1 Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The origin al language text remains definitive in event of dispute. THE SMALL ENTREPRENEUR - A GUIDE (MARCH 2009)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 1/43

1

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

THE SMALL ENTREPRENEUR- A GUIDE

(MARCH 2009)

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 2/43

2

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

!!!!!

"#$ %&'()*+,!!-# #./.$01 2,!31456%478+9&,1$:.;$

::$ $7: 7

<5=(."

.(.>).

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 3/43

1

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

CONTENTS

Who can become a small entrepreneur?PAGE 2

What does the small entrepreneur regime mean?PAGE 4

What are the other advantages for the small entrepreneur?PAGE 14

How to leave the small entrepreneur regime?PAGE 16

FACT SHEETSPAGE 18

ACCRE and the small entrepreneur

Statutory unemployment insurance and business start-up or take-over

Multiple business activities carried on either by an individual or withinthe same household

Public employees and the small entrepreneur scheme

Accreditation of quarterly contributions for basic pension purposes

Post-retirement employment and basic retirement pension schemes

APPENDICESPAGE 32

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 4/43

2

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Who canbecome a

smallentrepreneur?

!"!#$%&!''" !'&#!()

!"&" ##"

(

""&! '!"'!

#!'!!'!

" !'!

*&&%!%"&

!')" &

#!)'"&+&

#'!

The small entrepreneurscheme came into force

on 1 January 2009.

+0-)'')#'!,-!')&.')"!'&#!!"&#!&+"!')!''!'&''%')"%'#"%!'''8/'""""

"&!&.')!"!"#&'!"''!"!!"&'+012.!#!"!!!"1

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 5/43

3

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

)

The following three conditions need tobe fulfilled:

Make a declaration online atwww.lautoentrepreneur.fr or at abusiness start-up registration centre(Centre de Formalités des Entreprises -

CFE), at the Chamber of Commerce(commercial businesses), the TradesChamber (Chambre des métiers)(skilled trades) or the URSSAF(professional services) as appropriate;

Fulfil the eligibility criteria for themicro-enterprise tax regime* whichmeans that annual turnover must bebelow certain limits

• 80,000€ for commercial businessesselling goods, articles, supplies and

foodstuffs to take away or to beconsumed on the premises and provisionof accommodation.

• 32,000€ for businesses providing servicesother than those coming under the80,000€ threshold

• 32,000€ for other provision of servicestaxable in the category "bénéfices noncommerciaux" (BNC), mainly professionalservices.

(See list of these types of business in Appendix 2)

These ceilings will be reviewed annually inthe same proportion as the income taxscales.

Be eligible for VAT exemption. Anybusiness may be exempt from TVA (VAT)as long as its annual turnover does notexceed the micro-enterprise tax regimeceilings (80,000 € for commercial ventures(purchase/resale, sales of goods andservices to be consumed on the premisesand provision of accommodation) and32,000 € for services) and subject to the

trader not opting to operate a VAT scheme.Under this exemption, the business doesnot add (output) VAT on clients' invoicesand cannot recover (input) VAT on invoicesfrom its suppliers. However, certainbusiness activities are excluded from theVAT exemption (see Appendix 1).

Moreover, income tax arising from thesmall entrepreneur's business activities

may also be paid at a flat rate, based onthe turnover figure of all smallentrepreneurs whose householdassessable income for 2007 is below: • 25,195€ per family part,i.e:

• 25,195€ for a single person,

• 50,390€ for a couple,

• 75,585€ for a couple with two children... Thus, a single employed person whose2007 taxable income (“revenu fiscal de

reference”) is below:• 25,195€ and who elects to start up abusiness, in addition to his employment, asan small entrepreneur will pay each monthor quarter a single amount calculated onactual turnover which will be full settlementof both his social charges and income taxfor this business activity.For somebody whose assessable taxableincome (“revenu fiscal de reference”) isabove:

• 25,195€, he will pay the social charges atthe flat rate and include the additional netincome in his annual income as declaredon his tax return. 8?2&!''3*!"#"#&'."4!&'!"

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 6/43

4

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

What does the smallentrepreneur regime mean?

5"'!#""&!)&.#&

2)'!

&&!!&4!#!&''!'6'"

.& %!%

7 "

@A #

(!)'!'3*)'

'.#!..'&&&"#!!'()

'!"#!4!"&

0"!770818'0"

07'70*0"94!'!##!:&&5!&8%8;5:<88'&='!">

'&"6+

!'!& 8&7 '8(#!!'

"1)&"'

'&'8(&&".'

!!%%)!"&!"

Simplicity itself – youknow exactly what

you get in your pocketafter tax and charges

B

If you are a student, unemployed or

retired person or salaried employee whowants to be a small entrepreneur only,this scheme enables you to start upyour own business.

From the moment that you make yourdeclaration as a small entrepreneur,either on-line or at a business start-upregistration centre (CFE), comply withthe annual turnover thresholds and donot operate a VAT scheme, you willbecome eligible for all the schemeadvantages, i.e.:

a single monthly or quarterlypayment of social charges and tax:

• 12% social charges forcommercial businesses sellinggoods, articles and supplies andfoodstuffs to take away or eat onthe premises or provision ofaccommodation; plus 1% tax(income tax), together a singlepayment of 13% of your turnover.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 7/43

5

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

! "!

• 21.3% social charges forbusinesses providing servicesother than those coming underthe 80,000 euros threshold plus1.7% tax (income tax), togethera single payment of 23% ofyour turnover.

! #"!

•18.3% social charges on the

services provided byprofessionals (professionnelslibéraux) coming under theCaisse interprofessionnelle deprévoyance et d'assurancevieillesse (CIPAV) plus 2.2% tax(income tax), together a singlepayment of 20.5% of yourturnover.

(See list of these types of business in Appendix 2)

! #$!

Please note: certain businessactivities come under the 21.3% rate for social charges and 2.2% for income tax, i.e. a singlepayment at 23.5 %. This applies inparticular to commercial agents(See list in Appendix III).

Apart from the facility to pay at

source, in one payment and in fulldischarge on the basis of turnover,this scheme is designed tosimplify administrative burdensgenerally linked to businessstart-up:

;5/?!!!%&"!4!@"&!&!"!+.!%&&4!

2&!%%+"!"'4!)!'" !'"#"4!'#')!) !'!&

*'9#!!''"%! '#'&$!9%"&&%A.!B'4!&

'! '!+. "#)$!"'')'&#!!"&! ()+""')!&!")&".!!'!'*&&'/3*)."#!%

#!..'&&&C *&#!!/ • 1+D!#!!''+#&#!9

• &#!9• #'#!9• "#!81E9• '&##!

80<19• '!!'''#!9

• ##&#!

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 8/43

6

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

What does the small entrepreneur regime mean?

