ab Market drivers Continued upswing for the real estate market Residential real estate Increased threat level for private homes Commercial real estate Quality more important than ever Listed real estate Last yearʹ s performance hard to beat The real estate market in Switzerland 2011 UBS real estate focus Research Switzerland January 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ab

Market drivers Continued upswing for the real estate market

Residential real estate Increased threat level for private homes

Commercial real estate Quality more important than ever

Listed real estate Last yearʹs performance hard to beat

The real estate market in Switzerland2011

UBS real estate focusResearch Switzerland

January 2011

UBS real estate focus January 20112

Content

UBS real estate focus 2011

This report has been prepared by UBS AG

Please see the important disclaimer at the

end of the document Past performance is

not an indication of future returns The

market prices provided are closing prices on

the respective principal stock exchange

Publisher

UBS AG Wealth Management Research

(WMR) PO Box CH-8098 Zurich

Editor in chief

Claudio Saputelli

Editors

Anna Marie Focagrave Roy Greenspan

Authors

Daniel Bruumlllmann Patric Caillat Urs Faumls

Gunnar Herm Caesar Lack

Dalibor Maksimovic Stefan R Meyer

Achim Peijan Claudio Saputelli

Niklaus Scheerer Christian Unternaumlhrer

Thomas Veraguth Markus Wagemann

Editorial deadline

3 January 2011

Project management

Caspar Heer

Desktop

Werner Kuonen Margrit Oppliger

Linda Sutter

Translation

24translate St Gallen Switzerland

Pictures

wwwmasterfi lecom

Printer

Druckerei Flawil AG Flawil Switzerland

Languages

English German French and Italian

Contact

ubs-researchubscom

These authors are from units outside Wealth Manage-ment Research These units are not subject to all legal provisions governing the independence of fi nancial research The ldquoDirectives on the Independence of Financial Researchrdquo issued by the Board of Directors of the Swiss Bankers Association (SBA) do not apply

SAP No 83518E-1101

Editorial 3

At a glance 4

Market drivers

Business cycle and income 6

Infl ation and interest rates 7

Population and employment 8

Overview of property market drivers 8

Residential real estate

Homes ndash elevated threat level 10

Rental apartments ndash steady returns 12

Overview of residential properties 12

In focus

Imputed rental values ndash a violation of classic tax theory 13

Occupational pension withdrawals ndash a dangerous game 15

Full-service living ndash a hot new trend 17

Commercial real estate and special uses

Offi ce properties ndash separating the wheat from the chaff 20

Retail space ndash zero growth expected 22

Overview of commercial properties 22

In focus

Public-private partnership ndash more than a buzzword 23

Hospital real estate in upheaval 25

Global real estate investments ndash diversifi cation

opportunities abound 27

Listed real estate and investment foundations

Real estate equities ndash on solid ground 30

Real estate funds ndash an attractive addition to portfolios 31

Overview of listed real estate 32

In focus

The rise of Swiss real estate equities 33

Trend watch ndash exchange-traded real estate funds 35

Property investment groups of investment

foundations ndash on the advance 37

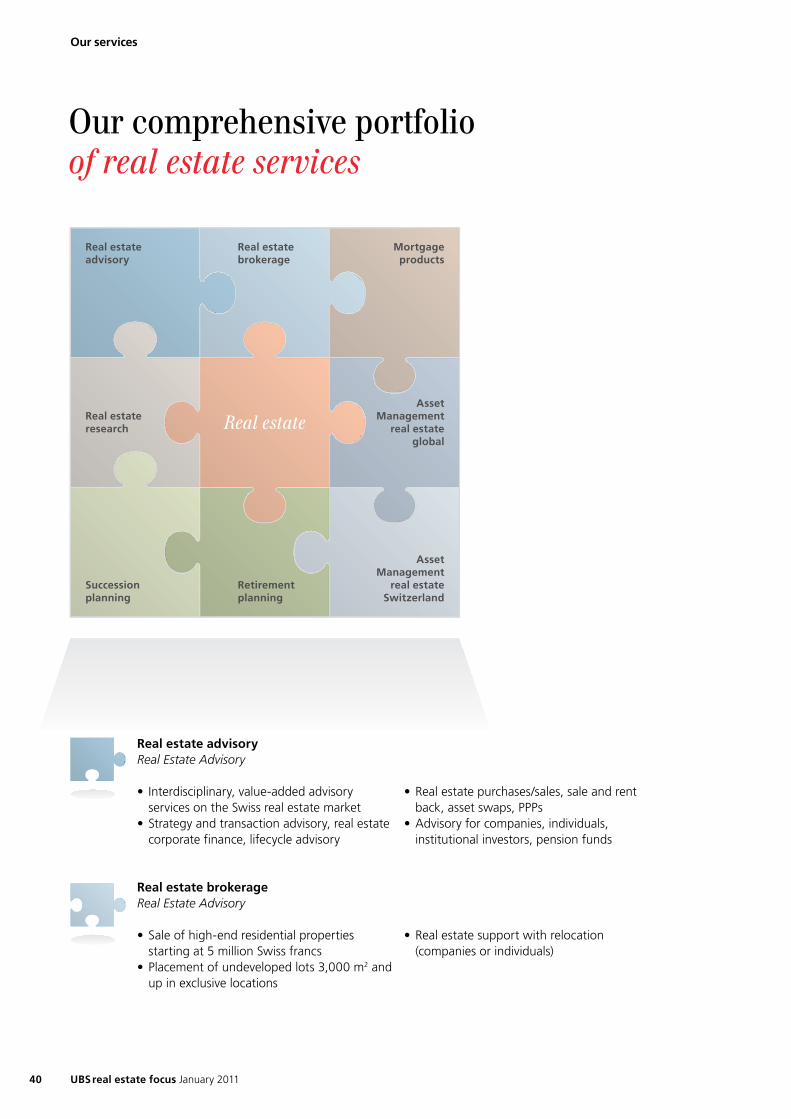

Our services

Our comprehensive portfolio of real estate services 40

Selection of research publications 42

Order or subscribe

UBS clients can subscribe to the print version of UBS real estate focus via their client advisor or

the Printed amp Branded Products Mailbox sh-iz-ubs-publikationenubscom

Electronic subscription is also available via the WMR portal on the UBS e-banking platform

UBS real estate focus January 2011 3

Editorial

Daniel Kalt

Claudio Saputelli

Dear reader

ldquoReal estate is at the core of almost every businessrdquo claims US real estate mogul

Donald Trump He is right ndash to an extent It is true that real estate dominates the

workdays of the authors of this new publication UBS real estate focus What really

matters for our business however is our clients They get us involved in a variety of

issues from basic advisory services on property transactions to complex fi nancing

deals for large PPP projects

Besides serving clients UBSrsquos real estate teams also gain insights by sharing ideas

and supporting one another in an internal network Over the years they have ac-

quired a broad and deep base of real estate expertise We share this expertise with

you in UBS real estate focus our new in-depth annual study of the real estate mar-

ket Every year brings new insights In our quest to fi nd client-specifi c real estate

solutions we continue to challenge ourselves explore new disciplines and develop

innovative ideas

UBS real estate focus consists of four chapters The fi rst chapter ldquoMarket driversrdquo

explains the main macroeconomic factors aff ecting the Swiss real estate market

The next two chapters ldquoResidential propertyrdquo and ldquoCommercial property and spe-

cial usesrdquo focus on direct real estate investments Chapter four looks at indirect real

estate investments ndash investment foundations and listed real estate Each chapter

begins with a market overview followed by three focus articles on the latest market

issues This structure helps you quickly get up to speed on the topics we cover

We hope that UBS real estate focus will help you make sound real estate decisions

