The Biomanufacturing Capacity Conundrum: Matching Supply and

Demand Over Space and Time

Delivery and Manufacturing of BiologicsSession ID #14010:00 – 11:30 AM

June 28, 2011

Agenda Howard L. Levine, Ph.D.

• President, BioProcess Technology Consultants, Inc.• Global Trends in Biomanufacturing: Separating the Haves from the Have-nots

William J. Fallon• Vice President Manufacturing and Operations, Halozyme Therapeutics, Inc.• Customer Perspective on Capacity Challenges and Needs

Roger Lias, Ph.D.• President, Eden Biodesign, Inc.• Acquisitions, Biosimilars, and CMO Consolidation: Food for Thought When

Planning for Long Term Biomanufacturing Requirements Parrish Galliher

• Founder and Chief Technology Office, Xcellerex, Inc.• The Biomanufacturing Capacity Conundrum: How to Manage Uncertainty of

Manufacturing Demand

BioProcess Technology Consultantswww.bptc.com

Global Trends in Biomanufacturing: Separating the Haves from the Have-nots

Howard L. Levine, Ph.D.President and Principal ConsultantBIO 2011 International ConventionWashington, DCJune 27 – 29, 2011

From Clone to Commercial®

Increasing Sales of Biopharmaceutical Products

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2010 2011 2012 2013 2014 2015 2016

Total D

emand (Kg/Year)

Year

Commercial BLA/NDA Phase 3Phase 2 Phase 1 Clincial

0125250375500625750875

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Sales ($B

)

YearBiopharmaceuticalsTraditional Pharmaceuticals

From Clone to Commercial®

Volumetric Capacity Requirements Double by 2016

0

550

1,100

1,650

2,200

2,750

2009 2010 2011 2012 2013 2014 2015 2016

Volume Re

quire

d (KL/Yr)

