Februaryt 2016 | HomeAid OC,

2016 Economic and Housing Outlook

Presented by: Kevin C. Gillen Ph.D., Chief Economist

2March 2016 | OC HomeAid

Agenda

I. Economic Trends in US and CA

II. Housing Market Trends in US and CA

III. Putting It All Together: Summary and

Where We Go From Here

ECONOMIC TRENDS IN US AND CA

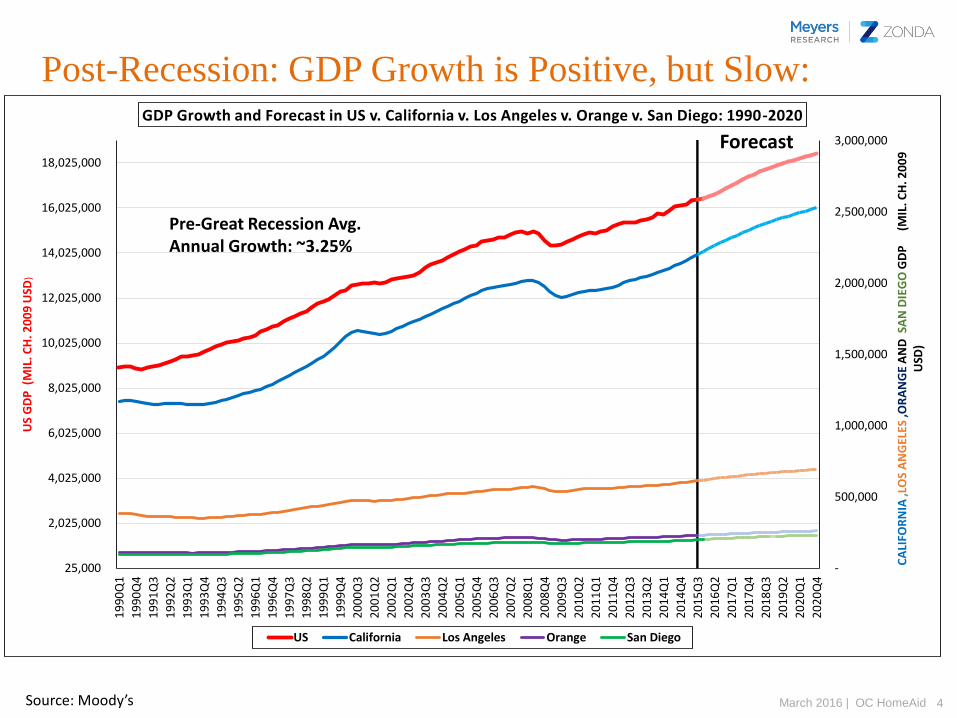

4March 2016 | OC HomeAidSource: Moody’s

Post-Recession: GDP Growth is Positive, but Slow:

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

25,000

2,025,000

4,025,000

6,025,000

8,025,000

10,025,000

12,025,000

14,025,000

16,025,000

18,025,000

1990

Q1

1990

Q4

1991

Q3

1992

Q2

1993

Q1

1993

Q4

1994

Q3

1995

Q2

1996

Q1

1996

Q4

1997

Q3

1998

Q2

1999

Q1

1999

Q4

2000

Q3

2001

Q2

2002

Q1

2002

Q4

2003

Q3

2004

Q2

2005

Q1

2005

Q4

2006

Q3

2007

Q2

2008

Q1

200

8Q

4

2009

Q3

2010

Q2

2011

Q1

2011

Q4

2012

Q3

2013

Q2

2014

Q1

2014

Q4

2015

Q3

2016

Q2

2017

Q1

2017

Q4

2018

Q3

2019

Q2

2020

Q1

2020

Q4

CA

LIFO

RN

IA,L

OS

AN

GEL

ES ,O

RA

NG

E A

ND

SAN

DIE

GO

GD

P

(M

IL. C

H. 2

00

9

USD

)

US

GD

P (

MIL

. CH

. 20

09

USD

)

GDP Growth and Forecast in US v. California v. Los Angeles v. Orange v. San Diego: 1990-2020

US California Los Angeles Orange San Diego

Forecast

Pre-Great Recession Avg. Annual Growth: ~3.25%

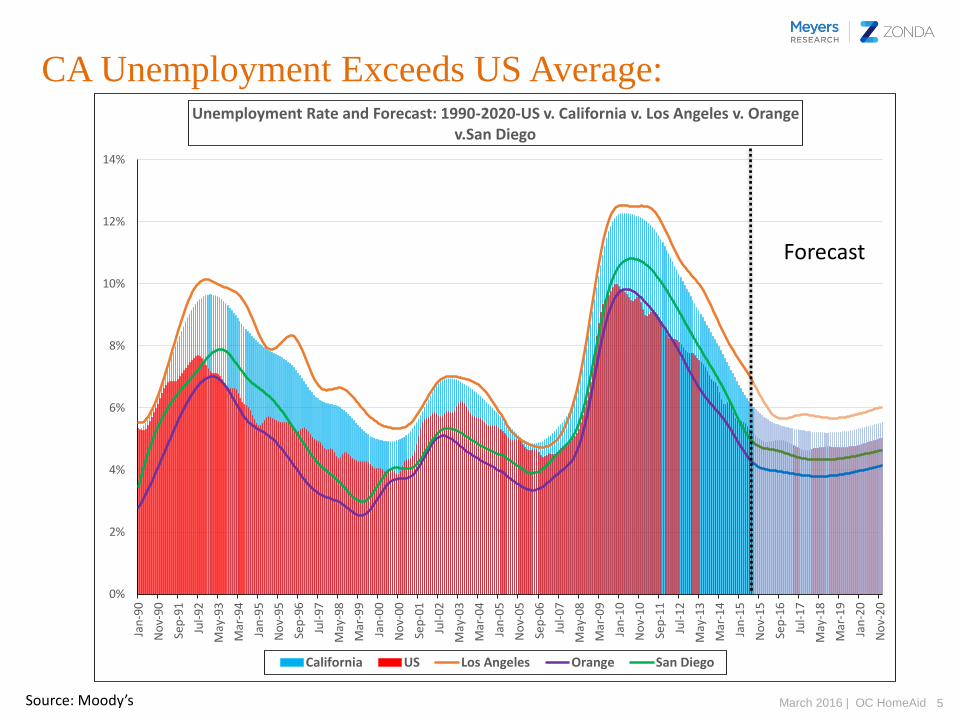

5March 2016 | OC HomeAidSource: Moody’s

CA Unemployment Exceeds US Average:

0%

2%

4%

6%

8%

10%

12%

14%

Jan

-90

No

v-90

Sep

-91

Jul-

92

May

-93

Mar

-94

Jan

-95

No

v-95

Sep

-96

Jul-

97

May

-98

Mar

-99

Jan

-00

No

v-00

Sep

-01

Jul-

02

May

-03

Mar

-04

Jan

-05

No

v-05

Sep

-06

Jul-

07

May

-08

Mar

-09

Jan

-10

No

v-10

Sep

-11

Jul-

12

May

-13

Mar

-14

Jan

-15

No

v-15

Sep

-16

Jul-

17

May

-18

Mar

-19

Jan

-20

No

v-20

Unemployment Rate and Forecast: 1990-2020-US v. California v. Los Angeles v. Orange v.San Diego

California US Los Angeles Orange San Diego

Forecast

6March 2016 | OC HomeAidSource: BLS, Moody’s

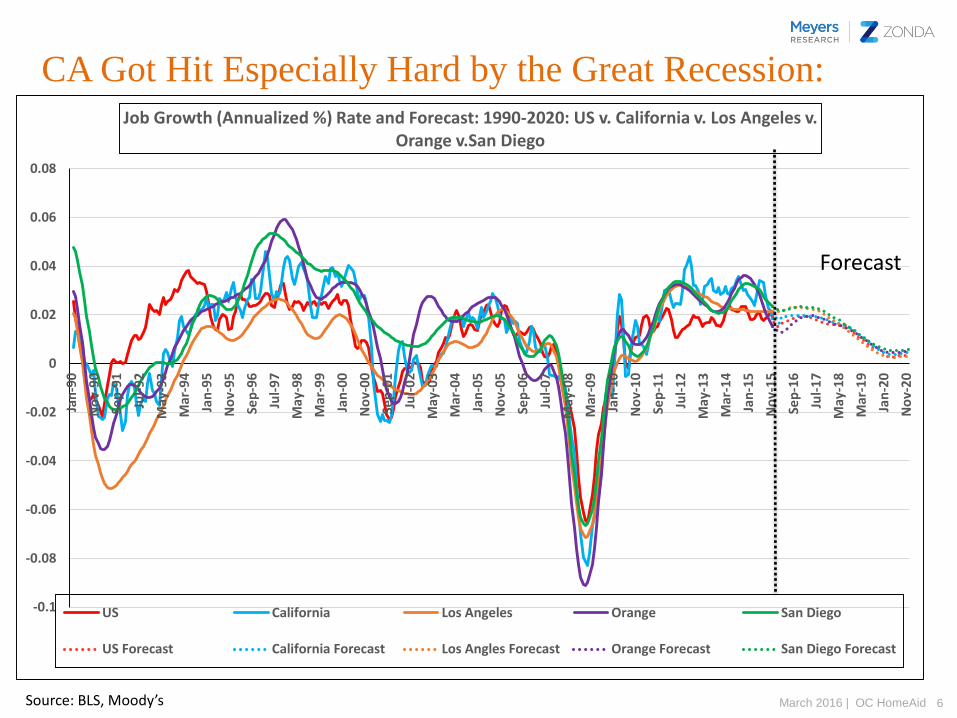

CA Got Hit Especially Hard by the Great Recession:

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

Jan

-90

No

v-9

0

Sep

-91

Jul-

92

May

-93

Mar

-94

Jan

-95

No

v-9

5

Sep

-96

Jul-

97

May

-98

Mar

-99

Jan

-00

No

v-0

0

Sep

-01

Jul-

02

May

-03

Mar

-04

Jan

-05

No

v-0

5

Sep

-06

Jul-

07

May

-08

Mar

-09

Jan

-10

No

v-1

0

Sep

-11

Jul-

12

May

-13

Mar

-14

Jan

-15

No

v-1

5

Sep

-16

Jul-

17

May

-18

Mar

-19

Jan

-20

No

v-2

0

Job Growth (Annualized %) Rate and Forecast: 1990-2020: US v. California v. Los Angeles v. Orange v.San Diego

US California Los Angeles Orange San Diego

US Forecast California Forecast Los Angles Forecast Orange Forecast San Diego Forecast

Forecast

7March 2016 | OC HomeAid

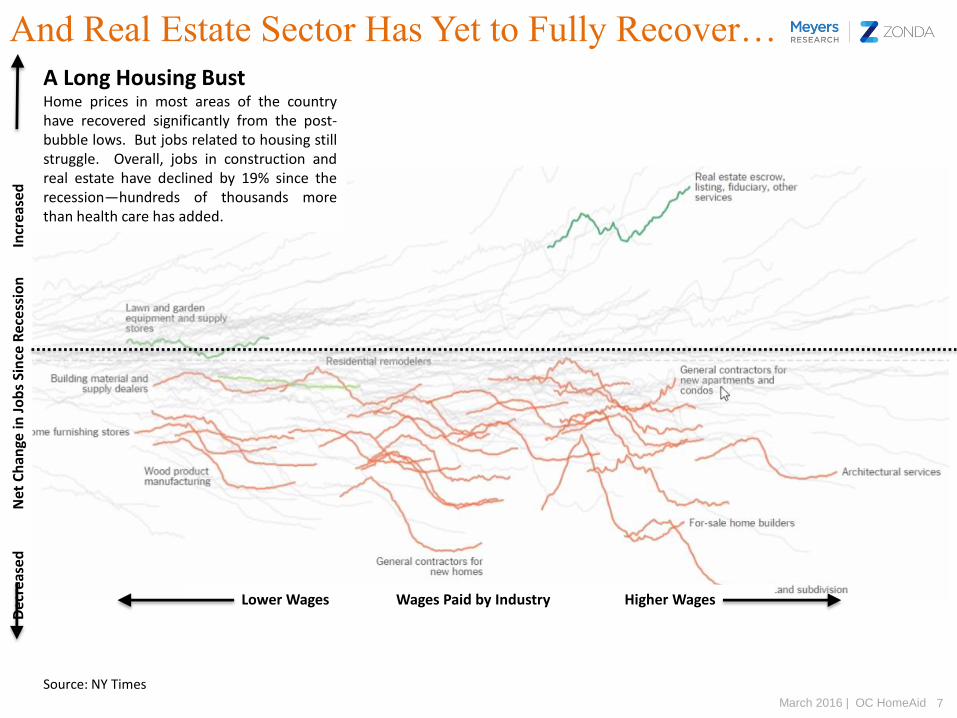

And Real Estate Sector Has Yet to Fully Recover…

Source: NY Times

Dec

reas

ed

Net

Ch

ange

in J

ob

s Si

nce

Rec

ess

ion

In

crea

sed

Lower Wages Wages Paid by Industry Higher Wages

A Long Housing BustHome prices in most areas of the countryhave recovered significantly from the post-bubble lows. But jobs related to housing stillstruggle. Overall, jobs in construction andreal estate have declined by 19% since therecession—hundreds of thousands morethan health care has added.

8March 2016 | OC HomeAidSource: Zonda

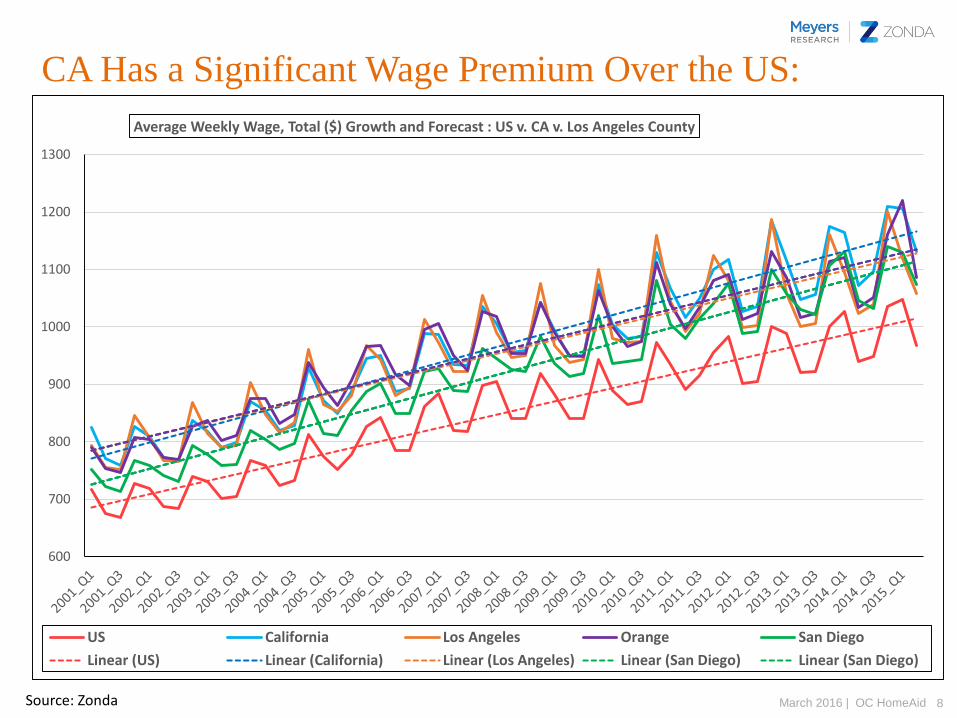

CA Has a Significant Wage Premium Over the US:

600

700

800

900

1000

1100

1200

1300

Average Weekly Wage, Total ($) Growth and Forecast : US v. CA v. Los Angeles County

US California Los Angeles Orange San Diego

Linear (US) Linear (California) Linear (Los Angeles) Linear (San Diego) Linear (San Diego)

9March 2016 | OC HomeAidSource: BEA and Moody’s

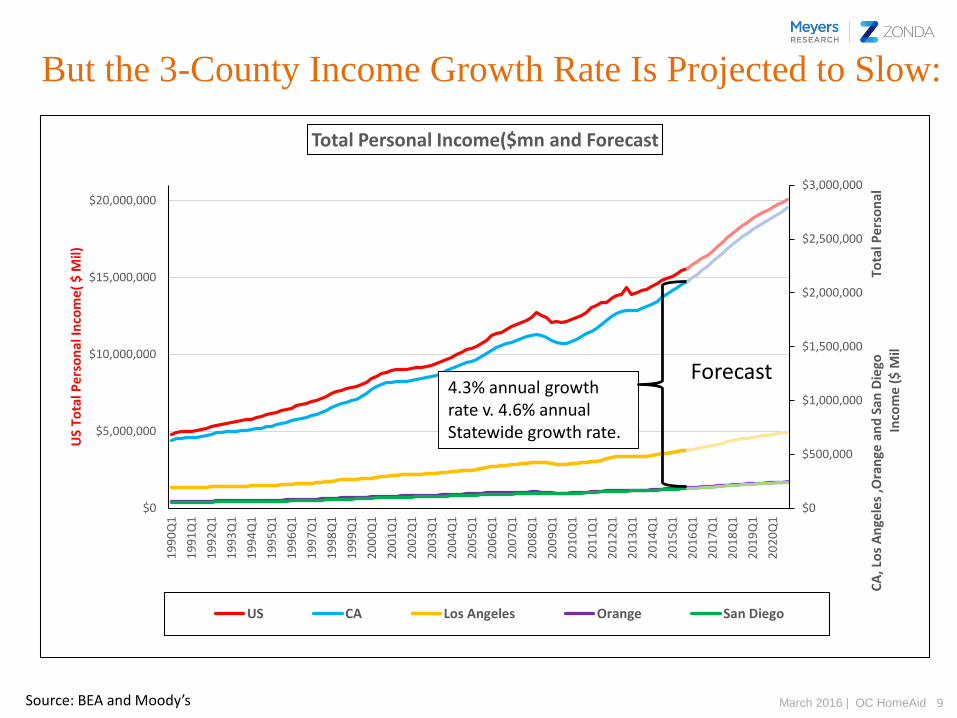

But the 3-County Income Growth Rate Is Projected to Slow:

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

19

90

Q1

19

91

Q1

19

92

Q1

19

93

Q1

19

94

Q1

19

95

Q1

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

20

18

Q1

20

19

Q1

20

20

Q1

CA

, Lo

s A

nge

les

,Ora

nge

an

d S

an D

iego

T

ota

l Pe

rso

nal

In

com

e (

$ M

il

US

Tota

l Pe

rso

nal

Inco

me

( $

Mil)

Total Personal Income($mn and Forecast

US CA Los Angeles Orange San Diego

4.3% annual growth rate v. 4.6% annual Statewide growth rate.

