Business presentation

August 2018

Our business

2

Harnessing synergy within businesses

Retail Broking

Distribution

Retail Business

Institutional Broking

Corporate Finance

Institutional Business

Wealth

Management

ICICI Securities: Natural beneficiary of

transforming savings environment

3

2nd largest non - bank mutual fund distributor#

Largest equity broker in India*

powered by ICICIdirect

Garnering scale in wealth management business

Strong online presence aided by pan India distribution

Leading investment bank in equity capital market

* By brokerage revenue and active customers in equities on

the NSE since FY14 - FY17 (Source: CRISIL Report)

# Source: AMFI, period: FY18

Equity Capital Market (ECM): IPO/FPO/InvIT, QIP/IPP, Rights

issue, Offer for sale)

Agenda

Company overview & strategy

Economic outlook & industry overview

Financial performance

4

Agenda

Company overview & strategy

Economic outlook & industry overview

Financial performance

5

Include investment in shares and debentures of credit / non-

credit societies and investment in mutual funds (other than

Specified Undertaking of the UTI) (Source: RBI, MOSPI)

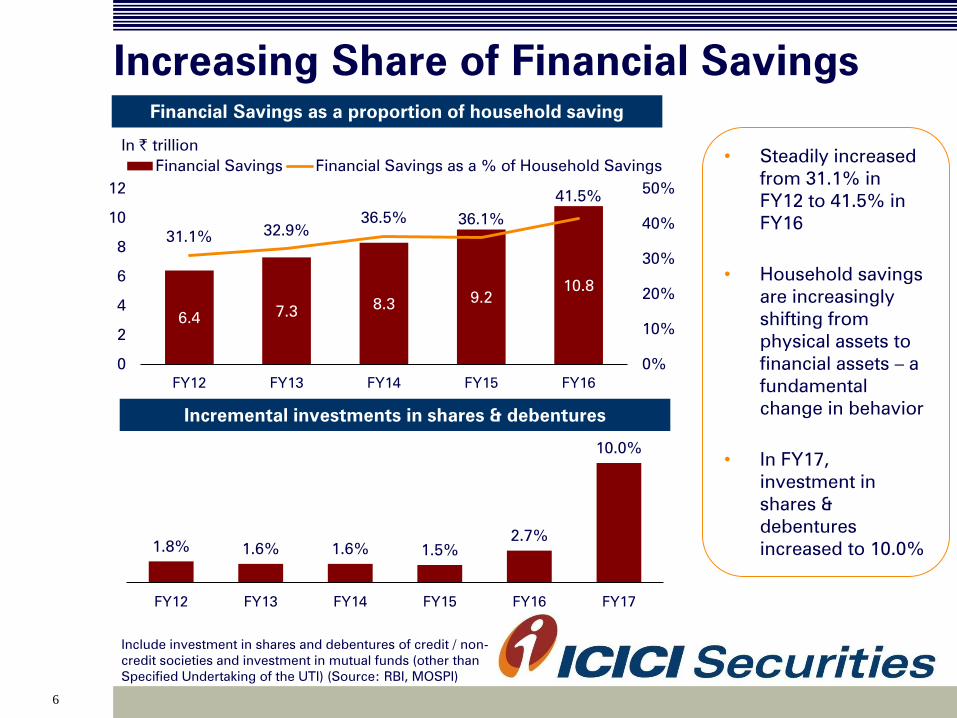

Increasing Share of Financial Savings

6.47.3

8.39.2

10.8

31.1%32.9%

36.5% 36.1%

41.5%

0%

10%

20%

30%

40%

50%

0

2

4

6

8

10

12

FY12 FY13 FY14 FY15 FY16

Financial Savings Financial Savings as a % of Household Savings

1.8% 1.6% 1.6% 1.5%

2.7%

10.0%

FY12 FY13 FY14 FY15 FY16 FY17

In ` trillion

6

• Steadily increased

from 31.1% in

FY12 to 41.5% in

FY16

• Household savings

are increasingly

shifting from

physical assets to

financial assets – a

fundamental

change in behavior

• In FY17,

investment in

shares &

debentures

increased to 10.0%

Financial Savings as a proportion of household saving

Incremental investments in shares & debentures

7

Financial sector being the key beneficiary

ADTO: Average daily turnover

Source: RBI, IRDA, AMFI, NSE, BSE, EIU

Indexed to

100 in FY14

100 100 100

165

131

95

149 149

116

200 213

146

348

259

162

Equity + Derivative

(ADTO)

MF AUM Insurance Premium (FY)

FY14 FY15 FY16 FY17 FY18

• Improved economic

conditions and

changing savings

pattern resulting in

to growth across

various asset classes

• India has high-

savings economy,

with household

savings as a

proportion of GDP at

19%

Growth Across Financial Asset Classes

Household saving as % of GDP 2016

1% 1%

4%

6%

9%

19%

24%

9%

South

Africa

Russia Japan Brazil USA India China World

Digital infrastructure set to expand

exponentially

8

Population

Approx. 1.3bn(1)