• Exemption from formalregistration and simplifieddeclaration. Business and skilled trades people are

usually required to register formallywith the 'Registre du commerce et dessociétés' (RCS) (Companies' Register)or with the 'Répertoire des métiers'(RM) (Trades Register). As a smallentrepreneur, and if you have opted for'pay as you go' payment of socialcontributions, you are exempt from thisrequirement. All you need do iscomplete a single simplified declarationform designed for the smallentrepreneur online atwww.lautoentrepreneur.fr, or at your

business start-up registration centre,which then serves as:

an application for the issueby INSEE (National StatisticsOffice) of a SIREN number, theunique identity number for yourbusiness;

a declaration of businessstart-up to the social securitycontributions agency dealing withself-employed workers (RSI)incorporating your option for the

simplified micro-social regime; declaration of business start-up

to the tax authorities incorporating, ifappropriate, your option for 'pay asyou go' payment of income tax. Thecompleted and signed form should besubmitted with a photocopy of youridentity document to the businessstart-up registration centre (CFE)appropriate for your type ofbusiness1:

1 %&'(()(*&'(+(& +

CFE run by the 'Chambre decommerce et d'industrie' (Chamber ofCommerce & Industry) for thoserunning commercial/retail businesses,

CFE run by the 'Chambre demétiers et de l'artisanat' (Chamber forSkilled Trades) for those carrying onbusiness as skilled trades people,whether full or part-time,

CFE run by the URSSAF for themajority of other services.

The declaration may also be madeonline at the one website.The relevant agencies will beautomatically advised about yourdeclaration.

Irrespective of your business sector, youcan declare your start-up online atwww.lautoentrepreneur.fr.

Please note: Commercial agents arestill required to register formally with theSpecial Register for Commercial Agents- RCAS (Registre spécial des agentscommerciaux) attached to thecommercial court in whose jurisdictionthey are domiciled.

• Exemption from pre-start uppreparatory course (for thosecarrying on business as skilledtradespeople) Skilled tradespeople (artisans) usuallyhave to follow and pay for a pre-start uppreparatory course usually organised bythe 'Chambre de métiers et del'artisanat' (Chamber for Skilled Trades)before they can register with the'Répertoire des métiers' (RM).

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 9/43

7

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Small entrepreneurs carrying onbusiness as skilled tradespeople underthis new scheme are not required tofollow such a course (but you may, ifyou wish, ask to follow it on a voluntarybasis).If, subsequently, you go on to registerformally with the 'Répertoire desmétiers' (RM), (either because youwish to or because your turnover

figure has exceeded the thresholdsshown above), you will be exempt fromthe requirement to follow the course.

• Option for 'pay as you go'payment of income tax atsource and in full discharge. This additional option is grantedsubject to your household's overallassessable income (revenue global de

reference) for 2007 not exceeding25,195 € per family part (quotientfamilial).

If your overall assessable incomeexceeds this threshold, you can still beeligible for other advantages offered bythis new regime (flat-rate payment ofsocial charges and exemption fromformal registration).

This option gives you a number ofadvantages2:

Pay as you go payment of incometax levied at source on your actualturnover or received earnings. Youpay your income tax at the sametime as your flat-rate social charges.You pay tax on your earningsreceived during the period (quarteror month) by applying the followingrates:

• 1% for commercial businessesselling goods, articles, suppliesand foodstuffs to take away or tobe consumed on the premises and

provision of accommodation;

2 ,--./0).

• 1.7% for businesses providingservices other than those comingunder the 80,000 € threshold

• 2.2% for other provision of servicestaxable under the category of'bénéfices non commerciaux' (BNC),i.e. mainly professional services. (See list of these types of business inAppendix 2).

When added together, these tax ratesand the social charges rates make upthe sole rate of contributions payable bythe small entrepreneur, i.e. 13% forcommercial businesses buying/sellingand comparable businesses (12% socialcharges + 1% tax), 23% for the provisionof services other than those comingunder the 80,000€ threshold (21.3%social charges + 1.7% tax), 20.5% forprofessional services (18.3% social

charges + 2.2% tax).

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 10/43

8

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

What does the small entrepreneur regime mean?

As with contributions and socialsecurity payments, if you receivedno takings, then you make nodeclaration and you pay no tax for

the period concerned in respect ofthat business.

Payment of this tax is at source and infull discharge: you only need to enterthe total of your turnover or receipts forthe year in the box provided for thispurpose on your annual income taxreturn. Your tax liability, whencalculated, will not include the taxalready paid in respect of yourbusiness during the previous tax year(See example at the bottom of this

page). Temporary exemption from

business tax (taxe professionnelle).By opting for the ‘pay as you go’payment of income tax, yourbusiness is fully exempt fromcontributions to business tax forthree years. Thus, if you start up on1 March 2009, you are exempt frombusiness tax for 2009, 2010 and2011.

B#

• What will not change: the conditionsunder which you operate your

business. Professional qualifications andstandards

Certain occupations are regulated andlegally require formal qualifications.

For skilled trades (artisans) in theconstruction and food industries,home-based hairdressing and beautyservices, etc., the business must be runor supervised by a person holding avocational qualification at a level at least

equal to CAP (certificat d'aptitudeprofessionnelle - vocational trainingcertificate) or with prior professionalexperience of at least three years in thatfield. Please see Appendix III for the listof relevant trades. You should seekinformation from the appropriatechamber, institute, professional orstatutory regulatory body about theregulations governing the sector inwhich you wish to operate your business.

'*1$!2)34&51$$!677$!89"$!

• *.!#&/ ()&.!#)CF)"&G)CDCH)

• *.!&/*.!!HHFH)H.IG;%

&#&&')I)HF*.I)FI)HF.G*.!&I)FHHJI) $C0DE%,*C0F,F&

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 11/43

9

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Business insurance

You must comply with therequirements for business insuranceappropriate to the type of businessyou operate.

What insurance is compulsory?It depends on the type of businessyou operate. There is a legalrequirement in some sectors (such

as construction) to take out aspecific type of insurance. Beforestarting your business you shouldalso seek information aboutinsurance requirements from theappropriate chamber, institute,professional or statutory regulatorybody.

What is the extent of theentrepreneur's liability?

Like any entrepreneur, the smallentrepreneur can be exposed toprofessional indemnity liability risks

in connection with his businessactivities. Taking out a professionalindemnity liability insurance policy isnot compulsory, except for certainbusinesses.

Duty of loyalty

In a similar way to any othercontracting party, an employee isbound to observe a duty of loyaltytowards his employer. Subject to

limits set by case law, this duty ofloyalty extends after the end of theemployee's contractual relationshipwith his employer.

If you are a salaried employee andyou wish to operate anindependent business in additionto your main employment, you arenot permitted to carry on the sametype of business set out in youremployment contract with youremployer's clients without thelatter's express agreement.Moreover, your employmentcontract may contain clausesprohibiting or restricting your rightto start up a business, in order toprotect the employer's interests.You should therefore check theclauses in your employmentcontract carefully if you are asalaried employee and you wish tocarry on an independentsupplementary business.

Compliance with generalregulations and professionaltechnical standards

Legal and regulatory provisions aswell as professional technicalstandards, especially relating tohealth and safety, employment lawas applied to salaried employees,consumer protection provisions allapply to the small entrepreneur.

@K@#"%

&+&'%!+!')#!'&!%'##!%)%.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 12/43

10

Please note: Whilst we have taken every care to provide an accurate translation,we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

What does the small entrepreneur regime mean?

• What will change: theconsequences of opting not toregister formally with the RCS orthe RM

If you have decided not to registerformally, you will not then be eligible forcertain rights reserved forentrepreneurs formally registered witha public legal register (e.g. RCS, RM).

Commercial leases Reminder of the principal specificprevisions of the statute relating tocommercial leases (Articles L.145-1 to

L.145-60 of the Code de commerce(French Commercial Code).

minimum term of lease fixed at 9years with tenant having the right toterminate at the end of each 3 yearperiod unless there is a clause tothe contrary;

rent capped at the three-yearlyreview or at renewal of the lease;

right of renewal for the lessee whorequests it prior to the expiration of

the lease; if the property ownerrefuses renewal, he pays thelessee compensation for eviction.

