March 2013

Gautham Gnanajothi, Industry Analyst - Energy & Power Systems

“50 Years of Growth, Innovation & Leadership”

Modular Data Centres – Transcending Traditional Data Centres

Modular Data Centres – Transcending Traditional Data CentresMarket Insight

© 2013 Frost & Sullivan Page 2

The ever-increasing need for data processing has led the data centre market to boom. This

high growth in data centres has led modern business organisations to be equipped with

cutting-edge technology, innovation and cost-effectiveness in order to sustain the competitive

environment. One of the radical developments in the data centre market is the “Modular

Data Centre” (MDC). It came to prominence in 2007 and has been on the growth trajectory

ever since. The traditional data centres, usually known as the brick-and-mortar facilities, face

certain basic challenges, like long construction period, capacity management, scalability and

high OPEX and CAPEX. The evolution of modular data centres promises to address these

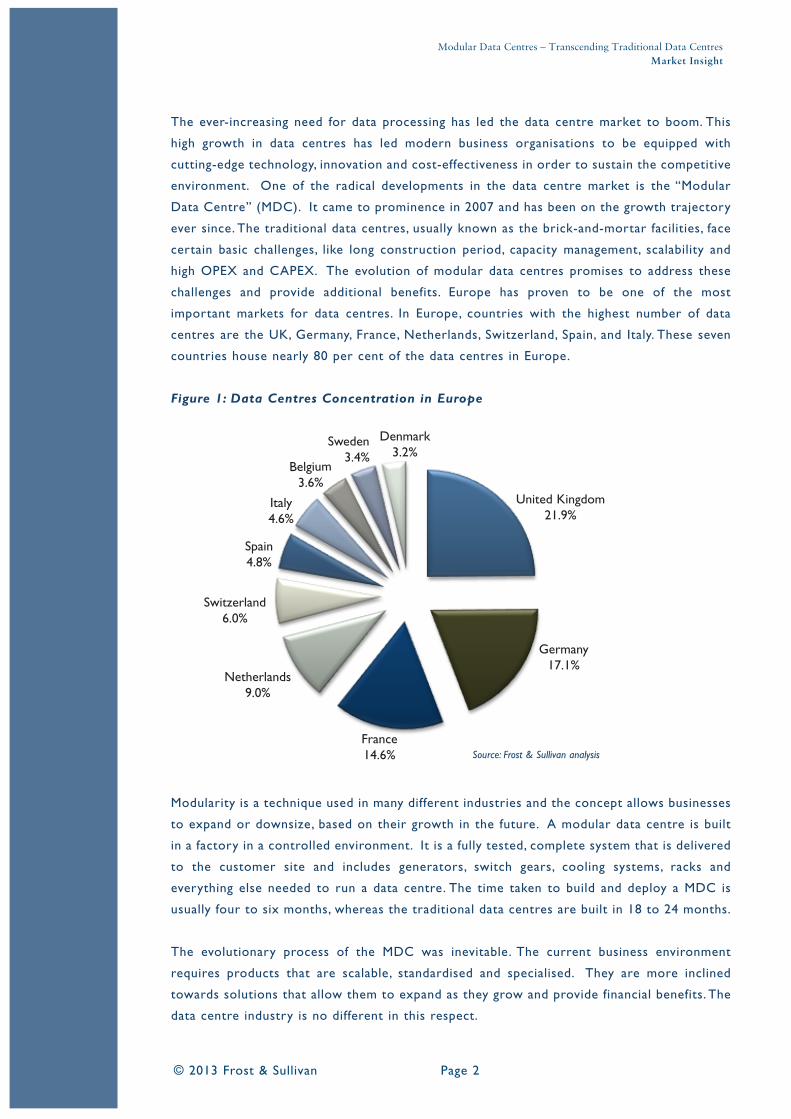

challenges and provide additional benefits. Europe has proven to be one of the most

important markets for data centres. In Europe, countries with the highest number of data

centres are the UK, Germany, France, Netherlands, Switzerland, Spain, and Italy. These seven

countries house nearly 80 per cent of the data centres in Europe.

Figure 1: Data Centres Concentration in Europe

Modularity is a technique used in many different industries and the concept allows businesses

to expand or downsize, based on their growth in the future. A modular data centre is built

in a factory in a controlled environment. It is a fully tested, complete system that is delivered

to the customer site and includes generators, switch gears, cooling systems, racks and

everything else needed to run a data centre. The time taken to build and deploy a MDC is

usually four to six months, whereas the traditional data centres are built in 18 to 24 months.

The evolutionary process of the MDC was inevitable. The current business environment

requires products that are scalable, standardised and specialised. They are more inclined

towards solutions that allow them to expand as they grow and provide financial benefits. The

data centre industry is no different in this respect.

