The G3 and BRICs Quarterly forecasts A report from the Economist Intelligence Unit

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The G3 and BRICsQuarterly forecastsA report from the Economist Intelligence Unit

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20101

Summary

l The Economist Intelligence Unit forecasts that growth in the BRICs (Brazil, Russia, India, China) will continue to outpace that of the biggest economies in the developed world in the coming quarters. However, the outlook for the G3 (US, Japan, Germany) suggests that a double-dip recession is now a diminishing risk.

l The G3 is expected to avoid outright deflation as exceptionally loose monetary policy offsets downward pressure on prices from deleveraging and sluggish labour markets. The BRICs will experience higher inflation, as capacity constraints emerge in some sectors. In addition, the BRICs are more exposed to increased raw material costs, which have a higher weighting in their consumer price indices. The combination of free money in the West and stronger growth in the BRICs will attract capital inflows into emerging markets and create the risk of asset price bubbles.

l We expect money market rates in the BRICS to tick up gradually in 2011-12 as robust demand creates inflationary pressures. The Federal Reserve (Fed, the central bank) and its European counterpart, the European Central Bank (ECB), are expected to keep short-term rates at current levels until the second half of 2012. This underpins our forecast of elevated term spreads over the next two years.

Forecastperiod

Real GDP growth: G3 versus the BRICs (% change, year on year)

Source: Economist Intelligence Unit.

-6

-4

-2

0

2

4

6

8

10

12

-6

-4

-2

0

2

4

6

8

10

12

BRICsG3

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

Q3Q199

Q3Q198

Q3Q11997

n TheforecastsinthisreportarebasedontheEconomistIntelligenceUnit’snewquarterlyeconomicmodels.Unlikethestructuralmodelstraditionallyusedtomakemacroeconomicforecasts,ourapproachcapturesbothglobalanddomesticrelationshipsbetweenvariables,andthecomplexdynamicsacrossquarters.ForecastsbyquarterwillnowbepublishedfortheG3andBRICcountriesacrossallourservices.Formoreinformationortoreceiveaccesstotheseforecasts,pleasecontactyournearestEconomistIntelligenceUnit office.

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20102

OutputThe four BRIC economies (Brazil, Russia, India, China) have consistently outperformed the G3 (US, Japan, Germany) over the past decade. The BRICs’ share of global GDP has risen from 9% in 2000 to an estimated 14% in 2010, on the basis of market exchange rates. Over the same period, the G3’s share of global GDP is estimated to have fallen from 37% to 30% on a purchasing power parity (PPP) basis and from 46% to 41% on a market exchange-rate basis.

We forecast that this trend will continue in the medium and long term. Growth in the US will be constrained by an ongoing process of deleveraging by the private sector, and by the withdrawal of fiscal stimulus. Real growth in the fourth quarter of 2010 is forecast to be 0.2% in quarter-on-quarter terms, with growth for 2011 as a whole expected to fall to 1.5% from 2.5% this year. Japan will confront fiscal and demographic challenges at home, but can rely on robust Chinese demand to continue to provide a source of export growth, even taking into account a loss of competitiveness from a strong yen. We forecast fourth-quarter real GDP growth of 0.4%, and a weaker outlook for 2011, with annual growth slowing to 1.2%. Germany’s export sector will benefit from strong demand in emerging markets but domestic demand is forecast to remain subdued; consumer demand fell on a quarter-on-quarter basis every quarter from the first quarter of 2009 to the first quarter of 2010, and the recovery since has been muted. We expect a growth slowdown in 2011 as recent benefits from the stock cycle end; growth on a quarter-on-quarter basis in the final quarter of 2010 is expected to fall to 0.3%, and to continue falling in subsequent quarters until a quarter of zero growth in the fourth quarter of 2011.

China is forecast to continue to post strong growth, despite both subdued growth in its developed-country export markets and some tightening of domestic policy to contain inflation and curb growth in bank lending. We estimate fourth-quarter growth of 1.6%, with growth in the first three quarters of 2011 forecast to average 2.4% before falling back through to the end of 2011 and beginning of 2012. China’s growth will continue to have a galvanising effect on other emerging markets, including Brazil

Forecastperiod

Real GDP growth: G3 (% change, year on year)

Source: Economist Intelligence Unit.

