Don’t Miss Out on NASP’sFall Conference!

Impact of the Affordable Care Act on Specialty Pharmacy

Moderator:Jim Smeeding, RPh, MPA

Professional AffairsNASP

Impact of the Affordable Care Act on Specialty Pharmacy

Lauren BarnesSenior Vice PresidentAvalere Health, LLC

Coverage Expansion

Medicaid Expansion Exchanges

Payment and Delivery Reforms

Payment Reforms ACOs

Coverage Expansion and Delivery System Reforms Provided in the ACA are Likely to Impact Specialty Pharmacy Business

New Eligibility Rules Will Increase Medicaid Enrollment by More Than 40 Percent in Almost Half of States, Which Has Implications for Specialty Pharmacy

WA

OR

NV

ID

MT

WY

COUT

AZ NM

TX

OK

KS

NE

SD

NDMN

IA

MO

AR

LAMS

AL GA

SC

NCTN

IL

WIMI

IN OH

PA

KYVA

FL

CA

NY

VT

ME

NH

MARI

WVDE

MD

NJ

AK

HI

CT

DC

Percent Increase in Medicaid Enrollment as Compared to Baseline Coverage Assuming All States Expand, 2022

40.1% – 50.0% (14)

≥ 50.1% (10)

30.1% – 40.0% (13)

≤ 20.0% (6)

Percent Change from 2022 BaselineMedicaid Enrollment

Source: Avalere Enrollment Model, assumes all states expand Medicaid

20.0% – 30.0% (8)

Coverage Expansion

Specialty Pharmacies Are Expected to Feel Increased Cost Pressure with Reimbursement Changes

Alabama received CMS approval to implement a reimbursement methodology based on AAC in September 2010

Oregon received CMS approval for a similar plan to reimburse pharmacies based on AAC in January 2011

Idaho implemented AAC in September 2011

Louisiana implemented AAC in September 2012

State Medicaid programs have led movement away from AWP to AAC (examples below)

These changes have adjusted ingredients costs and dispensing fees for pharmacies in Medicaid

» Ingredient Cost: Based on survey of invoices, does not include SPPs in survey

» Dispensing Fee: Based on review of the cost of dispensing, typically does not include SPPs

While these new reimbursement formulas are not including SPPs in surveys, they do reimburse SPPs using these metrics.

AAC = Average Acquisition CostAWP = Average Wholesale PriceCMS = Centers for Medicare & Medicaid ServicesSPP = Specialty Pharmacy Provider

Coverage Expansion

Approximately 18 Million Are Expected to Enroll in Subsidized Coverage Through Exchanges, Which May Increase Pressures on Specialty Pharmacy to Control Costs

WA

OR

NV

ID

MT

WY

COUT

AZ NM

TX

OK

KS

NE

SD

NDMN

IA

MO

AR

LAMS

AL GA

SC

NCTN

IL

WIMI

IN OH

PA

KYVA

FL

CA

NY

VT

ME

NH

MARI

WVDE

MD

NJ

AK

HI

CT

DC

Enrollment in Subsidized Coverage, 2022

301,000-450,000 (9)

≥ 451,000 (10)

151,000-300,000 (14)

≤ 150,000 (18)

Enrollment in Subsidized Coverage (2022)

Source: Avalere Enrollment Model, assumes all states expand Medicaid

Coverage Expansion

Upside/Downside Risk

Penalties Only

Nonpayment

Baseline/Performance Period

Medicare Payment and Delivery Reform Programs Will Impact Hospitals Over The Next Ten Years

Source: Centers for Medicare & Medicaid ServicesACO = Accountable Care Organization; VBP=Value-based Purchasing

2008 2009 2011 2013 20172015 20182016

Hospital Inpatient Quality Reporting Program1

ACOs2

Readmission Penalties for Low Performers

20142010 2012

Bundled Payment for Care Improvement

Hospital Acquired Conditions3

Hospital Outpatient Quality Reporting Program1

Hospital VBP4

Private Payers are also engaging in a variety of payment and delivery reform to curb growing costs and encourage value.

Payment and Delivery Reform

Payment Reform Forces Hospitals to Build New Competencies, Which Could Alter Thinking about Drugs

Impact on Health Systems

Reductions in Payment

Changes in Volume/ Access

Increase in Transparency

Transfer of Risk

Aggregate & Capture Data

Work Closely with Physicians

Focus on Costs

Be Responsive to Different Payment Models

Select and Comply with a Core Set of Clinical Guidelines

Hospitals will have to be able to:

© Avalere Health LLCPage 9

Identify Partners Who Can Offer Integrated Solutions

Payment and Delivery Reform

Specialty Pharmacy’s Role within ACOs will Depend Upon the Model and Structure of the ACO

Adapted from Brookings Institution and Dartmouth Institute for Health Policy and Clinical Practice. “The Accountable Care Organization (ACO) Learning Network,” October 6, 2009.

