Unit – 1 Introduction to

AccountingDr. Kasamsetty Sailatha

Associate Professor and ChairpersonDepartment of Management and Commerce

Amrita School of Arts and SciencesAmrita Vishwa Vidyapeetham

Mysuru

1

• Introduction to Accountings

• Introduction to Accounting and book-keeping

• Accounting concepts

• Accounting conventions

2

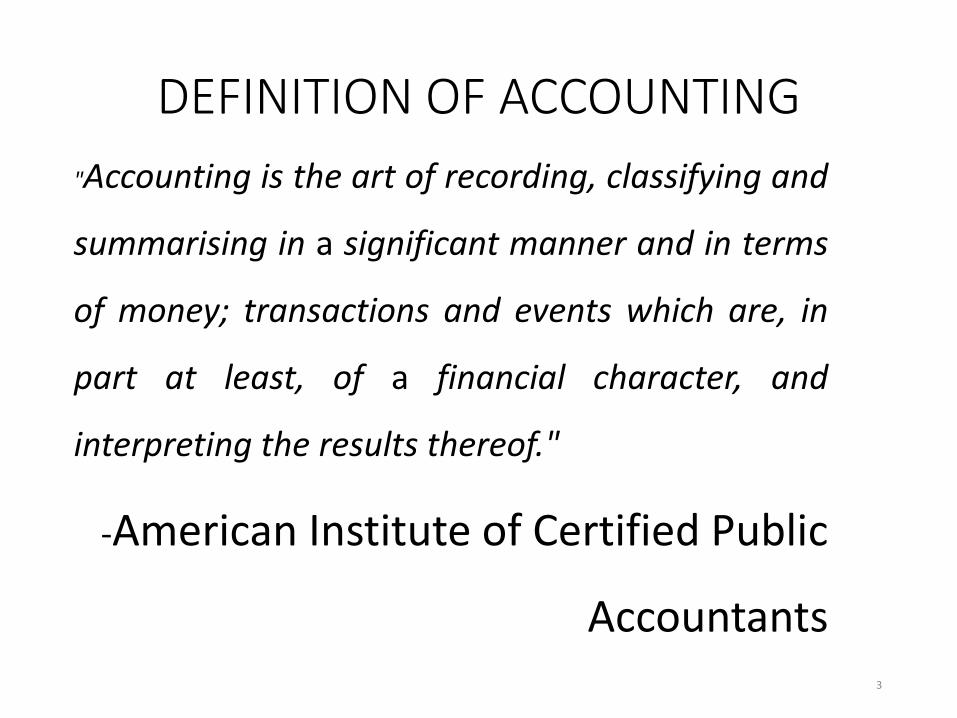

DEFINITION OF ACCOUNTING

"Accounting is the art of recording, classifying and

summarising in a significant manner and in terms

of money; transactions and events which are, in

part at least, of a financial character, and

interpreting the results thereof."

-American Institute of Certified Public

Accountants3

DEFINITION OF ACCOUNTING

"Accounting is the science of recording and classifying

business transactions and events, primarily of a financial

character, and the art of making significant summaries,

analysis and interpretations of those transactions and

events and communicating the results to persons who

must make decisions or form judgment."

-Smith and Ashburne

4

DEFINITION OF ACCOUNTING

"Accounting is the process of identifying,

measuring and communicating economic

information to permit informed judgments

and decisions by users of the information."

-American Accounting Association

5

Meaning of AccountingThus, accounting is a process of

collecting,

recording,

summarising and

communicating financial information to the users for decision-making.

6

ATTRIBUTES (CHARACTERISTICS) OF ACCOUNTING

The definitions of accounting bring to light the following attributes of Accounting:

1. Identification of Financial Transactions and Events

2. Measuring the Identified Transactions

3. Recording

4. Classifying

5. Summarising

6. Analysis and Interpretation

7. Communicating

7

Financial Transactions or Events

RecordingJournal1. Cash Book2. Purchase Book3. Sales Book4. Purchases Return Book5. Sales Return Book6. Bills Payable Book7. Bills Receivable Book8. Journal Proper

Classifying (Posting into Ledger)

SummarizingTrial BalanceTrading and Profit and Loss Account Balance Sheet.

