COTTON (Gossypium Spp.) VALUE CHAIN ANALYSIS: THE CASE OF ARBAMINCH ZURIA DISTRICT, GAMO GOFA ZONE, ETHIOPIA MSc THESIS ABAYNEH FEYSO April 2017 HARAMAYA UNIVERSITY, HARAMAYA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COTTON (Gossypium Spp.) VALUE CHAIN ANALYSIS: THE CASE

OF ARBAMINCH ZURIA DISTRICT, GAMO GOFA ZONE,

ETHIOPIA

MSc THESIS

ABAYNEH FEYSO

April 2017

HARAMAYA UNIVERSITY, HARAMAYA

i

Cotton (Gossypium Spp.) Value Chain Analysis: The Case of

Arbaminch Zuria District, Gamo Gofa Zone, Ethiopia

A Thesis Submitted to School of Agricultural Economics and

Agribusiness, Postgraduate Program Directorate

HARAMAYA UNIVERSITY

In Partial Fulfillment of the Requirements for the Degree of MASTER

OF SCIENCE IN AGRICULTURE (AGRIBUSINESS AND VALUE

CHAIN MANAGEMENT)

Abayneh Feyso

April 2017

Haramaya University, Haramaya

ii

APPROVAL SHEET

POSTGRADUATE PROGRAM DIRECTORATE

HARAMAYA UNIVERSITY

We hereby certify that we have read and evaluated this Thesis prepared, under our

guidance, by Abayneh Feyso entitled “Cotton (Gossypium Spp.) Value Chain Analysis:

The Case of Arbaminch Zuria District, Gamo Gofa zone, Ethiopia”. We recommend

that it be submitted as fulfilling the Thesis requirement for the Degree of Master of

Science in Agriculture (Agribusiness and Value Chain Management).

Mengistu Ketema (PhD) ____________ _________

Major Advisor Signature Date

Bosena Tegegne (PhD) ____________ _______

Co-Advisor Signature Date

As a member of the Board of Examiners of the MSc. Thesis Open Defense

Examination, we certify that we have read and evaluated the Thesis prepared by

Abayneh Feyso and examined the candidate. We recommend that the Thesis be

accepted as fulfilling the Thesis requirements for the Degree of Master of Science in

Agriculture (Agribusiness and value chain management).

________________ ___________ _________

Chairperson Signature Date

____________________ ___________ _______

Internal Examiner Signature Date

_________________ ______________ _______

External Examiner Signature Date

iii

DEDICATION

This thesis is dedicated to my elder sister Zena Feyso, who had played key role in nursing

and educating me, and who was eager to see my successes, but passed away. God let her

soul rest in peace.

iv

STATEMENT OF THE AUTHOR

First, I declare that this thesis is my work and that all sources of materials used for this

thesis have been acknowledged. This thesis has been submitted in partial fulfillment of the

requirements for MSc degree at the Haramaya University and is deposited at the University

Library to be made available to borrowers under rules of the Library. I seriously declare

that this thesis is not submitted to any other institution anywhere for the award of any

academic degree, diploma, or certificate.

Brief quotations from this thesis are allowable without special permission provided that

accurate acknowledgement of source is made. Requests for permission for extended

quotation from or reproduction of this manuscript in whole or in part may be granted by

Haramaya University Post Graduate Program Directorates when in his or her judgment the

proposed use of the material is in the interests of scholarship. In all other instances,

however, permission must be obtained from the author.

Name: Abayneh Feyso Signature: ______________

Place: Haramaya University, Haramaya

Date of Submission: ____________________

v

BIOGRAPHICAL SKETCH

The author was born in Abeshige district, Guraghe zone, Southern Nations, Nationalities

and Peoples Regional State in June 1989 G.C. He attended his primary and junior

secondary school at Tadele Kulit primary school and high school and preparatory at Goro

compressive secondary school at Wolikite, capital of Guraghe zone. After completing his

preparatory school, he joined Haramaya University College of Agriculture and

Environmental Sciences under regular program in 2009 and completed his BSc. degree in

Rural Development and Agricultural Extension in 2011. He then joined Southern

Agricultural Research Institute based at Arbaminch Agricultural Research Center as a

junior socio-economic researcher in 2012 worked there until he joined Haramaya

University in September, 2015 to pursue his post graduate study in Agribusiness and Value

Chain Management.

vi

ACKNOWLEDGMENTS

My warmest gratitude goes to my major advisor Dr. Mengistu Ketema and my co-advisor

Dr. Bosena Tegegne for their inspiring guidance, encouragement, critical and constructive

comments starting from the inception of research idea to the final thesis write up.

My particular appreciation and deepest gratitude goes to my mother w/ro Aster Awano

who has devoted her life in nursing me with affection and love which played great role in

the success of my life. I would like to thank my elder brother, Ato Tadele Feyso for

couching, scheduling and financial support from lower class to first degree achievement.

My thanks also goes to my wife W/ro Abinet Dejene for advice, affection and love in my

stay in Haramaya University to attend class and for her hospitality during data collection as

well while working on my thesis. My heartfelt appreciation and great thanks go to

Arbaminch Agricultural research center employees specially; Ato Awoke Mensa, W/rt

Selamawit Markos and Ato Amaro Yalke for their great help when my computer fails to

work. Also my great thank goes to Dr. Ashebir Balcha, center manager of Arbaminch

Agricultural Research Center, for providing me with the necessary materials and

facilitation during data collection.

I feel deep sense of gratitude to my friends and classmates especially to Engida Gebre,

Gedefew Kindu and Adugnaw Anteneh for their cooperation, idea sharing and memorable

moments during the entire period of my post-graduate study. I would also like to extend

my appreciation to Arbaminch zuria district Agricultural office workers, Arbaminch town

trade and industry office workers and development agents of the study kebeles for their

support during data collection. Finally, I would like to thank all cotton chain actors

included for this study who extended their warm hospitality and generously shared their

views and made this work possible.

vii

LIST OF ABBREVIATIONS AND ACRONYMS

CSA Central Statistical Agency

EDIR Ethiopian Development Research Institute

EIA Ethiopian Investment Agency

ETB Ethiopian Birr

GDP Gross Domestic Product

GTP Growth and Transformation Plan

ICAC International Cotton Advisory Commission

IPM Integrated Pest Management

LDC Least Developed Countries

MoAN Minister of Agriculture and Natural Resource

PAN Pest Action Network

SCP Structure-Conduct-Performance

SME Small and Micro Enterprises

SNNPR Southern Nations Nationalities and Peoples Regional State

USA United States of America

VIF Variance Inflation Factor

viii

TABLE OF CONTENTS

DEDICATION iii

STATEMENT OF THE AUTHOR iv

BIOGRAPHICAL SKETCH v

ACKNOWLEDGMENTS vi

LIST OF ABBREVIATIONS AND ACRONYMS vii

LIST OF FIGURES xii

LIST OF TABLES IN THE APPENDIX xiii

ABSTRACT xiv

1. INTRODUCTION 1

1.1. Background of the Study 1

1.2. Statement of the Problem 2

1.3. Objectives of the Study 4

1.4. Scope and Limitations of the Study 4

1.5. Significance of the Study 5

1.6. Organization of the Thesis 5

2. LITERATURE REVIEW 6

2.1. Concepts and Definitions of Value Chain 6

2.2. Types of the Value Chains 7

2.3. Value Chain Analysis Framework 8

2.3.1. Value Chain Mapping 8

2.3.2. Measuring Performance 11

2.4. Upgrading 11

2.5. Methods of Evaluating Marketing System 13

2.5.1. The Structure, Conduct and Performance (SCP) Model 14

2.5.1.1. Market structure 14

2.5.1.2. Market conduct 16

2.5.1.3. Market performance 16

2.6. Empirical Studies 17

2.7. Conceptual Framework of the Study 20

3. RESEARCH METHODOLOGY 21

3.1. Description of the Study Area 21

3.2. Types of Data, Sources and Methods of Data Collection 22

ix

TABLE OF CONTENT (Contiued)

