Housing Market and Economic Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS ® Presentation at OAR Legislative and Economic Summit Oklahoma City, OK February 6, 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Housing Market and

Economic OutlookLawrence Yun, Ph.D.Chief Economist

NATIONAL ASSOCIATION OF REALTORS®

Presentation at OAR Legislative and Economic Summit

Oklahoma City, OK

February 6, 2013

Forecast #1: Inflation will be Notably Higher by 2015

• No Threatening Inflation Signs for 2013

• But Inflation rises to 4% to 6% in 2015

• Well above Fed’s preferred rate of 2%

• But not in double‐digits as in 1970s

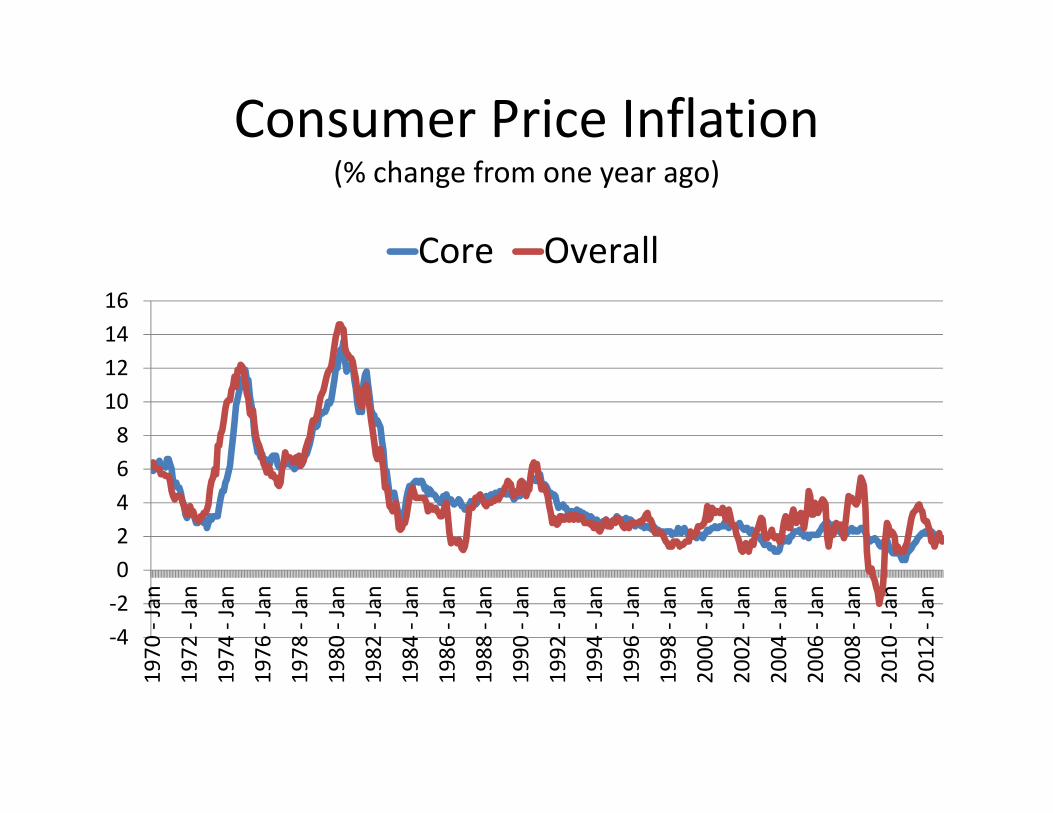

Consumer Price Inflation(% change from one year ago)

‐4‐20246810121416

1970

‐ Jan

1972

‐ Jan

1974

‐ Jan

1976

‐ Jan

1978

‐ Jan

1980

‐ Jan

1982

‐ Jan

1984

‐ Jan

1986

‐ Jan

1988

‐ Jan

1990

‐ Jan

1992

‐ Jan

1994

‐ Jan

1996

‐ Jan

1998

‐ Jan

2000

‐ Jan

2002

‐ Jan

2004

‐ Jan

2006

‐ Jan

2008

‐ Jan

2010

‐ Jan

2012

‐ Jan

Core Overall

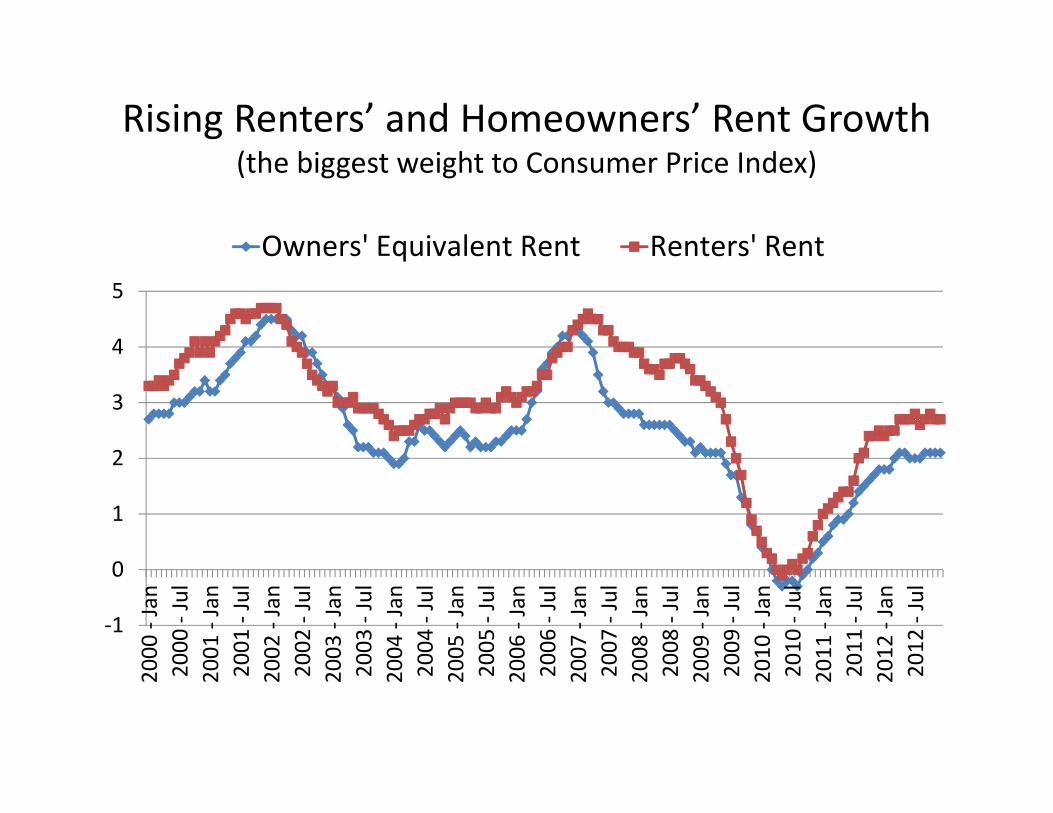

Rising Renters’ and Homeowners’ Rent Growth (the biggest weight to Consumer Price Index)

‐1

0

1

2

3

4

5

2000

‐ Jan

2000

‐ Jul

2001

‐ Jan

2001

‐ Jul

2002

‐ Jan

2002

‐ Jul

2003

‐ Jan

2003

‐ Jul

2004

‐ Jan

2004

‐ Jul

2005

‐ Jan

2005

‐ Jul

2006

‐ Jan

2006

‐ Jul

2007

‐ Jan

2007

‐ Jul

2008

‐ Jan

2008

‐ Jul

2009

‐ Jan

2009

‐ Jul

2010

‐ Jan

2010

‐ Jul

2011

‐ Jan

2011

‐ Jul

2012

‐ Jan

2012

‐ Jul

Owners' Equivalent Rent Renters' Rent

0%

10%

20%

30%

40%

50%

60%

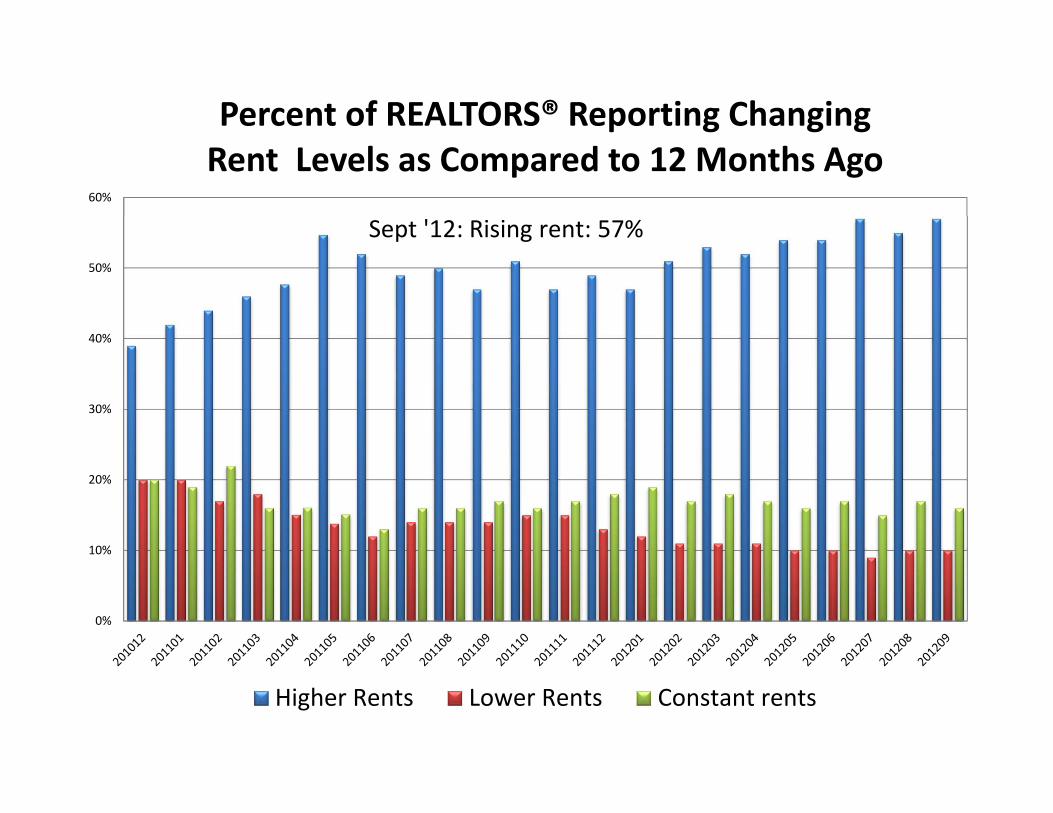

Percent of REALTORS® Reporting Changing Rent Levels as Compared to 12 Months Ago

Higher Rents Lower Rents Constant rents

Sept '12: Rising rent: 57%

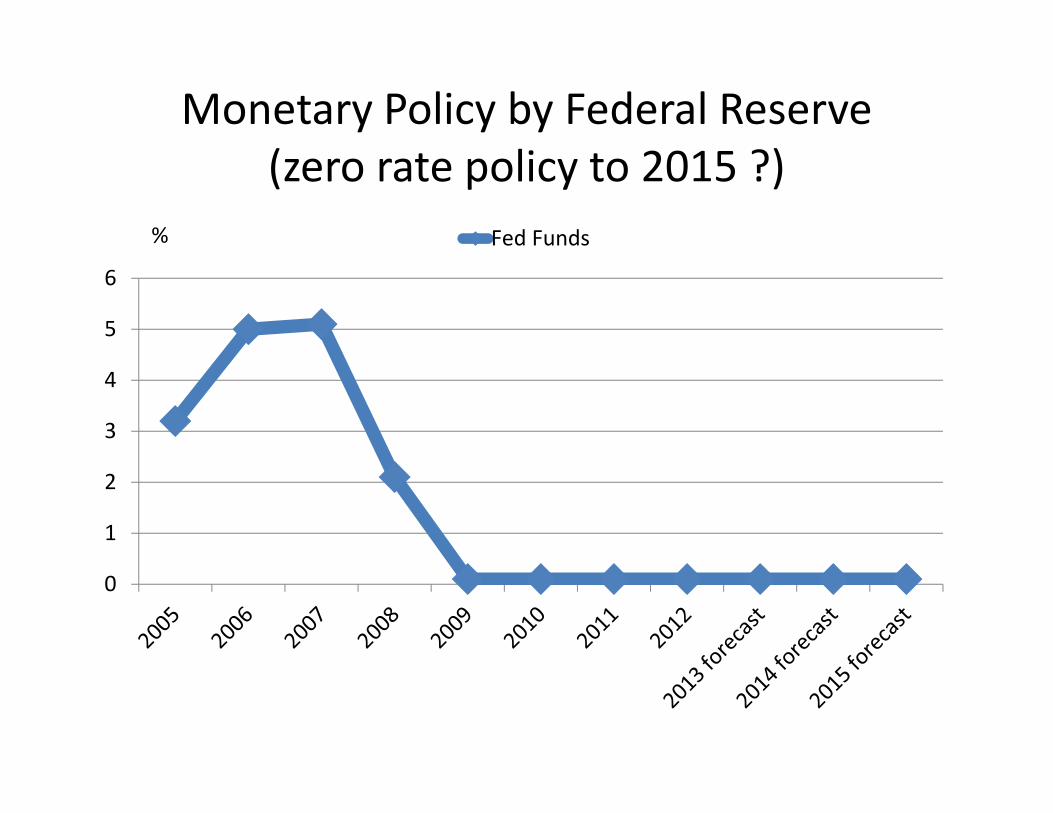

Monetary Policy by Federal Reserve (zero rate policy to 2015 ?)