Multi-Specialty

Group

Illustrative ACO 1

Hospital

Multi-Specialty Group

Post-Acute Care Facility

Home Health

Mental Health Facility

Primary Care Group

Illustrative ACO 3

Hospital

Multi-Specialty Group

Primary Care Group

Illustrative ACO 2

Payment reforms will shift clinical and financial risk downstream to providers. Providers will need to broaden perspective of costs to account for the entire health care system when making treatment decisions.

Payment and Delivery Reform

The Specialty Pharmacy Industry Has an Opportunity to Define Their Role Within The Changing Market

Source:Adapted from Brookings Institution and Dartmouth Institute for Health Policy and Clinical Practice. “The Accountable Care Organization (ACO) Learning Network,” October 6, 2009.

Hospital

Multi-Specialty

Group

Post-Acute Care Facility

Home Health

Mental Health Facility

Primary Care Group

Future Customer Focus

Hospital

Multi-Specialty

Group

Primary Care Group

Current Customer Focus

The changing environment will force providers to focus on broader integration; Specialty Pharmacy can play a role in managing drugs throughout this continuum of care.

SP

SP

No Medicare ACOs

AK

HI

CA (23)

AZ (8)

NV (3)

OR(2)

MT(1) MN

(5)

NE(2)

SD

ND

ID(1)

WY(1)

OK(1)

KS(1)

CO (2)

UT(1)

TX (16)

NM (3)

SC (3)

FL (32)

GA (11)

AL(1)

MS (2)

LA(2)

AR(3)

MO(4)

IA (7)

VA(6)

NC (6)TN (7)

IN (9)

KY (7)

IL (8)

MI (9)

WI (7)

PA (3)

NY (18)

WV

VT (2)

ME (4)

RI-2

DE - 1

MD - 9

NJ

MANH

WA(2)

OH(8)

D.C. - 2

Both MSSP and Pioneer ACOs

MSSP ACOs

7

18

NJ -10

Source: CMS Medicare Shared Savings Program website: http://www.cms.gov/Medicare/Medicare-Fee-for-Service-Payment/sharedsavingsprogram/index.html?redirect=/sharedsavingsprogram/Note: MSSP and Pioneer ACOs often serve Medicare beneficiaries in more than one state. Since the numbers embedded in the map capture this, they do not add up to equal the number of ACO entities approved by CMS through January1, 2013.

CT-8

States with Medicare ACOs

Between the Medicare Shared Savings Program and Pioneer ACOs, CMS Has Launched More than 250 ACOs

PR

2

ACOs

Health Systems Across the Country Exhibit Characteristics of ACOs

0AK

HI

CA

AZ

NV

OR

MT

MN

NE

SD

ND

ID

WY

OK

KSCO

UT

TX

NMSC

FL

GAALMS

LA

AR

MO

IA

VA

NCTN

IN

KY

IL

MIWI

PA

NY

WV

VT

ME

RICT

DEMD

NJ

MA

NH

WA

OH

D.C.

5-7

3-4

8-10

2

1

Source: Leavitt Partners Center for ACO Intelligence, “Growth and Dispersion of Accountable Care Organizations,” November 2011.

