passenger cars

Total

469% Increase in the 1999-2005 period In 2000, sales surged to 300,965 units from only 98,813 units in 1999, due to deregulation in

importing duties After 2001, sales grew steadily until peaking at 533,917 units in 2005. In 2006, sales dropped to 318,904 units as a result of drastic hikes in the oil fuel price late 2005.

The fuel price hike weakened the buying power of the people. •

469%

Source: Gaikindo – Q1 2007

(41)

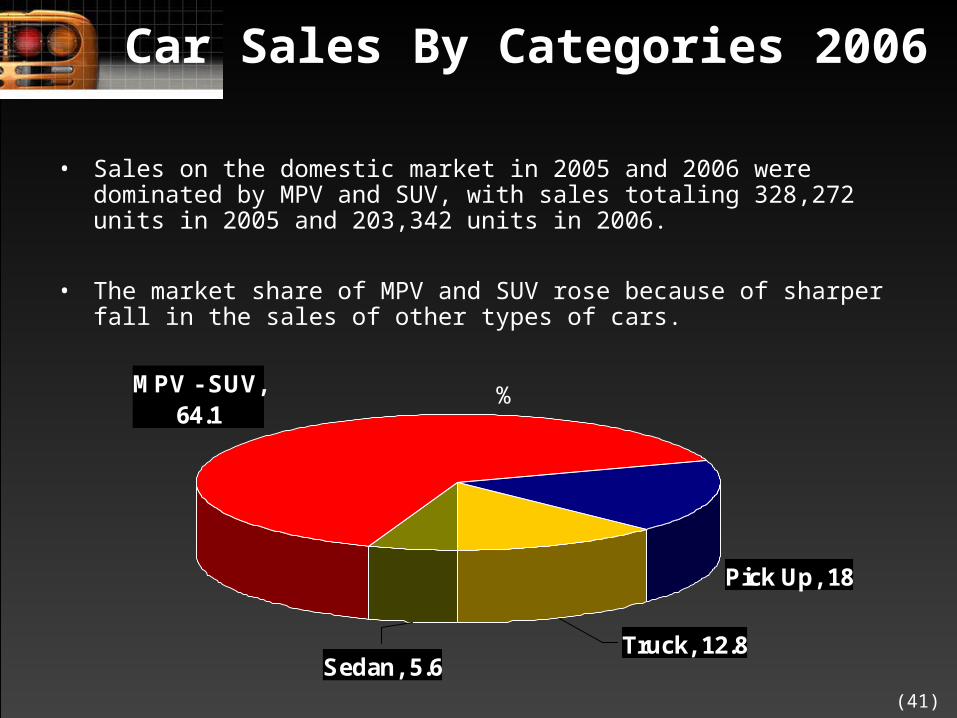

Car Sales By Categories 2006

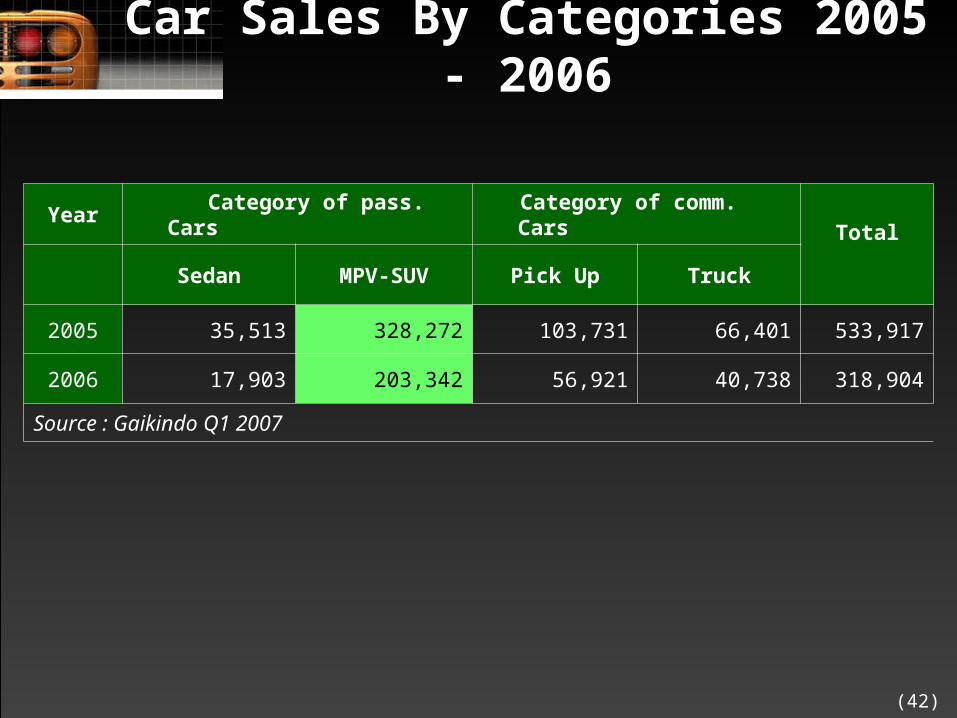

• Sales on the domestic market in 2005 and 2006 were dominated by MPV and SUV, with sales totaling 328,272 units in 2005 and 203,342 units in 2006.

• The market share of MPV and SUV rose because of sharper fall in the sales of other types of cars.

MPV - SUV, 64.1

Pick Up, 18

Truck, 12.8Sedan, 5.6

%

(42)

Car Sales By Categories 2005 - 2006

Year Category of pass. Cars Category of comm. CarsTotal

Sedan MPV-SUV Pick Up Truck

2005 35,513 328,272 103,731 66,401 533,917

2006 17,903 203,342 56,921 40,738 318,904

Source : Gaikindo Q1 2007

(43)