We have made our analyses more actionable by including boxes with recommenda-

tions in the focus articles We do agree with Donald Trump in one regard ldquoIn order

to build your wealth and improve your business smarts you need to know about

real estaterdquo

We hope you enjoy reading this issue of UBS real estate focus

Claudio Saputelli

Head Real Estate Research

Wealth Management Research

Daniel Kalt

Chief Economist Switzerland

Wealth Management Research

UBS real estate focus January 20114

At a glance

Residential real estate

Home prices continue to soar This up-

ward trend has not fl attened out as ex-

pected in previous quarters The public is

increasingly worried about a real estate

bubble ndash with some justifi cation Caution

is advised Page 10

The rental apartment market is stable and

harbors upside potential Prices for multi-

family dwellings have made commercial

properties increasingly attractive to inves-

tors Page 12

In focus

Imputed rental values ndash

a violation of classic tax theory

The taxation of imputed rental values as

income is controversial For years there

have been heated discussions about this

issue Last summer the Federal Council

threw its hat in the ring supporting a

total abolition of the tax in order to sim-

plify the tax code Page 13

Occupational pension with -

drawals ndash a dangerous game

An estimated 520000 withdrawals have

been made from retirement accounts since

1995 The withdrawn capital is expected

to exceed 35 billion Swiss francs in 2010

The possible impact on future retirement

benefi ts remains unknown but the risks

should not be ignored Page 15

Full-service living ndash a hot new trend

Full-service living is an innovative concept

that caters to urban residentsrsquo demand

for greater comfort and higher living

standards Already established abroad

this model is fast gaining adherents in

Switzerland Page 17

Commercial real estate and

special uses

The Swiss offi ce property market came

through the global economic crisis in

relatively good shape We expect price

pressure from tenants to widen the per-

formance gap between central and

peripheral locations Page 20

Consumer confi dence is stronger in Swit-

zerland than in many other countries This

benefi ts retailers and real estate investors

alike but investment performance increas-

ingly hinges on property quality Page 22

In focus

Public-private partnership ndash more

than a buzzword

Governments and companies have a

long history of collaboration However

public-private partners have to do more

than just work together They also need

to defi ne processes to structure their

relationship allocate risk award con-

tracts and lay down ground rules for

the partnership Page 23

Hospital real estate in upheaval

Switzerlandrsquos hospital system is complex

Its structure buildings and fi nancing are

on the cusp of a radical transformation

This change opens up attractive opportu-

nities for investors Page 25

Global real estate investments ndash

diversifi cation opportunities abound

The global real estate market is frag-

mented along national and regional lines

o en making entrance into specifi c mar-

kets diffi cult Direct and indirect real

estate investment products can overcome

these barriers and they off er attractive

diversifi cation opportunities in a global

economy Page 27

Listed real estate and investment

foundations

Real estate equities performed well in

2010 ndash partly due to their own merits

and partly due to a favorable economic

environment The coming year looks to

be much tougher though Page 30

Exchange-traded real estate funds appeal

to investors because they combine fea-

tures of stocks bonds and real estate

This mix is refl ected in the riskreturn

profi les of funds making them an attrac-

tive choice for mixed portfolios

Page 31

In focus

The rise of Swiss real estate equities

This young segment of the Swiss equity

market has seen plenty of IPOs acquisi-

tions rights issues and secondary off er-

ings Despite their short histories and

rapid changes Switzerlandrsquos leading real

estate equities are good choices for de-

fensive long-term investors Page 33

Trend watch ndash exchange-traded

real estate funds

Swiss real estate funds are the current

darlings of private and institutional inves-

tors Strong demand has given rise to

new products and improved transpar-

ency More IPOs rights issues and sec-

ondary off erings should keep market

momentum strong Page 35

Property investment groups of

investment foundations ndash

on the advance

Investment foundations hold real estate

investments with strong market posi-

tions and impressive momentum They

off er attractive product features Pen-

sion fundsrsquo property contributions make

a signifi cant contribution to fueling

growth Page 37

UBS real estate focus January 2011 5

Market drivers

Green lights ahead for key demand drivers

UBS real estate focus January 20116

Market drivers

Business cycle and income

We expect the Swiss economy to grow

more than 2 percent in the next two years

This is well above the historical average

and should boost real estate prices

The Swiss economy has been on the rebound

since mid-2009 Its recession was much mild er

than in most other industrialized western coun-

tries Indeed the Swiss economy is not only

recovering faster than expected it is recovering

faster than the rest of Europe According to the

State Secretariat for Economic Aff airs (Seco) real

gross domestic product (GDP) has expanded an

average of 3 percent in terms of annualized

quarter-on-quarter growth since the recession

ended It even broke above precrisis levels in the

third quarter of 2010

Suffi cient skilled personnel and healthy

balance sheets

The Swiss economy probably owes its surpris-

ingly strong momentum to an agreement with

the European Union on the free movement of

persons Free movement stimulates economic

growth by making it easier for companies to

hire skilled staff The resulting immigration also

supports consumption and construction invest-

ment and directly increases GDP Plus unlike

many other industrialized western countries

Switzerlandrsquos private- and public-sector balance

sheets are in rude health Switzerland is one of

the few countries that did not live beyond its

means in the run-up to the crisis Compared

to other countries Switzerland as a whole

(governments households and companies) has

relatively large holdings of net foreign assets

ndash over 100 percent of GDP Switzerland is also

in an enviable position in terms of public fi -

nances It has a nearly balanced budget and

gross debt ratio of around 40 percent This

positions it to weather the current debt crisis

much better than the highly indebted majority

of industrialized western countries

Following the meteoric upswing of recent

quarters we expect economic growth to con-

tinue at robust albeit lower levels Growth will

be supported by continued immigration a glo-

bal economic upturn and the Swiss National

Bankrsquos very expansive monetary policy Specifi -

cally we expect the economy to grow 23 per-

cent in 2011 and 21 percent in 2012 This is

signifi cantly higher than the average growth

rate of 17 percent over the last 30 years Due

to the strong franc domestic consumption will

probably drive growth instead of exports as in

the precrisis years

Economic growth fuels demand for

real estate

International studies have found that the in-

come elasticity of housing demand is slightly

below 1 In other words a 1 percent increase

in income leads to an increase in housing

spending of slightly less than 1 percent The

expected growth rates which are relatively

high in historical comparison should lead to

a correspondingly high increase in housing

spending While this spending will most likely

fuel the construction of new housing it

should also drive up the prices of existing resi-

dential properties due to the scarcity of land

in Switzerland Prices for commercial real es-

tate should also benefi t from the strong do-

mestic economy

114112

108110

102100

104106

9698

2008 2009 20102005 2006 2007

Strong Swiss economy

Sources Reuters EcoWin UBS WMR

Inflation-adjusted GDP 1st quarter 2005 = 100

SwitzerlandGermany

SpainFrance

United Kingdom USItaly

Caesar Lack

Wealth Management Research

UBS AG

UBS real estate focus January 2011 7

Market drivers

2008 2009 2010 20112002 2003 2004 2005 2006 2007

Historically low interest rates about to end

Sources Bloomberg UBS WMR

Historical and projected interest rates in percent

4540

3035

1510

2025

005

Money market rates (Libor 3-m)5-year interest rates (swap)

10-year interest rates (swap)