Year

Commercial BLA Phase 3 Phase 2 Phase 1 Clinical

From Clone to Commercial®

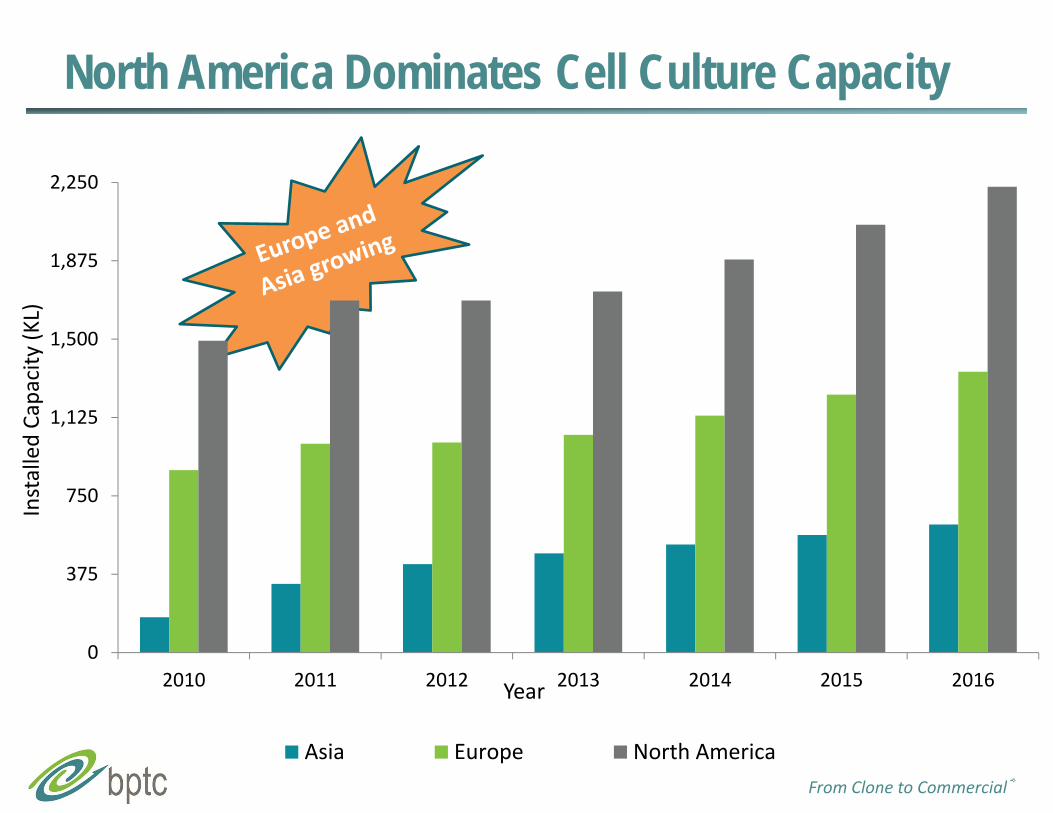

North America Dominates Cell Culture Capacity

0

375

750

1,125

1,500

1,875

2,250

2010 2011 2012 2013 2014 2015 2016

Installed Capacity (K

L)

Year

Asia Europe North America

From Clone to Commercial®

Product Companies Control >65% of Capacity

0

900

1,800

2,700

3,600

4,500

2010 2011 2012 2013 2014 2015 2016

Total Vo

lume (KL)

Year

CMO Both Product Co.

From Clone to Commercial®

AmgenBiogen Idec

BI

Sanofi

J&J

Lilly

Lonza

PfizerRoche

All Others

Celltrion

Ten Companies Control >75% of CapacityAmgen

Biogen Idec

BI

Sanofi

J&J

Lilly

LonzaPfizer

Roche

All Others

BMS

2011

2016

From Clone to Commercial®

CMO Capacity Predominately at <10,000 L

0

5

10

15

20

25

30

<1,000 L 1,000 < 10,000 L 10,000 < 100,000 L >100,000 L

No. Com

panies

Total Volume (L)

Product (2010) Both (2010) CMO (2010) Product (2016) Both (2016) CMO (2016)

From Clone to Commercial®

Capacity Utilization Grows to 65% by 2016

0

700

1,400

2,100

2,800

3,500

4,200

2009 2010 2011 2012 2013 2014 2015 2016

Volume Re

quire

d (KL/Yr)

YearCommercial Clinical BLA Phase 3 Phase 2

Phase 1 Available Capacity Drivers Pass Drivers Fail Most Probable

Assumes no increase in current titers

From Clone to Commercial®

Capacity Utilization at Top 5 Product CompaniesReaches 50% by 2016

0

400

800

1,200

1,600

2,000

2009 2010 2011 2012 2013 2014 2015 2016

Installed Capacity (K

L)

YearCommercial Clinical BLAPhase 3 Phase 2 Phase 1Available Capacity

44% 43% 43% 48% 49% 52% 50% 47%

Includes Sanofi, Roche, Amgen, J&J, Pfizer

From Clone to Commercial®

Utilization Pushes 75% for the Rest of the Industry

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014 2015 2016

Installed Capacity (K

L)

Year

Commercial Clinical BLA Phase 3 Phase 2 Phase 1 Available Capacity

32% 40% 37% 58%45% 74%72% 75%

From Clone to Commercial®

Trends That Will Impact Future Capacity Utilization Success or failure of a limited number of high volume products currently in

late stage clinical development• Acquisition of “volume driver” product candidates by product

companies having significant capacity may free up CMO capacity Mergers and acquisitions, resulting in redundant facilities

• Companies moth‐balling or not starting up facilities due to excess capacity include Pfizer, Roche, Amgen, Lilly, and others…

Personalized medicine will put greater focus on smaller markets and niche products• Fewer “blockbuster” drugs with high volume demand

Introduction of biosimilars will result in wider demand for capacity but not necessarily an increase in industry‐wide demand

Increases in process productivity and overall facility utilization…• 2X increase in productivity will reduce overall capacity requirements by

approximately 25% by 2013

From Clone to Commercial®

Increases in Titer and Facility Utilization…Lowers Demand for Capacity

20092010201120122013201420152016

0

600

1,200

1,800

2,400

3,000

3,600

4,200

0.5x 1x 1.5x 2x

Volume Re

quire

ments (K

L)

Titer Increase

20092010201120122013201420152016

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.5x 1x 1.5x 2x

Capacity Utiliza

tion (%

)

Titer Increase

From Clone to Commercial®

Manufacturing Facilities of the Future

Designed for modern, state‐of‐the art processes• Cell culture titers of titer >5 g/L• Platform purification with overall yields of >70%

Expanded use of single‐use and disposable technologies to reduce capital investment and operating costs

Incorporate greater DSP space and capabilities• Ratio of USP to DSP space will decrease

Smaller bioreactors to produce similar quantities to today’s facilities• Reduced capital requirements may enable smaller companies to

construct their own facilities rather than outsource

Thank You!

