Energy Security in aEnergy Security in a

Resource Constrained WorldResource Constrained World

Presented by: Erica Johnson

Chief Officer: Customer Network Business

Eskom

27 October 2008

AMEU Conference

Presentation Themes

Global Resource Constraints – regional energy constraints understood within the global context

Current South African energy position – understanding the hard realities

Climate change and technology options - a range of choices but at what cost

Closer to home – what’s happening in electricity supply

In conclusion – what’s the current opportunity for South Africa

Global Energy Trends

Global energy market trends

• Energy market is huge – 10% of worlds GDP or $ 6 trillion pa

• Energy demand increasing rapidly

• Leading innovators, technologists and financiers moving into energy – next potential boom will dwarf information technology

• Slowly moving to the true cost of energy – new economic models, full life cycle costing & impacts

• Incremental change rather than revolutionary, but things can change rapidly

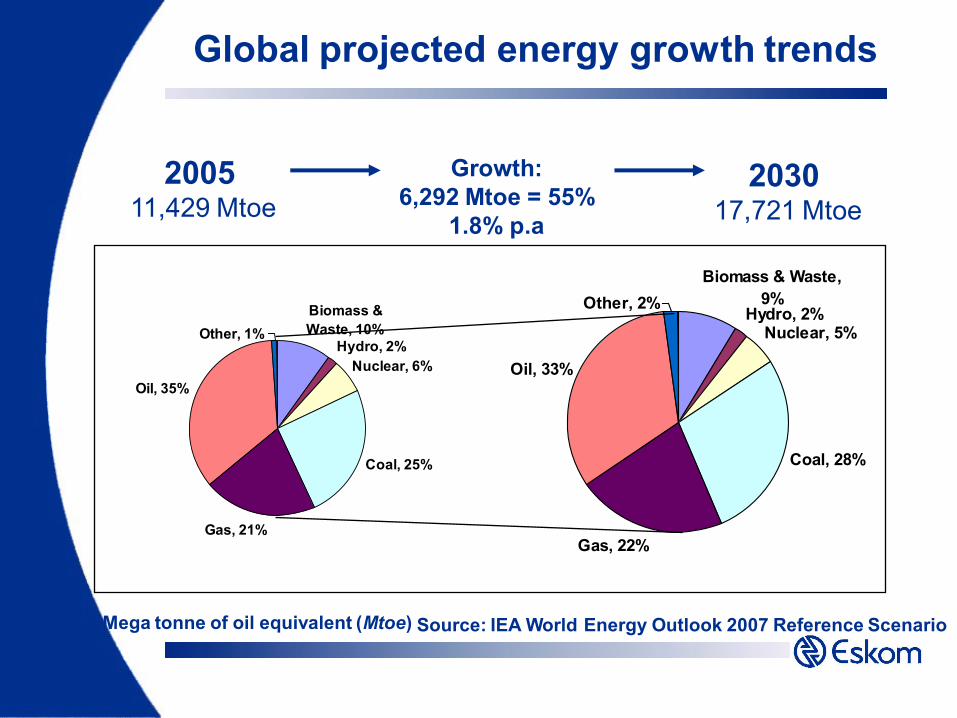

Hydro, 2%Nuclear, 5%

Coal, 28%

Gas, 22%

Oil, 33%

Other, 2%

Biomass & Waste,

9%

Global projected energy growth trends

Mega tonne of oil equivalent (Mtoe)

200511,429 Mtoe

203017,721 Mtoe

Growth:

6,292 Mtoe = 55%

1.8% p.a

Source: IEA World Energy Outlook 2007 Reference Scenario

Biomass &

Waste, 10%

Hydro, 2%

Nuclear, 6%

Coal, 25%

Gas, 21%

Oil, 35%

Other, 1%

Global energy trends leading to

resource constraints

• Demand Growth– Global usage patterns have changed and will accelerate

– Substantial economic growth in Asia, overtaking European and North American energy demand

• Improvements in energy intensity will soften impact of growth

• Supply limitations– There is a finite supply of fossil fuels

– The Hubbert peak proposition

• Point in time where fossil fuel production in a region peaks before going into decline

• The peak has occurred in specific regions

• Debate regarding the global peak – is it approaching or has it already been reached?