Forecast

Interest rates in Switzerland are extremely

low right now We expect this to change in

2011 The domestic economyrsquos robust

growth expected rise in infl ation and nec-

essary tightening of monetary policy all

point to higher interest rates

Imports account for over one quarter of the

basket of goods used to track consumer price

infl ation ndash petroleum products alone make up

almost 5 percent The strong franc has fueled

import price defl ation in recent months which

has dragged year-on-year infl ation below 05

percent as measured by the national consumer

price index Since we do not expect the franc

to appreciate further we think exchange rates

should gradually lose their defl ationary power

this year Commodity prices have also risen

sharply in recent months together with the

elimination of the exchange rate eff ect this

should drive up import prices during the year

The persistent strength of the domestic econo-

my should also drive up the prices of domestic

goods We expect infl ation to reach almost

1 percent in 2011 and to trend towards

2 percent in 2012

SNB to make interest rate move in fi rst

half-year

UBS Economic Research Switzerland forecasts

higher infl ation than the Swiss National Bank

(SNB) The SNB surprisingly lowered its infl ation

forecast in its monetary policy assessment of

September 2010 and confi rmed its low infl a-

tion forecast in its monetary policy assessment

of December 2010 We expect the SNB to raise

its infl ation forecast again and possibly hike

interest rates 025 percent in the fi rst half of

the year to prevent the domestic economy and

real estate markets from overheating

Swiss Confederation bonds are benefi ting from

their status as an international safe haven

Europersquos debt crisis and loose monetary policy

worldwide have driven investors into Swiss

government bonds and pushed yields down to

levels not seen since 1965

We believe however that investors should

prepare themselves for rising interest rates and

bond yields in the medium term The economic

recovery should continue and loose monetary

policy should tighten up during the year Bond

markets usually preempt monetary tightening

and raise yields in advance Overall higher in-

terest rates will probably be introduced gradu-

ally and we expect interest rates to remain

historically low this year

Financing terms remain attractive

Real estate fi nancing will remain inexpensive

for now which will support real estate prices

The mortgage reference interest rate used to

calculate residential rents will rise marginally

but not until the second half of the year Rent

increases on commercial properties will also be

limited They are generally tied to infl ation

which is currently low

Infl ation and interest rates

Achim Peijan

Wealth Management Research

UBS AG

Caesar Lack

Wealth Management Research

UBS AG

UBS real estate focus January 20118

Market drivers

Population growth has been above aver-

age in recent years fueled mainly by an

exceptionally high infl ux of immigrants

Employment has remained surprisingly

robust since the 2009 recession The

fi nancial crisis has barely le a mark on

the tertiary sector

Switzerlandrsquos population has grown vigor-

ously for the 33rd year in a row Our extra-

polation based on provisional monthly data

provided by the Federal Statistical Offi ce pre-

dicts growth of 11 percent in 2010 Over the

last 40 years Switzerland has only seen pop-

ulation growth exceed 1 percent seven times

ndash including four out of the last four years

The free movement of persons from the EU-

17 and EFTA member states instituted in

June 2007 has obviously le its mark This

fi nding is borne out by a detailed analysis

of net migration While net migration (in-

cluding status changes) accounted for about

50 percent of population growth in the

1980s and 1990s it has recently contributed

80 percent and more (2007 91 percent) The

cantons of Vaud Obwalden Fribourg Ge-

neva Aargau and Zurich likely experienced

above-average growth in 2010 Given the

positive economic prospects overall we ex-

pect the population to grow around 1 per-

cent again in 2011

Employment also growing

Employment has also grown in recent years In

terms of full-time equivalents (FTEs) employ-

ment climbed a record-breaking 84 percent

during the 2005ndash2008 boom period In 2009

however total employment became sluggish for

several quarters The slowdown was largely con-

centrated in manufacturing although employ-

ment numbers went up again slightly in the third

quarter of 2010 This has also brightened senti-

ment in the secondary sector The service sector

by contrast recorded overall growth of 07 per-

cent even in the depths of the 2009 recession

The commercial real estate market is mainly af-

fected by the offi ce and retail sectors In the fi rst

three quarters of 2010 the offi ce sector saw a

negligible 02 percent year-on-year increase in

employment Retail employment also managed

to grow during this period ndash by 12 percent

Thus retail more than compensated for the prior

yearrsquos drop in employment

Housing demand remains strong

Continued population growth should keep hous-

ing demand strong Prices will only so en ndash espe-

cially for privately owned homes ndash if residential

construction steps up In the commercial real

estate market demand for retail space is show-

ing signs of improvement Demand for offi ce

space by contrast will most likely be driven by

space optimization

Claudio Saputelli

Wealth Management Research

UBS AG

Population and employment

Overview of property market drivers

Unless otherwise indicated all fi gures refer to percentage growth over the previous year

Business cycle and income 20111 20102 2009 2008 10 yrs3

Real gross domestic product 23 27 ndash19 19 17

Real construction investment 13 34 30 00 11

Real wage growth 07 04 26 ndash04 07

Infl ation and interest rates

Average annual infl ation 09 07 ndash05 24 09

3-month Libor CHF4 12 02 03 07 10

Yield on 10-yr Swiss Federal bonds4 24 18 19 21 25

Population and employment

Population 11 11 11 14 09

Employment in FTE 12 07 ndash01 27 10

Unemployment rate 34 39 37 26 32

1 Forecast UBS WMR Sources Seco BFS UBS WMR2 Forecast or extrapolations from UBS WMR (as of January 3 2011)3 Average 2001 to 20104 Year-end

Residential real estate

The Swiss property market is not overheated overall but vigilance is still warranted

UBS real estate focus January 201110

Homes ndash elevated threat level

Home prices continue to soar This up-

ward trend has not fl attened out as ex-

pected in previous quarters The public is

increasingly worried about a real estate

bubble ndash with some justifi cation Caution

is advised

Meteorological language is o en razor-sharp

Fog is ldquodenserdquo when visibility is less than a

quarter of a mile Gentle rain is a ldquodrizzlerdquo if

the water droplets have diameters between

02 and 05 millimeters The sky is ldquoovercastrdquo

if clouds cover over nine-tenths of it but only

ldquocloudyrdquo if they cover seven-tenths No won-

der economists o en envy meteorology for its

crisp terminology Their fi eld is much fuzzier

For example no economist can identify the

exact criteria that defi ne a real estate bubble

Experts agree that real estate is somehow

heavily overvalued in a bubble but cannot say

how much or how long prices have to in-

crease before a hot market becomes a full-

blown bubble

Real estate bubbles are usually followed by a

rapid dramatic fall in prices Not even this

criterion though provides a tangible defi ni-

tion of a real estate bubble Because bubbles

are not governed by any quantifi able criteria

the public and even experts are far too quick

to label many buoyant markets ldquobubblesrdquo

This has been happening in Switzerland since

early last year a er a recent steep spike in

home prices Letrsquos consider the facts The

Swiss property market began its rise in 1998

Condominium prices have climbed 56 percent

since then while single-family home prices

have gained 37 percent according to the

Wuumlest amp Partner indexes Is this sustainable

To fi nd out economists compare home prices

to three factors rents infl ation and income

Condominiums less aff ordable

Rental apartments are valid substitutes for

houses thanks to Switzerlandrsquos mature body

of landlord-tenant law so excessive discrep-

ancies between the two price trends can indi-

cate market imbalances In the past 12 years

rents rose by roughly the same percentage as

prices for single-family houses The diver-

gence though visible was insignifi cant given

the period of time and diff erences in quality

Rental apartments tend to be older lower-

cost properties while the interior quality of

condominiums has recently improved dramati-

cally As for the infl ation comparison count-

less international studies have shown that

infl ation-adjusted property prices are stagnant

over the long term This was certainly the case

in the Swiss house market between 1970 and

2000

Real estate prices have signifi cantly outpaced

infl ation since 2000 though leaving a worry-

ing gap between the two curves Theoreti-

cally the maximum potential drop in home

prices is the current diff erence between the

curves 33 percent for condominiums and

26 percent for single-family houses Another

well-regarded economic approach by con-

trast links the long-term home price trend to

disposable household income This is called

ldquohousing aff ordabilityrdquo If real estate prices

rise faster than disposable income this ap-

proach says that homes are less aff ordable for

households Demand weakens and prices fall

Average disposable income in Switzerland has

risen by roughly 35 percent since 1998 So

while the aff ordability of single-family houses

in Switzerland has remained more or less

steady during this period it has fallen consid-

erably for condominiums

Large regional discrepancies

This fi nding only applies to Switzerland as a

whole but local real estate markets vary

widely Average annual increases in condo-

Residential real estate

300

250275

175150

200225

100125

98 04 06 080200 1080 82 84 86 88 90 92 94 96

House prices not overheated overall

Sources BFS Wuumlest amp Partner UBS WMR

House prices compared to rent and disposable income (1980 = 100)