3.3. Sampling Procedures and Sample size 23

3.3.1. Producer sampling 23

3.3.2. Sampling of Processors 24

3.3.3. Sampling of Traders 24

3.4. Methods of Data Analysis 25

3.4.1. Descriptive Data Analysis 25

3.4.1.1. Value chain analysis 25

3.4.1.2. Structure Conduct and Performance (S-C-P) model 26

3.4.2. Econometric Analysis 29

3.4.2.1. Model Specification 29

3.4.2.2. Definition of variables and hypothesis 29

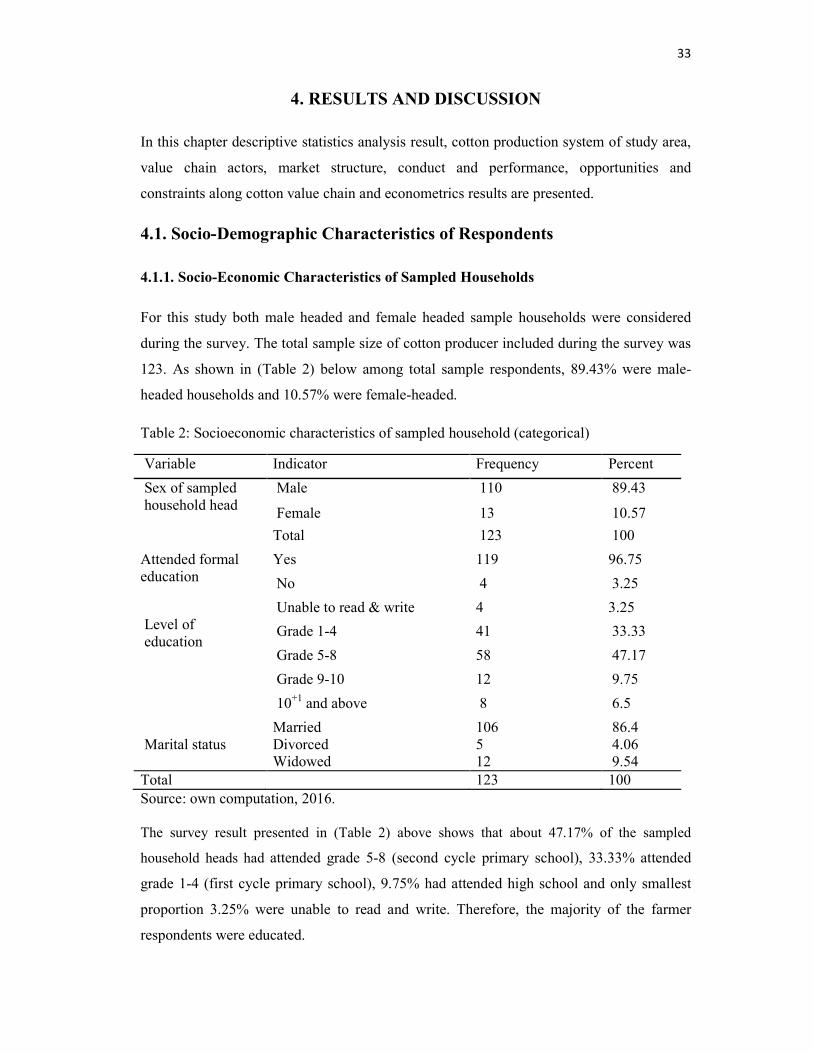

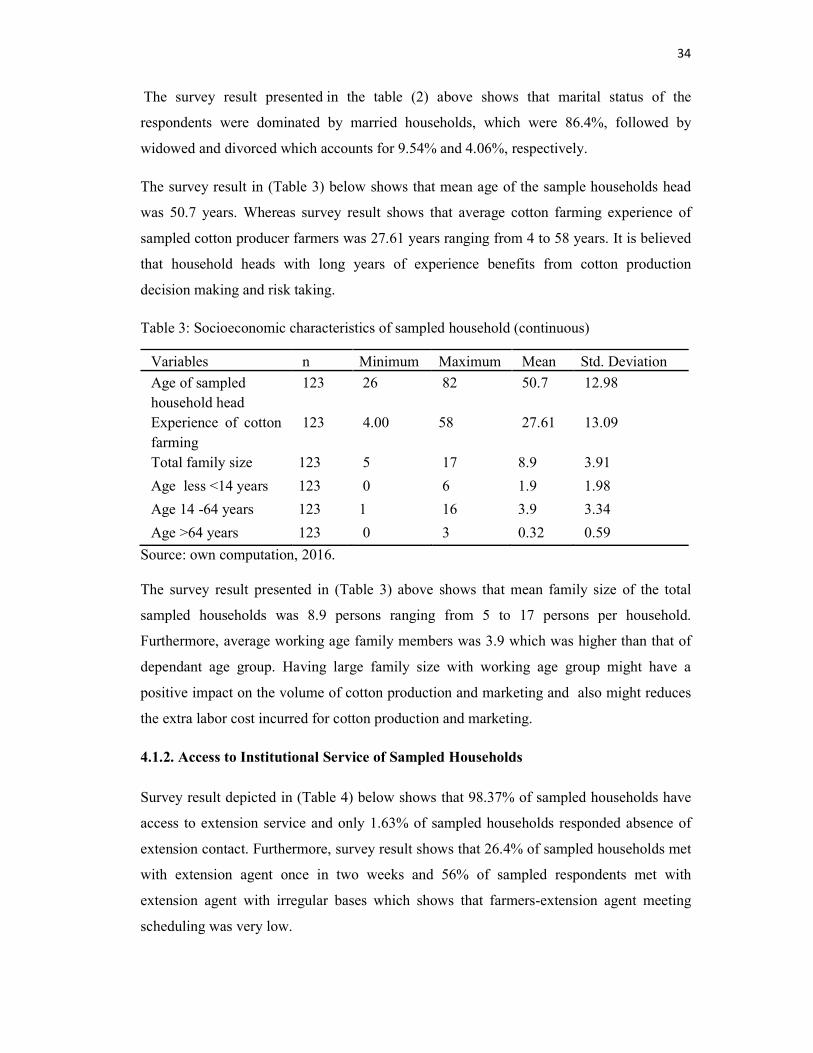

4. RESULTS AND DISCUSSION 33

4.1. Socio-Demographic Characteristics of Respondents 33

4.1.1. Socio-Economic Characteristics of Sampled Households 33

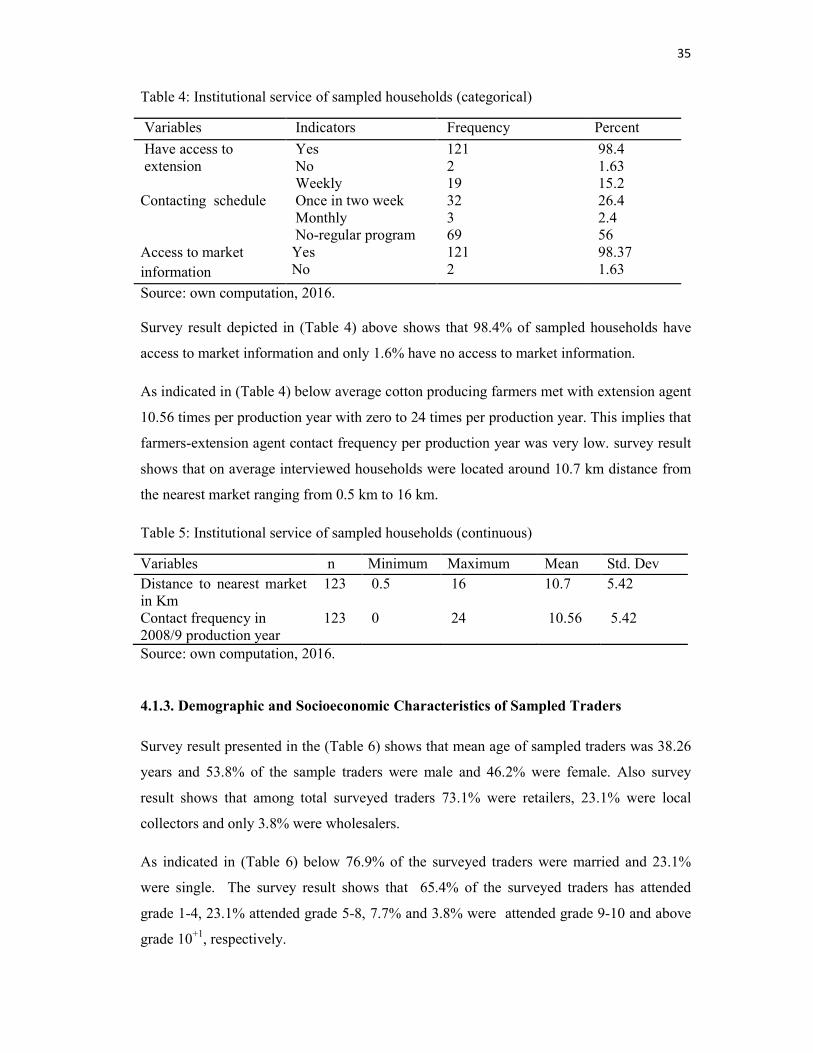

4.1.2. Access to Institutional Service of Sampled Households 34

4.1.3. Demographic and Socioeconomic Characteristics of Sampled Traders 35

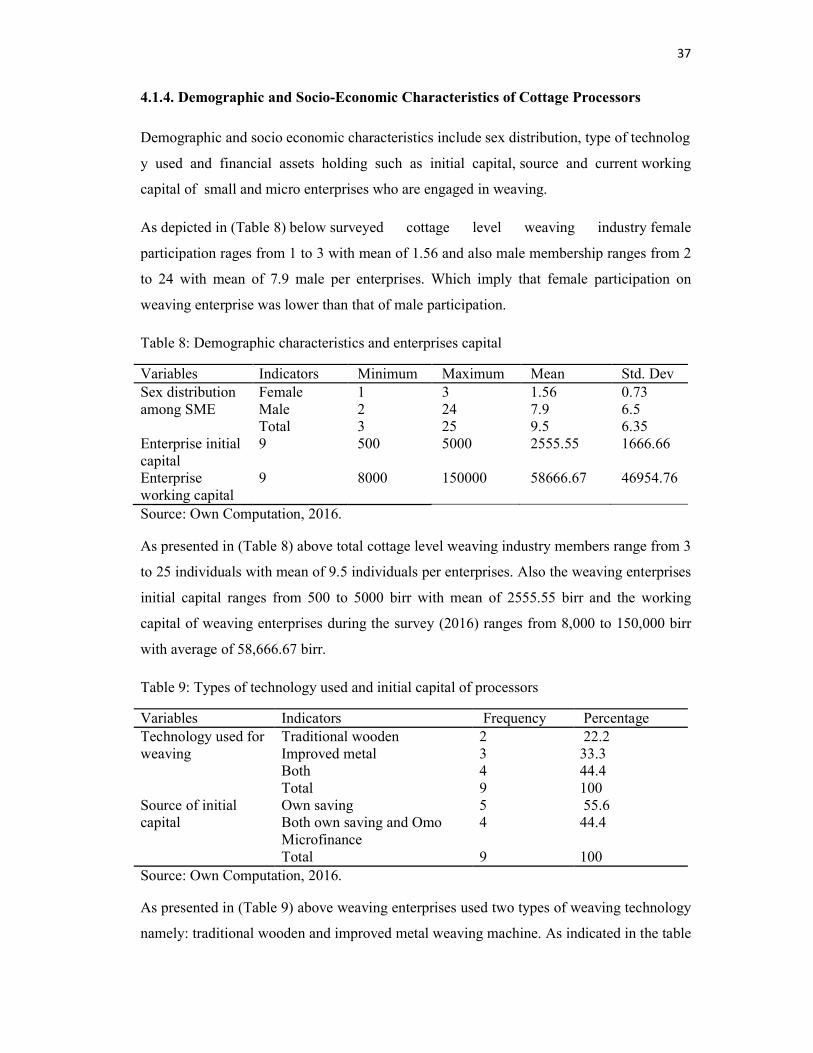

4.1.4. Demographic and Socio-Economic Characteristics of Cottage Processors 37

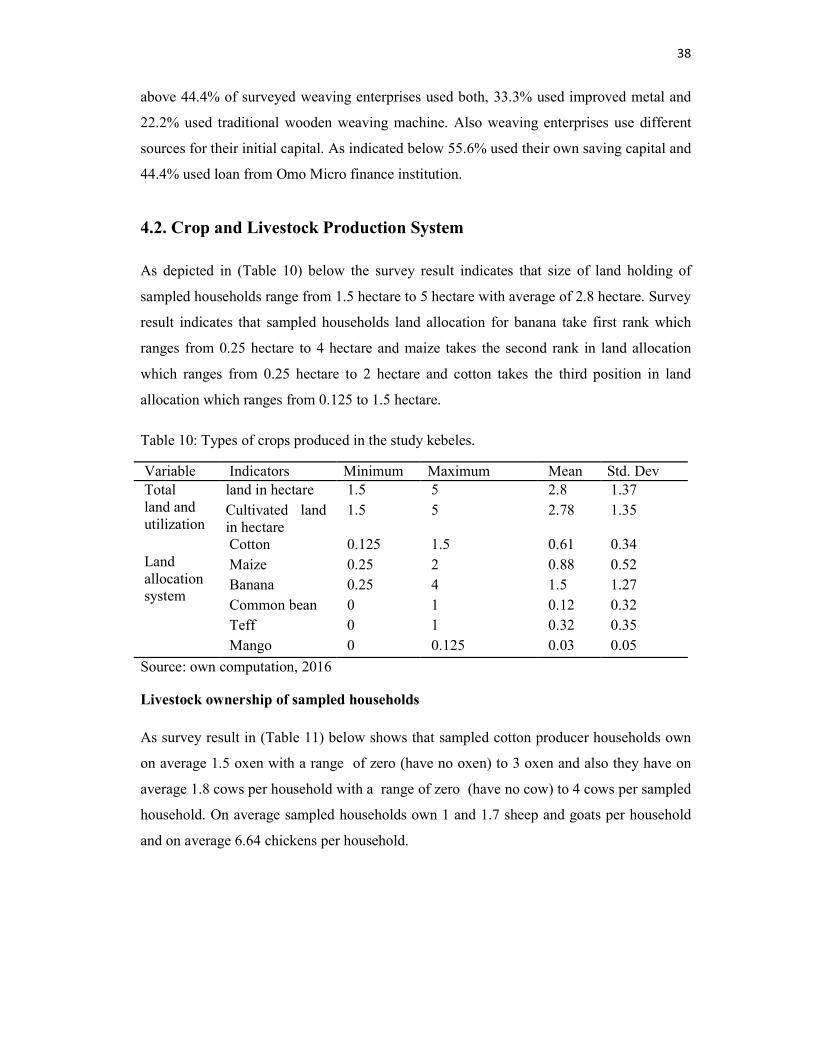

4.2. Crop and Livestock Production System 38

4.2.1. Cotton Production System 39

4.2.2. Cotton Production Calendar and Profitability Analysis 40

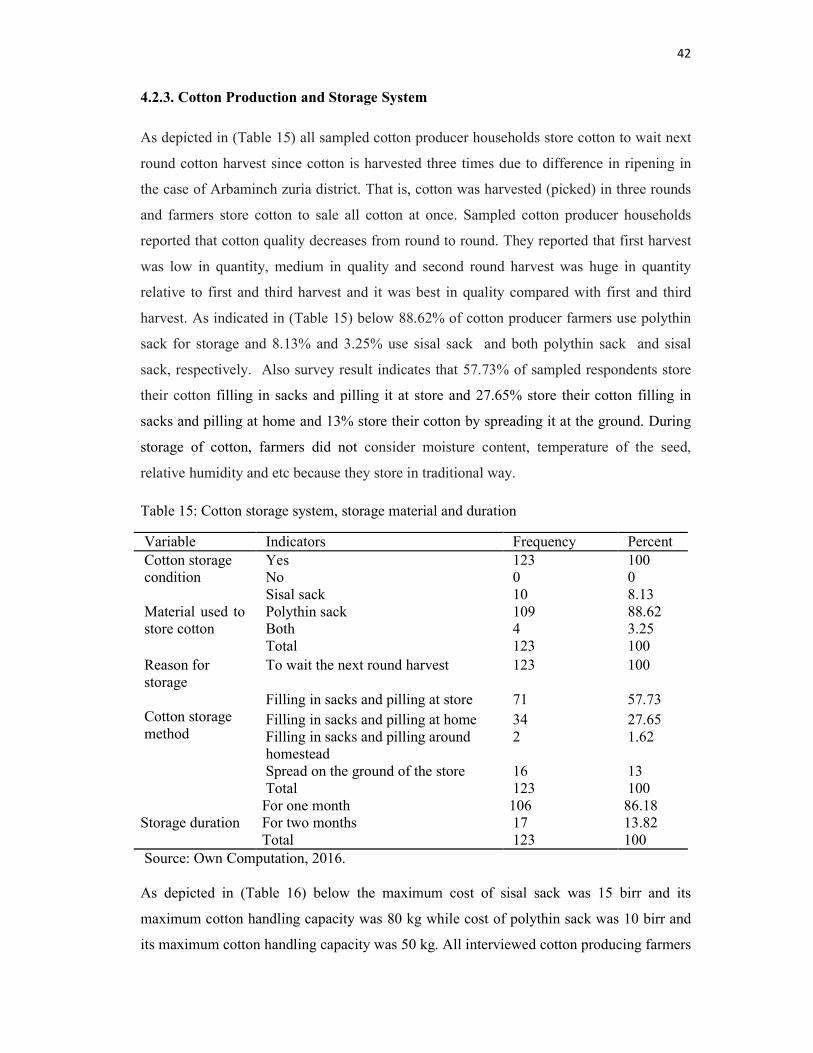

4.2.3. Cotton Production and Storage System 42

4.3. Major Cotton Value Chain Actors and Their Functions 43

4.3.1. Support Institutions 45

4.3.2. Cotton Value Chain Map of Arbaminch Zuria District 46

4.3.3. Value Addition and Financial Analysis of Cotton Value Chain 47

4.4. Cotton Value Chain Upgrading and Governance 52

4.5. Cotton Marketing Channels and Structure-Conduct-Performance 53

4.5.1. Cotton Marketing Channel 53

4.5.2. Cotton Market Structure-Conduct-Performance 55

4.5.2.1. Cotton Market Structure 55

4.5.2.2. Cotton Market Conduct 58

4.5.2.3. Cotton market performance 59

x

TABLE OF CONTENT (Contiued)

4.6. Econometric Results 60