South African Energy Position

Regional comparisons of Energy Intensity

Source: EPRI, WRI (2005), Earthtrends data web site

South Africa’s energy intensity grew from 1990 to 2000 before dipping by

2004 due to growth in the tertiary sectors(finance, retail etc) relative to energy

intensive primary sectors (manufacturing and mining)

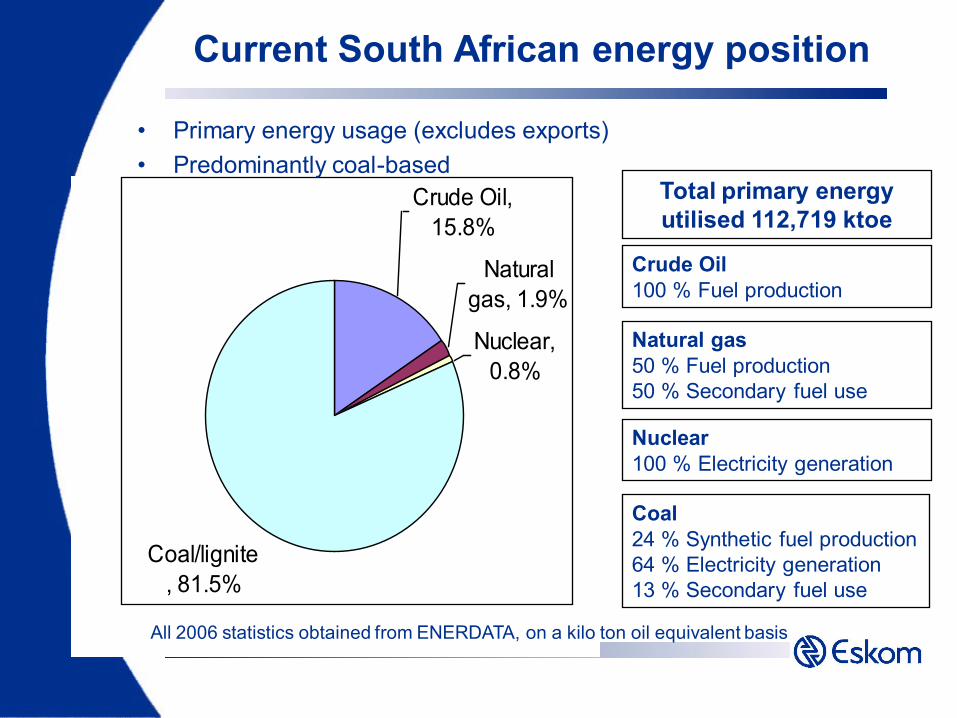

Crude Oil,

15.8%

Natural

gas, 1.9%

Nuclear,

0.8%

Coal/lignite

, 81.5%

Current South African energy position

• Primary energy usage (excludes exports)