-10

-8

-6

-4

-2

0

2

4

6

8

-10

-8

-6

-4

-2

0

2

4

6

8

GermanyJapanUS

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

Q3Q199

Q3Q198

Q3Q11997

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20103

Forecastperiod

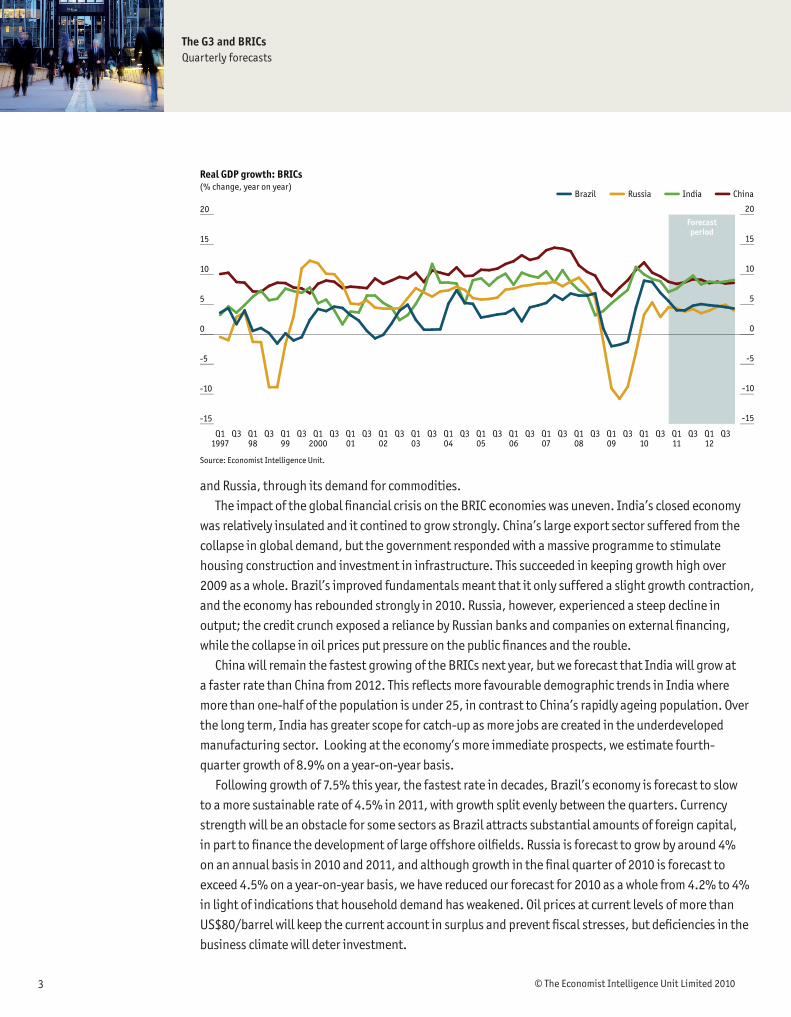

Real GDP growth: BRICs (% change, year on year)

Source: Economist Intelligence Unit.

-15

-10

-5

0

5

10

15

20

-15

-10

-5

0

5

10

15

20

ChinaIndiaRussiaBrazil

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

Q3Q199

Q3Q198

Q3Q11997

and Russia, through its demand for commodities. The impact of the global financial crisis on the BRIC economies was uneven. India’s closed economy

was relatively insulated and it contined to grow strongly. China’s large export sector suffered from the collapse in global demand, but the government responded with a massive programme to stimulate housing construction and investment in infrastructure. This succeeded in keeping growth high over 2009 as a whole. Brazil’s improved fundamentals meant that it only suffered a slight growth contraction, and the economy has rebounded strongly in 2010. Russia, however, experienced a steep decline in output; the credit crunch exposed a reliance by Russian banks and companies on external financing, while the collapse in oil prices put pressure on the public finances and the rouble.

China will remain the fastest growing of the BRICs next year, but we forecast that India will grow at a faster rate than China from 2012. This reflects more favourable demographic trends in India where more than one-half of the population is under 25, in contrast to China’s rapidly ageing population. Over the long term, India has greater scope for catch-up as more jobs are created in the underdeveloped manufacturing sector. Looking at the economy’s more immediate prospects, we estimate fourth-quarter growth of 8.9% on a year-on-year basis.

