BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014, 11:00 a.m. (CEST)

Ludwigshafen

Analyst Conference Call Script (Full Version)

Kurt Bock Hans-Ulrich Engel

The spoken word applies.

Third Quarter 2014

Financial highlightsOctober 24, 2014

BASF with higher sales and earnings despite declining demand

Page 2

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Cautionary note regarding forward-looking statements

This presentation may contain forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. Forward-looking statements may include, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand. BASF has based these forward-looking statements on its views and assumptions with respect to future events and financial performance. Actual financial performance could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements. The information contained in this presentation is subject to change without notice and BASF does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

2BASF Q3 2014 Analyst Conference Call October 24, 2014

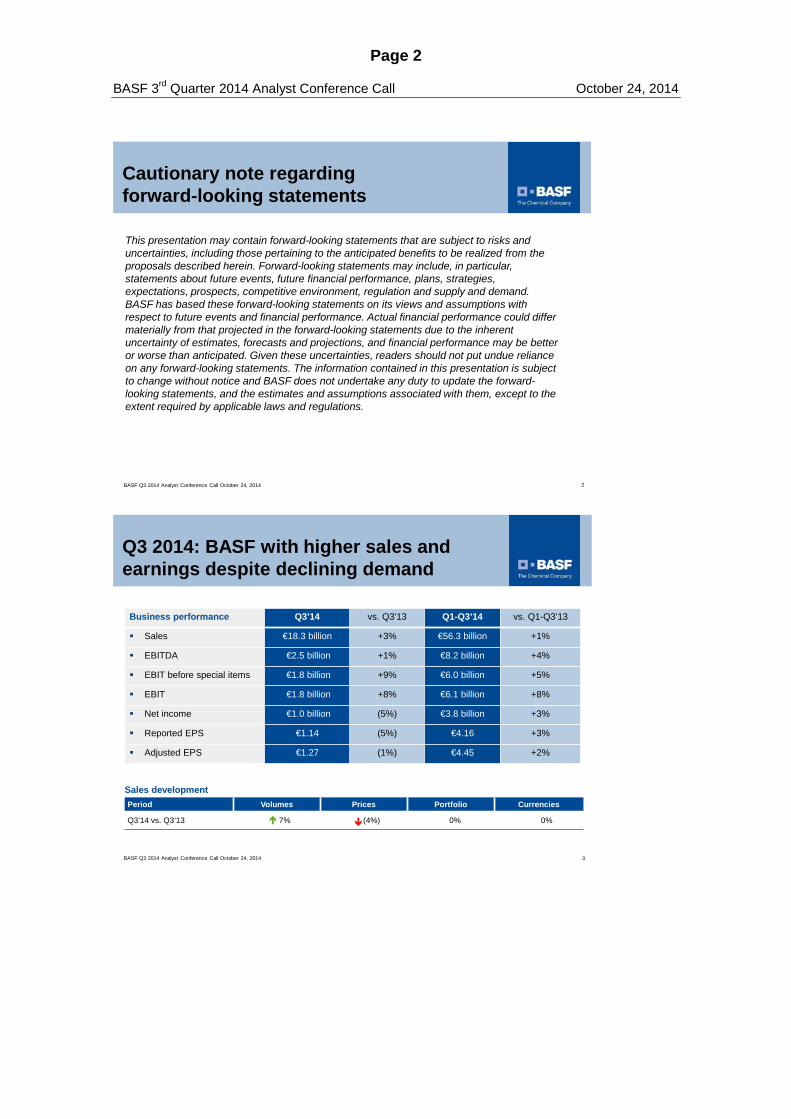

Q3 2014: BASF with higher sales and earnings despite declining demand

Sales developmentPeriod Volumes Prices Portfolio Currencies

Q3’14 vs. Q3’13 7% (4%) 0% 0%

3

Business performance Q3’14 vs. Q3’13 Q1-Q3’14 vs. Q1-Q3’13

Sales €18.3 billion +3% €56.3 billion +1%

EBITDA €2.5 billion +1% €8.2 billion +4%

EBIT before special items €1.8 billion +9% €6.0 billion +5%

EBIT €1.8 billion +8% €6.1 billion +8%

Net income €1.0 billion (5%) €3.8 billion +3%

Reported EPS €1.14 (5%) €4.16 +3%

Adjusted EPS €1.27 (1%) €4.45 +2%

BASF Q3 2014 Analyst Conference Call October 24, 2014

Page 3

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Kurt Bock

Ladies and Gentlemen, good morning and thank you for joining us.