• Predominantly coal-based

All 2006 statistics obtained from ENERDATA, on a kilo ton oil equivalent basis

Coal

24 % Synthetic fuel production

64 % Electricity generation

13 % Secondary fuel use

Crude Oil

100 % Fuel production

Natural gas

50 % Fuel production

50 % Secondary fuel use

Nuclear

100 % Electricity generation

Total primary energy

utilised 112,719 ktoe

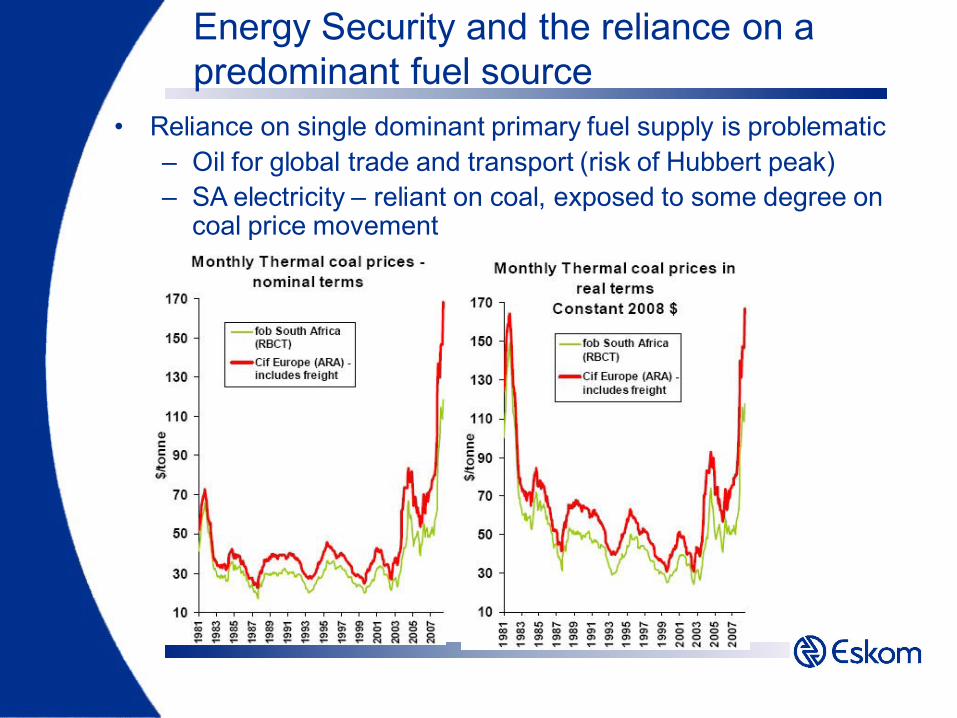

Energy Security and the reliance on a

predominant fuel source

Source: EPRI, Macquarie Research

• Reliance on single dominant primary fuel supply is problematic

– Oil for global trade and transport (risk of Hubbert peak)

– SA electricity – reliant on coal, exposed to some degree on coal price movement

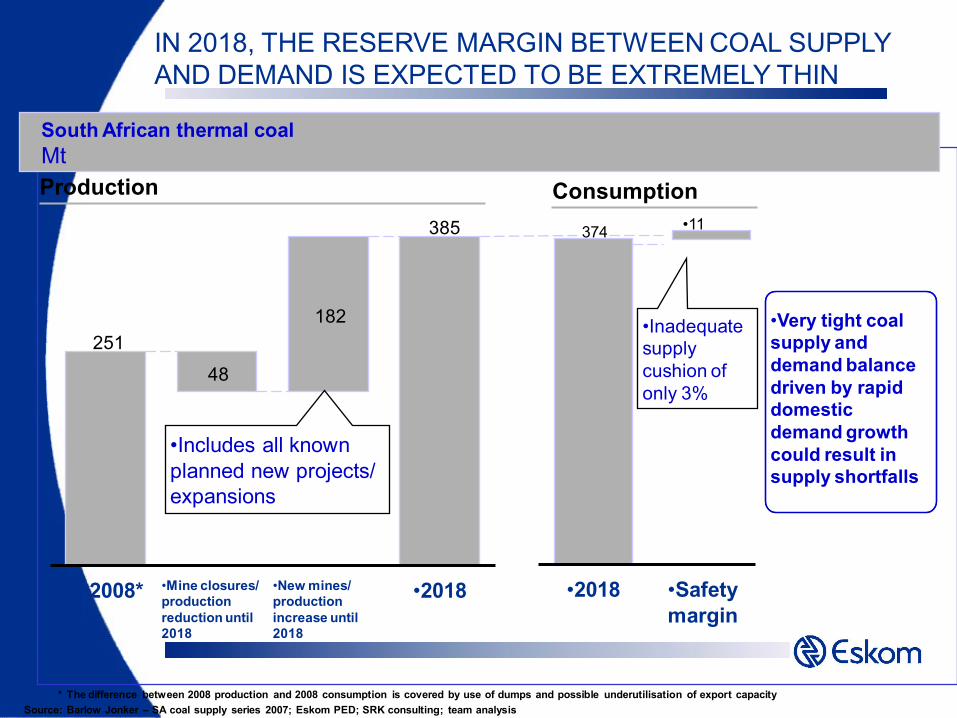

IN 2018, THE RESERVE MARGIN BETWEEN COAL SUPPLY

AND DEMAND IS EXPECTED TO BE EXTREMELY THIN

South African thermal coal

Mt

•2008* •Mine closures/

production

reduction until

2018

•New mines/

production

increase until

2018

•2018

•11

•2018 •Safety

margin

Production Consumption

* The difference between 2008 production and 2008 consumption is covered by use of dumps and possible underutilisation of export capacity