Entitlement to vote and stand forelection at respective chambers

If you are not registered at theCompanies' register (RCS) or theTrades Register (RM), you will notbe a voting member of either achamber for skilled trades or achamber of commerce & industrynor will you be required to pay therelevant annual subscription.

@K2&)'!)!%'&.'&&"8'"081*0"0)!#"#&"&&!%#!!"# %!#!#!"2&! #"#&"&!!" %! ..

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 13/43

11

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

For those already running a business (sole trader,providing professional services ('profession libérale')...)

*#!&!&"##

'!)&I L!M)

%"')'')!'''!&#

'!).''&.'&&""

&"8'"081

*0"0

BG

• Option to take up thesimplified micro-social regime.

You may apply for the simplified'pay as you go' social securityregime reserved for smallentrepreneurs. You need to makean application in writing to theoffice handling the social securityregime for independent workers towhich you are currently affiliatedat the latest by 31 December ofthe year preceding the one inwhich the scheme is to apply.Businesses already existing on 1January 2009 may exceptionallyexercise their option to take up thesimplified micro-social regime upto 31 March 2009 for anapplication relating to 2009. Thechoice of payment option appliesfor a whole year. You can thuspay your personal social chargesat source and in full dischargecalculated on earnings received ata flat rate of:

The entrepreneuralready running a

business maytherefore not

'de-register' hisbusiness.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 14/43

12

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

What does the small entrepreneur regime mean?

• 12% social charges on commercialbusinesses selling goods, articles,supplies and foodstuffs to take awayor eat on the premises or provision ofaccommodation21.3% for businesses providingservices other than those comingunder the threshold of 80,000 euros;

82&&&"'&%'!."!82@3)"!'#!&I L!M'&'!*''!"

#!

• Option for 'pay as you go'payment of income tax at sourceand in full discharge

You may apply for the additionaloption of 'pay as you go' payment ofincome tax levied at source onturnover from a sole trader business(entreprise individuelle), provided youhave opted for the simplified

micro-social regime (see paragraphabove) and provided that your overallhousehold income does not exceed25,195€ per family part (quotientfamilial).

How to take up this option?

You should advise the RSI (regime forindependent workers) office currentlydealing with your affairs about yourwish to take up this option at the latest

by 31 December of the year precedingthe one in which the option is to apply.

However, exceptionally, you mayqualify for this regime in 2009 if youexercise your option before 31 March2009.

Your contributions will be recalculatedand any overpayment will bereimbursed. This option gives you thebenefit of 'pay as you go' payment ofincome tax levied at source on yourturnover or takings.

You pay your income tax at the sametime as your flat-rate social charges.You pay tax on your takings duringthe period (quarter or month) byapplying the following rates:

• 1% for businesses whose main

activity is to sell goods, articles,supplies or foodstuffs to take awayor to eat on the premises, or toprovide accommodation;

• 1,7% for businesses whose mainactivity is to provide services otherthan those coming under thethreshold of 80,000 euros;

Payment of this tax is at source andin full discharge: you will not be dueto pay any further tax on this income

at the end of the year.

• What will not change

Choosing to opt for the simplifiedmicro-social regime and for 'pay asyou go' income tax at source will nothave any impact on the conditionsunder which you operate yourbusiness. As set out above, you mustcomply with regulations relating toprofessional standards andqualification, business insurance,restraint of trade (in respect of anyemployer), general legal regulationsand professional technical standards.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 15/43

14

Please note: Whilst we have taken every care to provide an accurate translation,we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

What are theother advantages for the

small entrepreneur? '!)!4!&

&%"&&#!N'

'O*@'%""'&''!"

#!

'

Business owners under the micro-enterprise tax regime, whetherformally registered or not, benefitfrom less onerous accountingrequirements.

They are required only to keep asimple ledger showing the amountand origin of their businesstakings, in chronological order,showing payments in cashseparate from other payments.

References to supportingdocumentation (invoices, bills, etc.)should be shown in this ledgerwhich should be written up everyday.

Furthermore, where the mainactivity of the business is sellinggoods, articles, supplies orfoodstuffs to eat on the premisesor to take away, or the provision ofaccommodation, business ownersare also required to keep a ledgershowing, in year order, details oftheir purchases, showing themethod of payment andreferences to supportingdocumentation (invoices, bills,etc.).

Business owners must keep allinvoices or other supportingdocumentation relating to theirpurchases, sales of goods orprovision of services.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 16/43

15

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

H #$>

• What assets can be madeexempt from seizure?

All land whether developed orundeveloped (plots of land, houses)not designated for business purposes.

• How to make your personalproperty assets exemption fromseizure?

By making a declaration of exemptionfrom seizure before a notary, which issubsequently published in Register ofMortgages (Bureau de la Conservation

des Hypothèques) in the place wherethe property is located as well as in theappropriate public legal register (if youare formally registered) or the journalof legal notices in the departmentwhere the business is located (if youare not formally registered).

• What are the consequences ofthis declaration of exemption fromseizure?

The property designated in thedeclaration may no longer be seizedby your business creditors where thedebts arose after the publication of

the declaration unless you decide towaive the exemption from seizure infavour of one or more creditors or inrespect of all or part of yourproperty assets (by a waiver beforea notary and published in the sameway and with the same bodies asthe original declaration).

The property so protected can

include not only your principalprivate residence but also all yourland whether developed orundeveloped not designated forbusiness purposes. You also haveright to waive the exemption fromseizure in favour of one or morecreditors which may allow you toaccess credit more easily.

+$

The small entrepreneur has accessto the collective insolvencyprocedures for businessesexperiencing difficulties whateverthe type of business activity.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 17/43

16

Please note: Whilst we have taken every care to provide an accurate translation,we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

How to leave the smallentrepreneur regime?

4

If you opted for the newmicro-social regime and the 'payas you go' payment of income taxat source for the smallentrepreneur and you ceasetrading, even during the course ofthe tax year, you are not liable forany remaining social charges orincome tax relating to your

business (above that due on yourlast declared turnover figure) onceyou have made a declaration atthe business start-up registrationcentre (CFE) that you haveceased trading.

'

If you opted for thesimplified micro-social regime

and the 'pay as you go' paymentof income tax at source but youno longer wish to stay on thescheme even though you are stilleligible, you should make aspecific request at the latest bythe 31 December of the yearpreceding the one in which youwish to revert to the regimeunder ordinary law.In fact, any change in themethod of paying socialcontributions may not be made

for a period of less than a year.

If you opt for the simplified'régime réel' tax regime, you leavethe micro-enterprise tax regime inthe year in which the option is toapply. Consequently, you leavethe simplified micro-social regimeand the 'pay as you go' paymentof income tax at source that sameyear.

':0,

If you do not produce any turnoverfor 12 consecutive months, youwill cease to qualify for the smallentrepreneur regime. If you ceasetrading, you should send adeclaration to the CFE dealingwith your affairs. If you were tocontinue trading, you can stay inthe micro-enterprise tax regime(see Appendix I) but you must

formally register with theCompanies' register (RCS) and/orthe Trades Register (RM), asappropriate to your business.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 18/43

17

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

'$$

If you exceed the eligibilitythresholds for the micro-enterprisetax regime (80,000€ for commercialventures - purchase/resale, sales of

goods and services to be consumedon the premises and provision ofaccommodation - and 32,000€ forservices) you continue to be eligiblefor the simplified tax and socialsecurity regime and exemption fromformal registration during the firsttwo years this limit was exceededprovided that your turnover figurewas not in excess of 88,000€(commercial ventures) or 34,000€(services).

