Logistics Clusters: Prevalence and Impact by Liliana Rivera M.S. Environmental B.A. Economics, Universidad de Los Andes, Colombia, 2003 Economics, University of Maryland - Universidad de Los Andes, Colombia, 2004 M. Eng. Supply Chain Management and Logistics, MIT, 2010 Submitted to the Engineering Systems Division in partial fulfillment of the requirement for the degree of Doctor of Philosophy at the Massachusetts Institute of Technology June 2014 © Massachusetts Institute of Technology. All rights reserved Signature redacted Signature of Author............... .......................................................................................... Engineering Systems Division June1,2014 Certified b y Signature reaactea ...... ............................................................................. /V Yossi Sheffi Elis-/a Gra /Professor Engineering Systems and Civil and Environmental Engineering Thesis Supervisor Certified h Sianature redacted y ................ ..... ............... ........ ........ Karen Polenske Peter de Florez Professor of Regional Political Economy Department of Urban Studies and Planning ..................................................... Signature redacted y .............. Accepted by............. Si~ Lisa D'Ambrosio Research Scieptist, MIT AgeLab Qinature redacted ................................................................... ..... Roy Welsch Profe!or of Statistics and Management Science and Engineering Systems Signature redacted Richard Larson Mitsui Professor of Engineering Systems Chair, Engineering Systems Division Education Committee MASSACHUSETTS INS1fftE OF TECHNOLOGY JUN 19 2014 LIBRARIES

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Logistics Clusters: Prevalence and Impactby

Liliana Rivera

M.S. EnvironmentalB.A. Economics, Universidad de Los Andes, Colombia, 2003Economics, University of Maryland - Universidad de Los Andes, Colombia, 2004M. Eng. Supply Chain Management and Logistics, MIT, 2010

Submitted to the Engineering Systems Divisionin partial fulfillment of the requirement for the degree of

Doctor of Philosophy

at theMassachusetts Institute of Technology

June 2014© Massachusetts Institute of Technology. All rights reserved

Signature redactedSignature of Author............... ..........................................................................................

Engineering Systems DivisionJune1,2014

Certified by Signature reaactea...... .............................................................................

/V Yossi SheffiElis-/a Gra /Professor Engineering Systems and Civil and Environmental Engineering

Thesis Supervisor

Certified h Sianature redactedy ................ ..... ... ..... .. .. ........... ........

Karen PolenskePeter de Florez Professor of Regional Political Economy Department of Urban Studies and Planning

..................................................... Signature redacted

y ..............

Accepted by.............

Si~

Lisa D'AmbrosioResearch Scieptist, MIT AgeLab

Qinature redacted................................................................... .....Roy Welsch

Profe!or of Statistics and Management Science and Engineering Systems

Signature redactedRichard Larson

Mitsui Professor of Engineering SystemsChair, Engineering Systems Division Education Committee

MASSACHUSETTS INS1fftEOF TECHNOLOGY

JUN 19 2014

LIBRARIES

2

Logistics Clusters: Prevalence and Impact

by

Liliana Rivera

Submitted to the Engineering Systems Divisionin partial fulfillment of the requirement for the degree of

Doctor of Philosophy

Abstract

Governments around the world are investing significant resources in the development and expansion oflogistics clusters. This dissertation analyzes the cluster phenomenon focusing on four topics. First, itdevelops a methodology to identify clusters and applies it to the context of the US. By analyzing the caseof logistics clusters, this thesis contributes to a more general debate in the industrial clusters literature:while many authors see industrial clusters growing, others see them dispersing. Evidence of increasingconcentration of the logistics industry in clusters in the US over time is tested and documented. Inaddition, some evidence that logistics activities in counties inside clusters show higher growth than incounties outside clusters is found.

Second, this thesis studies the relationship between freight accessibility and logistics employment in theUS. It develops an accessibility measure based on a gravity model, focusing on four different modes oftransportation: road, rail, air, and maritime. Using a Partial Least Squares model, these four differentfreight accessibility measures are combined into two constructs, continental and intercontinental freightaccessibility, and then analyzed against logistics employment. Results show that highly accessiblecounties attract more logistics employment than other counties. The analyses also show that it isimportant to control for the effect of population, since it explains the most variation in the logisticsemployment across counties.

Third, this dissertation also analyzes the benefits of logistics clusters, possibly explaining their continuousgrowth and wide popularity among both private agents and policy makers during the last decade. Usinginterview data and grounded theory, four major driving forces that may explain their growing presence areidentified: collaboration, value added services, upward mobility and job creation at different levels.

Finally, using a quantitative approach this thesis analyzes two major effects of agglomeration on firmslocated within logistics clusters: more collaboration and the provision of more value added services. Usingsurvey data and structural equation modeling these hypotheses are tested using information from theZaragoza (Spain) Logistics Cluster. The results show that companies located in logistics clusters docollaborate more and offer more value added services than companies that are not agglomerated.

Thesis Supervisor: Yossi SheffiTitle: Elisha Gray 11 Professor of Engineering Systems and Civil and Environmental Engineering

3

4

Acknowledgments

I want to thank my advisor Prof. Yossi Sheffi for his help and unlimited support over the last 4 years.Yossi's patience, feedback and confidence in me made this dissertation possible. I admire his endlesscreativity and his ability to always give the right advice.

I thank my committee members Karen Polenske, Lisa D'Ambrosio and Roy Welsch for their valuablecomments and suggestions. Karen reminded me that perseverance is a key part of a PhD and life ingeneral. Lisa was always there encouraging me to continue, and Roy asked questions that improved thequality of this thesis.

I also want to thank Fran Van den Heuvel and Jan Fransoo from Technische Universiteit Eindhoven.Frank was a visiting student at MIT-Center for Transportation and Logistics -CTL in the fall of 2011, weworked together during his stay in Cambridge. This enriching collaboration led to Chapter 2 of thisdissertation. Jan was a visiting Professor at CTL and his advice was key for me to get on track with mydissertation.

I am grateful to people at the CTL, especially to Edgar Blanco and Bruce Arntzen, who were my firstconnections to MIT. Edgar was also my thesis advisor during the Master is Supply Chain Management inmy first year at MIT. Their insight has always been valuable.

I benefited from conversations with Roberto Perez-Franco, about qualitative methods for research (andabout life); and with Basak Kalkaci, Shardul Phadnis and Tony Craig about the content and quality of myresearch.

I want to thank the Zaragoza Chamber of Commerce and Zaragoza Logistics Center for their invaluablehelp in conducting the survey for chapter 4.

Last but not least, I thank my family for their unconditional love and support. My parents who have alwaysbeen there for me (even from far away), my husband Andres who has always believed in me and madethis PhD journey possible, and my son Gabriel Emilio who literally gave me the last kicks I needed tofinish this dissertation.

S

6

Table of Contents

1. Introduction ................................................................................................................................. 131.1. W hy study logistics clusters?..................................................................................................... 131.2. Research questions..........................................................................................................................14

1.2.1. Agglom eration of logisticsfirms.......................................................................................... 141.2.2. Im pact of the agglom eration of logistics firm s............................................................. 15

1.3. Outline..................................................................................................................................................16

2. Logistics agglom eration in the US .................................................................................... 172.1. Introduction ....................................................................................................................................... 172.2. Industrial and Logistics Clusters............................................................................................ 182.3. Exploratory research ...................................................................................................................... 192.4. Identifying Clusters..........................................................................................................................212.5. M odel....................................................................................................................................................22

2.5.1. Data .................................................................................................................................................... 252.6. Results: Cluster Identification.................................................................................................. 26

2.6.1. Comparison of the results with those of other methods ............................................. 282.7. Results: Trends and Dynam ics............................................................................................... 30

3. Relationship between freight accessibility and logistics employment in UScounties ................................................................................................................................................. 33

3.1. Introduction ....................................................................................................................................... 333.2. Relationship between accessibility and employment ..................................................... 343.3. Accessibility m easures ................................................................................................................... 363.4. Freight accessibility measures for logistics establishments in the US....................... 37

3.4.1. Gravity-based accessibility m easures ............................................................................... 383.4.2. Road accessibility .......................................................................................................................... 383.4.3. Air, m aritim e, and rail accessibility.................................................................................. 39

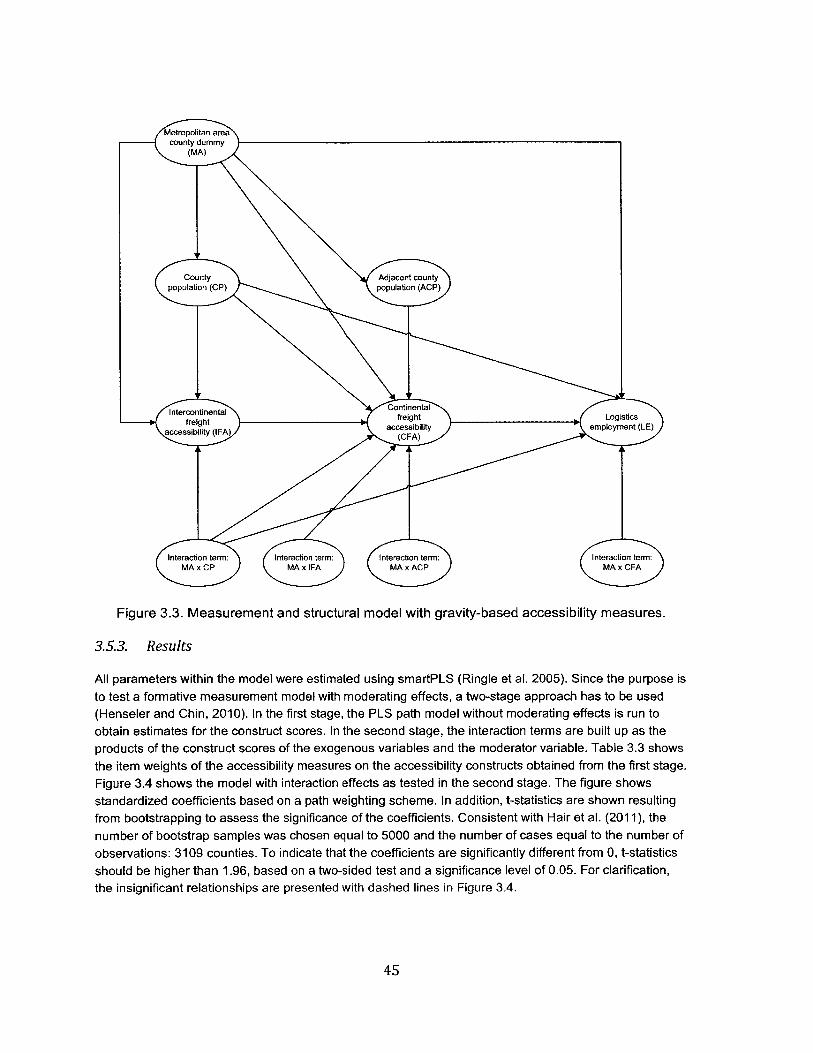

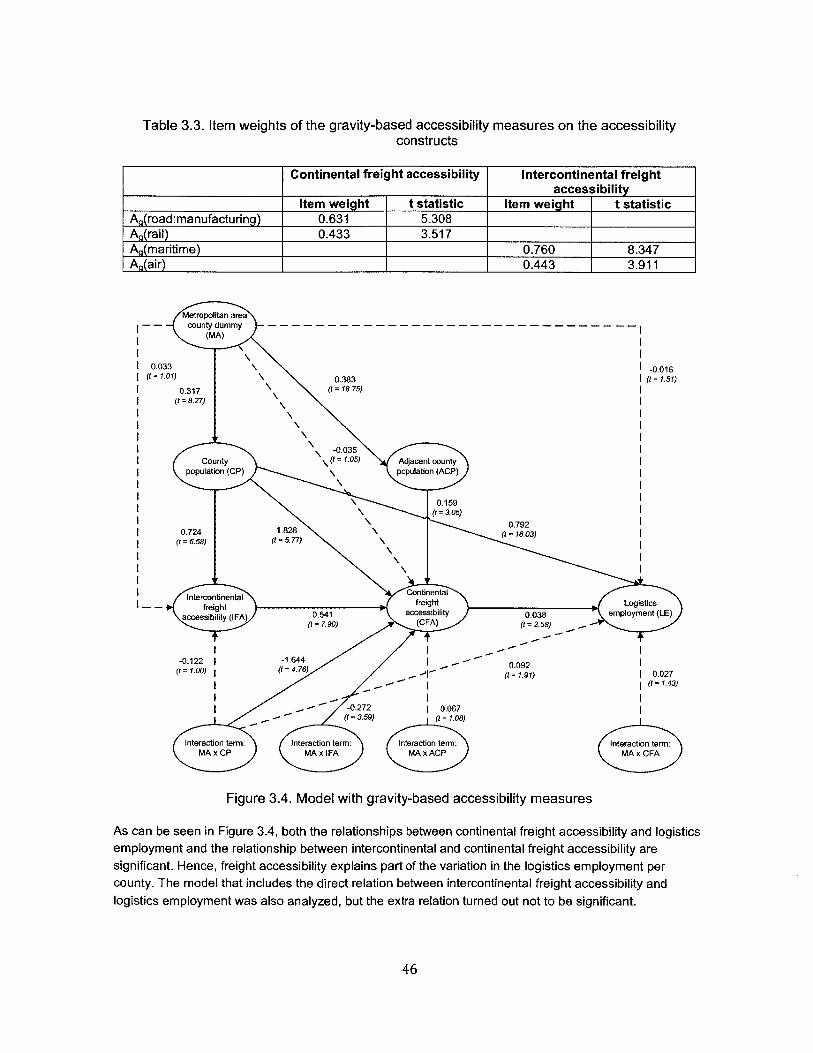

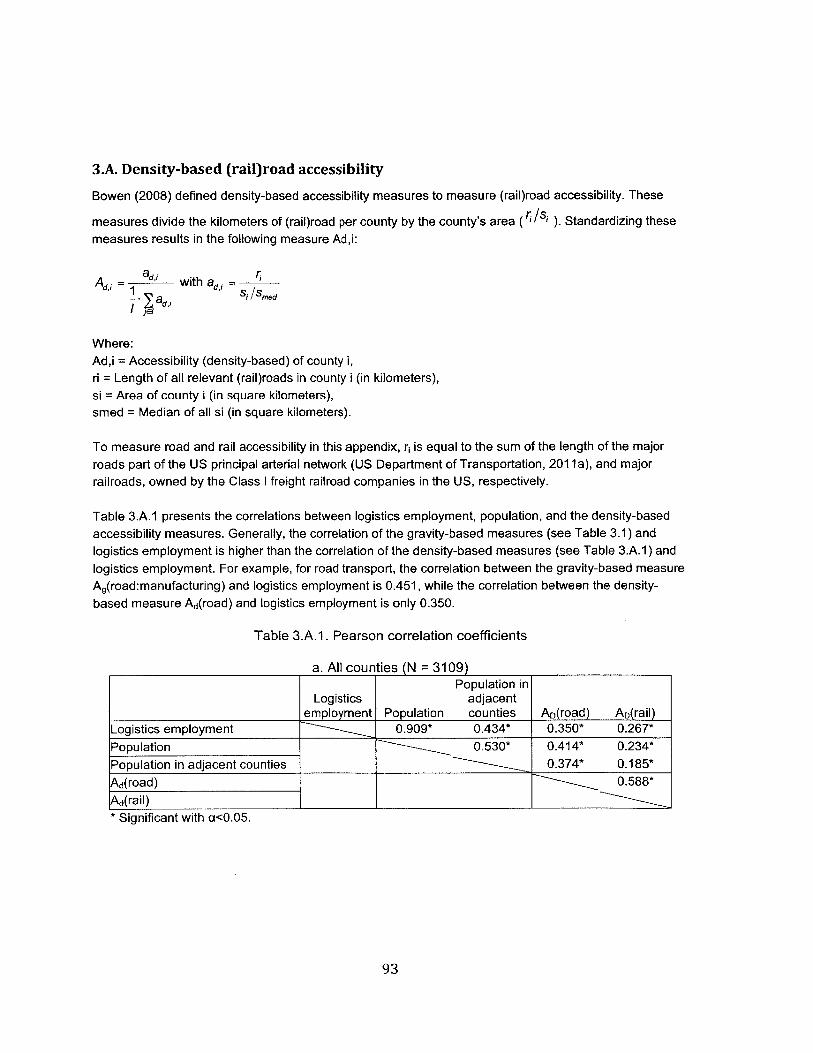

3.5. Accessibility of US counties and the relation to logistics.............................................. 403.5.1. M aterial used .................................................................................................................................. 403.5.2. M ethodology.................................................................................................................................... 433.5.3. Results................................................................................................................................................ 4 5