Today we will present to you our Q3 results, which are solid amidst

a noticeable weakening of markets especially in Europe. We will

also brief you on our preliminary view on 2015. As promised to you

earlier this year we will update you on how we see our strategic

targets in view of the current economic environment. Let’s start with

Q3:

[Chart 3: Q3 2014: BASF with higher sales and earnings despite declining demand]

BASF operated in an increasingly challenging environment in the

third quarter. Geopolitical tensions and an elevated level of

uncertainty surrounding the global macroeconomic development

significantly affected demand in the chemical markets. Especially

in the Euro-zone macro indicators started to turn negative. The

ongoing tensions between Russia and the Ukraine directly

impacted the economy in these two countries and business

sentiment in the region.

In Latin America, Brazil is technically in a recession, after two

consecutive quarters of negative GDP growth. On the positive

side, North American GDP continued to expand somewhat faster

than expected. In China the impact of economic stimuli weakened

and recovery in Japan was modest. The oil price was impacted by

weaker demand as well as dampened growth expectations. On a

Page 4

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

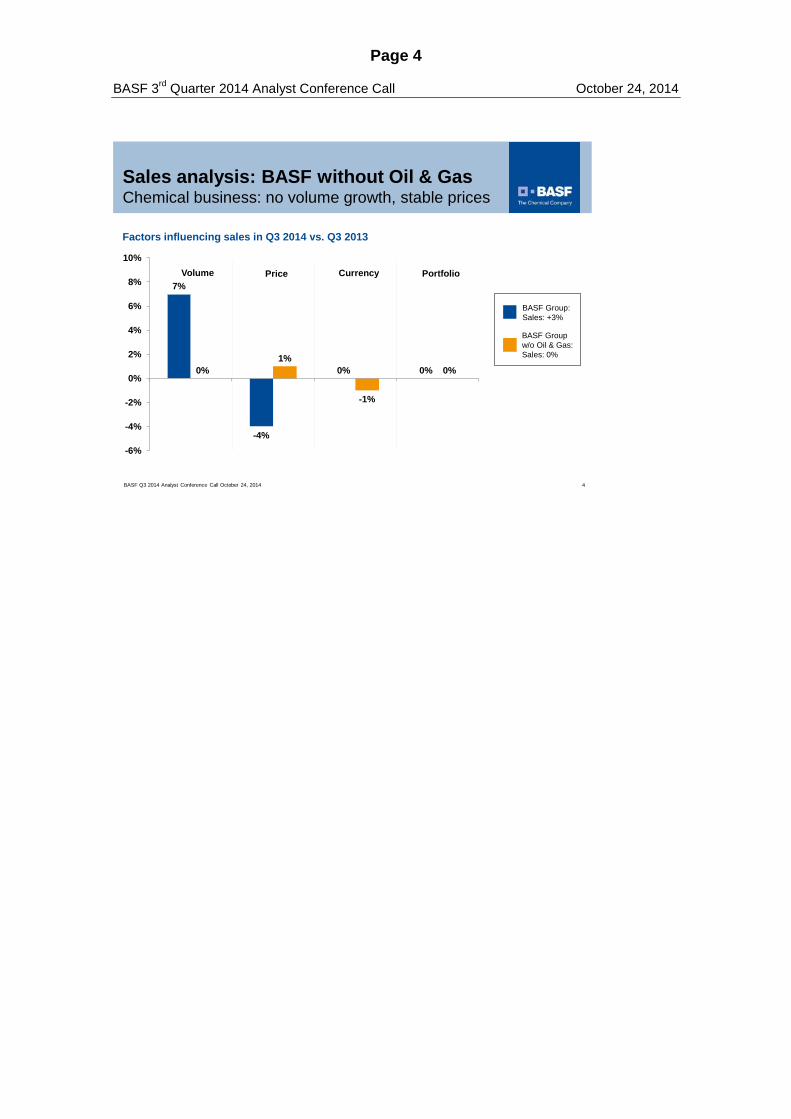

Sales analysis: BASF without Oil & Gas Chemical business: no volume growth, stable prices