Following growth of 7.5% this year, the fastest rate in decades, Brazil’s economy is forecast to slow to a more sustainable rate of 4.5% in 2011, with growth split evenly between the quarters. Currency strength will be an obstacle for some sectors as Brazil attracts substantial amounts of foreign capital, in part to finance the development of large offshore oilfields. Russia is forecast to grow by around 4% on an annual basis in 2010 and 2011, and although growth in the final quarter of 2010 is forecast to exceed 4.5% on a year-on-year basis, we have reduced our forecast for 2010 as a whole from 4.2% to 4% in light of indications that household demand has weakened. Oil prices at current levels of more than US$80/barrel will keep the current account in surplus and prevent fiscal stresses, but deficiencies in the business climate will deter investment.

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20104

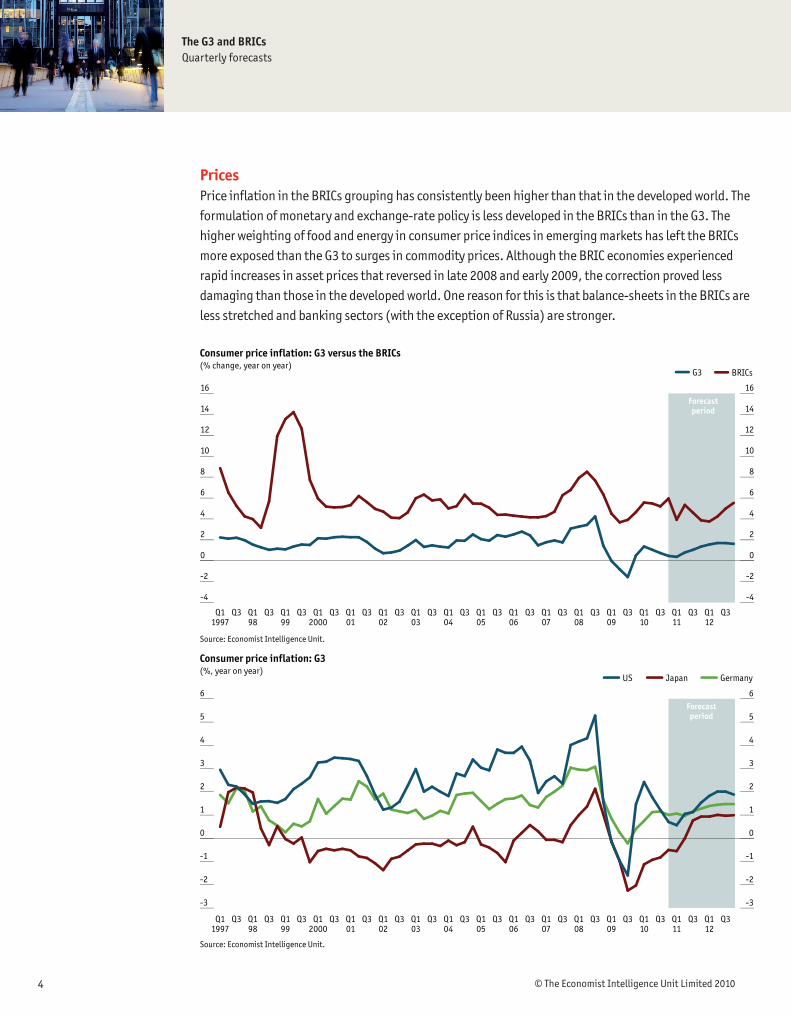

PricesPrice inflation in the BRICs grouping has consistently been higher than that in the developed world. The formulation of monetary and exchange-rate policy is less developed in the BRICs than in the G3. The higher weighting of food and energy in consumer price indices in emerging markets has left the BRICs more exposed than the G3 to surges in commodity prices. Although the BRIC economies experienced rapid increases in asset prices that reversed in late 2008 and early 2009, the correction proved less damaging than those in the developed world. One reason for this is that balance-sheets in the BRICs are less stretched and banking sectors (with the exception of Russia) are stronger.

Forecastperiod

Consumer price inflation: G3 (%, year on year)

Source: Economist Intelligence Unit.