4.6.1. Factors Affecting Farm Household Level Cotton Supply to Market 61

4.7. Challenges and Opportunities of Actors along Cotton Value Chain 63

4.7.1. Cotton Production Opportunities 63

4.7.2. Cotton Production Challenges 64

4.7.3. Cotton Marketing Opportunities 64

4.7.4. Cotton Marketing Challenges 64

5. SUMMARY, CONCLUSION AND RECOMMENDATIONS 65

5.1. Summary and Conclusion 65

5.2. Recommendations 67

6. REFERENCES 69

7. APPENDICES 78

xi

LIST OF TABLES

Table Page

Table 1: Sample distribution of Selected Kebeles 24

Table 2: Socioeconomic characteristics of sampled household (categorical) 33

Table 3: Socioeconomic characteristics of sampled household (continuous) 34

Table 4: Institutional service of sampled households (categorical) 35

Table 5: Institutional service of sampled households (continuous) 35

Table 6: Demographic and socio economic characteristics of traders (categorical) 36

Table 7: Family size and trading experience of traders 36

Table 8: Demographic characteristics and enterprises capital 37

Table 9: Types of technology used and initial capital of processors 37

Table 10: Types of crops produced in the study kebeles. 38

Table 11: Types of livestock owned by sampled households 39

Table 12: Cotton land allocation system and cropping pattern 39

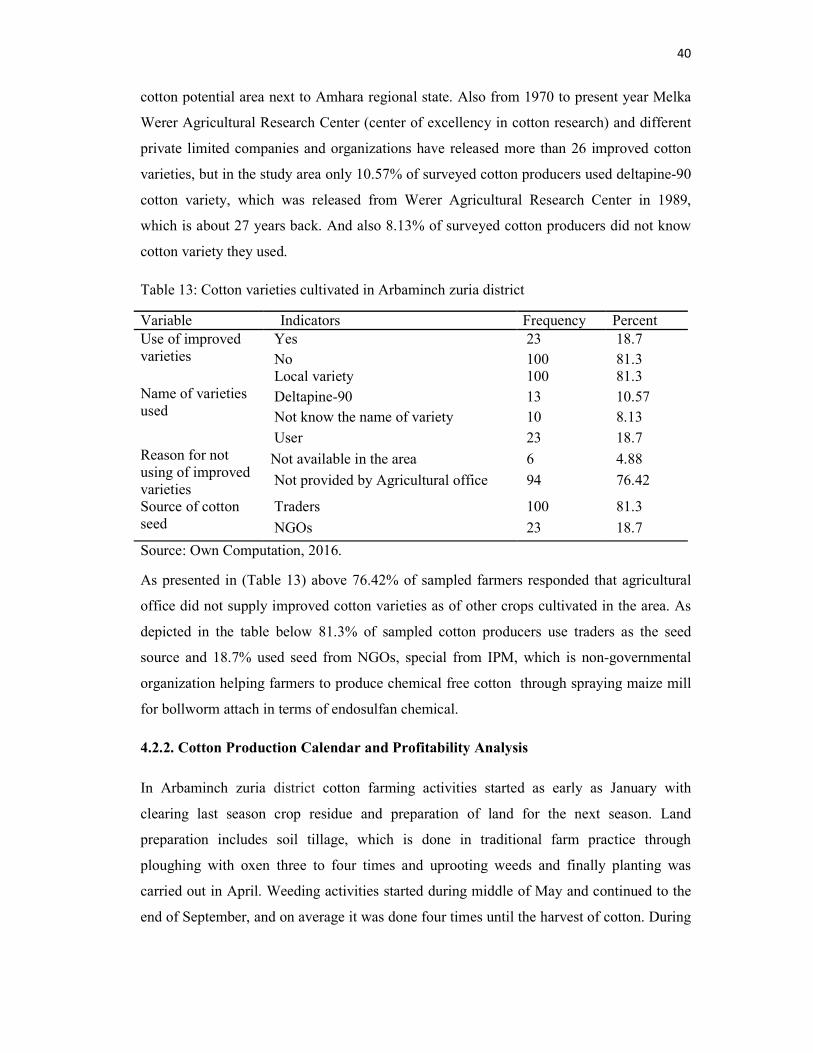

Table 13: Cotton varieties cultivated in Arbaminch zuria district 40

Table 14: Cotton farming financial analysis per hectare and per 100kg 41

Table 15: Cotton storage system, storage material and duration 42

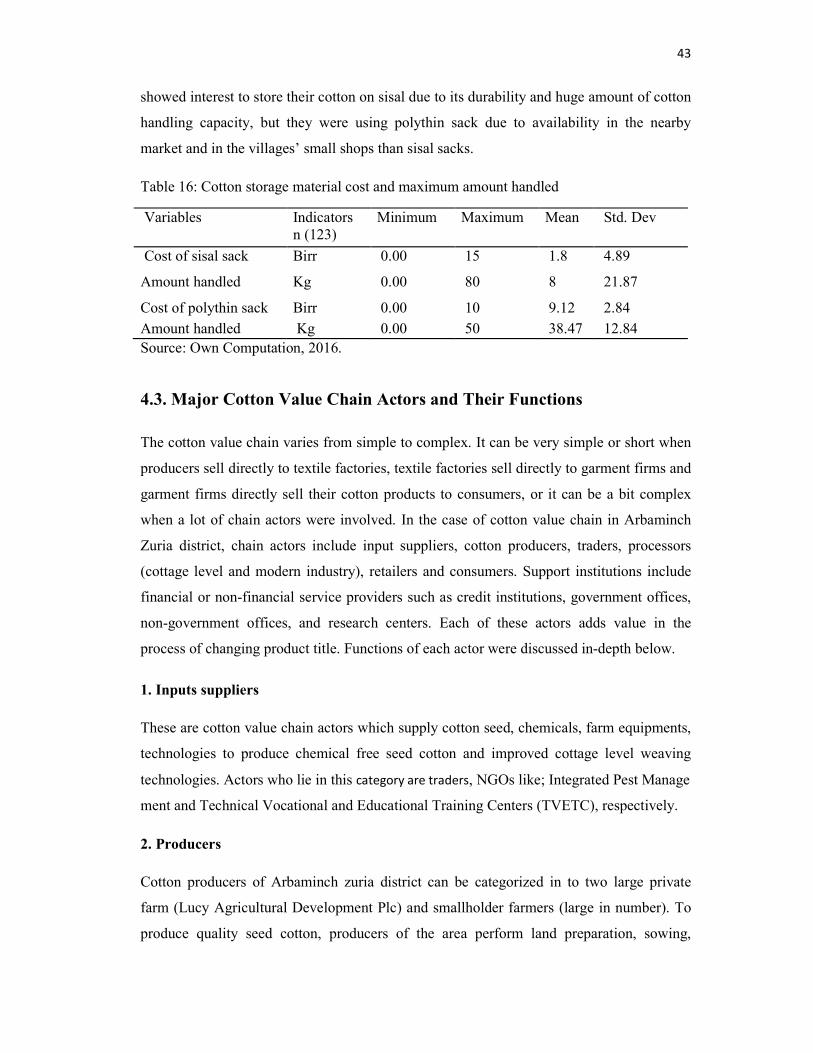

Table 16: Cotton storage material cost and maximum amount handled 43

Table 17: Financial analysis of local collectors 48

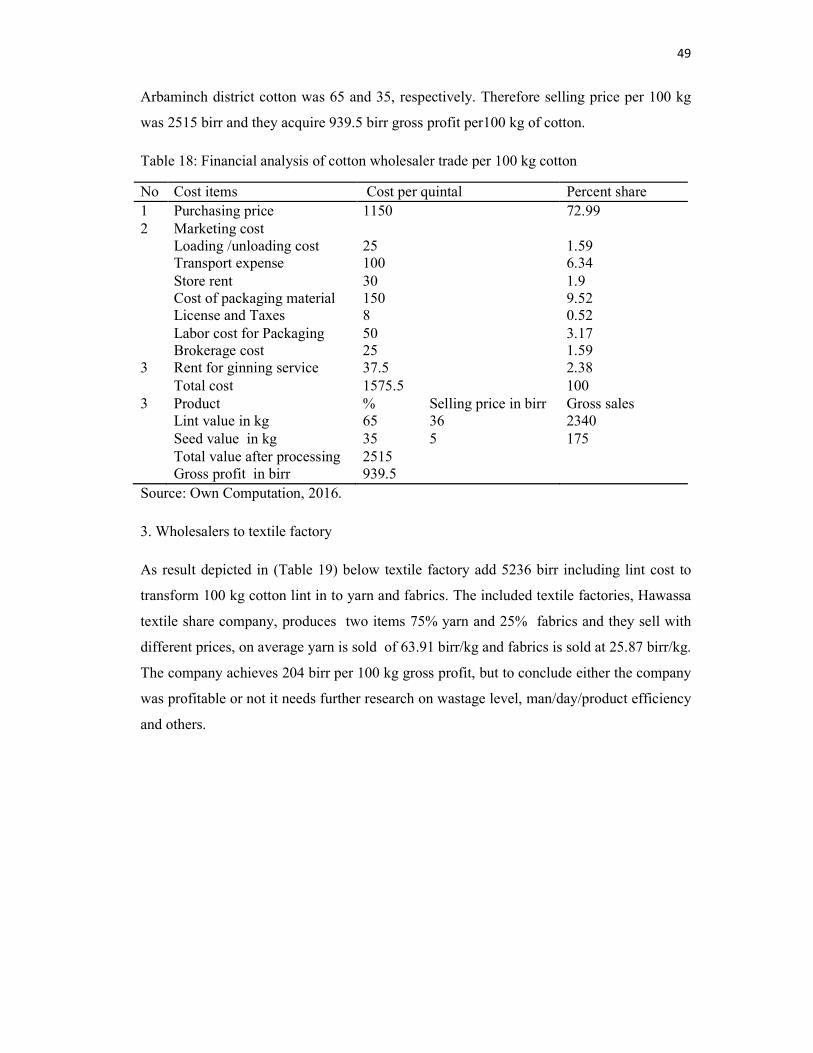

Table 18: Financial analysis of cotton wholesaler trade per 100 kg cotton 49

Table 19: Hawassa textile company value adding activities and cost-benefit analysis. 50