Source: Barlow Jonker – SA coal supply series 2007; Eskom PED; SRK consulting; team analysis

•Very tight coal

supply and

demand balance

driven by rapid

domestic

demand growth

could result in

supply shortfalls

48

182

385

251

•Includes all known

planned new projects/

expansions

374

•Inadequate

supply

cushion of

only 3%

SA energy economy change drivers

• Electricity generation and new build programme

– Low grade coal no longer cheap

– Global competition for equipment supply and scare skills

– Rising costs of current electricity production

– Daunting environmental costs and global pressure on Eskom to reduce carbon footprint

– Huge capital requirements for new plant.

– Funding access limitations in the current global credit crunch?

– Government financial support required and tariffs need to increase substantially

– Coal and classic nuclear the only short/medium term viable options

– Rapid build program and investment in new mines required

• But the opportunity to fundamentally shift the energy landscape lies in these multitude of change drivers…..

Looking to the Future

Long-Term Electricity Demand Forecasts

Long term forecasts - national + foreign

30000

40000

50000

60000

70000

80000

90000

2005 2010 2015 2020 2025

MW

Position

Moderate

Additional 40 000MW added to current capacity

56 710MW

77 960MWEskom position based on 4%

electricity growth supporting

6% GDP growth

Eskom moderate position

2.3% electricity growth

based GDP growth of 4%

Climate Change• IPCC links fossil fuel burning to global

warming

– Focus on shifting primary energy from fossil fuels

– Expected that SA will have Kyoto II obligations on emissions

– DME targets for renewable energy production

– ISEP-11 includes 1620MW of renewable capacity

– Base load nuclear power stations present an opportunity to limit the carbon emissions

• Adaptation has to start now!

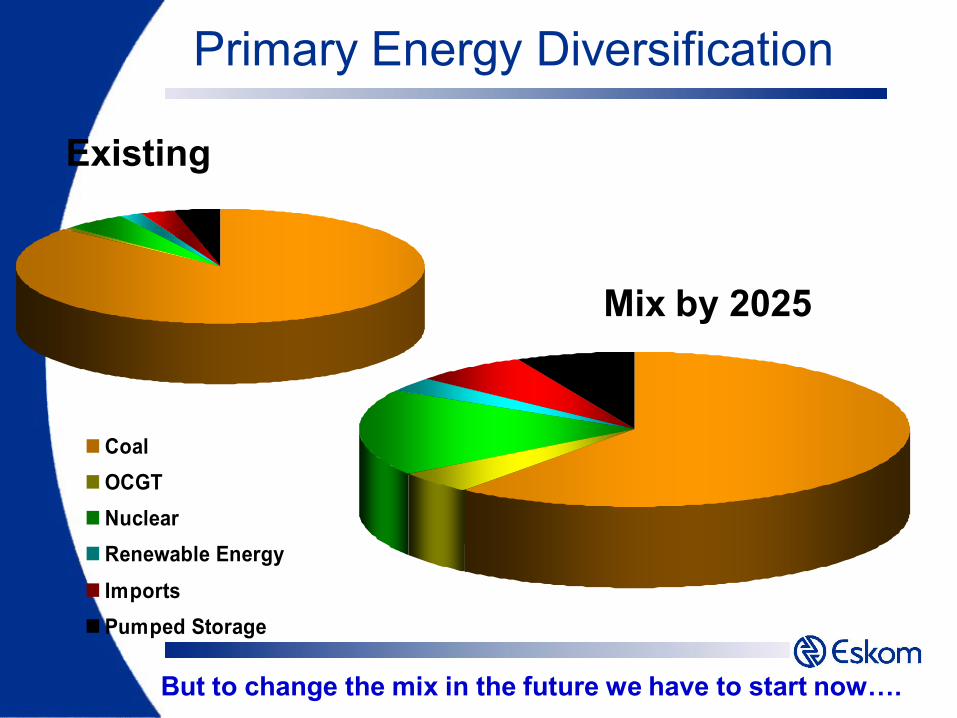

Primary Energy Diversification

Coal

OCGT

Nuclear

Renewable Energy

Imports

Pumped Storage

Existing

Mix by 2025

But to change the mix in the future we have to start now….