-3

-2

-1

0

1

2

3

4

5

6

-3

-2

-1

0

1

2

3

4

5

6

GermanyJapanUS

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

Q3Q199

Q3Q198

Q3Q11997

Forecastperiod

Consumer price inflation: G3 versus the BRICs (% change, year on year)

Source: Economist Intelligence Unit.

-4

-2

0

2

4

6

8

10

12

14

16

-4

-2

0

2

4

6

8

10

12

14

16

BRICsG3

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

Q3Q199

Q3Q198

Q3Q11997

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20105

In the G3, policies of inflation-targeting and floating exchange rates are well established and were deemed to be working well during the “Great Moderation” of the past decade (a period of sustained, non-inflationary growth). However, although consumer prices were stable and low, asset prices were rising rapidly. Bubbles developed and eventually burst, giving rise to the greatest financial crisis of the modern era. Changes in the conduct of monetary policy are in prospect. Central bankers will need to take asset prices into account when setting policy rates. However, in the US the Fed is currently seeking to boost asset prices and avert deflation through its programme of quantitative easing (QE), whereby it prints money to buy government bonds and other assets with a view to stimulating demand.

We forecast that these measures will help to avert outright price falls in the US in 2011, although quarterly average inflation is forecast to remain below 0.5% until the final quarter of next year. Further out, a domestic demand recovery should help to create inflationary pressure. In the longer term, there are questions about the exit strategy from QE and whether the Fed will be able to sell its portfolio of assets back to the market without creating severe dislocations in credit markets.

Japan has been flirting with deflation for much of the past decade. The current strength of the yen will tend to entrench deflationary pressures. The Bank of Japan (BOJ, the central bank) has responded with its own version of QE (equivalent to around US$60bn) as well as intervening in the foreign-exchange market, selling yen, for the first time since 2004. These measures are expected to help Japan to avoid deflation in 2011-12, although consumer price inflation will struggle remain above 0.1% on a quarter-on-quarter basis over the coming quarters, and is estimated to be flat in the final quarter of 2010.

China experienced very low or negative inflation for much of the past decade as it emerged as a world manufacturing power and added huge amounts of capacity. But it has been the exception among the BRICs. In India, large fiscal deficits have contributed to inflationary pressures. Both Russia and Brazil have been undergoing a gradual price stabilisation process after experiencing high

Forecastperiod

Consumer price inflation: BRICs (%, year on year)

Source: Economist Intelligence Unit.

-5

0

5

10

15

20

25

30

-5

0

5

10

15

20

25

30

ChinaIndiaRussiaBrazil

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20106

inflation in the 1990s. We forecast that inflation rates in the BRIC countries will converge in 2011-12. In Russia and India,

inflation is forecast to continue to trend lower following the price surges of recent years. Indian price inflation is estimated to have fallen to 1.5% quarter on quarter in the final quarter of 2010, and is forecast to bottom out at 1% in the first quarter of 2011 before rising throughout the year. In Russia’s case, price growth on a quarter-on-quarter basis will remain higher in the near-term, with averages of 2% and 3% in the fourth quarter of 2010 and first quarter of 2011 respectively, before falling back as oil prices fall and the strength of the rouble helps to bear down on prices. The forecast uptick in Chinese inflation reflects the strength of domestic demand, and the authorities are tightening policy to ensure that inflation does not spiral out of control. We expect year-on-year inflation of 5% in the fourth quarter of 2010. Further modest monetary tightening is in prospect in Brazil to keep inflation within the target range of the Banco Central do Brasil (BCB, the Central Bank).

Exchange ratesThere have been a number of themes and cycles in foreign-exchange markets since the onset of the financial crisis. The US dollar has played the role of a safe haven at times of risk aversion, rising strongly against the euro and emerging-market and commodity currencies in the second half of 2008. Conversely, when markets are in risk-seeking mode, the dollar has been used as a funding currency for carry trades and has fallen. Anticipation of QE2 contributed to heavy selling of the dollar in the third quarter of 2010.

The yen has experienced a sustained rally since mid-2008, largely reflecting its status as a safe haven currency, but the appreciation is also a consequence of Japan’s positive current-account balance. This is creating problems for Japanese manufacturers, which are shifting more of their production offshore. Policymakers have tried to stem the yen’s strength by intervening in the foreign-exchange market for the first time since 2004 and by introducing a relatively small QE programme.

Forecast period

Nominal exchange-rate indices (US$:LCU)

Source: Economist Intelligence Unit.