Table 20: Items produced and production cost 50

Table 21: Summary value addition of farmers to textile factory 51

Table 22: Value addition summary of raw cotton to handloom 51

Table 23: Channel of cotton flow and amount sold. 53

Table 24: Amount of cotton sold to different types of traders 53

Table 25: Cotton traders’ Herfindahl-Hirschman Index (HHI) 55

Table 26: Cotton producer households’ information sources and gathering system 56

Table 27: Market entry barriers 57

Table 28: Cotton marketing conduct elements 58

Table 29: Cotton marketing margin and marketing costs and profit (birr/100kg) 59

Table 30: Factors affecting household level cotton supply to market 61

xii

LIST OF FIGURES

Figure Page

1. Elements of value chain analysis 8

2. Conceptual framework 20

3. Location of Arbaminch zuria district 22

4. Cotton value chain map of Arbaminch zuria district 47

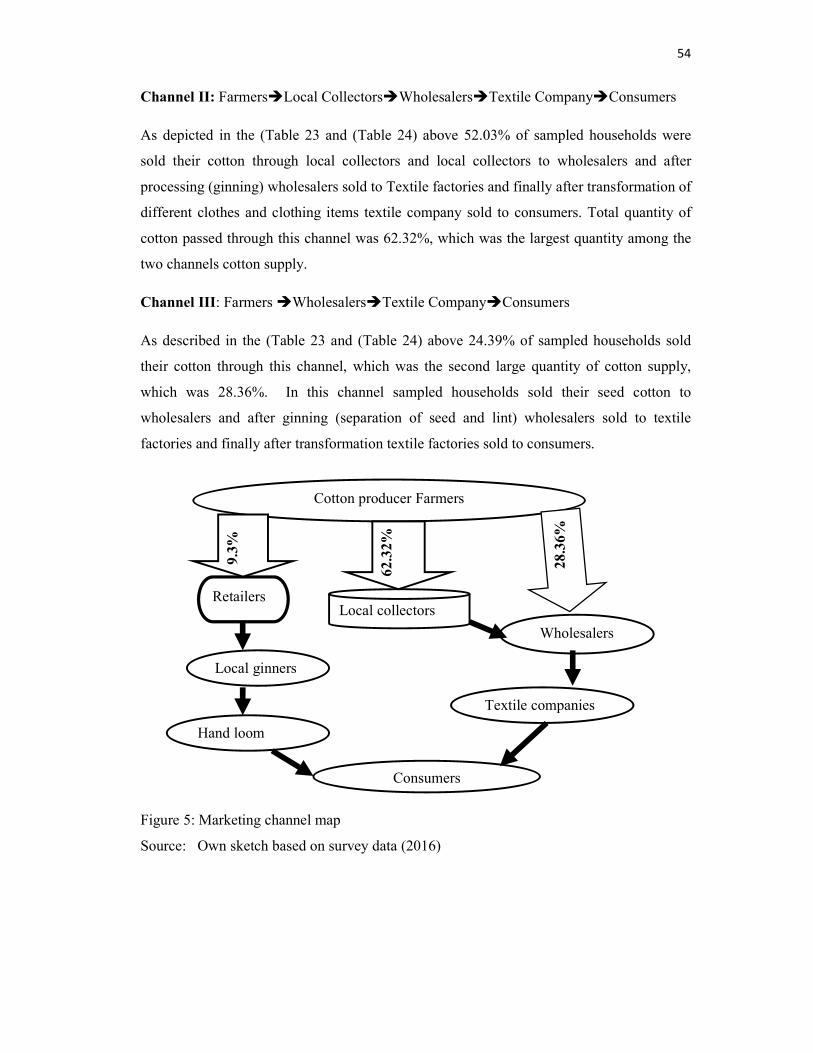

5. Marketing channel map 54

xiii

LIST OF TABLES IN THE APPENDIX

Appendix table 1: Statistical Test Results 79

Appendix table 4: Survey Questionnaire 80

xiv

Cotton (Gossypium Spp.) Value Chain Analysis: The Case of

Arbaminch Zuria District, Gamo Gofa zone, Ethiopia

ABSTRACT

Gamo Gofa zone is the second largest cotton growing area in the country after the Amhara

Region, but cotton marketing had been a challenge for the farmers as they were getting

low prices from the local middlemen. Value chains can be seen as a vehicle by which new

forms of production, technologies, logistics and organizational relations and networks are

introduced. This study was conducted on cotton value chain analysis the case of

Arbaminch Zuria district of the zone with general objective of this study was to evaluate value

chain of cotton in Arbaminch Zuria District. Specific objectives of the study were: to identify actors

and their roles along cotton value chain, to identify cotton value addition activities and to develop

value chain map, to analyze the structure, conduct and performance of the cotton market, to

identify constraints and opportunities in cotton production and marketing and to analyze factors

affecting market supply of cotton at farm level in the study area. For this study, both primary and

secondary data were used. A total of 123 sample households were selected from three kebeles of

Arbaminch zuria district and 26 cotton traders, 9 small and micro enterprises, and one textile

company were interviewed using semi structured questionnaire. Descriptive statistics and

Econometrics models were used to analyze the data. Descriptive statistics results show that the

main cotton value chain actors in the study area are input supplier, producers, local collectors,

wholesalers, ginners, cottage level weavers, textile factories and retailers. Market concentration

ratio at district level was calculated using HHI and its value was 0.553, which shows that cotton

marketing was highly concentrated on hands of few in the study area., long existing tradition of

cotton farming and governmental and NGO support were cotton production opportunities while,

substituting cotton by other crops, lack of access to new and improved cotton varieties were cotton

production challenges of the study area. Increased market demand, proximity to and existence of

textile factories and establishment of new industry parks were cotton marketing opportunities

while, production and supplying of cotton with in similar period, bulkiness, and spoilage, were

cotton marketing challenges in the study area. Econometrics models analysis shows that size of

land allocated to cotton in hectare, use of improved seed and current year cotton price and number

of extension contact were significant and positively related whereas cotton farming experience and

distance to nearest market were found to be significant and negatively related to quantity of cotton

supply. Provision of new improved cotton varieties, regulation and implementation of cotton price

tariffs, strengthening and provision of sustainable and knowledge based extension service and

monitoring land planning of farmers were recommended to improve and strengthening cotton

value chain in the study area.

Keywords: Cotton, Value Chain, Chain Actors, Marketing, Arbaminch Zuria

1. INTRODUCTION

1.1. Background of the Study

The textile and garment industry is one of the oldest, largest and most global industries in

the world. It is the typical ‘starter’ industry for countries engaged in export-oriented

industrialization and is labor-intensive. Textile and garment industries offer a range of

opportunities including entry-level jobs for unskilled labor in developing countries. The

technological features of the textile and garment industry have made it suitable as the first

step on the ‘industrialization ladder’ in poor countries some of which have experienced a

very high output growth rate in the sector (Gereffi, 2002). According to African

Development Bank Group (2014), textile and garment sector contributed about 6.5% and

2.8% of the total value added of manufacturing in 2000/01 and 2010/11, in Ethiopia,

respectively. In terms of export earnings, the sector has contributed on average 2.3% to

Ethiopia’s total export earnings between 2000 and 2012.

The Growth and Transformation Plan (GTP) of Ethiopia considers the development of

textile industries among others and gives special attention and growing significance to

enhancing export revenues by means of substantial investments in value addition (GTP I,

2010). With regard to raw inputs, the country is endowed with a total arable land area of 2.6

million hectares for growing cotton. Moreover, Ethiopia is well endowed with water

resources (ADBG, 2014). However, study by Sutton and Kellow (2010) indicated that only

2.8%, or 73.000 hectares, is utilized for production of cotton. According to ADBG (2014),

the production cost of Ethiopian cotton is 66.3% that of Chinese cotton, 57.3% that of

American cotton, and 90.8% that of Indian cotton. Thus, there is considerable scope for

expansion of cotton planting and increased yields which would improve the domestic

supply of raw material for the textile industry at globally competitive prices. However, the

current domestic cotton production is much below the potential and it became a constraint

with respect to backward integration of the country’s textile and garment industry (EIA,

2012).

The economic value of cotton in the Ethiopian economy is significant. Firstly, it is a major

industrial input for textile firms. The textile and garment industry is one of the priority

areas in Ethiopia’s industrial policy. Secondly, cotton is a major export crop. The country

2

earned 10.6 million USD in 2009/2010 and 0.5 million USD in 2010/2011 from cotton

export (EDRI, 2015).

Cotton is grown in many regions in the country. In each region, there are wide potential

areas; in Tigray 269,130 ha, in Amhara 678,710 ha, in SNNPR 600,900 ha, in Oromia

407,420 ha, in Gambella 316,450 ha, in Benshangul 303,170ha, in Afar 200,000 ha, and in

Somali 225,000 ha. Gamo Gofa zone is the second largest cotton growing region in the

country after the Amhara Region (MoANR, 2004). But study conducted by PAN-UK

(2014) indicated that cotton marketing had been a challenge for the farmers as they were

getting low prices from the local middlemen. Having these evidences, cotton value chain

study is conducted in Gamo Gofa zone.

Given the economic and social importance of cotton to the country in general and to Gamo

Gofa zone in particular, value chain analysis may contribute to an increase in marketable

surplus by scaling-down the losses arising due to inefficient production, processing,

storage, and transportation. Because, value chains can be seen as a vehicle by which new

forms of production, technologies, logistics, labor processes and organizational relations

and networks are introduced (Trienekens, 2011). This was the basic reason why cotton

value chain study was designed in Gamo Gofa zone.

1.2. Statement of the Problem

Cotton is grown in 80 countries world‐wide, with a total of 100 countries were involved in

cotton imports and exports. It is sown on 2 to 2.5% of global arable land. Cotton is one of

the most important global crops in terms of land area, after wheat, rice, corn and soy beans

(Townsend, 2010).

Cotton is a critical crop for many African countries, and the supply of adapted and quality

seed to farmers is essential to ensure productive and remunerative cotton sectors for

farmers, traders and states (Traidcraft Policy Unit, 2011).

Ethiopia is believed to be one of the origins of cotton, and cotton cultivation is deep-rooted

in the history of the country’s agriculture. It is one of the major cash crops in the country

and is extensively grown in the lowlands under large-scale irrigation schemes and also it is

grown on small-scale farms under rain-fed agriculture. However, Ethiopia share only about

5% of total cotton produced in Africa (EIA, 2012). As to total arable and potential area for

cotton production, the country is utilizing below potential. According to Bosena et al.

3

(2011) out of the country’s total potential areas for cotton production, only about 4% is

being utilized. As a result, the amount of cotton produced in the country is low.

In Ethiopia, there are three major groups of cotton producers, namely: the smallholder

.farmers, large state farms and private commercial farms. Cotton produced by the state

farms and private commercial farms is mainly used in the modern textile manufacturing

sector and to some extent exported to foreign countries. On the other hand, cotton produced

by smallholder farmers is for the large part used by the hand loom sector (EDRI, 2014).

Generally there is adequate and growing domestic and world demand for cotton production

in the country. The major markets for Ethiopian cotton are Africa, Asia and Europe, with

Asia alone accounting for 67% of the total exports (EIA, 2012). Still the cotton sub-sector

offers a unique opportunity for Ethiopia in terms of serving as a bedrock upon which the

country can shift to high value added technological transformation following its strong

backward and forward linkages with various sectors and its provision of employment

opportunities for the large number of the rural poor. The Government of Ethiopia wishes to

take a deliberate effort and action to stimulate the growth and potential of this sub-sector in

terms of making cotton one of the major commercial crops in the country (Zerihun, 2015).