Consumer pricesHouse prices Zurich reg

House prices SwitzerlRental apt Switzerland

House prices Lake GenevaDisposable income

Claudio Saputelli

Wealth Management Research

UBS AG

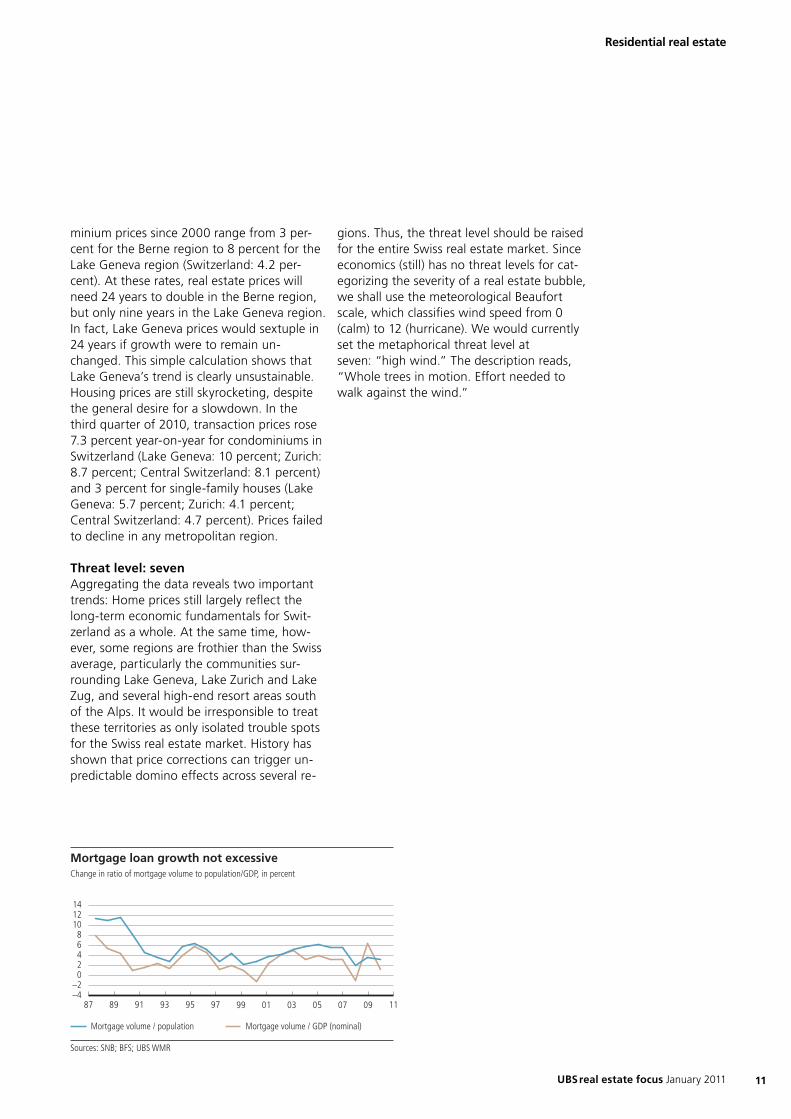

UBS real estate focus January 2011 11

minium prices since 2000 range from 3 per-

cent for the Berne region to 8 percent for the

Lake Geneva region (Switzerland 42 per-

cent) At these rates real estate prices will

need 24 years to double in the Berne region

but only nine years in the Lake Geneva region

In fact Lake Geneva prices would sextuple in

24 years if growth were to remain un-

changed This simple calculation shows that

Lake Genevarsquos trend is clearly unsustainable

Housing prices are still skyrocketing despite

the general desire for a slowdown In the

third quarter of 2010 transaction prices rose

73 percent year-on-year for condominiums in

Switzerland (Lake Geneva 10 percent Zurich

87 percent Central Switzerland 81 percent)

and 3 percent for single-family houses (Lake

Geneva 57 percent Zurich 41 percent

Central Switzerland 47 percent) Prices failed

to decline in any metropolitan region

Threat level seven

Aggregating the data reveals two important

trends Home prices still largely refl ect the

long-term economic fundamentals for Swit-

zerland as a whole At the same time how-

ever some regions are frothier than the Swiss

average particularly the communities sur-

rounding Lake Geneva Lake Zurich and Lake

Zug and several high-end resort areas south

of the Alps It would be irresponsible to treat

these territories as only isolated trouble spots

for the Swiss real estate market History has

shown that price corrections can trigger un-

predictable domino eff ects across several re-

gions Thus the threat level should be raised

for the entire Swiss real estate market Since

economics (still) has no threat levels for cat-

egorizing the severity of a real estate bubble

we shall use the meteorological Beaufort

scale which classifi es wind speed from 0

(calm) to 12 (hurricane) We would currently

set the metaphorical threat level at

seven ldquohigh windrdquo The description reads

ldquoWhole trees in motion Eff ort needed to

walk against the windrdquo

Residential real estate

1412

810

20

46

ndash4ndash2

09 1187 89 91 93 95 97 99 01 03 05 07

Mortgage loan growth not excessive

Sources SNB BFS UBS WMR

Change in ratio of mortgage volume to populationGDP in percent

Mortgage volume population Mortgage volume GDP (nominal)

UBS real estate focus January 201112

The rental apartment market is stable

and harbors upside potential Prices for

multi-family dwellings have made com-

mercial properties increasingly attractive

to investors

The cooler economy and slightly lower immi-

gration had no notable impact on overall

housing demand The number of apartments

under construction in Switzerland tapered off

marginally during the recession but has not

reached a turning point by any means Low

interest rates also supported construction in

2010 Over 70000 apartments were under

construction at the end of the third quarter of

2010 This is a record and almost 12 percent

higher than in 2009 The number of building

permits indicated that construction activity

will drop slightly in 2011 Given the recent

improvements in the economic environment

no signifi cant increase in vacancy rates is ex-

pected Switzerland has the lowest vacancy

rate in Europe at 09 percent

Scarcity drives rent increases

Low vacancy rates in urban areas have sup-

ported the growth in rents Switzerland as

a whole saw rents increase by an average of

2 percent in the fi rst three quarters of 2010

although performance varied widely between

regions Near Lake Geneva nominal rents

rose nearly 7 percent those in southern Swit-

zerland went up around 31 percent In other

major regions rents only increased by 08 to

16 percent during the same period Rents will

probably increase further given the economic

environment but each region should always

be analyzed separately Despite continued

construction in Zurich demographic trends

should soak up the additional supply A swell-

ing population in the Geneva region is facing

a very scarce supply which is driving up rents

More rural regions such as the Jura and parts

of Central Switzerland will see rents fall

Careful analysis of investments

Yield-seeking investors have buoyed invest-

ment demand Many have focused on rental

apartments and thus have raised prices for

existing multi-family dwellings While the rent-

al apartment market does not appear over-

heated among professional investors we still

recommend carefully analyzing prospective

investments We expect this yearrsquos overall

appreciation return on multi-family dwellings

to remain on par with prior years Since the

economy is expected to improve we assume

rising rents will push up commercial property

valuations This could enable commercial real

estate to outperform multi-family dwellings

in 2012

Rental apartments ndash steady returns

Gunnar Herm

Global Asset Management

UBS AG

Residential real estate

Overview of residential properties

Unless otherwise indicated all fi gures refer to percentage growth over the previous year

Residential construction and vacancies 20111 20102 2009 2008 10 yrs3

Net increase in number of homes 45 000 42 000 38 977 44 717 38 255

Residential vacancy rate 10 09 09 10 10

Rental apartments

Asking prices for rental apartments 15 17 35 42 31

Asking prices for new rental apartments ndash15 ndash12 ndash45 15 38

Price index for passing rents 10 11 24 25 17

Mortgage reference interest rate 5 30 28 30 35 ndash

Number of vacant rental apartments 31 000 28 947 26 343 28 138 29 567

Performance on residential direct investment 50 50 53 61 564

Owner-occupied homes

Asking prices for condominiums 30 49 64 41 42

Closing prices for condominiums 25 59 33 47 44

Asking prices for single-family homes 25 47 50 27 30

Closing prices for single-family homes 15 23 04 38 27

Variable mortgage interest rate all banks 5 30 27 27 28 33

Growth in mortgage loans all banks 45 51 49 34 41

Number of vacant condominiums 8 000 7 766 8 418 8 980 7 9381 Forecast UBS WMR Sources Wuumlest amp Partner BFS SNB IPD UBS WMR2 Forecast or extrapolations from UBS WMR (as of January 3 2011)3 Average 2001 to 20104 Average 2006 to 20105 Year-end