Mobile Users

Approx. 1.2bn(2)

Internet Users

Approx. 432

million(2)

Mobile Data Subscribers

Approx. 408 million(3)

(34% of total mobile

users - increasing to 66%

by FY22)

Smartphone

Penetration

at 30%(4)

(increasing

to 66% by FY22)

Source: CRISIL Report

(1) Population in 2016 (Source: EIU); (2) Source: CRISIL

Report; (3) Calculated as total mobile users (Approx.1.2bn) *

Share of mobile data subscribers as a proportion of overall

mobile users in FY17 (34%) (Source: TRAI and CRISIL

Report); (4) In FY17 (Source: CRISIL Report)

Supportive structural

reforms leading to

positive change in

consumer behaviour

• Demonetization

• Aadhar

• Financial inclusion

• Goods & Services Tax

• Direct Benefit

Transfer

99

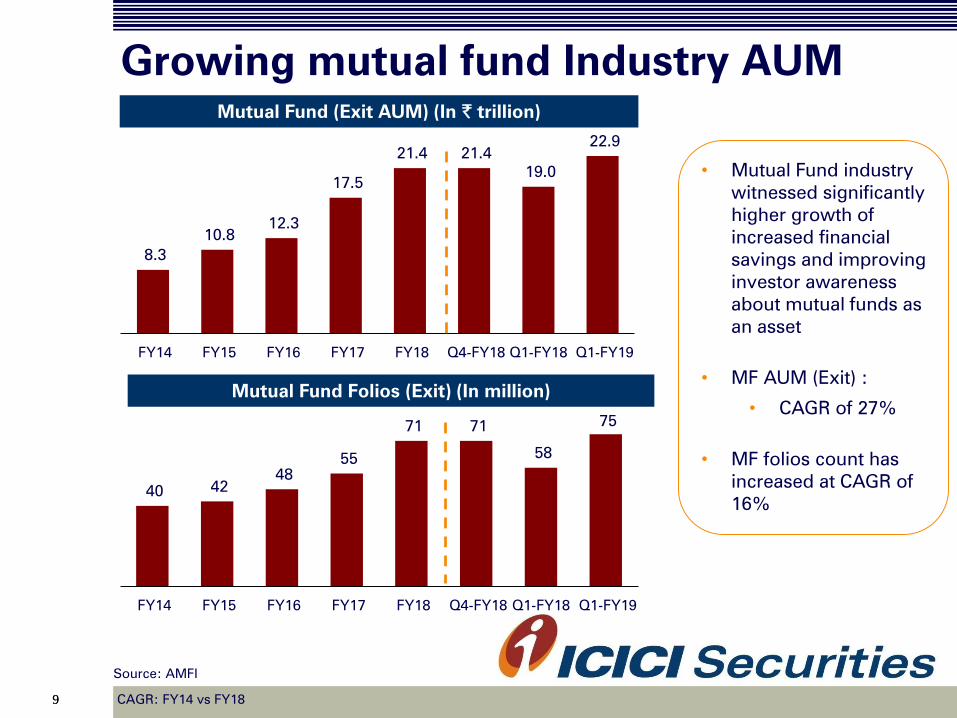

Growing mutual fund Industry AUM

8.3

10.8

12.3

17.5

21.4 21.4

19.0

22.9

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

Source: AMFI

• Mutual Fund industry

witnessed significantly

higher growth of

increased financial

savings and improving

investor awareness

about mutual funds as

an asset

• MF AUM (Exit) :

• CAGR of 27%

• MF folios count has

increased at CAGR of

16%

40 42

48

55

71 71

58

75

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

Mutual Fund (Exit AUM) (In ` trillion)

Mutual Fund Folios (Exit) (In million)

CAGR: FY14 vs FY18

10

Increase in primary market issuances

337

643 579 536

1,899

475 416

124

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

113

97

74

87

157

41

2718

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

• ECM issuance

increased at CAGR of

54%

• No. of ECM issuance

increased at a CAGR

of 9%

• IPO/FPO/InvIT

pipeline of over ` 700

#bn (SEBI filling)

• Over 60 issues

• Divestment target of

` 800 bn for FY2019

ECM Issuance mobilized (` in billion)

ECM Issuance

ECM : Includes IPO/FPO/InvIT, QIP/IPP, Rights Issue, Offer

for Sale, Source: Prime database

# Source SEBI: SEBI approval received & awaited (as on 28th

Aug 2018)