0

1

2

3

4

5

6

Fed Funds%

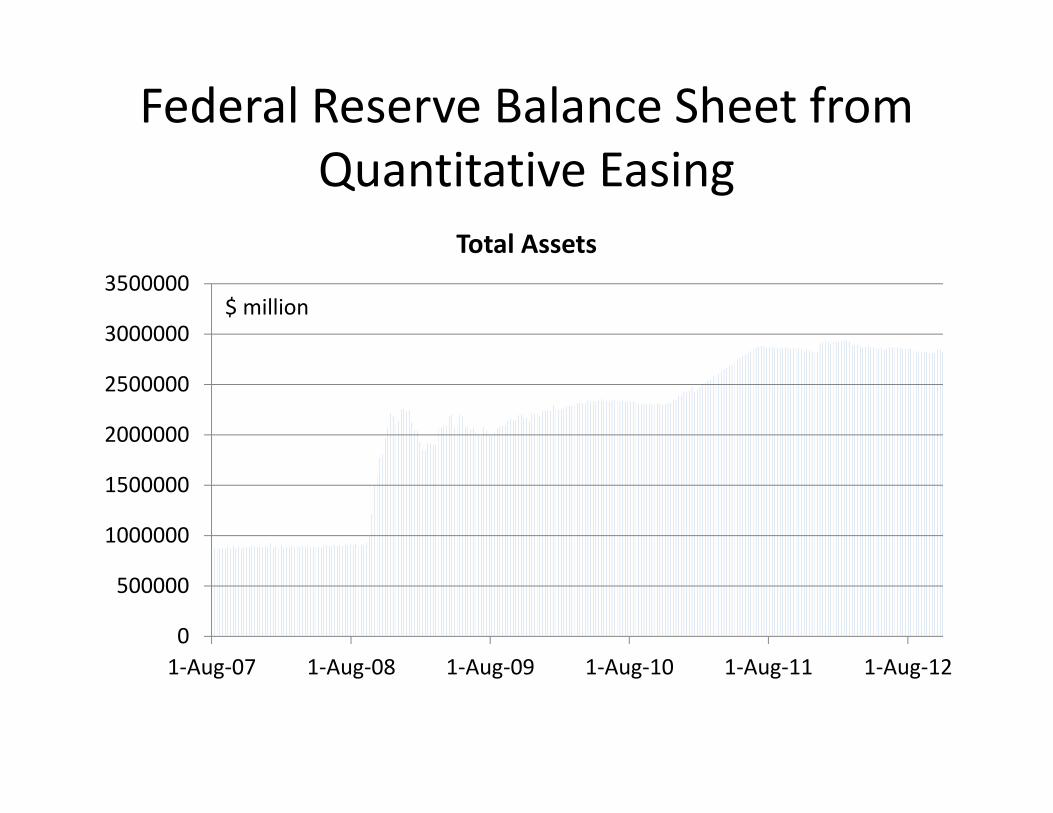

Federal Reserve Balance Sheet from Quantitative Easing

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

1‐Aug‐07 1‐Aug‐08 1‐Aug‐09 1‐Aug‐10 1‐Aug‐11 1‐Aug‐12

Total Assets

$ million

Federal Government Tax Revenue and Spending

05000001000000150000020000002500000300000035000004000000

1970

‐ Jan

1972

‐ Jan

1974

‐ Jan

1976

‐ Jan

1978

‐ Jan

1980

‐ Jan

1982

‐ Jan

1984

‐ Jan

1986

‐ Jan

1988

‐ Jan

1990

‐ Jan

1992

‐ Jan

1994

‐ Jan

1996

‐ Jan

1998

‐ Jan

2000

‐ Jan

2002

‐ Jan

2004

‐ Jan

2006

‐ Jan

2008

‐ Jan

2010

‐ Jan

2012

‐ Jan

Revenue Spending

12‐month tally in $ million

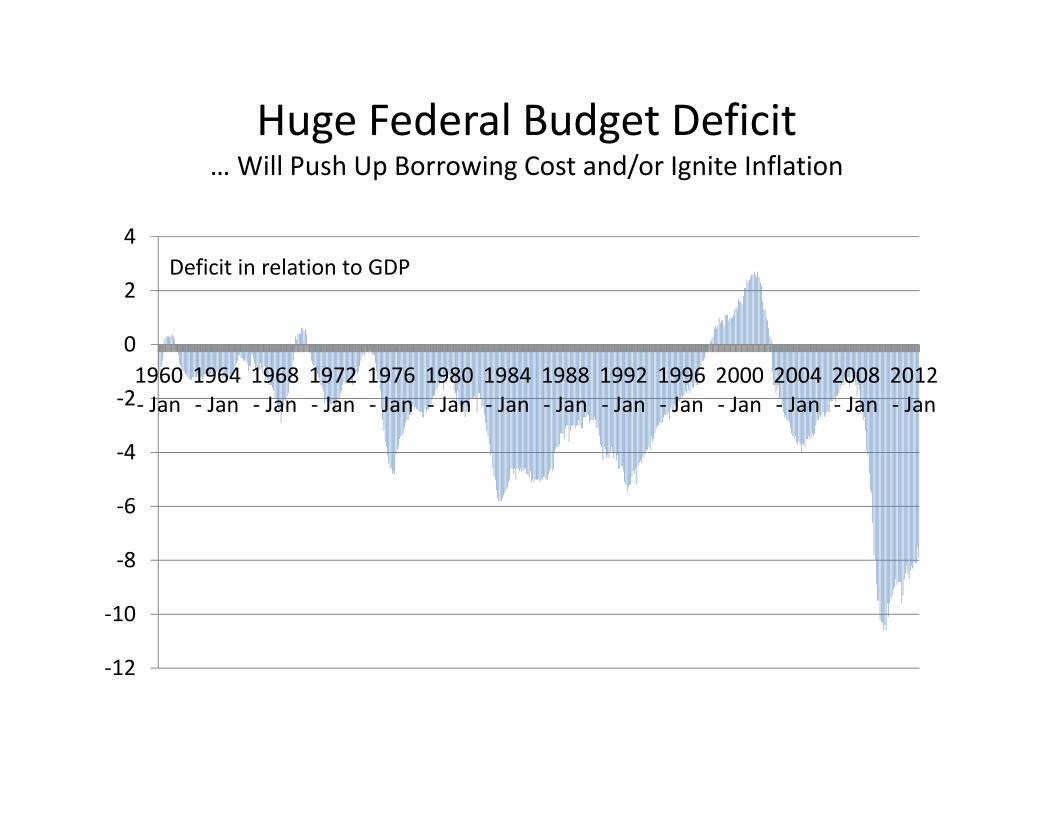

Huge Federal Budget Deficit … Will Push Up Borrowing Cost and/or Ignite Inflation

‐12

‐10

‐8

‐6

‐4

‐2

0

2

4

1960‐ Jan

1964‐ Jan

1968‐ Jan

1972‐ Jan

1976‐ Jan

1980‐ Jan

1984‐ Jan

1988‐ Jan

1992‐ Jan

1996‐ Jan

2000‐ Jan

2004‐ Jan

2008‐ Jan

2012‐ Jan

Deficit in relation to GDP

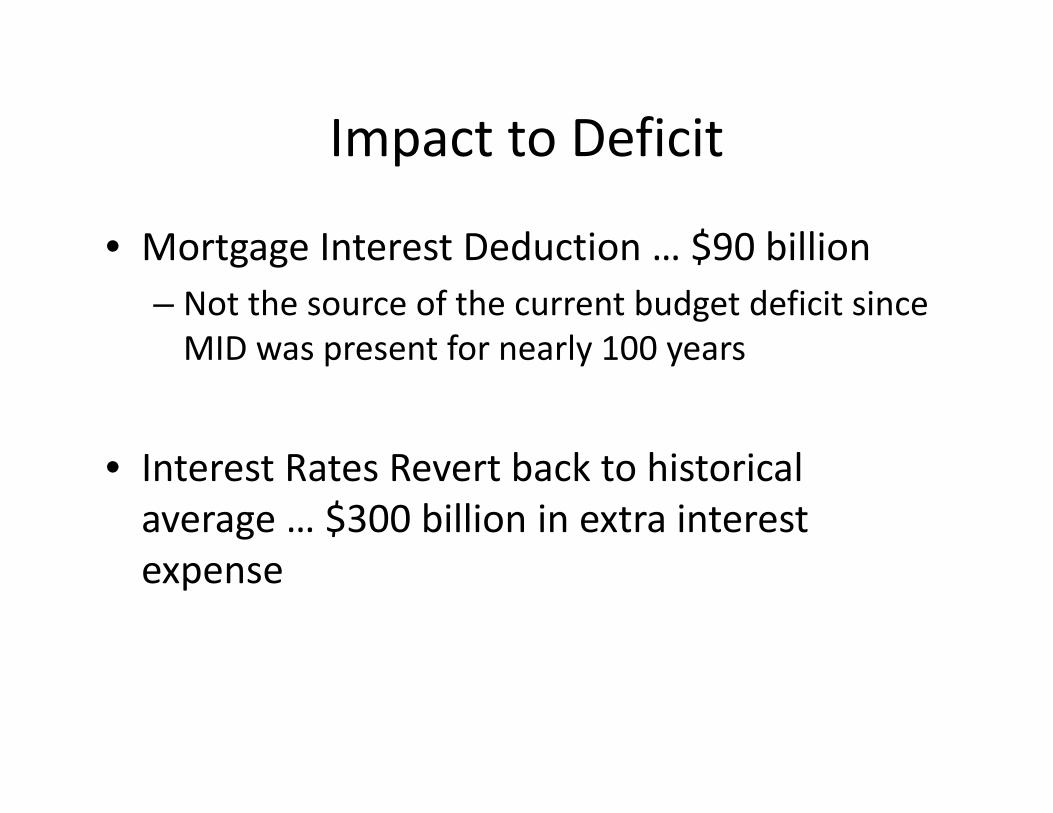

Impact to Deficit

• Mortgage Interest Deduction … $90 billion– Not the source of the current budget deficit since MID was present for nearly 100 years

• Interest Rates Revert back to historical average … $300 billion in extra interest expense

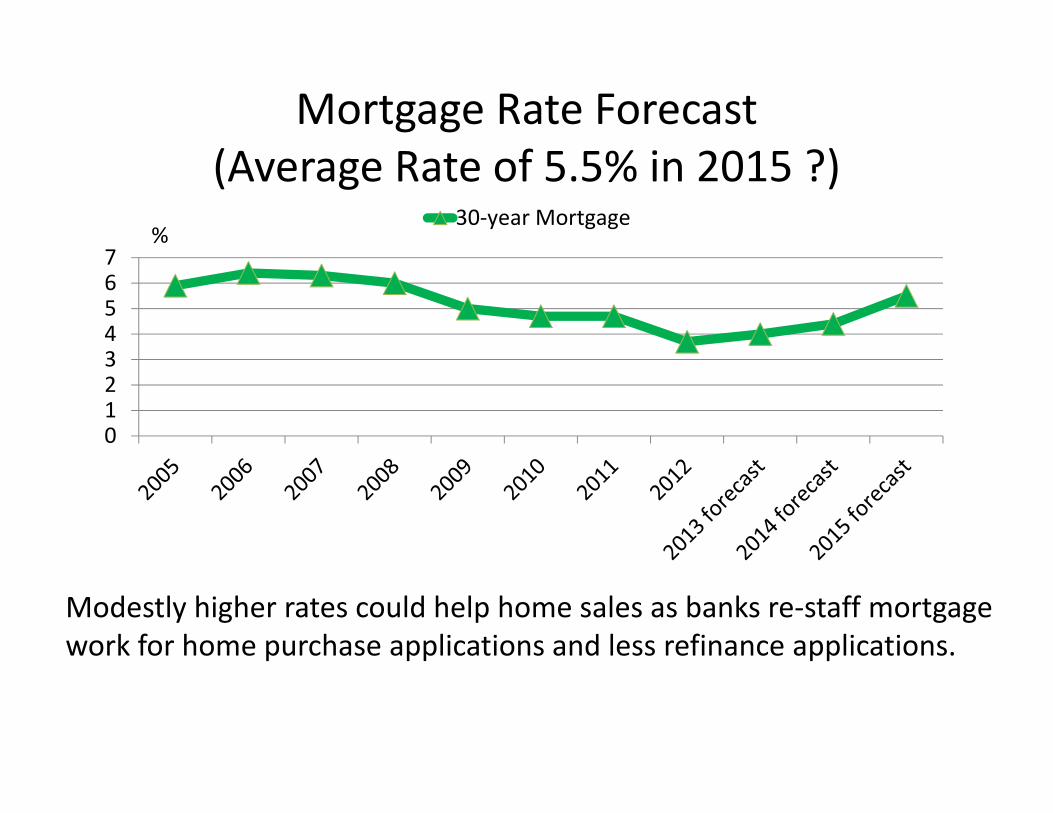

Mortgage Rate Forecast(Average Rate of 5.5% in 2015 ?)

01234567

30‐year Mortgage%

Modestly higher rates could help home sales as banks re‐staff mortgage work for home purchase applications and less refinance applications.

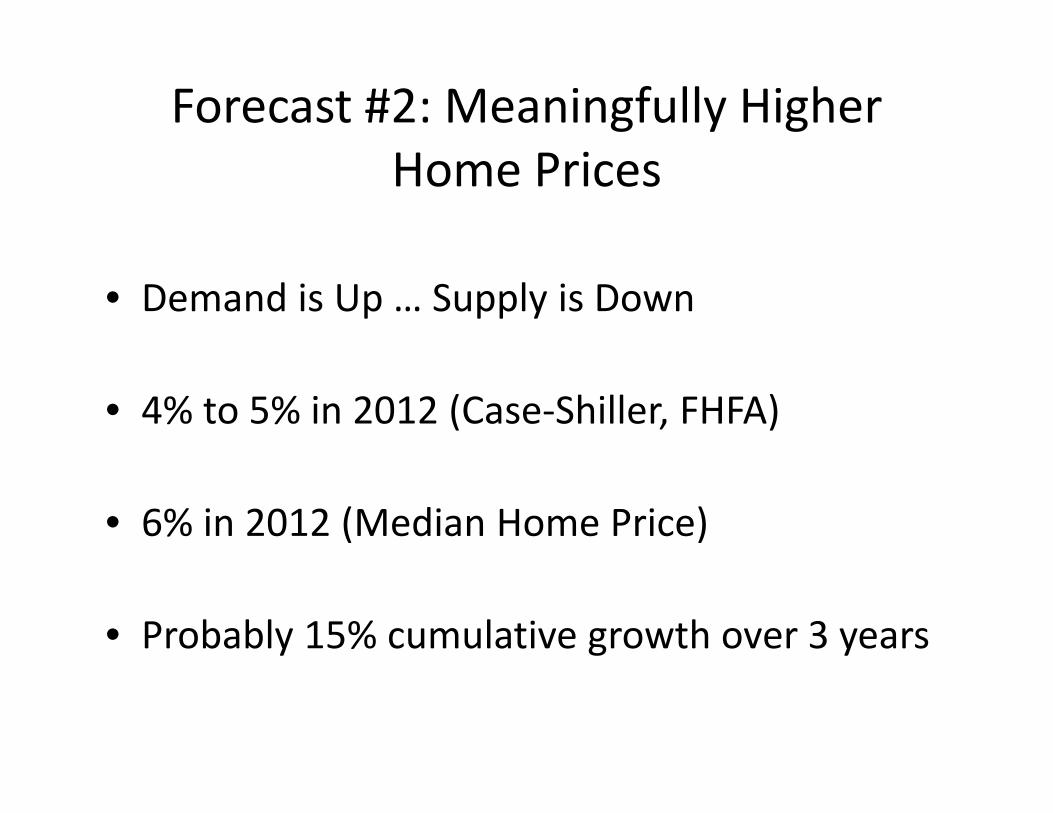

Forecast #2: Meaningfully Higher Home Prices

• Demand is Up … Supply is Down

• 4% to 5% in 2012 (Case‐Shiller, FHFA)

• 6% in 2012 (Median Home Price)