UBS real estate focus January 2011 13

Imputed rental values ndash a violation of classic tax theory

The taxation of imputed rental values as

income is controversial For years there

have been heated discussions about this

issue Last summer the Federal Council

threw its hat in the ring supporting a

total abolition of the tax in order to sim-

plify the tax code

In January 2009 the Swiss Homeownersrsquo As-

sociation (HEV Schweiz) launched a popular ini-

tiative titled ldquoLiving Securely in Old Agerdquo The

Federal Council rejected the initiative and now

aims to abolish the tax on imputed rental val-

ues (IRV) by instituting an indirect counterpro-

posal In exchange it will eliminate tax deduc-

tions on private interest payments with certain

exceptions Maintenance costs will no longer

be tax-deductible either except for high-quali-

ty energy effi ciency and environmental protec-

tion measures

Root of the problem taxing imputed

rental values

Interestingly the endless debate about IRV

taxes always links IRV to mortgage interest and

other tax-deductible expenses They are treat-

ed as parts of one indivisible system However

we can best evaluate the systemrsquos macroeco-

nomic eff ects by examining each component

separately Letrsquos begin with IRV It represents

the rent revenues that homeowners could the-

oretically earn if they rented out their home on

the open market It is taxed as a form of invest-

ment income This IRV tax allegedly puts ten-

ants and homeowners on an equal footing on

the premise that homeowners are better off

economically since they live rent-free

This is a specious argument in our view First

tenants unlike homeowners bear no invest-

ment risk for their home and no opportunity

costs for their assets (profi ts not earned on

assets tied up in real estate) Second the gov-

ernment greatly benefi ts from homeownersrsquo

risk-taking when properties are sold ndash it levies

a he y property gains tax on any capital gains

Losses by contrast are fully borne by the

property seller Third the IRV tax does a poor

job of evening the odds between tenants and

homeowners Simply consider how IRV are

determined There are few comparable proper-

ties particularly for single-family homes and

luxury properties making it diffi cult or impos-

sible to calculate the market rents that underlie

the IRV Finally the cantons use diff erent and

sometimes quite complicated assessment

methods to calculate IRV This violates classic

tax theoryrsquos maxim that tax laws should be

both simple and transparent

Mortgage interest deduction ndash the other

side of the coin

What about the fl ip side of the home tax sys-

tem the deductions for mortgage interest and

maintenance expenses As the law stands the

tax on IRV automatically allows homeowners

to claim these deductions as ldquoprofessional ex-

pensesrdquo If IRV taxes were revoked the govern-

ment could be more pragmatic about mort-

gage interest There are three main reasons

why deductions for owner-occupied homes

should be eliminated in our opinion as the

Federal Council is essentially proposing to do

First the deductions give households an incen-

tive to take on too much debt While this is not

necessarily bad in itself it is still not something

the government should be expressly encourag-

ing Second allowing income tax deductions

for debt interest pushes part of the home buy-

errsquos interest rate risk onto the government and

thus the taxpayer As interest rates rise home-

owners can claim larger interest deductions

thereby reducing their tax bills Tenants by

contrast bear the full interest rate risk under

current tenant-landlord law through the refer-

ence mortgage interest rate Third it is unfair

to permit homeowners to claim deductions for

Current system for taxing home ownership is complicated

Source UBS WMR

Impact of home ownership on income tax

Taxable income WITHOUT home ownership

Taxable income WITH home ownership

+ Imputed rental valuendash Maintenance costsndash Mortgage interest

Current system of taxes on home ownership

In focus Residential real estate

Claudio Saputelli

Analyst UBS AG

Claudio Saputelli

Wealth Management Research

UBS AG

UBS real estate focus January 201114

The leverage formula is decisive

Whenever taxes on home ownership change homeowners wonder

whether they should pay down their mortgages To answer this ques-

tion it helps to consider the leverage formula (use of debt to improve

return on equity) If the return on a long-term investment exceeds the

current mortgage rate it makes more sense to put money in long-term

investments than in extra mortgage payments If mortgage rates ex-

ceed long-term returns however it might be better to pay down the

mortgage If mortgage rates and long-term investment returns are

equal homeowners cannot improve their fi nancial situation by tweak-

ing mortgage payments Besides determining the ideal debt level we

strongly recommend diversifying Homeowners should not put all their

eggs in one basket but rather assemble a widely diversifi ed portfolio

Given the low correlation between direct real estate investments and

other asset classes portfolio construction theory recommends not

concentrating all your assets in your home

living expenses when tenants cannot deduct a

single cent

Dubious exceptions from interest

deductions

The Federal Council is hoping to satisfy its

constitutional mandate to encourage home

ownership by permitting fi rst-time home buy-

ers to claim mortgage interest deductions up

to a certain franc limit over 10 years This

ldquofi rst-time buyer deductionrdquo would also ben-

efi t high-income households which obviously

misses the point and should therefore be re-

considered Under the Federal Councilrsquos indi-

rect counterproposal taxpayers with interest

income could still off set mortgage interest

against the full amount of their interest in-

come This is also a one-sided policy that large-

ly benefi ts homeowners who can deduct mort-

gage interest from their taxable interest and

securities income

The indirect counterproposal will eliminate in-

come tax deductions for maintenance costs as

well as private mortgage interest This is a step

in the right direction A er all tenants do not

receive tax breaks on their living expenses

However the Federal Council is making excep-

tions to allow deductions on energy effi ciency

and environmental protection measures that

meet specifi c energy criteria It would be very

labor-intensive and therefore expensive to reg-

ularly defi ne and review eligible measures for

each individual homeowner A more effi cient

method would directly subsidize eco-friendly

energy systems and construction materials

The tax on imputed rental values

should be abolished

The current tax on IRV makes little economic

sense in our view If it were abolished there

would be no need for many deductions and

exceptions which is why we think the govern-

ment should simplify the tax code by com-

pletely eliminating this tax on home ownership

That way homeowners can preserve both their

homes and their sanity around tax time

In focus Residential real estate

UBS real estate focus January 2011 15

Occupational pension withdrawals ndash a dangerous game

An estimated 520000 withdrawals have

been made from retirement accounts since

1995 The withdrawn capital is expected

to exceed 35 billion Swiss francs in 2010

The possible impact on future retirement

benefi ts remains unknown but the risks

should not be ignored

The ldquoDispatch on the Encouragement of

Home Ownership with Occupational Retire-

ment Assetsrdquo was published in the August

1992 Federal Gazette It states ldquoThe home

ownership rate in Switzerland is extremely

low compared to other countries Raising it is

an urgent national and social priorityrdquo Also

policymakers tended to oversimplify the mat-

ter when they claimed the low home owner-

ship rate showed too little was being done to

reach the political goal of widespread home

ownership among the population

Swiss home ownership rate remains low

The home ownership rate was 31 percent in

1990 By 2000 fi ve years a er a home own-

ership encouragement law began to allow

prospective home buyers to pledge and with-

draw pension assets 346 percent of all per-

manently occupied homes were owner-occu-

pied The Swiss Federal Housing Offi ce now

puts the home ownership rate at 39 percent

In Germany the rate is 42 percent compared

to 57 percent in France and 70 percent in

Italy

Why the low ownership rate First condo-

minium ownership was not introduced to

Switzerland until 1965 Second the Swiss

rental apartment market is relatively effi cient

compared to other countries which dulls the

incentive to own a home So what caused

the spike in the home ownership rate in the

1990s In that decade home prices fell a er

the real estate bubble burst declining sharply

relative to national income Third Switzer-

landrsquos ldquobaby boomersrdquo are now 40 and older

ndash the cohort where home ownership is most

common Finally people have been free to

pledge or withdraw occupational pension as-

sets for home purchases since 1995 However

it is not clear whether this statutory option

has acted as a genuine incentive or only had a

bandwagon eff ect

Occupational pensions unsuitable for

encouraging home ownership

The explicit goal of the occupational pension

system ndash established in 1985 to supplement

the old age and survivorsrsquo pension system

(AHV) ndash is to maintain a certain standard of

living when the policyholder retires dies or

becomes disabled As fully funded schemes

occupational pensions represent the most

politically attractive pot of money for encour-

aging home ownership Withdrawing pension

assets however does more than reduce

future retirement benefi ts It can also lower

death and disability benefi ts if they depend

on the amount of built-up capital (defi ned

contribution plan) Thus pension withdrawals

are a poor vehicle for encouraging home

ownership since they clearly undermine the

main purpose of occupational pensions to

provide an annuity or lump-sum payout in

retirement age

The ldquoDispatch on the Encouragement of

Home Ownershiprdquo shrugs off doubts as

follows ldquoEncouraging home ownership serves

the purpose of occupational pensions because

living expenses represent one of the largest

costs for retireesrdquo But this claim rings hollow

It ignores the need to distribute investment

risks and choose assets that off er security and

an adequate return ndash as stipulated by the Fed-

eral Act on Occupational Pensions People

who withdraw pension assets are fully ex-

Thomas Veraguth

Wealth Management Research

UBS AG

In focus Residential real estate

350040004500

3000

15001000

20002500

0500

4500040000

3000035000

1500010000

2000025000

05000

0995 96 97 98 99 00 01 02 03 04 05 06 07 08

Pension withdrawals relatively constant since 2003

Sources EDI ESTV UBS WMR

Total amount and number of withdrawals per year since 1995

Number of annual withdrawals (right-hand scale)