11+

ACOs

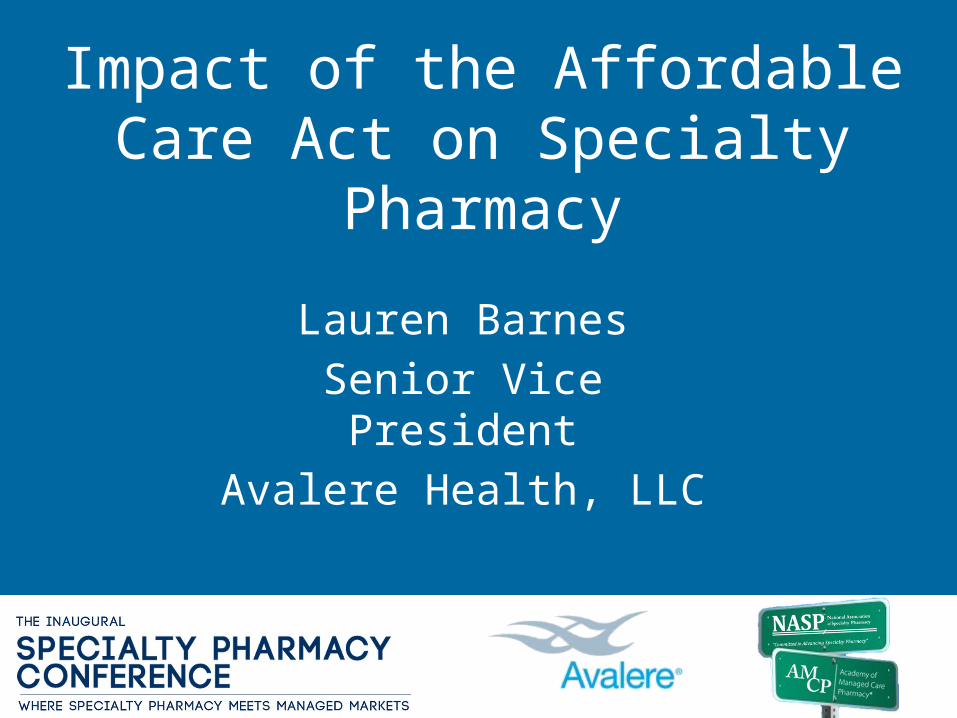

Numerous ACA Provisions in Effect, But Major Changes Start in 2014

2010 2011 2012 2013 2014 2015

MA = Medicare Advantage VBP = Value-based PurchasingHRRP = Hospital Readmissions Reduction Program FPL = Federal Poverty LevelMTM = Medicare Therapy Management CHIP = Children’s Health Insurance ProgramACO = Accountable Care Organization ACA = Affordable Care ActBPCI = Bundled Payment for Care Improvement Initiative

Exchanges and Insurance ReformsMedicareMedicaid & 340BQuality/Value ReformsFinancing Other

VBP Program Launches

Medicaid Maintenance of Effort Requirements End

Center for Medicare and Medicaid Innovation

Medicaid Drug Rebate Increase

Establish Patient-Centered Outcomes Research Institute

Drug Manufacturer Annual Fee

Independent Payment Advisory Board Recommendations Effective

Part D Coverage Gap Closing Begins

Medicaid Expansion to 133% FPL

Expands 340B Participation

Coverage Expansion of Preventive Services

Extend Dependent Coverage to 26 years

MA Payments Frozen

MA Regionally-Adjusted Benchmarks Phase-In Begins

MA Quality Payments Begin Essential Health Benefits

Package in Effect

Medicare Shared Savings Program (ACOs)

Exchanges Begin Operations

Part D MTM Requirements Begin

CHIP Reauthorization Expires

BiosimilarsAppeals and Grievances Requirements

Prevention and Public Health Fund

Medical Device Excise Tax

Health Insurer Fee

Provider Payment Reductions

Individual and Employer Insurance Mandates Take Effect in January 2014

HRRP Begins

Announcement of BPCI participants

Meaningful Use Incentive Payments Begin

Meaningful Use Penalties Begin

Panel Discussion

The intersection of businessstrategy and public policy

Data, Metrics, and Reporting: What Role will Specialty Pharmacy Play?

Brian Nightengale, RPh, PhD President

Xcenda, AmerisourceBergen Consulting Services

Every major aspect of ACA assumes broad access to credible data and sufficient stakeholder collaboration to ensure measurement and reporting

Questions Remain Regarding Impact on SP

• Complex therapeutic areas may offer the best opportunities to demonstrate quality and outcomes

• But, will these low volume, yet expensive specialty therapeutics area be a big focus out of the gate?

– If so, then SPs will likely play an increasingly collaborative role in

• Providing support for complex therapy management within the new coordinated care delivery models

• Providing the necessary data typically required for specialty focused diseases

• Will PCORI’s and other agencies priorities align with the market and/or be relevant to Specialty Pharmacy?

– Currently many initial pilot programs focus on primary care or care delivery• What impact might CER have on the drugs SPs offer to customers?

– Either increasing or limiting access– Changing contracts/rebates with manufacturers of drugs that did not perform well under

CER

Impact on Specialty Pharmacy

March 2009, Amerisource Bergen’s Managed Care Network (MCN™) primary market research

Payer reactions to the statement:“Private payers will use CER data to require enrollees to pay some or all of the additional costs of more expensive drugs, procedures, or technologies for which there is no evidence of superior effectiveness.”

N=43

How much do you agree with this statement?

March 2009 N=41 June 2008 N=68

Questions Remain Regarding Impact on SP

• Stakeholders will need to address care management and quality improvement issues related to small patient populations

– Across specialty therapeutic areas, data needs and reporting requirements differ significantly based on medical complexities

– Is there sufficient data and collaboration to effectively measure?

