Part-Timer Retirement: Should You Switch to Social Security?

Presented by Cliff Liehe

Los Angeles, April 13. 2007

Revised by Phyllis Eckler, February 2008

What’s Happening?

Part-Timers in the Los Angeles Community College District may soon have the opportunity to switch from the CalSTRS Cash Balance (CB) retirement plan to Social Security.

If you are in CB, you need to decide if you should switch to Social Security; i.e., if the switch would benefit you.

How Does CB Work?

CB is a “cash balance” plan (hybrid of a “defined benefit” plan and a “defined contribution” plan)

Immediate vesting Contributions: 3.75% employee, 4.25%

employer, and tax deferred Guaranteed interest rate “Portable”: if you quit teaching, your CB funds

can be rolled over to another retirement plan No administrative fees

How are CB Benefits Calculated?

The retirement benefit is the employee’s account balance at time of retirement: i.e., total of all contributions (employee and employer) plus all compounded annual guaranteed interest

The benefit is paid as a lump sum or, if over $3500, may be paid as a lifetime annuity based on age and account balance

What Would My Monthly Annuity from Cash Balance Be?A chart of your monthly Cash Balance annuity

benefit is available at the site below :

http://www.calstrs.com/Calculators/DBS_annuity_calcs_SR_REVISED.pdf

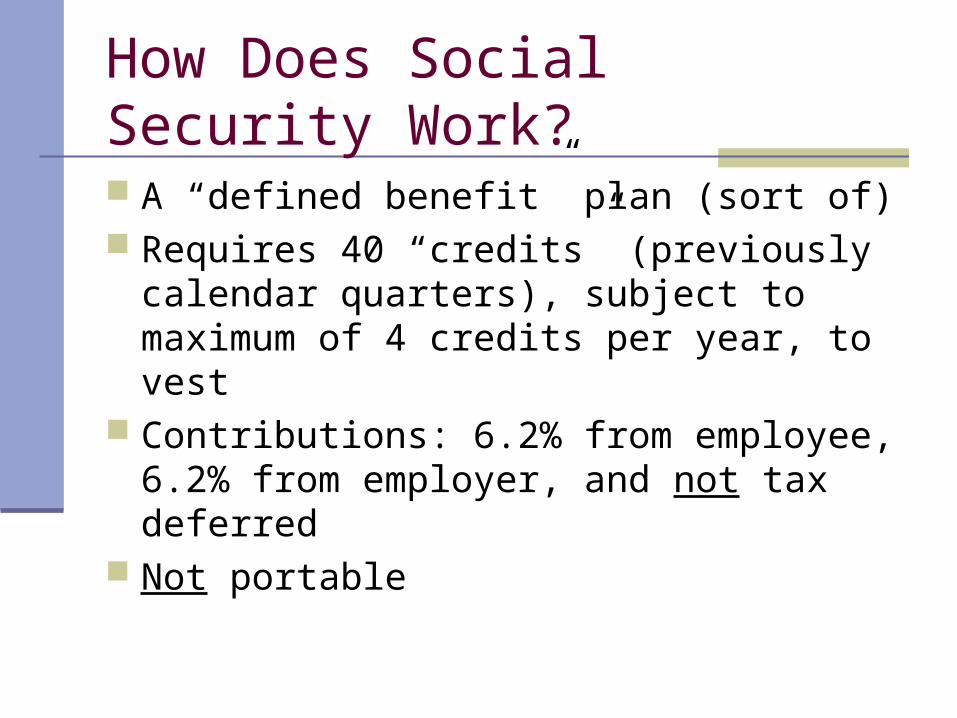

How Does Social Security Work?

A “defined benefit” plan (sort of) Requires 40 “credits” (previously calendar

quarters), subject to maximum of 4 credits per year, to vest

Contributions: 6.2% from employee, 6.2% from employer, and not tax deferred

Not portable

How Are Social Security Benefits Calculated In General? The retirement benefit formula is based on an

employee’s highest 35 years’ earnings (many more years than other defined benefit plans)

The formula favors lower wage earners

How Are Social Security Benefits Calculated Specifically? First, all past earnings, subject to a maximum

for each year, are indexed for inflation Then the highest 35 years’ indexed earnings

are added together Next, the sum is divided by 420 (number of

months in 35 years) to get average monthly indexed earnings

No, this is not the benefit. We’re not done yet--see next slide.