60

70

80

90

100

110

120

130

140

60

70

80

90

100

110

120

130

140

China India RussiaBrazil Germany Japan

Q4Q3Q2Q112

Q4Q3Q2Q111

Q4Q3Q2Q110

Q4Q3Q2Q109

Q4Q3Q2Q12008

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20107

We expect the dollar to recoup some of its losses against the euro in 2011 as debt problems in the euro zone periphery remain to the fore, damaging sentiment towards the single currency. The yen is forecast to remain strong in 2011-12 but is vulnerable to a sell-off in the medium term as Japan’s saving rate delines, raising questions over the financing of its huge public debt.

When inflation differentials are taken into account, the profiles of the key bilateral exchange rates change slightly, and, significantly, the renminbi has experienced a stronger appreciation than the nominal rate would suggest. Conversely, the yen’s appreciation is less marked when very low Japanese inflation is taken into account.

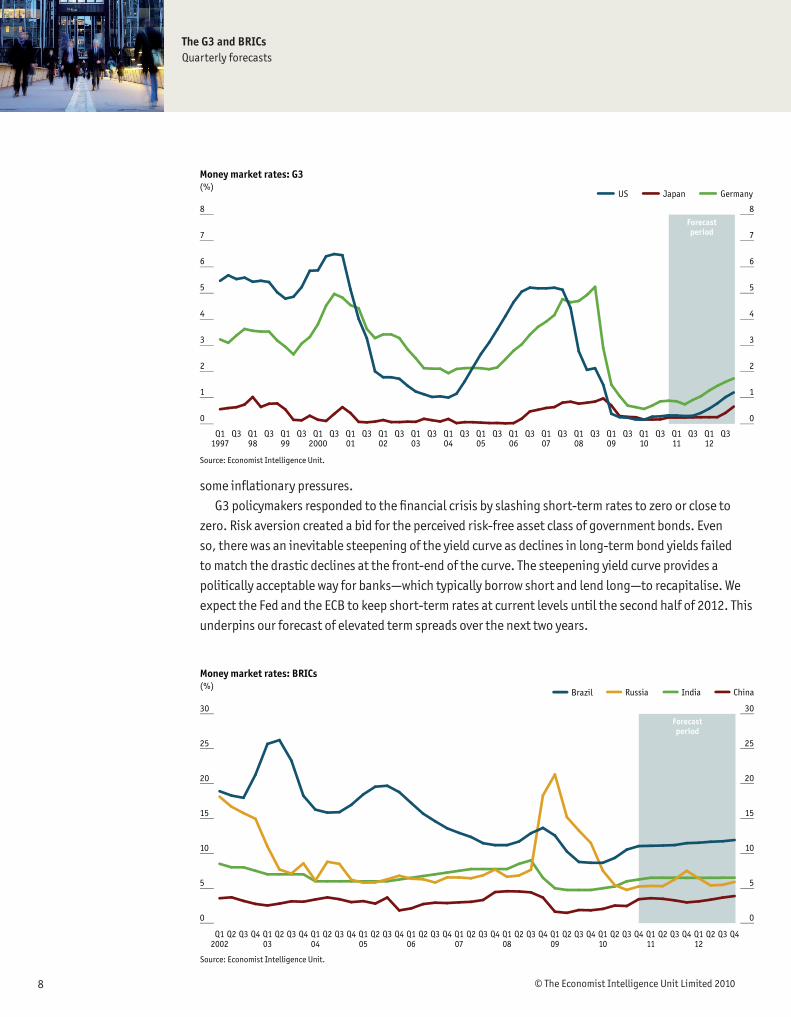

Interest ratesMoney market rates in the G3 have fallen sharply in the wake of the crisis, reflecting cuts in policy rates to close to zero. We do not expect the US and the ECB to start raising policy rates until the second half of 2012. Money market rates will tick upward ahead of policy rates in response to market conditions, a trend already established in the euro zone.

Money market rates in the BRICs have been much higher and more volatile than in the developed world. This reflects higher inflation in some cases, plus a lack of credibility on the part of policymakers. For example, in Brazil, even though the Central Bank has built up a good track record on price stabilisation over the past decade, real interest rates have remained among the highest in the world. The government’s high borrowing needs is also a factor, exerting upward pressure on interest rates.