BioProcess Technology Consultants, Inc.12 Gill Street, Suite 5450Woburn, MA 01801

+1.781.281.2703

Howard L. Levine, Ph.D.

Customer Perspective on Capacity Challenges and Needs

William J. FallonVP, Manufacturing & Operations

Halozyme Therapeutics, Inc.

Case Study: Halozyme Therapeutics, Inc.• Mid-Size biotechnology company

•~100 employees•Founded 1998•Listed on NASDAQ (HALO)

•~$650M Market Cap•Develops products based on biology of extracellular matrix

•Drug delivery•Route of administration change

•Endocrinology•Diabetes

•Oncology•Solid tumors

•Dermatology•Commercial and clinical products

San Diego, CA

Development Strategy has Three Anchors

• First platform technology (Enhanze™)•Recombinant human hyaluronidase (rHuPH20, PH20)•Supplied to partners under collaboration agreements

•Roche, Baxter, ViroPharma, Intrexon•Development of proprietary therapeutics

•PH20-Insulin formulations•PEGPH20•rHu-cathepsin-L

•Commercial Products•HYLENEX®

•Cumulase™

Halozyme’s Manufacturing Strategy•Process, product, analytical development performed in-house•Produce materials to support internal/partner development efforts including preclinical

•Utilize lab/pilot scale facilities•Outsource all cGMP manufacturing/testing

•2 drug substance CMOs•Clinical/commercial

•3 drug product CMOs•1 clinical, 2 commercial

•Multiple analytical testing labs•Focus on technology transfer and technical/quality oversight of third party operations

Critical Manufacturing Needs (Bulk DS)• Access to flexible capacity

•Low volume for clinical stage products•100’s L/yr (sporadic demand)

•Larger volume for commercial/partnered products•50,000+ L/Yr (demand forecast driven)

•Standard process technology = portability•Stirred tank bioreactors, column chromatography, filtration•Ability to transfer technology to multiple sites

•Not encumbered with CMO IP•Costs: Modest start-up fees and low COGS

Manufacturing Capacity Challenges• Access to suitable capacity (clinical/commercial)

•Better now than 5+ years ago•More clinical stage CMOs available to work with smaller companies

•Lack of experience (operations, regulatory) can pose risks•Larger, established CMOs willing to work with smaller companies

•Cost and flexibility can be issues•Multiple sites needed for supply assurance

•Avoid IP barriers•Costs

•High start-up costs/time (mitigated by disposables technology)•Reducing/optimizing COGS (productivity and yield improvements)

Summary Observations• Access to suitable capacity (clinical/commercial) currently exists for volumes in the range of up to ~50,000 L/yr

•Plan on lead time of 6-9 months for confirmed slots•Recent purchases by CMOs of product company approved commercial facilities provides for new capacity opportunities

• CMOs typically allow for portability of processes•Care must be taken to avoid IP or non-standard process technologies

• Use of disposable equipment can reduce initial capital costs, validation costs and minimize lead time to production

•Although it does increase materials cost• Productivity improvements and process yield optimization remain primary mechanism for reducing COGS

Thank You

William J. FallonVP, Manufacturing & Operations

Halozyme Therapeutics, Inc.

AcquisitionsBiosimilars andCMO Consolidation

Food for Thought When Planning for Long Term Biomanufacturing Requirements

Roger Lias, Ph.D.President, Eden Biodesign, Inc.

A Watson Group Company

It’s Far More Complex Than “Available Liters”………• “Available capacity” is not necessarily:

• A good technical/process fit for your product• A good strategic fit for your company• Going to be available over the life of your project• Going to be available to you!