– Typical “population management” approaches may not apply

• What capital investments will be needed to address the increasing data and reporting demands and who will pay?

Are Credible and Reliable Data Available?

1. EMD Serono. “EMD Serono Specialty Digest, 7th Edition. Managed Care Strategies for Specialty Pharmaceuticals ” (Note: data represented in graphs was collected via an online survey of 93 health plans representing over 115 million lives).

Outcome Measures for Oncology Outcome Measures for Rheumatoid Arthritis

Impact of ACA on Specialty Pharmacy

Dean Erhardt, MBAD2 Pharma Consulting, LLC

D2 Mission Statement

D2 is a Life Sciences consulting firm consisting of accomplished industry personnel who provide hands on expertise in all aspects of channel management.

We provide strategic and tactical commercialization expertise to emerging and existing pharmaceutical,

biotech and specialty organizations focusing on the individuals client’s defined business objectives.

Brief on Healthcare Reform• The good

– In theory fewer uninsured Americans should lead to a lower-cost health care system

– No cap on benefits– No Pre-existing conditions– Kids stay on coverage through age 26– “Free” preventive healthcare

• The Bad– Wrong incentives???

• Patients’ rights advocates have expressed that the model incentivizes providers to save money by cutting corners in treatment

– Increase healthcare costs • 20 M people w/ incomes up to 400% FPL ($92K) to receive subsidies

– Decisions in the hands of unelected bureaucrats– Various cross subsidies (transferring wealth w/o using the tax code)

• Young, healthy pay more to cross subsidize older, sicker• The Ugly?

– Expands power with the IRS – multiple new taxes– 2700 pages of legislation yet to be defined– Approx. 2000 “at the description of the Secretary”

Confidential 25

Specialty Pharmacy Challenges

The other driver of change…

How the FDA pipeline of specialty drugs will impact the existing supply chain?

27Confidential 27 27

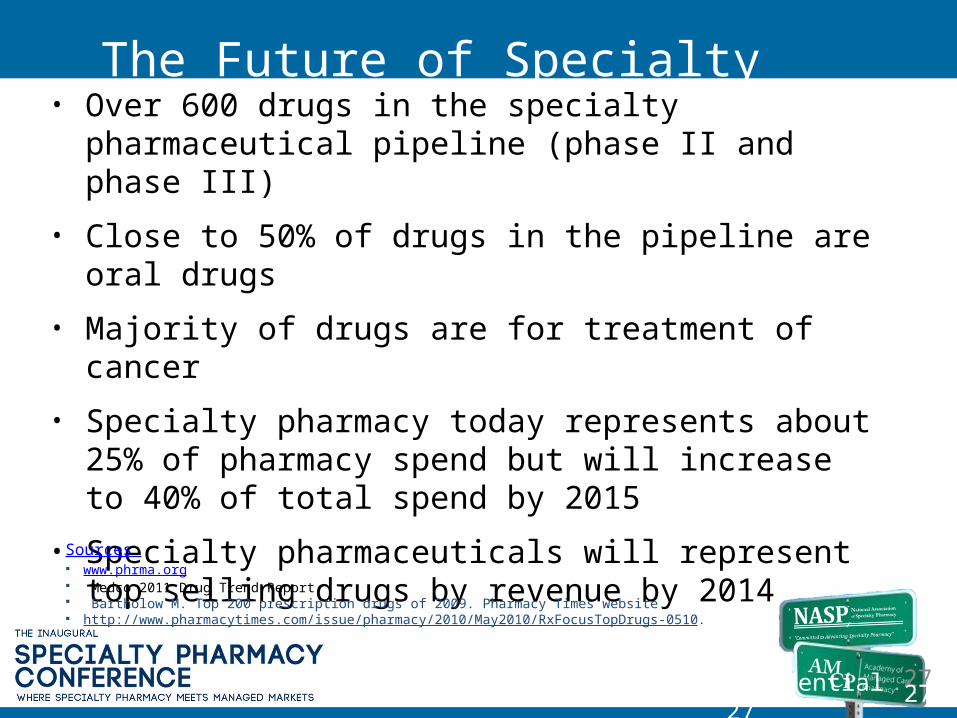

The Future of Specialty Pharmacy• Over 600 drugs in the specialty pharmaceutical pipeline

(phase II and phase III)

• Close to 50% of drugs in the pipeline are oral drugs

• Majority of drugs are for treatment of cancer

• Specialty pharmacy today represents about 25% of pharmacy spend but will increase to 40% of total spend by 2015

• Specialty pharmaceuticals will represent top selling drugs by revenue by 2014

Sources www.phrma.org Medco 2011 Drug Trend Report Bartholow M. Top 200 prescription drugs of 2009. Pharmacy Times website. http://www.pharmacytimes.com/issue/pharmacy/2010/May2010/RxFocusTopDrugs-0510.