CAGR: FY14 vs FY18

Agenda

Company overview & strategy

Economic outlook & industry overview

Financial performance

11

1212

Leading equity broker in India

501595 560

618

798 798

654

814

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

2.5 2.8

3.2 3.6

4.0 4.0 3.7

4.1

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

44 65 101

187

372 447

297

466

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

ADTO in ` bn

4.7% 6.6% 7.8% 9.0%4.5%

ADTO : Turnover on NSE and BSE excluding proprietary

Market share : The ratio of our ADTO to the sum of the ADTO

on NSE and BSE excluding proprietary turnover

9.2%

Active clients on NSE (In thousand)

Operational accounts (In million)

Volume and market share (%)

• Maintained leadership in

terms of active clients

• CAGR of 12% in active

clients on NSE

• 4.1 million strong base of

operational accounts

• 4.6 Lacs new client

acquisition in FY18

• 9.0% market share (FY18)

• CAGR ADTO grew at

71% compared to

market 44%

8.8%8.7%

CAGR: FY14 vs FY18

1313

ICICIdirect : 3-in-1 Proprietary electronic brokerage platform

Retail focused technology platform

Research

• Coverage of ~ 240

Indian stocks across

sectors

• 40+ member team

• Comprehensive

portfolio management

tools

• Robust real-time risk

management

• Over 95% broking

transaction performed

online

• Over 28% equity

transactions through

mobile devices on NSE

• Highest ever brokerage

revenue of over ` 9 bn in

FY18

• Revenue growth of

31% in FY18 over

FY17

• CAGR of 19%

• ~ 90% contribution in

overall broking revenue in

FY18

4,621

7,027

6,070

7,016

9,174

2,498 2,044 2,024

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

Retail Brokerage (In ` million)

CNBC TV18 & UTI Financial Advisor Awards 2017-18

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

CAGR: FY14 vs FY18

1414

Growing scale of institutional broking

Servicing large cross-section of institutional clients

• Leading procurement

in IPOs, QIPs, OFSs

and Block deal

• Direct market access

(DMA) capabilities

Research

• Coverage of 240+

Indian stocks across

sectors

• Macro and thematic

coverage

• ~40 member team

• Conducted

international investor

conference in USA,

Asia Pacific

• Deep rooted

relationships with

global fund managers

• Revenue growth of 44% in

FY18 over FY17

• CAGR of 33%

• Dedicated sales teams

across India, Asia Pacific

and the United States

339

527 537

740

1,069

256 224

274

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

Institutional Brokerage (In ` million)

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

CAGR: FY14 vs FY18

1515

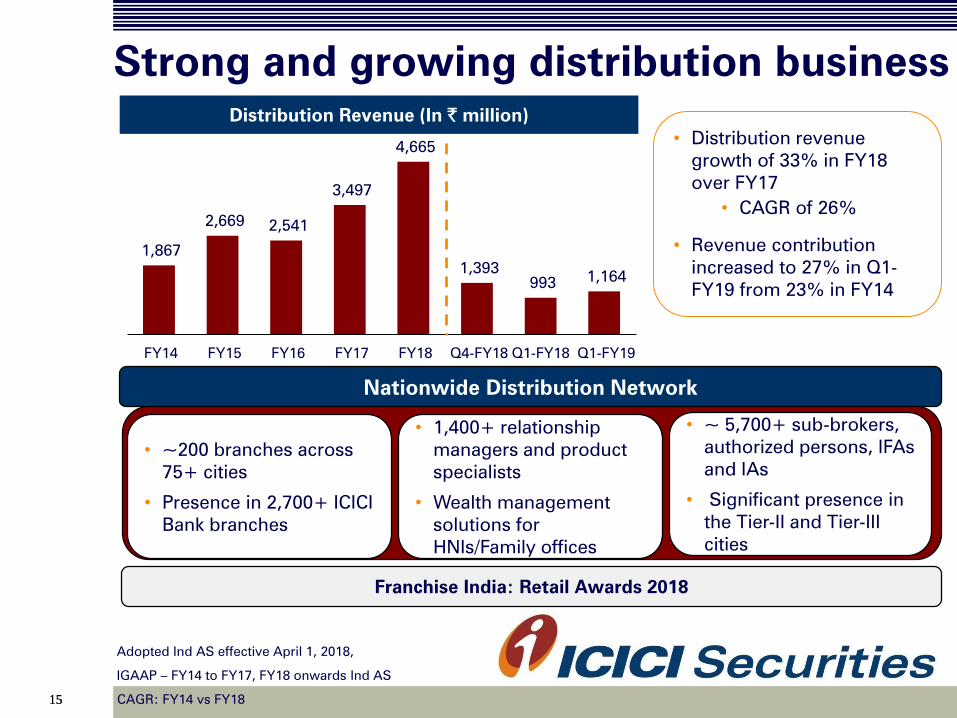

Nationwide Distribution Network

• ~200 branches across

75+ cities

• Presence in 2,700+ ICICI

Bank branches

• ~ 5,700+ sub-brokers,

authorized persons, IFAs

and IAs

• Significant presence in

the Tier-II and Tier-III

cities

• 1,400+ relationship

managers and product

specialists

• Wealth management

solutions for

HNIs/Family offices

Strong and growing distribution business

1,867

2,669 2,541

3,497

4,665

1,393

993 1,164

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

• Distribution revenue

growth of 33% in FY18

over FY17

• CAGR of 26%

• Revenue contribution

increased to 27% in Q1-

FY19 from 23% in FY14

Distribution Revenue (In ` million)