Technology Options

Efficiency

Transmission

Renewables

Nuclear

Coal

Gas turbines

Pumped storage

Technology Options

• Developing countries moving to green solutions

• Wind power has come of age – growing at 30% pa

• Carbon capture may make coal ok – expensive and risky

• Nuclear – maybe they can overcome the image problem

• Photo Voltaic is getting steadily cheaper – reduces network needs and opens up distributed power provision

• Geothermal – potential, but extraction still tricky

• Biofuels – smart crops and processes likely with potential for an agrarian revolution in poor equatorial regions

Technology Challenges• Renewable options

– Hydro: run of river (less

predictable) versus damming

rivers (environmental and

social impacts)

– Wind: costly and highly

unpredictable (impact on

system stability)

– Solar: costly and weather-

dependent

– Progress is being made

(technology wise) – will it be

enough?

Palmiet Pump Storage

Technology Challenges• Diversification of resources

– Energy White Paper calls for diversification of primary energy,

relevant for energy security

– Only alternative fuel source possibilities in South Africa

• Natural gas

– Limited local potential for natural gas currently (piped or

imported LNG)

– A very expensive choice but with a lower carbon emissions

footprint than coal

• Nuclear programme

– Historically nuclear power not competitive with coal

– Politically and socially unpalatable (post Chernobyl and 3

Mile Island)

– Climate change and carbon taxes may make nuclear viable

• Issues of storage of spent fuel remain and self-sufficiency in fuel

production remain

…we need to push the energy conversion frontier…..

Carbon Capture and

Storage HVDC

Transmission

Ocean

Current

Energy

Solar Thermal

Advanced

efficiency

Regional

Hydro

Power

Advanced

Nuclear

Underground

Coal gasification

Biomass

Cogeneration

Technology opportunities under development

Reliability of Electricity Supply in South Africa

Impact of 3000 MW reduction

20000

22000

24000

26000

28000

30000

32000

34000

36000

38000

40000

42000

44000

46000

480001

98

8

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Peak D

em

an

d a

nd

Cap

acit

y

Actual Peak Demand Expected Peak DemandActual Peak Demand less Load Reductions Expected Peak Demand less Load ReductionsInstalled Capacity Operational CapacityOperational plus Contingency Capacity

