The State and Future of U.S. Solar

Shayle Kann

Vice President, Research

Greentech Media

U.S. Solar Market Insight Conference

December 2013

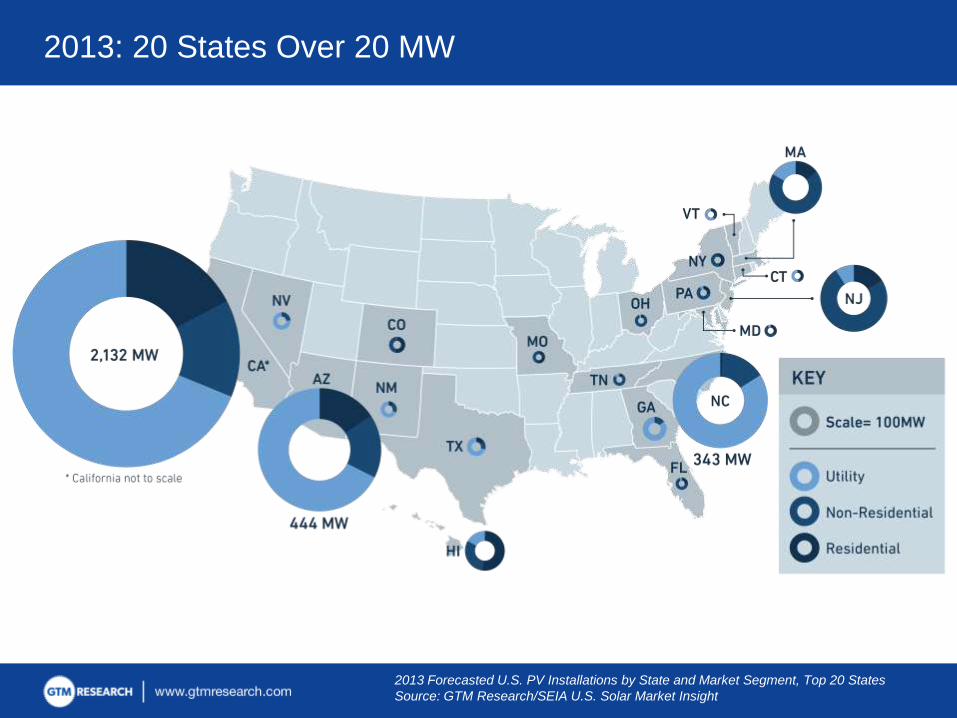

2013: 20 States Over 20 MW

2013 Forecasted U.S. PV Installations by State and Market Segment, Top 20 States

Source: GTM Research/SEIA U.S. Solar Market Insight

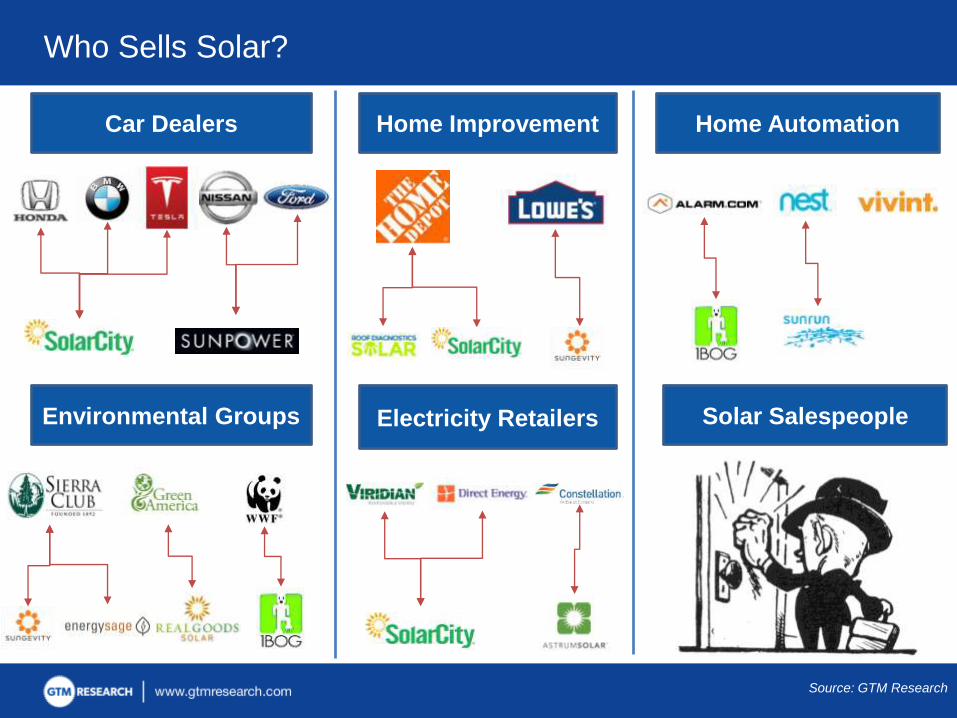

Who Sells Solar?