7%

-4%

0% 0%0%1%

-1%

0%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Factors influencing sales in Q3 2014 vs. Q3 2013

Price Currency PortfolioVolume

BASF Group: Sales: +3%

BASF Group w/o Oil & Gas:Sales: 0%

BASF Q3 2014 Analyst Conference Call October 24, 2014 4

Page 5

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

euro basis, the average price for Brent crude oil was 8 percent

lower than in Q3 2013.

In Q3, BASF generated sales of 18.3 billion euros, up 3 percent.

Volumes grew by 7 percent driven by higher gas trading volumes.

On a Group level, prices were down 4 percent, but contrary to

previous quarters we experienced no negative currency effects.

To better understand what happened in Q3 we should take a

closer look at our price-volume-currency development (slide 4).

Without Oil & Gas we saw no volume growth globally; in Europe

BASF’s sales even declined by 4 percent. However, we were able

to maintain our prices overall and therefore also margins.

Currency has lost its negative impact, however, did not yet

provide tailwind in Q3.

EBITDA came in 1 percent higher at 2.5 billion euros.

EBIT before special items increased by 9 percent to 1.8 billion

euros, supported by considerably higher earnings in Chemicals

and Oil & Gas. We saw a slight increase in Functional Materials &

Solutions and stable earnings in Performance Products.

Agricultural Solutions reported a strong earnings decrease due to

lower volumes and higher fixed costs.

EBIT before special items in Other improved significantly. The

share price development led to the dissolution of provisions for

our long-term incentive program.

BASF recognized special items in EBIT of minus 32 million euros.

This was partially related to restructuring measures especially in

Performance Products.

Page 6

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Page 7

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

EBIT amounted to 1.8 billion euros, an increase of 8 percent

versus prior year.

The tax rate was at 28.3 percent compared to 23.1 percent in the

third quarter of 2013. In the prior-year quarter, the tax-rate was

affected by a tax-free one-time gain from the divestment of the 15

percent stake in the Norwegian Edvard Grieg field.

Net income decreased by 5 percent to 1 billion euros.

At 1.27 euros, adjusted earnings per share were at last year’s

level (Q3 2013: 1.28 euros).

In Q3, operating cash flow reached 2.1 billion euros, an increase

of around 170 million euros.

Free cash flow slightly increased to 820 million euros despite

higher capex.

Page 8

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

BASF Q3 2014 Analyst Conference Call October 24, 2014

Recent transaction with Statoil

Acquisition of participations in oil & gas fields in Norway

Purchase price amounts to US$1.25 billion

Increase of production to ~60,000 boepd in Norway

Additional reserves andresources of ~170 millionboe

Restructuring of Performance Products

Strengthening of R&D platforms

Important corporate developments

5

BASF to sell textile chemicals business toArchroma

Paper Chemicals division to be dissolved, product lines moved to other divisions

Strategic options for parts of kaolin business in evaluation

Total earnings improvement of ~€500 million by 2017

Future set up of global research platforms:

- Process Research & Chemical Engineering, led out of Europe

- Bioscience Research, led out of North America (from 2015)

- Advanced Materials & Systems Research, led out of Asia (from 2016)

Page 9

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 5: Important corporate developments]

We continue to take measures directed at further improving our

portfolio and strengthening earnings. Let me highlight some of the

most important developments since Q2 reporting.

On September 12, 2014 we announced an agreement with Statoil

of Norway that will strengthen our partnership and enhance

BASF’s earnings and cash flow generation in our core region

Europe. Reserves and resources will rise by approximately 170

million barrels of oil equivalent, and our production in Norway will

increase from currently around 40,000 boe/day to about 60,000

boe/day. The purchase price for the assets amounts to 1.25 billion

US dollars. Closing is expected by the end of 2014, with the

effective date of January 1, 2014.