The town of Arbaminch, (505 km south of Addis Ababa) is the administrative centre for the

Gamo Gofa Zone in the Southern Nations Nationalities and Peoples Region (SNNPR) of

Ethiopia, the second largest cotton growing regions in the country after Amhara Region

(MoANR, 2004). However, most studies which have been conducted on cotton (Bosena,

2008, Bosena et al., 2011; EIA, 2012; PAN-Ethiopia, 2014) have focused only on

production and marketing aspects and were limited to a specific (Awash Valley, Humera,

Metema and Abobo) areas. Again, few researches which were conducted by individuals

and institutions (Zerihun, 2015; EDRI, 2014 & EDRI, 2015) focused only on value chain

aspect. This study was designed to analyze cotton value chain, market structure, conduct

and performance concurrently and to identify factors affecting household cotton supply to

market to generate information about its entire value chain in the study area due to absence

of adequate information on cotton value chain, market structure, conduct and performance

cotton marketing had been a challenge for the farmers as they were getting low prices from

the local middlemen (PAN-UK, 2014).

According to Mengistu (2010), without having well established coordination among the

value chain actors and convenient marketing systems, the potential increment in

4

productivity, rural incomes and foreign exchange earnings resulting from dispersed efforts

and introduction of improved production technologies alone could not be effective.

In order to narrow the aforementioned research gaps on the study area; this stud tried

to answer the following questions:

1. What are the major activities done to add value in cotton?

2. Who are the actors along cotton value chain?

3. How efficient is cotton value chain?

4. How is the benefit from trade shared among cotton value chain actors?

5. What are the factors that affect market supply of cotton in the study area?

6. What are the constraints and opportunities in cotton production and marketing?

1.3. Objectives of the Study

General objective

The general objective of the study was to evaluate value chain of cotton in the case of

Arbaminch zuria district.

The specific objectives of the study were:

1. To identify actors and their roles along cotton value chain in the study area.

2. To identify cotton value adding activities and to develop value chain map in the study

area.

3. To analyze structure, conduct and performance of cotton market in the study area.

4. To analyze factors affecting market supply of cotton at farm level in the study area

5. To identify constraints and opportunities in cotton production and marketing in the

study area.

1.4. Scope and Limitations of the Study

The study concentrated on cotton value chain analysis in Arbaminch zuria district at three

Kebeles with sample size of 123 cotton producer farm households, 26 traders, 9 small and

micro enterprises and one modern textile factory. The study focused mainly on the cotton

value chain actors that include producers, processors, local collectors, wholesalers, retailers

and support institutions.

Limitation of the study was that cotton goes through two main stages of processing:

primary processing, where seed cotton is transformed into lint and seed, where lint is

5

transformed into yarn for garment production and secondary processing, where seed is

transformed into food oil and seed cake for animal feed. However, due to data complexity

this cotton value chain analysis focused only on the primary processing. Another limitation

of the study was that the empirical analysis was done based on cross-sectional data.

However, households may change their cotton production and marketing decisions from

one year to the next depending on production and market conditions.

1.5. Significance of the Study

The study generated valuable information on cotton value chain, market structure-conduct

and performance and determinants of quantity of cotton supplied to market that might assist

development practitioners and policy makers to make relevant decisions in the development

of cotton value chain and marketing to improve the livelihood of cotton value chain actors.

Also it may serve as a reference material for further research on similar topics and other

related subjects.

1.6. Organization of the Thesis

This thesis is organized in five chapters. The first chapter has already dealt with

introduction. The second chapter contains the reviewed literature and empirical studies. The

third and fourth chapters deal with the research method, results and discussion of the

research, respectively. Finally, the fifth chapter presents summary, conclusions and

recommendations.

6

2. LITERATURE REVIEW

In this chapter concepts and definitions of value chain, theoretical and empirical reviews,

types of value chain and conceptual framework were reviewed and presented.

2.1. Concepts and Definitions of Value Chain

In the mid 1980s, Porter developed the concept of the value chain in the context of his work

on competitive advantage (Porter 1985). He developed his concept to analyze specific

activities through which companies may create value by breaking down their activities into

value-added. Porter distinguished two important value-adding activities of an organization:

primary activities (inbound logistics, operations, outbound logistics, marketing, and sales)

and support activities (strategic planning, human resource management, technology

development, and procurement) (Porter 1985). However, Porter’s value chain approach is

restricted to the firm level neglecting the analysis of up or downstream activities beyond the

company. The commonly accepted definition of value chain was stated by Kaplinsky and

Morris (2002): they defined “The value chain describes the full range of activities which

are required to bring a product or service from conception, through the different phases of

production, delivery to final consumers, and final disposal after use”. Under this definition

the value chain can be seen as “incorporating production, exchange, distribution and

consumption of a given product or service” (Kaplinsky, 1998).

The value chain can also be defined as “a sequence of organizations that are involved in

consecutive production activities” (Roduner, 2005). Thus, no matter which definition is

applied by value chain scholars, all definitions of value chain includes all stages from

production to consumption of a particular product: “from gate to plate” or “from cradle to

grave”.

One of the core concepts in value chain analysis is value added (VA). According to FAO,

(2006b) the value added refers to the creation of wealth, the contribution of the particular

production process, or particular chain, to the growth of the economy. Value added

measures the increase in wealth for the nation as a whole, as represented by the sum of

remuneration to labor, interest charges and taxes in addition to the net margin of the

producers. From a more focused point of view value added represents the worth that has

been added to a product or a service at each stage of production or distribution. An

7

economic agent can calculate the value added as a difference between the full value of the

output and the value of the purchased inputs (McCormick and Schmitz, 2001).

Value added is created at different stages and by different actors throughout the value

chain. Value added may be related to quality, costs, delivery times, delivery flexibility,

innovativeness, etc. The size of value added is decided by the end-customer’s willingness

to pay. Opportunities for a company to add value depend on a number of factors, such as

market characteristics (size and diversity of markets) and technological capabilities of the

actors. Moreover, market information on product and process requirements is key to being

able to produce the right value for the right market. In this respect finding value adding

opportunities is not only related to the relaxation of market access constraints in existing

markets but also to finding opportunities in new markets and in setting up new market

channels to address these markets (Trienekens, 2011).

2.2. Types of the Value Chains

Different types of the value chains can be recognized based on the number of processing

stages, spatial relationship of economic activities and the structure of involved participants

of the chains. Sturgeon (2001) has classified the value chains according to organizational

scale and to spatial scale. Based on this classification supply chain, value chain and

production network, all fall under organizational scale.

Gereffi et al. (2005) classified value chains based on the type of the value chain

governance. According to the type of governance, he classified value chain as follows:

chains ruled by markets, modular value chains, relational value chains, captive value chains

and hierarchy structured value chains. In a much broader sense of governance, the value

chains can be classified into buyer-driven chains, characterized by labor-intensive

industries and relevant to developing countries; into producer-driven chains, characterized

by capital and technology intensive industries and where producers take responsibility for

assisting the efficiency of both their suppliers and their customers. Value chain analysis is

important both conceptually and practically and can provide insight on the areas of

intervention and upgrading with the aim of value chains development (McCormick and

Schmitz, 2001). Value chains analysis is production networks in which business actors

exploit competitive resources and operate within an institutional environment. Therefore,

we conceptualize a value chain as a network of horizontally and vertically related

8

companies that jointly aim at/work towards providing products or services to a market

(Trienekens, 2011).

2.3. Value Chain Analysis Framework

The VCA framework centers around three major segments that describe each production

link in the value chain: source, make, and deliver. Each activity mapped on the value chain

diagram can be represented by a cost breakdown. Quantification of the value chain by

measuring monetary value and time is undertaken along the source-make-deliver construct

for each production activity. This measurement framework provides a consistent way to

organize and classify cost and time figures for comparison across diverse production

activities. The resulting monetary value and time measurements are then further analyzed

and transformed to derive metrics such as value added and productivity to identify

performance gaps. Firm-level performance is measured and inferred for the sector as a

whole. Establishing benchmarks for selected indicators against competitor countries, good

practice cases, and international standards can help in assessing the relative competitiveness

of the sector.

According to FIAS (2007), the value chain analysis typically includes the following key

elements or steps: choose the sector(s) to assess, analyze the market, map the value chain,

measure the performance of the chain and establish benchmarks, analyze performance gaps

(focusing on government and market failures).

Figure 1: Elements of value chain analysis

Source: FIAS, 2007

2.3.1. Value Chain Mapping

The first step of a value chain analysis is the so-called mapping. In order to do so, the

boundaries to other chains need to be defined. The main idea is initially to identify the

actors and then to ‘map’ the traced product flows within the chain including input supply,

production, processing, and marketing activities. The objective is to give an illustrative

representation of the identified chain actors and the related product flows. A mapped value

Sector Choice

Market Analysis

Value Chain Mapping

Measure Performance

Analysis of Performance Gaps

9

chain includes the actors, their relationships, and economic activities at each stage with the

related physical and monetary flows (Winter, 2009)

A value chain map allows one to depict all activities, actors, and relationships among

segments of the chain, and the interactions between producers and intermediaries.

Information from a market analysis is used in conjunction with detailed firm data to

understand the sourcing, production, and delivery segments of an industry at micro levels.

This process of obtaining disaggregated information about a firm (or a farm) or about a

number of firms (or farms) and subsequent extrapolation to an industry or sector allows one

to better understand (FIAS, 2007).

There are two different kinds of approaches used for mapping.

1. Functional and Institutional Analysis

The FAO provides a set of modules, which presents a systematic approach to value chain

analysis for agricultural commodities. The mapping is denoted as a functional and

institutional analysis (FAO 2006a) which starts with constructing a ‘preliminary map’ of a

particular chain to provide an overview of all chain actors (institutional analysis) and the

type of interaction between them (functional analysis). The results can be presented either

in a table or in a flow chart, which is called the ‘preliminary map’ of the chain. The FAO

(2006a) methodology includes three essential aspects for developing a preliminary map.

These are: The principal functions of each stage, agents carrying out these functions,

principal products in the chain and their various forms into which they are transformed

along the entire chain.

Once the flow chart has been drawn, these flows are quantified, both in physical and

monetary terms. The procedure allows assessing the relative importance of the different

stages or segments of the chain. Applied was this methodology for example by Rudenko

(2008) identifying and mapping the relevant value chain stages for the cotton and wheat

value chain in Uzbekistan.

Kaplinsky and Morris (2002) suggest similar procedures for implementing value chain

analysis. Their concept consists of two steps in order to map the value chain of interest. The

first step includes drawing an ‘initial map’, which shows the chain boundaries including the

main actors, activities, connections and some initial indicators of size and importance. The

second step consists of elaborating the refined map by quantifying key variables such as

10

value-added, and by identifying strategic and non-strategic activities. This refined map can

be understood as a framework for showing chain statistics (Schmitz, 2001).

2. Financial and Economic Value Chain Analysis

FAO provides a methodology for commodity chain analysis focusing on the product level.

The FAO methodology comprises two separate parts: (a) financial analysis, and (b)

economic analysis. Financial analysis is undertaken from the perspective of individual

agents. The aim is to determine their financial costs and benefits. In contrast, economic

analysis is undertaken from the perspective of the society or the overall economic system

(national economy, sector, or chain), considering shadow prices and opportunity costs in its

calculation. Both analyses are conducted for a defined period, usually one year. For

financial and economic commodity chain analysis, different indicators are calculated based

on the concept of value added to derive findings according to the chain performance and

impact on agents and the government. Hence, the value added for each step of the chain as

well as the overall value added of the entire chain are calculated and interpreted as the

creation of economic wealth by one or more productive activities. By definition, the

amount of total value added “measures the contribution of the commodity chain to Gross

Domestic (or National) Product” (FAO, 2006b). The calculation of the value-added (VA) is

defined as:

VA = Y – II

The value of the intermediate inputs (denoted as II) used in the productive activities has to

be subtracted from the value of the output of a product i(denoted as Y). The difference

represents the value-added from an individual agent j. Thus, to calculate the value added,

all costs and sales for the relevant stages have to be measured. In addition, the underlying

product and input prices are essential. Hence, financial and economic analyses differ in the

underlying price. While financial analysis is based on actual market prices, economic

analysis is based on shadow prices. Consequently, if there are any price distortions, the

financial analysis will reflect those.