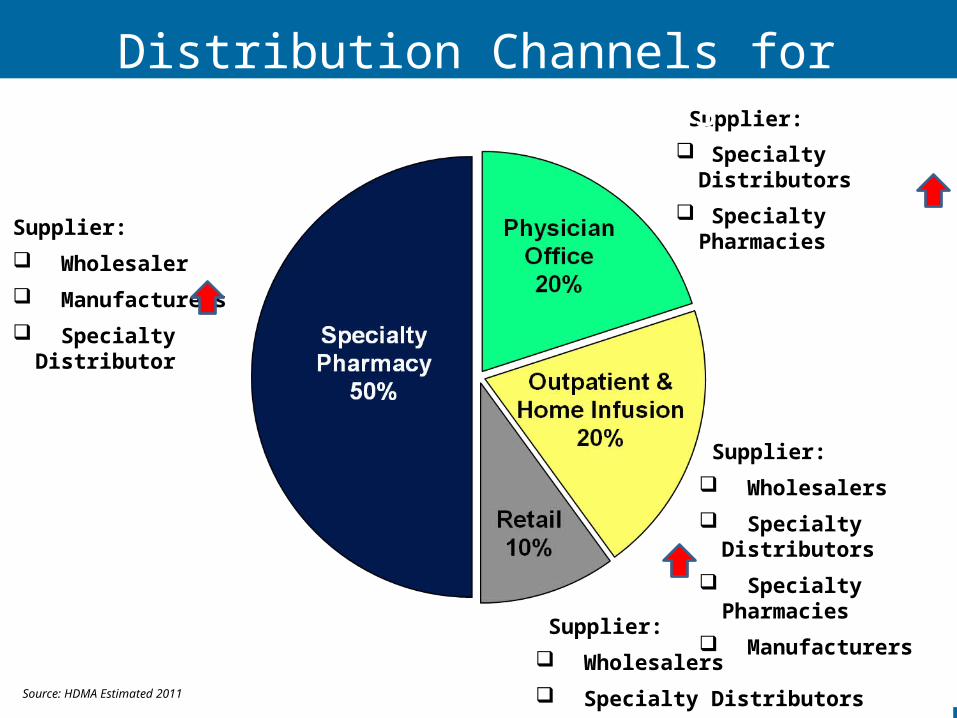

Supplier:

Wholesaler

Manufacturers

Specialty Distributor

Supplier:

Specialty Distributors

Specialty Pharmacies

Supplier:

Wholesalers

Specialty Distributors

Specialty Pharmacies

Manufacturers

Supplier:

Wholesalers

Specialty Distributors

Distribution Channels for Specialty Products

Source: HDMA Estimated 2011

Key Considerations• How does a specialty pharmacy support patient

initiatives across an ACO?• What are the data requirements necessary to support

reporting ACO initiatives?• How/where does pharma (big/small) fit?

Potential Levers in SP Management

Medical Management

• Referral mgmt• Utilization mgmt• Case management• Disease mgmt• Step therapy• Prior authorization• Retro review

Consumer Engagement

• Awareness campaign• Engagement (Health by

Choice)• Shared decision making• Benefit design• Tiered copays• Preferred networks• Education programs

(wellness)• Transparency – quality

& cost

Network Management

• Renegotiate contracts• Case rates/commodity

pricing• Risk sharing

(capitation, ACO)• Gainsharing• Incentives – reward

achievement of targets• Bundled payments• Site of service

differentials• Transparency• Direct care to Centers

of Excellence

THANK YOU…

How Will Specialty Pharmacy Evolve In A Risk-Sharing Environment?

A Pharmaceutical Industry Colleague Perspective

Jeffrey A. Bourret, MS, RPh, FASHPSenior Director, Medical Affairs

Medical Lead, Specialty & Payer Channel CustomersPfizer Specialty Care

Specialty Pharmacy Evolution• Ongoing development of core services

– Specialty therapy management– Medication adherence (Achieving vs Improving)– Cost management