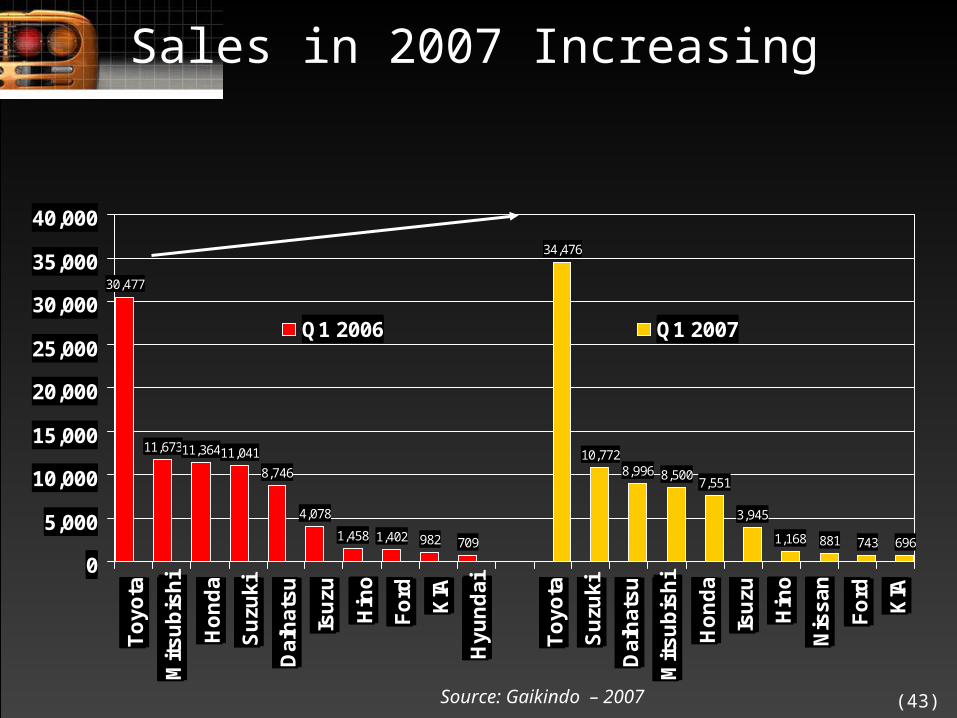

Sales in 2007 Increasing

30,477

11,67311,36411,041

8,746

4,078

1,458 1,402 982 709

34,476

10,7728,996 8,500

7,551

3,945

1,168 881 743 696

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

To

yo

ta

Mit

su

bis

hi

Ho

nd

a

Su

zuk

i

Da

iha

tsu

Isu

zu

Hin

o

Fo

rd

KIA

Hy

un

da

i

To

yo

ta

Su

zuk

i

Da

iha

tsu

Mit

su

bis

hi

Ho

nd

a

Isu

zu

Hin

o

Nis

sa

n

Fo

rd

KIA

Q1 2006 Q1 2007

Source: Gaikindo – 2007

(44)

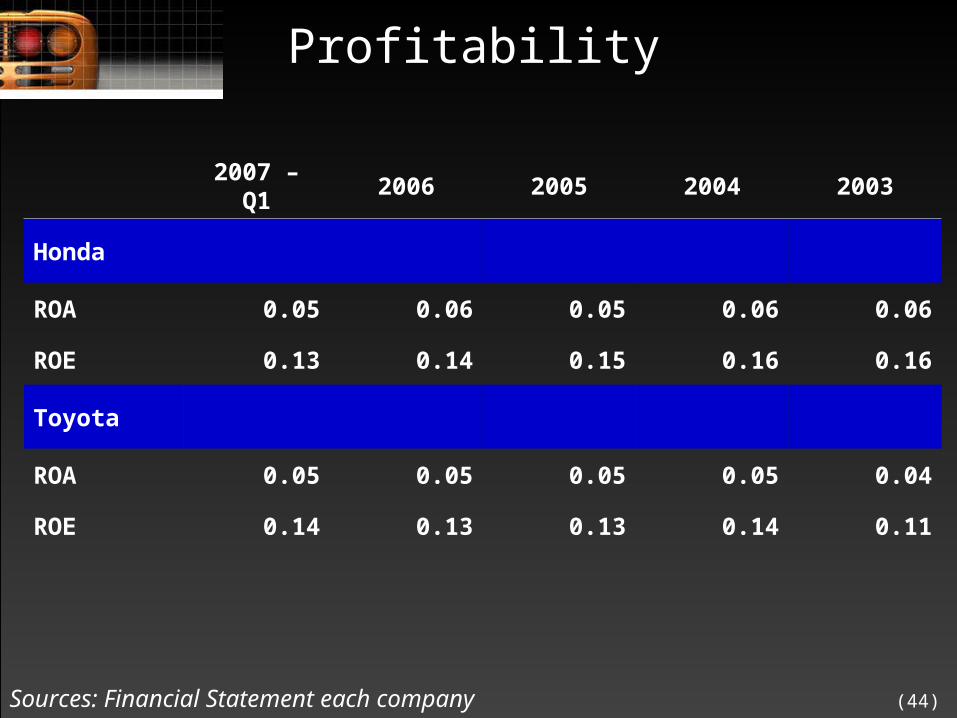

Profitability

2007 – Q1 2006 2005 2004 2003

Honda

ROA 0.05 0.06 0.05 0.06 0.06

ROE 0.13 0.14 0.15 0.16 0.16

Toyota

ROA 0.05 0.05 0.05 0.05 0.04

ROE 0.14 0.13 0.13 0.14 0.11

Sources: Financial Statement each company

(45)

Competitive Competitive StrategyStrategy

(46)