• Probably 15% cumulative growth over 3 years

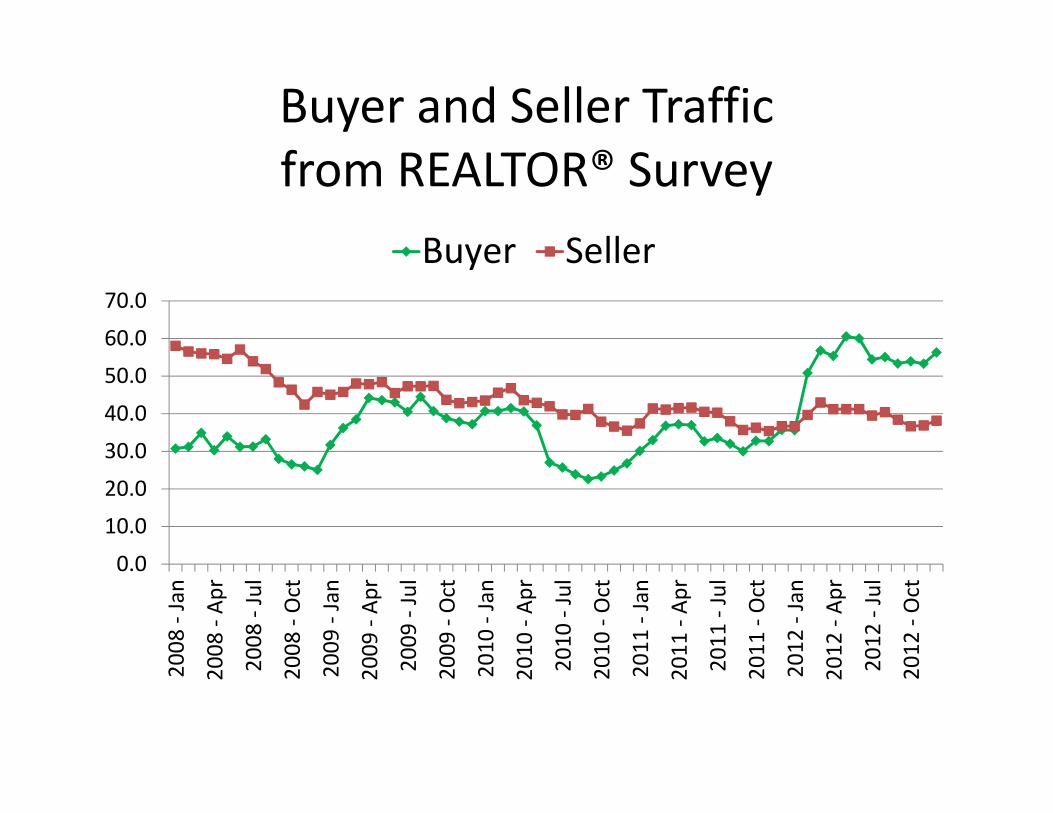

Buyer and Seller Traffic from REALTOR® Survey

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2008

‐ Jan

2008

‐ Ap

r

2008

‐ Jul

2008

‐ Oct

2009

‐ Jan

2009

‐ Ap

r

2009

‐ Jul

2009

‐ Oct

2010

‐ Jan

2010

‐ Ap

r

2010

‐ Jul

2010

‐ Oct

2011

‐ Jan

2011

‐ Ap

r

2011

‐ Jul

2011

‐ Oct

2012

‐ Jan

2012

‐ Ap

r

2012

‐ Jul

2012

‐ Oct

Buyer Seller

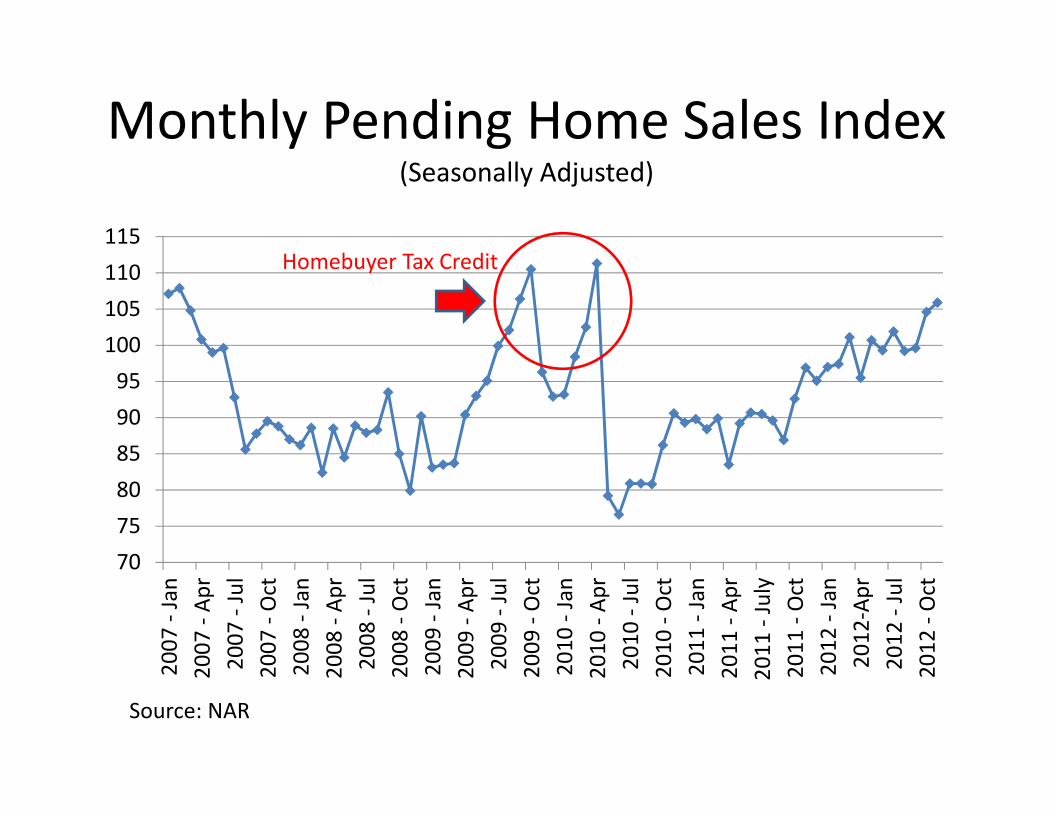

Monthly Pending Home Sales Index(Seasonally Adjusted)

707580859095100105110115

2007

‐ Jan

2007

‐ Ap

r2007

‐ Jul

2007

‐ Oct

2008

‐ Jan

2008

‐ Ap

r2008

‐ Jul

2008

‐ Oct

2009

‐ Jan

2009

‐ Ap

r2009

‐ Jul

2009

‐ Oct

2010

‐ Jan

2010

‐ Ap

r2010

‐ Jul

2010

‐ Oct

2011

‐ Jan

2011

‐ Ap

r2011

‐ July

2011

‐ Oct

2012

‐ Jan

2012

‐Apr

2012

‐ Jul

2012

‐ Oct

Homebuyer Tax Credit

Source: NAR

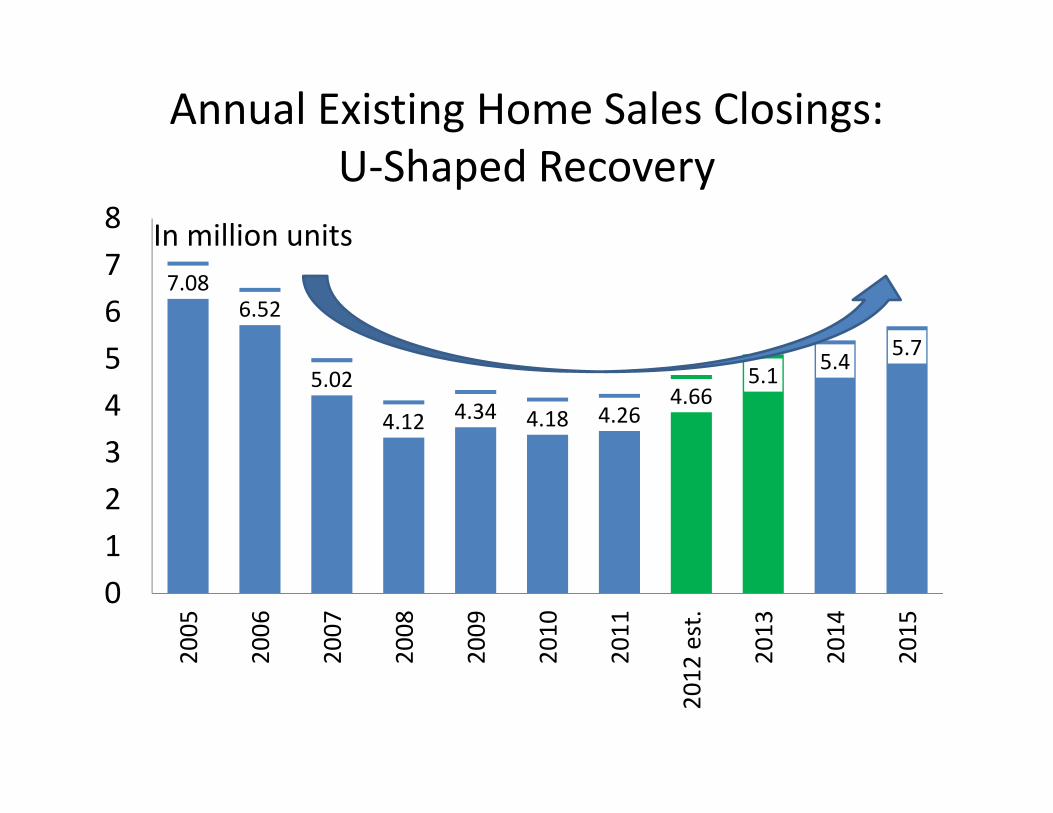

Annual Existing Home Sales Closings:U‐Shaped Recovery

7.086.52

5.02

4.12 4.34 4.18 4.264.66

5.1 5.4 5.7

012345678

2005

2006

2007

2008

2009

2010

2011

2012

est.

2013

2014

2015

In million units

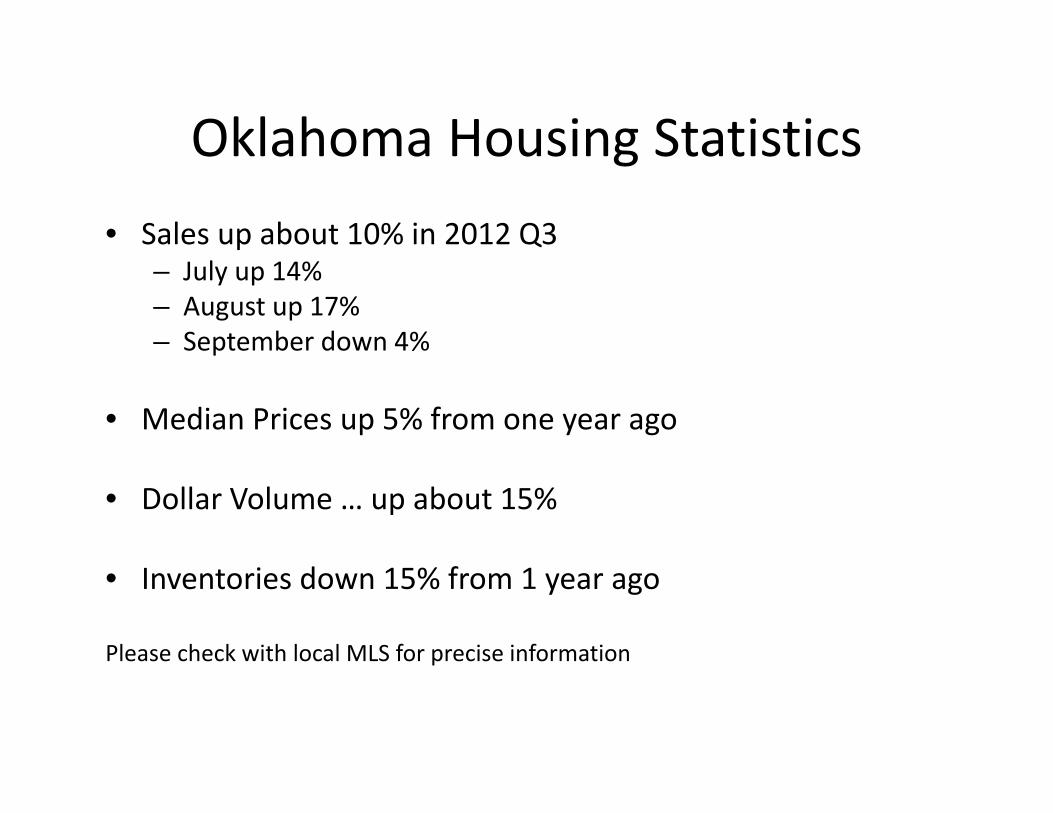

Oklahoma Housing Statistics• Sales up about 10% in 2012 Q3

– July up 14%– August up 17%– September down 4%

• Median Prices up 5% from one year ago

• Dollar Volume … up about 15%

• Inventories down 15% from 1 year ago

Please check with local MLS for precise information

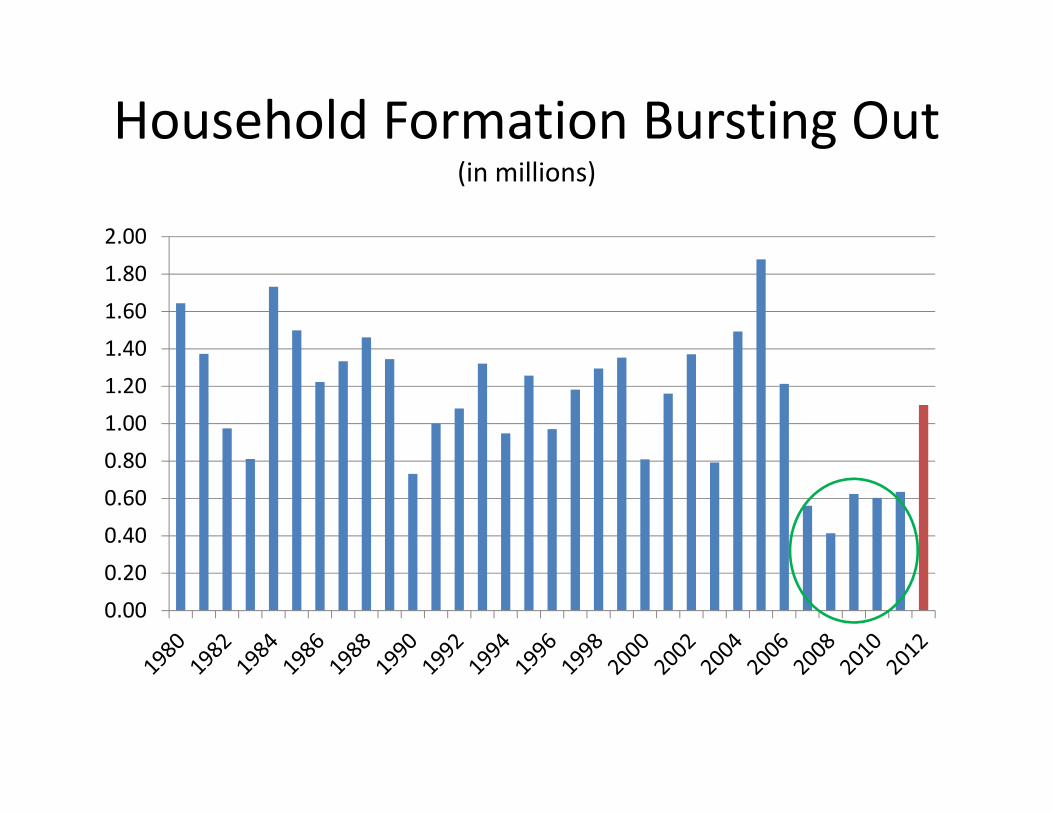

Household Formation Bursting Out(in millions)

0.00

0.200.40

0.600.80

1.001.20

1.401.60

1.802.00

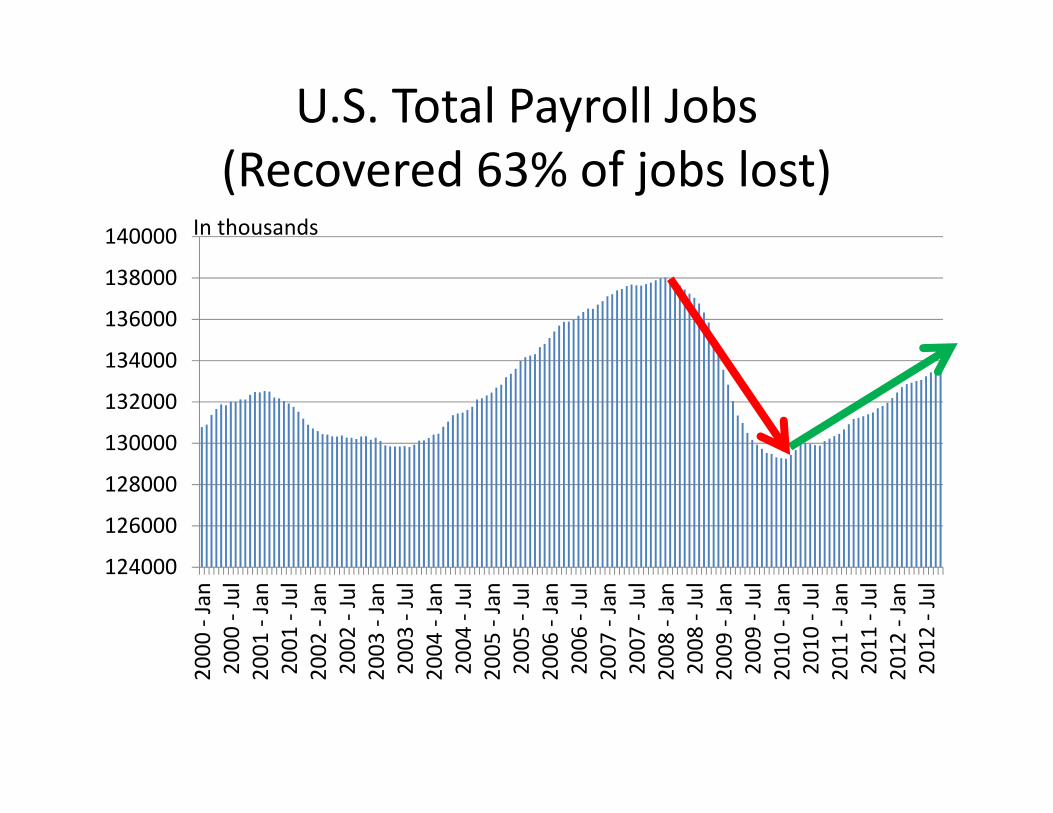

U.S. Total Payroll Jobs(Recovered 63% of jobs lost)