• Biopharmaceutical manufacturing capacity tends to change hands

• There is instability in the biopharmaceutical contract manufacturing market

• Biosimilars will impact available capacity….…..but how?

Eden Biodesign

• Founded in 2000 as a consultancy• Awarded bid to run UK’s National Biomanufacturing Centre in 2003• Licensed cGMP manufacturing facility in Liverpool, UK• Until January 2010 an independent private company offering process

development and cGMP manufacturing services to the global market• Mammalian cell culture; microbial fermentation; viral production platforms

• Acquired by Watson Pharmaceuticals (NYSE: WPI) in January 2010• Now designated as Watson’s “Center of Excellence for Biologics”• Continuing significant legacy third party projects, but no longer

seeking new “fee-for-service” clients• Formally withdrawing from the biopharmaceutical contract

manufacturing market at this event.

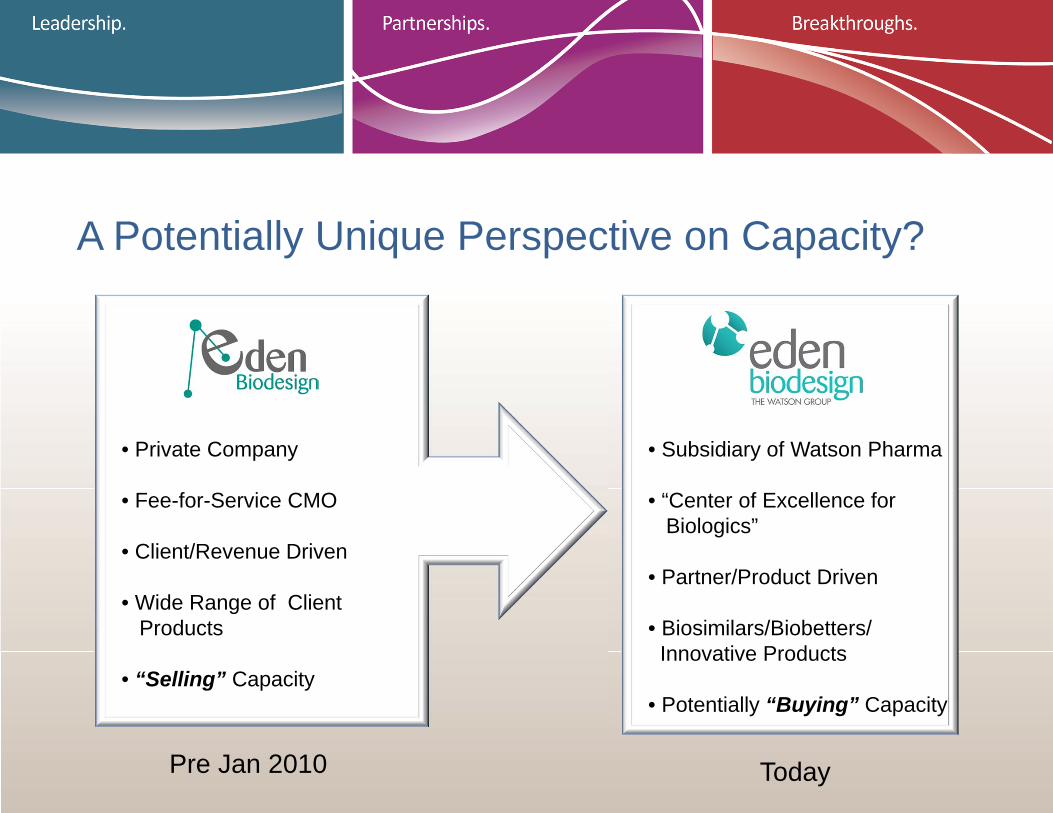

A Potentially Unique Perspective on Capacity?