The overall value added is the following:

agentschainchainchain VAIIYVA

It makes possible to identify which stage contributes to the highest share of the value

added, which stage to the lowest, and if there is an overall positive value added.

Afterwards, the question that arises is: how is the created wealth distributed among

fundamental agents. This is especially interesting for policy makers, who want the

11

households to get a fair share in the profit. Thus, another possibility of calculating the

value-added is the following:

ijijijijij TISWDGAVA )(

After calculating the creation and distribution of the value added among the agents, the next

step is the economic impact analysis. It includes the investigation of upstream induced

effects of productive activities because of the demand for intermediate inputs from the rest

of the national economy. In this part of the analysis, the chain is viewed as an integral part

of the national economy similar to input-output analysis Indicators are built to evaluate the

chain’s impact on growth and income in terms of chain distribution to developmental

policy objectives (FAO 2006c).

2.3.2. Measuring Performance

The performance of an industry or sector may be explained by: examining various activities

in the production chain and comparing these with national or international benchmarks;

identifying gaps in performance; and probing into the underlying policies, institutions, and

infrastructure-related inefficiencies that directly affect productivity and competitiveness.

The metrics used to measure the performance of a value chain include: Cost, time value

added and productivity. Cost and productivity are the underlying factors in determining the

competitiveness of an industry. Costs encompass monetary costs and utility costs as well as

transactions costs.

2.4. Upgrading

The practical usefulness of value chain analysis stems helps to find those segments of the

value chains which need to be improved or upgraded. The notion of upgrading, as used in

studies on competitiveness, describes a range of activities aimed at manufacturing better

products, or increasing production metrics or moving into more skilled activities (Porter,

1990; Kaplinsky, 2000).

Gereffi (1999) defines upgrading as: “a process of improving the ability of a firm or an

economy to move to more profitable and/or technologically sophisticated capital and skill-

intensive economic niches.”

According to Kaplinsky and Morris (2002), upgrading is a process of adopting innovation –

a process which recognizes relative endowments and the existence of rents. According to

12

Humphrey and Schmitz (2002), the typology of upgrading distinguishes three main

upgrading possibilities: functional; product; and process upgrading.

Kaplinsky (2002) gives four directions in which economic actors can upgrade: increasing

the efficiency of internal operations, enhancing inter-firm linkages, introducing new

products and changing the mix of activities conducted within the firm. One of the main

tasks of upgrading is focused on exploring and employing competitive advantages. A value

chain approach can help to formulate or to shape the upgrading strategies by describing and

analyzing sources for competitiveness (Schmitz, 1999).

Process upgrading: increasing the efficiency of internal processes such that these are

significantly better than those of rivals, both within individual links in the chain and

between the links in the chain (Humphrey and Schmitz, 2001).

Process upgrading focuses on the one hand on upgrading the product and on the other hand

on optimization of production and distribution processes. Product and process upgrading

are most common in developing country value chains (Trienekens, 2011).

Product upgrading: introducing new products or improving old products faster than rivals.

This involves changing new product development processes both within individual links in

the value chain and in the relationship between different chain links (Humphrey and

Schmitz, 2001).Upgrading of value added in products is always related to (potential)

demands in a market. These can be related to intrinsic (product quality, composition,

packaging, etc.) and extrinsic product attributes, which are related to typical process

characteristics (Trienekens, 2011).

Functional upgrading: increasing value added by changing the mix of activities conducted

within the firm or moving the locus of activities to different links in the value chain

(Humphrey and Schmitz, 2001).

Chain upgrading/inter-sectoral upgrading: moving to a new value chain. According to

Gereffi (1999) chain up grading is “how value adding activities have been moved from

developed to developing countries leading to new and more fine-meshed industry structures

worldwide.”

Upgrading of Value Chain-network Structure: Upgrading of the network structure

includes upgrading of horizontal as well as vertical relationships focusing on taking part in

the right market channel. Collaboration with horizontal partners may include joint

13

purchasing of production inputs, joint use of production facilities and joint marketing of

products. Moreover, in its most sophisticated form, horizontal collaboration might result in

product differentiation combining value adding activities with other sectors of the economy

(inter-sectoral upgrading) Trienekens et al. (2009).

Upgrading of vertical network (structure) relationships should focus on being part of the

right channel aiming at the right market. Developing country value chains are now

increasingly trying to differentiate their market outlets, which makes them less dependent

on their current customers (Trienekens, 2011).

Upgrading of Governance Structures: Modern market-oriented chains have the tendency

to become shorter (with fewer actors) as intermediaries between producers and downstream

parties in the chain become superfluous because of the emergence of direct trading

relationships between large producers (or producer groups) and downstream parties

(Gereffi, 2003).

2.5. Methods of Evaluating Marketing System

The development of reliable and stable market system has been an important element in

commercialization and specialization in the agricultural sector. In order to evaluate the

functioning and performance of the market, there are three different approaches namely

traditional, Structure-Conduct-Performance (SCP), and the New Empirical Industrial

Organization (NEIO) approaches that integrate SCP with value chain analysis. The SCP

approach was developed in the United State as a tool to analyze the market organization of

industrial sector and it was later applied to assess the agricultural system and this

framework was to evaluate the performance of industries in the USA (Meijer, 1994).

Efficiency factors can be evaluated by examining marketing enterprises for structure,

conduct and performance (Abbott and Mekeham, 1979). The performance of a certain

market or industry depends on the conduct of its sellers and buyers which, in turn, is

strongly influenced by the structure of the relevant markets (Scarborough and Kydd, 1992;

Margrath, 1992). Variables relevant in appraising firm’s behavior can be put into three

general categories structure, conduct, and performance related variables.

14

2.5.1. The Structure, Conduct and Performance (SCP) Model

The central hypothesis (of the SCP framework) is that observable structural characteristics

of a market determine the behavior of firms within that market, and that the behavior of

firms within a market, give structural characteristics, determines measurable market

performance Martin (2002). Environmental and internal conditions of the firm have an

influence on the actions and behavior of the firm. On the other hand, the composite of

firm’s actions is not equivalent to a complete description of overall market result. Only

some important actions and their consequences on performance of the firm are relevant

(Andargachew, 1990).

Structure -Conduct and Performance model is one of the most common and pragmatic

methods of analyzing a marketing system. It analyzes the relationship between functionally

similar firms and their market behavior as a group and, it is mainly based on the nature of

various sets of market attributes and relations between them and their performance

(Scarborough and Kydd, 1992). This analytical method is based on the theory that market

structure and market conduct determine the performance of a marketing system.

2.5.1.1. Market structure

Market structure is defined as characteristics of the organization of a market which seems

to influence strategically the nature of competition by pricing behavior within the market

(Scott, 1995). Market structure is the description of the number and nature of participants in

a market. Structural characteristics may be used as a basis for classifying markets. Markets

may be perfectly competitive, monopolistic, or oligopolistic (Cramer and Jenson, 1982).

The four salient aspects of market structures include the degree of seller concentration, the

degree of buyer concentration, the degree of product differentiation, and the condition of

entry (Scott, 1995).

Competition plays a key role in harnessing the rivalry and the profit seeking of the market

place in order that it may serve the public interest (Khols and Uhl, 1985). Determining the

presence or absence of the requirements of the model of perfect competition can be used

indirectly to assess the economic efficiency of markets. Many studies concerned with the

efficiency of agricultural markets begin in this form of analysis.

Methods of measuring of market concentration are:-

1. Market Concentration Ratio

15

Considerable attention has been focused on market concentration as a measure of

competition in marketing. Concentration refers to the proportion of industry sales made by

its largest firms. In general, the more concentrated the industry sales, the more likelihood

that the market will be imperfectly competitive (Khols and Uhl, 1985).

Concentration ratio is one of the commonly used measures of market power, which in other

words, refers to the number and relative size of distribution of buyers or sellers in a market.

Concentration ratio measures the per cent of traded volume accounted for by a given

number of participants and is designated by the formula:

1,2,3,4r .0

r

i

SiCR

CR=is concentration ratio, Si =is the percentage share of the all firms and r = is the number

of the largest firms for which the ratio is to calculated

Khols and Uhl (1985) suggest that as a rule of thumb, a four enterprise concentration ratio

of 50 percent or more is indicative of a strong oligopolistic industry; of 33-50 per cent ratio

denotes a weak oligopoly, and less than that un-concentrated industry.

Despite wide application of concentration ratio as a measure of the ratio of market

concentration, there are limitations against the index. Scarborough and Kydd (1992)

suggest that calculating and using concentration ratios as a measure of market structure is

subject to empirical, theoretical and inferential problems. In least developed countries,

where firm records are usually not available publicly, it would be difficult to determine

such ratios on anything, but the most local of scales.

Another problem associated with concentration ratio is the arbitrary selection of r (the firms

that are taken to calculate the ratio). The ratio doesn’t indicate the size distribution of r

firms. However, when the numbers of participants in an industry is large it will be difficult

to organize oligopolistic behavior. Under such local circumstances, the concentration ratio

given above can be usefully determined (Scarborough and Kydd, 1992).

2. The Gini coefficient

Gini coefficient is most easily calculated from unordered size data as the “relative mean

difference,” that is the mean of the difference between every possible pair of individuals,

divided by the mean size (Taru et al., 2010). They further stated that the Gini coefficient

ranges from zero to one. A perfect equality in concentration (low) of sellers is expected if

Gini coefficient tends towards zero, while perfect inequality in concentration (high) of

16

sellers is expected if Gini coefficient tends towards one. If Gini coefficient equals to one

then the market is imperfect and if Gini coefficient is equals to zero the market is perfect

and competitive.

2.5.1.2. Market conduct

Market conduct implies the analysis of human behavioral pattern that are not readily

identifiable, obtainable, or quantifiable (Olukosi et al., 2005). Thus, the conduct refers to

the behavior of firms or the strategies used by the firms, like their pricing, buying, selling

e.t.c. These activities may require the firms to engage into informal cooperation or

collusion. Therefore in the absence of a theoretical frame work for market analysis, there is

a tendency to treat conduct variable in a descriptive manner (Pomeroy and Trinidad, 1995).

2.5.1.3. Market performance

Performance of the market is reflection of the impact of structure and conduct on product

price, costs and the volume and quality of output (Cramers and Jensen, 1982). If the market

structure in an industry resembles monopoly rather than pure competition, then one expect

poor market performance.

As a method for analysis the SCP paradigm postulates that the relationship exists between

the three levels distinguished. Suppose a causal relations starting from the structure, which

determine the conduct, which together determine the performance (technological

progressiveness, growth orientation of marketing firms, efficiency of resource use, and

product improvement and maximum market services at the least possible cost) of

agricultural marketing system in developing countries (Meijer, 1994). Market performance

can be measured by marketing costs and margins and marketing efficiency.