124000

126000

128000

130000

132000

134000

136000

138000

1400002000

‐ Jan

2000

‐ Jul

2001

‐ Jan

2001

‐ Jul

2002

‐ Jan

2002

‐ Jul

2003

‐ Jan

2003

‐ Jul

2004

‐ Jan

2004

‐ Jul

2005

‐ Jan

2005

‐ Jul

2006

‐ Jan

2006

‐ Jul

2007

‐ Jan

2007

‐ Jul

2008

‐ Jan

2008

‐ Jul

2009

‐ Jan

2009

‐ Jul

2010

‐ Jan

2010

‐ Jul

2011

‐ Jan

2011

‐ Jul

2012

‐ Jan

2012

‐ Jul

In thousands

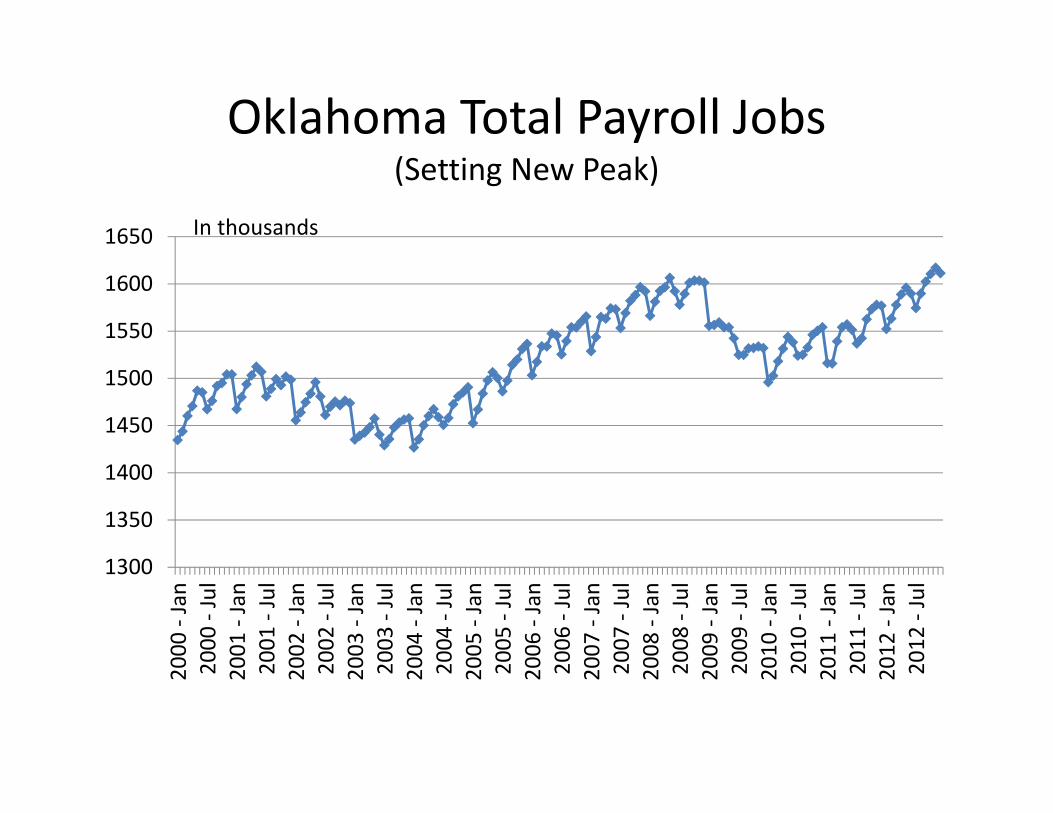

Oklahoma Total Payroll Jobs(Setting New Peak)

1300

1350

1400

1450

1500

1550

1600

1650

2000

‐ Jan

2000

‐ Jul

2001

‐ Jan

2001

‐ Jul

2002

‐ Jan

2002

‐ Jul

2003

‐ Jan

2003

‐ Jul

2004

‐ Jan

2004

‐ Jul

2005

‐ Jan

2005

‐ Jul

2006

‐ Jan

2006

‐ Jul

2007

‐ Jan

2007

‐ Jul

2008

‐ Jan

2008

‐ Jul

2009

‐ Jan

2009

‐ Jul

2010

‐ Jan

2010

‐ Jul

2011

‐ Jan

2011

‐ Jul

2012

‐ Jan

2012

‐ Jul

In thousands

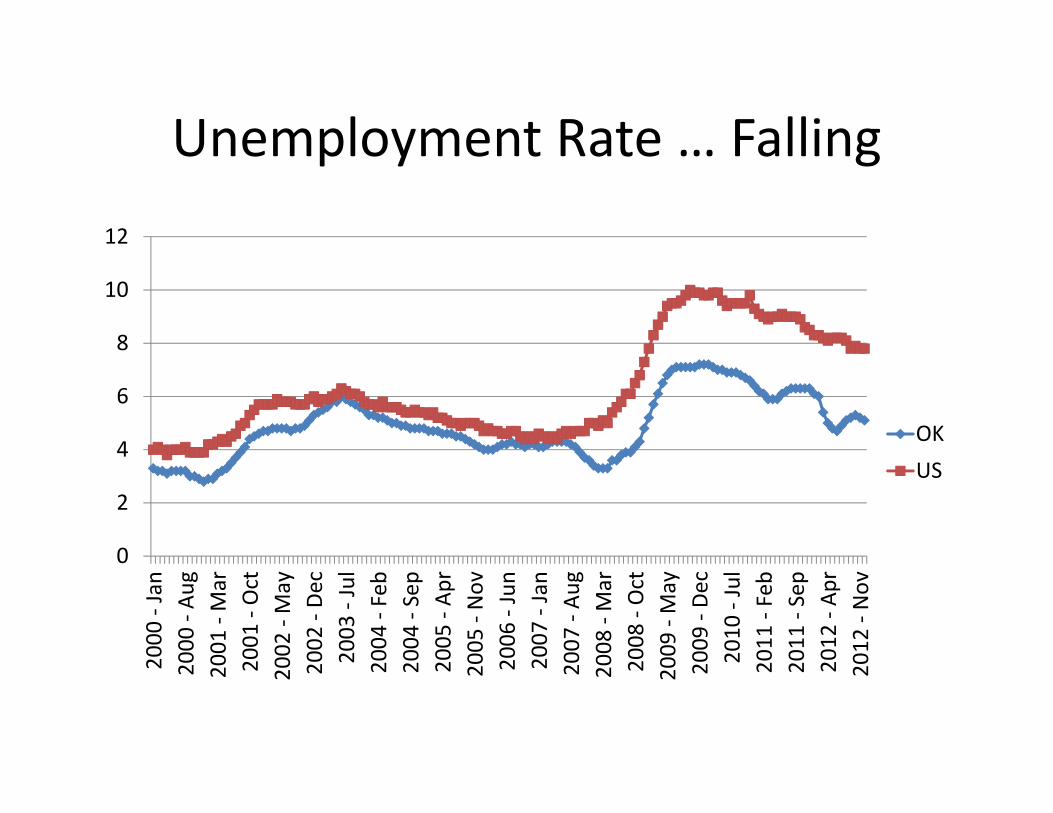

Unemployment Rate … Falling

0

2

4

6

8

10

12

2000

‐ Jan

2000

‐ Au

g2001

‐ Mar

2001

‐ Oct

2002

‐ May

2002

‐ De

c2003

‐ Jul

2004

‐ Feb

2004

‐ Sep

2005

‐ Ap

r2005

‐ Nov

2006

‐ Jun

2007

‐ Jan

2007

‐ Au

g2008

‐ Mar

2008

‐ Oct

2009

‐ May

2009

‐ De

c2010

‐ Jul

2011

‐ Feb

2011

‐ Sep

2012

‐ Ap

r2012

‐ Nov

OKUS

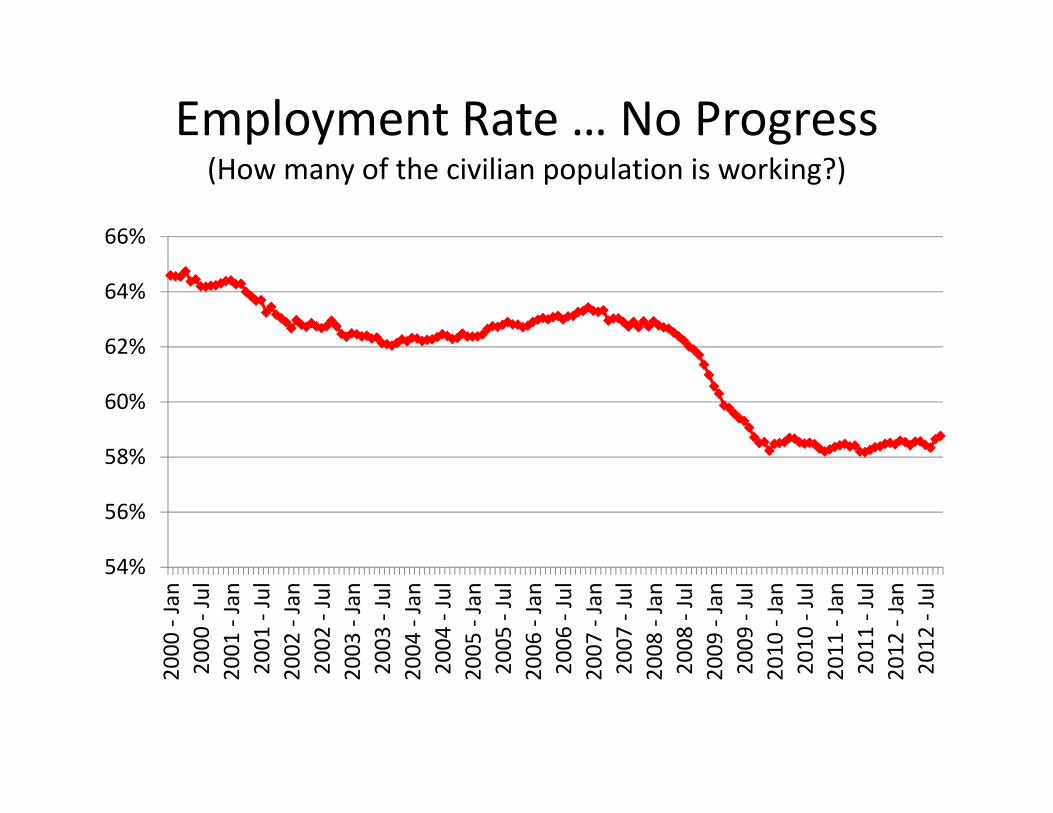

Employment Rate … No Progress(How many of the civilian population is working?)

54%

56%

58%

60%

62%

64%

66%

2000

‐ Jan

2000

‐ Jul

2001

‐ Jan

2001

‐ Jul

2002

‐ Jan

2002

‐ Jul

2003

‐ Jan

2003

‐ Jul

2004

‐ Jan

2004

‐ Jul

2005

‐ Jan

2005

‐ Jul

2006

‐ Jan

2006

‐ Jul

2007

‐ Jan

2007

‐ Jul

2008

‐ Jan

2008

‐ Jul

2009

‐ Jan

2009

‐ Jul

2010

‐ Jan

2010

‐ Jul

2011

‐ Jan

2011

‐ Jul

2012

‐ Jan

2012

‐ Jul

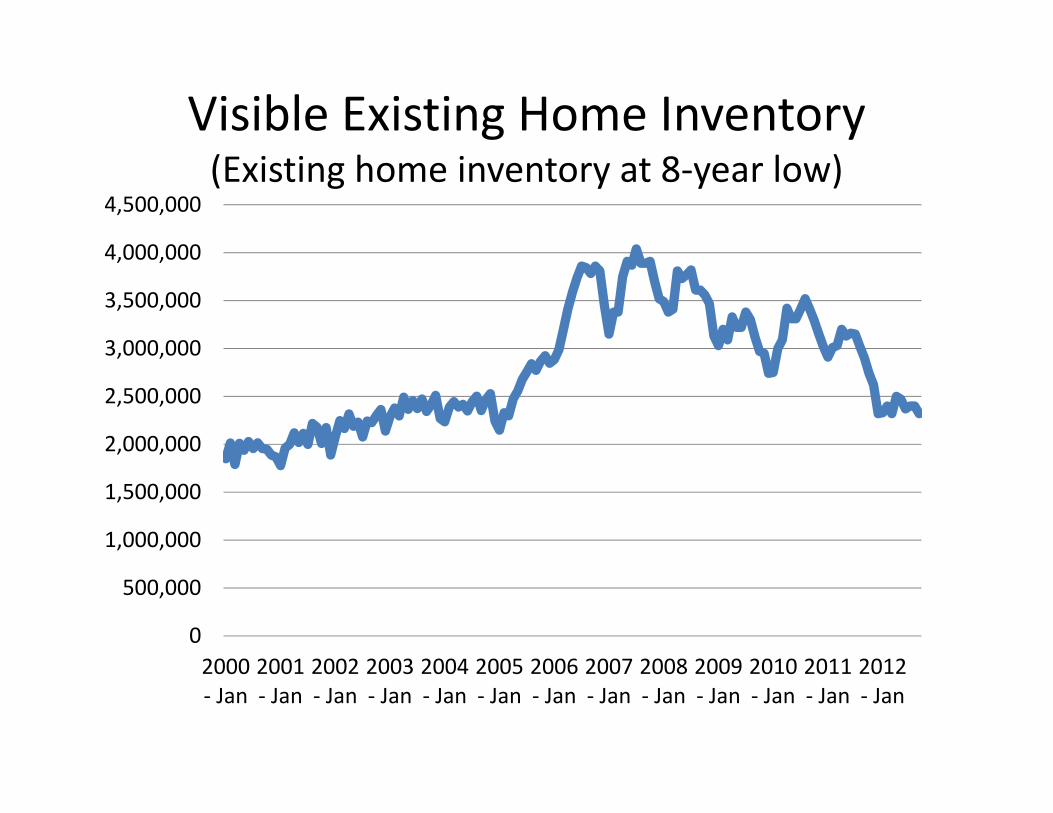

Visible Existing Home Inventory(Existing home inventory at 8‐year low)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2000‐ Jan