How Are Social Security Benefits Calculated Specifically? Then:

(1) The first $680 of monthly average is multiplied by 90%

(2) The amount of monthly average over $680 and not over $4,100 is multiplied by 32%

(3) The amount of monthly average over $4100 is multiplied by 15%

Finally, the three products are added together and the sum is rounded down to next lowest dollar to get the retirement benefit at “full retirement age”

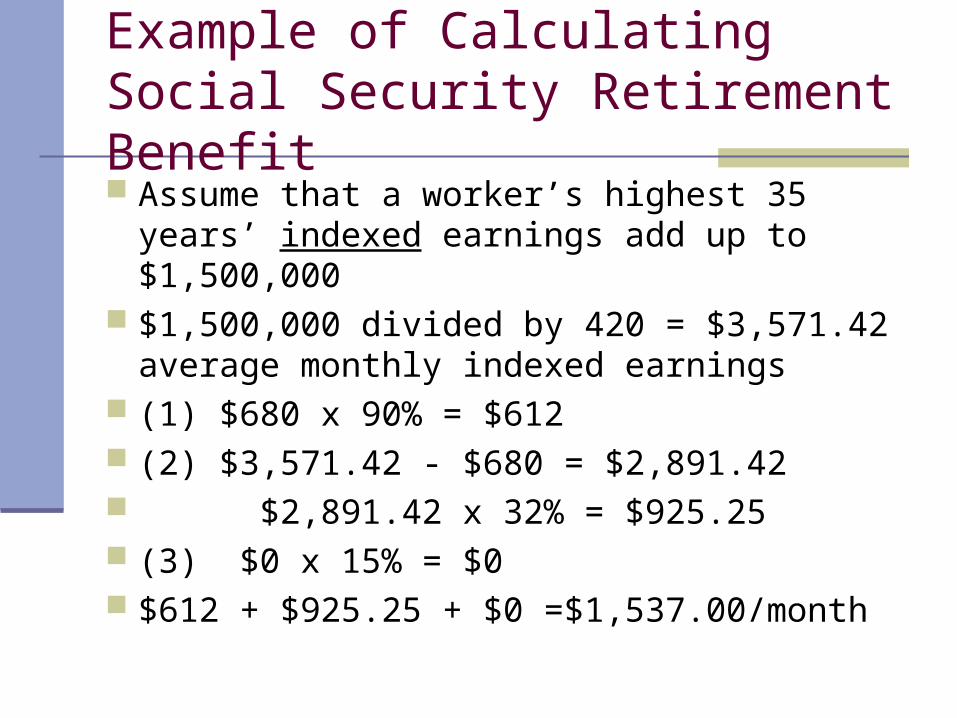

Example of Calculating Social Security Retirement Benefit Assume that a worker’s highest 35 years’

indexed earnings add up to $1,500,000 $1,500,000 divided by 420 = $3,571.42

average monthly indexed earnings (1) $680 x 90% = $612 (2) $3,571.42 - $680 = $2,891.42 $2,891.42 x 32% = $925.25 (3) $0 x 15% = $0 $612 + $925.25 + $0 =$1,537.00/month

What Are The “WEP” and “GPO”?

“WEP” is the Windfall Elimination Provision It may reduce your Social Security retirement

benefits See SSA publication No. 05-10045

“GPO” is the Government Pension Offset It may reduce or even wipe out your Social

Security spousal, widow, or widower benefits See SSA Publication No. 05-10007

Should You Switch to Social Security?

[Will Social Security Go Broke?] Will You Be Vested in Social Security If You

Switch? When Do You Plan to Retire? Do You Want Portability If You Quit

Teaching? How Much Withholding Can You Afford? Will You Be Affected by the WEP or GPO? Will You Get More Retirement Income If You

Switch?