Car Dealers Home Improvement Home Automation

Environmental Groups Electricity Retailers Solar Salespeople

Source: GTM Research

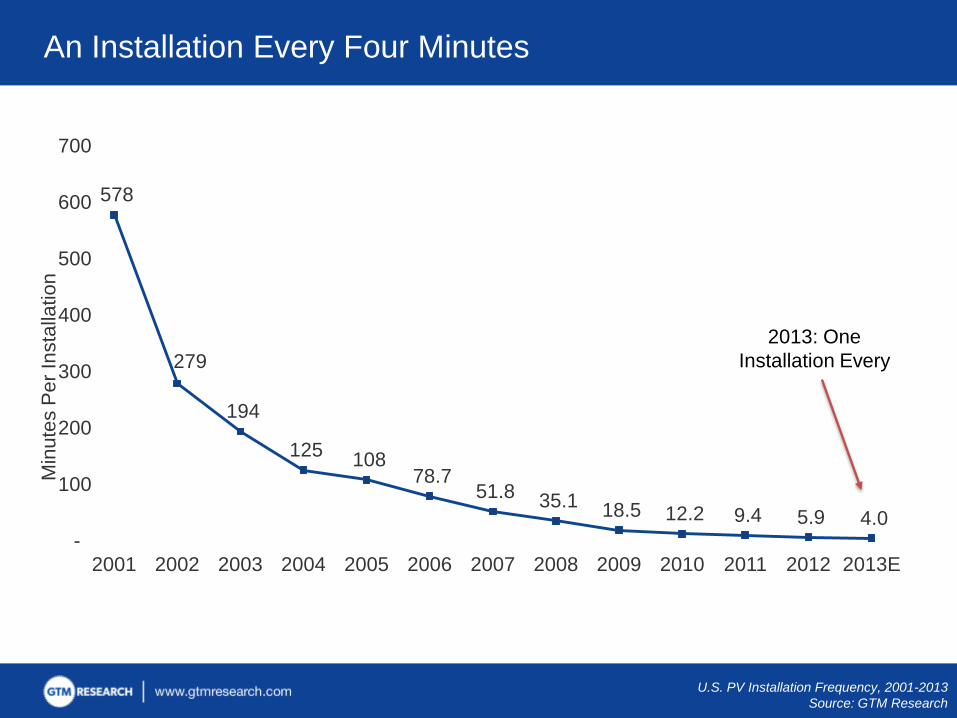

An Installation Every Four Minutes

578

279

194

125 108

78.7 51.8 35.1

18.5 12.2 9.4 5.9 4.0 -

100

200

300

400

500

600

700

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E

Min

ute

s P

er

Insta

llatio

n

2013: One

Installation Every

U.S. PV Installation Frequency, 2001-2013

Source: GTM Research

Our Checklist

In order to be mainstream, solar must be…

a primary source of new electric capacity

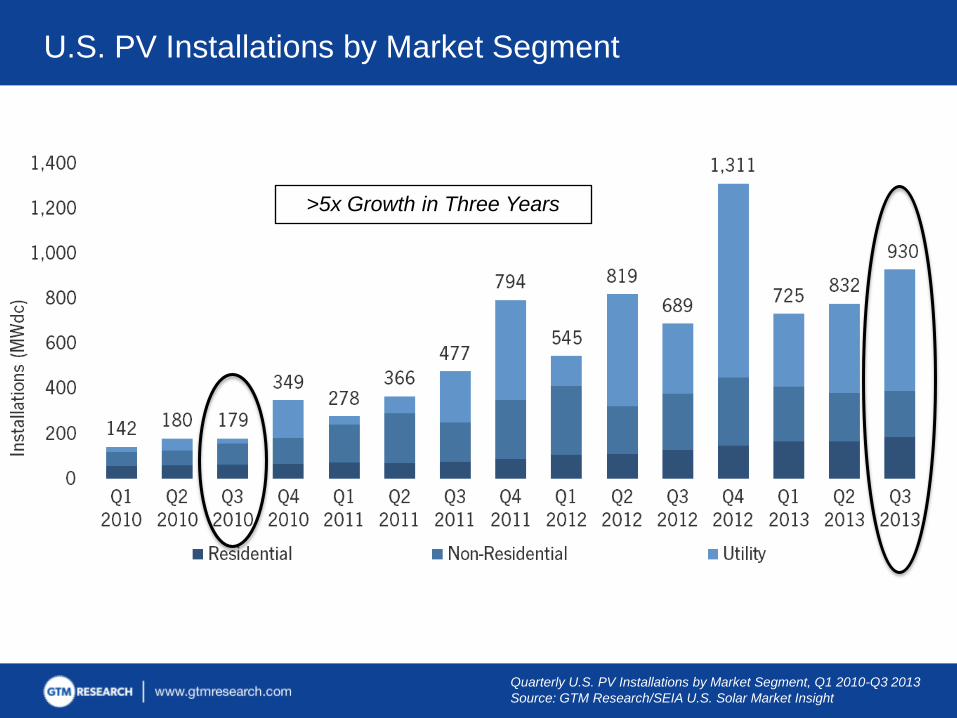