Analysis and Interpretation

Communicating to the Users

ACCOUNTING PROCESS

8

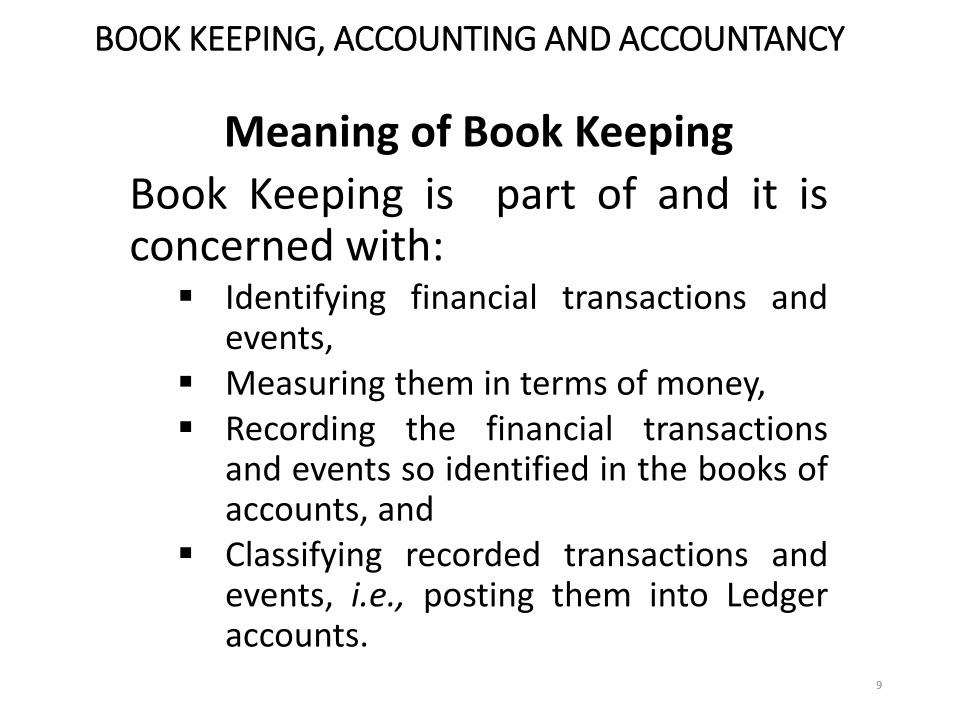

BOOK KEEPING, ACCOUNTING AND ACCOUNTANCY

Meaning of Book Keeping

Book Keeping is part of and it isconcerned with:

Identifying financial transactions andevents,

Measuring them in terms of money, Recording the financial transactions

and events so identified in the books ofaccounts, and

Classifying recorded transactions andevents, i.e., posting them into Ledgeraccounts.

9

Definitions of Book Keeping

"Book Keeping is an art of recording in the books of accounts the monetary aspect of commercial and financial transactions."

• -Northcott

"Book Keeping is an art of recording business dealings in a set of books."

• -J.R. Batliboi

• "Book Keeping is the science and art of recording correctly in the books of accounts all those business transactions that result in the transfer of money or money's worth."

• -R.N. Carter

• "Bool: Keeping is the art of recording business transactions in a systematic manner."

• -A.N. Rosen Kampff

10

• Accounting:

•Accounting is an art of •recording, •classifying and •summarising the financial data and interpreting the results thereof. •Accounting is a wider concept than Book Keeping. •It starts where Book Keeping ends. In other words, Book Keeping is a part of accounting.

11

BOOK KEEPING, ACCOUNTING AND ACCOUNTANCY

DIFFERENCE BETWEEN BOOK KEEPING AND ACCOUNTING

12

Basis Book Keeping Accounting

1. Scope Book Keeping is concerned withidentifying financial transactions;measuring them in money terms;recording them in the books ofaccounts and classifying them.

Accounting is concerned withsummarising the recordedtransactions, interpreting themand communicating the results.

2. Stage It is a primary stage. It is a secondary stage. It beginswhere Book Keeping ends.

3. Objective The objective of Book Keeping isto maintain systematic records offinancial transactions.

The objective of accounting is toascertain net results of operationsand financial position and tocommunicate information to theinterested parties.

BOOK KEEPING, ACCOUNTING AND ACCOUNTANCY

DIFFERENCE BETWEEN BOOK KEEPING AND ACCOUNTING

13

4. Nature of Job This job is routine innature.

This job is analytical anddynamic in nature.

5. Performance Junior staff performs thisfunction.

Senior staff performs thisfunction.

6. Relation Book Keeping is the basisfor accounting.

Accounting begins whereBook Keeping ends.

7. Special Skills Book Keeping ismechanical in nature andthus, does not requirespecial skills.

Accounting requires specialskills and ability to analyseand interpret.