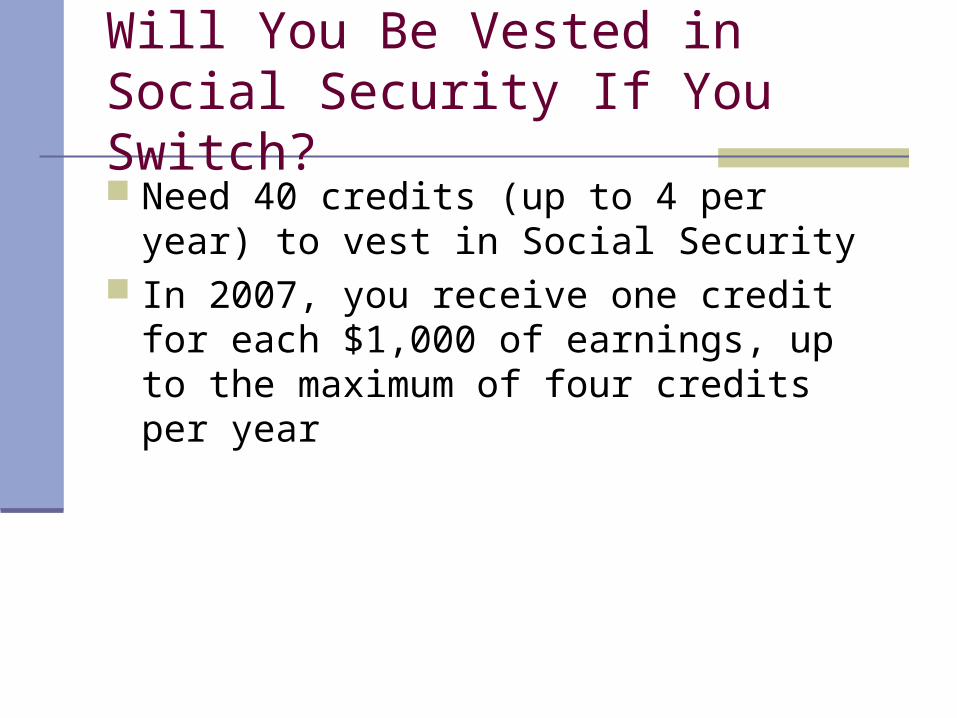

Will You Be Vested in Social Security If You Switch? Need 40 credits (up to 4 per year) to vest in

Social Security In 2007, you receive one credit for each

$1,000 of earnings, up to the maximum of four credits per year

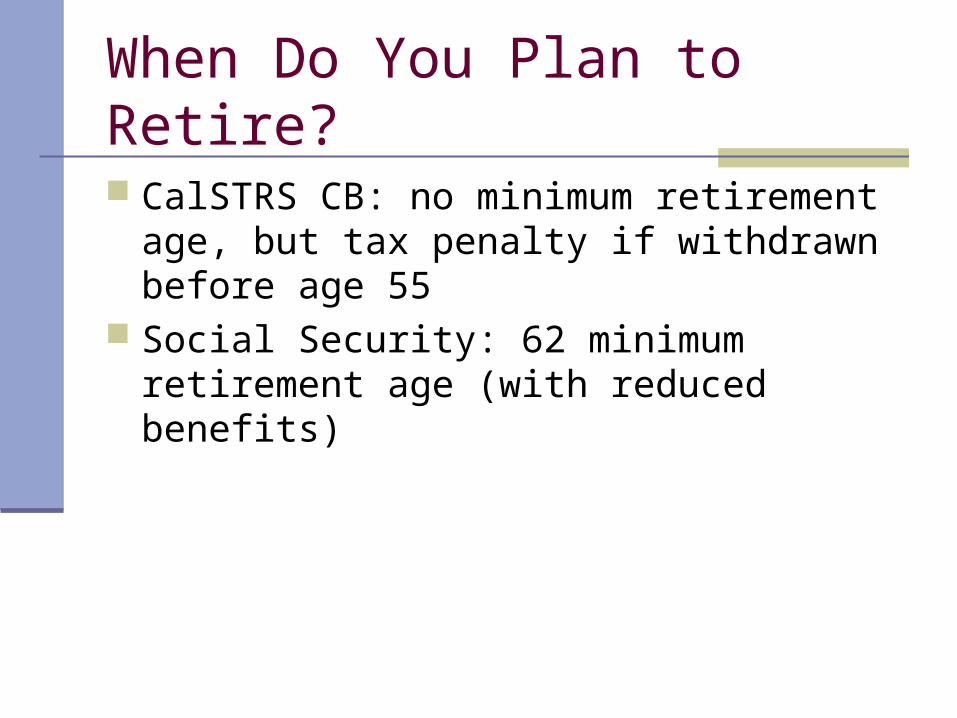

When Do You Plan to Retire?