U.S. PV Installations by Market Segment

>5x Growth in Three Years

Quarterly U.S. PV Installations by Market Segment, Q1 2010-Q3 2013

Source: GTM Research/SEIA U.S. Solar Market Insight

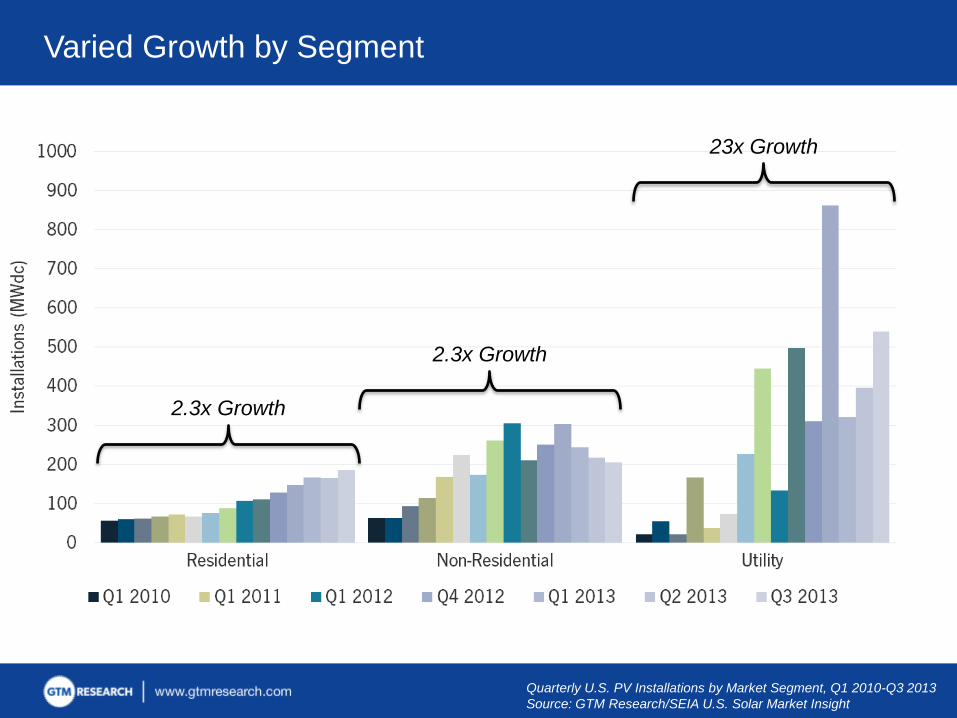

Varied Growth by Segment

Quarterly U.S. PV Installations by Market Segment, Q1 2010-Q3 2013

Source: GTM Research/SEIA U.S. Solar Market Insight

2.3x Growth

2.3x Growth

23x Growth

We’re Number Two!

New Capacity Additions, Q1-Q3 2012 and 2013. FERC figures used for all technologies other than

solar, GTM/SEIA figures used for solar

Source: FERC, GTM Research/SEIA U.S. Solar Market Insight

U.S.A.! U.S.A! U.S.A.!