See example in Appendix I.If your turnover exceeds 88,000€(commercial ventures) or 34,000€(services), the 'pay as you go'payment of income tax at sourceregime will cease retroactively at 1January of the year during which thislimit was exceeded, whereas thesimplified micro-social regime willcease on 31 December of that sameyear.

@K *#%#%!

'66 $$

If your assessable householdincome (revenue de référence devotre foyer) exceeds the 25,195€per family part (quotient familial)

limit (2007 assessable income),you will only lose eligibility for thenew tax regime in the second taxyear following the one in which thelimit was passed. You may,nevertheless, remain eligible forthe other advantages offered tothe small entrepreneur (socialsecurity regime and exemptionfrom formal registration).@K

*&H)IMHF#%!

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 19/43

18

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

ACCRE and the small entrepreneur

1. Current arrangementsapplicable up to 1 May 2009

*!''&#!!'#!''''&#&%"!''880!'.'&#!&"#/− #!'"'81E80<1'#9 −

&&I)#!.''%IG%&!!"128 *'&.""#"#&!.' *#.%&"&#!!#$'."/− !#&!.'&!#!!'#%&010%!7%9− &'&#&%!128&"!.'HG9− &')&'!.!128)"4!&&.'*&&)!&&"#!'!&#!

!)!"!%%&#!7$+44I)

− :'&'!&&#!!'& 880%!'&"H&8809− #!#"#&.'&&"&+#!)&!'!9− !".''"#880)'"81E80<1''#!!4!

#!&')')4!)&'!''2. Reforms applicable witheffect from 1 May 2009

*!&'!'

!&!"&#!.!#'"&!%4!%&&!""#!!

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 20/43

19

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

880'&'&.

:,313!1F31 *'"''#'!")F&'!D%C)F&%2&.)'&!%#%

#!#$!!'!")'!4!#"#& *#""%%"/.')#&!&&

)"& '')&"!"&'!#!"!#'"%! :+44I)0(,!!D(&'&")#&"&%"880* !&C)'!''&!/

0''"!%

I C

1

'!

1%'% HCG IG IG ICG

*)'+')#!P

CG G MG IG

@&%

"!82@3HCG MG ICG ICG

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 21/43

20

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Statutory unemployment insuranceand business start-up or take-over

*!%Q;<28,")&IL!)'""!%"&'%'&'"!'+"%#!'&!&!'#&

"!#!!'#$#+!%'+"+9$#+!!!'#&!"'''"!'!'%)'#'%#$#

+"+"%#! 0:#&!"+!%)$#+"!'#!!%'&!

!'#&&'!'IH)&)!#$#!"."G&&#&'!(&&')!&''#

'!9#!$!!.#+ , &"!Q;<28"IL!$#+"!'+"%#!+&&&#&!!'#&#'!#'&'$

#!*$#+"$#+'#!"6%&'#!&.

*:;<:=4&-;>-

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 22/43

21

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

2&#!&)''''"&'&!!'#&!'.!&"&&#&#& *$#+"$#+%"#&'#!"

+%''&'&&#&'

2&#!&'&)#!''&"!!'#&)##"!!'!%#&!!'#&#'%!

'

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 23/43

22

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Multiple business activities carried on either byan individual or within the same household

0 Boundary between

purchase/sales activities andprovision of services

2'"!#'&%&&&!%"''"'!)F

C)FThe 80,000€ ceiling applies to:

• '!&"#"&!&!&"9

• !&!&'!&&!)))&#+")!&!&!$)9

•&&!&&#!&7)!)

9

• '%&)5P5The 32,000€ ceiling applies to:

• %'%'!!''#"'"&'!2!)%'%!'''"!''#!)'!''#&9

• &"#""#&'!'"9

• +!''9

• '%&&!' , Multiple business

activities and increase inturnover ceilings • 2&)#!)!.!&%'!'%&'%&%&!'!+%)!%!.)F)"!%"'%&%!.C)F (.'/#!" %#!"4!& +#!

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 24/43

23

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

• 2&)#!)!'D%"! 528")%)%"!5;8")'#"!'"!

"""!%!.)F9")!!%"&%!.C)F(.'/&'!&"&5;8%528% *!'!%!

''&!%!''#!'%"!5285;8"• 2)&)#!)!%"!

5;8")%)D%"!528")'#"!'"!!%!.C)F

• 2&!!!'%%&'5285;8)'&%#"!'"&'#"!'"+!"#.C)F)F(.'/2*!'%"&&&

'!• @/2&#&! '#!%!)!%'&#!#'&#

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 25/43

24

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Public employees and the smallentrepreneur scheme

@!#')%&!#$!'#"&'"'%#!&"'&!"&"%)%"!#"##'!!&&" 0 Full-time or part-time public

employees ('temps plein' or 'tempspartiel') *'&'&#!''4!7& +94!&!'+%&!#$'#""&'Secondary activity as a smallentrepreneur - specific circumstances

&!''!#'#'%!'!)!'&)&&"/ .'!+)")")+!'%%!Small entrepreneur business start-upin all other situations

'!#'!'!))+)"!!'&%#!!'!) !'!'&

!#!)&'&)#)&%&'&2&#!!'"!"'!#')' +")&4!)"&" , Part-time flexible or casual

part-time public employees ('temps

incomplet' or 'non complet') *'&'''4!7&+94!!'#!"!"'!#'4!'' '&.#!''!#''''''%#!&")%'!'&) !'&)&%"%'"'2)"%'''&'!#!&!'"&!"&"%"""&&&!'#'!#'

References:Law no. 83-634 dated 13 July 1983Decree no. 2007-658 dated 2 May 2007Circular no. 2157 dated 11 March 2008