CalSTRS CB: no minimum retirement age, but tax penalty if withdrawn before age 55

Social Security: 62 minimum retirement age (with reduced benefits)

Do You Want Portability If You Quit Teaching? CalSTRS CB: Portable to another retirement

plan Social Security: Not portable

How Much Withholding Can You Afford? This should be irrelevant!

CalSTRS DB: 3.75% Social Security: 6.2%

Will You Be Affected By The WEP and/or GPO? CalSTRS CB is considered an “alternative

pension”, even if benefits are paid as a lump sum, and may subject you to the WEP and/or GPO

What if CB funds are transferred to an IRA or other retirement plan?

The WEP offset may be reduced or eliminated entirely if you have 21 or more years of “substantial earnings”

Other exceptions to the WEP or GPO are rare

If any part of your government pension is based on work not covered by Social Security, you may be affected by the Windfall Elimination Provision.

If any part of your government pension is based on work not covered by Social Security, you may be affected by the Windfall Elimination Provision.

Windfall Elimination ProvisionWindfall Elimination Provision

How Social Security Determines Your Benefit

Social Security benefits are based on earnings

Step 1 Your wages are adjusted for inflation

Step 2 Find the average of your 35 highest earnings years

Step 3 Result is “average indexed monthly earnings”

In 2007, the maximum earnings taxable for Social Security is $97,500 gross. Because of these maximum limits, the maximum payment in 2007 is $2116.

Example:

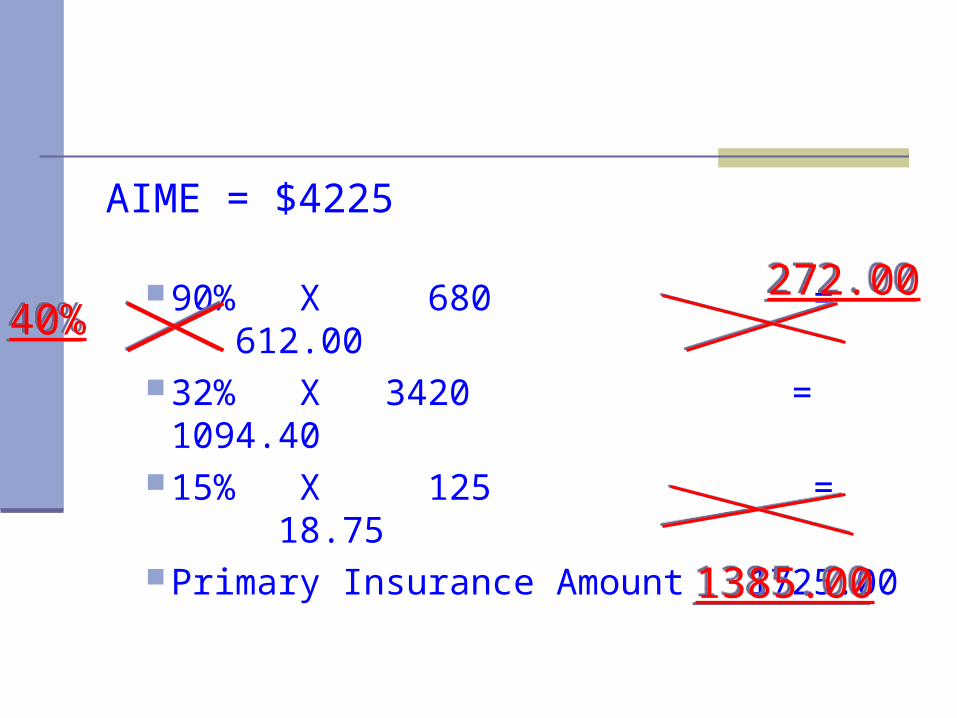

AIME = $4225

90% X 680 = 612.0032% X 3420 = 1094.4015% X 125 = 18.75Primary Insurance Amount 1725.00