We continue to restructure our Performance Products segment.

Four weeks ago, we published our plan to dissolve the Paper

Chemicals division. The structural changes in the market for

graphical paper require further adjustments to our positioning: We

aim to enhance value chain synergies by combining the main

product lines with the corresponding operations in our

Performance Chemicals and Dispersions & Pigments divisions.

These changes will be effective from January 1, 2015.

Furthermore, we are evaluating strategic options for parts of our

kaolin business. This adjustment allows to further optimize our

asset base while maintaining our commitment to the paper

industry.

As announced just last week, we have agreed to sell our global

textile chemicals business to Archroma. The parties have agreed

Page 10

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Page 11

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

not to disclose financial details. Closing is expected to take place

in the first quarter of 2015.

Before we come to the business performance of our segments, let

me briefly inform you about the next step that we will take to

enhance BASF’s innovation power. We are developing the

organization of our research platforms and will bundle

competencies, further globalize research and thereby strengthen

our worldwide R&D Verbund. The new organization will be based

on three global platforms starting January 2015:

Our Process Research & Chemical Engineering will

continue to be headquartered in Ludwigshafen.

Our Biosciences Research will be managed from

Research Triangle Park, North Carolina.

And finally, the headquarters of Advanced Materials &

Systems Research will be moved to our Innovation

Campus Asia Pacific in Shanghai by 2016.

These measures will strengthen our network with research

partners and customers and make BASF’s R&D even more

effective and efficient.

With this I hand it over to Hans.

Page 12

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

ChemicalsEarnings growth despite flat volumes

diates Monomers 1,587

(1%)

Petrochemicals1,913

(1%)

€4,201 (1%)

development Volumes Prices Portfolio Currencies

vs. Q3’13 0% (1%) 0% 0%

6

527 510601 570 616

0

200

400

600

800

Q3 Q4 Q1 Q2 Q3

20142013

Page 13

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 6: Chemicals – Earnings growth despite flat volumes]

Sales in the Chemicals segment were on prior-year level, with

overall flat volumes and slightly lower prices. Higher earnings in

Petrochemicals driven by strong profitability in the cracker business

were partly offset by lower results in Monomers, especially in Asia.

EBIT before special items came in considerably higher.

Sales in Petrochemicals reached the level of the prior-year

quarter, on higher prices but lower volumes. Our North American

business benefitted from the expansion of the refitted Port Arthur

cracker. In Europe, the ongoing outage at our Ellba joint venture

with Shell in Moerdijk led to a sales decrease. In acrylics, volumes

remained on a high level globally, but prices were under pressure

especially in Asia Pacific. EBIT before special items came in

considerably higher due to the strong performance of our cracker

products in North America and Europe.

Sales in Monomers also were on prior year’s level. We

experienced higher volumes in MDI and polyamides. Volumes in

polyols were lower due to the outage at Moerdijk. Margins for

caprolactam remained on a low level, while for isocyanates they

came under significant pressure in Asia Pacific. EBIT before

special items decreased considerably.

In Intermediates sales reached the level of the prior-year third

quarter. The seasonal slowdown in most standard products was

more pronounced than usual, but high-margin specialties sold

well. EBIT before special items was up considerably, supported

by fixed cost reductions.

Page 14

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

PerformanceChemicals

847

+3%

hemicals

€3,919 (1%)

hemicals

n h

Dispersions& Pigments

1,003

0%

development Volumes Prices Portfolio Currencies

s. Q3’13 0% 0% 0% (1%)

376

216

427 435376

0

200

400

600

Q3 Q4 Q1 Q2 Q3

7

20142013

Page 15

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 7: Performance Products: Sales and earnings stability during restructuring]

In Performance Products sales were almost unchanged. Volumes

and prices were flat but we faced slightly negative currency effects.

EBIT before special items came in on prior-year level, benefitting

from strict fixed cost control. The ongoing restructuring measures

resulted in negative special items of 10 million euros.