Franchise India: Retail Awards 2018

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

CAGR: FY14 vs FY18

1616

Leading non-bank MF distributor

76 120

160

212

305 339

266

348

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

789

1,540

1,117

1,657

2,847

857 606

773

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

Mutual Fund revenue (In ` million)

Mutual Fund Average AUM (In ` billion)

Mutual Fund SIP count# (In million)

• CAGR growth of 38% in

MF revenues

• Revenue contribution

increased to 18% in

Q1-FY19 from 10% in

FY14

• CAGR growth of 42% in

MF average AUM

• 26% growth in

Market MF average

AUM

• CAGR growth of 44% in

SIP count

• “Open-source” distribution

model

• Distribute 2,300+

mutual funds

# Trailing 12 months triggered SIP

0.24 0.32

0.44

0.60

1.03 1.0

0.7

1.1

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

CAGR: FY14 vs FY18

1717

Diverse third party product bouquet

• Premium growth

• CAGR of 22%

• ~ 3% contribution in

overall revenue in FY18

• Life and general insurance products

• Participation in IPOs, OFS, public bond offerings

• 3rd

party corporate fixed deposits

• Portfolio management services / Alternate investment funds

• Loan products from ICICI Bank

• Amongst the first to distribute National Pension System policies online

4,129

5,625

6,816

8,390

9,038

3,233

1,532 1,619

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

Multiple 3rd

party products supporting “one-stop shop” proposition

Life Insurance Premium (In ` million)

CAGR: FY14 vs FY18

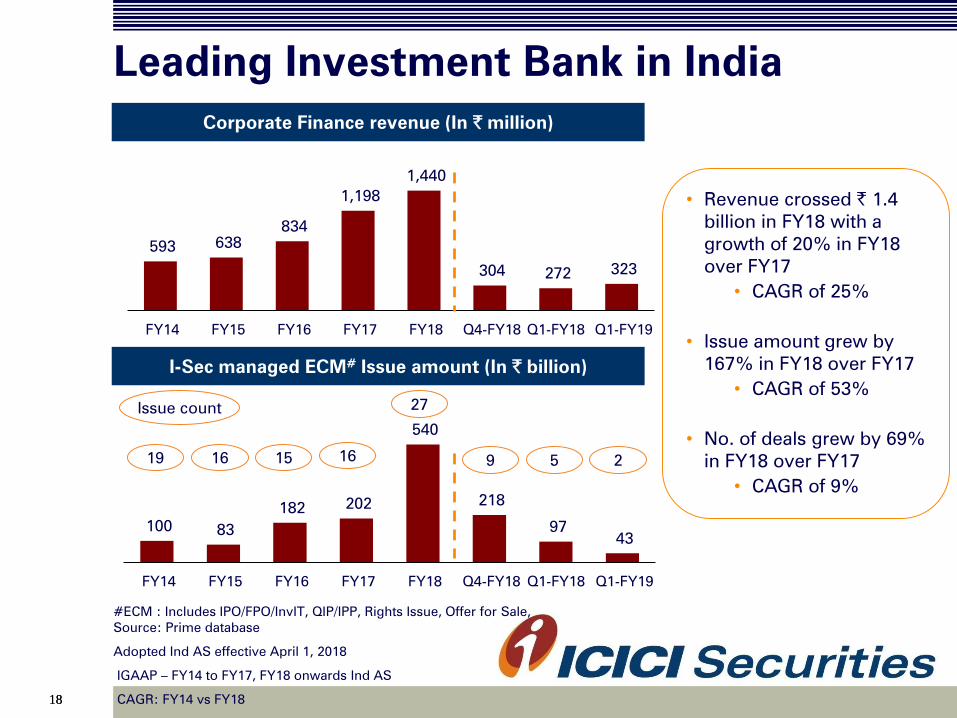

1818

• Revenue crossed ` 1.4

billion in FY18 with a

growth of 20% in FY18

over FY17

• CAGR of 25%

• Issue amount grew by

167% in FY18 over FY17

• CAGR of 53%

• No. of deals grew by 69%

in FY18 over FY17

• CAGR of 9%

593 638

834

1,198

1,440

304 272 323

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

Leading Investment Bank in India

100 83

182 202

540

218

97

43

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

16 15 16

27

19

Issue count

Corporate Finance revenue (In ` million)