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 26/43

25

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

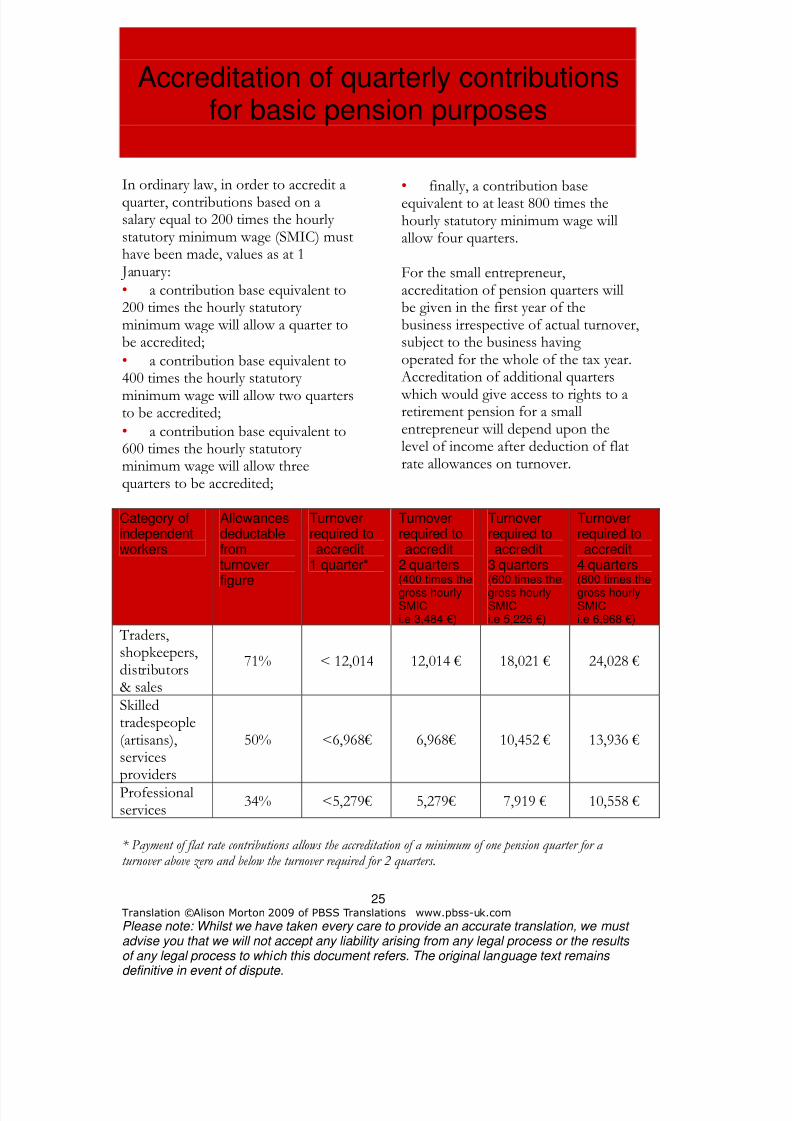

Accreditation of quarterly contributionsfor basic pension purposes

2)4!)#!#4!!!!"128!%#)%!I L!/ • #!#4!%!!!"4!#9• #!#4!%!!

!"4!#9• #!#4!%!!!"4!#9

• &)#!#4!%!!!"&!4!('!)&'4!#"%&&#!'%&!!%)!#$#!%"'&&. &4!

!"%"'&'!'!'%&&!&&!%

Category ofindependentworkers

Allowancesdeductablefromturnoverfigure

Turnoverrequired toaccredit

1 quarter*

Turnoverrequired toaccredit

2 quarters(400 times the

gross hourlySMICi.e 3,484 €)

Turnoverrequired toaccredit

3 quarters(600 times the

gross hourlySMICi.e 5,226 €)

Turnoverrequired toaccredit

4 quarters(800 times the

gross hourlySMICi.e 6,968 €)

*)'+')#! P

IG RI)I I)IF I)IF )F

1+'')%'%

HG R)MF )MF I)HF IC)MCF

@&%

CG RH)MF H)MF )MIMF I)HHF

;?@?#?

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 27/43

26

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Post-retirement employment and basicretirement pension schemes

*&"!"''''&!'&''!'+%#!!'!Conditions of combining retirement with working 0 General conditions

()!'%!11!(!"&M)''"!"")"!!"

""&M#'&' !)"%"'− &"&&%!&&#!4!&&&!

'9− &"&H , Other conditions

:!##

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 28/43

27

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Regime

Current position: for those retiring without afull pension, or before 65, the previous rules

for combining retirement and working willcontinue to apply.

0''"!/• ""7"

"77.''")• "!!"7""')• 1'".').'&'"&'!#'"%%)"%

'!#')+!"

8#"'!&#'

&'"%&&&"'#&!&''!!'''&!'!&'#&'"%&&"#&"'&"#IG&128!!"AB1)##=1)#)1=1)#)&CC2CC&5NB: the retirement pension from these basic retirementpension schemes may therefore be combined with incomefrom employment which gives rise to affiliation to otherbasic retirement pension schemes (non-salaried workers'regime and special regimes for public employees, workersin state-owned industrial organisations and sailors). *'''"'&9)&%9&&#!9$!%9#9''!II&'8!%9

!9%!!'''&!"&	!"D"D"&'#.'&'%!') &+&8<<S!777/II!811E"#++&'%!'/&'"#+.&&&%&&')

#%&')"&&"#''AB1)##=1)#)#&CC

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 29/43

28

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Social security/employment status of

retired people

Current position: for those retiring without afull pension, or before 65, the previous rules

for combining retirement and working willcontinue to apply.

;&'+)!012

*#'&&'+#'+'+)!&&

'&!"I)C!)''&%2&'T00!%UU%!TQ1%!#UU!##.!!"CC)!2&&'.")'&'#!'&'4!'#!&.!&

'AB1"D)1=1"D))#&CCNB: the retirement pension for these non-salaried(self-employed) workers may therefore be combined withincome from employment which gives rise to affiliation toother basic retirement pension schemes (salaried workers'regime and the regime for professional service providers).

Special circumstances: carrying on workingafter transfer/sale of a business

*#!'"#'&D#!"#H)''&+&.!"!AB1"D)1)=1"D)")&CC2'!")""&#!#<M&.'&#"'!&

!%.!&)"!AB1"D)1)=1"D)")#&CC

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 30/43

29

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Social security/employment status of

retired people

Current position: for those retiringwithout a full pension, or before 65, theprevious rules for combining retirement

and working will continue to apply.0 &'&%'%

8#"'&%#'&'&%'%!&!!&#!

!"CC)!2&!.)%!!%#&'&'&'&'#!'Special circumstances/&'&)"&!"+!*''

'")&%!''%#&"&')$!%9#AB1D")1=1D")&CC;5/#'&'&%'%&## &'"%&&#'+""&+&'+)!

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 31/43

30

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Post-retirement employment and basicretirement pension schemes

Consequences of combiningpost-retirement work andpension

0 Contributions due '!+'&%'%##'#!&+)

!+2'&"')'"!'&''+#'#!''"'#!&&%.#"#!/+&#!)#!#!&#'"!''#!!!%#!!&!#!NB: if going back to work under thesmall entrepreneur scheme, pensioncontributions are included in thesimplified micro-social deductions. , Benefits

Q''!)%!#&& "&''

• If the new activity comesunder the regime which ispaying the retirement pension

− 1+''/&!"'&#'6%)#!''&!'''

−

*)'+')#!PV/&!"'&#'6%)&'&!''')!""#++

− @&%'%#7!./&!"'&#'!'''

1'/&!"'&#'!'''W If the new activity doesnot come under the regimewhich is paying the retirementpension (not including lawyers('avocats'))

8#!'#!'''

"%

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 32/43

31

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Appendix I The micro-enterprise tax regime

Who is eligible for the micro-enterprisetax regime?

To be eligible for the micro-enterprise taxregime you must:

Carry on business as a soletrader;

Only those individuals running a businesson their own account are eligible for the

micro-enterprise tax regime; registeredcompanies are excluded, evenpartnerships as defined under Article 8 ofthe CGI (Tax Code), as are not-for-profitassociations.

Have a turnover which does notexceed the specific ceiling applyingto business sector in which youoperate;

The new annual turnover ceilings are asfollows:

• 80,000 € where the main businessactivity is the sale of goods, articles,supplies and foodstuffs to take away oreat on the premises or the provision ofaccommodation;

• 32,000 € for businesses where themain activity is the provision ofservices other than those comingunder the 80,000 euros threshold;

• 32,000€ for the provision ofservices taxable under the categoryof 'bénéfices non commerciaux'(BNC), i.e. mainly professionalservices.

These thresholds will be reviewedannually within the same parametersas the first band in the income taxscale.