Sales in Dispersions & Pigments were stable. In Europe

demand slowed, whereas in Asia Pacific we experienced good

volume growth across most product groups. Total volumes came

in slightly higher and prices were stable. EBIT before special

items increased slightly due to lower fixed costs related to the

successful implementation of our restructuring program.

In Care Chemicals, sales were flat on lower volumes but higher

prices. Especially volumes in hygiene were down due to

aggressive competition and better product availability. In Q3 2013,

the market was tight due to the outage of a competitor’s SAP

plant. Personal care specialties also saw a decrease in demand.

EBIT before special items went slightly down.

Sales in Nutrition & Health came in slightly lower. We saw higher

demand for animal nutrition as well as aroma chemicals, but faced

tough competition in human nutrition and pharma. Prices

remained stable. The market environment for vitamins remained

very competitive. EBIT before special items decreased slightly.

Sales in Paper Chemicals decreased significantly driven by

declining demand in the graphical paper market. Our fixed cost

Page 16

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Page 17

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

reduction measures helped to maintain EBIT before special items

on prior-year level.

Performance Chemicals sales were up slightly, driven by

significantly higher volumes in most of our businesses. Demand

for fuel & lubricant solutions increased globally. Oilfield & mining

solutions also developed positively. We experienced good

demand for water solutions but competitive pressure remained

high. We faced slightly lower prices and incurred portfolio effects

related to the divestiture of our PolyAd business. EBIT before

special items slightly increased.

Page 18

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Functional Materials & SolutionsContinued robust demand from automotive

ts

ConstructionChemicals

565

(2%)

Coatings736

+1%

€4,527+2%

development Volumes Prices Portfolio Currencies

s. Q3’13 1% 2% 0% (1%)

mance ls

300238

311356

310

0

200

400

Q3 Q4 Q1 Q2 Q3

8

20142013

Page 19

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 8: Functional Materials & Solutions – Continued robust demand from automotive]

In Functional Materials & Solutions, sales were up slightly,

supported by continued robust demand from the automotive

industry. We realized higher volumes and prices, but still faced

negative currency effects in all divisions. EBIT before special items

slightly increased due to higher contributions from Coatings and

Catalysts.

Sales in Catalysts increased significantly on higher volumes and

prices. Volume growth was driven by high demand from mobile

emission and chemical catalysts. Sales from precious metals

trading grew to 685 million euros versus 657 million euros a year

ago. EBIT before special items considerably increased driven by

higher volumes.

In Construction Chemicals sales came in slightly lower, as

higher volumes and prices could only partially compensate the

structural effect related to the divestment of our German wall

systems business in Q4 2013. While we experienced a positive

business development in North America, demand in most

European countries was subdued. Fixed cost reductions from our

efficiency program resulted in a slight improvement of EBIT

before special items.

Sales of our Coatings division were slightly up due to higher

prices. For OEM coatings and refinish coatings we saw good

demand in Europe and North America, robust business in Asia

Pacific and a decline in volumes in South America.

Page 20

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Page 21

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Industrial coatings developed very positively due to better

business with coil and wind energy coatings. Sales in decorative

paints slightly decreased, as higher prices could not fully offset

lower volumes. EBIT before special items was up considerably

supported by effective fixed cost control.

Sales in the Performance Materials division were stable with

volumes being flat. Engineering plastics and our specialties such

as Cellasto and Ultrason developed positively due to high

demand from the transportation industry. PU systems, however,

saw lower demand for appliances and construction applications,

especially in Europe. Prices were slightly down. Plant start-ups

and higher R&D expenses led to an increase in fixed costs and

EBIT before special items decreased significantly.

Page 22

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Agricultural SolutionsStrong earnings decline in seasonally slow quarter

9BASF Q3 2014 Analyst Conference Call October 24, 2014

Q3’14 segment sales (million €) vs. Q3’13

Sales development Period Volumes Prices Portfolio Currencies

Q3’14 vs. Q3’13 (4%) 2% 0% (1%)

0

100

200

Q3 Q30

300

600

900

1,200

Q3 Q3

1,018(3%)

43

(75%)

1721,054

20142013 20142013

Page 23

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 9: Agricultural Solutions – Strong earnings decline in seasonally slow quarter]

In Agricultural Solutions we experienced a disappointing business

in this seasonally slow quarter. Excellent crop conditions led to good

harvests for key crops globally, strongly pushing down crop

commodity prices. Our sales decreased by 3 percent versus the

very strong prior-year quarter, mainly due to lower volumes in North

America and Europe. Nevertheless, we were able to increase prices

in all regions.