I-Sec managed ECM#

Issue amount (In ` billion)

#ECM : Includes IPO/FPO/InvIT, QIP/IPP, Rights Issue, Offer for Sale,

Source: Prime database

Adopted Ind AS effective April 1, 2018

IGAAP – FY14 to FY17, FY18 onwards Ind AS

9 5 2

CAGR: FY14 vs FY18

1919

IPO/FPO/InvIT

Sbi Life

Insurance

ICICI Lombard

General

Insurance

IRB InvIT Fund

Au Small

Finance Bank

Housing &

Urban

Development

Aster DM

Healthcare

Galaxy

Surfactants

Security &

Intelligence

Services

Sandhar

Technologies

Matrimony.Com

Newgen

Software

Technologies

` 83.9 bn

` 50.3 bn

` 19.1 bn

` 9.8 bn

` 7.8 bn

` 5.0 bn` 57.0 bn

` 12.1 bn

` 9.4 bn` 5.1 bn

` 4.2 bn

Recent marquee deal

INDINFRAVIT

Trust` 31.5 bn

2020

Srikalahasthi

Pipes

Ramkrishna

Forgings

Satin Creditcare

Network

` 2.5 bn

` 2.0 bn

` 1.5 bn

NMDC Ltd

` 12.3 bn

NLC India Ltd

` 7.2 bn

Hindustan

Copper Ltd.` 4.1 bn

National

Aluminium Co` 12.0 bn

Offer for Sale

Recent marquee deal

QIP/IPP

Union Bank Of

India

Edelweiss

Financial

Services

Jindal Steel &

Power

Mahindra &

Mahindra

Financial

Quess Corp

ITD Cementation

` 20.0 bn

` 15.3 bn

` 12.0 bn

` 10.6 bn

` 8.7 bn

` 3.4 bn

ICICI Prudential

Life Insurance` 11.4 bn

2121

VRL Logistics

Ltd` 0.4 bn

Sobha ltd

` 0.6 bn

Marathon

Nextgen Realty

Ltd` 1.5 bn

SKF India Ltd.

` 3.9 bn

Buyback

Tata Steel

` 127 bn

Mahindra

Lifespace

Developers ` 3.0 bn

Rights Issue

Deewan

Housing Finance` 109 bn

SQS India BFSI

Ltd.` 1.3 bn

NCD’s Open Offer

Advisory

Actis PE (Pine

Labs)` 5.3 bn

Small Business

Fincredit India ` 12.9bn

Larsen & Tourbo

Ltd` 5.2 bn

Fairfax Financial

Holdings Ltd.` 24.7 bn

IDBI Bank Ltd.