Not operate a VAT scheme;

All businesses are exempt fromoperating a VAT scheme as long astheir turnover does not exceed themicro-enterprise tax regime ceilingsand the owner does not opt to operate

a VAT scheme. Under this system thebusiness does not add (output) VATon clients' invoices and cannot recover(input) VAT on invoices from itssuppliers.

Please note! If a business chooses tooperate a VAT scheme, it will nolonger be eligible for themicro-enterprise tax regime.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 33/43

32

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Not run a specifically'excluded' business;

Businesses 'excluded' from themicro-enterprise tax regime includethose covered by the specialagriculture VAT scheme, certaincommercial or non-commercialbusinesses such as plant hire andhire/leasing of consumer durables,

sale of new vehicles in other EUmember states, businesses comingunder the property VAT scheme(property dealing, propertydevelopment, estate agency,operations dealing in propertycompanies; in contrast, leasingbusinesses and letting of furnishedpremises or premises which will befurnished are eligible), letting of emptyoffice space, court and state officials,literary, scientific or artistic output,professional sport, as long as thoseconcerned have chosen to beassessed on the basis of averageincome over the past two or fourpreceding years, futures marketdealing, trade options exchange anddealing in equity warrants.

Not opt for assessmentunder the simplified 'réel' taxregime.

The micro-enterprise regime isgranted as of right if the conditionsshown above are met, but thebusiness owner may if he wishesopt to be assessed under the'régime réel'.

In general terms, how doestaxation under themicro-enterprise tax regimework?

The following rules will apply,unless the entrepreneur has optedfor the 'pay as you go' payment ofincome tax at source.

Business owners declare theirturnover and receipts received inconnection with their businessactivity during the tax year on theirhousehold tax return.

These are used to work out a profit;when calculating the income taxdue, the tax authorities apply flatrate allowances equivalent torunning costs; these vary accordingto the type of business activity, asfollows:

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 34/43

33

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Appendix I (continued)

• 71% for businesses whose

activity is the sale of goods, articles,supplies and foodstuffs to takeaway or eat on the premises or theprovision of accommodation;

• 50% for businesses whosemain activity is to provide servicesother than those coming under the80,000 euros threshold;

• 34% for non-commercialbusinesses.

The turnover figure less allowancesthen serves as the basis for levyingincome tax in accordance withprogressive scale rates. This tax ispayable in three instalments, or bymonthly payments, in the yearfollowing the year for which thebusiness declared the income. Theself-declaration requirements aresimple and straightforward; flatrates for deducting running costs

mean that accounting procedurescan kept very simple.

What are the consequences ifbusiness turnover increases?

So that businesses can transfersmoothly out of the very simplemicro-enterprise and VATexemption regimes if the ceilingsare breached, the scheme allowsbusinesses to stay in the scheme

for two years providing that thefollowing two conditions are met:firstly, the thresholds of 88,000€(commercial sales) or 34,000€(provision of services) are notexceeded, and secondly, the small

entrepreneur does not operate a VAT

scheme at any time during the year inquestion.

The benefit of the exemption isgranted in year N if: • turnover in year N does notexceed 88,000€ and the turnover inyear N-1 did not exceed 80,000€

• or the turnover in year N does notexceed 88,000€ and the turnover inyear N-1 did not exceed 88,000€ and

turnover in year N-2 did not exceed80,000€.

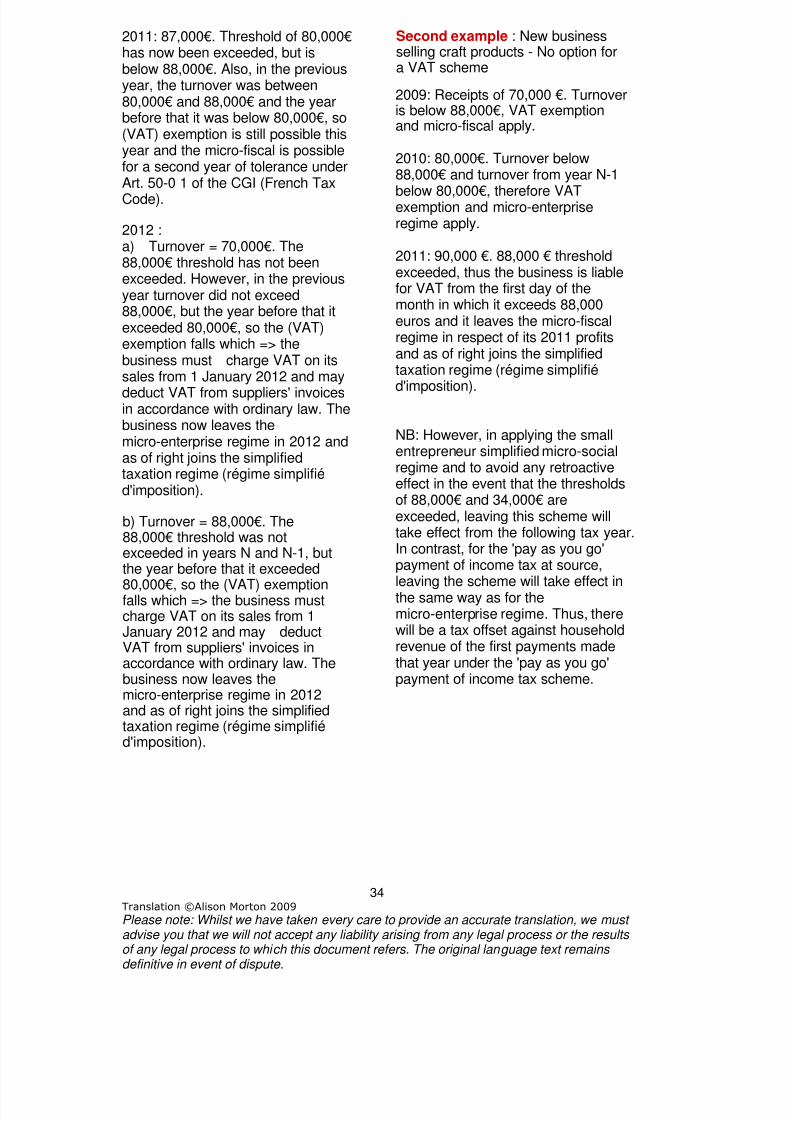

Two worked examples to illustratehow this works: These examples do not take into account any annual updating of the thresholds which will apply to turnover achieved from 1 January 2010 .

First example: New business sellingregional produce - No option for aVAT scheme.

2009: receipts of 79,000€. Turnover isbelow the limit, VAT exemption andmicro-fiscal regime applied.

2010: 82,000€. Please note! Nowabove threshold of 80,000€ but below88,000 €, however, in the previousyear, turnover was less than 80,000€which => VAT scheme exemptionapplies as does the first year oftolerance under the micro-fiscal

regime.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 35/43

34

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

2011: 87,000€. Threshold of 80,000€has now been exceeded, but isbelow 88,000€. Also, in the previousyear, the turnover was between80,000€ and 88,000€ and the yearbefore that it was below 80,000€, so(VAT) exemption is still possible thisyear and the micro-fiscal is possiblefor a second year of tolerance underArt. 50-0 1 of the CGI (French Tax

Code).