4. The benefits of logistics clusters....................................................................................... 494.1. Introduction ....................................................................................................................................... 494.2. Industrial Agglom eration Literature ..................................................................................... 50

4.2.1. Industrial clusters benefits......................................................................................................... 504.2.2. Logistics clusters............................................................................................................................ 514.2.3. Assum ptions ..................................................................................................................................... 52

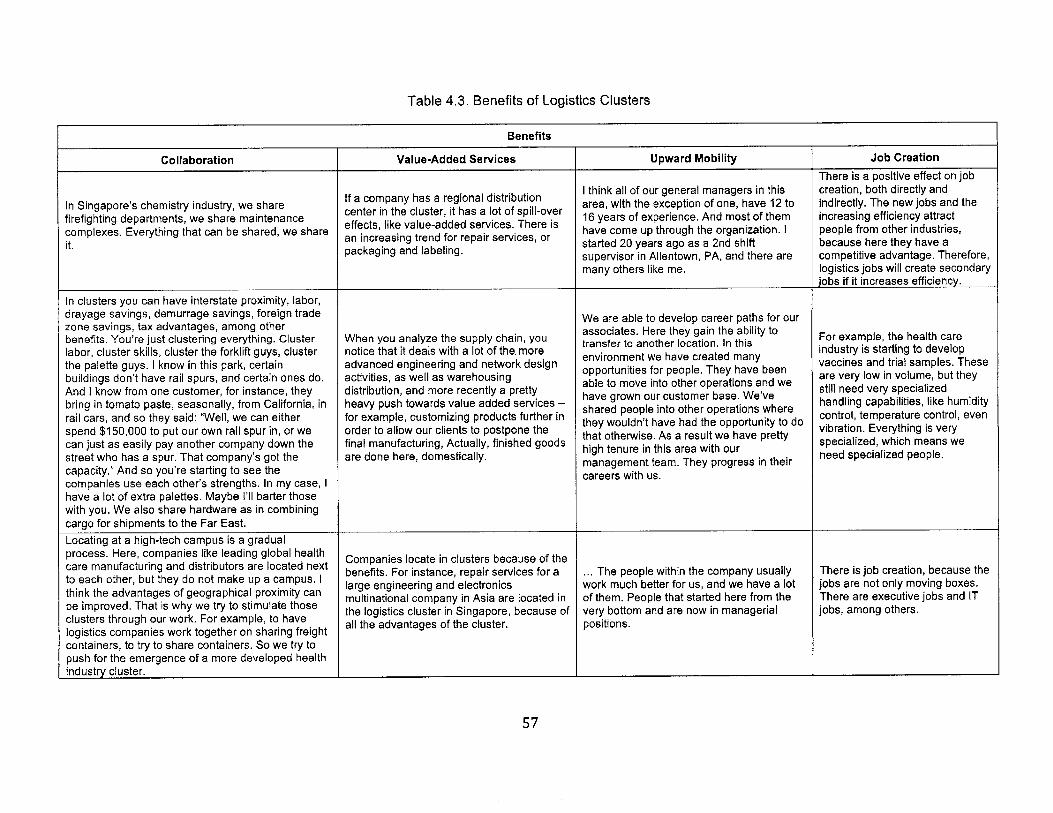

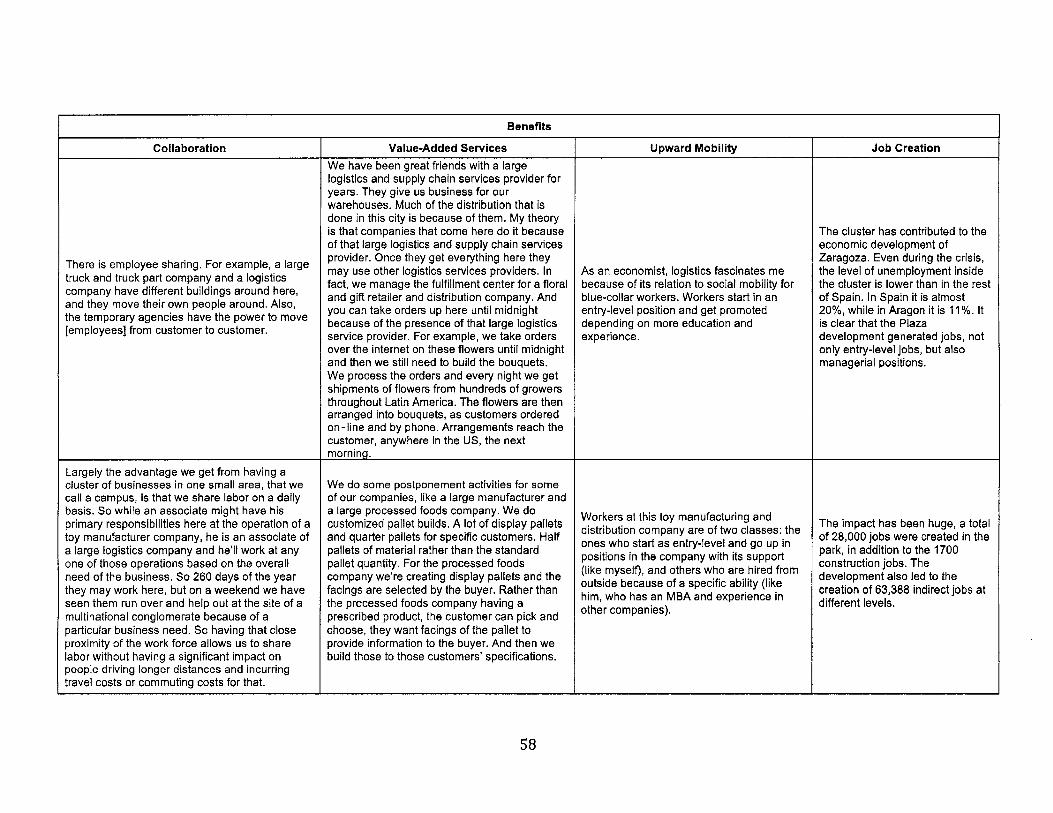

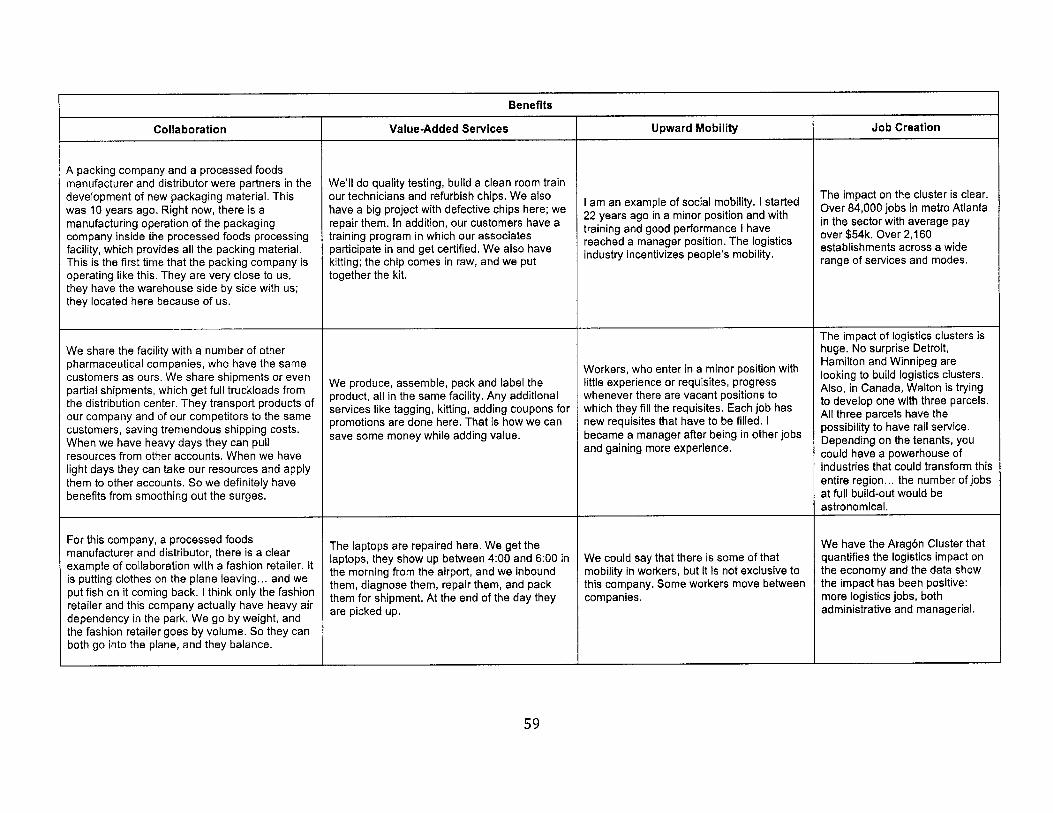

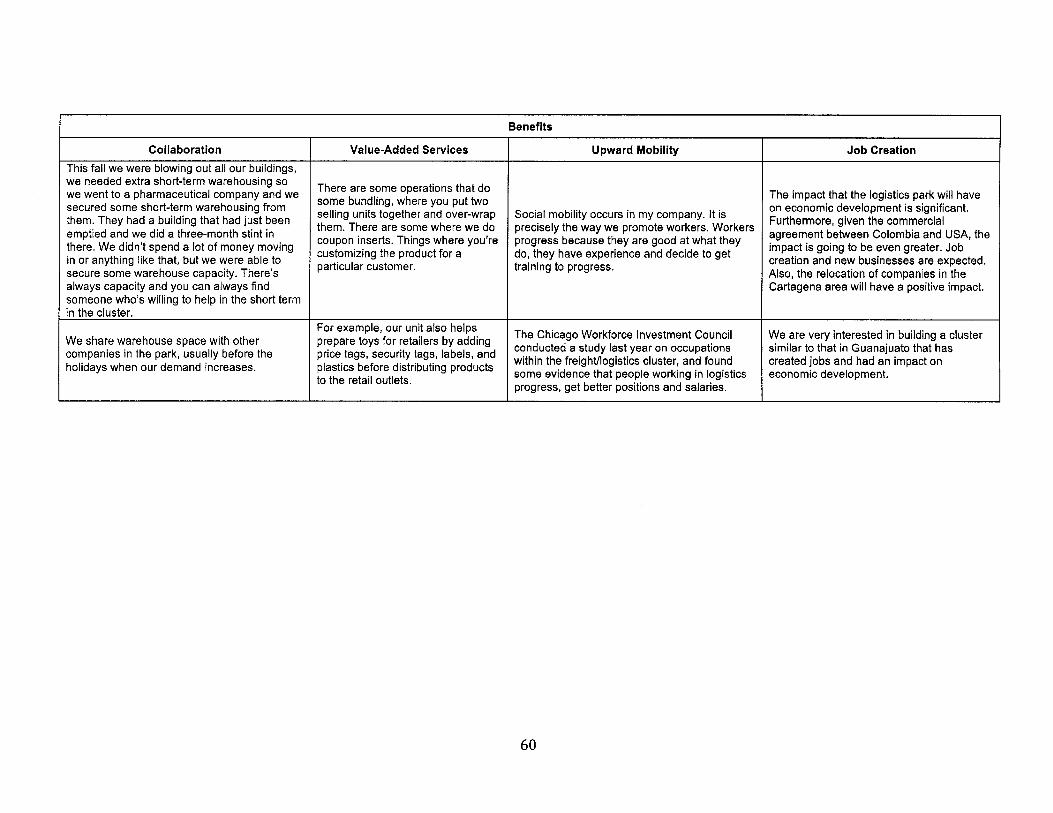

4.3. M ethods ............................................................................................................................................... 524.3.1. Sam ple ............................................................................................................................................... 524.3.2. Data collection................................................................................................................................ 554.3.3. Data analysis................................................................................................................................... 55

7

4.4. Results ................................................................................................................................................ 614.4.1. Operational advantages from collaboration ................................................................ 614.4.2. Value added services .................................................................................................................... 6 24.4.3. Upw ard m obility ............................................................................................................................ 624.4.4. Job grow th at m ultiple levels ............................................................................................. 63

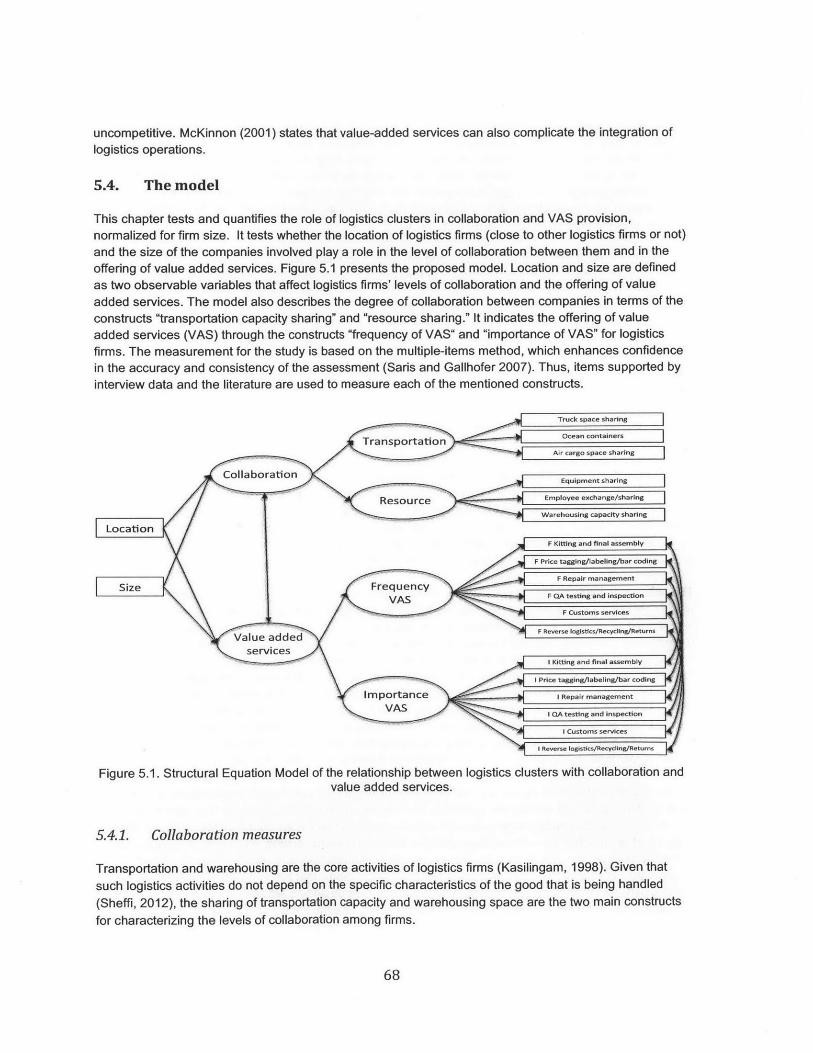

5. Impacts of agglomeration on logistics firms................................................................ 655.1. Introduction ....................................................................................................................................... 655.2. Collaboration and logistics clusters..................................................................................... 665.3. Value added services and logistics clusters ....................................................................... 675.4. The m odel ........................................................................................................................................... 68

5.4.1. Collaboration m easures.............................................................................................................. 685.4.2. Value added services m easures........................................................................................... 695.4.3. Impact of location and company size on collaboration and value added services70