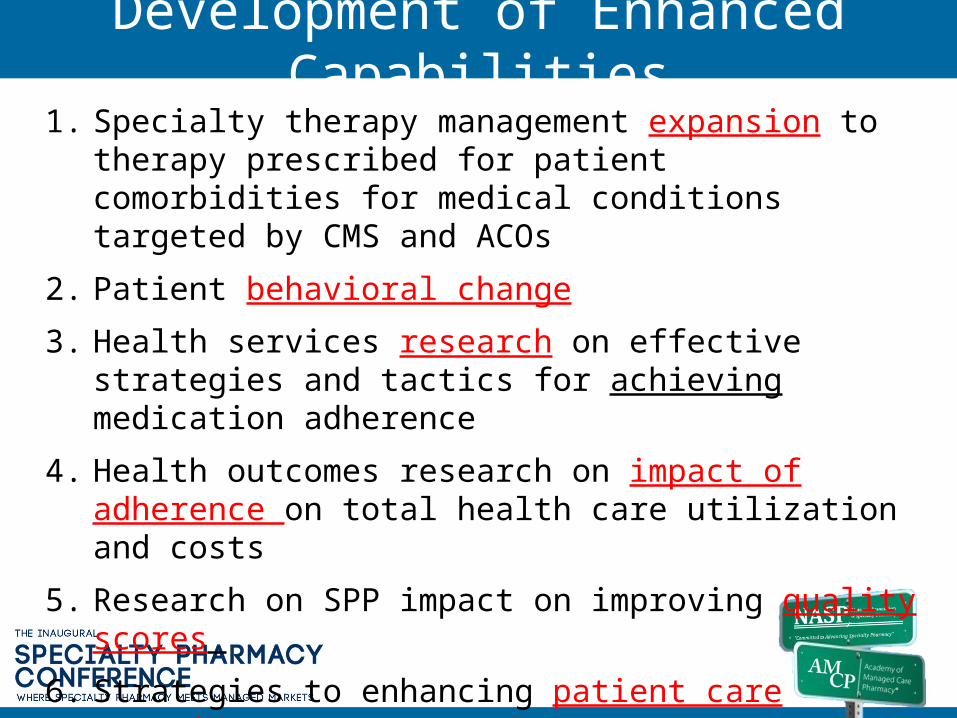

Development of Enhanced Capabilities1. Specialty therapy management expansion to therapy prescribed

for patient comorbidities for medical conditions targeted by CMS and ACOs

2. Patient behavioral change

3. Health services research on effective strategies and tactics for achieving medication adherence

4. Health outcomes research on impact of adherence on total health care utilization and costs

5. Research on SPP impact on improving quality scores

6. Strategies to enhancing patient care experience

Specialty Pharmacy Evolution: Patient Support

• Specialty Therapy Management– Patient education

– Telephonic adherence support

• Evolution– Expanded role in patient , family and caregiver education

– Certification of patients on appropriate use of medication

– Data capture & integration with medical/pharmacy

– Generation of data on patient outcomes

Medicare Shared Savings Program Final Rule

• Quality measures and reporting– CMS will score 23 quality measures in

calculating the performance standard, spanning four equally weighted domains:

• Patient/caregiver experience (7 measures)• Care coordination/patient safety (6 measures)• Preventive health (8 measures)• At-risk populations (12 measures)

• Specialty pharmacy can potentially impact each core domain & could be called on to play more active role

Finalized Measures Will Target High Impact Conditions

• Diabetes• Heart failure • Coronary artery disease• Ischemic vascular disease• Hypertension• COPD• Tobacco use

• Patient experience• Immunizations• Readmissions• Medication reconciliation• Use of EHRs• Screenings (cancer,

depression, fall risk, weight)

Most high impact conditions targeted by ACOs areco-morbidities for patients with medical conditions

requiring specialty therapy

Comparative Effectiveness Research

Drug Surgery

Device Surgery

Drug Device

Drug A Drug B

An Option Ripe for Specialty Pharmacy Evolution

• Patient education incentives• Medication use certification• Family & caregiver education• Patient self-reported assessments