Total annual amount in CHF million

UBS real estate focus January 201116

posed to the one-sided non-diversifi able and

considerable risks of the real estate market for

years at a time

Total sum withdrawn remains low

The statistics tell a nuanced story of how

withdrawals are being used to fi nance home

purchases The capital invested in occupatio n-

al pension schemes has nearly doubled since

1995 reaching 600 billion Swiss francs in

2009 The total increase was almost 290 bil-

lion francs which dwarfs the 35 billion francs

withdrawn between 1995 and 2009 This rep-

resents just 12 percent of the capital growth in

occupational pension schemes over the past

15 years On average annual withdrawals ac-

count for around 05 percent of the total capi-

tal invested in occupational pensions By com-

parison Wuumlest amp Partner estimates that all the

single-family homes and condominiums in

Switzerland had an aggregate market value of

124 trillion Swiss francs in 2010 Mortgages

taken out by private households amounted to

566 billion francs in September 2010

The withdrawal statistics also harbor another

surprise the continuity of the amounts with-

drawn The average withdrawal has remained

within a tight corridor of 60000 to 73000

Swiss francs since 1995 The average peaked

in 2003 at 73160 francs This is not an exces-

sive amount A typical Swiss home sells for

680000 francs In 1995 withdrawals ac-

counted for 6 percent of all expenses incurred

by Swiss occupational pensions consisting of

annuities and lump-sum payments and 167

percent of all the schemesrsquo lump-sum and

cash payments The 2009 percentages were

roughly 6 and 22 percent respectively

Moderation is key

From an economic perspective certain poten-

tial problems arise from the legislaturersquos deci-

sion to allow consumers to make early pen-

sion withdrawals for home purchases Luckily

consumers have exercised considerable self-

restraint as indicated by the data on the

number of withdrawals and total money with-

drawn per year Less than 1 percent of all

members of occupational pension schemes

make withdrawals each year This is in part

due to restrictions inserted in the legislation

by lawmakers such as a tax on withdrawals

As a result we are cautiously optimistic about

the future of home fi nancing but recommend

pledges over withdrawals

In focus Residential real estate

Weighing the pros and cons of withdrawals

Pension withdrawals have been allowed for home purchases since

1995 Home ownership is conventionally viewed as a sound way to

prepare for retirement The reality is diff erent in our view Homes

make unattractive alternatives to capital investment given their op-

portunity costs and loss in value due to aging Pension assets are

nonetheless used in up to one fi h of all purchases of existing proper-

ties and one third of new ones Withdrawals are particularly common

for ldquothreshold householdsrdquo (low income low savings rate) However

there are no current offi cial impact analyses In 2004 written surveys

by Hornung revealed that withdrawals play an important role Never-

theless the question remains open as to whether less affl uent employ-

ees are cutting their future benefi ts too heavily by purchasing a home

Impact analyses used to be the responsibility of the Federal Offi ce of

Social Insurance under Article 18 of the Home Ownership Encourage-

ment Ordinance ndash until this Article was abolished on 22 August 2007

For these reasons the pros and cons of a withdrawal must be weighed

carefully when purchasing a home

UBS real estate focus January 2011 17

Full-service living ndash a hot new trend

Full-service living is an innovative concept

that caters to urban residentsrsquo demand for

greater comfort and higher living stand-

ards Already established abroad this

model is fast gaining adherents in Swit-

zerland

Greater prosperity and a steadily growing

number of small households are driving demand

for new models of living with integrated ser-

vices This trend extends beyond wealthy te-

nants and senior citizens The upper middle

class including many ldquoDINKsrdquo ndash double income

no kids ndash is less willing to spend precious free

time on tedious errands or exhausting chores

Even young families are increasingly discovering

the modelrsquos benefi ts

Growing importance of new models

of living

Living models have adapted to peoplersquos chang-

ing needs Over the years we have seen the

emergence of nursing homes independent liv-

ing and assisted-living communities There is

now an even richer more diverse menu of

options ranging from boarding houses to full-

service living While this latest model may re-

main a niche product for several years we think

demand will stay strong for the foreseeable

future thanks to demographic change growing

interest in support and services and a greater

overall need for higher living standards Of-

ferings need to be aligned with target group

needs and interests though Our experience

with the ldquoJames ndash Full-service Livingrdquo project

shows that models should be tailored to both

the target group and local conditions

James ndash Full-service Living

The James ndash Full-service Living concept is the

brainchild of our real estate fund UBS (CH) Prop-

erty Fund ndash Swiss Mixed ldquoSimardquo In 2007 the

fund opened the fi rst James apartment complex

in Zurich with around 280 apartments In 2009

the UBS Foundation for the Investment of Pen-

sion Fund Assets built a second James complex

in Lausanne tailored to the local area Thirty-

four of the 114 apartments were designed spe-

cifi cally for older or disabled residents The third

James complex is under construction in Winter-

thur and will open its doors to tenants in mid-

2011 It conveniently combines living and shop-

ping thanks to a direct connection between the

roughly 150 apartments and a shopping center

restaurants and a parking garage

The James ndash Full-service Living concept refl ects

todayrsquos needs and lifestyles It embraces not

only modern communication technologies (In-

ternet e-mail) but also direct personal interac-

tion (James is physically on the premises) At a

James complex rent includes a wide array of

concierge services such as receiving guests

accepting packages and purchases or reserving

concert tickets or tables at restaurants Not to

mention a broad selection of agrave la carte services

such as laundry service apartment cleaning pet

care plant watering or vacation service These

services are billed separately under a pay-as-

you-go scheme

Components of full-service living

Home concierge services are new to Switzer-

land ldquoConciergerdquo is a French word that origi-

nally described the castle gatekeeper Today it

mainly designates French superintendents or

caretakers of residential buildings But ldquocon-

cierge servicerdquo increasingly refers to comprehen-

sive personal services for tenants and visitors as

well The word is commonly used in luxury ho-

tels where a conciergersquos duties extend far be-

yond receiving guests Concierges are complete-

ly at the disposal of a discerning clientele The

James concept embraces this principle When

tenants and visitors enter a James apartment

complex it should be readily apparent that this

is more than just a place to live The James ndash

Full-service Living concept can also adapt to

Patric Caillat

Global Asset Management

UBS AG

Possible concept for full-service living

Source UBS GRE Switzerland

The three components of ldquoJames ndash Full-service Livingrdquo

Living as a core service

Basic services included in rent

Agrave la carte services

In focus Residential real estate

UBS real estate focus January 201118

residentsrsquo new and changing needs over time

thanks to its extensive modular service off ering

The program is based on three components

residential use integrated basic services and

additional agrave la carte services

The apartment is the core service and as such

must perfectly satisfy tenantsrsquo requirements in

terms of location infrastructure amenities and

aesthetics The rent must also include several

basic services that are important to the target

groups This diff erentiates James from a regular

apartment complex Residents can also use

many diff erent agrave la carte services They simply

pick the services they need and pay for them

separately which makes the apartment some-

thing like a hotel To be successful the concept

has to combine these elements intelligently

while taking local circumstances into account

Other models on the market

Several models with slightly diff erent approach-

es have been launched in recent years Besides

James ndash Full-service Living from UBS Global As-

set Management other full-service models in-

clude ldquoLiving Servicesrdquo from Credit Suissersquos Real

Estate Asset Management department and

ldquoBonacasardquo from Bracher und Partner AG

Combining services with attractive living can

give a property its own unique character and

ensure its long-term appeal This fact helps

support intelligent real estate marketing How-

ever full-service living can only work if the

services benefi t users operators and owners

alike While Switzerland has no long-term ex-

perience with such models it certainly has the

conditions and outlook needed to achieve a

win-win situation

Added value at an attractive price

ldquoFull-service livingrdquo seems to be a growing demand For it to work

users and operators will have to answer a crucial question ldquoWhat

value do the services providerdquo They should off er tangible benefi ts to

tenants And they should pay off for the landlord or operator A er