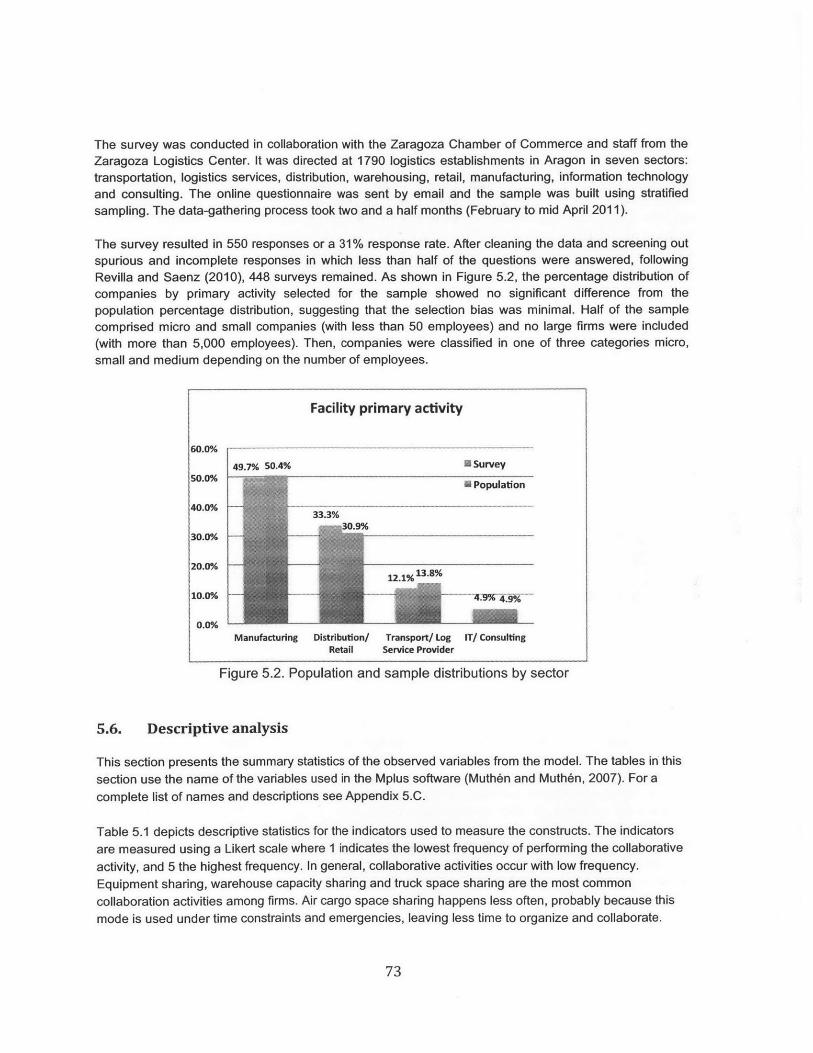

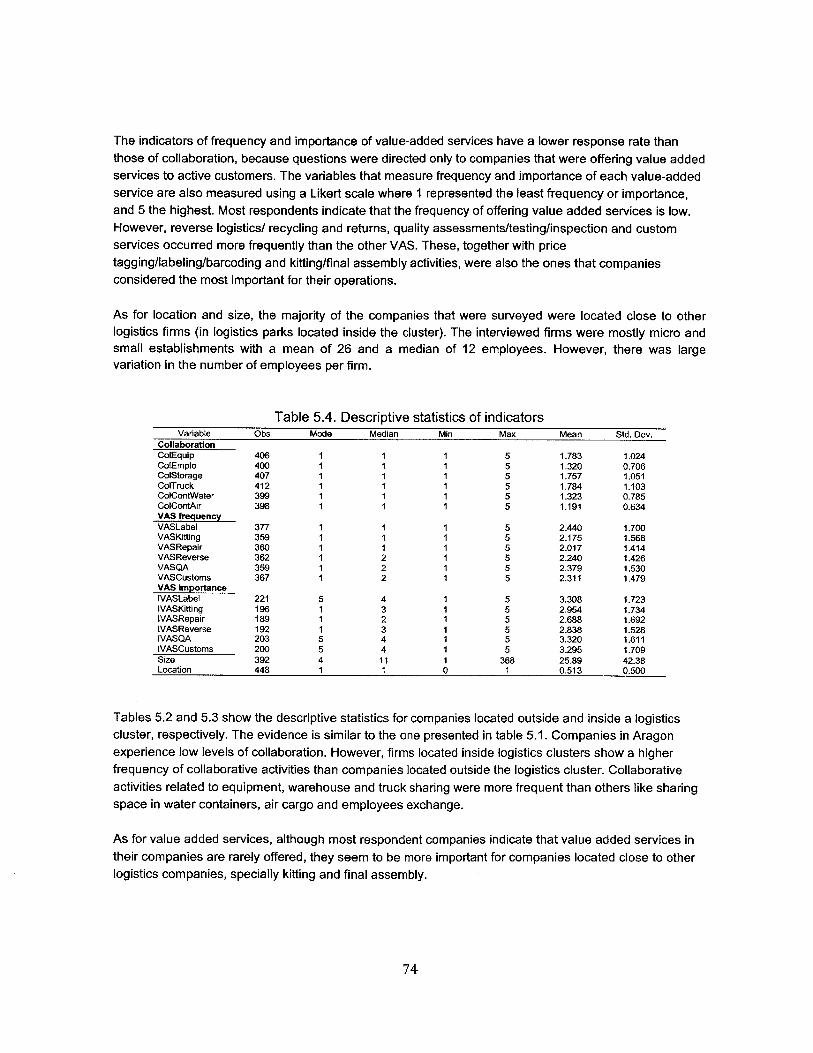

5.5. D ata collection...................................................................................................................................725.6. D escriptive analysis.........................................................................................................................735.7. M odel estim ation and results.................................................................................................. 78

6. Con clusions .................................................................................................................................. 8 16.1. Further research...............................................................................................................................82

R eferences......................................................................................................................................... 119

8

List of Figures

2.1 Determ ination of LEP Cutoff Value................................................................................................ 25

2.2. Number of logistics clusters considering different critical values, 2008.....................................26

2.3 U S Logistics Clusters 2008..................................................................................................................27

2.4 Logistics Clusters and Free Trade Zones in the US.........................................................................28

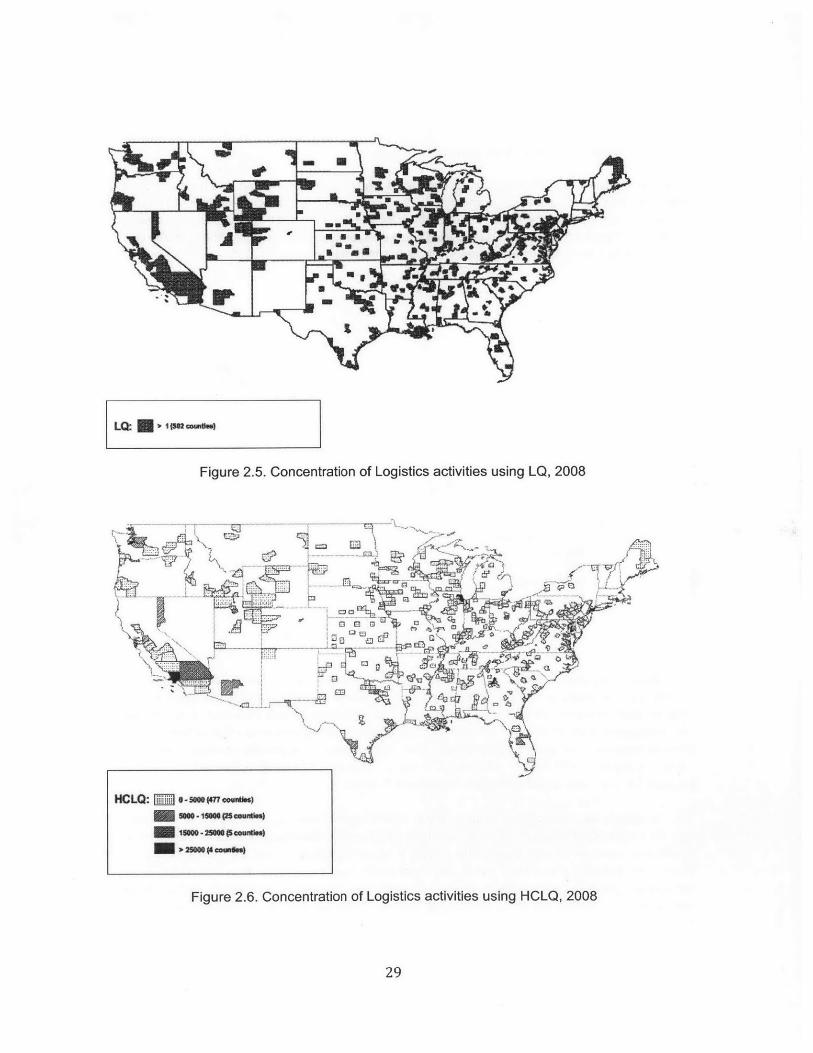

2.5. Concentration of Logistics activities using LQ, 2008...................................................................29

2.6. Concentration of Logistics activities using HCLQ, 2008.............................................................29

2.7. U S Logistics Clusters, 1998 ................................................................................................................. 30

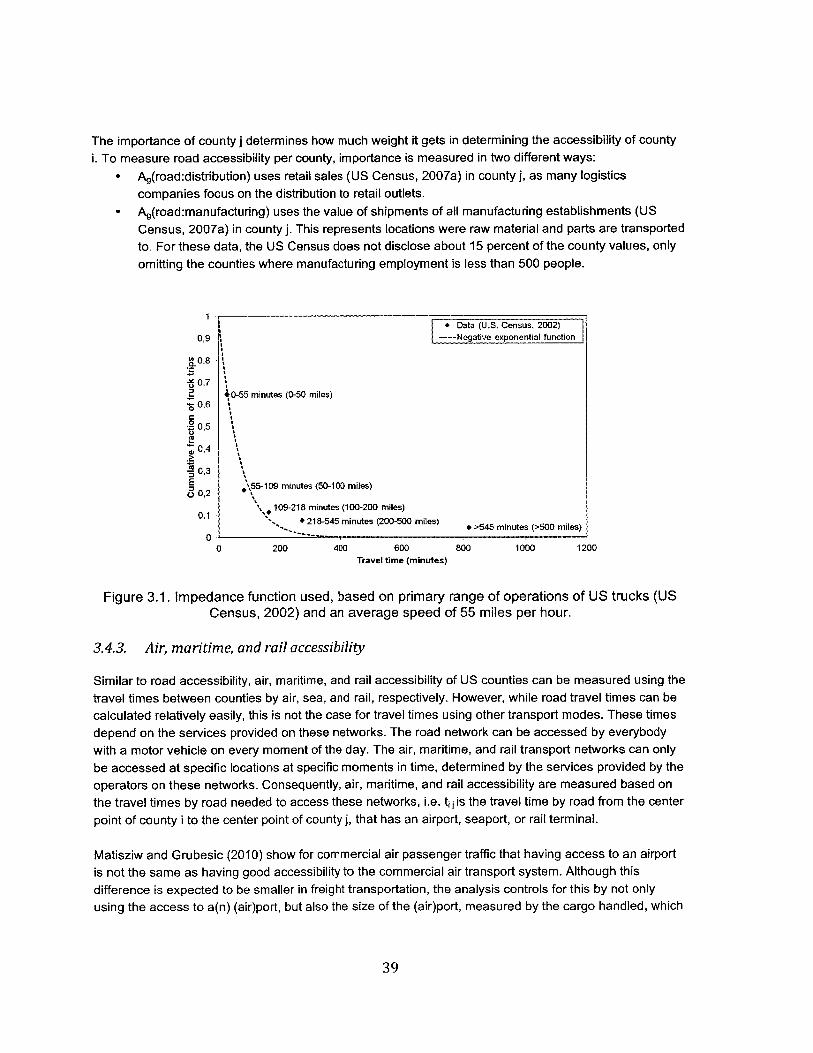

3.1. Impedance function used, based on primary range of operations of US trucks and an average

sp eed of 55 m iles p er hour........................................................................................................................39

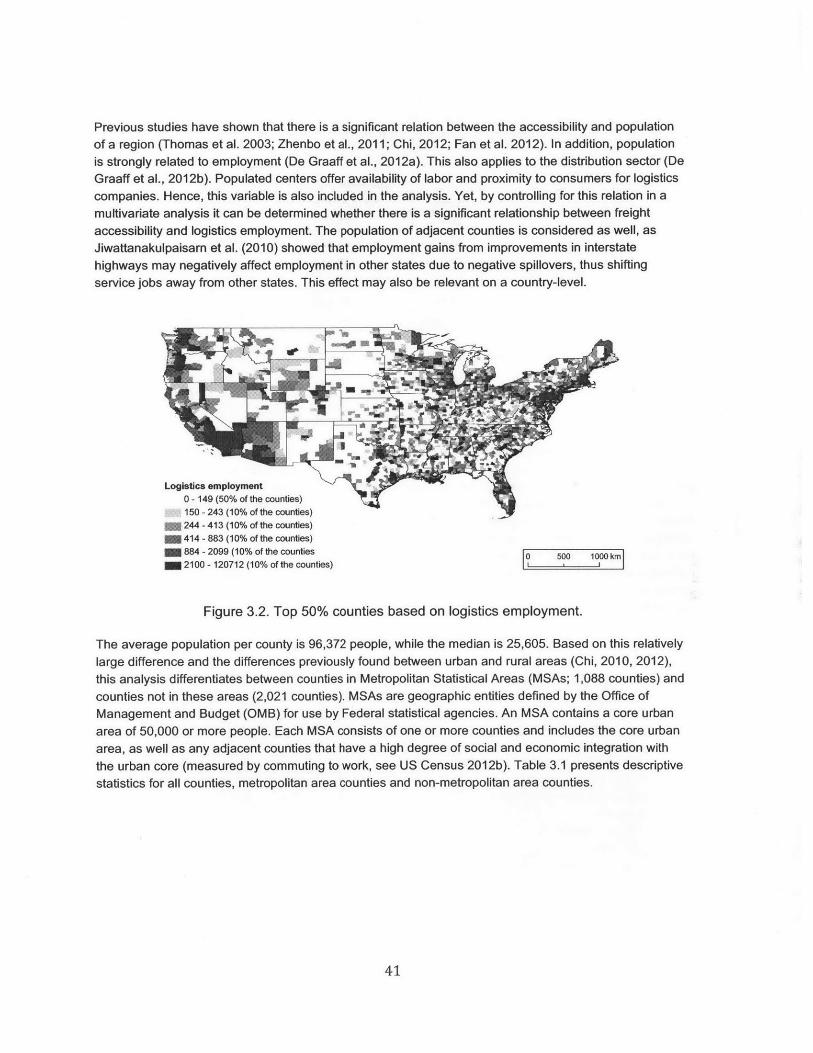

3.2. Top 50% counties based on logistics employment..........................................................................41

3.3. Measurement and structural model with gravity-based accessibility measures......................45

3.4. Model with gravity-based accessibility measures............................................................................46

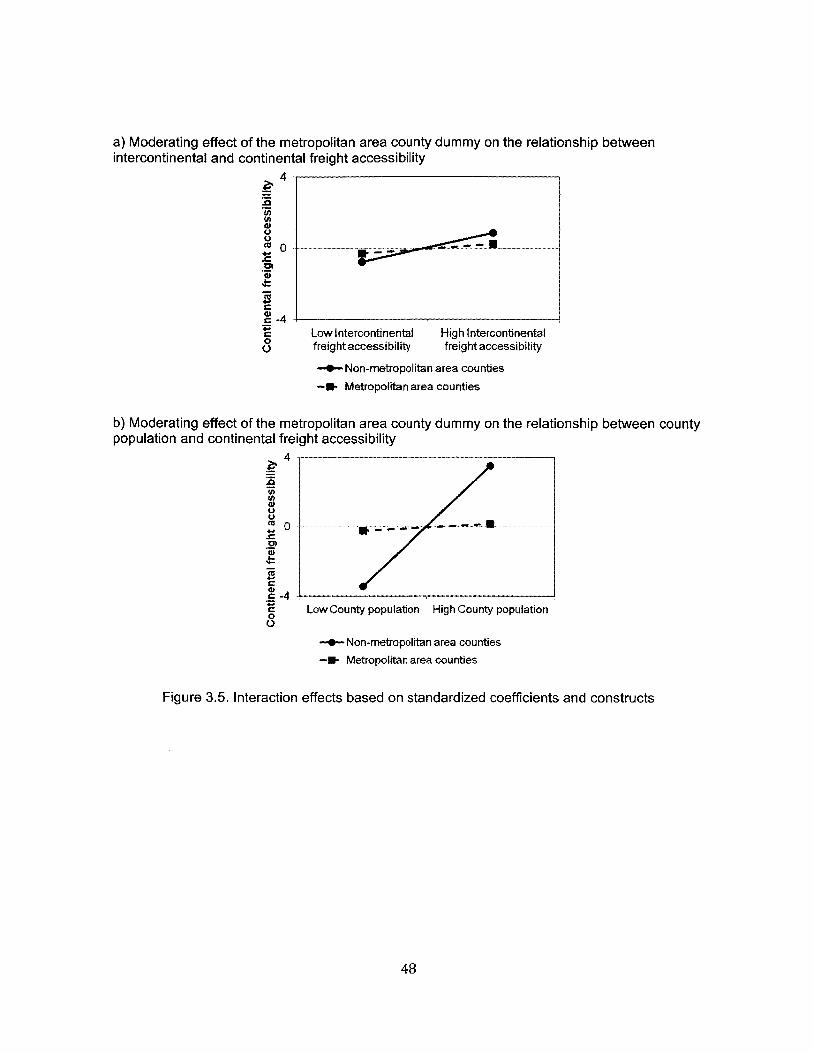

3.5. Interaction effects based on standardized coefficients and constructs.....................................48

5.1. Structural Equation Model of the relationship between logistics clusters with collaboration and

valu e added services.............................................................................................................. ................ 68