Business in Europe declined considerably. Lower prices for

oilseed rape led to reduced acreage and consequently demand

for oilseed herbicides declined.

In North America sales dropped significantly, as excellent crop

conditions and low commodity prices adversely impacted demand

especially for our yield-boosting Plant Health products.

Sales in South America were slightly up, supported by higher

volumes and prices. Our recent launches Kixor® and Xemium®

developed well, while there was tough competition in insecticides.

In Asia Pacific sales slightly increased, thanks to higher prices

across the region.

EBIT before special items in Q3 2014 fell considerably on lower

volumes, a less favorable product mix and higher fixed costs. For

the remainder of the year we see business momentum building up in

South America and we currently experience no significant negative

exchange rate impact on earnings. Market response to our

Xemium®-based fungicide solutions is positive. With our positioning

Page 24

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Page 25

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

and strong product pipeline we are optimistic that we are able

to continue our success story in Agricultural Solutions.

Page 26

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

62

451*

194

265

0

100

200

300

400

500

Q3/2013 Net Income Q3/2014 Net Income

Exploration &Production

611

(19%)

Gas

€3,670+17%

Natural Gas Trading

Exploration & Production

Net income

development Volumes Prices/Currencies Portfolio

s. Q3’13 43% (26%) 0%

422

360

310

504

10

4 Analyst Conference Call October 24, 2014

* Incl. one-time disposal gain of 164 million euros from the divestment of a 15% stake in Edvard Grieg field

Page 27

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 10: Oil & Gas – Considerably higher sales and earnings]

In the Oil & Gas segment, sales grew considerably. This was driven

by higher volumes in Natural Gas Trading. EBIT before special

items significantly exceeded prior-year results attributable to higher

contributions from Natural Gas Trading. Net income came in at 265

million euros, a decrease of 186 million euros. In Q3 2013, we had

recognized a disposal gain of 164 million euros from the divestment

of a 15 percent stake in the Edvard Grieg field in the North Sea.

Sales in Exploration & Production decreased considerably due

to lower volumes as well as lower oil and gas prices. The average

price for Brent crude oil decreased by 8 percent to 102 US$ per

barrel. In euro terms it was also 8 percent lower. Volume was

about 10 percent lower. EBIT before special items declined by 14

percent to 310 million euros on lower volumes and prices.

Contrary to prior year we did not have an offshore lifting in Libya.

These missing contributions could not be compensated by higher

earnings in Norway.

Sales in the Natural Gas Trading business grew considerably

due to higher volumes especially on the European spot markets.

EBIT before special items recovered strongly after a relatively

weak first half 2014.

Page 28

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Review of “Other”

Million € Q3’14 Q3’13Sales 977 947EBIT before special items (7) (105)Thereof Corporate research

Group corporate costsCurrency result, hedges and othervaluation effectsOther business

(96)(53)100

23

(90)(57)(74)

59

Special items (20) (24)

EBIT (27) (129)

11BASF Q3 2014 Analyst Conference Call October 24, 2014

Page 29

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 11: Review of „Other“]

EBIT before special items in Other improved strongly from minus

105 million euros to minus 7 million euros, driven by a better

currency result and the recent share price development which led to

the dissolution of provisions for our long-term incentive program.

Page 30

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Cash Flow Solid cash flow in Q1-Q3 2014

Million € Q1-Q3’14 Q1-Q3’13Cash provided by operating activities 4,765 5,982Thereof Changes in net working capital

Miscellaneous items(739)(425)

374(327)

Cash provided by investing activities (3,625) (4,629)thereof Payments related to tangible / intangible assets (3,426) (3,038)

Acquisitions / divestitures 355 (1,093)Cash used in financing activities (995) (1,300)thereof Changes in financial liabilities

Dividends 1,661

(2,656)1,304

(2,604)

12BASF Q3 2014 Analyst Conference Call October 24, 2014

Page 31

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 12: Solid cash flow in Q1-Q3 2014 ] Let me turn to our cash flow. Please be reminded, that we will

summarize the first nine months of 2014.