all they are not provided for free in any model Either they are in-

cluded in the rent or they are charged according to a pay-as-you-go

scheme Several key questions have to be answered from the start

Who is the target audience What services do they want While this

might seem trivial at fi rst glance experience shows that the venturersquos

success or failure depends on precisely these issues and how they are

handled in practice Over the long term full-service living concepts

will only succeed if they provide tenants with added value at an at-

tractive price The program must also be able to adapt to residentsrsquo

changing needs

In focus Residential real estate

Commercial real estate and special uses

The market separates the wheat from the chaff

UBS real estate focus January 201120

Offi ce properties ndash separating the wheat from the chaff

The Swiss offi ce property market came

through the global economic crisis in rela-

tively good shape We expect price pres-

sure from tenants to widen the perform-

ance gap between central and peripheral

locations

Offi ce space is the most important sector of

the Swiss commercial real estate market The

commercial property market was estimated

to be worth 68 billion Swiss francs at the end

of 2009 according to Investment Property

Databank (IPD) Some 588 percent of this

total was offi ce space while retail properties

made up 377 percent and industrial real es-

tate 35 percent

Stable demand factors

Besides being large the offi ce property seg-

ment also refl ects Switzerlandrsquos federal struc-

ture even though 17 and 10 percent of the

total offi ce space lies in the fi nancial centers of

Zurich and Geneva respectively Financial and

business services represent over 18 percent of

total employment in Switzerland ndash a high per-

centage compared to other countries The

Swiss fi nancial industry unlike its peers else-

where exited the global fi nancial crisis rela-

tively unscathed While the EUrsquos fi nancial sec-

tor shed jobs at a rapid rate Switzerlandrsquos

growth rate merely slackened in 2009 but still

remained positive Part-time employment is

also becoming more widespread in Switzer-

land As elsewhere in Europe Swiss companies

are focusing on boosting employee productiv-

ity Future employment growth looks likely to

be moderate as a result

Rising importance of quality

The prospect of slow but positive employment

growth highlights the importance of analyzing

the supply of offi ce space Offi ce vacancy rates

range from 2 to 6 percent in Swiss cities This is

moderate compared to other countries and has

recently fueled growth in offi ce rental rates In

crisis-stricken 2009 for example IPD found

that Swiss offi ce rents rose 1 percent Offi ce

completions have been much higher in Ger-

man-speaking Switzerland than western Swit-

zerland in recent years In 201112 around

150000 msup2 of new offi ce space will enter the

market in Zurich compared to only 60000 msup2

in Geneva It is important to diff erentiate the

various kinds of offi ce space on the market For

example we are skeptical about the medium-

term prospects of non-integrated offi ce prop-

erties (poor access to transportation and low

availability of services) on the periphery of cit-

ies and urban agglomerations given the bur-

geoning interest in environmental sustainabil-

ity Even if immigration infl ows continue to be

strong expanding the labor market companies

still need to provide attractive workplaces for

their employees Easily accessible central offi ce

locations will gain even more importance Un-

der these pressures the offi ce market should

start to more clearly separate the wheat from

the chaff Downtown locations where offi ce

space is scarce should perform well while

non-integrated offi ce properties will struggle

to attract tenants Rents for these peripheral

locations will be squeezed since they are main-

ly used for extremely cost-sensitive back-offi ce

functions Through renovation or new con-

structions in contrast downtown locations

should see further appreciation and attractive

returns For this reason we think rents for

high-end offi ce space should rise further

Positive appreciation rate

Despite falling interest rates and government

bond yields initial yields in the institutional

offi ce segment have hardly budged according

to IPD They were 58 percent in 2008 and

2009 In contrast to many European real estate

markets the appreciation rate is still positively

Commercial real estate and special uses

5

34

0ndash1

12

ndash3ndash2

2008 2009 2010 2011 20122003 2004 2005 2006 2007

Forecast

No drop in employment in Switzerland

Source Experian Business Services June 2010

Employment growth in financial and business services in percent

SwitzerlandEU15

Gunnar Herm

Global Asset Management

UBS AG

UBS real estate focus January 2011 21

correlated with the rental growth rate in the

Swiss offi ce property market The percentage

increase in the granting of commercial mort-

gages has not exceeded the Swiss infl ation

rate either Both these factors mean the Swiss

commercial property market is on solid ground

The fall in government bond yields has height-

ened the relative appeal of commercial proper-

ties driving investment demand for this asset

class Nevertheless for 2011 we recommend

that offi ce real estate investors review carefully

the riskreturn profi le for each property and

refuse to compromise on their investment cri-

teria Most buyers are using their own funds at

present and can easily tap capital markets for

their debt fi nancing needs Unlike in previous

years few highly geared investors are active in

the Swiss property market

The Swiss National Bank has refrained from

interest rate hikes even though the Swiss

economy emerged hale and hearty from the

global crisis and is helping to drive European

economic growth Rising interest rates would

not however automatically trigger property

devaluation in the commercial institutional

real estate market Interest rates also refl ect

prevailing economic growth Fast growth

tends to raise rent revenues and thus prop-

erty valuations While this is not necessarily

an automatic reaction investors with proper-

ties in sustainable locations should not worry

if interest rates rise from the current historic

lows

Stable performance expected

Overall we expect the Swiss offi ce property

market to deliver steady performance in 2011

driven by stable returns while property values

should appreciate only modestly Appreciation

rates are based on expected rental growth due

to an improving economic environment and

not on speculative changes in appreciation

returns As such the Swiss offi ce property

market refl ects the countryrsquos sound economic

fundamentals

Commercial real estate and special uses

8

4

6

0

2

ndash22008 2009 2010 20112003 2004 2005 2006 2007

Forecast

Slight potential for appreciation expected

Sources IPD UBS GREPast performance is no indication for future performance

Performance of Swiss office market pa

Net cash flow yieldAppreciation return

UBS real estate focus January 201122

Consumer confi dence is stronger in Swit-

zerland than in many other countries This

benefi ts retailers and real estate investors

alike but investment performance in-

creasingly hinges on property quality

While its consumers did not escape the global

economic crisis entirely unscathed the Swiss

retail sector seems relatively unfazed Infl a-

tion-adjusted retail revenues still rose by

around 05 percent in 2009 despite the cycli-

cal weakness compared with up to 43 per-

cent in the boom years Rising unemployment

fanned uncertainty in 2009 but unemploy-

ment started falling again in February 2010

and consumers regained confi dence This

should support retail revenue The retail sec-

tor is expected to see real revenue growth in

excess of 2 percent for 2010 and in the cur-

rent year

Concentration continues

Switzerlandrsquos robust purchasing power and

strong economic environment relative to its

European neighbors has encouraged many

foreign retailers to set up business here In the

fi rst stage of expansion they are focusing on

downtown shopping districts and prime shop-

ping centers This means lower-quality loca-

tions and shopping centers will have an uphill

battle Restoring competitiveness o en re-

quires costly extensive work The Swiss retail

property sector signifi cantly outperformed the

overall Swiss real estate market in 2009 log-

ging an overall rise of 63 percent Mean-

while rents increased by more than 3 percent

in 2009 and 2010 according to Wuumlest amp Part-

ner This is largely due to changing quality

diff erences between property categories

Performance diff erentiation

Property quality and location will become ever

more important to retailersrsquo siting decisions

and the success of retail property invest-

ments That is why we expect to see even

greater discrepancies in retail property per-

formance Construction has been proceeding

at a rapid pace in some regions recently and

older outdated shopping centers have been

renovated This has fueled competition for

tenants leaving little leeway for rent increases

in the retail market in 2011 The overall mar-

ket should thus see zero growth Only high-

end locations and well-managed properties

should rise above the fl at rental trend We

also expect property appreciation rates to

settle at between 1 and 2 percent in the

years ahead

Retail space ndash zero growth expected

Commercial real estate and special uses

Gunnar Herm

Global Asset Management

UBS AG

Overview of commercial properties

Unless otherwise indicated all fi gures refer to percentage growth over the previous year