5.2. Population and sample distributions by sector............................................................................73

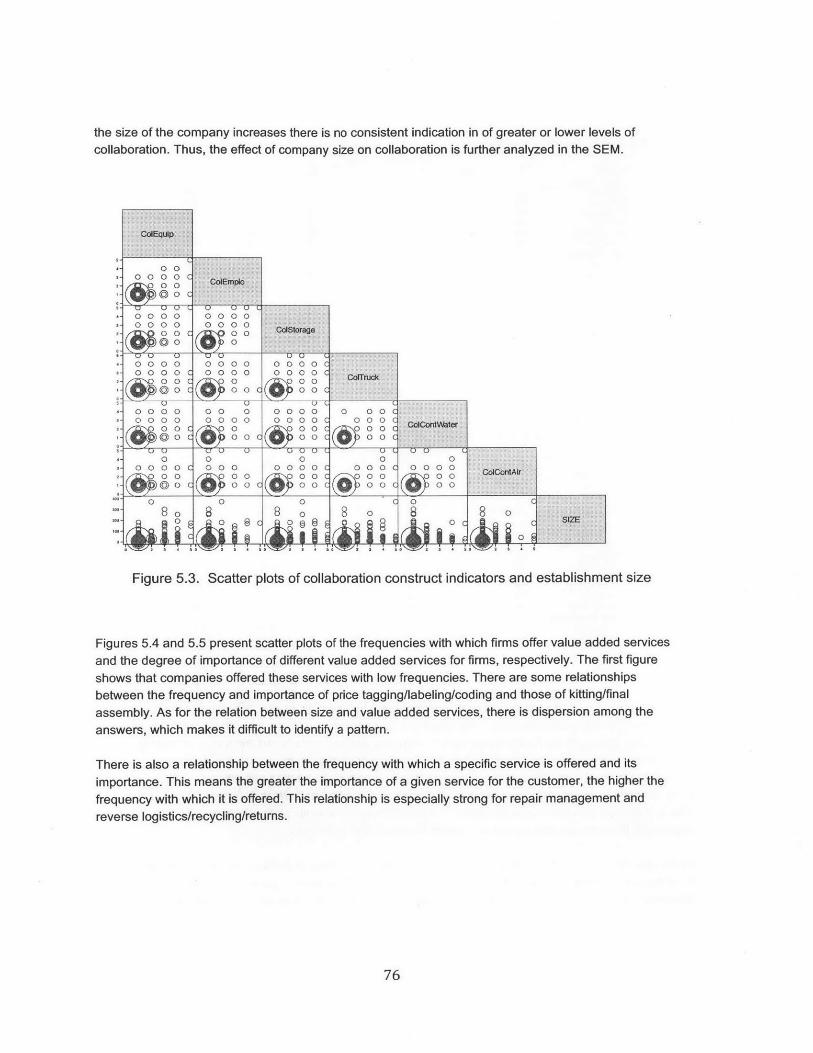

5.3. Scatter plots of collaboration construct indicators and establishment size............................76

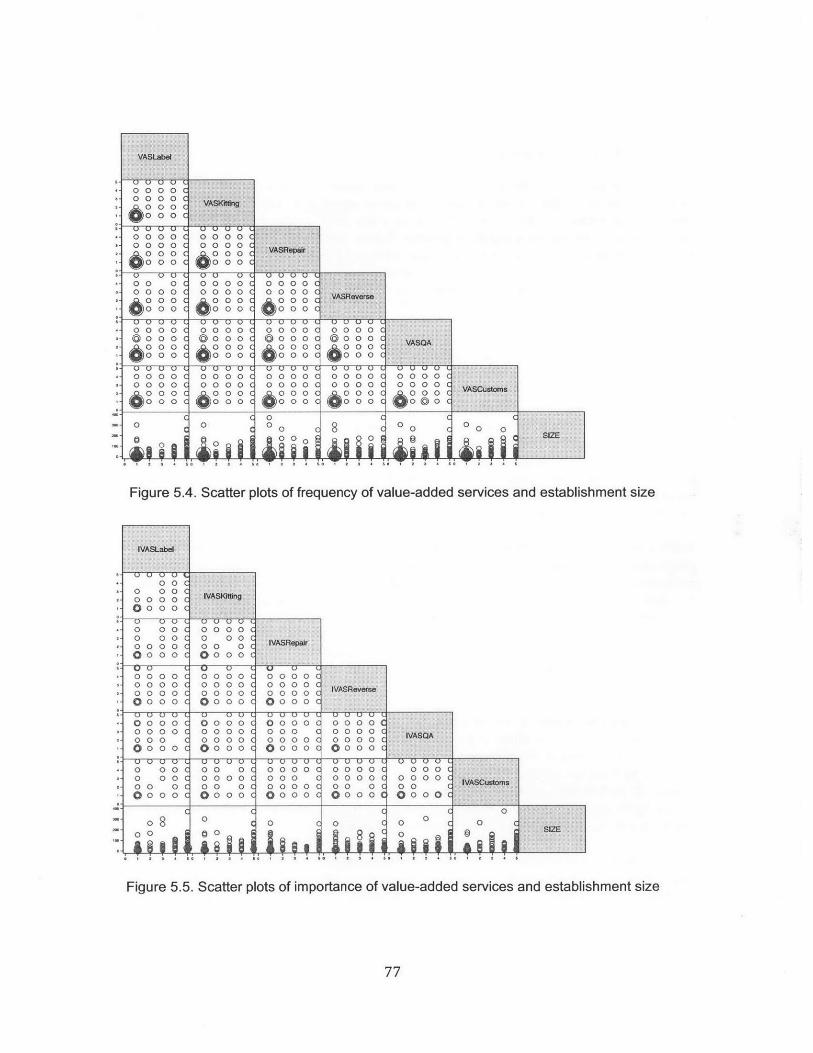

5.4. Scatter plots of frequency of value-added services and establishment size................................77

5.5. Scatter plots of importance of value-added services and establishment size............................77

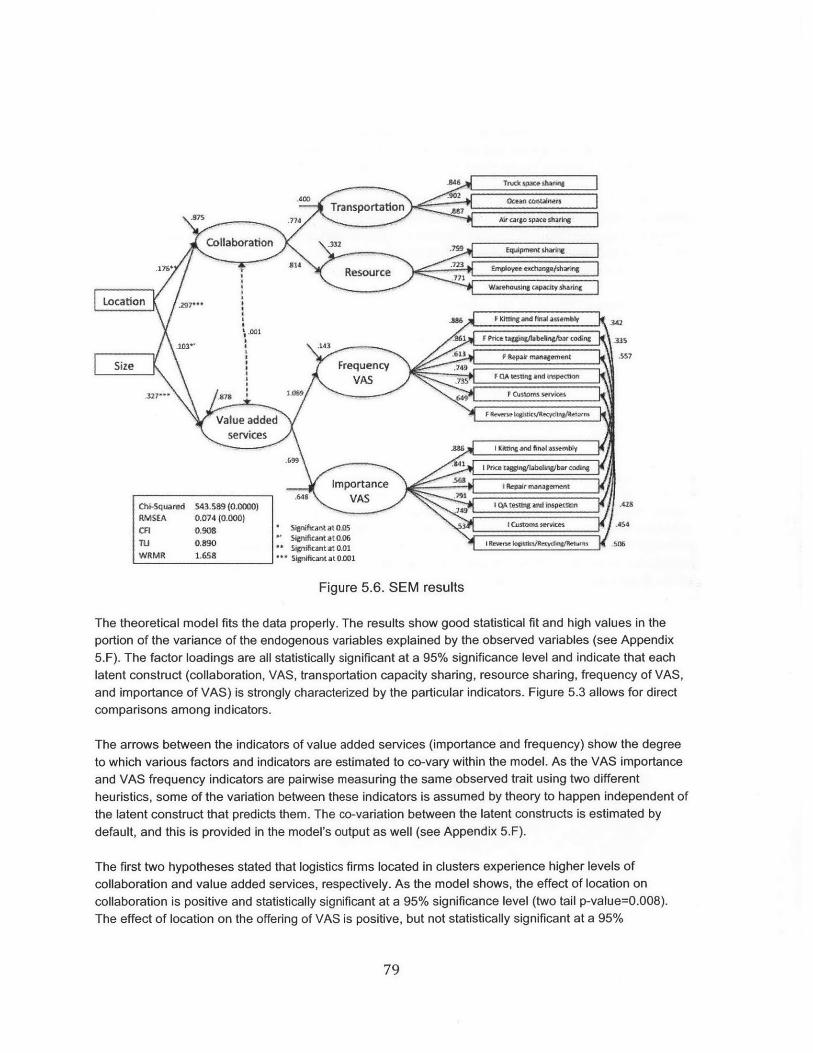

5.6. SEM results...................................................................................... ............ ... --....................------ 79

9

10

List of Tables

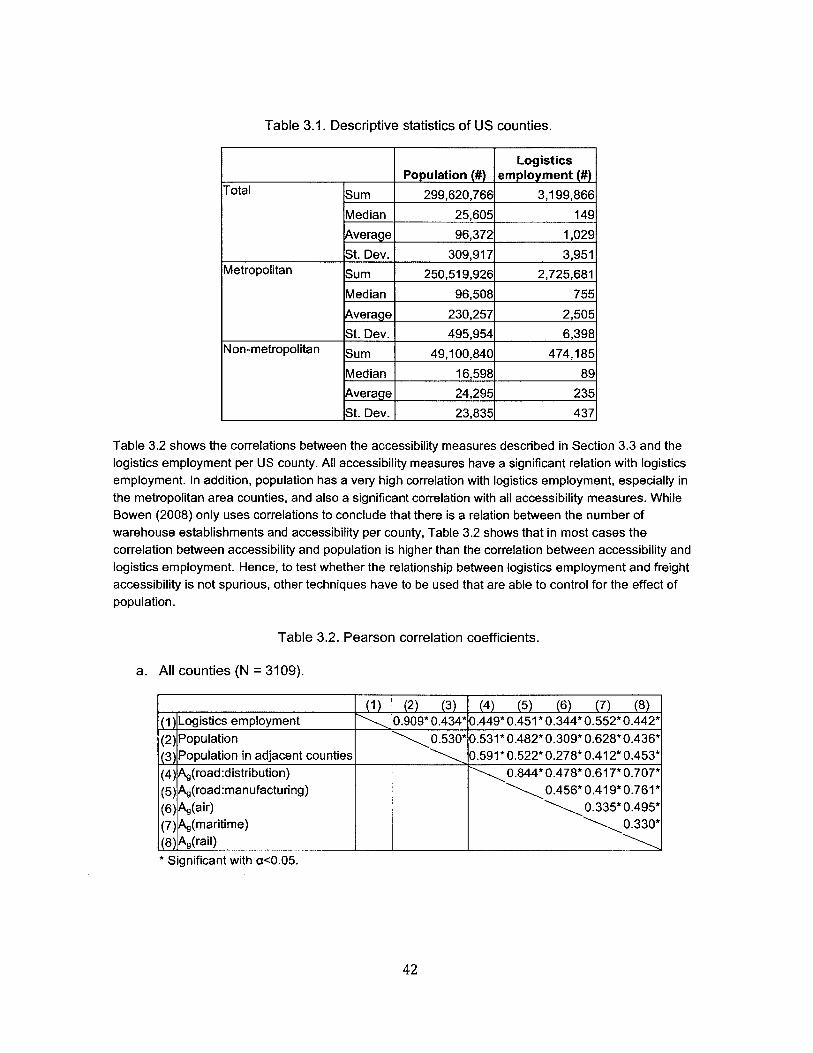

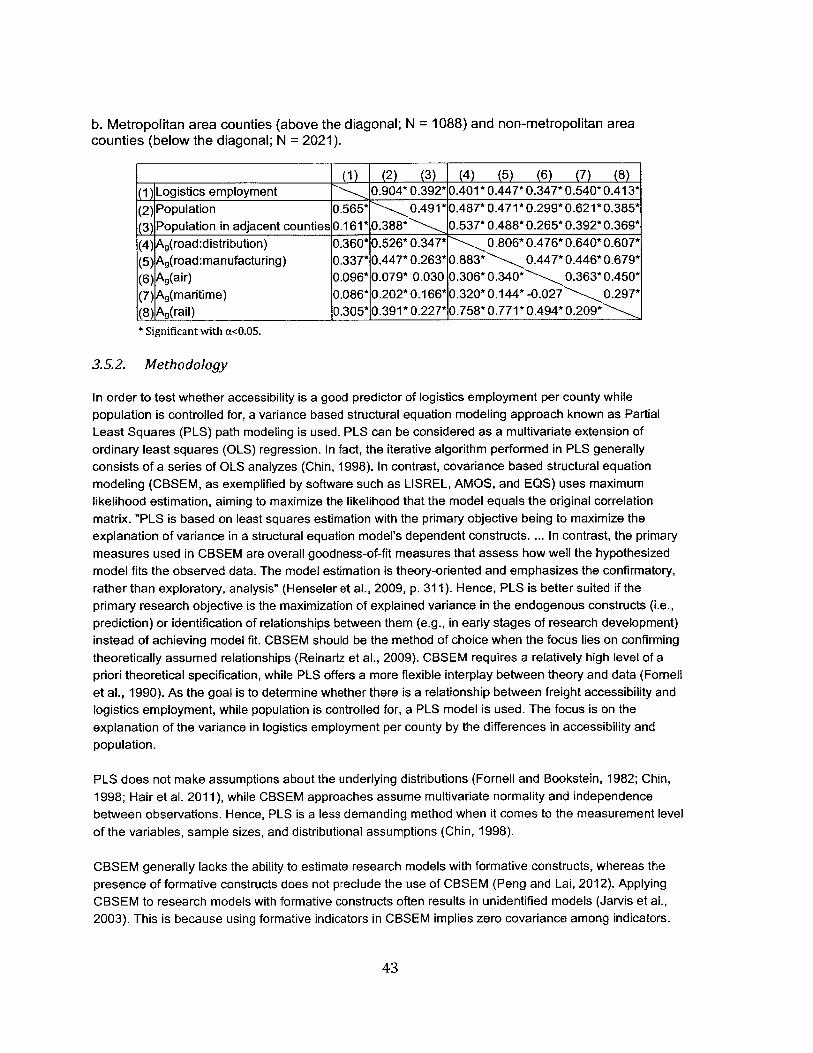

3.1. Descriptive statistics of US counties............................................................................................. 42

3.2. Pearson correlation coefficients.................................................................................................... 42

3.3. Item weights of the gravity-based accessibility measures on the accessibilityconstructs............................................................................................................................................................46