•Accountancy•Accountancy refers to a systematicknowledge of accounting.•It explains how to deal with variousaspects of accounting.•It educates us why and how to maintainthe books of accounts and how tosummarise the accounting informationand communicate it to the users.•In the words of Kohler, accountancyrefers to the entire body of the theory andpractice of accounting

14

•Accounting and Accountancy

Accountancy is an area of knowledgewhereas accounting is the action or processused in this area.

Accounting depends on the rules andprinciples framed by the Accountancy butAccountancy does not depend onAccounting.

It may be said that Accountancy is the wholething while Accounting is the applicationpart of accountancy.

15

OBJECTIVES OF ACCOUNTINGThe objectives or functions of accounting are:

Maintaining Systematic Records of Financial Transactions an Events

Ascertaining Profit or Loss

Ascertaining Financial Position

Assisting the Management

Communicating Accounting Information to Users

16

FUNCTIONS OF ACCOUNTINGThe functions of accounting are:

Maintaining Systematic Records

Communicating the Financial Results

Meeting Legal Requirements

Protecting Business Assets

Assistance to Management

Stewardship

17

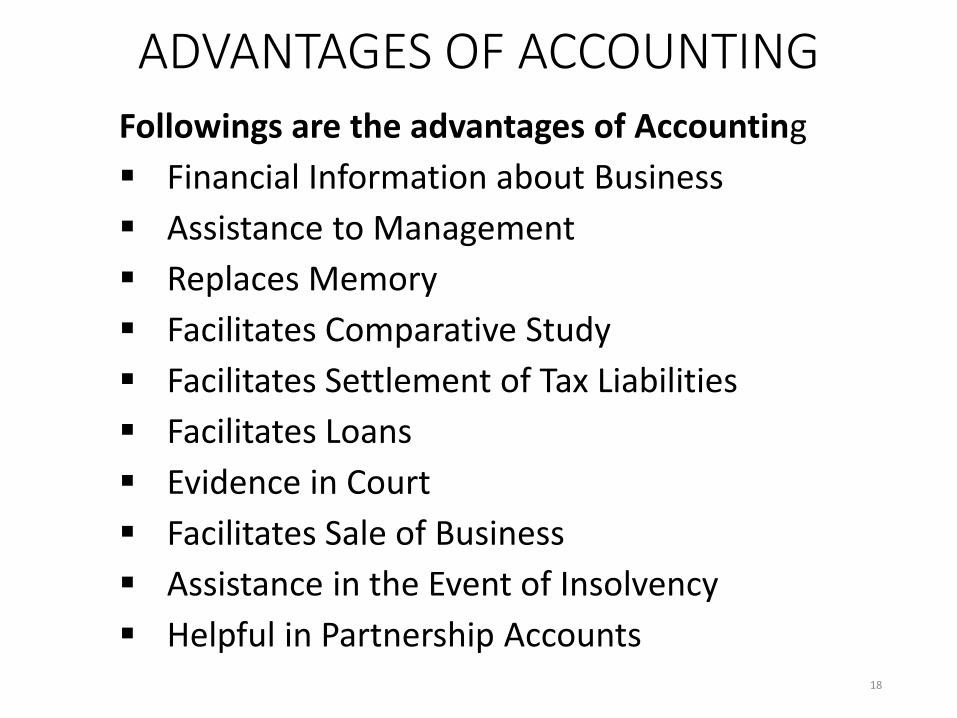

ADVANTAGES OF ACCOUNTING

Followings are the advantages of Accounting

Financial Information about Business

Assistance to Management

Replaces Memory

Facilitates Comparative Study

Facilitates Settlement of Tax Liabilities

Facilitates Loans

Evidence in Court

Facilitates Sale of Business

Assistance in the Event of Insolvency

Helpful in Partnership Accounts18

LIMITATIONS OF ACCOUNTINGFollowings are the limitations of accounting

Accounting is not Fully Exact

Accounting does not Indicate the Realisable Value

Accounting Ignores the Qualitative Elements

Accounting Ignores the Effect of Price Level Changes

Accounting may Lead to Window Dressing

19

SYSTEMS OF ACCOUNTINGThe systems of recording transactions in the books of accounts are two namely:

1. Double Entry System and

2. Single Entry System.

20

Double Entry SystemThe Double Entry System of accounting was developed in the 15th Century inItaly by Lucas Pacioli.

Under the system, every transaction has two aspects-Debit and Credit and atthe time of recording a transaction, it is recorded once on the debit side andagain on the credit side.