United Kingdom21.9%

Source: Frost & Sullivan analysis

Germany17.1%

France14.6%

Netherlands9.0%

Switzerland6.0%

Spain4.8%

Italy4.6%

Denmark3.2%

Sweden3.4%

Belgium3.6%

The traditional data centres still continue to dominate the market. However, the challenges

they pose are increasing. Moreover, the current IT environment is constantly evolving and

changing. cloud-based applications, virtualisation and other such trends are changing the

outlook of a traditional data centre. In such conditions, it becomes mandatory to look at data

centre capacity planning from a different angle. The dawn of modular data centres has proved

to be the much-awaited solution for all these challenges. The MDC is still in a nascent stage,

and the design and technology is yet to be accepted on a full scale. There are some early

adopters; however, the market is still sceptical about its benefits and advantages over

traditional data centres. The evolutionary process of the MDC from a traditional brick-and-

Mortar building involves an intermediary product, which is the “Containerised Data Centre”

(CDC). The idea of a data centre in a container was ground breaking. It is a self-contained

module comprised of computing, networking and storage resources.

Modular Data Centre Facility

These modules are designed to fit in an ISO-approved container. The external size of the

container is ISO restricted; however, the internal configuration can be changed in any fashion.

It can be either one container housing all the components or separate containers for each

component, like power, cooling, server racks, etc. The CDC solution offers excellent benefits,

like higher efficiency, high reliability, mobility, easy maintenance, and lower build time. In spite

of these benefits, there were a few issues that did not make them the perfect solution for an

enterprise. High rigidity of the containers, lack of ability to customise, and size restrictions

that led to less space for set up and maintenance were some of the key issues. This led to

the next step in the evolutionary process, which was the MDC. It offered all the benefits of

a CDC and effectively addressed the disadvantages.

It redefined the concept of data centres. They were no longer required to be built on site,

reducing the construction time significantly. Additionally, each module can be customised to

meet the power, cooling and rack requirement of the customer.

Modular Data Centres – Transcending Traditional Data CentresMarket Insight

© 2013 Frost & Sullivan Page 3

Source: http://www.techweekeurope.co.uk/

The modules are tested and commissioned before deployment, and modules can be added or

removed based on the customer’s business growth.

The global MDC market size estimated to be about $400 million to $500 million in 2011.

Since it is a relatively new technology, the market participants are sceptical in adopting it.

Frost & Sullivan predicts that it will take at least two years for the momentum to pick up.

The MDC market is expected to grow at a CAGR (Compounded Annual Growth Rate) from

2011 – 2015 of 35 per cent to 45 per cent. It can be expected that the MDC will

revolutionise the data centre market, around half of the large data operators will go modular

in the next five years. This trend has been clearly identified by the server vendors/OEMs, such

as HP, IBM, SGI, Dell, Cisco, Cirrascale, Bull, AST, Schneider Electric, Emerson Network Power,

Silver Linings, and Telenetix. They have included modular and containerised data centres in

their portfolio. Apart from these, there are specialised MDC providers, which include IO,

NxGen Modular, COLT, Cannon, Pacific Voice and Data, BladeRoom, Pelio & Associates, Dock

IT, Lee Technologies (acquired by Schneider Electric), Datapod and Turbine Air Systems

(TAS)/Celestica (CLS).

The evolution of MDC from the traditional data centres is a huge step forward in the history

of the data centre market. It has the potential to completely overshadow the traditional data

centres in the next five to seven years. The current IT environment is becoming highly fast

paced and the associated costs are also on the rise. This trend has forced IT executives to

rethink the traditional data centre approach, which no longer provides optimum solution. The

emergence of MDC has provided the much-awaited solution for data centre flexibility, and

this is complimented by significantly reduced build time and lower OPEX and CAPEX. MDCs

are not far from becoming the most viable and sought-after solutions available in the market.

Modular Data Centres – Transcending Traditional Data CentresMarket Insight

About Frost & Sullivan

Frost & Sullivan, the Growth Partnership Company, works in collaboration with clients to

leverage visionary innovation that addresses the global challenges and related growth

opportunities that will make or break today’s market participants. For more than 50 years,

we have been developing growth strategies for the Global 1000, emerging businesses, the

public sector and the investment community. Is your organisation prepared for the next

profound wave of industry convergence, disruptive technologies, increasing competitive

intensity, Mega Trends, breakthrough best practices, changing customer dynamics and

emerging economies?

Contact Us: Start the discussion

CONTACT US +44 (0) 20 7343 8383 • [email protected] • www.frost.com