Forecast

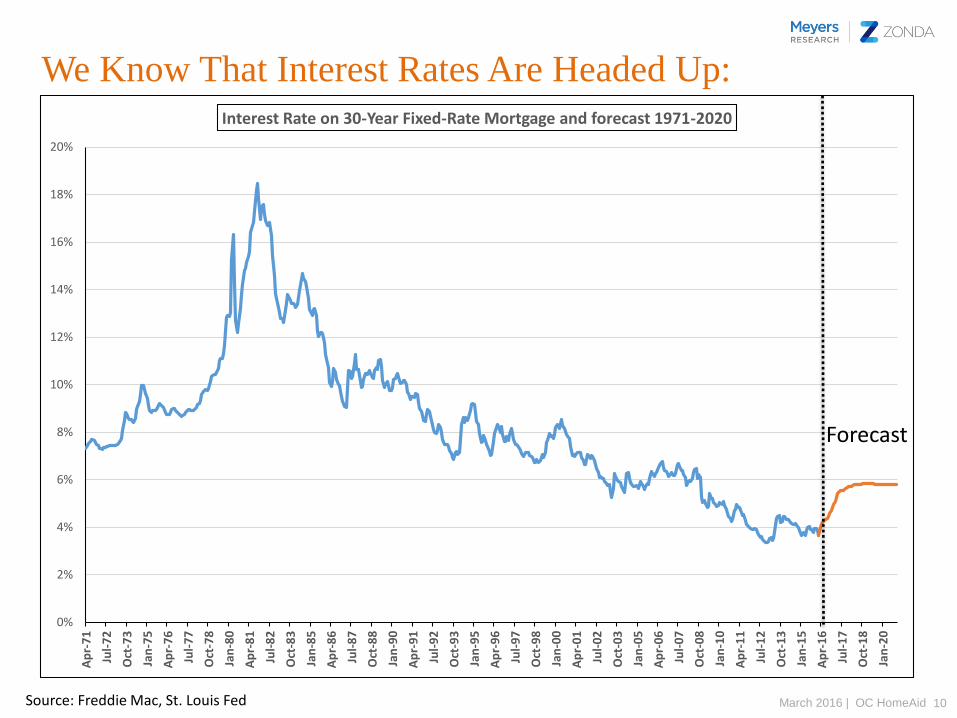

10March 2016 | OC HomeAidSource: Freddie Mac, St. Louis Fed

We Know That Interest Rates Are Headed Up:

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Ap

r-7

1

Jul-

72

Oct

-73

Jan

-75

Ap

r-7

6

Jul-

77

Oct

-78

Jan

-80

Ap

r-8

1

Jul-

82

Oct

-83

Jan

-85

Ap

r-8

6

Jul-

87

Oct

-88

Jan

-90

Ap

r-9

1

Jul-

92

Oct

-93

Jan

-95

Ap

r-9

6

Jul-

97

Oct

-98

Jan

-00

Ap

r-0

1

Jul-

02

Oct

-03

Jan

-05

Ap

r-0

6

Jul-

07

Oct

-08

Jan

-10

Ap

r-1

1

Jul-

12

Oct

-13

Jan

-15

Ap

r-1

6

Jul-

17

Oct

-18

Jan

-20

Interest Rate on 30-Year Fixed-Rate Mortgage and forecast 1971-2020

Forecast

11March 2016 | OC HomeAidSource: Zonda

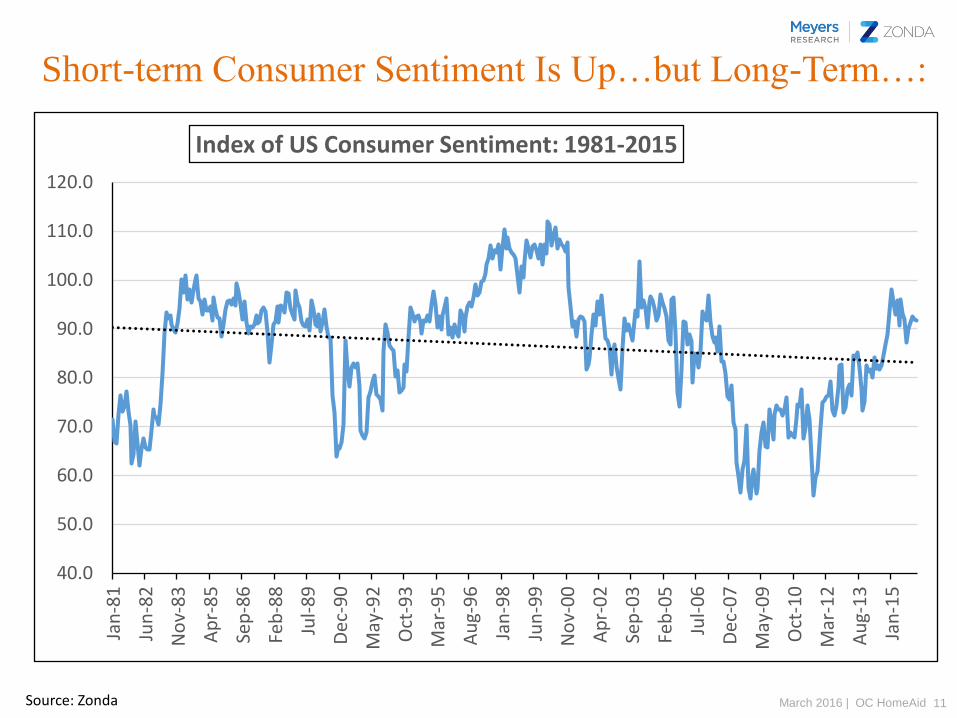

Short-term Consumer Sentiment Is Up…but Long-Term…:

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

Jan

-81

Jun

-82

No

v-83

Ap

r-8

5

Sep

-86

Feb

-88

Jul-

89

Dec

-90

May

-92

Oct

-93

Mar

-95

Au

g-9

6

Jan

-98

Jun

-99

No

v-00

Ap

r-0

2

Sep

-03

Feb

-05

Jul-

06

Dec

-07

May

-09

Oct

-10

Mar

-12

Au

g-1

3

Jan

-15

Index of US Consumer Sentiment: 1981-2015

HOUSING MARKET TRENDS IN US AND CA

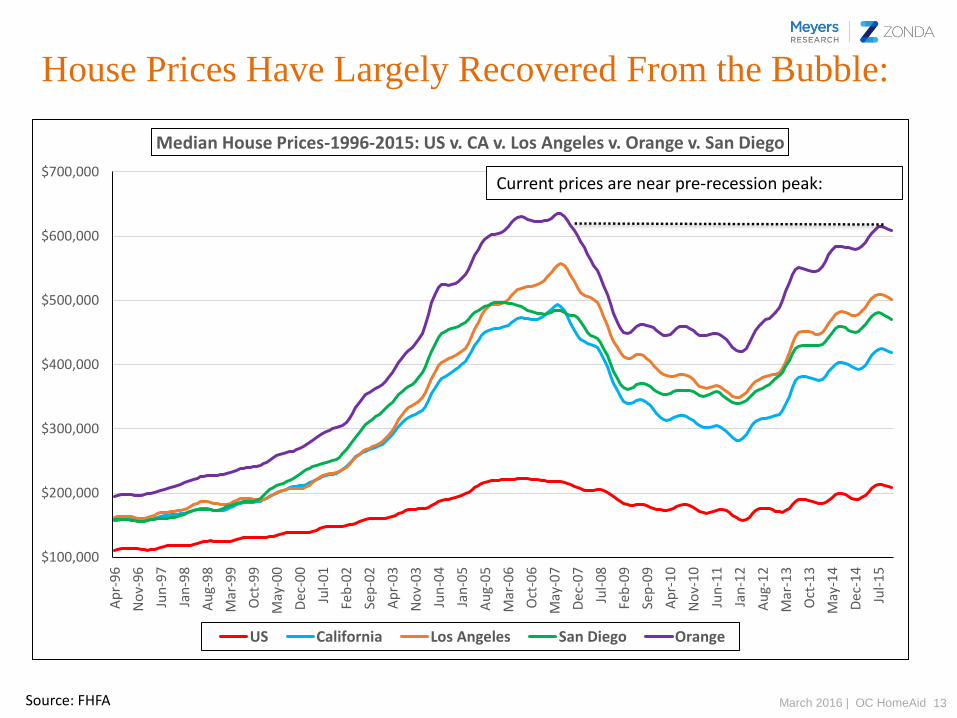

13March 2016 | OC HomeAidSource: FHFA

House Prices Have Largely Recovered From the Bubble:

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

Ap

r-9

6

No

v-96

Jun

-97

Jan

-98

Au

g-9

8

Mar

-99

Oct

-99

May

-00

Dec

-00

Jul-

01

Feb

-02

Sep

-02

Ap

r-0

3

No

v-03

Jun

-04

Jan

-05

Au

g-0

5

Mar

-06

Oct

-06

May

-07

Dec

-07

Jul-

08

Feb

-09

Sep

-09

Ap

r-1

0

No

v-10

Jun

-11

Jan

-12

Au

g-1

2

Mar

-13

Oct

-13

May

-14

Dec

-14

Jul-

15

Median House Prices-1996-2015: US v. CA v. Los Angeles v. Orange v. San Diego

US California Los Angeles San Diego Orange

Current prices are near pre-recession peak:

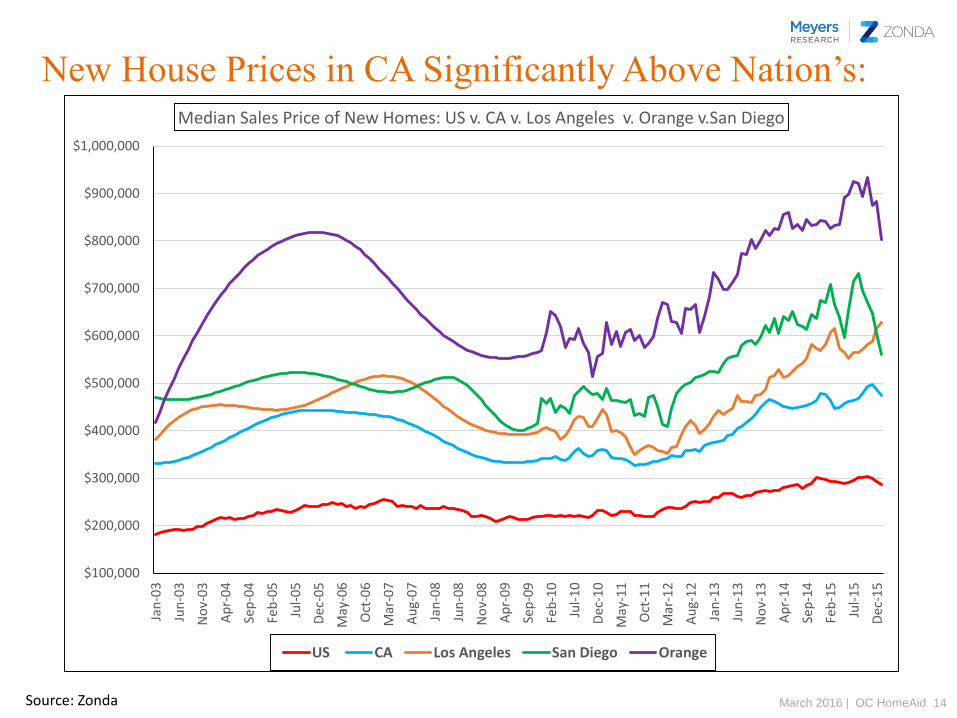

14March 2016 | OC HomeAidSource: Zonda

New House Prices in CA Significantly Above Nation’s:

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000Ja

n-0

3

Jun

-03

No

v-03

Ap

r-0

4

Sep

-04

Feb

-05

Jul-

05

Dec

-05

May

-06

Oct

-06

Mar

-07

Au

g-0

7

Jan

-08

Jun

-08

No

v-08

Ap

r-0

9

Sep

-09

Feb

-10

Jul-

10

Dec

-10

May

-11

Oct

-11

Mar

-12

Au

g-1

2

Jan

-13

Jun

-13

No

v-13

Ap

r-1

4

Sep

-14

Feb

-15

Jul-

15

Dec

-15

Median Sales Price of New Homes: US v. CA v. Los Angeles v. Orange v.San Diego

US CA Los Angeles San Diego Orange

15March 2016 | OC HomeAidSource: Zonda

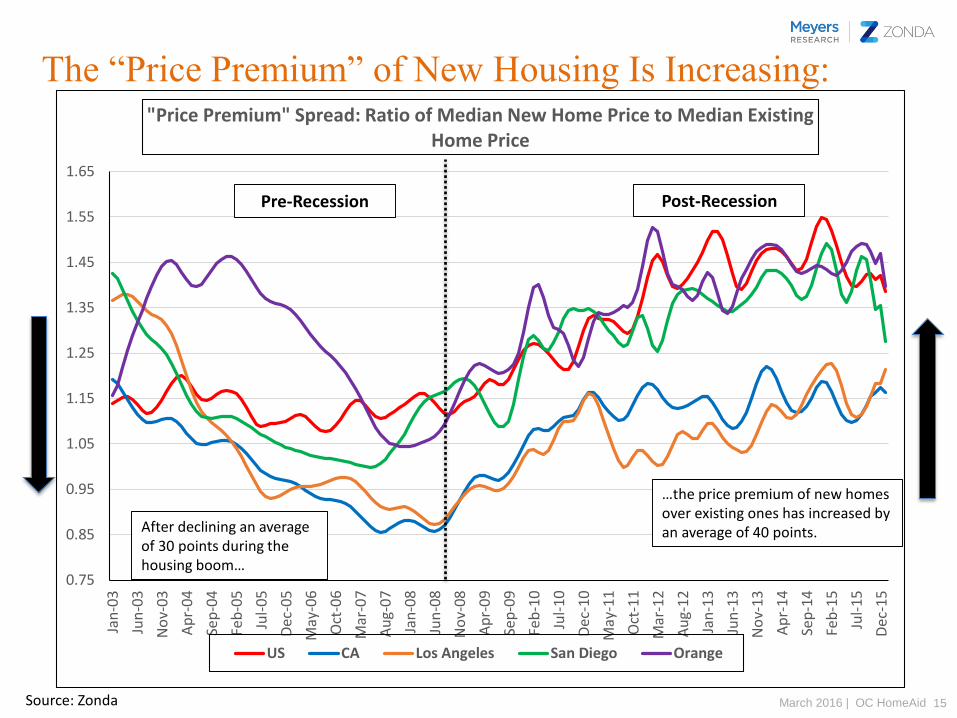

The “Price Premium” of New Housing Is Increasing:

0.75

0.85

0.95

1.05

1.15

1.25

1.35

1.45

1.55

1.65

Jan

-03

Jun

-03

No

v-03

Ap

r-0

4

Sep

-04

Feb

-05

Jul-

05

Dec

-05

May

-06

Oct

-06

Mar

-07

Au

g-0

7

Jan

-08

Jun

-08

No

v-08

Ap

r-0

9

Sep

-09

Feb

-10

Jul-

10

Dec

-10

May

-11

Oct

-11

Mar

-12

Au

g-1

2

Jan

-13

Jun

-13

No

v-13

Ap

r-1

4

Sep

-14

Feb

-15

Jul-

15

Dec

-15

"Price Premium" Spread: Ratio of Median New Home Price to Median Existing Home Price

US CA Los Angeles San Diego Orange

Pre-Recession Post-Recession

After declining an average of 30 points during the housing boom…

…the price premium of new homes over existing ones has increased by an average of 40 points.

16March 2016 | OC HomeAidSource: Zonda

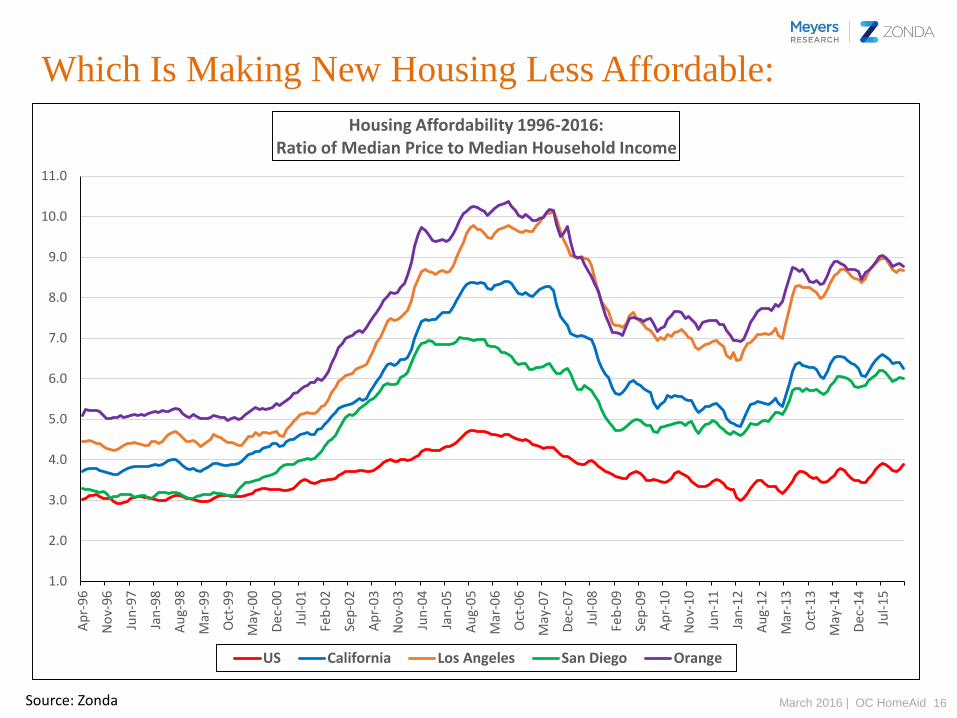

Which Is Making New Housing Less Affordable:

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

Ap

r-9

6

No

v-96

Jun

-97

Jan

-98

Au

g-9

8

Mar

-99

Oct

-99

May

-00

Dec

-00

Jul-

01

Feb

-02

Sep

-02

Ap

r-0

3

No

v-03

Jun

-04

Jan

-05

Au

g-0

5

Mar

-06

Oct

-06

May

-07

Dec

-07

Jul-

08

Feb

-09

Sep

-09

Ap

r-1

0

No

v-10

Jun

-11

Jan

-12

Au

g-1

2

Mar

-13

Oct

-13

May

-14

Dec

-14

Jul-

15

Housing Affordability 1996-2016:Ratio of Median Price to Median Household Income

US California Los Angeles San Diego Orange

17March 2016 | OC HomeAidSource: US Census

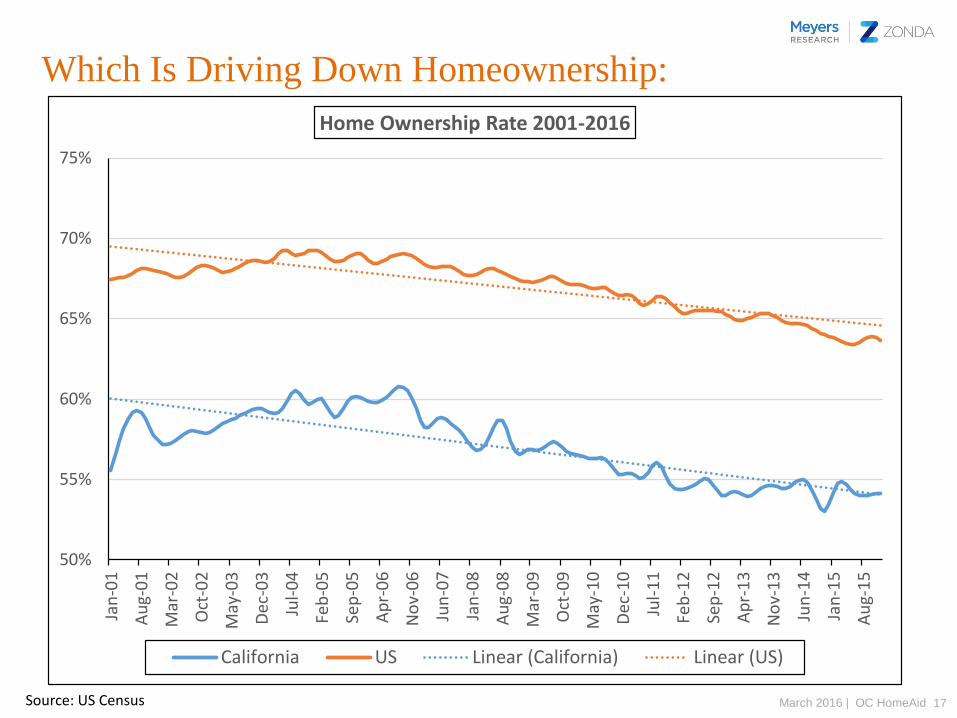

Which Is Driving Down Homeownership:

50%

55%

60%

65%

70%

75%

Jan

-01

Au

g-0

1

Mar

-02

Oct

-02

May

-03

Dec

-03

Jul-

04

Feb

-05

Sep

-05

Ap

r-0

6

No

v-06

Jun

-07

Jan

-08

Au

g-0

8

Mar

-09

Oct

-09

May

-10

Dec

-10

Jul-

11

Feb

-12

Sep

-12

Ap

r-1

3

No

v-13

Jun

-14

Jan

-15

Au

g-1

5

Home Ownership Rate 2001-2016

California US Linear (California) Linear (US)

18March 2016 | OC HomeAidSource: Zonda

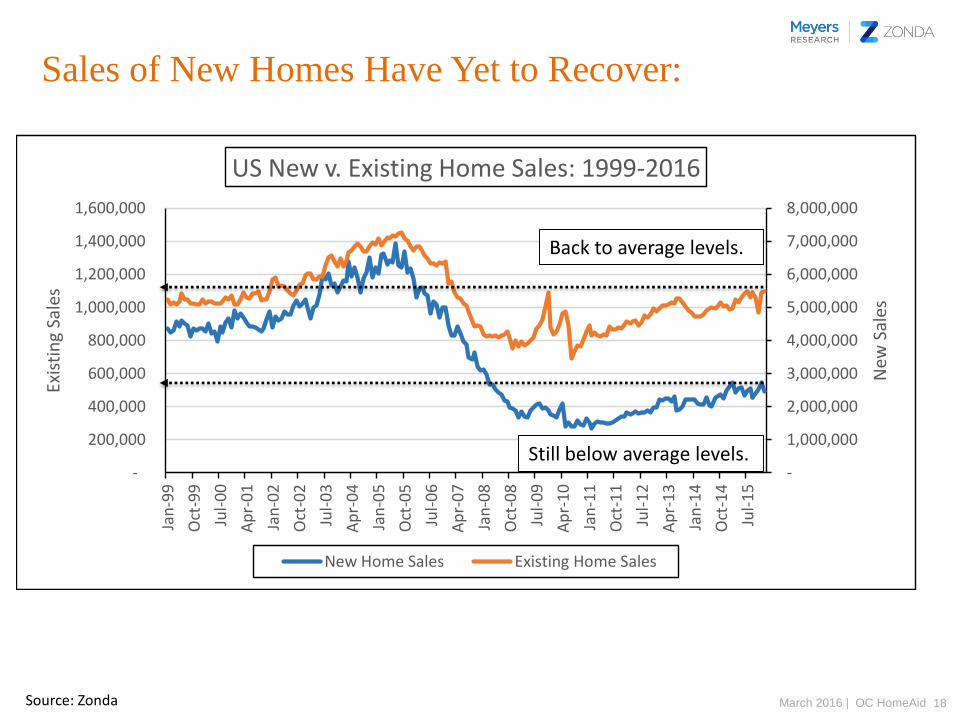

Sales of New Homes Have Yet to Recover:

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Jan

-99

Oct

-99

Jul-

00

Ap

r-0

1

Jan

-02

Oct

-02

Jul-

03

Ap

r-0

4

Jan

-05

Oct

-05

Jul-

06

Ap

r-0

7

Jan

-08

Oct

-08

Jul-

09

Ap

r-1

0

Jan

-11

Oct

-11

Jul-

12

Ap

r-1

3

Jan

-14

Oct

-14

Jul-

15

New

Sal

es

Exis

tin

g Sa

les

US New v. Existing Home Sales: 1999-2016

New Home Sales Existing Home Sales

Back to average levels.

Still below average levels.

19March 2016 | OC HomeAidSource: Census, NAR, NAHB

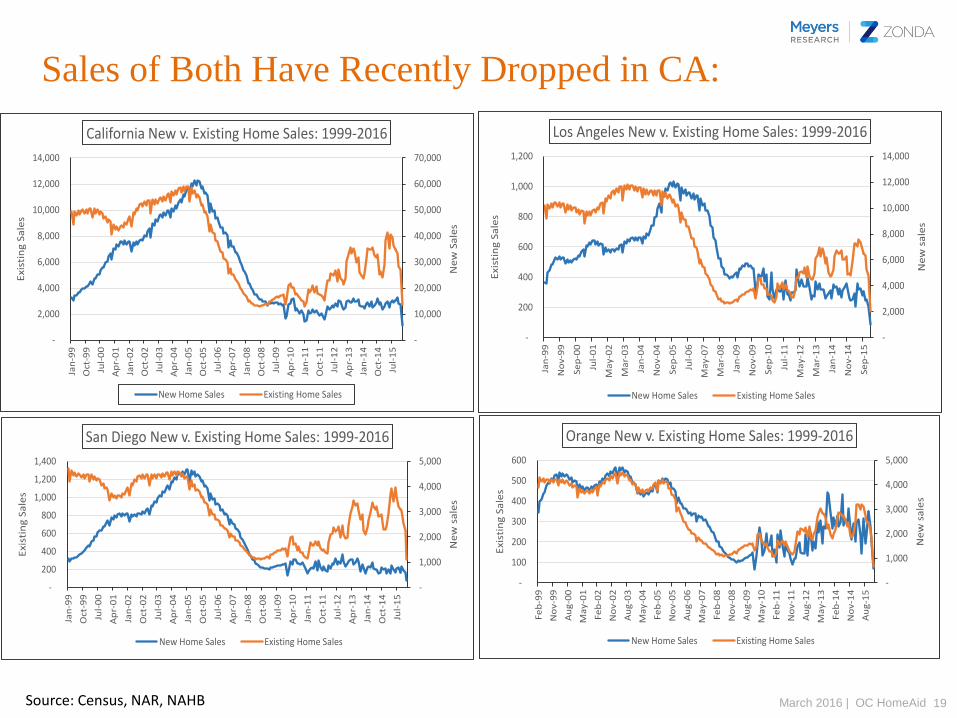

Sales of Both Have Recently Dropped in CA:

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan

-99

Oct

-99

Jul-

00

Ap

r-0

1

Jan

-02

Oct

-02

Jul-

03

Ap

r-0

4

Jan

-05

Oct

-05

Jul-

06

Ap

r-0

7

Jan

-08

Oct

-08

Jul-

09

Ap

r-1

0

Jan

-11

Oct

-11

Jul-

12

Ap

r-1

3

Jan

-14

Oct

-14

Jul-

15

Ne

w S

ale

s

Exi

stin

g S

ale

s

California New v. Existing Home Sales: 1999-2016

New Home Sales Existing Home Sales

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

-

200

400

600

800

1,000

1,200

Jan

-99

No

v-9

9

Se

p-0

0

Jul-

01

Ma

y-0

2

Ma

r-0

3

Jan

-04

No

v-0

4

Se

p-0

5

Jul-

06

Ma

y-0

7

Ma

r-0

8

Jan

-09

No

v-0

9

Sep

-10

Jul-

11

Ma

y-1

2

Ma

r-1

3

Jan

-14

No

v-1

4

Se

p-1

5

Ne

w s

ale

s

Exi

stin

g S

ale

s

Los Angeles New v. Existing Home Sales: 1999-2016

New Home Sales Existing Home Sales

-

1,000

2,000

3,000

4,000

5,000

-

200

400

600

800

1,000

1,200

1,400

Jan

-99

Oct

-99

Jul-

00

Ap

r-0

1

Jan

-02

Oct

-02

Jul-

03

Ap

r-0

4

Jan

-05

Oct

-05

Jul-

06

Ap

r-0

7

Jan

-08

Oct

-08

Jul-

09

Ap

r-1

0

Jan

-11

Oct

-11

Jul-

12

Ap

r-1

3

Jan

-14

Oct

-14

Jul-

15

Ne

w s

ale

s

Exi

stin

g S

ale

s

San Diego New v. Existing Home Sales: 1999-2016

New Home Sales Existing Home Sales

-

1,000

2,000

3,000

4,000

5,000

-

100

200

300

400

500

600

Fe

b-9

9

No

v-9

9

Au

g-0

0

Ma

y-0

1

Fe

b-0

2

No

v-0

2

Au

g-0

3

Ma

y-0

4

Fe

b-0

5

No

v-0

5

Au

g-0

6

Ma

y-0

7

Fe

b-0

8

No

v-0

8

Au

g-0

9

Ma

y-1

0

Fe

b-1

1

No

v-1

1

Au

g-1

2

Ma

y-1

3

Fe

b-1

4

No

v-1

4

Au

g-1

5

Ne

w s

ale

s

Exi

stin

g S

ale

s

Orange New v. Existing Home Sales: 1999-2016

New Home Sales Existing Home Sales

20March 2016 | OC HomeAidSource: Zillow

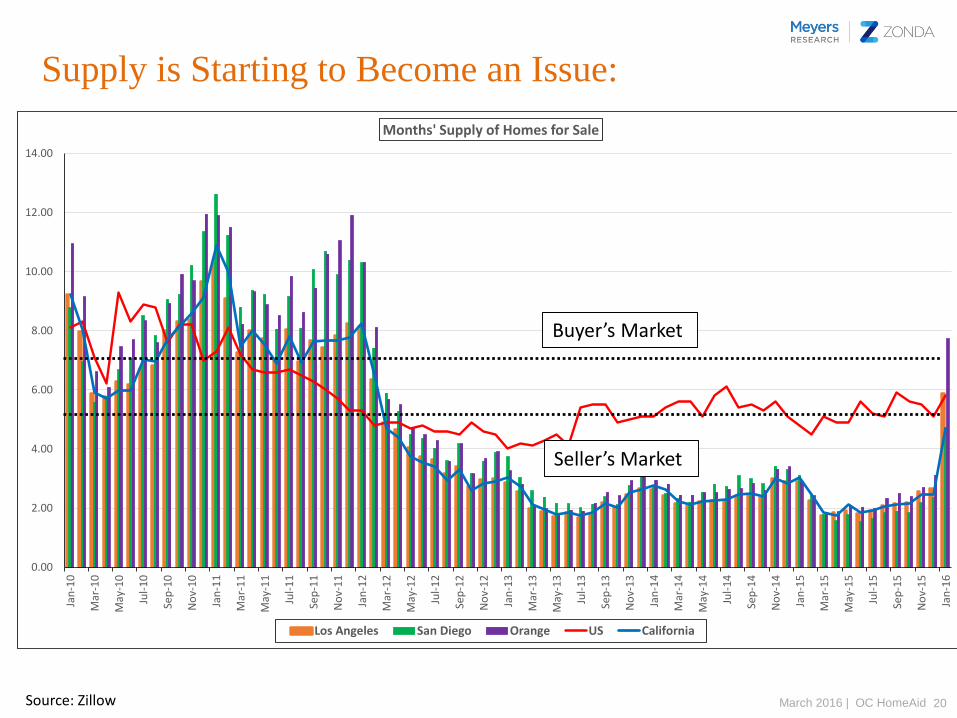

Supply is Starting to Become an Issue:

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-10

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-11

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-12

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-13

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-14

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-15

Jan

-16

Months' Supply of Homes for Sale

Los Angeles San Diego Orange US California

Buyer’s Market

Seller’s Market

21March 2016 | OC HomeAidSource: RealtyTrac

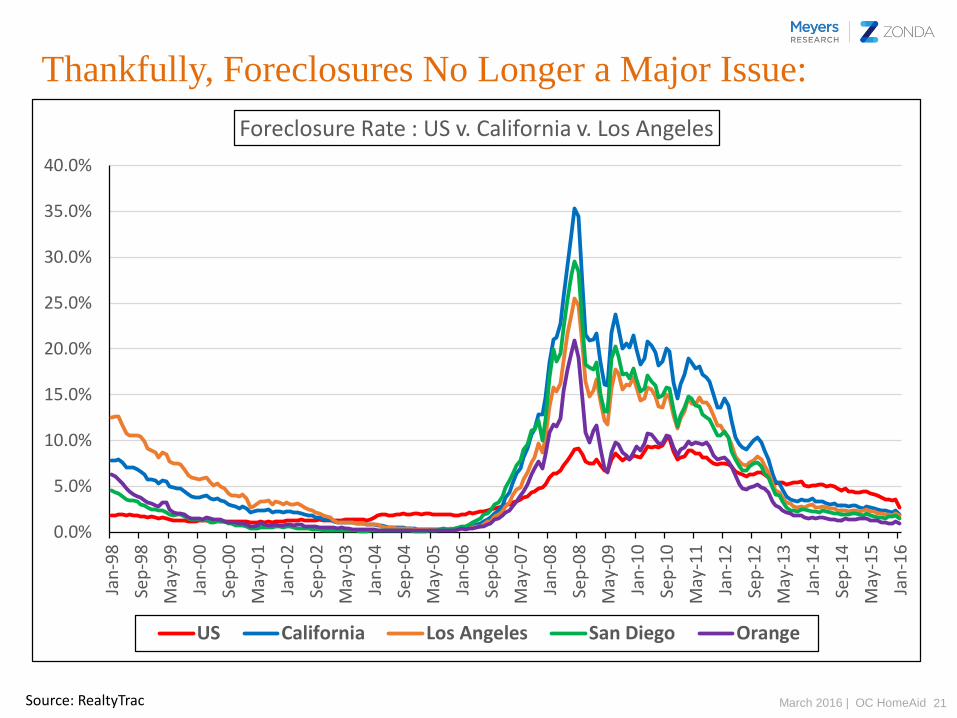

Thankfully, Foreclosures No Longer a Major Issue:

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Jan

-98

Sep

-98

May

-99

Jan

-00

Sep

-00

May

-01

Jan

-02

Sep

-02

May

-03

Jan

-04

Sep

-04

May

-05

Jan

-06

Sep

-06

May

-07

Jan

-08

Sep

-08

May

-09

Jan

-10

Sep

-10

May

-11

Jan

-12

Sep

-12

May

-13

Jan

-14

Sep

-14

May

-15

Jan

-16

Foreclosure Rate : US v. California v. Los Angeles

US California Los Angeles San Diego Orange

22March 2016 | OC HomeAidSource: Zonda

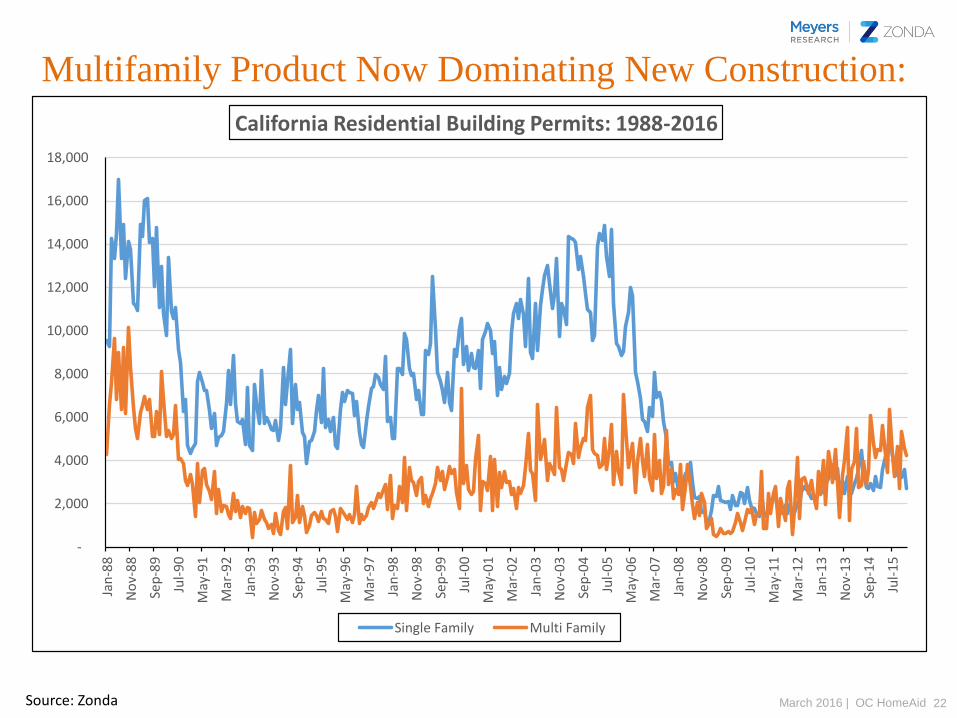

Multifamily Product Now Dominating New Construction:

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jan

-88

No

v-8

8

Sep

-89

Jul-

90

May

-91

Mar

-92

Jan

-93

No

v-9

3

Sep

-94

Jul-

95

May

-96

Mar

-97

Jan

-98

No

v-9

8

Sep

-99

Jul-

00

May

-01

Mar

-02

Jan

-03

No

v-0

3

Sep

-04

Jul-

05

May

-06

Mar

-07

Jan

-08

No

v-0

8

Sep

-09

Jul-

10

May

-11

Mar

-12

Jan

-13

No

v-1

3

Sep

-14

Jul-

15

California Residential Building Permits: 1988-2016

Single Family Multi Family

23March 2016 | OC HomeAidSource: NAHB

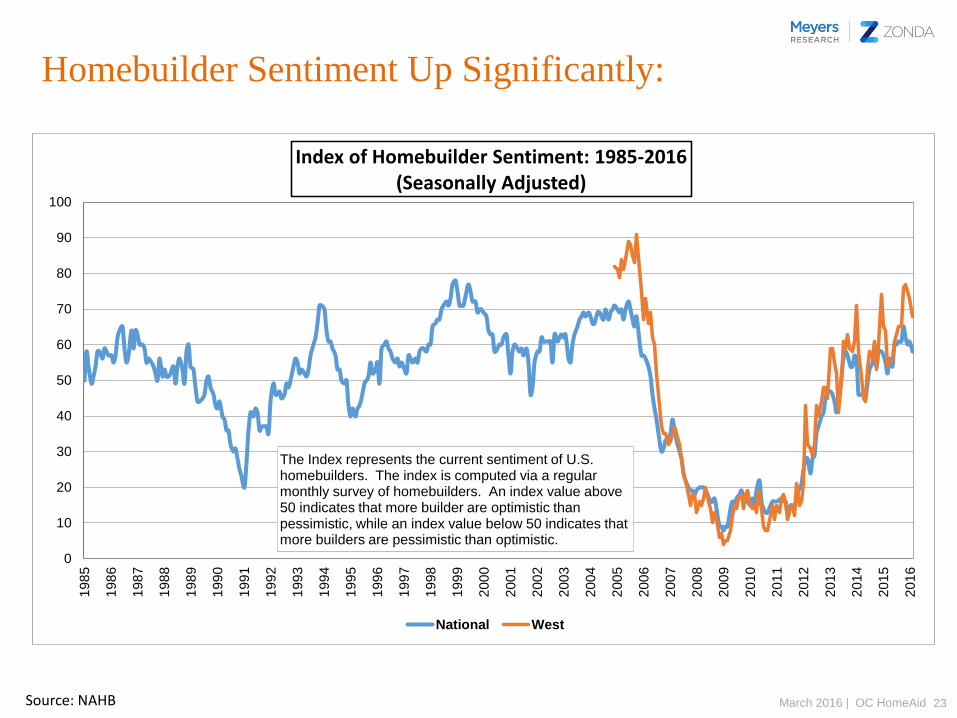

Homebuilder Sentiment Up Significantly:

0

10

20

30

40

50

60

70

80

90

100

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

Index of Homebuilder Sentiment: 1985-2016(Seasonally Adjusted)

National West

The Index represents the current sentiment of U.S.homebuilders. The index is computed via a regular monthly survey of homebuilders. An index value above 50 indicates that more builder are optimistic than pessimistic, while an index value below 50 indicates that more builders are pessimistic than optimistic.