Historical Growth in Electricity Demand

-4

-2

0

2

4

6

8

10

12

14

16

18

20

03 05 07 09 11 13 15

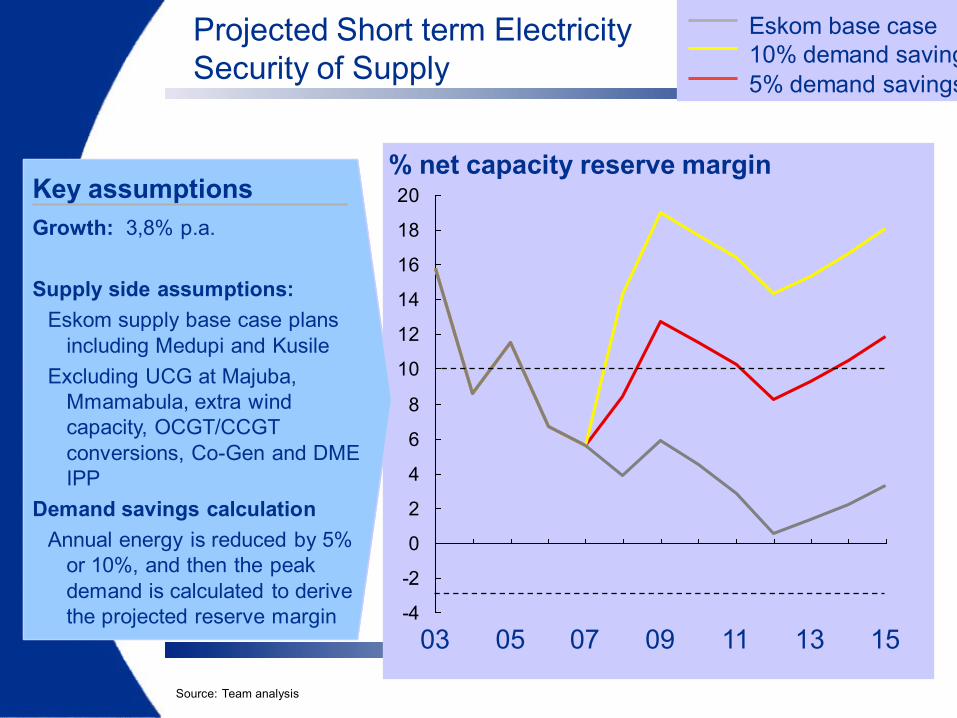

Projected Short term Electricity

Security of Supply

Eskom base case

10% demand savings

5% demand savings

% net capacity reserve marginKey assumptions

Growth: 3,8% p.a.

Supply side assumptions:

Eskom supply base case plans

including Medupi and Kusile

Excluding UCG at Majuba,

Mmamabula, extra wind

capacity, OCGT/CCGT

conversions, Co-Gen and DME

IPP

Demand savings calculation

Annual energy is reduced by 5%

or 10%, and then the peak

demand is calculated to derive

the projected reserve margin

Source: Team analysis

Long Term Adequacy Plans• Eskom plans (ISEP-11)

– >40GW new build by 2026 (up to

20GW nuclear)

– Ten year build plan

• Two coal-fired base load

stations

• A third base load station yet to

be approved

• Two pump-storage schemes

• Meeting renewable energy

targets

• Emergency peaking plant

• Demand-side management

– Risk of growth not materialising

• Short term mitigation measures

may have long term economic

impact

Ankerlig

OCGT

Medupi

Approved New Build Programme

Return to Service:

Camden: 7 of 8 units in commercial operation

Grootvlei: 2 of 6 units in commercial operation by end May

Komati: 9 units, none in commercial operation as yet

Coal Fired Plant: Medupi and Kusile approved. Units coming on line over 5 year period 2012 – 2016

Wind Power: 100 MW wind farm by 2010

Pumped storage plant: Ingula on line by 2013

Open Cycle Gas Turbines: Doubling of capacity at Ankerlig and Gourikwa from 2009

Nuclear programme: Commercial process underway

Medupi coal fired

power station in

Lephalale

Ingula pumped

storage scheme near

Ladysmith

Return to Service of

Grootvlei (Komati

and Camden) in

Mpumalanga

Gas 1 at Ankerlig

(and Gourikwa) in the

Western Cape

Short Term Mitigation• Until new build kicks in (2012+) require short term mitigation of

intense demand management

– For short-term security of supply

– To adapt to the increased costs of current production

– To optimise the need for long-term build

• Power Conservation Programme (PCP)

– Growth Management

• Limits new projects (>20MVA) until system can

accommodate additional demand

– Energy Conservation Scheme (ECS)

• Mandatory reductions in consumption since voluntary

reductions have not been successful thus far

• Require 10% savings to ensure adequate security margins

and continued economic growth

Short-term Mitigation

• Demand Management

– Pricing

• Expansion plan requires significant capital injection

• Debt costs on top of increased fuel costs

• Lead to substantial price increases

• 2008/09 approved increase was 27,5% nominal

• Higher price increases required over next few years

– Energy efficiency and conservation

• Least cost mechanism to improve security of supply

• Low historic electricity cost has lead to wastage

• Price increases may prompt increased efficiency

• Programmes required to ensure savings are realised

• Conservation less about using energy more efficiently,

but using energy less

Short Term Mitigation

• Supply side options being pursued

– Pilot National Co-generation Programme (PNCP)