2012 :a) Turnover = 70,000€. The88,000€ threshold has not beenexceeded. However, in the previousyear turnover did not exceed88,000€, but the year before that itexceeded 80,000€, so the (VAT)exemption falls which => thebusiness must charge VAT on itssales from 1 January 2012 and may

deduct VAT from suppliers' invoicesin accordance with ordinary law. Thebusiness now leaves themicro-enterprise regime in 2012 andas of right joins the simplifiedtaxation regime (régime simplifiéd'imposition).

b) Turnover = 88,000€. The88,000€ threshold was notexceeded in years N and N-1, butthe year before that it exceeded

80,000€, so the (VAT) exemptionfalls which => the business mustcharge VAT on its sales from 1January 2012 and may deductVAT from suppliers' invoices inaccordance with ordinary law. Thebusiness now leaves themicro-enterprise regime in 2012and as of right joins the simplifiedtaxation regime (régime simplifiéd'imposition).

Second example : New businessselling craft products - No option fora VAT scheme

2009: Receipts of 70,000 €. Turnoveris below 88,000€, VAT exemptionand micro-fiscal apply.

2010: 80,000€. Turnover below88,000€ and turnover from year N-1

below 80,000€, therefore VATexemption and micro-enterpriseregime apply.

2011: 90,000 €. 88,000 € thresholdexceeded, thus the business is liablefor VAT from the first day of themonth in which it exceeds 88,000euros and it leaves the micro-fiscalregime in respect of its 2011 profitsand as of right joins the simplifiedtaxation regime (régime simplifié

d'imposition).

NB: However, in applying the smallentrepreneur simplified micro-socialregime and to avoid any retroactiveeffect in the event that the thresholdsof 88,000€ and 34,000€ areexceeded, leaving this scheme willtake effect from the following tax year.In contrast, for the 'pay as you go'payment of income tax at source,leaving the scheme will take effect inthe same way as for themicro-enterprise regime. Thus, therewill be a tax offset against householdrevenue of the first payments madethat year under the 'pay as you go'payment of income tax scheme.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 36/43

35

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Appendix II

List of professional services coming under the Caisseinterprofessionnelle de prévoyance et d'assurance vieillesse(CIPAV)As shown on the list published by CIPAV (www.cipav-retraite.fr)

[Translator’s note: The only authentic 'title' of a regulated profession is that in the original French.Any translation of this title in this document is purely indicative. Alphabetical order follows the original French; where the title is almost identical, the English only is given, e.g. Pilot ]

A Accompagnateur de groupes - Groupguide/escortAccompagnateur en moyenne montagne -Low altitude guide/escortAdministrateur provisoire étude huissier de justice - Receiver at the huissier de justice's(baliff's) office

Agent privé de recherches - PrivateresearcherAide relationnelle - Personal interlocutor oradvocateAnalyste programmeur- Analyst programmerAnimateur d'art - Art leader/organiserAnimateur-speaker - Professional speakerArchitectArchitecte d'intérieur - Interior designerArchitecte naval - Naval architectAssistant aéroportuaire (agent de sécurité,vigile) - Airport staff (security guard, etc.)Assistant social - Social assistant

Attaché de presse - Media spokespersonAuteur de mots croisés - Crossword compiler

CCapitaine expert - Cargo superintendantCaricaturist/cartoonistCartographe - Cartographer/map-makerCeramicistChargé d'enquête - Market research projectmanagerCiseleur - EngraverCoachCoach sportif - Sports coach

ColouristConcepteur - Designer/stylistConférencier - Public speaker/lecturerConseil artistique - Artistic advisorConseil commercial - Sales consultantConseil de gestion - Management consultantConseil de sociétés - Business consultant

Conseil d'entreprise - Corporate advisorConseil en brevet d'invention - Patentadvisor/agentConseil en communication -Communications consultantConseil en formation - Training advisorConseil en informatique - IT consultant

Conseil en management - ManagementconsultantConseil en marketing - Marketing consultantConseil en organisation - EfficiencyconsultantConseil en publicité - Advertising consultantConseil en relations publiques - PRconsultantConseil ergonome - Ergonomic consultantConseil financier - Financial consultantConseil littéraire - Literary consultant/agentConseil logistique - Logistics consultantConseil médical - Medical consultantConseil qualité comptable - Accountingquality consultantConseil scientifique - Scientific consultantConseil social - Social consultantConseil technique - Technical consultantCoordinatorCoordinateur de travaux - Work coordinatorCorrespondants locaux de presse - Localmedia correspondantsCréateur d'art - Creative artist

D Decorator

Décorateur conseil - Decorating consultantDécorateur ensemblier - Interiordecorator/designerDesignerDessin chirurgical - Medical illustratorDessin de bijoux - Jewellery designerDessin de publicité - Commercial artist

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 37/43

36

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Dessinateur - DraughtsmanDessinateur industriel - Industrial designerDessinateur projeteur - IndustrialdraughtsmanDessinateur technique - Technical designerDocumentaliste - Information officer/librarian

EÉducateur - Educator (often specialised)Émailleur - EnamellerEnquêteur social - Social researcherEntraîneur d'échecs - ChessmasterEntraîneur sportif - Sports trainerErgothérapeute - Occupational therapistEsthéticienne à domicile - Home-basedbeauty therapistEsthétique industrielle - Industrial designÉtalagiste - Window dresser/Display stylistÉtudes de marchés - Market researchExpertExpert agricole - Agricultural expertExpert automobiles - Vehicle expertExpert en écritures - Records and accountsentry specialist

Expert en objets d'art - Expert in works of artExpert forestier - Forestry expertExpert judiciaire - Legal expertExpert maritime - Maritime expertExpert près les tribunaux - Expert attached tothe courtExpert tarificateur - Underwriter

FFerronnier d'art - Craftsman in wrought ironFormateur - Instructor/trainer

G GeobiologistGéologue - GeologistGéomètre - Land surveyorGérant de holding - Holding companymanagerGérant de tutelle - Legal guardian for adultsGraphiste - Graphic designerGraphologue - GraphologistGuide de montagne - Mountain guideGuide touristique - Tourist guide

H HistorianHôtesse d'exposition - Event reception staff

IIngénierie informatique - IT engineerIngénieur conseil - Consultant engineerIngénieur du son - Sound engineer

Ingénieur expert - Expert engineerIngénieur informatique - IT engineerIngénieur œnologue - Expert oenologistIngénieur thermicien - Heat physicistInterpreterInventorInventorite (pharmacie) - Inventorist/stockcontroller (pharmacy* (Possible typo in original French )Investigator

JJoueur professionnel - Professional player

LLecteur - ReaderLicier - Tapestry weaver

MMaître d'œuvre - Project managerMaître-nageur - Swimming instructorManipulateur d'électrocardiologie - ECGtechnicianMaquettiste - Layout artist/model makerMédecin conseil - Consultant physicianMédiateur pénal - Criminal rehabilitation &reintegration specialistMétreur - Quantity surveyorModelModéliste - Fashion designer/pattern makerMoniteur - Instructor/councellor/coach/groupleaderMoniteur de ski - Ski instructorMoniteur de voile - Sailing instructorMosaïste - Mosaic cutter and setterMusicothérapeute - Musical therapist

NNaturalistNaturopathNoteur copiste - Music copyistNutritionist

OOsteopath

PPaysagiste - Landscaper

Peintre sur soie - Silk painterPhotographe d'art - Artistic photographerPilotPotterPrédicateur - PreacherProfesseur - Teacher/professorProfesseur de danse - Dance teacher

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 38/43

37

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Professeur de dessin - Art teacherProfesseur de langues - Language teacherProfesseur de musique - Music teacherProfesseur de sport - Games teacherProfesseur de tennis - Tennisteacher/instructorProfesseur de yoga - Yoga teacherPsychoanalystPsychologist counsellorPsychomotricien - Psychomotor therapist