Cumulative New PV Installations in 2013, U.S. vs. Germany

Source: GTM Research

Our Checklist

In order to be mainstream, solar must be…

cost-competitive without reliance on fickle incentives

a primary source of new electric capacity

We are the 82%

2013 U.S. PV Installations by State, Q1-Q3 2013

Source: GTM Research/SEIA U.S. Solar Market Insight

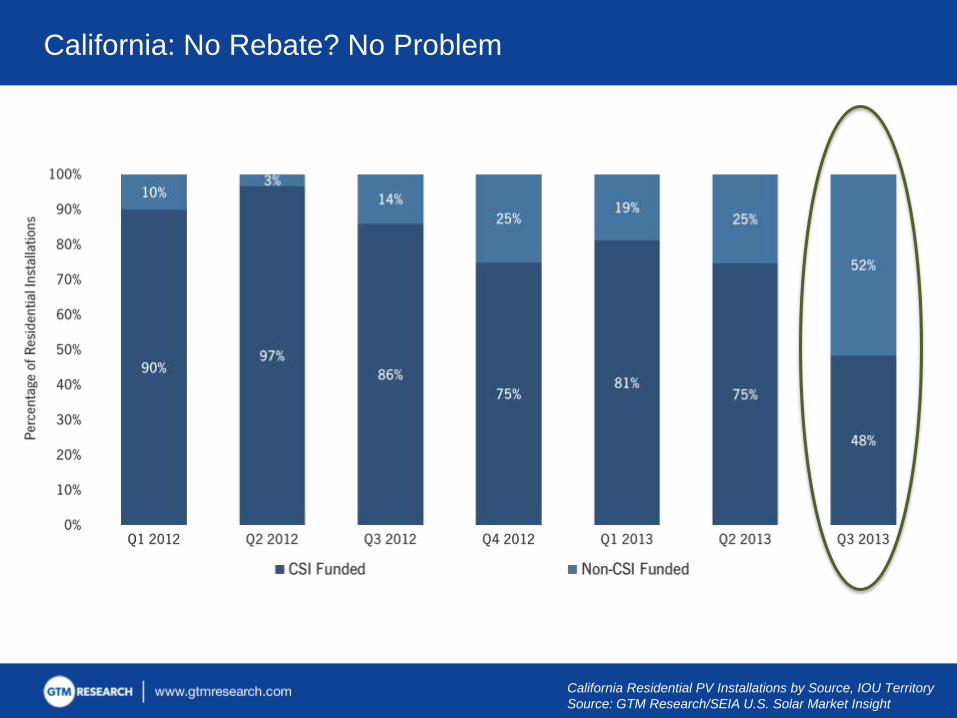

California: No Rebate? No Problem

California Residential PV Installations by Source, IOU Territory

Source: GTM Research/SEIA U.S. Solar Market Insight

taken seriously by the electricity industry

Our Checklist

In order to be mainstream, solar must be…

cost-competitive without reliance on fickle incentives

a primary source of new electric capacity

The Utility Transformation Report Bandwagon

2013 Net Metering Battlegrounds

Source: GTM Research

CA

ID

AZ

TX

CO

GALA

MOVA

VT

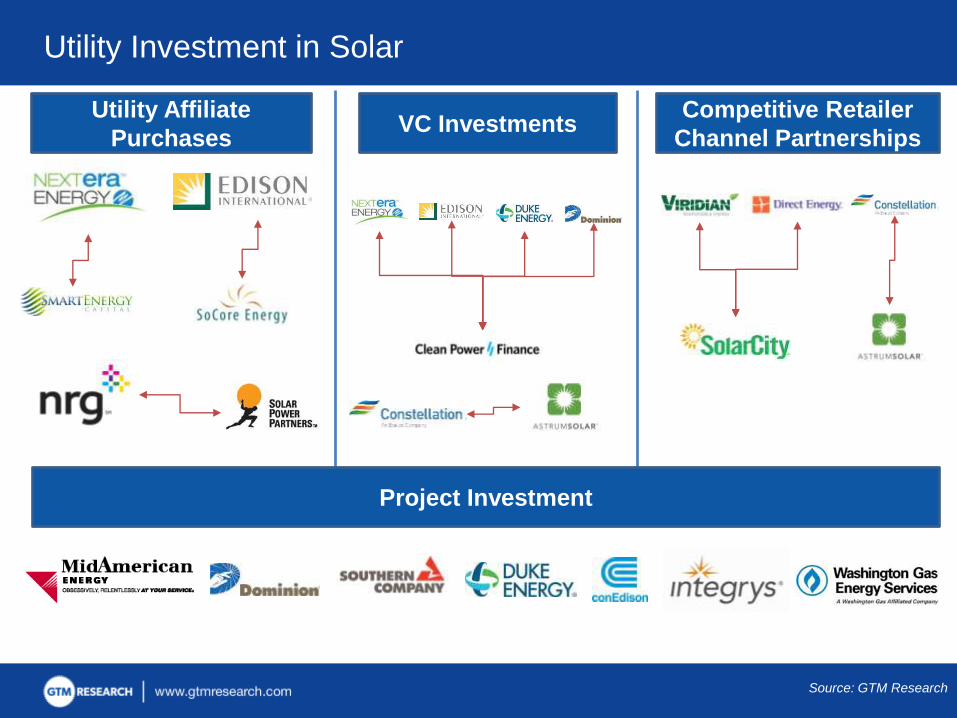

Utility Affiliate

PurchasesVC Investments