The Double Entry System has proved to be a scientific and complete system ofaccounting followed by every enterprise and organisation.

For example, at the time of cash purchases, goods are acquired and in returncash is paid.

In the transaction, above two aspects are involved, i.e., receiving goods andpaying cash

Under the Double Entry System, both these aspects are recorded.

One part, i.e., the receipt of goods is debited and the second part, i.e., paymentof cash is credited.

21

Features of the Double Entry System

It maintains a complete record of each transaction.

It recognises the two-fold aspect of everytransaction, viz., the aspect of receiving (value in)and the aspect of giving (value out).

In this system, one aspect is debited and otheraspect is credited following the rules of debit andcredit.

Since, one aspect of a transaction is debited and theother is credited, the total of all debits is alwaysequal to total of all credits. It helps in establishingarithmetical accuracy by preparing the Trial Balance.

22

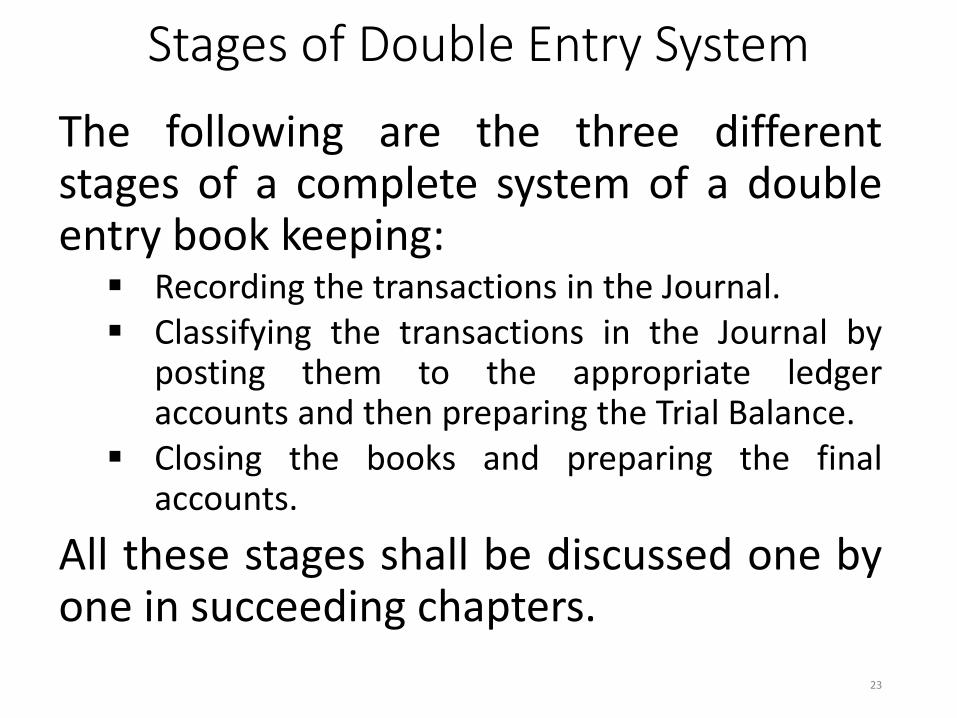

Stages of Double Entry System

The following are the three differentstages of a complete system of a doubleentry book keeping:

Recording the transactions in the Journal. Classifying the transactions in the Journal by

posting them to the appropriate ledgeraccounts and then preparing the Trial Balance.

Closing the books and preparing the finalaccounts.

All these stages shall be discussed one byone in succeeding chapters.

23

Advantages of the Double Entry System

The main advantages of Double Entry System are

Scientific System

Complete Record of Transactions

A Check on the Accuracy of Accounts

Ascertainment of Profit or Loss

Knowledge of Financial Position

Full Details for Purposes of Control

Comparative Study is Possible

Helps Management in Decision-Making

No Scope of Fraud24

Single Entry SystemSingle Entry System of recording transactions inthe books of accounts, may be defined to be anincomplete Double Entry System.In this system, all transactions are not recordedon the double entry basis.As regards some transactions, both aspects ofthe transactions are recorded, as regards others,either one aspect is recorded or not recorded atall.Instead of maintaining all the accounts, onlyPersonal Accounts and Cash Book aremaintained under this system.

25

Single Entry SystemThe accounts maintained under thissystem are incomplete and unsystematicand therefore, not reliable.

The Single Entry System is also known asAccounts from Incomplete Records.

Since all transactions are not recordedunder double entry principle, it is notpossible to prepare a Trial Balance.

As a result, the Profit and Loss Accountand the Balance Sheet cannot beprepared.