In Russia, rates spiked higher following the failure of Lehman Brothers in September 2008. This was a reversal of the trend in the other BRIC countries and the rest of the world. Russia raised interest rates and ran down its foreign-exchange reserves in an unsuccessful attempt to support the rouble, which came under pressure as oil prices collapsed. This contrasted with the stance of Brazil’s Central Bank which allowed the Real to depreciate and conserved its foreign-exchange reserves.

We expect money market rates in the BRICs to tick up gradually in 2011-12 as robust demand creates

Forecast period

Real exchange-rate indices (US$:LCU)

Source: Economist Intelligence Unit.

70

80

90

100

110

120

130

70

80

90

100

110

120

130

China India RussiaBrazil Germany Japan

Q4Q3Q2Q112

Q4Q3Q2Q111

Q4Q3Q2Q110

Q4Q3Q2Q109

Q4Q3Q2Q12008

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20108

some inflationary pressures. G3 policymakers responded to the financial crisis by slashing short-term rates to zero or close to

zero. Risk aversion created a bid for the perceived risk-free asset class of government bonds. Even so, there was an inevitable steepening of the yield curve as declines in long-term bond yields failed to match the drastic declines at the front-end of the curve. The steepening yield curve provides a politically acceptable way for banks—which typically borrow short and lend long—to recapitalise. We expect the Fed and the ECB to keep short-term rates at current levels until the second half of 2012. This underpins our forecast of elevated term spreads over the next two years.

Forecastperiod

Money market rates: G3 (%)

Source: Economist Intelligence Unit.

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

GermanyJapanUS

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

Q3Q199

Q3Q198

Q3Q11997

Forecastperiod

Money market rates: BRICs (%)

Source: Economist Intelligence Unit.

0

5

10

15

20

25

30

0

5

10

15

20

25

30

ChinaIndiaRussiaBrazil

Q4Q3Q2Q112

Q4Q3Q2Q111

Q4Q3Q2Q110

Q4Q3Q2Q109

Q4Q3Q2Q108

Q4Q3Q2Q107

Q4Q3Q2Q106

Q4Q3Q2Q105

Q4Q3Q2Q104

Q4Q3Q2Q103

Q4Q3Q2Q12002

The G3 and BRICsQuarterly forecasts

© The Economist Intelligence Unit Limited 20109

Points to take away

l After a strong rebound from the 2008 recession, we forecast growth in the BRIC countries to moderate slightly, but to remain strong. The G3 economies face structural challenges, which will dampen growth prospects in the medium term, although the risk of a return to recession is now believed to have diminished.

l The two economic groupings face contrasting inflation challenges: for the BRICs, inflation prospects are vulnerable to commodity price fluctuations, while for the G3, falling prices remain a possibility. The threat of deflation will mean loose monetary conditions and the use of unconventional monetary policy in the G3 for the near term.

l Given underlying structural weaknesses in the economies of some euro member countries, we expect the euro to depreciate against the dollar over the coming year, although the outlook for exchange rates remains unusually uncertain. We also forecast a steady, moderate appreciation of the renminbi against the dollar in 2011 and 2012.

Forecastperiod

Term spread and real GDP growth: G3 (%)

Source: Economist Intelligence Unit.

-3

-2

-1

0

1

2

3

4

5

-6

-4

-2

0

2

4

6

8

10

G3 real GDP; right scaleGermany; left scaleJapan; left scaleUS; left scale

Q3Q112

Q3Q111

Q3Q110

Q3Q109

Q3Q108

Q3Q107

Q3Q106

Q3Q105

Q3Q104

Q3Q103

Q3Q102

Q3Q101

Q3Q12000

Q3Q199

Q3Q198

Q3Q11997

While every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsor of this report can accept any responsibility or liability for reliance by any person on this white paper or any of the information, opinions or conclusions set out in this white paper.

Cover image - © renkshot/Shutterstock

LONDON26 Red Lion SquareLondon WC1R 4HQUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8500E-mail: [email protected]

NEW YORK750 Third Avenue5th FloorNew York, NY 10017United StatesTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchai Hong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

GENEVABoulevard des Tranchées 161206 GenevaSwitzerlandTel: (41) 22 566 2470Fax: (41) 22 346 93 47E-mail: [email protected]

Related Documents