Advisory

Federal Bank

` 4.0 bn

KIMS Hospitals

Recent marquee deal

Key strategy

22

Continue investing in technology and innovation

Strengthen our leadership position in the brokerage

business

Strategically expand our financial product distribution

business through cross-selling

Leverage our leadership in equity capital markets to

strengthen our financial advisory businesses

Diversify our revenue streams and continue reducing

revenue volatility

Agenda

Company overview & strategy

Economic outlook & industry overview

Financial performance

23

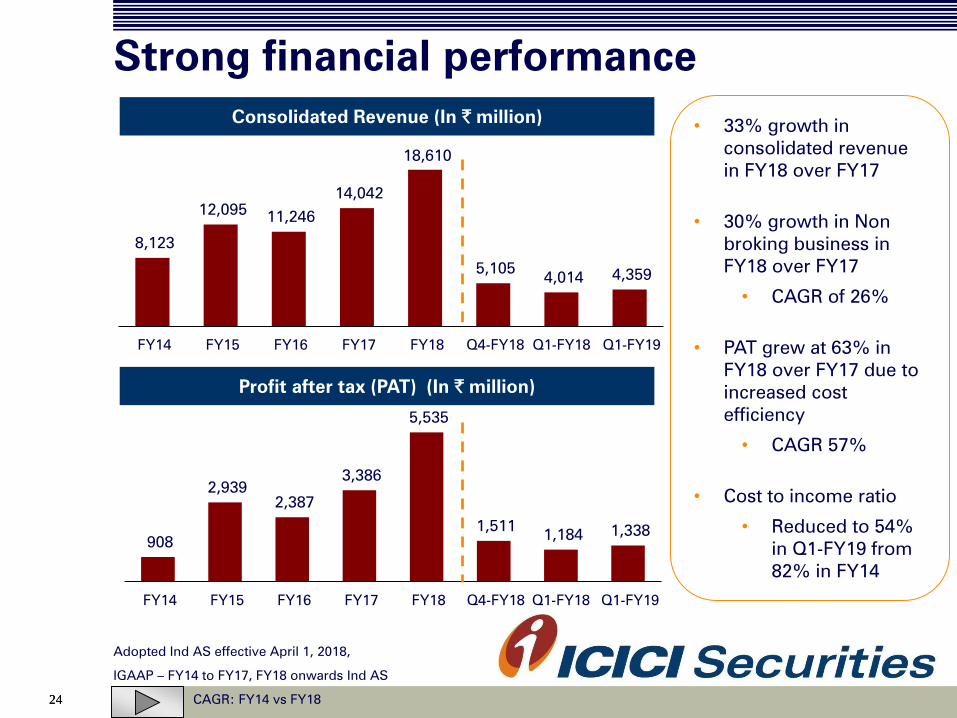

2424

Strong financial performance

8,123

12,095 11,246

14,042

18,610

5,105 4,014 4,359

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

908

2,939

2,387

3,386

5,535

1,511 1,184

1,338

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

• 33% growth in

consolidated revenue

in FY18 over FY17

• 30% growth in Non

broking business in

FY18 over FY17

• CAGR of 26%

• PAT grew at 63% in

FY18 over FY17 due to

increased cost

efficiency

• CAGR 57%

• Cost to income ratio

• Reduced to 54%

in Q1-FY19 from

82% in FY14

Consolidated Revenue (In ` million)

Profit after tax (PAT) (In ` million)

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

CAGR: FY14 vs FY18

2525

Consistent dividend payout

400

1,611 1,611

2,050

3,028

FY14 FY15 FY16 FY17 FY18

• Highest dividend

payout in FY18

• Consistent high

return on equity

due to asset light

model

38%

100%

65%

77%82% 80%*

90%*

59%*

FY14 FY15 FY16 FY17 FY18 Q4-FY18 Q1-FY18 Q1-FY19

55% 67% 61%47% 55%

Dividend payout ratio

Equity dividend : FY18 includes interim dividend and proposed final dividend

Dividend payout (%) = Dividend on equity shares / (profit after tax – (dividend on preference shares + dividend distribution tax on

preference shares)

Return on equity = PAT : Average networth excluding Other Comprehensive Income and Translation reserve

* Annualised

Equity Dividend ` million

Return on equity

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

Safe harbor

26

Except for the historical information contained herein, statements in this release which contain words

or phrases such as 'will', ‘would’, ‘indicating’, ‘expected to’, etc., and similar expressions or variations

of such expressions may constitute 'forward-looking statements'. These forward-looking statements

involve a number of risks, uncertainties and other factors that could cause actual results,

opportunities and growth potential to differ materially from those suggested by the forward-looking

statements. These risks and uncertainties include, but are not limited to, the actual growth in demand

for broking and other financial products and services in the countries that we operate or where a

material number of our customers reside, our ability to successfully implement our strategy, including

our use of the Internet and other technology, our growth and expansion in domestic and overseas

markets, technological changes, our ability to market new products, the outcome of any legal, tax or

regulatory proceedings in India and in other jurisdictions we are or become a party to, the future

impact of new accounting standards, our ability to implement our dividend policy, the impact of

changes in broking regulations and other regulatory changes in India and other jurisdictions as well

as other risk detailed in the reports filed by ICICI Bank Limited, our holding company with United

States Securities and Exchange Commission. ICICI Bank and ICICI Securities Limited undertake no

obligation to update forward-looking statements to reflect events or circumstances after the date

thereof.

This release does not constitute an offer of securities.

2727

Thank you

Safe harbor

28

This appendix is intended to provide information on the key impacts of transition to Ind AS on the

Company’s reported equity and reported profit. The information presented in this communication

includes key accounting differences between Indian GAAP and Ind AS that are relevant for the

Company in qualitative and quantitative terms. Ind AS financial statements incorporated in the

presentation as well as explained in the Appendix are based on the principles/interpretations and

regulations known to date and may be affected by changes to Ind AS or the interpretation thereof

published/notified hereafter. The Appendix is for use of readers of the financial information of the

Company and is not intended to serve as a guide on Ind AS and/or an exhaustive statement of Ind AS

transition aspects.