F

Pre Jan 2010 Today

• Private Company

• Fee-for-Service CMO

• Client/Revenue Driven

• Wide Range of Client Products

• “Selling” Capacity

• Subsidiary of Watson Pharma

• “Center of Excellence for Biologics”

• Partner/Product Driven

• Biosimilars/Biobetters/Innovative Products

• Potentially “Buying” Capacity

Watson’s Center of Excellence for Biologics

• Cell Line Development/Banking/Storage• Process & Analytical Development• cGMP Manufacturing from Licensed Facility (Liverpool, UK)• Project/Alliance Management• Regulatory

• Clinical Development• Legal/IP• Distribution• Commercialisation

Capacity Planning Options• Build Capacity• Buy Capacity• Partner• Outsource

• Traditional CMO • Excess Capacity Provider

………………..Historically and currently a “volatile” marketplace

Change and Consolidation in the CMO & “Excess Capacity” Space• A “tough market” in recent years

Out of Business

• Fewer “standalone” independent CMOs

• Consolidation & change

“Excess Capacity Players”

• Clinical failures & pipeline uncertainty mean that “excess capacity” can become available because of “over build”, but the world changes quickly!

Offered capacity but now needed for internal projects

Still offer contract manufacturing services

Freemont facility to Boehringer Ingelheim…………… ?

The Potential Impact of Biosimilars

• Huge current international interest in biosimilars• Improving EU market and potential US market opening• Many products currently in development

• Significant investment in cGMP manufacturing infrastructure by biosimilar players• India, China, Korea, Eastern Europe• E.g. 2009 Samsung announcement of $389 million investment in biosimilars

and 2011 announcement of $266 million partnership with Quintiles Transnational to develop biomanufacturing infrastructure that will be offered on a contract basis (30,000L of cell culture capacity planned).

But……• Rumors of Celltrion pulling out of contract manufacturing space to focus on

biosimilar portfolio (partnered with Hospira)

Biosimilar Impact….. Supply or Demand?

• How many biosimilar products will make it to market in highly regulated markets and what will penetration be?• Improved productivity over innovator targets?• Demand = only a percentage of innovator capacity requirements• Essentially “replacement capacity” – may even free-up capacity at innovator?

• Likely biosimilar major players (presumably) have capacity secured • E.g. Sandoz (in-house); Teva/Lonza; Hospira/Celltrion; Pfizer? Merck?

• Will facilities currently being built by global biosimilar players become broadly available?• Designed for supply to highly regulated markets or to serve domestic markets?• Appropriate quality standards?• Success of biosimilar portfolio?• Made available to third parties?

Observations For Discussion• Clinical scale cGMP capacity remains “broadly available” via CMOs

• Availability of disposable technologies; platform processes and a maturing pool of expertise makes in-house cGMP infrastructure investment more attractive

• Large scale capacity remains available from CMO majors, who continue to make market-driven investment in manufacturing infrastructure• E.g. Lonza, Boehringer Ingelheim

• “Excess capacity providers” continue to make capacity available• But careful long term planning required to ensure future and long-term availability. • May require unconventional relationships to secure capacity over the long term.• Improving process titers may continue to “release” capacity

• Significant international investments in cGMP infrastructure (esp. in Asia) –driven, in part, by biosimilars. Impact to be determined……

• Will it become available?• Appropriate quality for highly regulated markets?

The Biomanufacturing Capacity Conundrum: How to Manage Uncertainty of Manufacturing Demand

Parrish M. GalliherXcellerex. Inc.

The Problem: Uncertainty of Mfg. DemandIndustry trends that increase capacity demands:• more drug companies• more drugs in pipeline• blockbuster drugs• fewer large facilities being built

Industry trends that decrease capacity demands:• fewer blockbusters• higher titers• more potent drugs• niche markets

What can a manufacturer do to plan for demand uncertainty ?