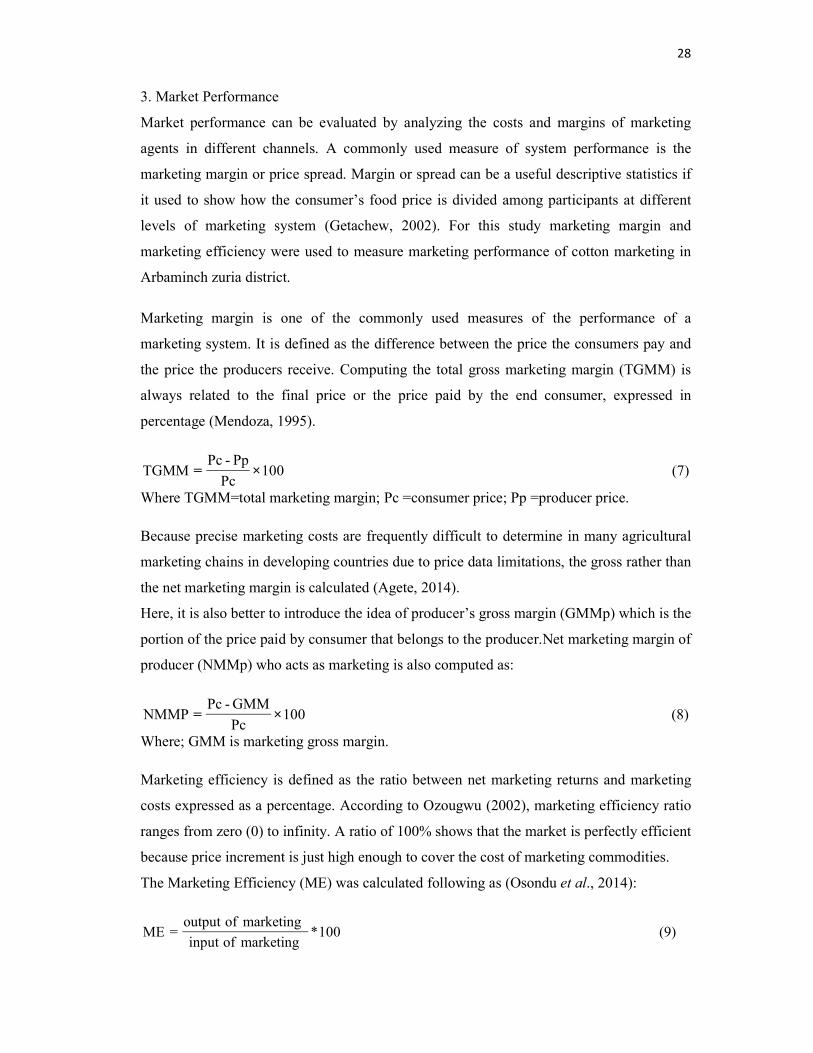

1. Marketing costs and margins

A marketing margin may be defined as a difference between the price paid by consumers

and that obtained by producers or; the price of a collection of marketing services that is, the

outcome of the demand for and the supply of each service (Tomek and Robinson, 1990).

The relative share of the different market participants will be estimated using the marketing

margin analysis. The total marketing margin in the marketing system constitutes the

marketing costs plus profit earned by the different participants in the system.

17

100price Selling

price purchasingprice SellingMM

Where MM=marketing margin.

Marketing cost is measured by cost of resources used in providing marketing services.

Hence it is the current expenses incurred in the performance of the marketing functions as a

commodity moves from the importers to the ultimate consumers. It includes the costs of

transportation, marketing charges, costs of loading/offloading and storage. The marketing

inputs are the costs of providing marketing services while the outputs are the benefits or

satisfaction created or value added to the commodity as it passes through the marketing

system.

2. Marketing efficiency

Marketing efficiency is defined as the ratio between net marketing returns and marketing

costs expressed as a percentage (Osondu et al., 2014). According to Ozougwu (2002),

marketing efficiency ratio ranges from zero (0) to infinity. A ratio of 100% shows that the

market is perfectly efficient because price increment is just high enough to cover the cost of

marketing.

For cotton marketing in Arbaminch district, Marketing Efficiency (ME) was calculated by

adopting Osondu et al., (2014) and Olukosi and Isitor, (1990) procedures as follows:

100*marketing of input

marketing of output=ME

2.6. Empirical Studies

According to Dawit (2005) the flow of agricultural produce from the producer to the

consumer goes along chain of intermediaries, who, without creating value-added, but keeps

on stretching the chain. He also explained that the involvement of these superfluous

intermediaries has constrained the development of the sector and derived the farmers of

equitable returns.

Rehima (2007) adopted Tobit model to identified factors that affect market supply of

pepper at Halaba special Woreda and Silti zone of South Nations, Nationalities Peoples

Regional State. The study result shows that market distance, quantity of pepper produced,

18

frequency of contacts with extension agents and access to market information influenced

market supply of pepper. All variables were influenced market supply of pepper positively,

while distance to market influenced market supply of pepper negatively.

Bosena (2008) adopted multiple regression model to identify major factors affecting farm

level market supply of cotton at Metema district of Amhara region. The results obtained

from this analysis indicated that number of oxen owned by household, land allocated for

cotton in hectare, the productivity of cotton per hectare, and access to credit for cotton were

significant factors affecting farm level cotton market supply.

Marshal (2011) conducted Value Chain Analysis of Sugarcane research identified different

inefficiencies regarding input usage and production of sugarcane. First, education level of

producers is low. Second, small scale and subsistent farming because of small land area

possession. Third, there was water shortage because of poor coordination. Fourth, farmers

continue to use low yielding unimproved seed cane varieties. Fifth, farmers could not

afford to use fertilizers and pesticides. Sixth, there is a limited credit access. Seventh, the

extension service given is minimal. Finally, the cooperative activity is weak. Marshal

employed multiple regression model for the research to identify factors affecting

marketable sugarcane supply. This research results revealed that marketable supply is

significantly affected by yield, education, lagged price, access to credit, farm size, delay

(quality) and the number of successive harvest.

Bosena et al. (2011) used multiple regression model to identify factors affecting marketable

supply of cotton at Metema district of Amhara region. This research result revealed that

from hypnotized variables only three variables affected marketable supply of cotton at farm

level at Metema district of Amhara region. Namely productivity of cotton, land allocated to

cotton production and access to credit were affected marketable supply of cotton positively.

Zekarias et al. (2012) used multiple regression model to identify determinants of forest

coffee supply in south western Ethiopia. Result from market structure analysis revealed that

producers, assemblers and wholesalers are the major actors involved in the market chain of

coffee.

Wendmagegn (2014) adopted multiple linear regression model for study conducted on

market chain analysis of coffee in dale district of southern Ethiopia, to identify factors

affecting coffee market supply. Wendmagegn’s study revealed that eight variables namely

19

sex of the household head, education level of household head, quantity of coffee produced,

access to extension service, price of coffee in 2011/12, distance to the nearest market, non-

farm income and access to market information were found to be the significant factors

affecting the market supply of coffee at household level. He also further categorized factors

which affected coffee marketable supply in to two namely positive factor and negative

factor. Based on his study Sex of the household head, education level of the household

head, quantity of coffee produced, access to extension service, price of coffee in 2011/12,

and access to market information influenced market supply of coffee positively while

distance to the nearest market and non-farm income were found to have a significant

negative effect on coffee market supply.

Gashahun (2015) conducted research on white pea bean value chain analysis at Adami Tulu

Jido Kombolcha District of Eastern Shewa zone of Oromia region and comes up with

weakness of value chain actors. Gashahun’s white pea bean value chain analysis research

revealed with; vertical linkage between farmers with wholesalers is observed to be weak.

There is no transparency and farmers get biased price information from wholesalers

through their brokers. The linkage between farmers with primary cooperatives is also weak,

primary cooperatives are not performing based on their motto, the organizational structures

of primary cooperatives were observed to be very weak and fragile. There was no

meaningful vertical integration between exporters, wholesalers and farmers at all. Also

Gashahun had employed multiple linear regression model to analyze factors affecting yield

of white haricot bean and five variables were found to affect significantly. Namely; Age of

household head affected negatively, the rest variables livestock, household head education,

use of fertilizer and extension contact affected marketed supply affected positively.

Yimer (2015) used Linear multiple Regression model to identify factors affecting

marketable supply of fruits. The analysis result of this research revealed that five variables

were significantly affected the marketable supply of fruit at household level. Namely

quantity of fruit produce, education level of the household head, market information,

distance to the market, and extension service are variable that significantly influence the

marketable supply of fruits by household.

From these studies, one can conclude that most of the characteristics of value chain actors

as well as factors that affect the marketable supply of commodity differ from commodity to

commodity. Difference in the marketing system of these commodities, type of commodities

20

and location of the study area may result differences in factors affecting market supply of

the commodities. Hence, it is important to conducting value chain and market structure

conduct-performance consistent research to come up with chain behavior and market SCP

to analyze factors affecting market supply of cotton.

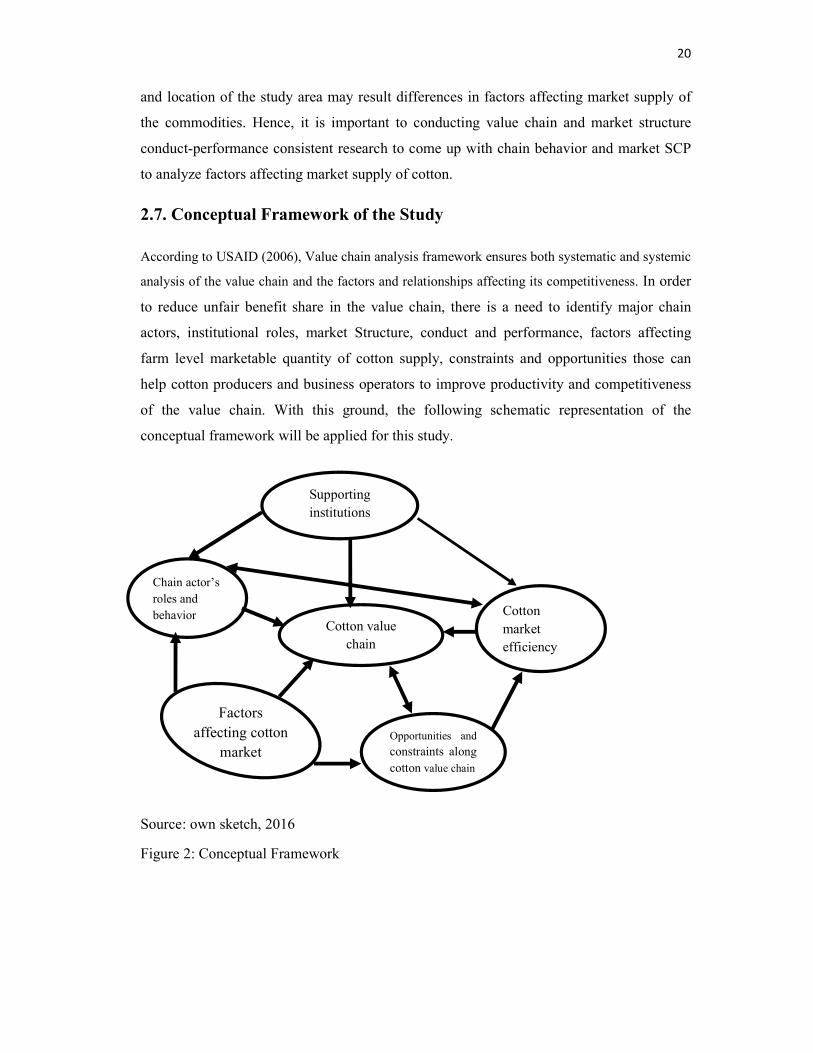

2.7. Conceptual Framework of the Study

According to USAID (2006), Value chain analysis framework ensures both systematic and systemic

analysis of the value chain and the factors and relationships affecting its competitiveness. In order

to reduce unfair benefit share in the value chain, there is a need to identify major chain

actors, institutional roles, market Structure, conduct and performance, factors affecting

farm level marketable quantity of cotton supply, constraints and opportunities those can

help cotton producers and business operators to improve productivity and competitiveness

of the value chain. With this ground, the following schematic representation of the

conceptual framework will be applied for this study.

Source: own sketch, 2016

Figure 2: Conceptual Framework

Supporting

institutions

Cotton

market

efficiency

Chain actor’s

roles and

behavior Cotton value

chain

Opportunities and

constraints along

cotton value chain

Factors

affecting cotton

market

21

3. RESEARCH METHODOLOGY

In this chapter description of study area, data types, data collection method, sampling

procedures and data analysis method are presented.

3.1. Description of the Study Area

Arbaminch zuria district is one of the districts found in Gamo Gofa zone of the Southern

Nation’s Nationalities and Peoples Regional State (SNNPRs). The District is located at a

distance of 275 and 505 km from the regional city, Hawassa and the country capital, Addis

Ababa, respectively. Geographically, the district is located between 5°42´ and 6°13´North

latitude and 37°19´ and 37°41´ East longitude. It is bordered on the south by the Dirashe

district (Segen Peoples zone), on the west by Bonke, on the north by Dita and Chencha, on

the northeast by Mirab Abaya district, and on the southeast by the Amaro district (Segen

Peoples zone). The district covers 1001 km² and has twenty nine rural kebeles and one

District town. Based on 2007 population census, Arbaminch zuria district had a total

population of 164,529 of whom 82,199 (49.9%) are men and 82,330 (50.1%) are women

(CSA, 2007).