26

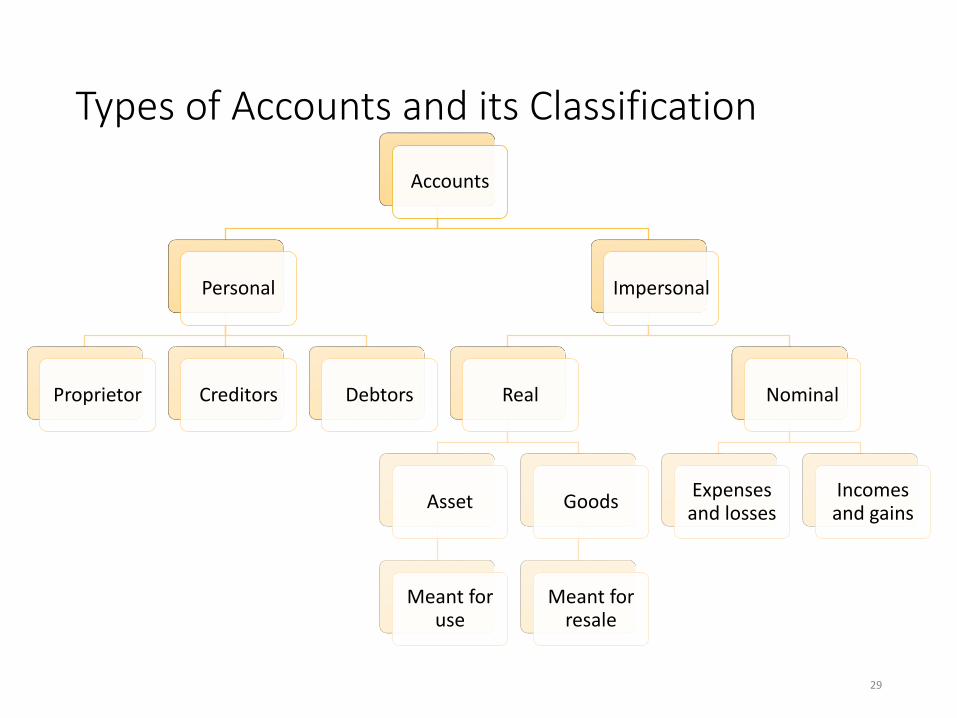

Types of Accounts and Golden rules of Accounting:

•Personal Account: Accounts of persons with who the business has dealing are known as personal Account. • Natural person: Name of an Individual ex. Name of Customers,

supplier etc.

• Artificial person or legal bodies: name of any firm or company ex. Bank co-operative society, educational institution firms’ name.

• Representative personal accounts: all accounts representing outstanding to outstanding expenses and accrued or prepaid incomes are personal accounts Ex. Out standing salaries, rent, wages or prepaid expenses or accrued or prepaid incomes.

•Rule: Debit the Receiver and Credit the Giver

27

• Real Account: Accounts in which the business records the real things owned by it i.e. assets are known as real accounts. • Real accounts are two types:

• Tangible • Intangible

• Rule: Debit what comes in and credit what goes out

• Nominal Accounts: It relates to the items which exist in name only. Ex. Expenses, incomes etc. Or in other words, accounts which records expenses losses income and gains of the business are known as nominal accounts.

• Rule: Debit all expenses and losses and credit all incomes and gains.

28

Types of Accounts and its Classification

29

Accounts

Personal

Proprietor Creditors Debtors

Impersonal

Real

Asset

Meant for use

Goods

Meant for resale

Nominal

Expenses and losses

Incomes and gains

Accounting Concepts and Conventions

•Need for Accounting Concepts and Conventions

•Development of Accounting concepts and conventions• Utility • Objectivity• Feasibility

•Classification of accounting concepts and conventions

• Important terms in accounting

30

Concepts of Accounting:• The Generally Accepted Accounting Principles (GAAP) are all termed

concepts by some experts.

• Some others call all of them conventions.

• However an overwhelming majority of authors on accounting distinguish between concepts and conventions.

• Concepts:1. The entity concept

2. The money measurement concept

3. Going concern concept

4. Dual aspect concept

5. Accounting period concept

6. Cost concept

7. Revenue recognition concept or realization concept

8. Matching concept

9. Accrual concept

10. Objective evidence concept

31

Conventions:

•Convention of full disclosure

•Convention of consistency

•Convention of materiality (relative importance)

•Convention of conservatism (playing safe, is the defensive accounting mechanism against uncertainty)

32