40%40%272.00272.00

1385.001385.00

Exception of the Windfall Elimination ProvisionException of the Windfall Elimination Provision

% of First FactorYears of Coverage in Benefit Formula

30 or more 9029 8528 8027 7526 7025 6524 6023 5522 5021 45

% of First FactorYears of Coverage in Benefit Formula

30 or more 9029 8528 8027 7526 7025 6524 6023 5522 5021 45

Government Pension Offset (GPO)Government Pension Offset (GPO)

If you receive a government pension based on work not covered by Social

Security, your Social Security spouse’s or widow(er)’s benefits may

be reduced.

If you receive a government pension based on work not covered by Social

Security, your Social Security spouse’s or widow(er)’s benefits may

be reduced.

Example:$900 of Government pension 2/3 = $600Social Security Spouse Benefits = $500No cash benefit payable by Social Security

Example:$900 of Government pension 2/3 = $600Social Security Spouse Benefits = $500No cash benefit payable by Social Security

Government Pension Offset (GPO)Government Pension Offset (GPO)

Spouse’s Benefits Only

2/3 of amount of Government pension will be used to reduce the Social Security spouse’s benefit

Spouse’s Benefits Only

2/3 of amount of Government pension will be used to reduce the Social Security spouse’s benefit

Will You Get More Retirement Income If You Switch? You need to estimate your CB and Social

Security benefits under different scenarios and compare the results

The bad news: Math is involved All estimates require making assumptions

which may or may not turn out to be true The good news:

Social Security has calculators available to do the math for you

What Are The Possible Scenarios?

1) You stay in CB and will have no Social Security benefits

2) You stay in CB and will also have Social Security benefits

3) You switch to Social Security and will have minimal or no CB benefits

4) You switch to Social Security and will also have CB benefits

How Do You Estimate Your CB Benefits (conservatively)? You need your latest annual CalSTRS

Retirement Progress Report (statement) and a calculator

Find account balance on statement Add this year’s employee and employer

contributions (estimate or use last year’s ) to previous year’s account balance

Multiply sum by 1.0475 (interest rate for 2006-07 is 4.75%) to get new account balance

How Do You Estimate Your CB Benefits (conservatively)?

Repeat for each year you are in CB after this until your Social Security “full retirement age” (for comparison)

This lump sum estimate is in today’s dollars and assumes same load, salary, and 4.75% interest rate each year

To determine equivalent monthly benefit, use the CalSTRS DBS Member-Only Annuity table (also used for CB)

Example of Estimating CB Benefits (conservatively) Assume annual CB statement for last year

(2005-06) showed $2,000 current year contributions (employee and employer) and $20,000 account balance

Assume employees stays in CB until Social Security full retirement age in 2010

($20,000 + $2,000) x 1.0475 = $23,045 estimated new balance end of 2006-07

($23,045 + $2,000) x 1.0475 = $24,139.64 estimated new balance end of 2007-08

Example of Estimating CB Benefits (conservatively) ($24,139.64 + $2,000) x 1.0475 = $25,286.27

estimated new balance end of 2008-09 ($25,286.27 + $2,000) x 1.0475 = $26,487.36

estimated new balance end of 2009-10 (payable as lump sum or lifetime monthly annuity)

Looking at the CalSTRS DBS Member-Only Annuity table, the equivalent monthly benefit will be a little more than $205 per month

How Do You Estimate Your Social Security Benefits (conservatively)? You need your latest annual Social Security

Statement and a calculator (hard way) or an online computer (easy way)

Note: your statement includes estimates Hard way: follow instructions on back of SSA

publication No. 05-10070, Your Retirement Benefit: How It Is Figured

How Do You Estimate Your Social Security Benefits (conservatively)? Easy way (sort of):

Go to www.ssa.gov Under Retirement near middle of page click on

“Calculate Your Benefits” Download Calculator 3, Detailed Calculator When it asks amount of other government

pension, enter monthly CB amount previously estimated (calculator includes reduction for WEP)

Be sure to save your file (for future use) before ending calculator program