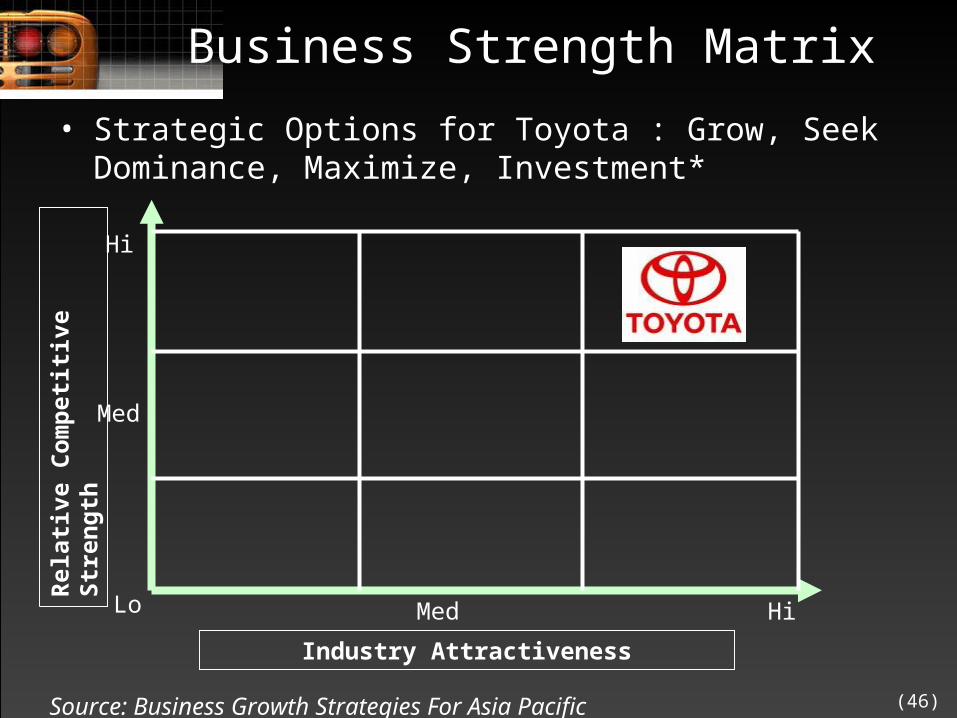

Business Strength Matrix

• Strategic Options for Toyota : Grow, Seek Dominance, Maximize, Investment*

Source: Business Growth Strategies For Asia Pacific

Rel

ativ

e C

om

pet

itiv

e S

tren

gth

Industry Attractiveness

HiLo

Hi

Med

Med

(47)