• Eskom buying energy from co-generation facilities

• Short term contracts

– Medium Term Power Purchase Programme (MTPPP)

• Eskom buying energy from any producer that can

meet the price parameters published by Eskom

• 10 year contracts

– Multi-site baseload IPP

• Eskom buying energy from successful bidders in

tender expiring end of 2009

• Long term contracts

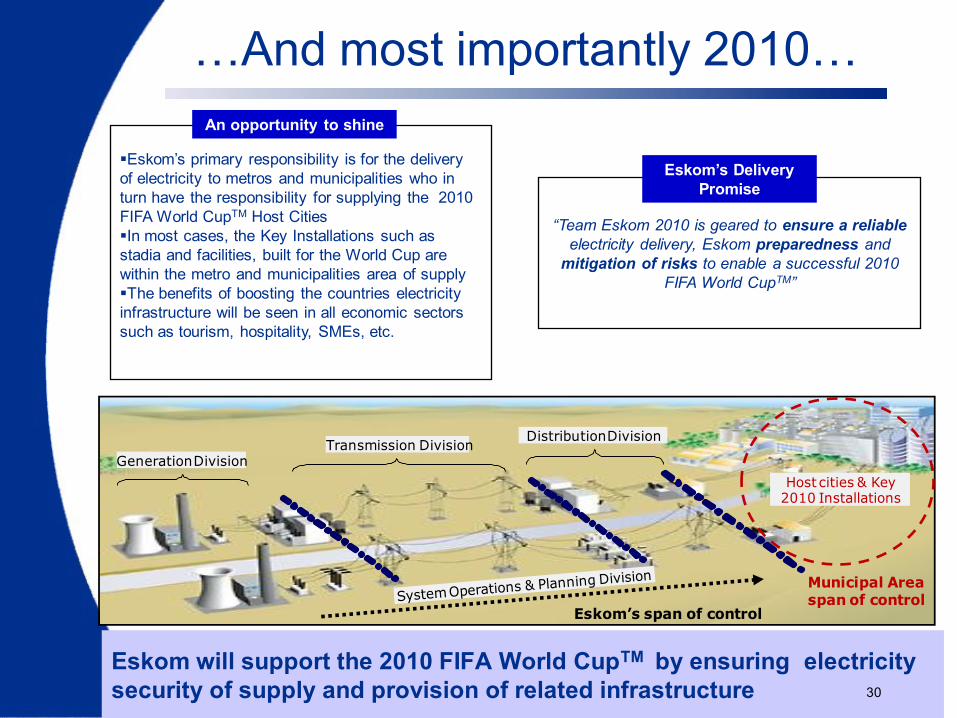

Eskom will support the 2010 FIFA World CupTM by ensuring electricity

security of supply and provision of related infrastructure 30

Generation DivisionTransmission Division

Distribution Division

Host cities & Key 2010 Installations

Eskom’s span of control

Municipal Area span of control

Eskom’s primary responsibility is for the delivery

of electricity to metros and municipalities who in

turn have the responsibility for supplying the 2010

FIFA World CupTM Host Cities

In most cases, the Key Installations such as

stadia and facilities, built for the World Cup are

within the metro and municipalities area of supply

The benefits of boosting the countries electricity

infrastructure will be seen in all economic sectors

such as tourism, hospitality, SMEs, etc.

An opportunity to shine

“Team Eskom 2010 is geared to ensure a reliable

electricity delivery, Eskom preparedness and

mitigation of risks to enable a successful 2010

FIFA World CupTM”

Eskom’s Delivery

Promise

…And most importantly 2010…

In Conclusion

Conclusion….

• The global energy landscape has changed irrevocably with the shift in demand patterns from the developing world

• The rapid local energy changes we are experiencing are not temporary - they are permanent and we must adapt to survive

• There is an opportunity to change the energy intensity of the South African economy

• The South African economy has a huge growth opportunity with the large-scale investments required in the energy sector

• SA electricity costs are artificially low and need to adjust to reflect our new constrained resource environment

• The supply constraints possibly a ‘blessing in disguise’ to get SA to confront more basic energy challenges

Thank YouThank You