2001‐ Jan

2002‐ Jan

2003‐ Jan

2004‐ Jan

2005‐ Jan

2006‐ Jan

2007‐ Jan

2008‐ Jan

2009‐ Jan

2010‐ Jan

2011‐ Jan

2012‐ Jan

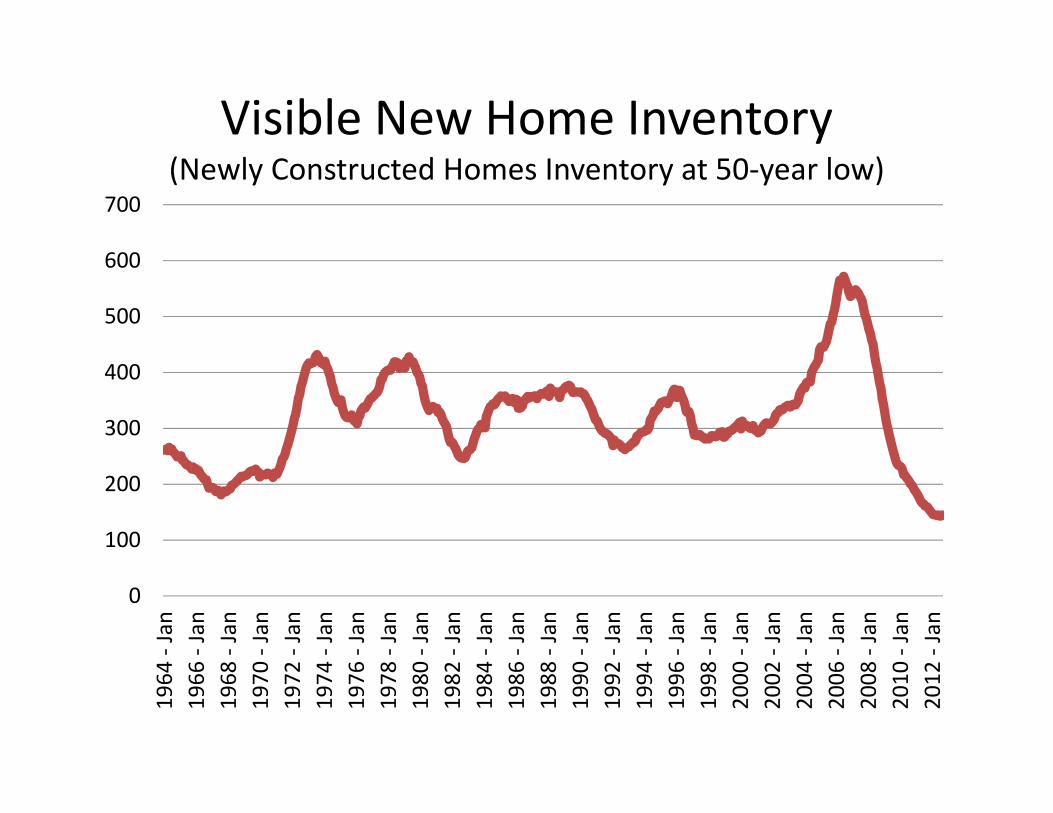

Visible New Home Inventory(Newly Constructed Homes Inventory at 50‐year low)

0

100

200

300

400

500

600

700

1964

‐ Jan

1966

‐ Jan

1968

‐ Jan

1970

‐ Jan

1972

‐ Jan

1974

‐ Jan

1976

‐ Jan

1978

‐ Jan

1980

‐ Jan

1982

‐ Jan

1984

‐ Jan

1986

‐ Jan

1988

‐ Jan

1990

‐ Jan

1992

‐ Jan

1994

‐ Jan

1996

‐ Jan

1998

‐ Jan

2000

‐ Jan

2002

‐ Jan

2004

‐ Jan

2006

‐ Jan

2008

‐ Jan

2010

‐ Jan

2012

‐ Jan

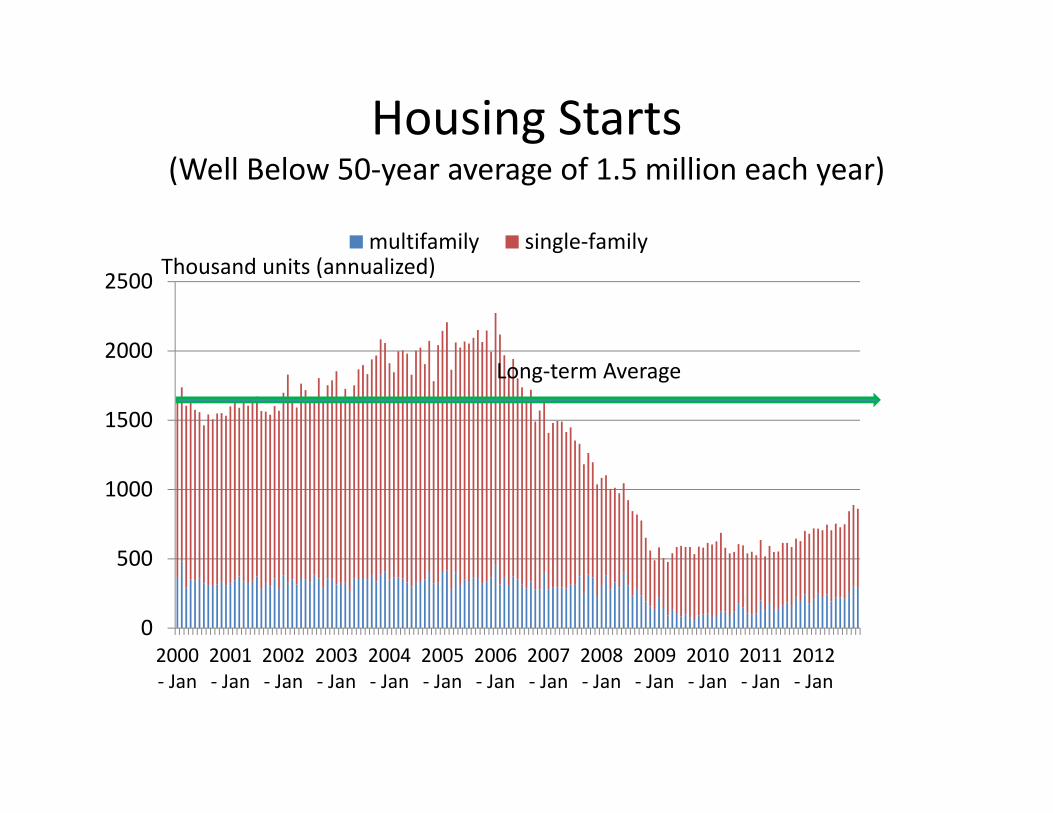

Housing Starts(Well Below 50‐year average of 1.5 million each year)

0

500

1000

1500

2000

2500

2000‐ Jan

2001‐ Jan

2002‐ Jan

2003‐ Jan

2004‐ Jan

2005‐ Jan

2006‐ Jan

2007‐ Jan

2008‐ Jan

2009‐ Jan

2010‐ Jan

2011‐ Jan

2012‐ Jan

multifamily single‐familyThousand units (annualized)

Long‐term Average

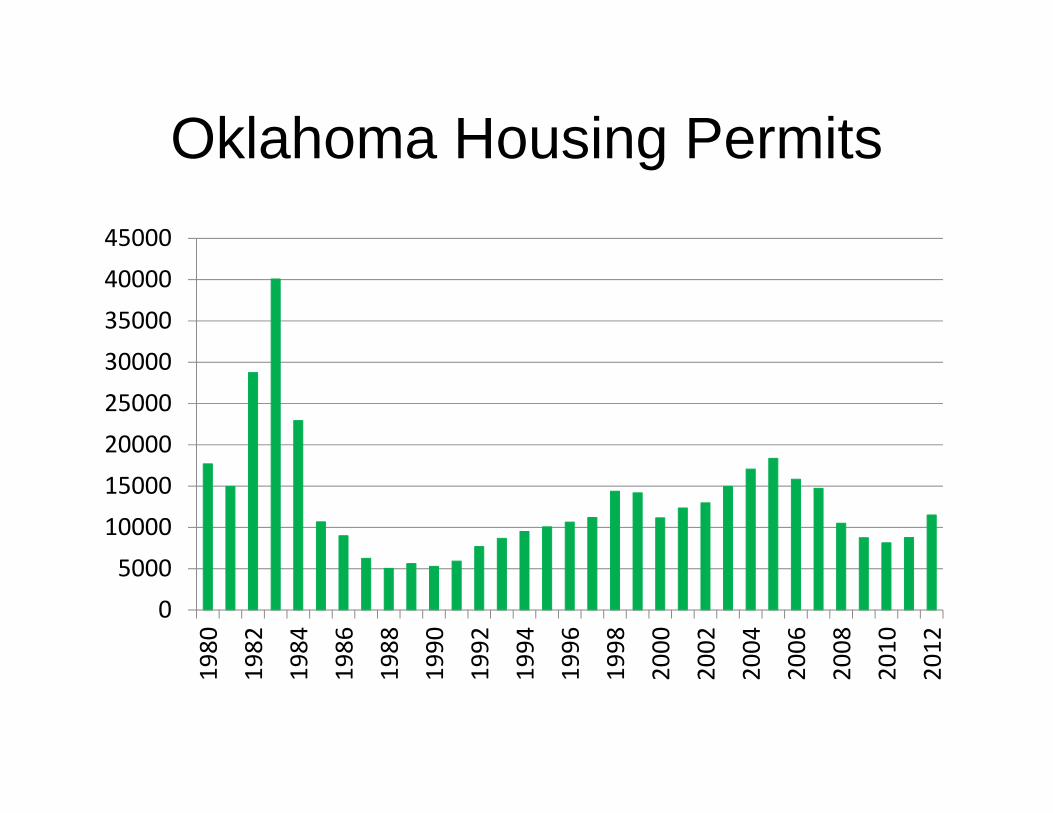

Oklahoma Housing Permits

05000

1000015000200002500030000350004000045000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

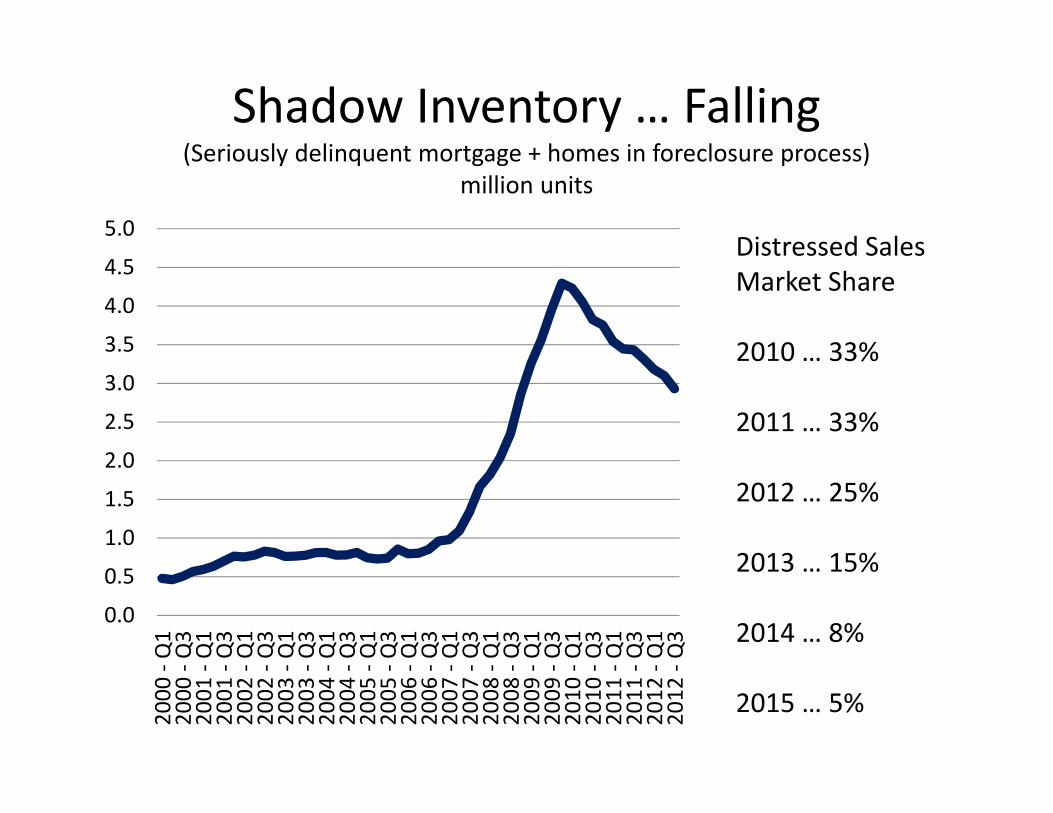

Shadow Inventory … Falling(Seriously delinquent mortgage + homes in foreclosure process)