2929

Appendix : A

3030

Particulars FY2014 FY2015 FY2016 FY2017 FY2018 Q1-FY19

Revenue 8,123 12,095 11,246 14,042 18,610 4,359

Expenses

Employee benefits

expenses3,274 3,921 4,013 4,847 5,504 1,366

Operating expenses 1,057 1,045 1,105 1,288 1,677 252

Finance costs 247 311 258 289 495 131

Other expenses 2,123 2,321 2,219 2,398 2,410 584

Total Expenses 6,701 7,598 7,505 8,822 10,086 2,333

Profit before tax 1,422 4,497 3,741 5,220 8,524 2,026

Tax expense 514 1,558 1,354 1,834 2,989 688

Profit after tax 908 2,939 2,387 3,386 5,535 1,338

OCI - - - - (16) (16)

Total comprehensive

income (TCI)- - - - 5,519 1,322

Consolidated P&L(` million)

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

3131

Particulars Q1-FY19 Q1-FY18 Y-o-Y%

Revenue 4,359 4,014 9%

Expenses

Employee benefits expenses 1,366 1,310 4%

Operating expenses 252 327 (23)%

Finance costs 131 101 30%

Other expenses 584 477 22%

Total Expenses 2,333 2,215 5%

Profit before tax 2,026 1,799 13%

Tax expense 688 615 12%

Profit after tax 1,338 1,184 13%

Other comprehensive income (OCI) (16) (27) (41)%

Total comprehensive income (TCI) 1,322 1,157 14%

Consolidated P&L: Quarterly

(` million)

# amount less then ` 1 million

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

Q4-FY18

5,105

1,325

574

141

694

2,734

2,371

860

1,511

#

1,511

3232

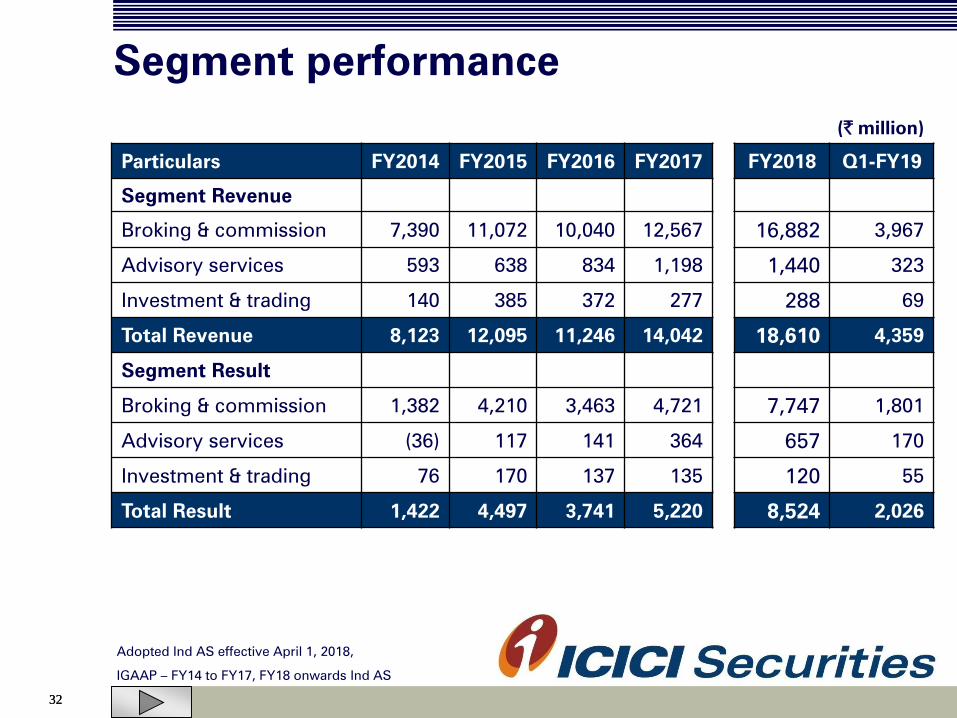

Segment performance

(` million)

Particulars FY2014 FY2015 FY2016 FY2017 FY2018 Q1-FY19

Segment Revenue

Broking & commission 7,390 11,072 10,040 12,567 16,882 3,967

Advisory services 593 638 834 1,198 1,440 323

Investment & trading 140 385 372 277 288 69

Total Revenue 8,123 12,095 11,246 14,042 18,610 4,359

Segment Result

Broking & commission 1,382 4,210 3,463 4,721 7,747 1,801

Advisory services (36) 117 141 364 657 170

Investment & trading 76 170 137 135 120 55

Total Result 1,422 4,497 3,741 5,220 8,524 2,026

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

3333

Segment performance: Quarterly

(` million)

Particulars Q1-FY19 Q1-FY18 Y-o-Y%

Segment Revenue

Broking & commission 3,967 3,659 8%

Advisory services 323 272 19%

Investment & trading 69 83 (17)%

Total Revenue 4,359 4,014 9%

Segment Result

Broking & commission 1,801 1,671 8%

Advisory services 170 88 93%

Investment & trading 55 40 38%

Total Result 2,026 1,799 13%

Adopted Ind AS effective April 1, 2018,

IGAAP – FY14 to FY17, FY18 onwards Ind AS

Q4-FY18

4,717

304

84

5,105

2,187

131

53

2,371

3434

Consolidated balance sheet (` million)