The population density of the study area varies from172 person/km2 to 2268 person/km2.

The mean monthly maximum and minimum temperature of the study area ranges between

33.8°C in February to 28.1°C in July and 18.2°C in April to 15.3°C in December. The

mean annual total rainfall of the study area is about 963.3 mm with two rainy seasons. The

main rainy season is March, April and May which have 172.35 mm and 129.13 mm mean

monthly rainfall in April and May, respectively. The second highest monthly rainfall is

recorded in September and October, 126.6 mm and 133.05 mm (WoANR, 2015).

The elevation of the study area ranges from 1200 meters above sea level around eastern

part to 3000 meter above sea level in north western part. Eastern part of the study area is

dominated by flat lying topography, while the northern and north western parts constitute

areas with high altitude (Mestewat, 2014).

On the basis of FAO (1984) soil classification system, the study area consists of seven soil

types. These are Xerosols, Vertisols, Fluvisols, Nitosols, Leptosols, Acrisols and

Solonchaks. The study area involves six major types of land use. These are settlement,

farmland, water bodies, forest, bush lands and bare lands. Farmland account about 46% of

22

the total area, including two private large farm lands (Amibara Agricultural development

plc and Lucy Agricultural development plc.) and farmers owned farm lands. The second

dominant land use is bush land area which accounts 34.1%, settlement areas account

12.5%, dense forest of the total area found around the two lakes accounts 5.7%, water

bodies accounts 0.85%, and bare lands account 0.85% found in different parts of the

district, which is left fallow (Mestewat, 2014).

Figure 3: Location of Arbaminch zuria district

3.2. Types of Data, Sources and Methods of Data Collection

Both primary and secondary data were used. The primary data were collected using semi-

structured questionnaires. To collect primary data from cotton producer farmers, enumerato

rs who speak local language (Gamogna) very well were hired and trained for data

collection. Data were collected under strict supervision of the researcher.

23

Secondary data were collected from different sources such as from district Agricultural and

Natural Resource Development Office reports, textile industry report, Gamo Gofa zone

Agricultural and Natural Resource Development department reports, Trade and Industry

Offices, bulletins and websites. Published and unpublished documents were reviewed to

secure relevant secondary information.

Quantitative and qualitative data were collected from respective sources and were used to

achieve the proposed objectives.

3.3. Sampling Procedures and Sample size

To draw representative sample respondents from those cotton value chain actors included in

the study; the following sampling method was employed.

3.3.1. Producer sampling

Two stage sampling procedure was employed to draw representative cotton producer

farmers. In the first stage, three kebeles were selected randomly from ten cotton producer

kebeles of the study district. In the second stage, households were selected randomly from

complete list of households of selected kebeles and sample size was determined according

to formula given by Yamane (1967) at 95% confidence interval with 9% precision level (e)

= 0.09

( ))1(

2eN+1

N=n

Where n: sample size for research use, N: total number of households of the Arbaminch

zuria district and e: designates precision level and ranges from 0.05 to 0.1. For this research

e=0.09 was taken as precision level. Because according to Meryem (2013). as ‘e’ gets

approaches to 0.05 the sample size gets larger and larger, as a result it becomes difficult to

manage. Sample size for each kebele was distributed based on proportional to size of total

households.

� =26931

1 + 26931 (0.09)�= 122.89 ≈ 123

24

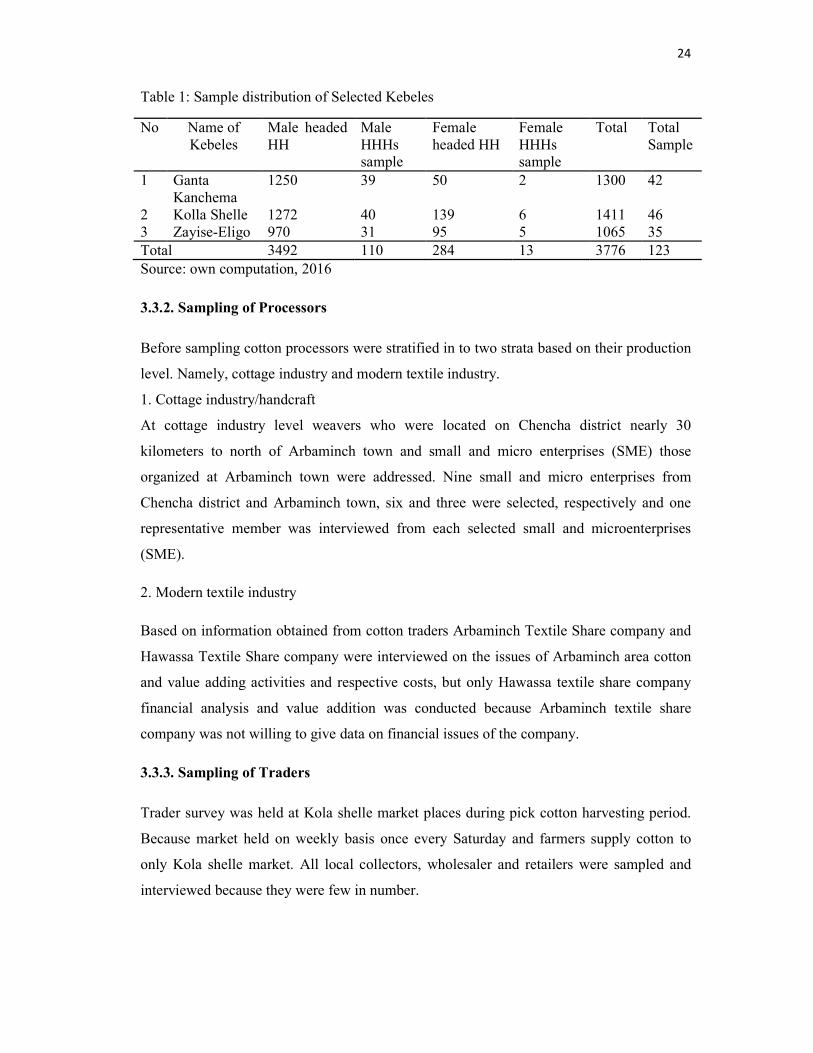

Table 1: Sample distribution of Selected Kebeles

No Name of Kebeles

Male headed HH

Male HHHs sample

Female headed HH

Female HHHs sample

Total Total Sample

1 Ganta Kanchema

1250 39 50 2 1300 42

2 Kolla Shelle 1272 40 139 6 1411 46 3 Zayise-Eligo 970 31 95 5 1065 35 Total 3492 110 284 13 3776 123 Source: own computation, 2016

3.3.2. Sampling of Processors

Before sampling cotton processors were stratified in to two strata based on their production

level. Namely, cottage industry and modern textile industry.

1. Cottage industry/handcraft

At cottage industry level weavers who were located on Chencha district nearly 30

kilometers to north of Arbaminch town and small and micro enterprises (SME) those

organized at Arbaminch town were addressed. Nine small and micro enterprises from

Chencha district and Arbaminch town, six and three were selected, respectively and one

representative member was interviewed from each selected small and microenterprises

(SME).

2. Modern textile industry

Based on information obtained from cotton traders Arbaminch Textile Share company and

Hawassa Textile Share company were interviewed on the issues of Arbaminch area cotton

and value adding activities and respective costs, but only Hawassa textile share company

financial analysis and value addition was conducted because Arbaminch textile share

company was not willing to give data on financial issues of the company.

3.3.3. Sampling of Traders

Trader survey was held at Kola shelle market places during pick cotton harvesting period.

Because market held on weekly basis once every Saturday and farmers supply cotton to

only Kola shelle market. All local collectors, wholesaler and retailers were sampled and

interviewed because they were few in number.

25

3.4. Methods of Data Analysis

Descriptive and econometric data analysis methods were used to analyze the data. Socio-

economic and demographic characteristics of value chain actors, value adding and market

structure- conduct- performance were analyzed using descriptive statistics. Econometric

model was used to analyze factors affecting quantity of cotton supplied to market.

3.4.1. Descriptive Data Analysis

This method of data analysis refers to the use of charts, ratios, percentages, means,

variances and standard deviations in the process of examining and describing socio-

economic and demographic characteristics of value chain actors, value adding activities,

chain actors’ roles and functions, marketing system and traders’ characteristics.

3.4.1.1. Value chain analysis

To come up with value chain analysis the following descriptive analysis were done:

1. Functional analysis and flow chart

Mapping the chain means giving a visual representation of the connections between actors

and tracing a product flow through an entire channel from the point of product concept to

the point of consumption(McCormick and Schmitz 2001; Kaplinsky and Morris 2002).

The starting point in value chain analysis is the so called chain mapping. To do so, the data

on all the involved agents, their activities, interactions among each other and flows of the

product through the production stages were identified and mapped.

According to FAO (2006a, b, and c), all the data sufficient for constructing the value chain

was presented in the form of a commodity flow chart. The flow chart visually highlights

interactions and flows between agents. It can also be a useful tool in achieving clarity in the

subsequent stages of analysis.

2. Financial analysis

Methods for analyzing the value chain aim basically at the analyses of the process of value

creation and income distribution (Rudenko, 2008).

According to FAO (2006b), methodology for analyzing the value chain includes financial

analysis and economic analysis. Financial analysis was used to determine the monetary

26

value added in the various segments of the chain actors. Total value added of the chain

represents all value created by all the agents of the chain.

(2) ∑VAagentsChain Added Value =

Value added: calculations carried out were in terms of the value created by individual

agents. If II is the value of intermediate inputs used and Y is the value of the output, then

the difference (Y-II) represents the value which the agent has added during the accounting

period to the value of the inputs in the process of production or processing. Value added

(VA) was defined by the equation and it was employed:

(3) II-YVA =

Value added measures the creation of wealth. At this stage, the calculation of value added

was carried out using market prices.

The financial profitability of activities in the chain was analyzed based on the agents’

activities, their economic results in the form of profits or losses.

)4( costs production Total

ProfitRR =

Where RR stands for Rate Return on the investment of cotton value chain.

3.4.1.2. Structure Conduct and Performance (S-C-P) model

1. Market structure

Market structure includes: a) the degree of buyer and seller concentration, defined by the

number of buyers and sellers in the market b) the degree of market transparency which

refers to the availability of relevant market information, its distribution among buyers and

sellers, and its adequacy in terms of price sharpening, quality comparisons and risk

reduction or uncertainty about the future. c) The condition of entry to the market referring

to the relative ease or difficulty with which seller may enter the market (Clodius and

Mueller, 1961). Market concentration can be measured by; concentration ratio, Gini-

coefficient and Hirschman Herfindahl index.

For this study only Hirschman Herfindahl index was used because unlike the four-firm

concentration ratio, the HHI reflects both the distribution of the market shares of the top

four firms and the composition of the market outside the top four firms. It also gives

27

proportionately greater weight to the market shares of the larger firms, in accord with their

relative importance in competitive interactions according to Wisdom et al. (2014).

Hirschman Herfindahl index is the sum of the squares of the market shares for each firm

within the industry and is always less than one. Market concentration is a function of the

number of firms in a market and their respective market shares.

HHI is calculated as:

∑=

=n

1i(5) 2

iMS HHI

Where: MSi: is the Market Share of seller i; and n: is the number of sellers in the market.

The market shares were calculated based on quantities of cotton handled by each seller as

follows:

(6)

∑n

1iVi

ViMSi

=

=

Where; Vi is the quantity of cotton handled by seller i (in kg); and ΣVI is the total quantity

of cotton handled by sellers in the market (in kg).

Depending on value, we can talk about non-concentrated markets, moderately concentrated

markets and highly concentrated markets. For non concentrated markets, market power is

very limited, which is a characteristic of perfect competition that has a low degree of

product differentiation. Moderately concentrated markets are having a moderate market

power, which is a characteristic of monopolistic competition with a high degree of product

differentiation and loose oligopoly. Highly concentrated industries, such as tight oligopoly