million units

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2000

‐ Q1

2000

‐ Q3

2001

‐ Q1

2001

‐ Q3

2002

‐ Q1

2002

‐ Q3

2003

‐ Q1

2003

‐ Q3

2004

‐ Q1

2004

‐ Q3

2005

‐ Q1

2005

‐ Q3

2006

‐ Q1

2006

‐ Q3

2007

‐ Q1

2007

‐ Q3

2008

‐ Q1

2008

‐ Q3

2009

‐ Q1

2009

‐ Q3

2010

‐ Q1

2010

‐ Q3

2011

‐ Q1

2011

‐ Q3

2012

‐ Q1

2012

‐ Q3

Distressed Sales Market Share

2010 … 33%

2011 … 33%

2012 … 25%

2013 … 15%

2014 … 8%

2015 … 5%

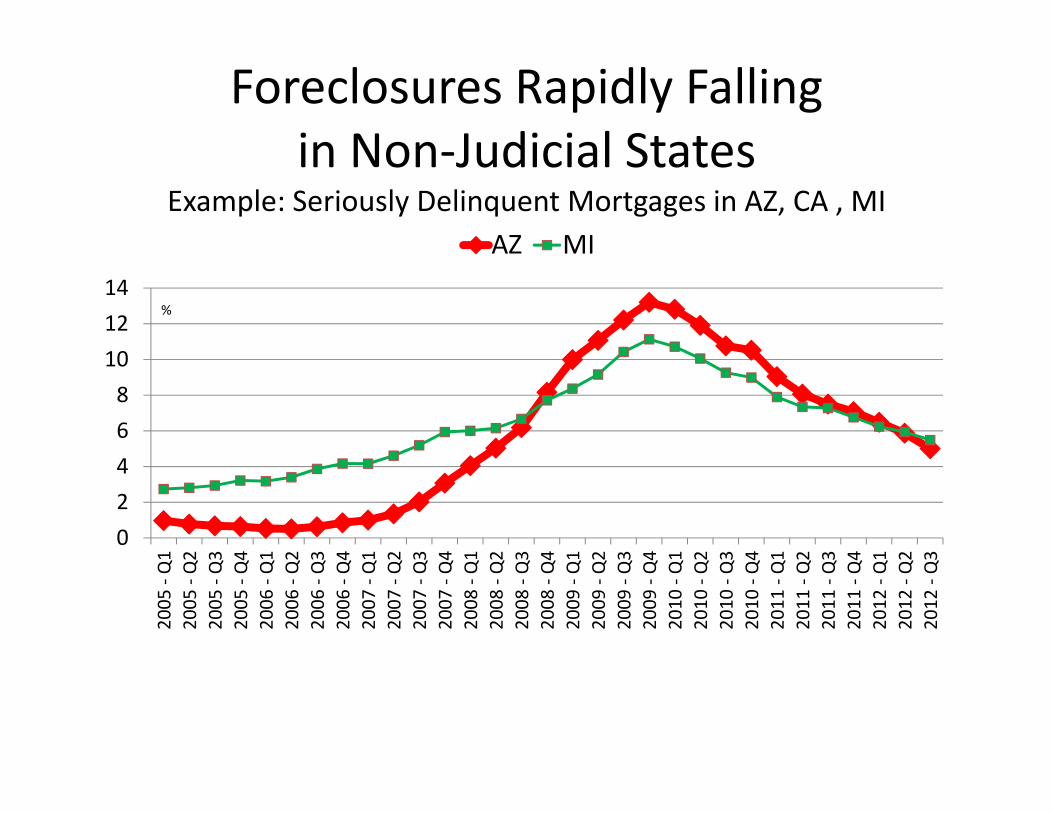

Foreclosures Rapidly Falling in Non‐Judicial States

Example: Seriously Delinquent Mortgages in AZ, CA , MI

02468101214

2005

‐ Q1

2005

‐ Q2

2005

‐ Q3

2005

‐ Q4

2006

‐ Q1

2006

‐ Q2

2006

‐ Q3

2006

‐ Q4

2007

‐ Q1

2007

‐ Q2

2007

‐ Q3

2007

‐ Q4

2008

‐ Q1

2008

‐ Q2

2008

‐ Q3

2008

‐ Q4

2009

‐ Q1

2009

‐ Q2

2009

‐ Q3

2009

‐ Q4

2010

‐ Q1

2010

‐ Q2

2010

‐ Q3

2010

‐ Q4

2011

‐ Q1

2011

‐ Q2

2011

‐ Q3

2011

‐ Q4

2012

‐ Q1

2012

‐ Q2

2012

‐ Q3

AZ MI

%

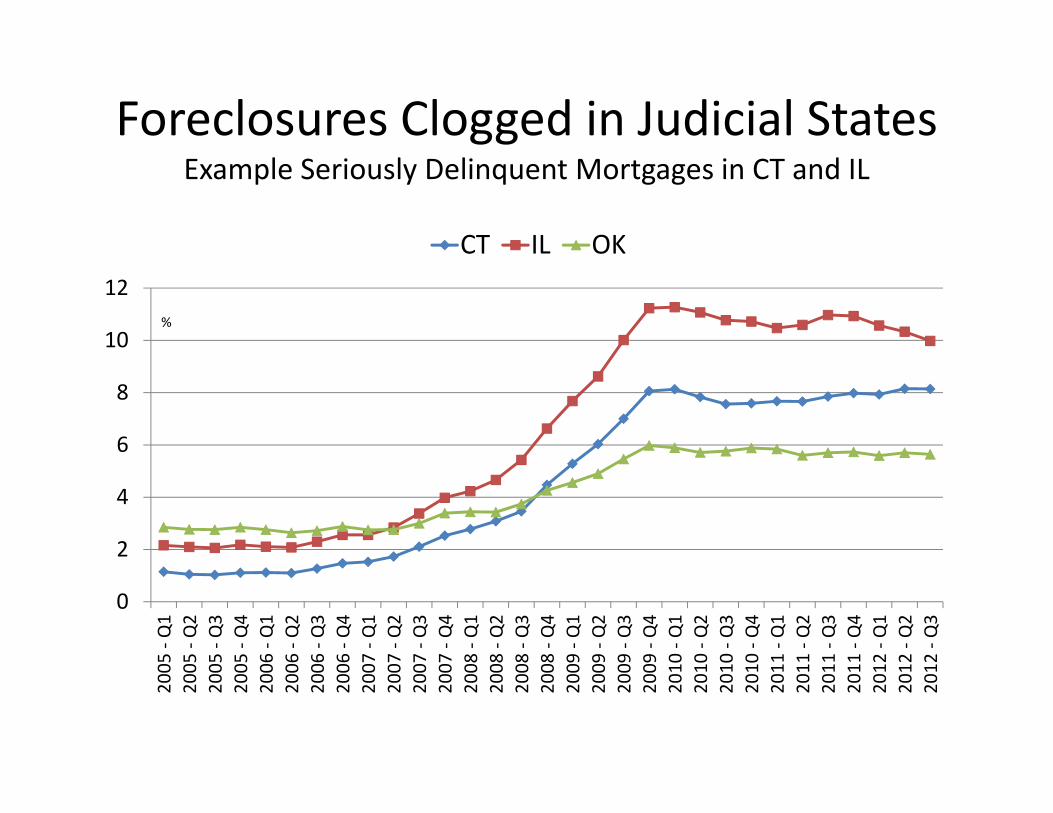

Foreclosures Clogged in Judicial States Example Seriously Delinquent Mortgages in CT and IL

0

2

4

6

8

10

12

2005

‐ Q1

2005

‐ Q2

2005

‐ Q3

2005

‐ Q4

2006

‐ Q1

2006

‐ Q2

2006

‐ Q3

2006

‐ Q4

2007

‐ Q1

2007

‐ Q2

2007

‐ Q3

2007

‐ Q4

2008

‐ Q1

2008

‐ Q2

2008

‐ Q3

2008

‐ Q4

2009

‐ Q1

2009

‐ Q2

2009

‐ Q3

2009

‐ Q4

2010

‐ Q1

2010

‐ Q2

2010

‐ Q3

2010

‐ Q4

2011

‐ Q1

2011

‐ Q2

2011

‐ Q3

2011

‐ Q4

2012

‐ Q1

2012

‐ Q2

2012

‐ Q3

CT IL OK

%

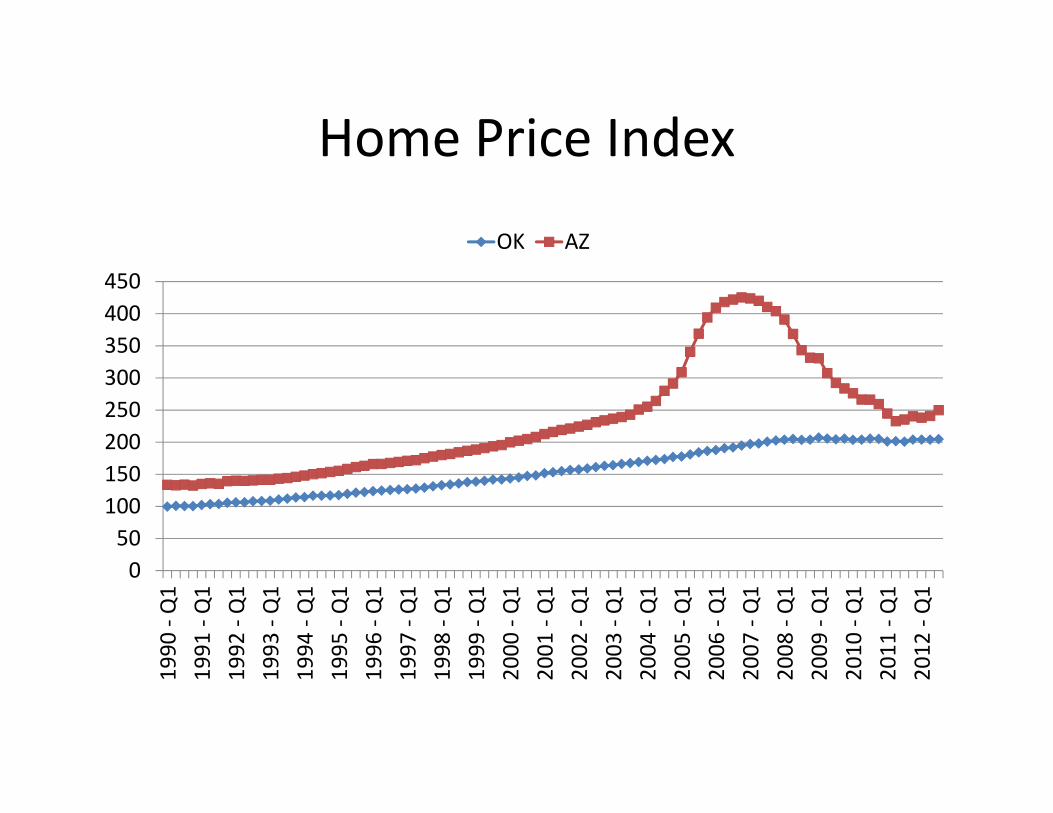

Home Price Index

050100150200250300350400450

1990

‐ Q1

1991

‐ Q1

1992

‐ Q1

1993

‐ Q1

1994

‐ Q1

1995

‐ Q1

1996

‐ Q1

1997

‐ Q1

1998

‐ Q1

1999

‐ Q1

2000

‐ Q1

2001

‐ Q1

2002

‐ Q1

2003

‐ Q1

2004

‐ Q1

2005

‐ Q1

2006

‐ Q1

2007

‐ Q1

2008

‐ Q1

2009

‐ Q1

2010

‐ Q1

2011

‐ Q1

2012

‐ Q1

OK AZ

Forecast #3: More Unequal Wealth Distribution

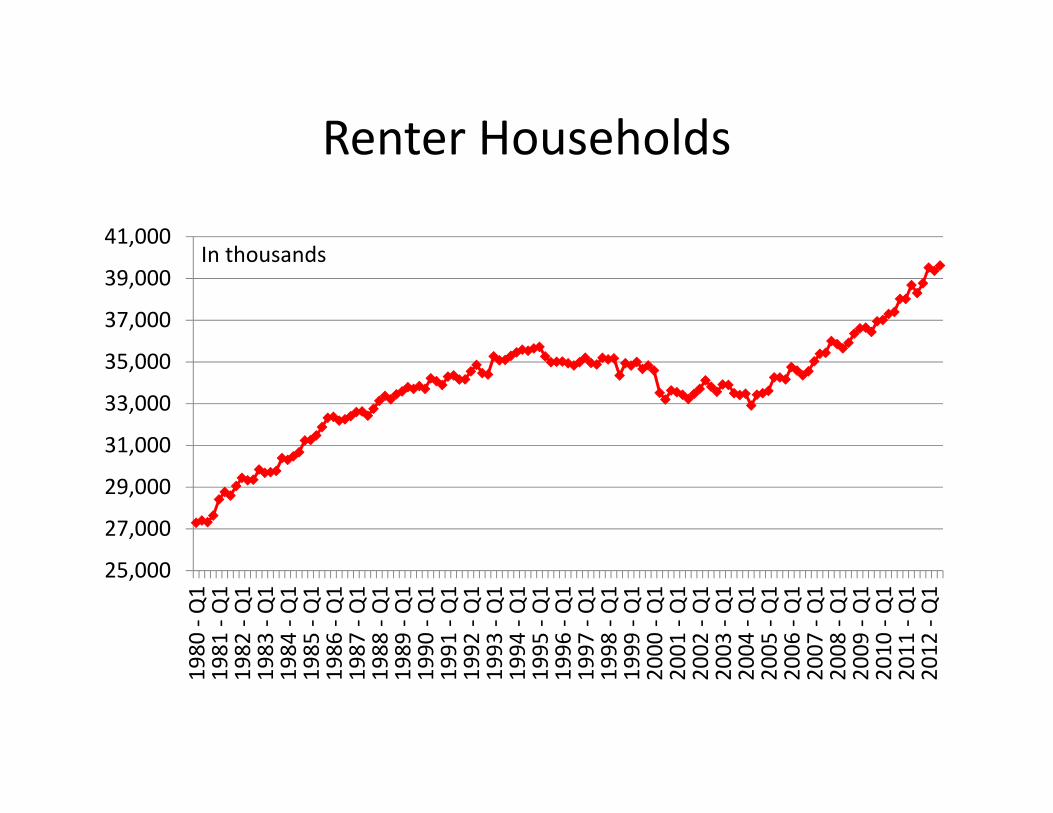

• Renters do not accumulate wealth• Renter population rising• Homeowners build wealth after buying at low prices

• Stagnant homeowner population• Tight Credit hinders ‘good’ renters from becoming homeowners

• Investors becoming increasing share of property owners

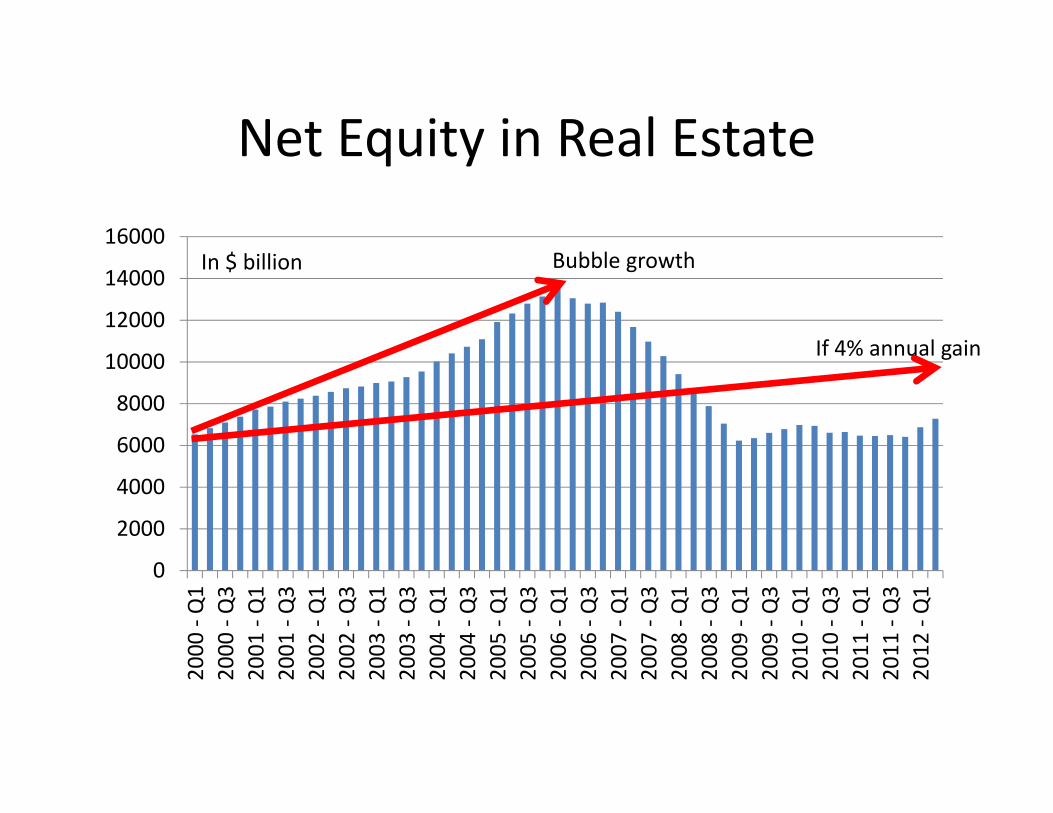

Net Equity in Real Estate

0

2000

4000

6000

8000

10000

12000

14000

16000

2000

‐ Q1

2000

‐ Q3

2001

‐ Q1

2001

‐ Q3

2002

‐ Q1

2002

‐ Q3

2003

‐ Q1

2003

‐ Q3

2004

‐ Q1

2004

‐ Q3

2005

‐ Q1

2005

‐ Q3

2006

‐ Q1

2006

‐ Q3

2007

‐ Q1

2007

‐ Q3

2008

‐ Q1

2008

‐ Q3

2009

‐ Q1

2009

‐ Q3

2010

‐ Q1

2010

‐ Q3

2011

‐ Q1

2011

‐ Q3

2012

‐ Q1

In $ billion

If 4% annual gain

Bubble growth

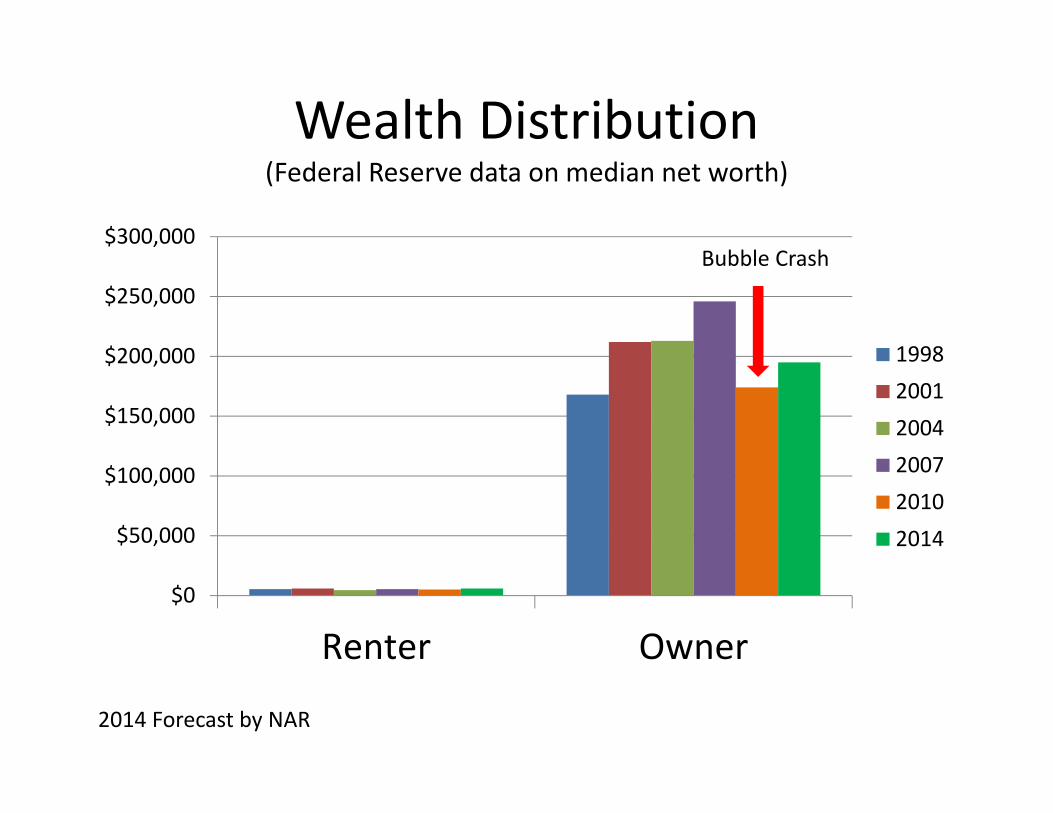

Wealth Distribution (Federal Reserve data on median net worth)