WHERE DO WE GO FROM HERE?

25March 2016 | OC HomeAid

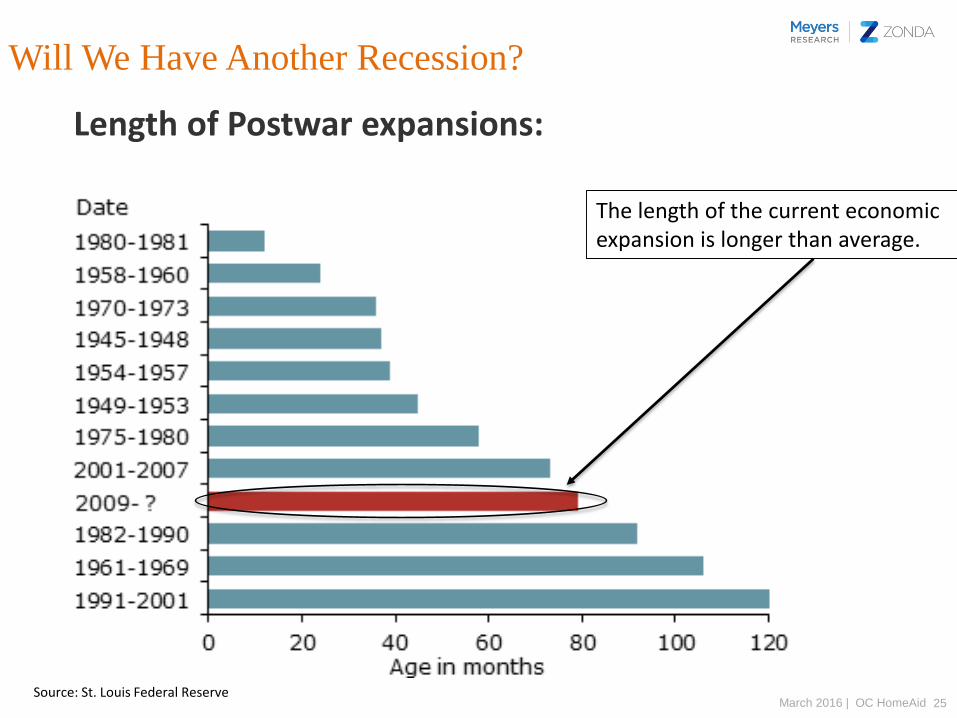

Will We Have Another Recession?

Source: St. Louis Federal Reserve

Length of Postwar expansions:

The length of the current economic expansion is longer than average.

26March 2016 | OC HomeAid

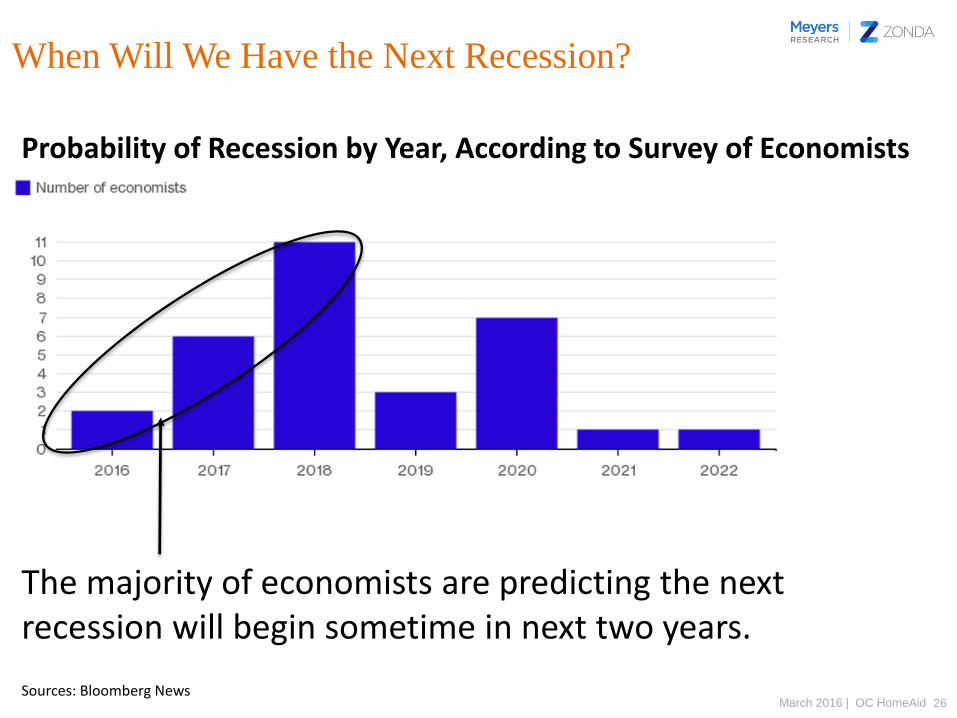

When Will We Have the Next Recession?

The majority of economists are predicting the next recession will begin sometime in next two years.

Probability of Recession by Year, According to Survey of Economists

Sources: Bloomberg News

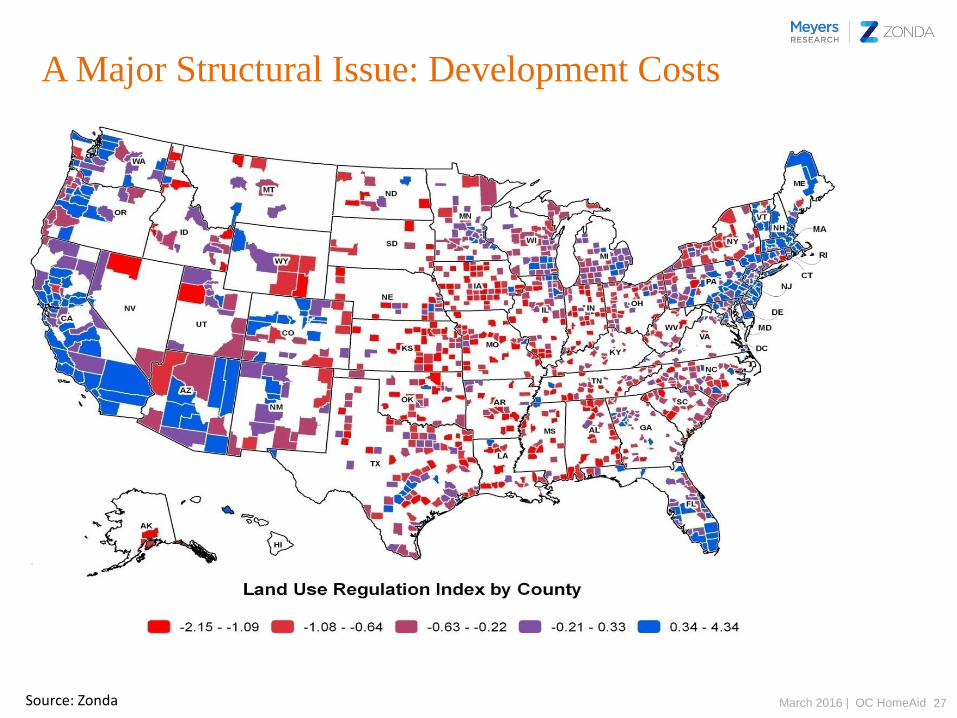

27March 2016 | OC HomeAidSource: Zonda

A Major Structural Issue: Development Costs

28March 2016 | OC HomeAidSource: Zonda

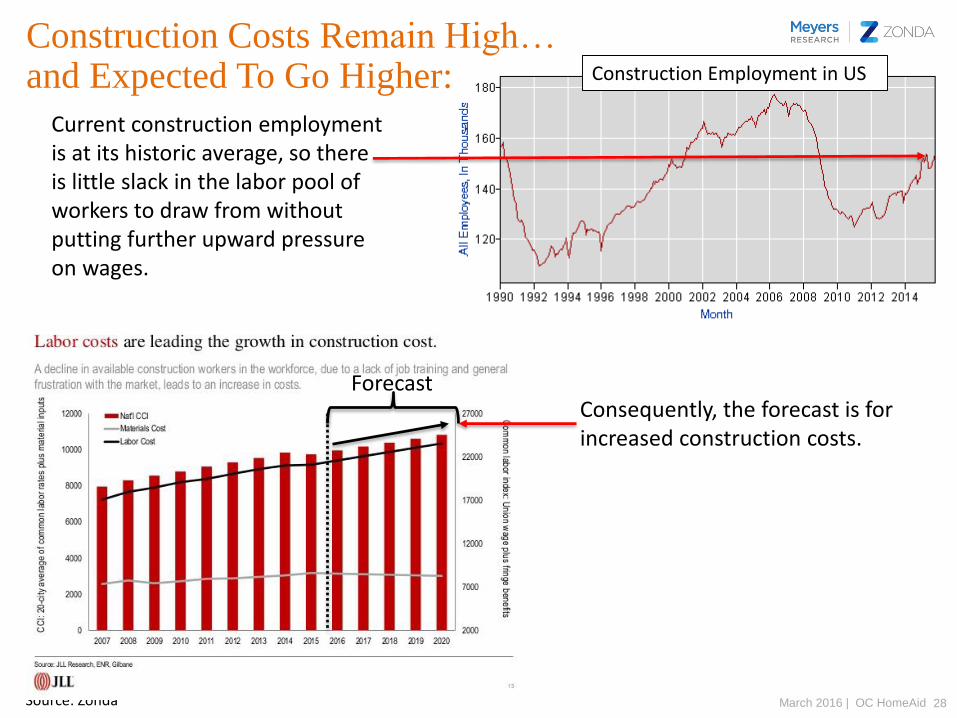

Construction Costs Remain High…and Expected To Go Higher:

Source: US BLS

Construction Employment in US

Current construction employment is at its historic average, so there is little slack in the labor pool of workers to draw from without putting further upward pressure on wages.