Employment revenue and sentiment 20111 20102 2009 2008 10 yrs3

Employment offi ce in FTE 05 03 17 42 20

Employment retail in FTE 05 12 ndash09 18 03

Real retail revenue working day-adjusted 25 28 05 33 19

Consumer sentiment index average ndash ndash58 ndash333 ndash70 ndash88

Offi ce space

Asking rents for offi ce space 00 07 40 08 12

Vacancy rate for offi ce space 48 45 43 43 ndash

Net cash fl ow yield 49 49 49 48 484

Appreciation return 08 08 04 10 104

Performance on offi ce direct investment 57 57 53 59 584

Retail space

Asking rents for retail space 05 36 34 06 14

Net cash fl ow yield 49 48 48 50 494

Appreciation return 04 05 15 14 224

Performance on retail direct investment 53 53 63 65 714

1 Forecast UBS WMR Sources Wuumlest amp Partner Colliers IPD BFS Seco UBS WMR2 Forecast or extrapolations from UBS WMR (as of January 3 2011) 3 Average 2001 to 20104 Average 2006 to 2010

UBS real estate focus January 2011 23

Public-private partnership ndash more than a buzzword

Governments and companies have a long

history of collaboration However public-

private partners have to do more than just

work together They also need to defi ne

processes to structure their relationship

allocate risk award contracts and lay

down ground rules for the partnership

Operating maintaining and repairing a build-

ing over a 25- to 30-year period costs about as

much as constructing it in the fi rst place (ex-

cluding fi nance costs) Even a er accounting

for the time value of money only two thirds of

the total budget go toward the initial construc-

tion with one third consumed by operating

costs over 25 to 30 years Planning for any

construction project should thus consider the

subsequent operational phase This is one of

the strengths of public-private partnerships

(PPPs)

Originally conceived abroad by governments

seeking a way out of fi nancial predicaments

today one of the PPP modelrsquos major virtues is

the fact that bidders already have to consider

the operational phase when they make their

bids PPP does not do half-measures either

Besides addressing operating costs directly the

bidders are also free to design a building and

or infrastructure that minimizes operating

costs PPP thus integrates the buildingrsquos future

operator in the bidding consortium from the

start thereby improving long-term planning

design and construction

The tendering procedure is the key

The core of every PPP project is a contract be-

tween a public-sector entity and a project com-

pany with a clearly defi ned scope of services

The long contract terms (generally 20 to 30

years) show that PPPs cover the propertyrsquos en-

tire lifecycle not just construction and fi nance

Successful PPP projects utilize well-designed

tendering procedures that integrate planning

design construction fi nance and operation

into the bids and encourage competition for

each stage of the project

Some government clients hold architecture

competitions and then solicit bids from com-

panies to build and operate the property This

is not true PPP The problem Since the archi-

tecture has already been determined the

private service provider has little leeway to

optimize construction andor operation in its

proposal And so while planning and opera-

tion may be more effi cient these gains are

swallowed up by the companyrsquos higher fi nanc-

ing costs compared to its government client

The typical PPP tendering procedure can de-

liver signifi cant savings ndash for both the project

company and the public-sector client Numer-

ous analyses of PPP projects in neighboring

countries have documented effi ciency gains of

15 to 20 percent not to mention shorter build-

ing periods in many cases In Switzerland the

effi ciency gains for above-ground projects

should range from 5 to 10 percent

Higher fi nancing costs

a hollow counterargument

Critics of prefi nancing and outsourcing ser-

vices to private providers o en argue that

companies have higher fi nancing costs than

governments Unfortunately they ignore the

fundamental diff erences between the public

sectorrsquos risks in a PPP project as versus projects

where the building is constructed by govern-

Typical structure of a PPP project

Source UBS Real Estate Advisory

Contract

Construction Operationmaintenance

User fee

Public sectorClient

(ordering party)

Project companies(contractorsconcession holders)

User

Typical shareholdersndash Investors (funds etc)ndash Generaltotal contractors (GCTC)ndash Operators

Supervisory authority

Investorsbanks

PermitProject

financing

Generaltotal contractor(designbuild)

Operator(public private)

Project company as the contractor

Christian Unternaumlhrer

Wealth Management amp

Swiss Bank UBS AG

Niklaus Scheerer

In focus Commercial real estate and special uses

UBS real estate focus January 201124

ment entities In a PPP project the private

contractor assumes construction and opera-

tion risks while government construction

places some or all of these risks on the public

sectorrsquos shoulders

Low public-sector fi nancing costs ultimately

stem from taxpayersrsquo implicit guarantee Re-

course to debt guarantees from taxpayers is

hard to justify though especially when the

risks and services could easily be offl oaded to

the private sector Risk allocation becomes dis-

torted by a kind of circular logic The taxpayers

are essentially guaranteeing their own debts as

the indirect project initiators Since this struc-

ture ignores the eff ective project risk in all fi -

nancing deliberations capital allocation is fre-

quently suboptimal

PPP projects by contrast clearly identify and

quantify all visible project risks and allocate

them to whomever can best judge and bear

them The private sector provides the project

fi nance although the government client is still

able or required to furnish greater or lesser

guarantees If guarantees are furnished how-

ever they are tied to a risk event so that the

client can manage the risks properly

Many potential areas of application

PPP projects are ideal for building transporta-

tion infrastructure They have also proven

their value over the last ten years in health-

care education criminal justice and national

defense particularly outside of Switzerland

Within Switzerland PPP models will probably

play the largest role in hospital fi nancing in

the near future Indeed the hospital fi nancing

reform slated for early 2012 (see ldquoHospital

property market in upheavalrdquo on page 25)

was motivated by a desire to create a level

playing fi eld for public- and private-sector

operators of acute care hospitals Having gov-

ernments build and operate hospitals would

not have been conducive to achieving this

goal This does not mean however that the

public sector has pulled out of the hospital

sector Instead it should assume a new role

as envisioned by the PPP paradigm Public and

private partners have unlimited scope for cre-

ativity in determining how they will share the

work It is important though for work alloca-

tion arrangements to be clearly structured

and consistently implemented by both part-

ners from the beginning PPP is not a game of

ldquohot potatordquo between the public and private

sectors

Intelligent risk allocation with PPP

PPP models are a viable form of fi nancing projects in Switzerland as

illustrated by the canton of Bernersquos new Neumatt Administrative

Center in Burgdorf The government is receiving a new piece of infra-

structure that it probably could not have built and fi nanced itself ndash

and the project is on schedule and on budget Debt-to-equity ratios

vary in PPP projects depending on the area of application and risk

structure Ten to 20 percent of project costs is the standard equity

ratio for above-ground projects where the private partner bears little

to no market risk This low ratio ndash which is only possible thanks to

the clear risk allocation of PPP projects ndash can deliver an attractive

return on equity and also optimizes overall fi nancing costs And that

protects government coff ers Large real estate investors would do

well to familiarize themselves with PPP since Switzerland is expected

to see many PPP projects in the future It makes sense to learn as

much as possible early on

In focus Commercial real estate and special uses

UBS real estate focus January 2011 25

Hospital real estate in upheaval

Switzerlandrsquos hospital system is complex

Its structure buildings and fi nancing are

on the cusp of a radical transformation

This change opens up attractive opportu-

nities for investors

The Swiss hospital real estate market is in up-

heaval Not only do the properties (largely

built in the 1970s and 1980s) need signifi cant

renovations but the hospital structure in many

cantons is outdated and balkanized Plus the

widespread shi from inpatient to outpatient

treatment is creating new demands on space