Future Kg demand/Biologic is decreasing:single use becomes commercial scale

Time

Man

ufac

turin

g Sc

ale

Smaller markets Improved

potencyImprovingtiter / yields

Single Use Scale

Stainless steel scale

2000L

20,000L

20L

Traditional Stainless Steel Facilities Too Inflexible, Slow and Costly for Capacity Uncertainty

• Prohibitive cost to build new mfg. capacity… $1500-2,000/sq ft

• $200-$400M total installed capital cost

• 4 year timeline for new capacity

• Risk of committing capital during early high-risk stage

• Expensive to operate and modify

• Limited long-term asset utilization

• Low terminal value (even lower in today’s disposable environment)

• Many are obsolete before they are validated

Previous Drivers for Drug Development Ignored Capacity Uncertainty

ScheduleCost

Quality

New Drivers for Capacity Uncertainty

Speed

Flexibility

- Higher titers- More potent drugs- Excess capacity

Asian competitionBiosimilars

- 90% drugs fail in clinic- Fewer blockbusters- Consolidation

Quality

Cost

100% StainlessFixed Systems,Single Product

New Manufacturing Tools for Capacity Uncertainty

1980’s

100% StainlessFixed Systems,Multi-Product

Mid 90s

TODAYIntegrated, single use

modular, portable FlexFactories

SS Systems,Disposables for Media, Buffers

2002

Many Flexible, Proven Single Use Components

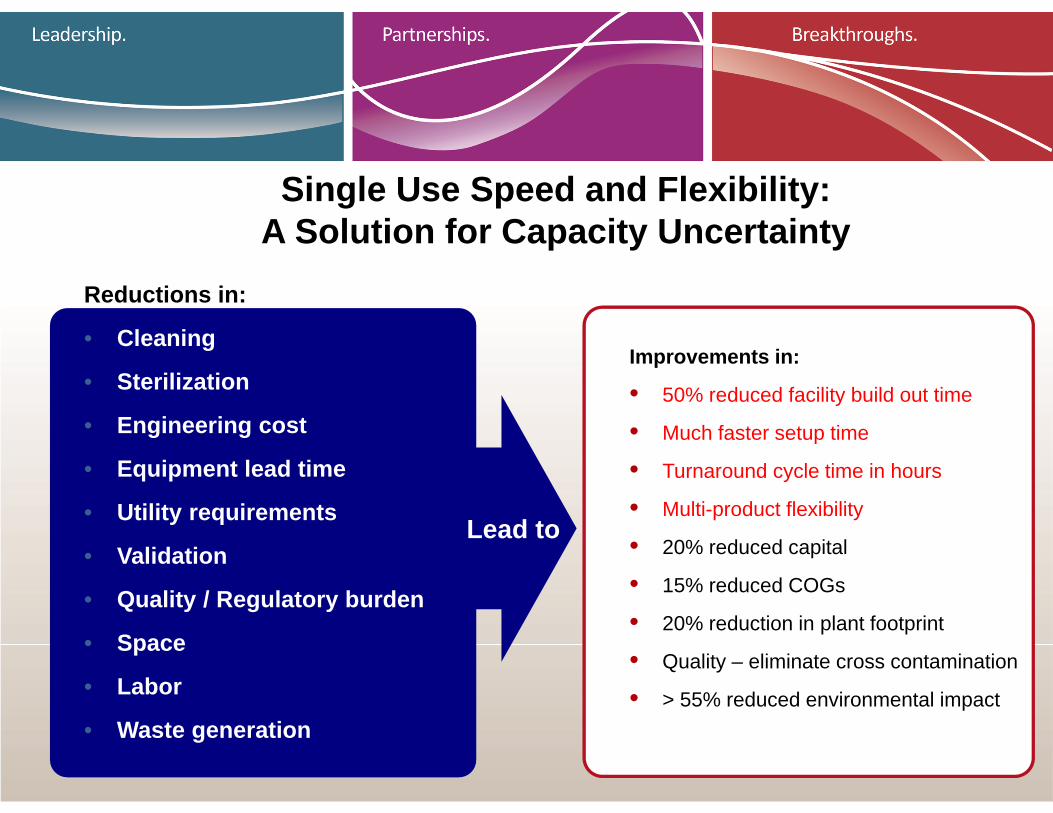

Reductions in:

• Cleaning

• Sterilization

• Engineering cost

• Equipment lead time

• Utility requirements

• Validation

• Quality / Regulatory burden

• Space

• Labor

• Waste generation

Single Use Speed and Flexibility: A Solution for Capacity Uncertainty

Lead to

Improvements in:

• 50% reduced facility build out time

• Much faster setup time

• Turnaround cycle time in hours

• Multi-product flexibility

• 20% reduced capital

• 15% reduced COGs

• 20% reduction in plant footprint

• Quality – eliminate cross contamination

• > 55% reduced environmental impact

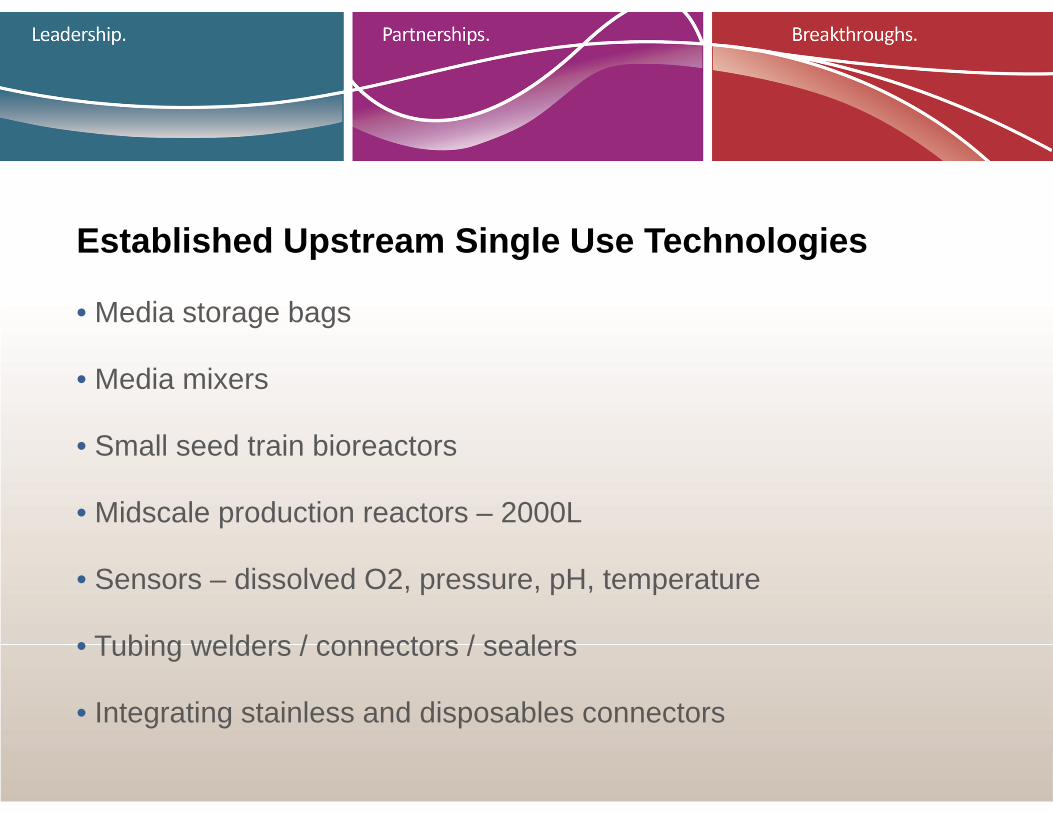

• Media storage bags

• Media mixers

• Small seed train bioreactors

• Midscale production reactors – 2000L

• Sensors – dissolved O2, pressure, pH, temperature

• Tubing welders / connectors / sealers

• Integrating stainless and disposables connectors

Established Upstream Single Use Technologies

Established and New Downstream Single Use Technologies

Established SU technologies• Buffer storage bags• Buffer mixers• Product storage bags• Sensors – pressure, pH, conductivity• Separations – limited to filtration:

• Cell harvest• Virus removal / sterilization• Concentration / buffer exchange

• Purification – membranes • Tubing welders / connectors / sealers• Integrating stainless and disposables

connectors

New SU Technologies

• SU Single Pass UF/DF

• Expanded bed columns

• Pre-packed columns

• Simulated moving bedColumns

• SU sensors: UV, flow

Single Use , High Speed, Flexible Manufacturing

FlexFactory: Fully IntegratedDisposable GMP Manufacturing

2000L GMP FlexFactory #2 at Xcellerex

9 months to GMP validated operations