At 4.8 billion euros cash provided by operating activities was

down by 1.2 billion euros. This was due to a cash outflow in net

working capital of 0.7 billion euros related to the reduction of trade

accounts payable as well as a planned build-up in inventories to

prepare for maintenance shutdowns.

Cash used in investing activities declined by 1 billion euros to 3.6

billion euros. While capex increased by 0.4 billion euros to 3.4

billion euros, cash payments for acquisitions decreased

considerably. In the same period of 2013, we had incurred cash

outflows of 1.1 billion euros for the acquisition of assets from

Statoil as well as the acquisition of Pronova BioPharma.

Free cash flow amounted to 1.3 billion euros in Q1-Q3 2014.

On a sequential basis we recognized a positive trend in cash flow:

While in H1 2014 free cash flow amounted to about 0.5 billion

euros, we generated 820 million euros of free cash flow in Q3

alone.

Coming back to the first nine months of 2014, financing activities

led to a cash outflow of 995 million euros, compared with an

outflow of 1.3 billion euros in the first three quarters of 2013. The

cash inflow resulting from the change in financial liabilities

amounted to 1.7 billion euros. This was mainly attributable to

BASF issuing several bonds with a principal amount of around 1.6

billion euros as well as taking out bank loans. The repayment of a

Page 32

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Page 33

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

bond with a principal amount of 1.25 billion euros had a

counterbalancing effect.

Net debt amounted to 13.9 billion euros, representing an increase

of 1.3 billion euros in comparison to prior year. At 39 percent, our

equity ratio remained at a healthy level.

Kurt, now back to you for the outlook.

Page 34

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

We aim to increase our sales volumes excluding the effects of acquisitions and divestitures.

Nonetheless, sales will decline slightly compared with 2013 due to the divestiture of the gas trading and storage business planned for autumn 2014 and negative currency effects.

Despite the challenging environment, we strive for a slight increase in EBIT before special items.

Outlook 2014

GDP: 2.3% (previous: 2.5%)

Industrial production: 3.4% (previous: 3.7%)

Chemical production: 4.0% (previous: 4.4%)

US$ / Euro: 1.35 (previous: 1.35)

Oil price (US$ / bbl): 105 (previous: 110)

Assumptions 2014

Outlook 2014

13BASF Q3 2014 Analyst Conference Call October 24, 2014

Page 35

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 13: Outlook 2014]

Coming to the outlook for 2014:

While BASF’s business in the third quarter was solid, we remain

cautious regarding the development of the macroeconomic

environment in the fourth quarter of 2014. We don’t expect an

increase of demand, assume ongoing economic volatility, and a

more modest global GDP growth for the remainder of the year.

Compared to Q2 reporting, we reduce some of our macroeconomic

assumptions for 2014 as follows:

- Global GDP growth is seen slightly lower now, at 2.3 percent

- Industrial production is expected to grow by about 3.4 percent

- We have reduced the growth expectation for the chemical

production by almost half a percent, to 4.0 percent

- We continue to see the average US$/€ exchange rate at 1.35

for the full year

- Regarding the oil price, we now forecast US$105 per barrel of

Brent oil, down from US$110 per barrel.

Despite the challenging environment, BASF strives to slightly

increase EBIT before special items for the full year 2014.

Page 36

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Update on key assumptions of the “We create chemistry” strategy

Growth 2010 – 2015(today‘s view)

Global GDP 2.6% p.a.

Chemical production

(excl. pharma)4.0% p.a.

Industrial production 3.4% p.a.

Growth 2010 – 2015(‘We create chemistry’ *)

3.4% p.a.

4.9% p.a.

4.6% p.a.

* Rebased figures, new base year 2010

BASF Q3 2014 Analyst Conference Call October 24, 2014 14

Page 37

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 14: Update on key assumptions of the ‘We create chemistry’ strategy]

Now I would like to update you on our “We create chemistry”-

strategy and the respective financial targets, which we published in

2011.