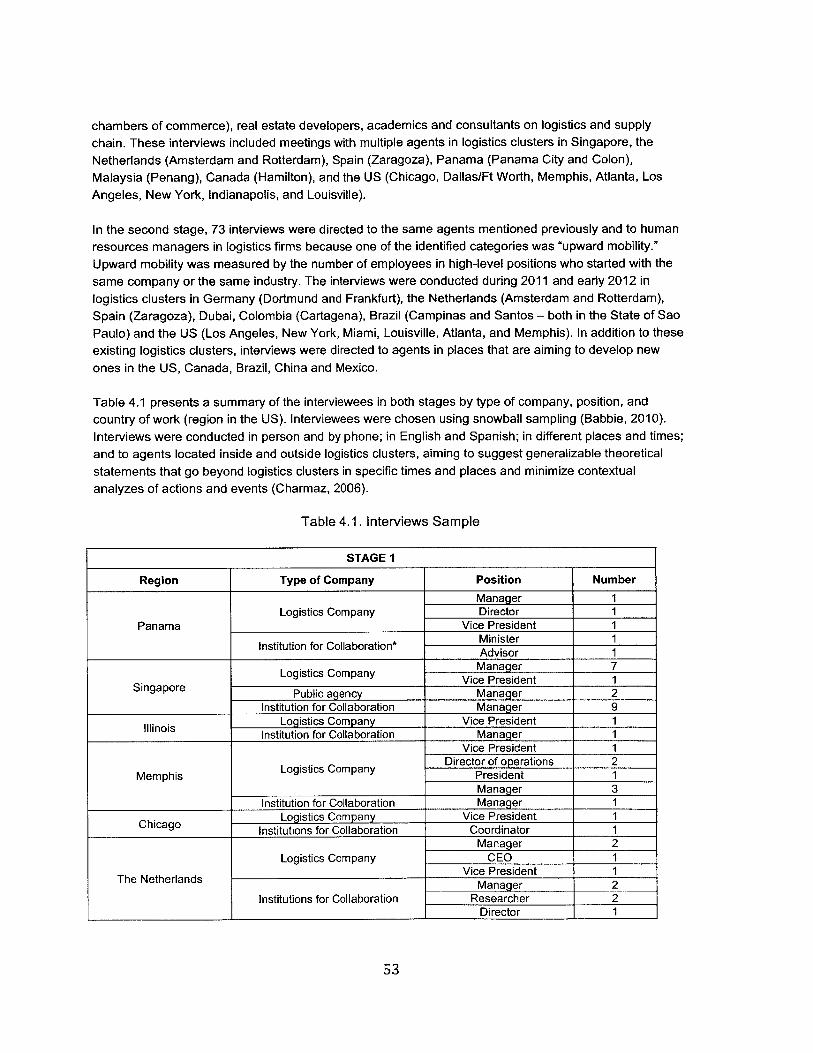

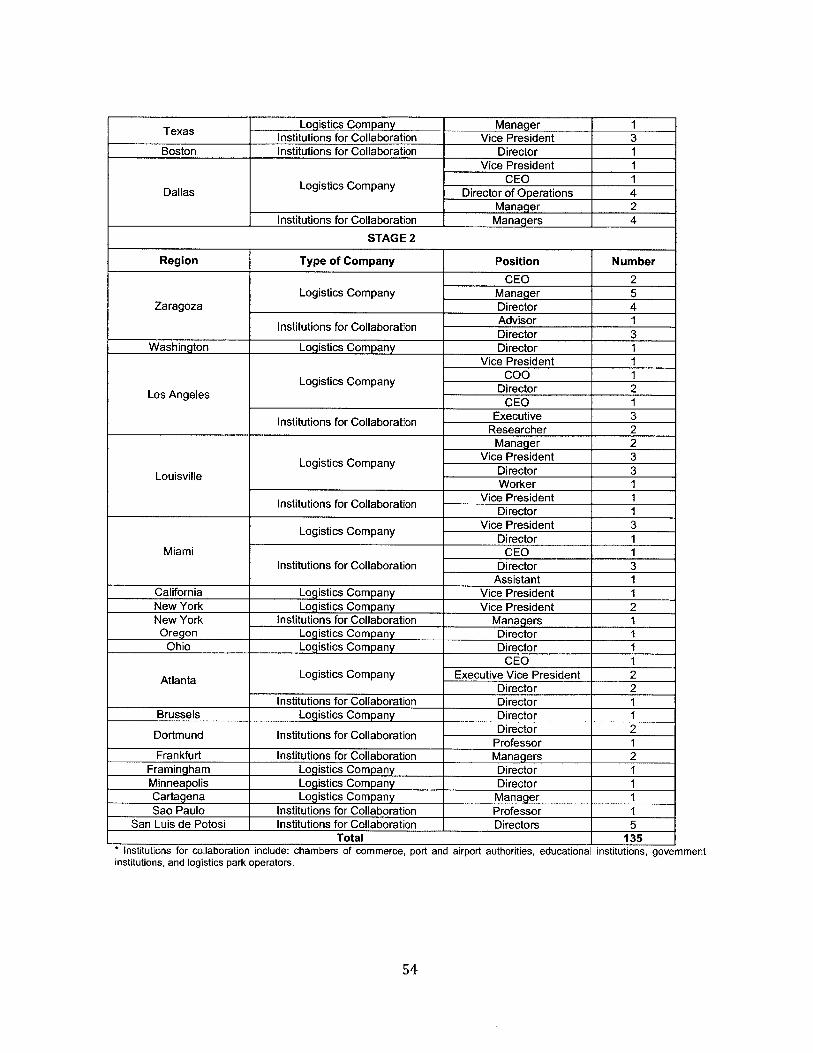

4.1. Interviews Sam ple..............................................................................................................................53

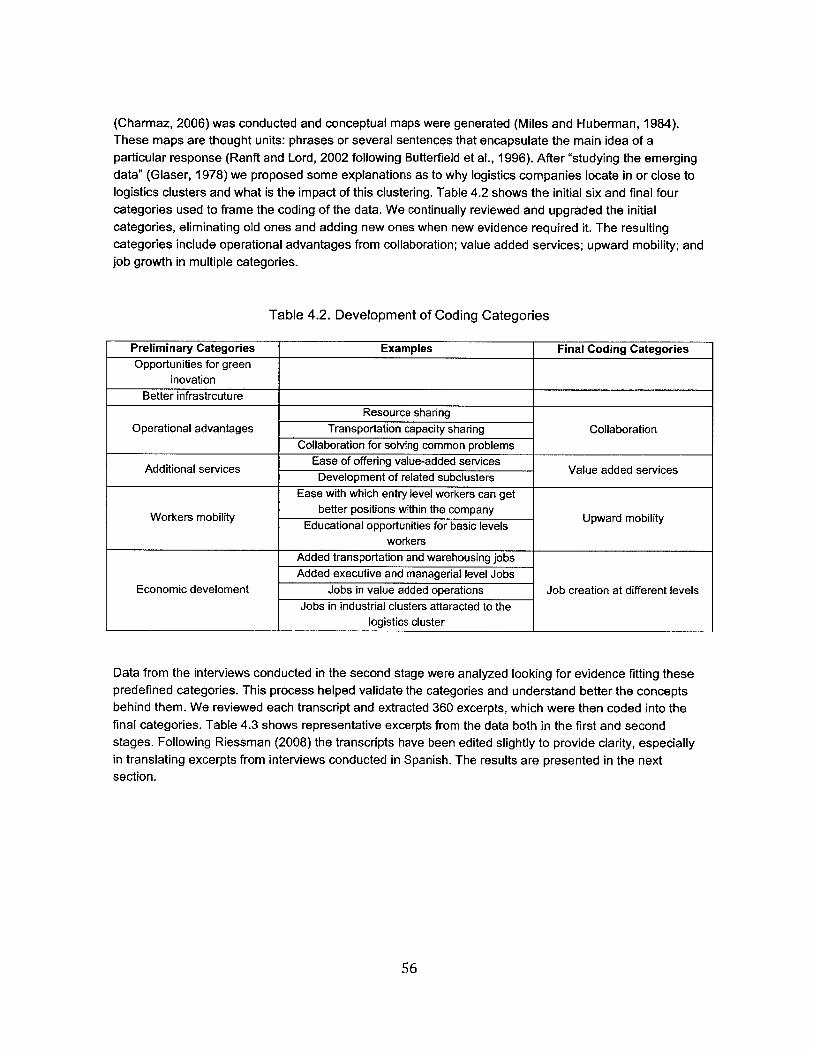

4.2. Developm ent of Coding Categories.........................................................................................................................56

4.3. Benefits of Logistics Clusters.............................................................................................................57

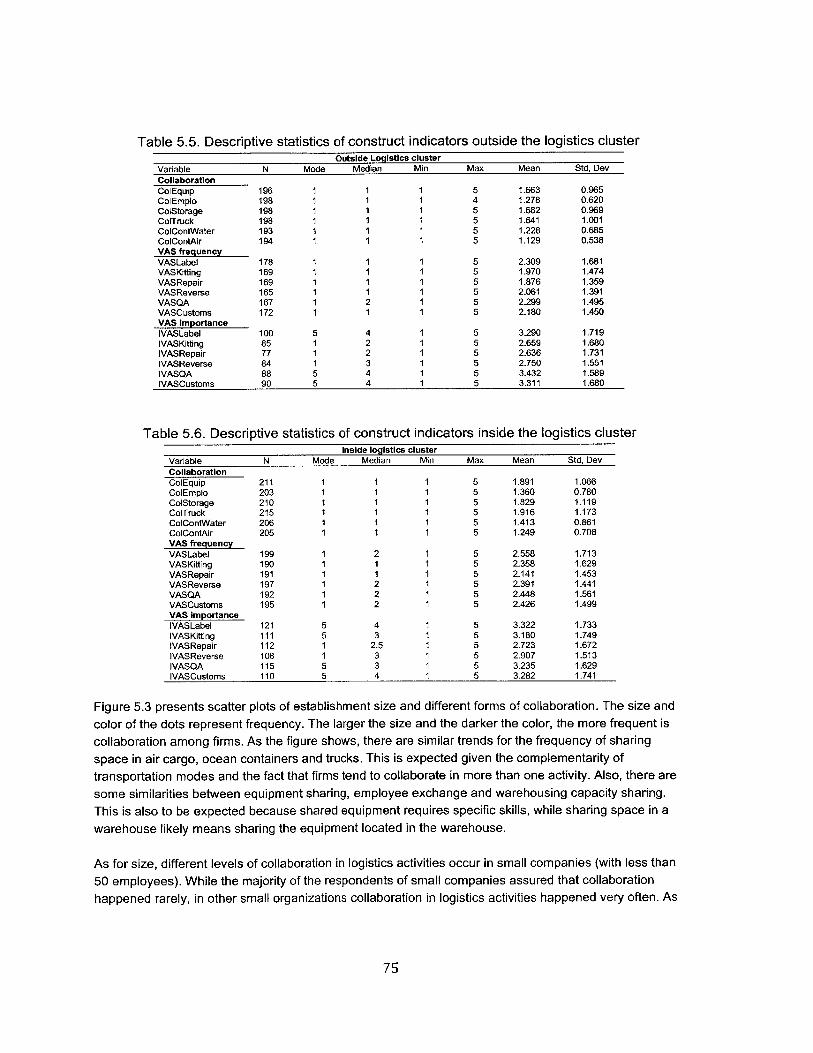

5.1. Descriptive statistics of indicators................................................................................................ 74

5.2. Descriptive statistics of construct indicators outside the logistics cluster................................ 75

5.3. Descriptive statistics of construct indicators inside the logistics cluster.................................. 75

11

12

Chapter 1

Introduction

The introduction of this dissertation contains three sections. The first provides the context for the thesisand explains the motivation. The second presents the research questions and the third explains theoutline.

1.1. Why study logistics clusters?

Logistics agglomerations defined as the geographical concentration of logistics-related activities are agermane (and popular) subject among logistics firms and policy makers all over the world. Places likeSingapore, Los Angeles, Rotterdam, Chicago, Zaragoza, Santos, and many others are large clustersattracting many logistics activities. Anecdotal evidence suggests that they are advantageous in terms ofconnections to other locations worldwide, availability of labor, collaboration among firms, and transportaccessibility. Policy makers are also interested in logistics clusters because of their positive impact onregional economic growth (Rollins et al., 2011). However, there is a lack of empirical evidence to showthe extent and magnitude of this phenomenon.

Many governments are investing considerable resources to either develop or expand logistics hubs'.These investments are driven by the expectation of positive impacts on the economy. For example,Panama has a five-year plan with an expected investment of more than $2 billion to position the countryas the logistics hub for the Americas. Part of the expected returns in value added services include US$1.5billion along with the creation of over 30,000 direct and indirect jobs by 2020. Similarly, the Dallaslogistics hub is being developed with over $500 million invested in the surrounding areas. A significantshare of this investment (25%) comes from public sources. The hub is expected to create over 60,000direct and indirect jobs with an estimated economic impact of more than $60 billion for the region by2035.

The importance of logistics agglomerations is even higher because of globalization. Logistics clusters arethe nodes of the global supply chains. These clusters comprise intermodal and multi-modal facilities withefficiencies in of transportation and storage that allow for freight consolidation. As globalizationaccelerates, these efficiencies are likely to attract even more cargo to logistics clusters and do so morefrequently, allowing for lower costs and better levels of service (Sheffi, 2012).

Despite the growing importance of logistics clusters for both companies and regional governments, thereare scant studies in the logistics and supply chain literature referring specifically to this phenomenon.

1 In this thesis cluster, hub and agglomeration both refer to the geographical concentration of logistics firms.

2 The content of this chapter has also been presented in Rivera et al. (2014).3 The content of this chapter has also been presented in Van den Heuvel et al. (2014). Besides Liliana Rivera andYossi Sheffi this paper was coauthored by Fran Van de Heuvel, Peter de Langen, Jan Fransoo, Karel van Donselaar,and Ad de Jong from the Eindhoven University of Technology.

13

Sheffi (2012) provides evidence on the relevance of logistics clusters based on interview data andhighlights the need for further research in this area. Related studies include research into port clusters (f.i.Haezendonck, 2001; De Langen, 2002); absolute and relative employment concentration areas (Van denHeuvel et al., 2013); supply clusters (Wu et al., 2006); and Aerotropolis or airport clusters (f.i. Kasarda,2008). These mostly focus on structure; for example, on describing the agents and interactions involvedin clusters. They also describe the activity of each cluster in terms of movement of cargo or value ofexports. Most of these authors draw conclusions regarding the impact of logistics clusters using the sameelements which the literature suggests for general industrial, without identifying benefits or costs specificto logistics clusters.

Regional economics has dealt extensively with industrial colocation. Marshall (1890) mentionedknowledge sharing, the formation of a labor pool and a supplier base as positive externalities fromagglomeration economies. A century later, some authors found that clusters also have a positive impacton productivity. Porter (1998) mentioned that colocation incentivizes firms not only to collaborate but alsoto compete, which encourages higher innovation, productivity, as well as more business formation andeconomic growth. Fesser (2008) used a value chain analysis approach to understand the linkages inclusters, while Ellison, Glaeser and Kerr (2007) provided empirical evidence of agglomeration economies.Other authors argued that the negative externalities of clusters such as congestion and increasing landand labor prices outweigh the benefits, driving firms to disperse and clusters to decrease (Feitelson andSalomon, (2000); Karsten (1996); and Dell'Orco et al. (2009)).

This dissertation focuses on the agglomeration of logistics companies and contributes to the discussionon cluster prevalence by empirically analyzing the case of the logistics industry. It suggests that logisticsclusters are, in fact, growing, rather than dispersing, despite their local impact on congestion and otherenvironmental issues. It also analyzes specific reasons that may explain why logistics firms agglomerate;separate than those that the literature attributes to general industrial clusters. Therefore, this dissertationprovides decision makers in firms about facility location choices and in governments regarding regionaleconomic development

1.2. Research questions

This dissertation focuses on two questions. The first analyzes whether logistics companies are clusteringor dispersing over space and over time. The second studies the specific impact of logistics clusters oncompanies.

1.2.1. Agglomeration of logisticsfirms

To be able to analyze the agglomeration of logistics firms, the first step is to identify where logisticscompanies locate, whether they cluster or not, and if the clustering trend increases or decreases overtime. Thus, the first question this thesis examines is:

Are logistics companies clustering or dispersing over time?