of disease activity• Patient satisfaction survey• Health outcomes research

Drug (Limited Support) Drug + Enhanced Support

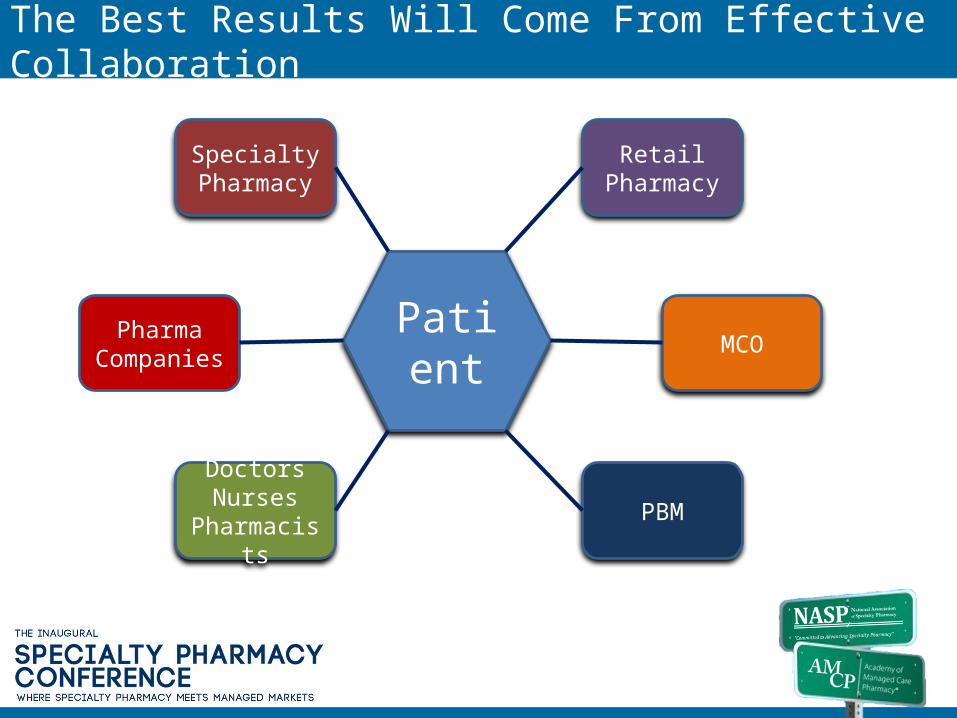

The Best Results Will Come From Effective Collaboration

Patient

DoctorsNurses

Pharmacists

PharmaCompanies

PBM

MCO

Retail Pharmacy

Specialty Pharmacy

Impact of ACA on Specialty Pharmacy

Presented by: Donald C. Balfour, M.D.President and Medical Director

Sharp Rees-Stealy Medical GroupApril 3, 2013

Sharp ACO Collaborations

• Commercial PPO Patients

• Sharp Community Medical Group (“SCMG”)

• Commercial PPO Patients

• SCMG and Sharp Rees-Stealy Medical Group (“SRSMG”)

• Pioneer ACO• Medicare Fee-

for-Service Beneficiaries

• Sharp HealthCare, SCMG, SRSMG

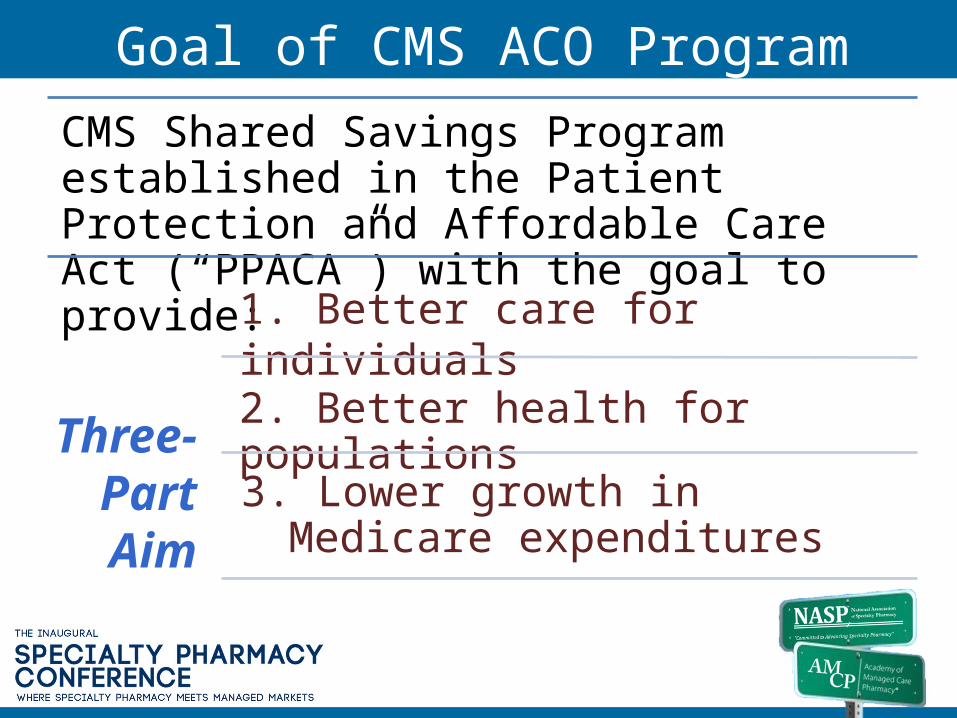

Goal of CMS ACO Program

CMS Shared Savings Program established in the Patient Protection and Affordable Care Act (“PPACA”) with the goal to provide:

1. Better care for individuals

2. Better health for populations

3. Lower growth in Medicare expenditures

Three-Part Aim

Pioneer ACO Footprint

• Began January 1, 2012• Collaboration between Sharp

HealthCare, SCMG and SRSMG– All SRSMG physicians, most SCMG

physicians (includes Graybill), and all Sharp hospitals

• 32,000 aligned beneficiaries– 74% with SCMG– 26% with SRSMG

Sharp HealthCare ACO

What Have We Accomplished?• Created

corporation• Named

leadership team• Developed

subcommittee structure

• Established provider and supplier network• Formed governing body, including consumer advocate

and patient representative

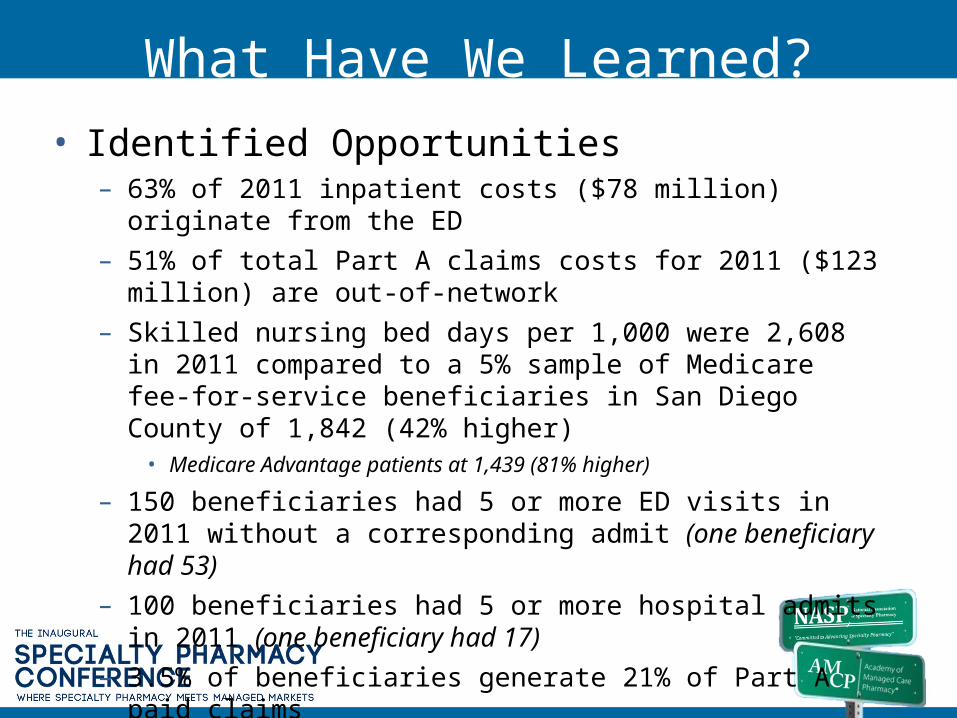

What Have We Learned?• Identified Opportunities

– 63% of 2011 inpatient costs ($78 million) originate from the ED– 51% of total Part A claims costs for 2011 ($123 million) are out-of-

network – Skilled nursing bed days per 1,000 were 2,608 in 2011 compared to a

5% sample of Medicare fee-for-service beneficiaries in San Diego County of 1,842 (42% higher)

• Medicare Advantage patients at 1,439 (81% higher)

– 150 beneficiaries had 5 or more ED visits in 2011 without a corresponding admit (one beneficiary had 53)

– 100 beneficiaries had 5 or more hospital admits in 2011 (one beneficiary had 17)

– 3.5% of beneficiaries generate 21% of Part A paid claims

Aim and Primary Drivers

Best Health, Best Care, Best Experience

Care Delivery Models

Care Coordination

Patient Engagement

Information Technology and Analytics

…………………………………………………………………………

…..

…………………………………………………………………………

…..

Alignment of Incentives

Years One and Two• Providers bill normally and receive standard fee-

for-service paymentsBilling

• Total cost of care for ACO beneficiaries is compared to a benchmark based on historical costs of the aligned population

Comparison

• If total expenses are less than target, and if quality metrics are achieved, a portion of the savings is returned to the ACO

Bonus

• The ACO is responsible for dividing the savings among ACO participantsDistribution

Year Three

• Must achieve quality targets as well as a minimum 2% annual savings in years one and two to receive population-based payments in year three

Payment Option

CMMI’s AIM is that 100% of Pioneer ACOs generate sufficient cost savings and quality

improvements to qualify for population-based payments in year three

Best Health,Best Care,

Best Experience

Don’t Miss Out on NASP’sFall Conference!