Psychosociologue - Social psychologistPsychothérapeute - Psychotherapist

RRaftingRéalisateur audiovisuel - AV producerRelieur d'art - BookbinderRépétiteur - Repitition coachRestaurateur d'art - Art restorer

SScénographe - Set designer

Secrétaire à domicile - Home-basedsecretarySkipperSportsmanSténotypiste de conférence - Courtreporter/stenotype reporterStylist

T Topographe - TopographerTraducteur technique - Technical translatorTranscripteur - TranscriberTravaux acrobatiques - Acrobatic performers

U Urbaniste - Town planner

VVérificateur - Auditor/inspectorVigile - Night watchman

:3%&4;*E

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 39/43

38

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Appendix III

Guide list of business activities fully affiliated to theRSI for social security purposes and coming under the

BNC tax category

The RSI portal publishes a list of individualentrepreneurs carrying on business asskilled tradespeople, industry or commercewho are fully affiliated to the RSI for theirsocial security protection, i.e. for sicknessinsurance as well as for old age pensionpurposes. However, from a tax point ofview, some of these business activities fallinto the 'bénéfices non commerciaux' (BNC)

category. Therefore, the relevant CFE isthe URSSAF.

For these business activities, the socialcontributions rate is 21.3% and the'pay as you go' rate of income tax atsource 2.2 % , being BNC, i.e. a totalrate of 23.5%. These business activitiesconsist of the following:

− astrologers, seers and other occultsciences;

− cartomancers (fortune-tellers);− healers, magnetic healers and

bonesetters ;− market operators, as their remuneration

is calculated in proportion of the stallfees received by them and they makedeductions from these fees at the timethey pay the local authority receiptsoffice;

− commercial agents1: in general, theirincome comes under the BNC category.However, as the function of commercial

agent in respect of certain companiesdoes not exclude that of salariedrepresentative on behalf of othercompanies, or carrying out commercialtransactions on their own behalf wherethey are taxed as making industrialand commercial profits (BIC), then the

actual conditions under which thebusiness is carried on must be carefullyestablished;

− commercial and industrialintermediaries: contracts madebetween companies and their clientsare generally concluded by thebusiness through an intermediarywhose tax position, often very variable,

is directly related to their legal status orthe nature of their links which tie themto people on whose behalf they act ordeal. ln this context, the commercialrepresentative is an intermediary tied toone or several companies on whosebehalf he prospects and concludespurchases, sales or provision ofservices without personally committinghimself. 'Independent representatives'or 'mandated representatives' carry outvery similar functions to those of

commercial agents. In this respect, theyare taxed in the BNC category;− owners of driving schools: as they

operate their business either as anindividual or as a partnership, they aretaxed as BNC since they are essentiallyconcerned with running their companyby directing, coordinating andcontrolling the lessons given by theirstaff,

− while still giving some instructionthemselves, which is generally the

case;− advertising designers such as

draughtsmen and illustrators not tied toadvertising agents or to an advertiserby employment contracts (as long asthey are not advertising graphic artists

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 40/43

39

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

producing stands for fairs andexhibitions or an advertising publisher);

− casual/intermittent journalists:remuneration received due to casual orintermittent contributions to newspapersor magazines are classed as BNC;

− negotiators and property salespeople:intermediaries buying or sellingproperty or businesses frequentlyrequire the services of a negotiator toprospect clients, conduct viewings andto bring buyers and sellers to anagreement. However, in this group,differentiation should be establishedbetween:

- those who have the status ofsalaried employees: i.e. those who,while remunerated by a variablepercentage of commission paid tothe estate agency, may not makesimilar transactions on their ownbehalf nor for other agencies, nor

exercise any follow-on right inrespect of the clients found; theyare also obliged to acceptinstructions every day from theagency which reserves the rightnot to pursue or follow up anycommitments made by thesenegotiators;

- those who are tied tointermediaries (estate agenciesin this particular case) by anagency contract (principal/agent)

which allows them in particular tocarry on another business orprofession and who have thestatus of independent workerstaxed under BNC category.

Please note: this list is intended as aguide only. Eligibility to be classed asBNC tax category is based on type ofbusiness but also depends on the actualconditions under which the business

operates. If unclear about tax categories,please contact the tax authorities.

1. Law no. 91-593 dated 25 June 1991 definesthem as agents ('mandataires')who as independent

professionals not tied by a service or employmentcontract, are mandated on a permanent basis tonegotiate and, where appropriate, conclude sales,purchase, rental or service provision contracts in thename of and on behalf of businesses or othercommercial agents.

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 41/43

40

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

Appendix IV

List of trades coming under the heading ofactivities subject to professional qualificationsand standards listed in section I of Article 16 ofthe Law dated 5 July 1996 and in Law no. 46-1173

dated 23 May 1946

I. - Maintenance and repair ofvehicles and machinery: car repairer,coachbuilder (vehicle body shop),bicycle and motor bicycle repairers,repairers of agricultural, forestry andpublic works machinery &equipment.

II. - Construction, maintenance and

repair of buildings: trades relating tothe building of structures, internalfitting and finishing.

III.- Installation, maintenance andrepair of networks and fittings forfluids as well as equipment andfittings for use in supplying gas,space heating in buildings andelectrical installations: plumber,heating engineer, AC installer, andother trades installing networks andsupply lines for water, gas andelectricity.

IV.- Chimney sweeping: chimneysweep

V.- Personal beauty treatments,other than medical or paramedicaltreatments, and non-medicalbeauty remodelling treatments forpersonal well-being: beautytherapist

VI.- Production of dentalprostheses: dental technician

VII.- Preparation and production offresh food products such as bread,baked cakes and pastry, meat,cooked meats (mostly porkderivatives), fish, preparation andproduction of non-industrialice-cream: baker, pastry/cakemaker, butcher, pork

butcher/delicatessen producer,fishmonger and ice-creamproducer

VIII.- Working farrier: farrier

IX. - Hairdressing

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 42/43

41

Please note: Whilst we have taken every care to provide an accurate translation, we must advise you that we will not accept any liability arising from any legal process or the results of any legal process to which this document refers. The original language text remains definitive in event of dispute.

List of abbreviations

ACOSS Agence centrale des organismes de sécurité socialeBIC

Bénéfices industriels et commerciauxCA Chiffre d'affairesCAP Certificat d'aptitude professionnelleCIPAV Caisse interprofessionnelle de prévoyanceet d'assurance vieillesseCFE Centre de formalités des entreprisesCGI Code général des impôtsINSEE Institut national de la statistiqueet des études économiquesLME Loi de modernisation de l'économieRCS Registre du commerce et des sociétésRM Répertoire des métiersRSI Régime social des indépendantsTPE Très petites entreprisesTVA Taxe sur la valeur ajoutéeURSSAF Union de recouvrement des cotisationsde sécurité sociale et d'allocations familiales

8/4/2019 AEGuide March2009 En

http://slidepdf.com/reader/full/aeguide-march2009-en 43/43

42

6%7;% &1'#&5!)

*)1!1U') *!1%

Contact for translator: [email protected]

Related Documents

![International Patient Safety Goals-Souzan 23 March2009[1]](https://static.cupdf.com/doc/110x72/5477a851b4af9f48108b492c/international-patient-safety-goals-souzan-23-march20091.jpg)