The geographical concentration of firms has drawn the interest of researchers in spatial economics, andseveral methods have been proposed to measure industrial concentration. Each method leads to anindicator of concentration which has its own advantages and limitations. A desirable indicator to identify

14

and define logistics clusters should: i) identify the concentration of activities, ii) indicate where thatconcentration is located iii) give a sense of the size of the concentration in the geographic area, iv)guarantee that the concentration is due to the presence of external economies of scale, v) work with theavailable data, and vi) be replicable.

The Location Quotient (LQ) method is the most commonly used indicator for identifying clusters(Polenske, 2003) because it requires little data. It is defined as the ratio of a particular industry's share ina geographical area's employment (say, a metropolitan area or a county) and that industry's share ofemployment in a larger reference area (in many cases the whole country). Thus, this index providesinformation about the relative weight of a particular industry's employment in a geographical area (relativeto the reference area). However, the LQ does not provide information regarding the absolute size of theindustry and it does not guarantee that concentration is due to external economies of scale. The absolutesize of the industry is relevant because LQ is a fraction, and the same result could be obtained througheither a large numerator or a small denominator. Also, an increase in an industry's LQ does notnecessarily imply the industrial cluster grows, since this could also be due to the reference area

dispersing. According to Forslid (2002, p. 287), "The differing sizes of the regions make relative indices aless attractive choice as a measure of industrial concentration." In addition, the LQ does not account for

the difference between a single large firm in a region and a set of multiple firms. Thus, it does notdistinguish whether the concentration of an activity is due to internal or external economies of scale.

To address these problems, this dissertation proposes a method that combines two indicators: theHorizontal Clustering Location Quotient (HCLQ), which solves the first problem related to the magnitudeof concentration, and the Logistics Establishments Participation (LEP), which solves the second problemregarding the presence of external economies of scale. This method is applied to the US because of theavailability of data at a low level of geographical aggregation, specifically at the county level.

1.2.2. Impact of the agglomeration of logisticsfirms

Economic literature has mentioned the benefits of colocation. These externalities include knowledgesharing, the formation of a labor pool and a supplier base, and increments in productivity and innovation.Other authors have identified additional benefits in industrial clusters. For example, Appold (1995)mentioned that being close to competitors expands a firm's market area and encourages new businessformation. Boari (2001) showed that the spatial agglomeration of firms generated spillovers of knowledge,technology and managerial practices.

Although there are many studies about the impact of clusters in industries such as information technology(f.i. Moulaert and Djellal, 1995; Globerman et al., 2005; Huber, 2012; Angel, 1991; Fallick et al., 2006;Grondeau, 2007), there are only a few references looking at the impact of the agglomeration of logisticsfirms and their conclusions are not similar. Sheffi (2012) claims that the colocation of logistics companieshas specific impacts on companies and employees, which is in addition to the impact observed in generalindustrial clusters. Interview data suggest that these benefits attract logistics firms to both new andestablished clusters. However, other authors claim that there are no benefits of logistics clusters and theyhave negative impact on society. Morgan (2012) states that the geographical concentration oftransportation, distribution and logistics companies does not provide benefits to companies or regions.Berechman (1994) says the agglomeration of logistics firms generates negative externalities, like

transport congestion, which encourage firms to disperse rather than locate inside a cluster.

15

The impact of the logistics agglomeration is studied in this thesis, by using qualitative and quantitativemethods in order to contribute to the discussion and to provide information to firms and policy makersrelevant in their decision making processes. Thus, the second question this dissertation analyzes, basedon the answer to the first question, is:

What are the consequences for logistics firms (from clustering)?

The results of this thesis agree with those of Sheffi (2012). Logistics clusters encourage morecollaboration and value added services for logistics firms, higher levels of upward mobility for employeesand employment creation for economic regions. These benefits are specific to the logistics sector and donot extend to other sectors.

1.3. Outline

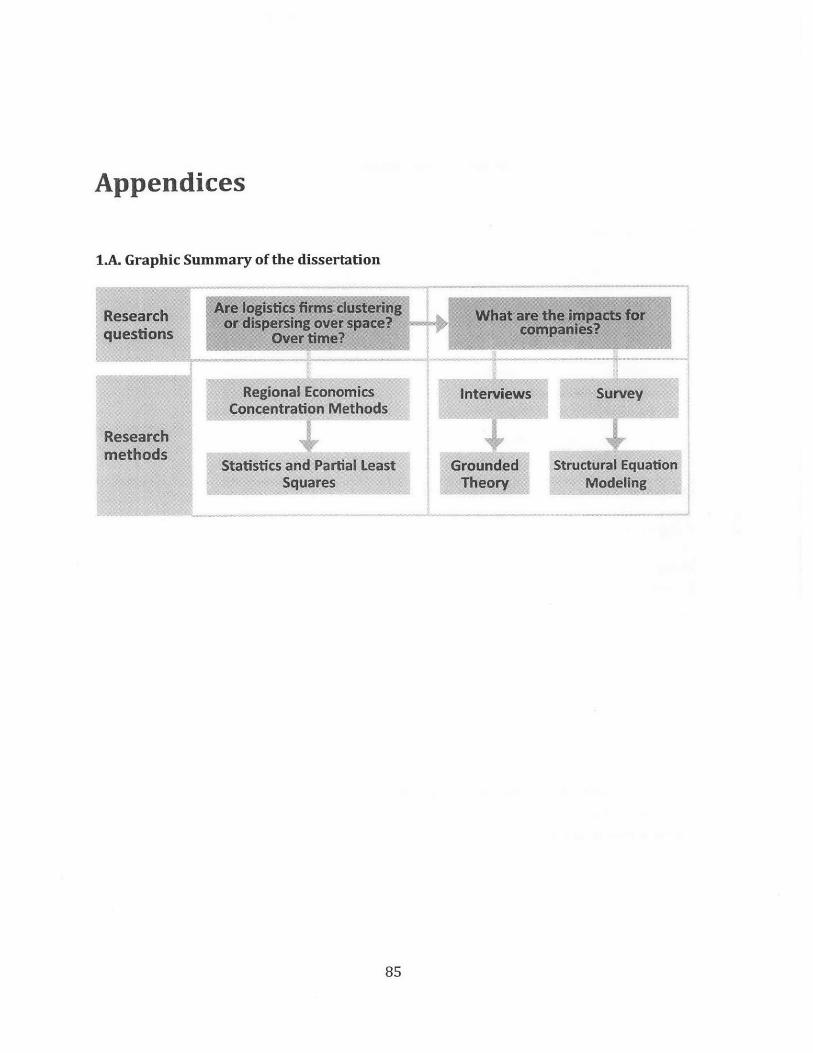

This thesis has two parts related to the two research questions: 1. Are logistics companies clustering ordispersing over time? and 2. What are the consequences for logistics firms? Each part comprises twochapters (See Appendix 1.A for a graphic summary of the dissertation).

In the first part, chapter 2 analyzes the prevalence of logistics clusters by looking specifically at the caseof the United States. Based on interviews and exploratory research the hypothesis that logisticscompanies are clustering and that this phenomenon is growing over time is analyzed. Then a two-indicator method to identify logistics clusters is introduced, aiming to satisfy the six conditions posed insection 1.1. This method is applied to the US, using county level data for the logistics sector (in terms ofemployment and establishments) in 1998 and 2008. The results show that the growth of logisticsoperations between 1998 and 2008 was higher in counties located inside the identified clusters than incounties outside of them.

Chapter 3 explores the relationship between freight accessibility and logistics employment. Using thesame data, gravity based accessibility measures (road, air, maritime and rail accessibility) at the countylevel are developed. Then, a partial least squares model is used to analyze the relationship. The resultsdemonstrate a positive correlation between freight accessibility and logistics employment at the countylevel in the US, even after controlling for the effect of county population.

In the second part, chapter 4 investigates the specific benefits of logistics clusters, using survey methodsto gather data (135 interviews) and grounded theory to analyze it. Results suggest that agglomeratedlogistics firms enjoy more opportunities to collaborate and offer value added services, and that logisticsclusters also seem to increase upward mobility for employees and create more logistics jobs at differentlevels. Chapter 5 analyzes the extent of collaboration and the provision of value added services inlogistics clusters. Using data from a survey conducted in the Zaragoza logistics cluster in Spain and astructural equation model, the thesis shows that agglomerated logistics firms enjoy higher levels ofcollaboration and value added services than firms located outside logistics clusters.

Finally, chapter 6 presents the conclusions and opportunities for further research.

16

Chapter 2

Logistics agglomeration in the US 2

2.1. Introduction

Governments around the world are investing significant resources in the development of new and theexpansion of existing logistics clusters, all of which are central nodes of the global freight transportationnetwork. They are motivated, in large part by a job creation agenda. For instance, the Government ofArag6n in Spain invested over E680 Million to develop Plataforma Logistica - Zaragoza (PLAZA), thelargest logistics park in Europe and the core of the Aragon logistics cluster. Panama is in the process ofdeveloping significant logistics clusters at both ends of the canal as part of the strategy to position thecountry as the center for trade and logistics for the Americas (Council of the Americas, 2011; Governmentof Panama, 2010). While new logistics hubs are being developed, existing clusters are expanding in scaleand scope. These include major ones such as Singapore, Rotterdam, Duisburg (Germany), Dubai,Santos (Brazil), and multiple US locations such as New York, Miami, Chicago, Dallas/Ft Worth, Memphis,Louisville and Los Angeles.

Logistics can be broadly defined as the group of functions associated with production, design, andmarketing, which include "...transportation, warehousing and facilities planning, and location"(Kasilingman, 1998). These activities add value to companies' supply chain and increasecompetitiveness.

The logistical need to move material, parts, and products into manufacturing, distribution and retaillocations creates the (derived) demand for freight transportation. To this end, efficient transportationoperations are crucial for efficient logistics since transportation costs are a relevant part of the retail price(Xu and Hancock, 2004). Also, the pressure to time-compress logistical operations and provide high levelof service gives transportation a central role in logistics (Groothedde, 2005; Stank and Goldsby, 2000).Furthermore, as stated by Rodrigue and Hesse (2006) "...the role of transportation is considered morethan a mere support to the mobility of freight within global commodity chains, but an integral part of thevalue generation process."

Dozens of interviews all around the world suggest that logistics clusters are growing. This finding is in linewith the many authors who document and explain the advantage of industry agglomeration, or clustering.They cite tacit knowledge exchange, the development of a local supply base, and the availability of aspecialized labor pool (Marshall, 1890; Fesser, 2008; Ellison et al., 2010). Other authors point out that theregions where these clusters reside enjoy high economic growth and a higher rate of innovation and

2 The content of this chapter has also been presented in Rivera et al. (2014).

17

capital formation than regions that do not include clusters (Porter 2000, 2003; Delgado et al., 2010,Benneworth and Henry, 2004). Other researchers, however, claim that negative externalities of clusters,the development of information technologies and the efficiency of global supply chains diminish theadvantages of geographical proximity, leading to dispersion of like-businesses (Caincross, 1997;Polenske 2001, 2003; Henderson and Shalizi, 2001). Also, Feitelson and Salomon (2000) point out to theincreasing congestion in transportation networks that could lead to dispersion of logistics activities.

Although large investments in logistics clusters seem to suggest that policy makers believe in theirpositive effects, and though there are some studies that account for their benefits (see for instanceKasarda, 2008; De Langen, 2002, 2004a; Wu et al., 2006), the prevalence of logistics clusters has notbeen studied yet. This chapter defines logistics clusters, explains their advantages and tests thisprevalence. It then uses a two-factor metric to identify logistics clusters in the US, validating the resultsthrough several approaches. Using data from 1998 and 2008 it provides evidence that logistics activitiesseem to be, in fact, agglomerating rather than dispersing over time.

Section 2.2 reviews the state of the art in clusters research, with an emphasis on logistics, and providessome context for the analysis. Section 2.3 presents findings from exploratory research used to developthe thesis of the chapter. Section 2.4 reviews the methodologies used to identify clusters, while Section2.5 depicts the model and the data used in analysis of the US. Sections 2.6 and 2.7 present the results,including a statistical analysis. Finally Section 2.8 concludes with final observations.

2.2. Industrial and Logistics Clusters

The literature concerning industrial clusters dates back to Marshall (1890), who discusses agglomerationeconomies and enumerates the externalities-based advantages for firms to co-locate. Economistsdistinguish among several types of agglomerations. Marshall (1890), and Weber and Friedrich (1929)discussed external economies of scale, resulting from multiple firms agglomerating geographically, asopposed to internal economics of scale, where a single firm expands its production (see, for exampleIsard and Schooler, 1959). Hoover (1937) defined two types of external economies of scale: urbanizationand localization. Urbanization economies arise when many firms from different industries concentrate inthe same region; localization economies arise when firms from a particular sector locate in the sameregion. This chapter is focused on external economies of scale and localization economies of logisticsfirms and operations.

Porter (1998) summarized the main benefits of industrial clustering as follows: "A cluster allows eachmember to benefit as if it had greater scale or as if it had joined with others formally, without requiring it tosacrifice its flexibility." A related branch of literature argues that clustered firms enjoy not only the benefitsof agglomeration economies (Fesser, 2008; Ellison et al., 2010), but also higher collective learning andtacit knowledge exchange (Keeble and Wilkinson, 2000; Maskell, 2001; Cohen and Fields, 1999; Leamerand Stoper, 2001). Intra-cluster competition drives firms to succeed by increasing their productivity,supercharging innovation, and by stimulating new business formation (Porter, 2000; Delgado et al.,2010). This also results is high economic growth (Baptista, 1998), reinforcing the importance ofgeographical concentration and supporting a continuing clustering trend.

However, several authors argued that the efficiency of supply chains, and advanced communicationstechnologies represent the "end of geography" (O'Brien, 1992) and the "death of distance" (Cairncross,

18

1997). Others point to the negative externalities of clusters such as congestion and higher prices of landand labor, creating incentives for firms to leave clusters (Henderson and Shalizi, 2001; Glasmeier andKibler, 1996; Teubal et al., 1991), as a result of "Dispersion Economies" (Polenske, 2003).

This chapter explores the role of clusters in logistics and transportation. A logistics cluster is defined asthe geographical concentration of firms providing logistics services, such as third-party-logistics (3PL-s),transportation carriers, warehousing providers and forwarders. Naturally, logistics clusters also includesuppliers for such activities, such as packaging manufacturers and transportation maintenance depots.

The academic literature includes only a few articles about logistics clusters with little mention of theirprevalence. Van den Heuvel et al. (2011) studied the logistics industry within three Provinces in theNetherlands, concluding that the concentration of relative and absolute employment in logistics firmsthere has increased in recent years.

The emergence of a logistics cluster depends on the quality of transportation service available in a region(Hong, 2007). Bok (2009) highlighted accessibility and general infrastructure quality as the main factorsaffecting the location preference of firms. Better accessibility typically drives logistics operations to locaterelatively close to each other (Berechman, 1994), as it reduces costs for firms (Rietveld, 1994). Hong(2007) asserted that transportation accessibility is one of the important determinants of location decisionsof foreign logistics firms.

Most of the literature related to logistics clusters is specific to ports or airports and not to the logisticssector in general. Haezendonck (2001), Kink and De Langen (2001) and De Langen (2002, 2004a,2004b) investigated maritime clusters, arguing that, based on their findings, the concentration of maritimeactivities in clusters is likely to increase. This is not surprising as one considers the, more familiar,increased concentration of airlines in "hub fortresses." The economics of hubs for maritime and air freightare similar.

Martin and Roman (2003) document the agglomeration of airfreight carriers in hub airports while Lindsayand Kasarda (2011) developed the concept of "Aerotropolis" - a full urban development around anairport. Interestingly, despite the attraction of airport and port clusters some observations suggest thattheir growth is sometimes constrained by lack of land and environmental regulations. The focus of thischapter, in any case, is on logistics clusters in general, many of which are not focused on either a port oran airport.

Finally, Wu et al. (2006) argue that China's economic advantage goes beyond labor costs, and can beexplained, in large measure, by the presence of "supply clusters." These clusters provide all the logisticsservices needed for the management of global supply chains. They add: "the large number of supplyclusters formed in China in recent years has contributed significantly to the nation's manufacturingcompetitiveness."