ForecastConsequently, the forecast is for increased construction costs.

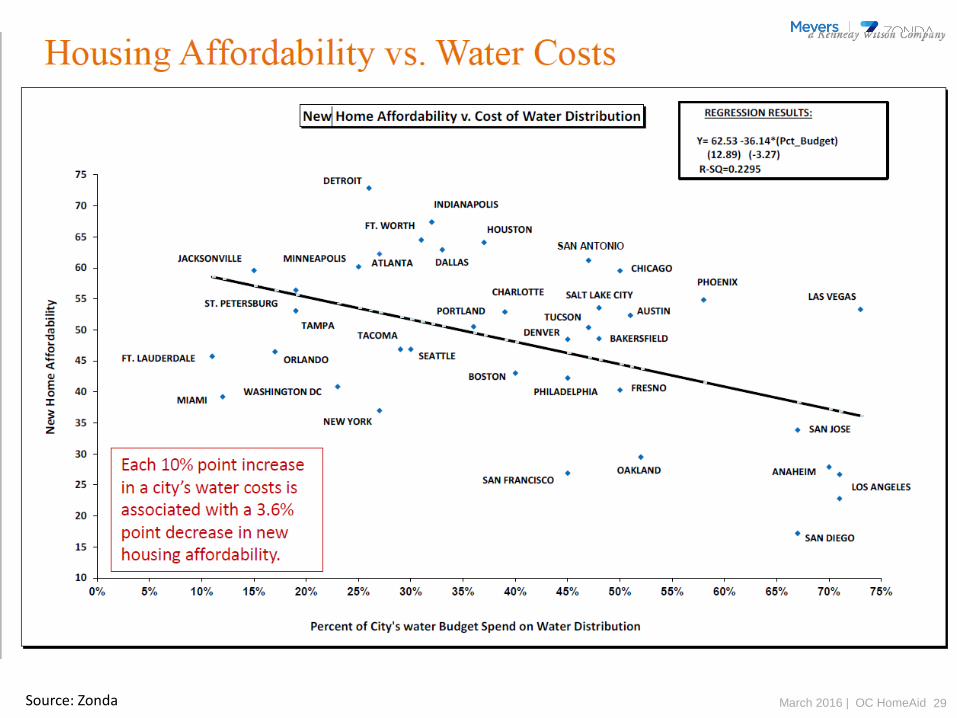

29March 2016 | OC HomeAidSource: Zonda

A Major Structural Issue: Development Costs

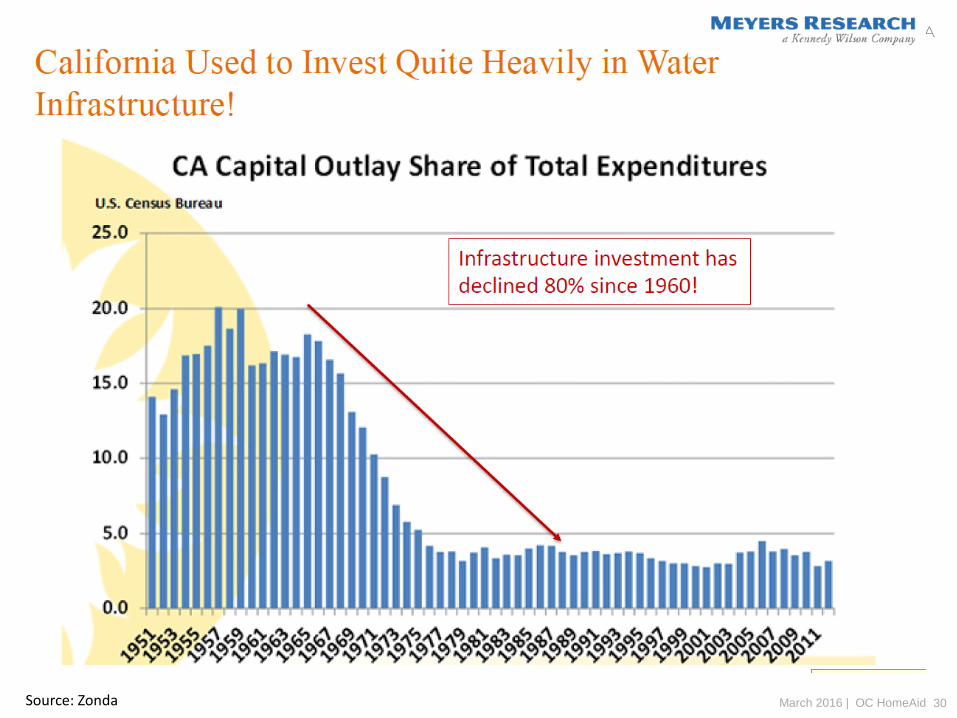

30March 2016 | OC HomeAidSource: Zonda

A Major Structural Issue: Development Costs

31March 2016 | OC HomeAidSource: Zonda

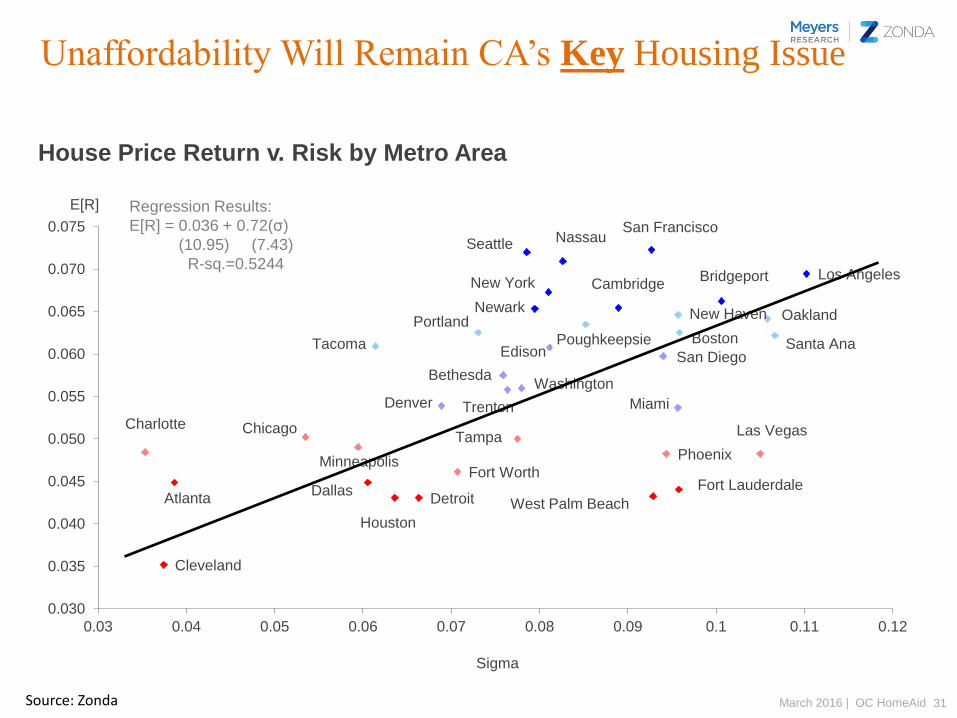

Unaffordability Will Remain CA’s Key Housing Issue

Cleveland

Denver Trenton

WashingtonBethesda

San DiegoEdisonTacoma Santa Ana

PortlandBostonPoughkeepsie

OaklandNew Haven

CambridgeBridgeportNew York

Los Angeles

NassauSeattleSan Francisco

Houston

Detroit West Palm Beach

Fort LauderdaleAtlanta

Dallas

Fort Worth

Phoenix

Las VegasCharlotte

Minneapolis

TampaChicago

Miami

Newark

0.030

0.035

0.040

0.045

0.050

0.055

0.060

0.065

0.070

0.075

0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.1 0.11 0.12

E[R]

Sigma

House Price Return v. Risk by Metro Area

Regression Results:

E[R] = 0.036 + 0.72(σ)

(10.95) (7.43)

R-sq.=0.5244

32March 2016 | OC HomeAidSource: Zonda

Unaffordability: Why You Should Care

• Short-Term: Leads to higher municipal service costs, and

eventually higher property taxes.

-Municipal workers (police, fire, sanitation, school

teachers) can’t afford to live in the municipality that

employs them.

• Long-Term: Leads to a contracting spiral of decline

-As the municipality becomes less affordable, home sales

drop, followed by population and employment declines, tax

base contracts, quality of public services erodes…leading

to further population and employment losses…and further

tax base contraction.

-Very difficult to reverse this spiral (ask Detroit).

33March 2016 | OC HomeAidSource: Zonda

Summary and Conclusions

• GDP Growth and House Price Appreciation expected to

continue, but at a decreasing rate.

-2016 expected to be a decent year…BUT:

-We are closer to the next recession than we are from the

previous one.

• Will still be several years before housing has completely

recovered from the last recession.

-Prices are there, but jobs and new home sales are not.

-Rising interest rates and labor costs plus next recession

won’t help.

=>Plan accordingly!

• You can’t do much about national cyclical factors, but you

can address local structural issues.

-Drought and high water costs are avoidable.

-Bring rationality to land use policy…get involved!

34March 2016 | OC HomeAidSource: Zonda

Thank You!

For further information, please contact:

Kevin Gillen, Ph.D.Chief Economist, Meyers Research LLC

215.880.6630