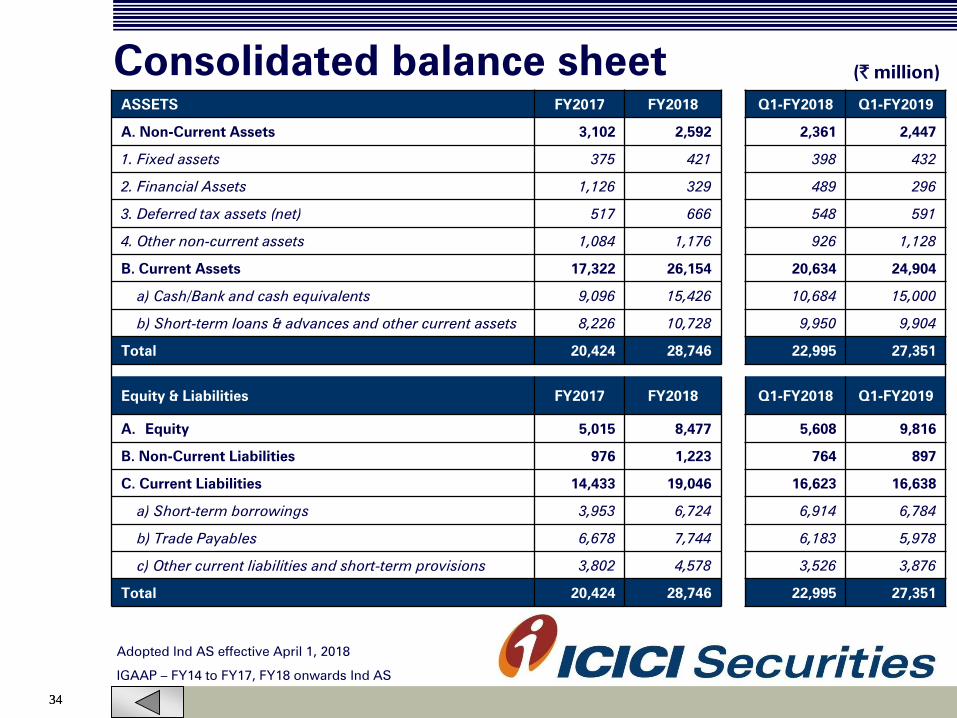

ASSETS FY2017 FY2018 Q1-FY2018 Q1-FY2019

A. Non-Current Assets 3,102 2,592 2,361 2,447

1. Fixed assets 375 421 398 432

2. Financial Assets 1,126 329 489 296

3. Deferred tax assets (net) 517 666 548 591

4. Other non-current assets 1,084 1,176 926 1,128

B. Current Assets 17,322 26,154 20,634 24,904

a) Cash/Bank and cash equivalents 9,096 15,426 10,684 15,000

b) Short-term loans & advances and other current assets 8,226 10,728 9,950 9,904

Total 20,424 28,746 22,995 27,351

Equity & Liabilities FY2017 FY2018 Q1-FY2018 Q1-FY2019

A. Equity 5,015 8,477 5,608 9,816

B. Non-Current Liabilities 976 1,223 764 897

C. Current Liabilities 14,433 19,046 16,623 16,638

a) Short-term borrowings 3,953 6,724 6,914 6,784

b) Trade Payables 6,678 7,744 6,183 5,978

c) Other current liabilities and short-term provisions 3,802 4,578 3,526 3,876

Total 20,424 28,746 22,995 27,351

Adopted Ind AS effective April 1, 2018

IGAAP – FY14 to FY17, FY18 onwards Ind AS

3535

Appendix : B

Impact on Profit and Loss account

36

(` million)

Impact on profit and loss accountPeriod ending

June, 2017

Year ending

March, 2018

Net profit as per Indian GAAP 1,147 5,577

Adjustments under Ind AS

A. Deferment of revenue 1 (10)

B. Allowances for expected credit losses (7) 6

B. CP borrowing cost adjustment 1 -

B. Fair valuation of securities 27 2

B. Valuation of Security Deposits (1) (4)

C. Accounting for compensation costs 26 (50)

D. Deferred tax on adjustments (22) (18)

E. Lease rent adjustment 12 32

Net profit as per Ind AS 1,184 5,535

Impact on Networth

37

(` million)

Impact on Net worthAs at April

1, 2017

As at March

31, 2018

Networth as per Indian GAAP 4,896 8,342

Adjustments under Ind AS

B. CP borrowing cost adjustment 1 1

B. Deferment of revenue (5) (16)

B. ECL on Trade receivables (10) (5)

B. Fair valuation of securities 28 30

B. Lease rent adjustment 173 206

B. Valuation of Security Deposits (7) (11)

E. Deferred tax on adjustments (61) (70)

Net worth as per Ind AS 5,015 8,477