Competitive Retailer

Channel Partnerships

Project Investment

Utility Investment in Solar

Source: GTM Research

Our Checklist

In order to be mainstream, solar must be…

cost-competitive without reliance on fickle incentives

a primary source of new electric capacity

taken seriously by the electricity industry

bankable

Project Finance Milestones Abound

Project Finance in Residential

SolarStock Performance: NRG Yield

Source: GTM Research, Google Finance

Setting the Precedent: SolarCity’s First Securitized Portfolio

Source: GTM Research, Google Finance

bankable

taken seriously by the electricity industry

Our Checklist

In order to be mainstream, solar must be…

cost-competitive without reliance on fickle incentives

a primary source of new electric capacity

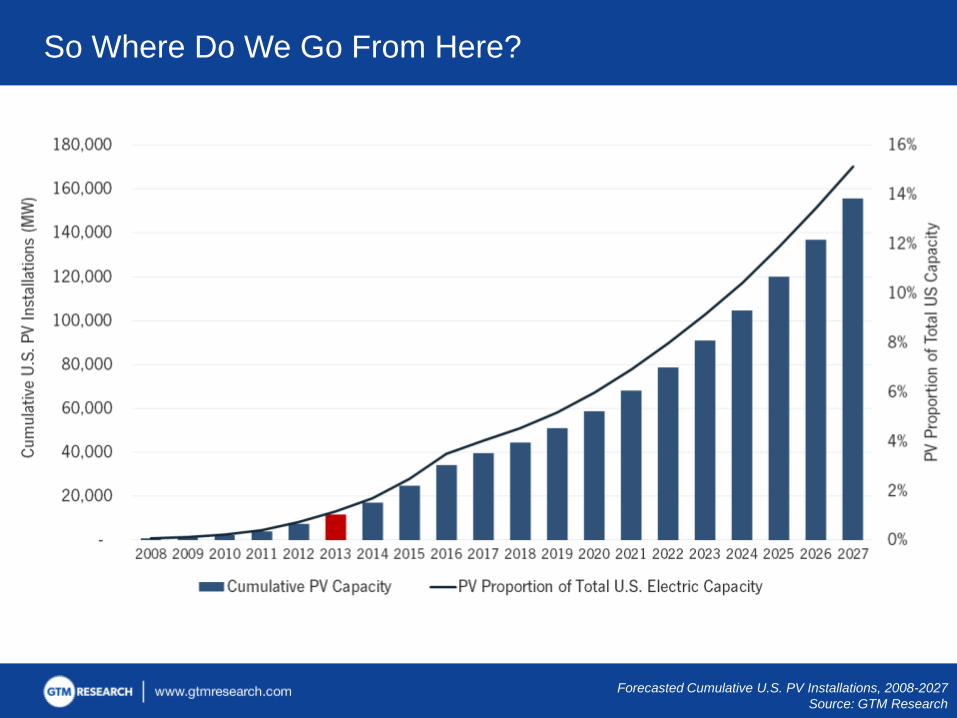

So Where Do We Go From Here?

Forecasted Cumulative U.S. PV Installations, 2008-2027

Source: GTM Research

Thank You!

Shayle Kann

Vice President, Research

Greentech Media