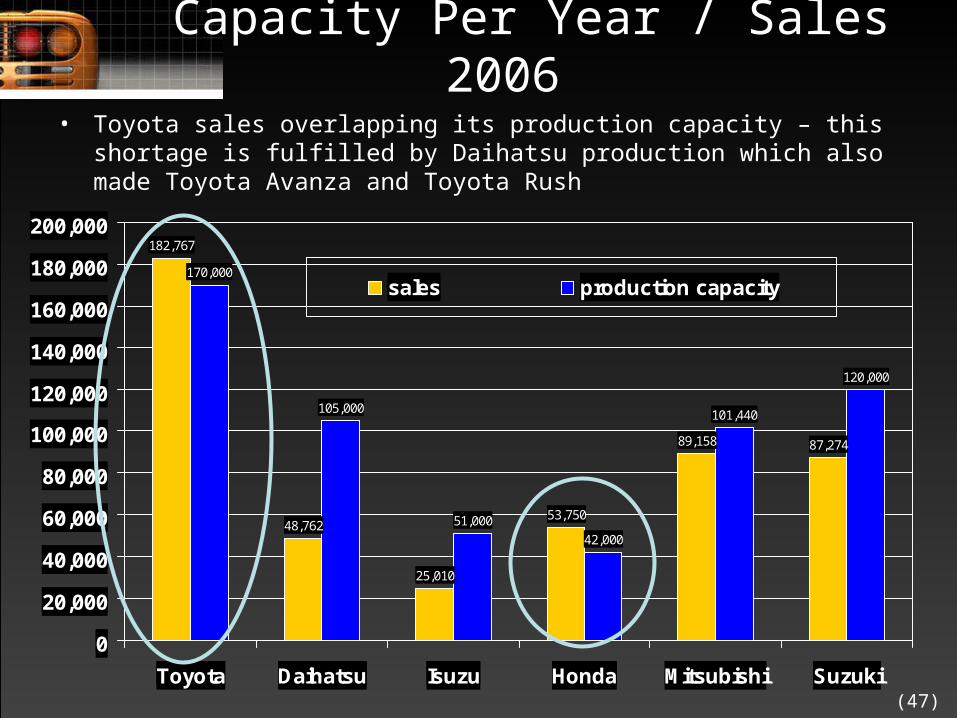

Capacity Per Year / Sales 2006

182,767

48,762

25,010

53,750

89,158 87,274

170,000

105,000

51,000

42,000

101,440

120,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Toyota Daihatsu Isuzu Honda Mitsubishi Suzuki

sales production capacity

• Toyota sales overlapping its production capacity – this shortage is fulfilled by Daihatsu production which also made Toyota Avanza and Toyota Rush

(48)

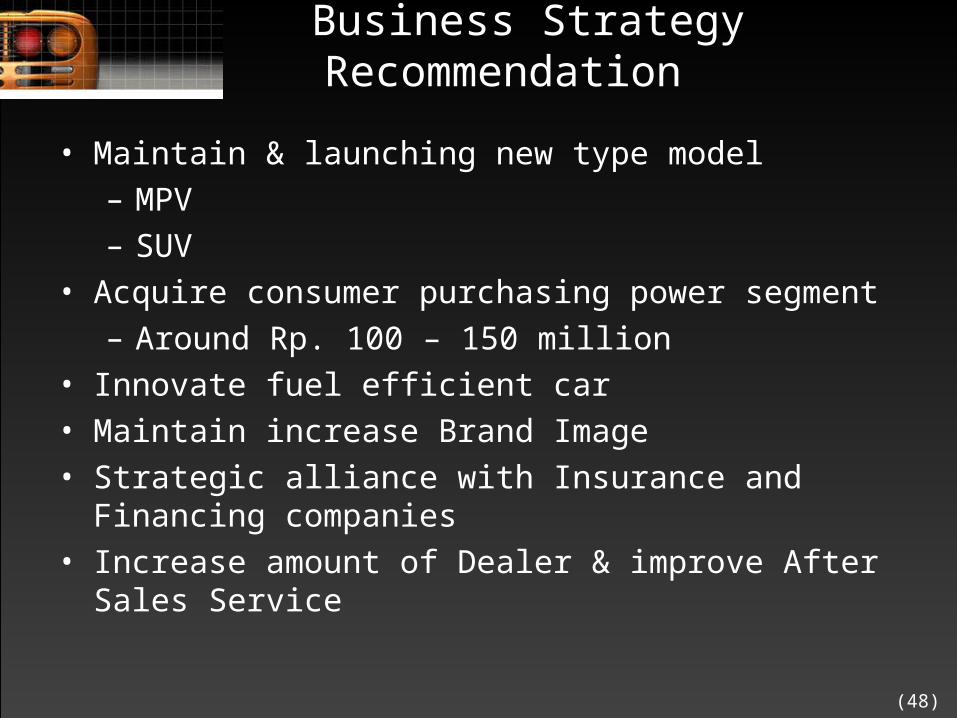

Business Strategy Recommendation

• Maintain & launching new type model – MPV– SUV

• Acquire consumer purchasing power segment– Around Rp. 100 – 150 million

• Innovate fuel efficient car• Maintain increase Brand Image• Strategic alliance with Insurance and Financing

companies• Increase amount of Dealer & improve After Sales

Service

(49)

Thank You

![COMPANY - Automotive Meetings...AUTOMOTIVE MANAGEMENT [PROYECTO] POLYCOND - Creating competitive edge for the European polymer processing industry driving new added-value products](https://static.cupdf.com/doc/110x72/608a5d8092464f3c971b5bef/company-automotive-meetings-automotive-management-proyecto-polycond-creating.jpg)