2.3. Exploratory research

During 2010 and 2011 the author conducted 135 interviews as part of an exploratory research with actors

in and around logistics clusters, resulting in three main findings relevant to the work reported in thischapter. First, these interviews suggest that logistics companies are clustering and those clusters are

19

growing. Second, Governments play a key and necessary role in logistics clusters' development. Andthird, logistics clusters attract transportation carriers who build their networks around such clusters.

A description of the methodology of data collection through interviews and the analysis of this qualitativedata is beyond the scope of this chapter and is the subject of chapter 4. In summary, the first stage wasexploratory and consequently open interviews were used to collect data. In the second stage more datawas gathered through semi structured interviews to confirm the initial findings (Babbie, 2010). Theinterviews were conducted in existing logistics clusters in Singapore, the Netherlands (Amsterdam andRotterdam), Germany (Duisburg and Frankfurt), Spain (Zaragoza), Panama (Panama City and Colon),Dubai, Brazil (Campinas and Santos - both in the State of Sao Paulo), Cartagena (Colombia), and theUS (New York, Miami, Chicago, Dallas/Ft Worth, Memphis, Louisville and Los Angeles). The data wasanalyzed using grounded theory tools (Glaser and Strauss, 1967; Glaser, 1978), and following Charmaz(2006). The process included coding and clustering analysis to organize the data, as well as an evolvingrevision of the categories and results.

The interview data suggest a consensus on the advantages of logistics clusters for companies andregional economies. As many researchers point out, lower cost may not be the only reason why a firmselects a particular location (see, for example, Castells 1996, DiPasquale and Wheaton 1996, Porter2001, Polenske 2003). Just as important, if not more, is the high-level of transportation services.

Sheffi (2010) summarizes the transportation cost and service advantages of logistics clusters, includingeconomies of scope, scale, and density; better service, and liquidity. Economies of scope arise due to thepresence of many shippers, helping the balance of movements in and out of the cluster, minimizingequipment idle time and empty repositioning moves. Economies of scale result from lower costs while theconcentration of logistics operations in the cluster produces higher freight volumes, allowing carriers touse larger conveyances and enjoy higher utilization. Economies of density arise because the larger thenumber of companies in the cluster, the more efficient pickup and delivery operations get. Better level ofservice result from the higher freight volume leading to higher frequency of services as well as moredirect services in and out of the logistics cluster. Finally, liquidity or price stability is the result of manyshippers located in the same geography, served by many transportation carriers, thus minimizingsituations of short-term mismatch between demand and equipment availability.

These advantages create a positive feedback loop rooted mainly in the economics of transportation: asmore firms join the cluster, transportation costs go down and service improves, which in turn attracts morefirms to the cluster, further reducing costs and improving transportation services.

In addition, the interviews suggest that companies in logistics clusters share equipment, lease space toeach other for short-term surges and lulls in activity; and work effectively together when a logisticscontract is moved from one provider to another. Cluster companies also have more weight in lobbying thelocal government, which in the case of logistics clusters the focus is typically on improved infrastructureand regulatory relief.

While many authors studying other industrial clusters (mainly high technology ones) argue that the role ofgovernment in their development and growth is minimal (OECD, 2001; Wadhwa, 2010), government is amajor player in logistics clusters. This is due not only to the significant transportation infrastructurerequirements of such clusters, but also due to the need for a favorable regulatory, tax, and trade policyenvironment. The interviews suggest that government interest in logistics clusters is, not surprisingly,

20

primarily driven by the potential benefits for the local economy with an emphasis on jobs. Interestingly,they are also viewed - mainly in the US - as a vehicle for "economic justice" based on "professionalmobility": providing starting jobs that pay better than the hotel or the agricultural industries to employeeswithout high level education, and allowing them to be promoted from within as this industry values "on thefloor experience" in its executives.

The interview data suggest that the major investments that are going into new and existing logistics

clusters will go on, and that these clusters are growing (not dispersing); this is the basic hypothesisexplored statistically in this chapter.

2.4. Identifying Clusters

Before tackling the question whether US logistics operations are clustering or dispersing, one needs toidentify the location of concentrations of logistics activities. Even by itself such identification can be ofvalue; it can help firms identify sites to set up distribution activities. Governments using this information

can identify competing regions that can then be used to benchmark effective policies (infrastructure,regulation, and administrative efficiency, among others) for success of logistics clusters.

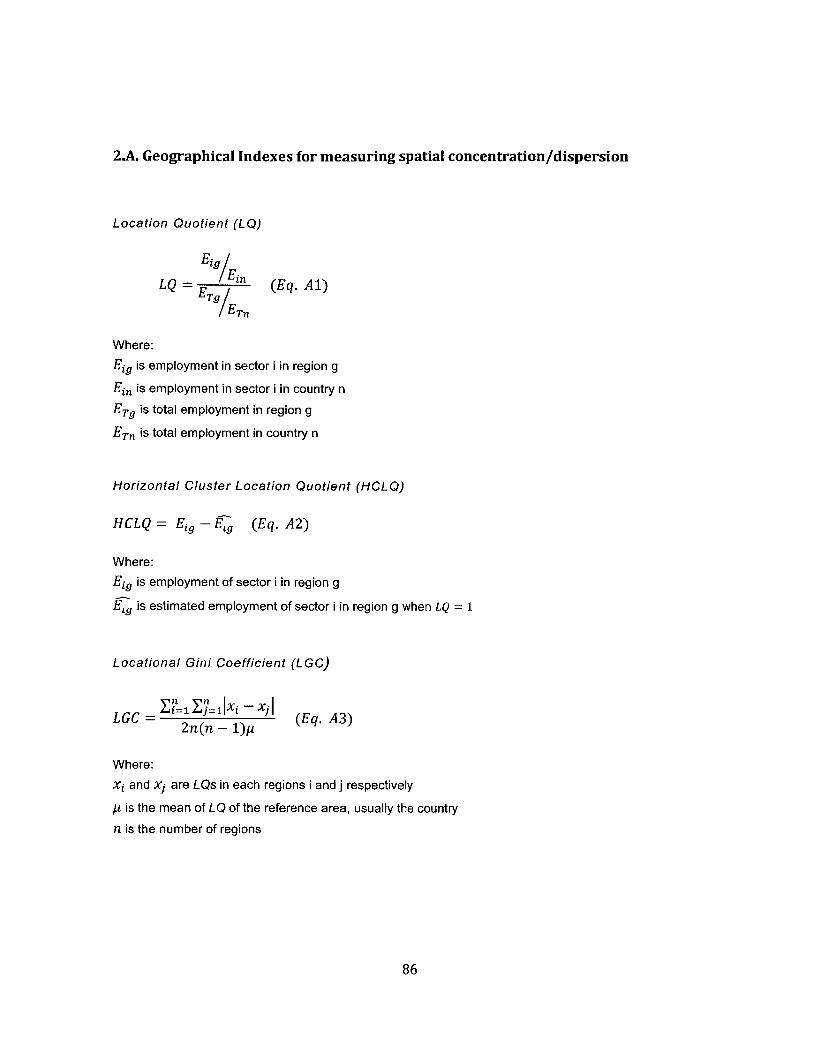

Several of the most common indices employed to measure industry geographical concentration includethe Location Quotient (LQ), Horizontal Clustering Location Quotient (HCLQ), Locational Gini Coefficient(LGC), Herfindahl-Hirschman Index (HHI), and the Ellison-Glaeser Index (EGGCI). Appendix 2.A containsthe formal definition of these indices.

Location Quotient (LQ) has widely been used in economic geography and regional economics since the1940s (Miller et al., 1991). In fact, it was used by De Langen (2004a) in his analysis of maritime clusters.This technique has remained popular in large part because it requires relatively little data (Isserman,1977). LQ is the ratio of employment share of the industry of interest in the area of interest and theemployment share of that industry in a reference area (which is typically the country).

Some of the studies that have used this technique include Paige and Nenide (2008) in their analysis ofthe agglomeration trends in the Central San Joaquin Valley in California; Braunerhjelm and Carlsson(1999) who set to identify cluster activity and its evolution in Ohio and Sweden; Held (1996), whoaddressed the question about the State's participation in generating economic development through acluster approach in the Hudson Valley of New York; and others (Zook, 2000 and Malmberg and Maskell,2002).

A value of the LQ greater than one suggests a higher than average share of employment in an industry ofinterest in a given area. Although this index provides information about the relative weight of a particularindustry's employment in a geographical area (relative to a reference area), it does not provide

information regarding the absolute size of the industry (Feser et al., 2002).

To correct this issue, Fingleton et al. (2004) proposed the Horizontal Cluster Location Quotient (HCLQ),which weighs LQ values with an indicator of magnitude, such as the local area share of nationwide jobs ina given industry. It thus takes into account both the relative and absolute local importance of the industry

under study. HCLQ is the number of jobs in the local industry that exceeds the number that would

produce LQ = 1 (Ratanawaraha and Polenske, 2007). An example is found in Echeverri-Carroll and Ayala

21

(2010). They analyze wage differentials caused by the agglomeration of high-tech companies in certaincities of the United States. Using the HCLQ they suggest that clustering is the key factor behindinnovation flows, knowledge spillovers and other cooperative linkages among firms.

Two additional measures of industry clusters include the Locational Gini Coefficient (LCG) and theHerfindahl-Hirschman Index (HHI). The former was proposed by Krugman (1991) to examine regionalincome disparities, based on the Gini coefficient used widely in studies of income inequality and poverty(see for example, Chakravarty, 1990; Lambert, 1989; Atkinson and Bourguignon, 2000). The LGC is anumber that captures the distribution of employment in an industry across geographic areas, relative tothe distribution of total employment. It signals the relative concentration pattern of employment in acertain economic sector in a given area in relation to other sectors in the same area.

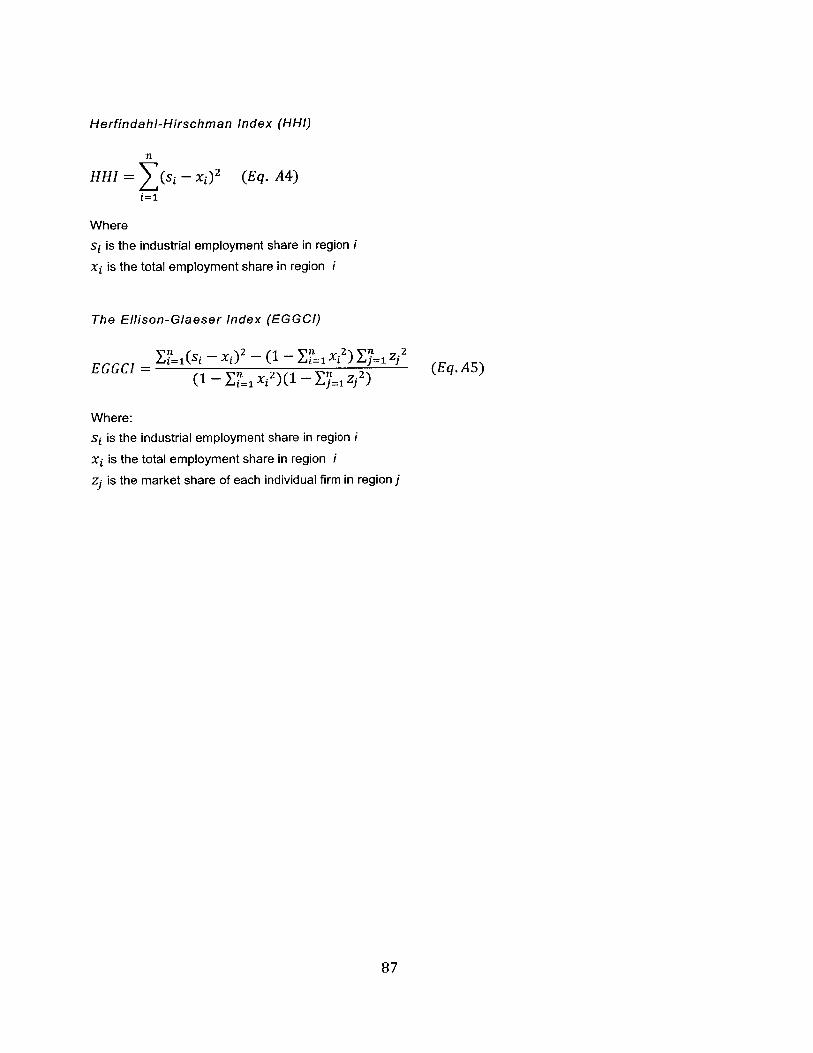

The HHI is defined as the aggregation of the industrial shares of all areas in a region, usually the country(Kim et al., 2000). It measures the extent to which a given industry is distributed throughout a largenumber of sub-areas (say, counties or other geographical sub-units).

Neither the LCG nor the HHI are aimed at identifying logistics (or any other) clusters. They measureindustry concentration in a country (or other reference area), but do not provide information on where theconcentration is located within that reference area. As such these indices are not considered further inthis chapter (they are defined, though in Appendix 2.A).

The main criticism of the LQ and HCLQ indices (and also of the LGC and HHI), is that, being based onemployment, they do not account for the difference between a single large firm in a region and a set ofmultiple firms, that is, "they do not distinguish whether the concentration of an activity is due to internal orexternal economies of scale" (Ratanawaraha and Polenske, 2007).

One of the most sophisticated methods to measure the degree of spatial concentration of firms is theEllison-Glaeser Index (EGGCI), which "eliminates the effect of the random distribution of establishmentson firms' locations by comparing the estimated spatial HHI for a given industry to the expected value ofHHI" (Li, 2006). However, the application of this measure is limited due to the extensive datarequirements and its sensitivity to the geographic units used. Additional limitations are rooted in thedifficulty of comparing the value of the index at the international level, because of the different sizesamong regions and countries (Ratanawaraha and Polenske, 2007). Consequently this index is alsoomitted from further discussion.

2.5. Model

A desirable indicator for identifying and defining logistics clusters should: i) identify the concentration ofactivities, ii) indicate where that concentration is located iii) give a sense of the size of the concentration inthe geographic area, iv) guarantee that the concentration is due to the presence of external economies ofscale, v) work with the available data, and vi) be replicable.

To tackle this challenge, this approach described here combines two indicators: the Horizontal ClusteringLocation Quotient (HCLQ) and a newly defined Logistics Establishments Participation (LEP) index. HCLQidentifies both the location and magnitude of the concentration of logistics activities. The LEP guaranteesthat the concentration is due to the presence of external economies. Both indices require a minimum

22

amount of available data (employment and establishment data), which in the US is available at the countylevel, from government statistics, thus allowing for replication. A cluster in this study is defined as a

county with concentration of logistics activities or several adjacent counties with such concentration.

HCLQ is defined as:

HCLQ 1 = Ej - E

Where:

E = Number of employees in the logistics industry in county j, and

E,= Expected number of logistics employees in county j, which is calculated as the number of logistics

jobs in the county that would produce a Location Quotient equal to one.

HCLQj > 0 implies that county j has a higher concentration of employment in the logistics industry than

the country as a whole. The magnitude of the concentration is indicated by the absolute value (extra

number of logistics employees in the county).

Since the objective here is to identify logistics clusters, there is a need to have not only concentration oflogistics employment, but also external economies of scale. This is particularly important since, asHenderson (2003) reports, activity at small and medium firms contributes significantly to external

economies of scale. Thus, this chapter introduces a Logistics Establishments' Participation (LEP) index,representing the share of the countrywide logistics establishments that a county has. It is defined asfollows:

es1LEPj ES

ES

Where:

esj = Number of logistics establishments in county j, and

ES = Number of logistics establishments in the country.

The larger the LEP of a given county, the larger is the number of logistics establishments located in the

county. A cutoff value of 0.1% was chosen. It implies that to be considered a cluster, a region has to haveat least 0.001 of the logistics establishments of the nation (in addition to HCLQ>0). This cutoff value waschosen using the known group validity method (Babbie, 2010) shown below. The rationale for and theeffects of the choice of the LEP cutoff value are shown in Section 2.6. The process leading to theparticular value of 0.1% can be summarized as follows:

1. Known clusters - Data from reports and interviews with experts in the logistics industry from the MITCenter for Transportation and Logistics, the Harvard Institute for Strategy and Competitiveness andthe Indiana Business Research Center were used to draw a list of seven known logistics clusters inthe US today. This list included Los Angeles, Chicago, Memphis, Louisville, Miami, Houston and NewYork/New Jersey.