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

Renter Owner

199820012004200720102014

2014 Forecast by NAR

Bubble Crash

Renter Households

25,000

27,000

29,000

31,000

33,000

35,000

37,000

39,000

41,000

1980

‐ Q1

1981

‐ Q1

1982

‐ Q1

1983

‐ Q1

1984

‐ Q1

1985

‐ Q1

1986

‐ Q1

1987

‐ Q1

1988

‐ Q1

1989

‐ Q1

1990

‐ Q1

1991

‐ Q1

1992

‐ Q1

1993

‐ Q1

1994

‐ Q1

1995

‐ Q1

1996

‐ Q1

1997

‐ Q1

1998

‐ Q1

1999

‐ Q1

2000

‐ Q1

2001

‐ Q1

2002

‐ Q1

2003

‐ Q1

2004

‐ Q1

2005

‐ Q1

2006

‐ Q1

2007

‐ Q1

2008

‐ Q1

2009

‐ Q1

2010

‐ Q1

2011

‐ Q1

2012

‐ Q1

In thousands

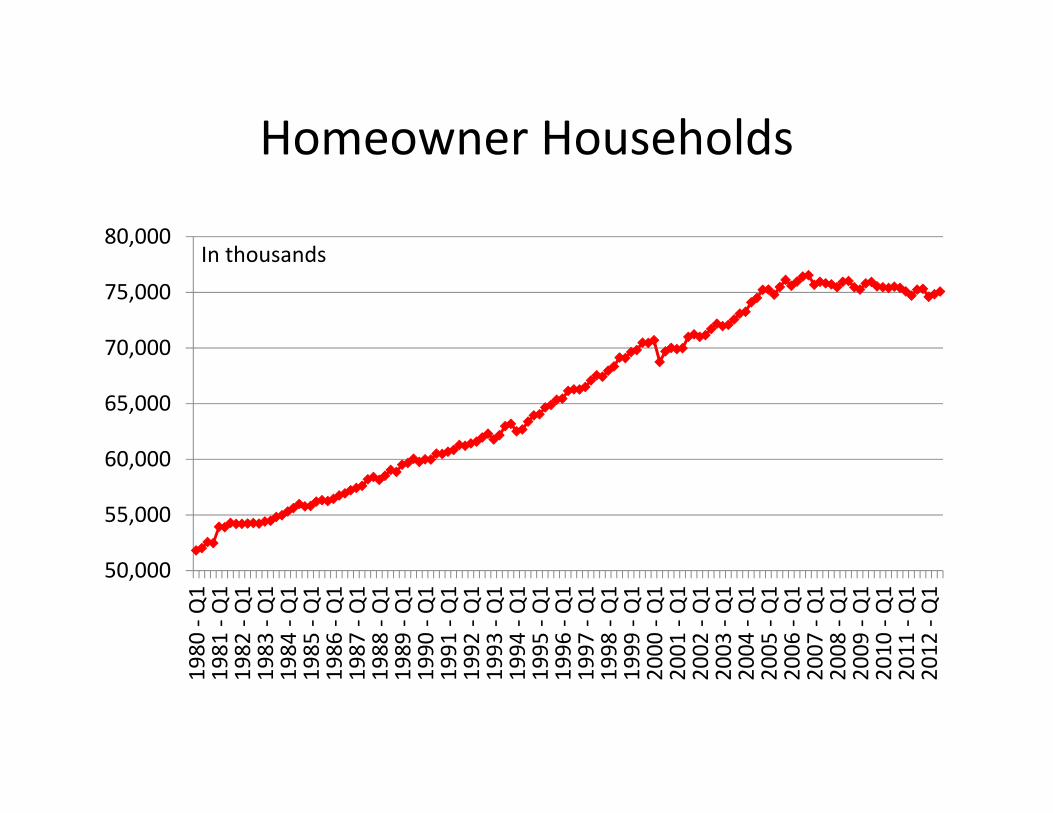

Homeowner Households

50,000

55,000

60,000

65,000

70,000

75,000

80,000

1980

‐ Q1

1981

‐ Q1

1982

‐ Q1

1983

‐ Q1

1984

‐ Q1

1985

‐ Q1

1986

‐ Q1

1987

‐ Q1

1988

‐ Q1

1989

‐ Q1

1990

‐ Q1

1991

‐ Q1

1992

‐ Q1

1993

‐ Q1

1994

‐ Q1

1995

‐ Q1

1996

‐ Q1

1997

‐ Q1

1998

‐ Q1

1999

‐ Q1

2000

‐ Q1

2001

‐ Q1

2002

‐ Q1

2003

‐ Q1

2004

‐ Q1

2005

‐ Q1

2006

‐ Q1

2007

‐ Q1

2008

‐ Q1

2009

‐ Q1

2010

‐ Q1

2011

‐ Q1

2012

‐ Q1

In thousands

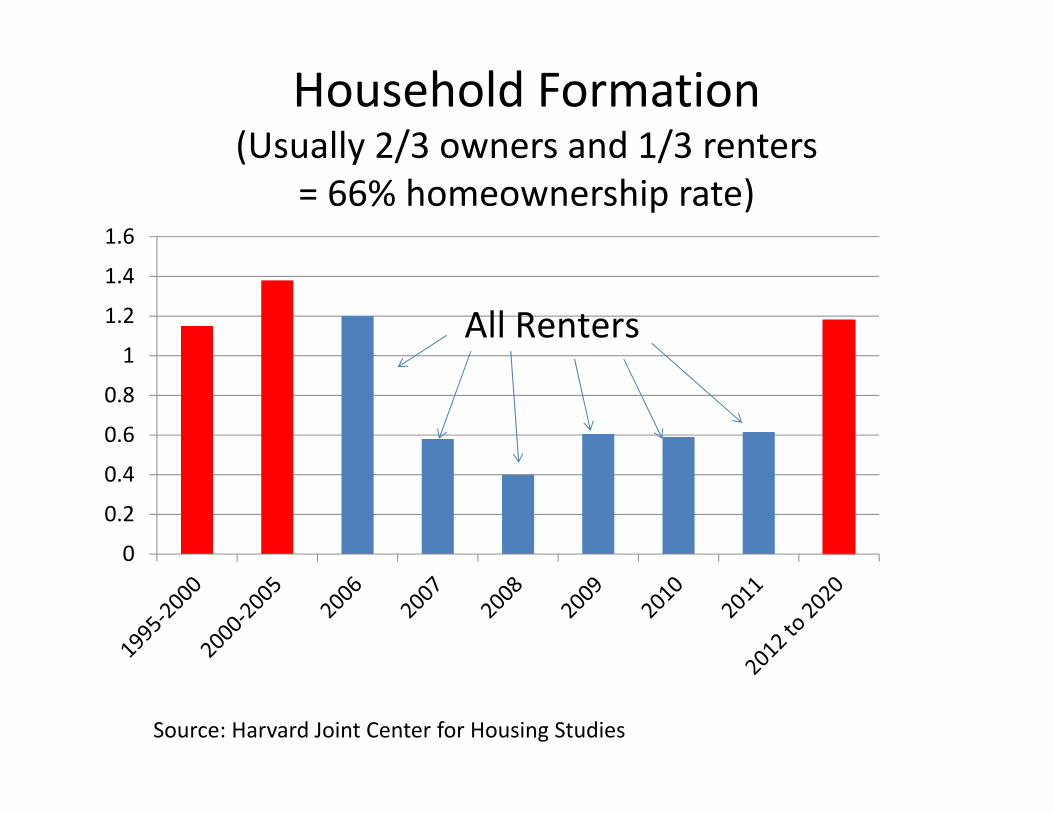

Household Formation(Usually 2/3 owners and 1/3 renters

= 66% homeownership rate)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

All Renters

Source: Harvard Joint Center for Housing Studies

Economic Backdrop

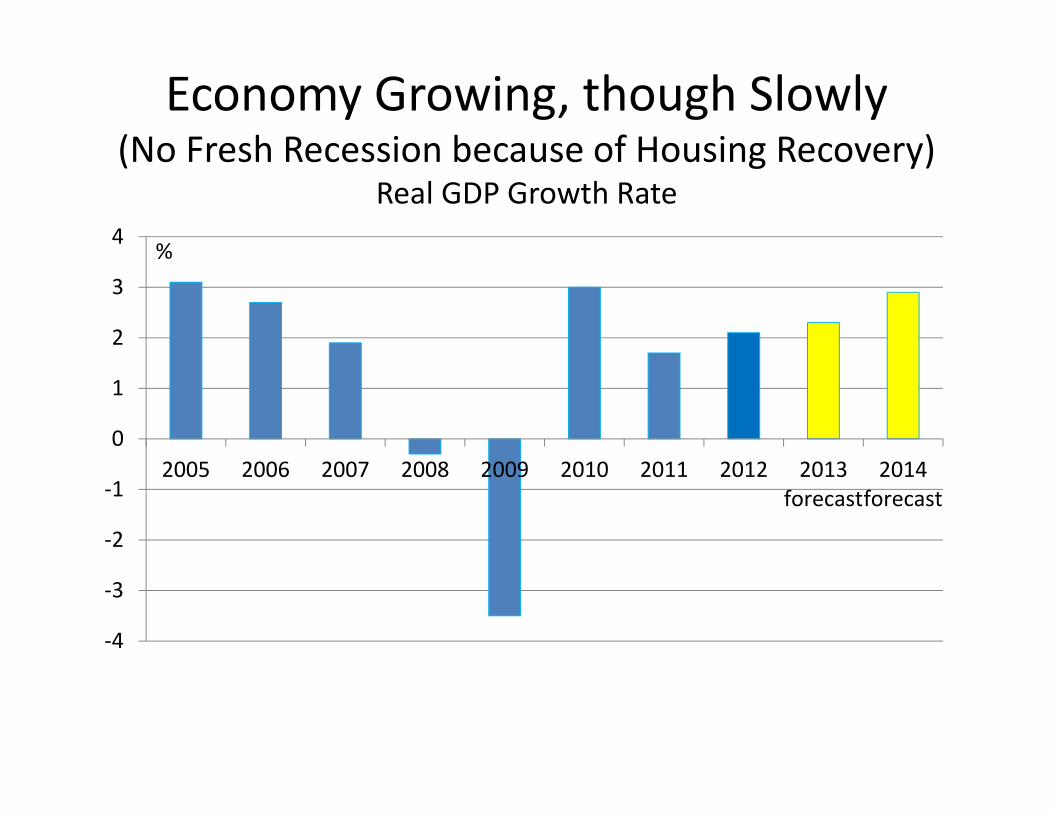

Economy Growing, though Slowly(No Fresh Recession because of Housing Recovery)

Real GDP Growth Rate

‐4

‐3

‐2

‐1

0

1

2

3

4

2005 2006 2007 2008 2009 2010 2011 2012 2013forecast

2014forecast

%

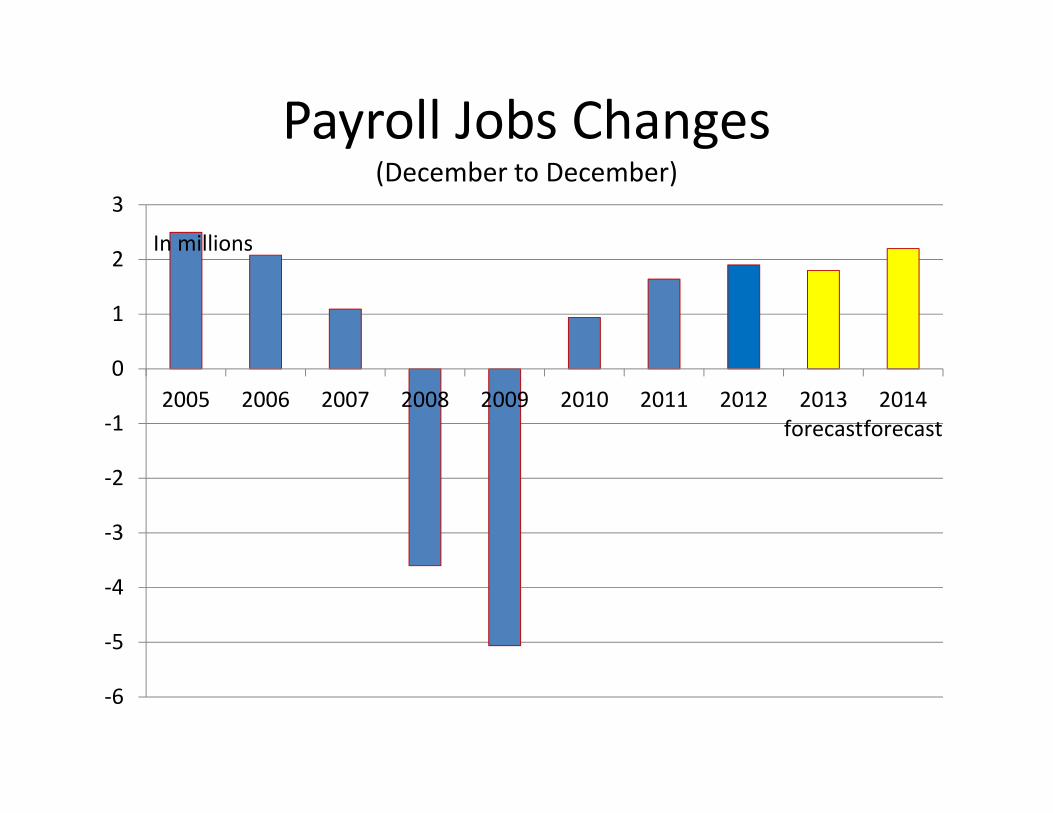

Payroll Jobs Changes(December to December)