Our strategy is based on long-term trends – growth of emerging

markets and certain customer industries, the growing relevance of

innovation, shifts in feedstock costs and industry dynamics – to

name just a few. We increased our investments in selected growth

markets, intensified and globalized R&D, accelerated the pruning of

our portfolio and sharpened the meaning of sustainability for BASF.

We also laid out our operational excellence program STEP, which

aims to achieve savings of 1 billion euros by the end of 2015.

And we announced specific financial targets for 2015 and 2020 in

terms of sales and earnings. We felt this to be necessary, also to

allow you to hold us accountable.

Today, well before starting the year 2015, we want to update you

where we stand.

With regard to our strategy, we are pretty much on track. The

decision to further globalize our R&D platforms mentioned earlier is

just one example of a series of initiatives and changes. Our portfolio

optimization is ongoing, resulting in more than 20 divestitures since

2011, which we balance with selected smaller acquisitions, many of

them technology-driven.

Our operational excellence program STEP is ahead of schedule. By

the end of 2015, we will most likely achieve improvements of 1.3

billion euros, 300 million euros more than planned.

Page 38

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

Page 39

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

And yet, it looks like we will achieve not all of our ambitious financial

targets by 2015. We worked very hard to reach them. However,

early this year we told you that hitting these targets would require an

economic recovery in major markets, especially in Europe, and a

margin improvement for some of our major basic products. It is

pretty obvious that this has not happened; we have seen a further

weakening.

Comparing the previously expected GDP, industry and chemical

production growth rates 2010 to 2015 with what we see today

underlines this growing gap.

The average annual growth of global GDP we now see about 0.8

percentage points lower than expected. Even more importantly, we

now assume growth of chemical production to be 4 percent instead

of 4.9 percent per year. This is still well above GDP and industrial

production. We all know the reasons for this development: Reduced

growth dynamics of emerging markets and a delayed recovery in

Europe.

Aside from lower demand growth which has adversely impacted our

business, we have experienced margin pressure in some of our

major product lines especially in China. To give you just one

example: The margin of caprolactam in Asia today is more than 50

percent lower than in 2011. We did not project such peak margins

into the future. However, the current margin squeeze is beyond of

what we had anticipated.

In Performance Products we have seen a typical commoditization in

selected product lines. This is why we initiated an additional

restructuring program, which will deliver about 500 million euros to

earnings from 2017 onwards.

Page 40

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

BASF Q3 2014 Analyst Conference Call October 24, 2014

EBITDA / EBITDA impact (billion €)

10

11

12

13

14

15

EBITDA target2015

Lower marketgrowth

Lowermargins

Divestituregas tradingand storage

Additionalcontribution

STEP

Positive FXeffects

2015 EBITDA(E)

Consensus

average

Lower market growth and lower margins adversely impact 2015 EBITDA expectation

15

Page 41

BASF 3rd Quarter 2014 Analyst Conference Call October 24, 2014

[Chart 15: Lower market growth and lower margins adversely impact 2015 EBITDA expectation]

We have summarized these effects in one slide. Lower market

growth and lower margins cost us more than 1 billion euros of

EBITDA each.

The planned divestiture of our gas trading and storage business

was not considered in 2011 and will lower sales by approximately

12 billion euros and EBITDA by 500 million euros.

STEP will generate additional earnings of 300 million euros. The

other positive factor, amounting to around 400 million euros, is the

exchange rate since we expected a weaker US dollar than we

currently see.

Most probably we will also see slightly lower growth going forward

and we do not expect an immediate cyclical recovery. We now

expect 2015 sales and EBITDA to be in line with current financial

market expectations. Analysts currently foresee 2015 EBITDA

between 10 billion euros and 12 billion euros. Clearly, we aim to

achieve the upper range. However, we will – as usual – provide you

with the outlook for 2015 at our annual analyst and investor

conference on February 27, 2015. That day we will also discuss our

updated long-term targets.

Be assured that we will remain committed to growing our business

profitably and further improving earnings resilience in the coming

years.

We are now happy to take your questions.