‐6

‐5

‐4

‐3

‐2

‐1

0

1

2

3

2005 2006 2007 2008 2009 2010 2011 2012 2013forecast

2014forecast

In millions

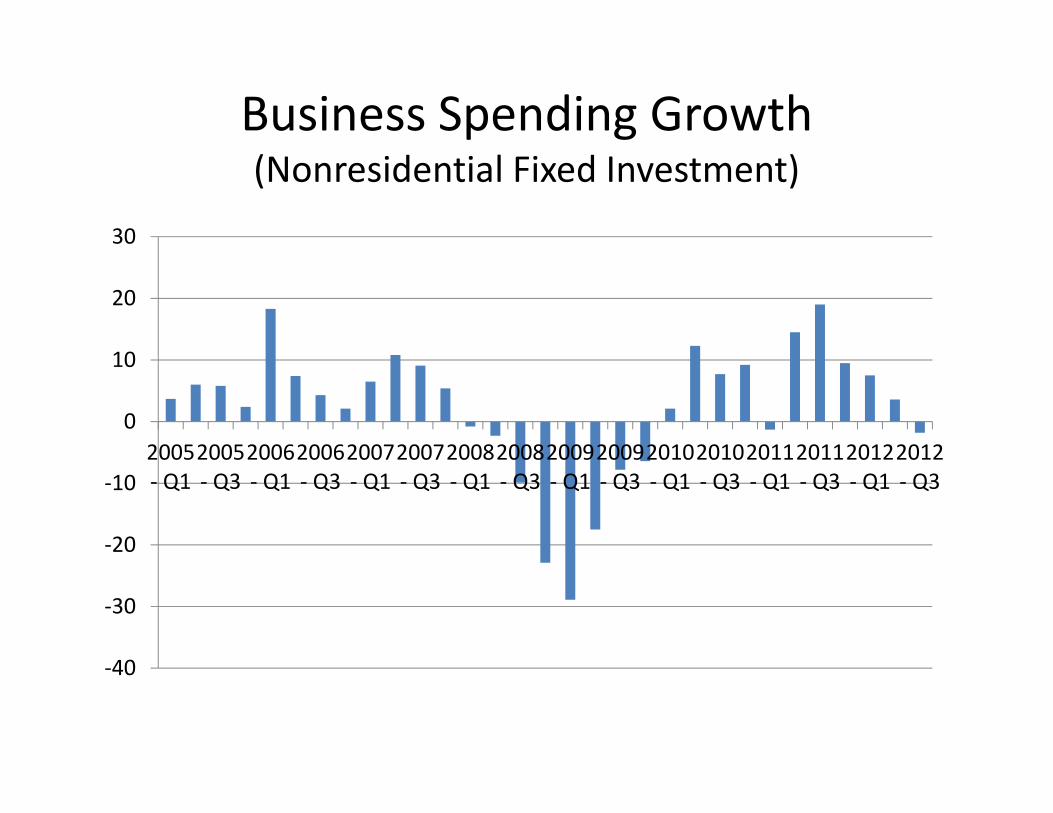

Business Spending Growth(Nonresidential Fixed Investment)

‐40

‐30

‐20

‐10

0

10

20

30

2005‐ Q1

2005‐ Q3

2006‐ Q1

2006‐ Q3

2007‐ Q1

2007‐ Q3

2008‐ Q1

2008‐ Q3

2009‐ Q1

2009‐ Q3

2010‐ Q1

2010‐ Q3

2011‐ Q1

2011‐ Q3

2012‐ Q1

2012‐ Q3

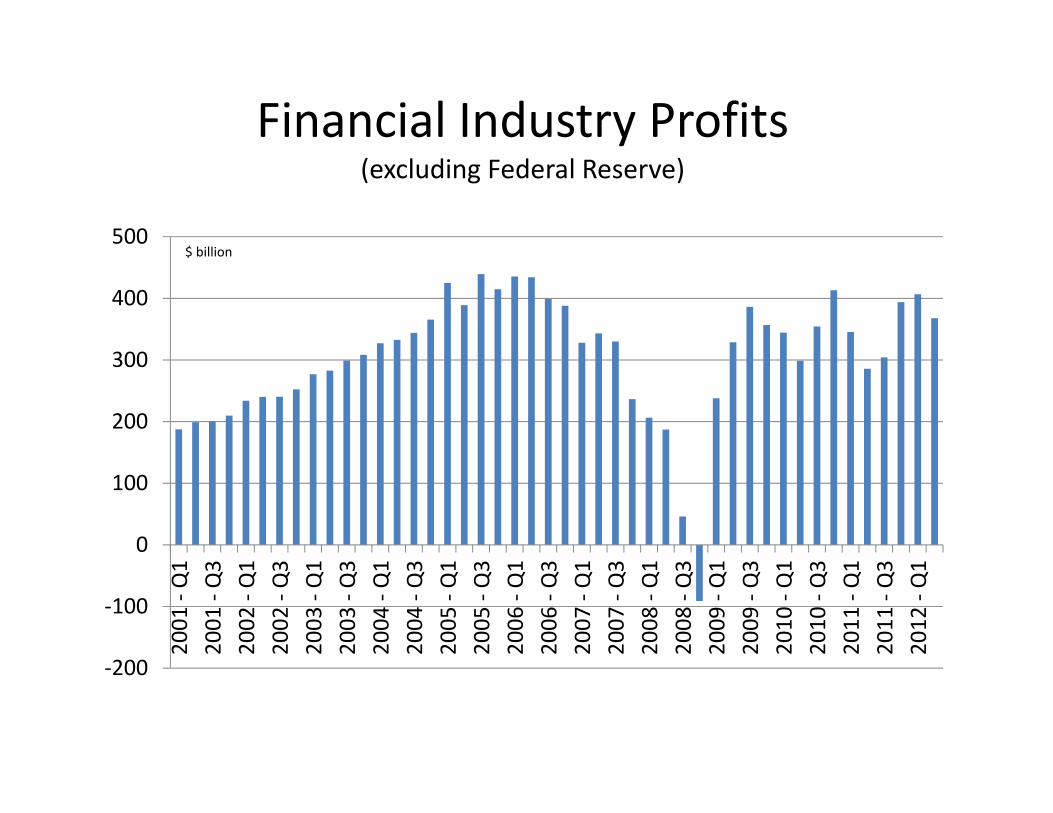

Financial Industry Profits(excluding Federal Reserve)

‐200

‐100

0

100

200

300

400

500

2001

‐ Q1

2001

‐ Q3

2002

‐ Q1

2002

‐ Q3

2003

‐ Q1

2003

‐ Q3

2004

‐ Q1

2004

‐ Q3

2005

‐ Q1

2005

‐ Q3

2006

‐ Q1

2006

‐ Q3

2007

‐ Q1

2007

‐ Q3

2008

‐ Q1

2008

‐ Q3

2009

‐ Q1

2009

‐ Q3

2010

‐ Q1

2010

‐ Q3

2011

‐ Q1

2011

‐ Q3

2012

‐ Q1

$ billion

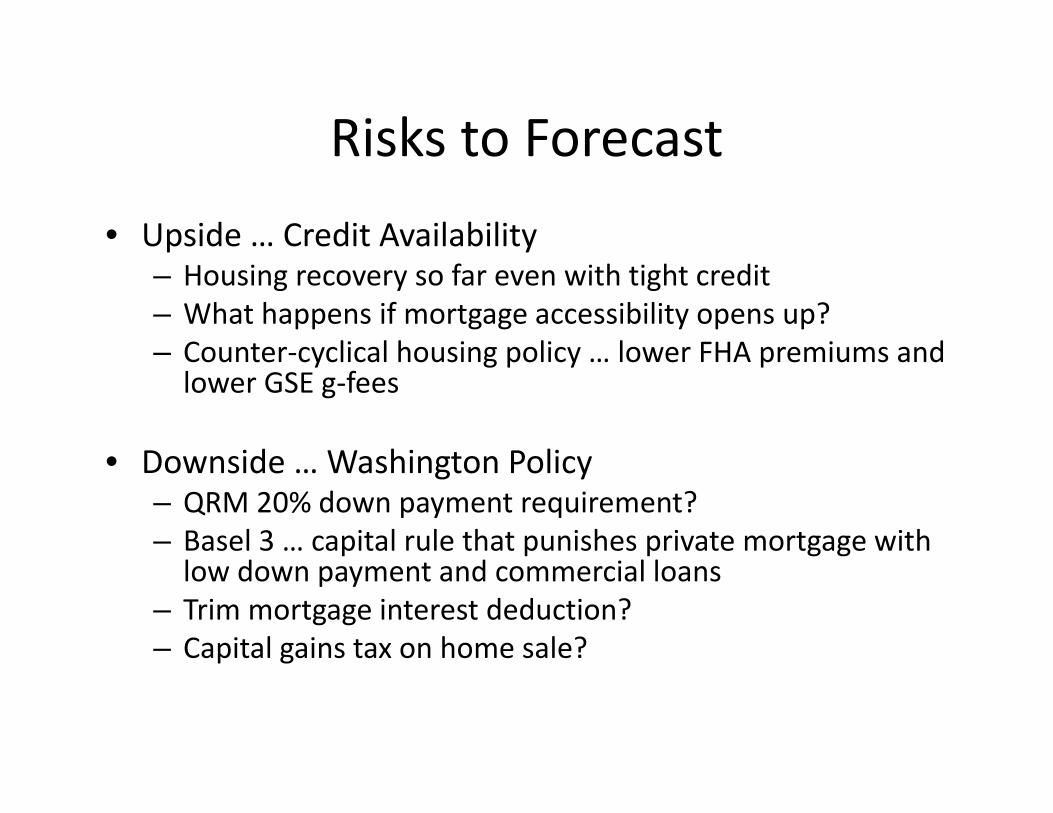

Risks to Forecast• Upside … Credit Availability

– Housing recovery so far even with tight credit– What happens if mortgage accessibility opens up?– Counter‐cyclical housing policy … lower FHA premiums and lower GSE g‐fees

• Downside … Washington Policy– QRM 20% down payment requirement?– Basel 3 … capital rule that punishes private mortgage with low down payment and commercial loans

– Trim mortgage interest deduction?– Capital gains tax on home sale?

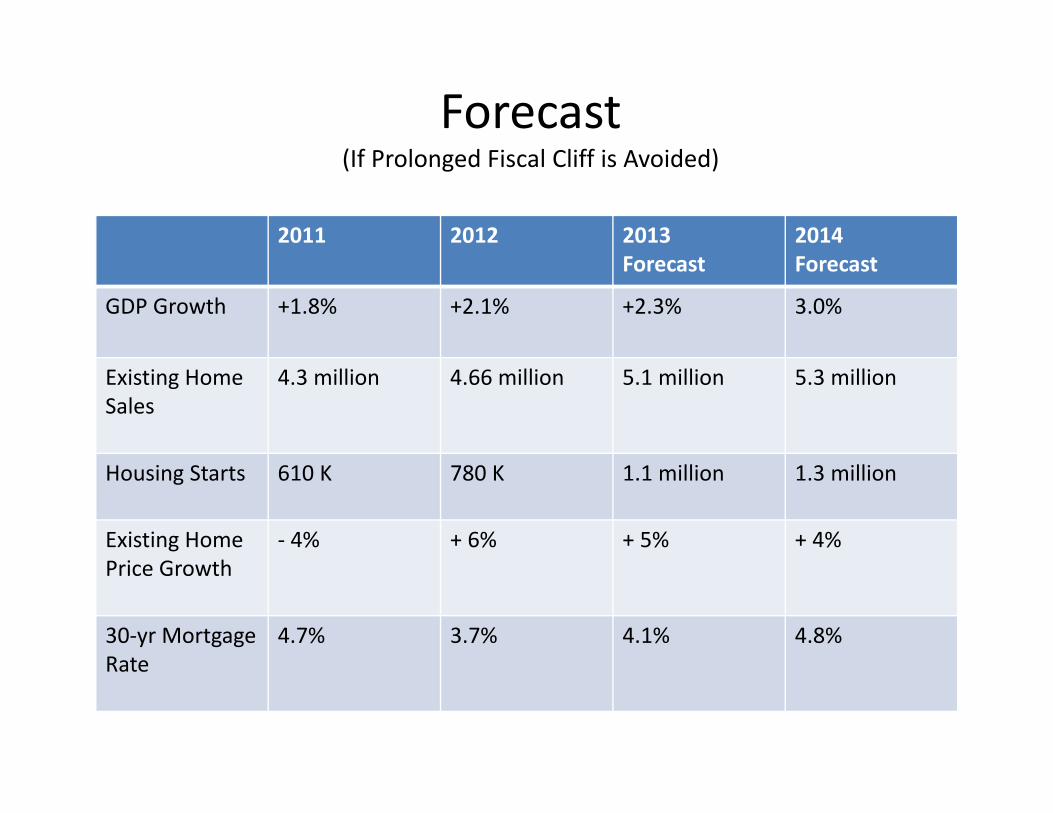

Forecast(If Prolonged Fiscal Cliff is Avoided)

2011 2012 2013Forecast

2014Forecast

GDP Growth +1.8% +2.1% +2.3% 3.0%

Existing Home Sales

4.3 million 4.66 million 5.1 million 5.3 million

Housing Starts 610 K 780 K 1.1 million 1.3 million

Existing Home Price Growth

‐ 4% + 6% + 5% + 4%

30‐yr MortgageRate

4.7% 3.7% 4.1% 4.8%

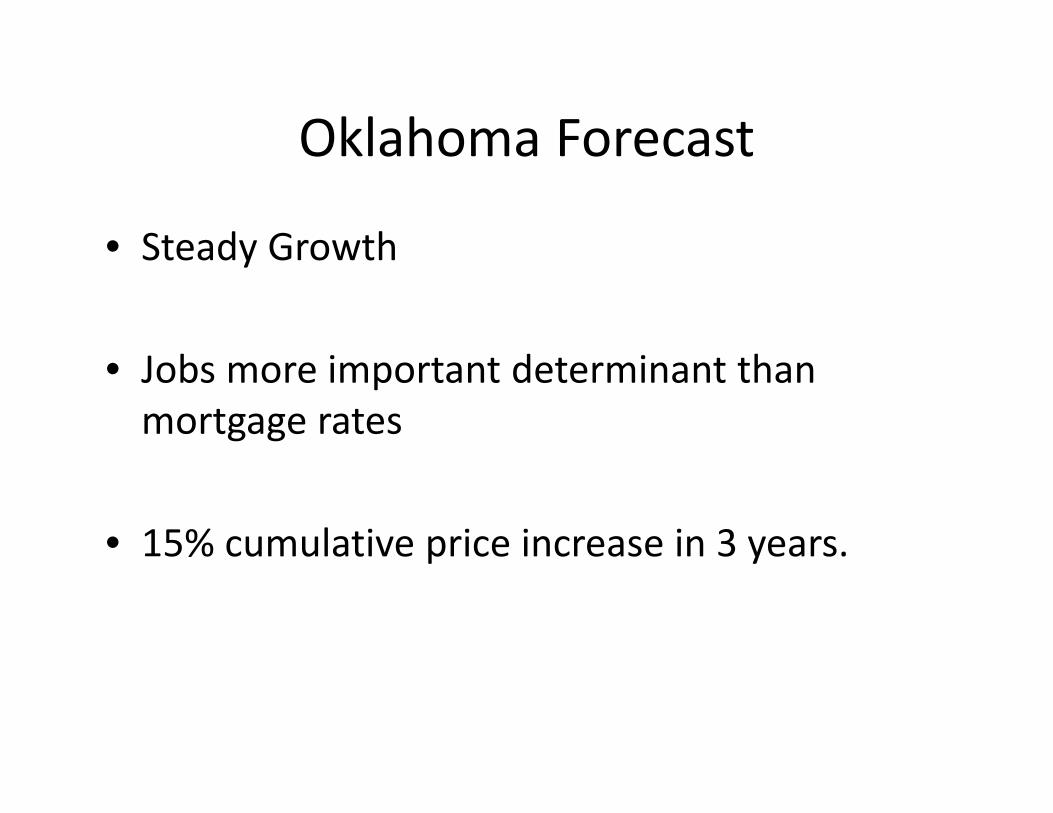

Oklahoma Forecast

• Steady Growth

• Jobs more important determinant than mortgage rates

• 15% cumulative price increase in 3 years.

For Daily Update and Analysis

• Twitter @NAR_Research

• Do not offend your homebuyers by offering …

Related Documents