23

2. Minimize Type / error - Starting from a LEP cutoff value of 1, the cutoff was decreased until all sevenknown clusters showed up in the list of identified clusters. This happened at a cutoff value of 0.2%. Atthis point 31 additional clusters were identified, all of which were recognized by the experts as actuallogistics clusters, thus minimizing type I error (HO: The identified cluster is a logistics clusters indeed).

3. The identification was further verified using information from City data. City data is a social andeconomic database for counties and cities in the US and Canada (http://www.city-data.com/). Thisdatabase was used as a secondary source, rather than a primary source, because it is private andlack of bias could not be ascertained. Also, the city data base covers only the US and Canada andnot available elsewhere else in the world. Lastly, the structure of this data base is such that to identifya cluster directly from city data one needs to examine whether each county has a concentration oflogistics activities, a manual task that prohibits detailed multiple analyzes.

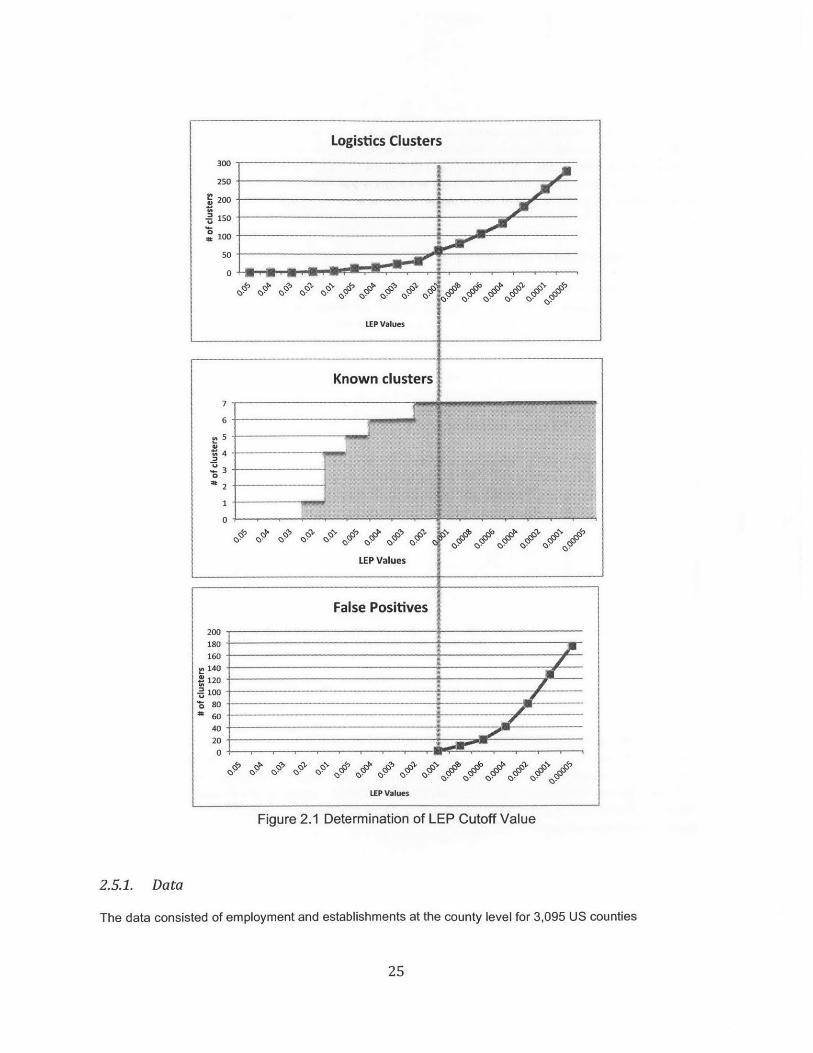

4. Minimize False positives - In order to capture additional logistics clusters, the LEP cutoff value wasdecreased continuously until, at 0.1%, false positives started showing up. False positives were alsochecked as "clusters" that did not appear in the city database and were not recognized by our expertsas actual logistics clusters. The number of false positives increased when the cutoff value wasreduced further. Therefore 0.1% became the LEP value that minimizes false positives, resulting in 61identified logistics clusters. The process is depicted graphically in Figure 2.1.

24

False Positives

200

180

160

140

S120

100S 80 - - -..... -. -.

6 80 ---- -- ------

40

200

LEP Values

Figure 2.1 Determination of LEP Cutoff Value

2.5.1. Data

The data consisted of employment and establishments at the county level for 3,095 US counties

25

Logistics Clusters300

250

200

150

S100

50

0

LEP Values

Known clusters

7

6

5

I'4

1

0

LEP Values

0 6 v 1 143

Irlo, Iz,

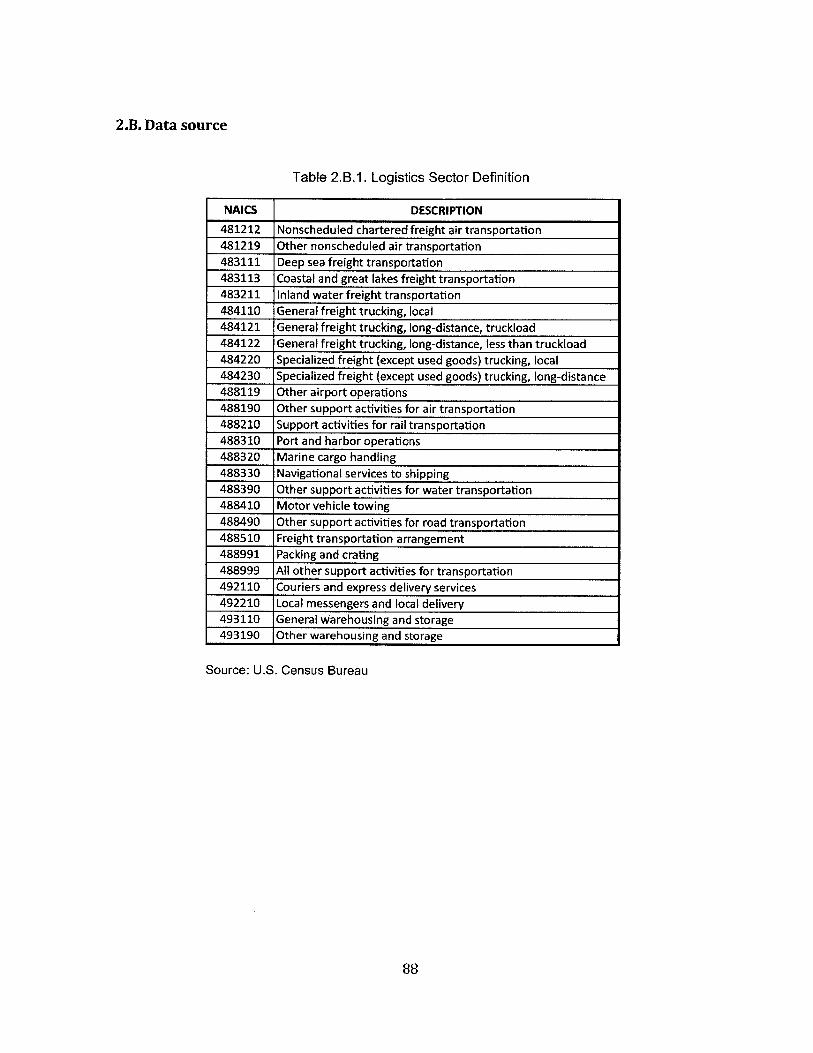

(excluding those of Hawaii, Alaska and Puerto Rico), based on the North American Industry ClassificationSystem (NAICS). Six-digit classification was used, based on the County Business Patterns (CBP) andStatistics of U.S. Businesses (SUSB) from the U.S. Census Bureau. The logistics sector definitionincludes the subsectors depicted in Table 2.B.1 in Appendix 2.B. Even a casual inspection of the datasource reveals the heavy weight of transportation activities in the database.

2.6. Results: Cluster Identification

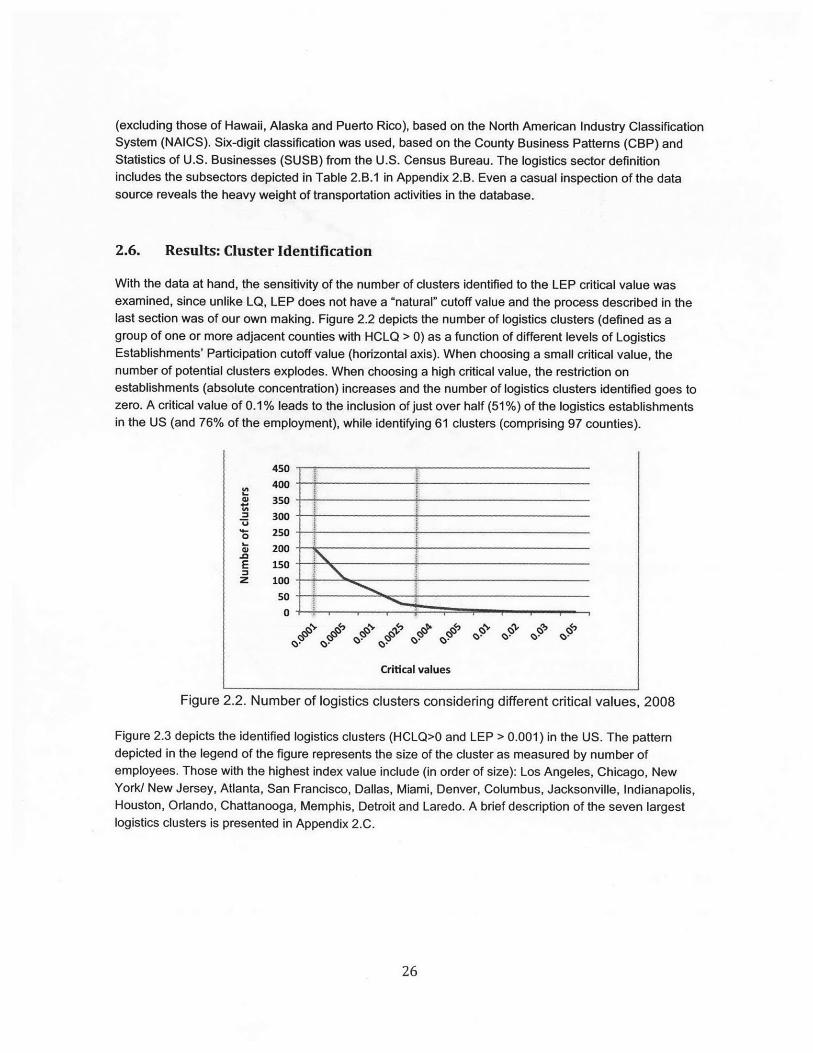

With the data at hand, the sensitivity of the number of clusters identified to the LEP critical value wasexamined, since unlike LQ, LEP does not have a "natural" cutoff value and the process described in thelast section was of our own making. Figure 2.2 depicts the number of logistics clusters (defined as agroup of one or more adjacent counties with HCLQ > 0) as a function of different levels of LogisticsEstablishments' Participation cutoff value (horizontal axis). When choosing a small critical value, thenumber of potential clusters explodes. When choosing a high critical value, the restriction onestablishments (absolute concentration) increases and the number of logistics clusters identified goes tozero. A critical value of 0.1% leads to the inclusion of just over half (51%) of the logistics establishmentsin the US (and 76% of the employment), while identifying 61 clusters (comprising 97 counties).

450400

.~3501

.2 300

'~250 -

200

E 150z 100

s0

Critical values

Figure 2.2. Number of logistics clusters considering different critical values, 2008

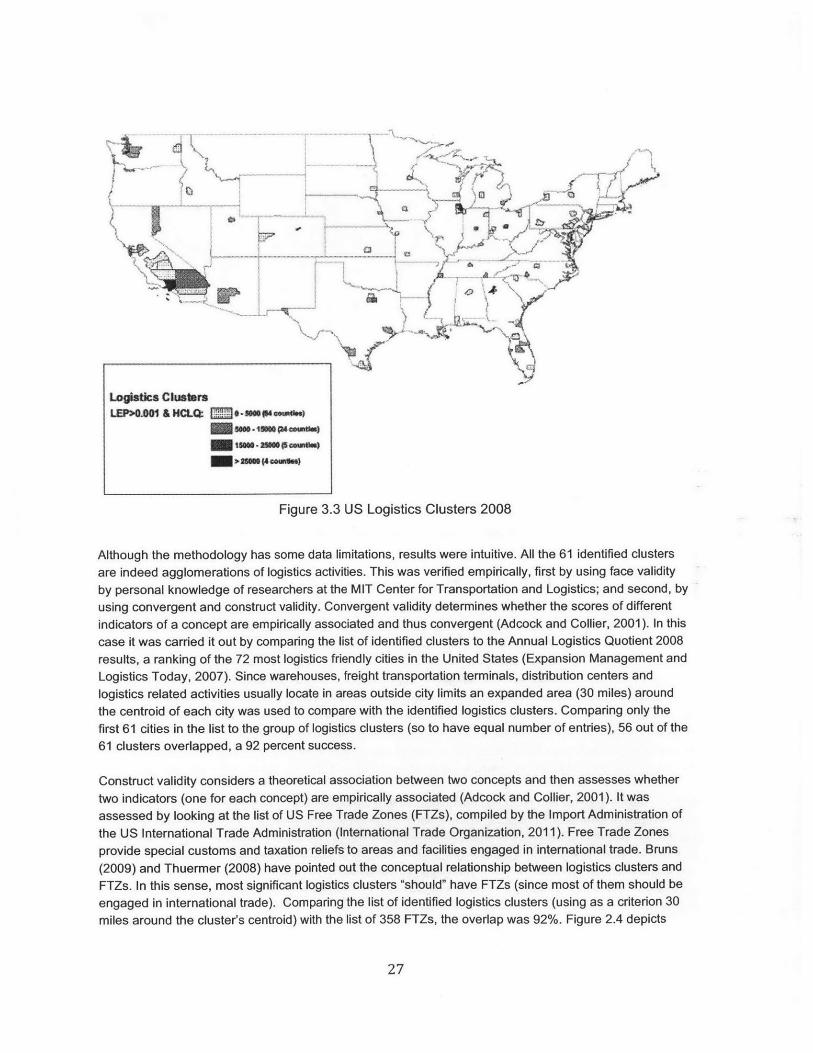

Figure 2.3 depicts the identified logistics clusters (HCLQ>0 and LEP > 0.001) in the US. The patterndepicted in the legend of the figure represents the size of the cluster as measured by number ofemployees. Those with the highest index value include (in order of size): Los Angeles, Chicago, NewYork/ New Jersey, Atlanta, San Francisco, Dallas, Miami, Denver, Columbus, Jacksonville, Indianapolis,Houston, Orlando, Chattanooga, Memphis, Detroit and Laredo. A brief description of the seven largestlogistics clusters is presented in Appendix 2.C.

26

.. ... ... ... ..... ... ... ... .. .. .. .. .. .. .. .. -... .. .. .. ..

.. ..........v-j

I.......

...... ..... .. .. .. .

Wot

Logbtics CatursLEP>O.W1 & HCLQ ---- sumsop*

inRW.1USSM..wmu)

Figure 3.3 US Logistics Clusters 2008

Although the methodology has some data limitations, results were intuitive. All the 61 identified clustersare indeed agglomerations of logistics activities. This was verified empirically, first by using face validity

by personal knowledge of researchers at the MIT Center for Transportation and Logistics; and second, byusing convergent and construct validity. Convergent validity determines whether the scores of differentindicators of a concept are empirically associated and thus convergent (Adcock and Collier, 2001). In this

case it was carried it out by comparing the list of identified clusters to the Annual Logistics Quotient 2008results, a ranking of the 72 most logistics friendly cities in the United States (Expansion Management andLogistics Today, 2007). Since warehouses, freight transportation terminals, distribution centers and

logistics related activities usually locate in areas outside city limits an expanded area (30 miles) around

the centroid of each city was used to compare with the identified logistics clusters. Comparing only the

first 61 cities in the list to the group of logistics clusters (so to have equal number of entries), 56 out of the61 clusters overlapped, a 92 percent success.

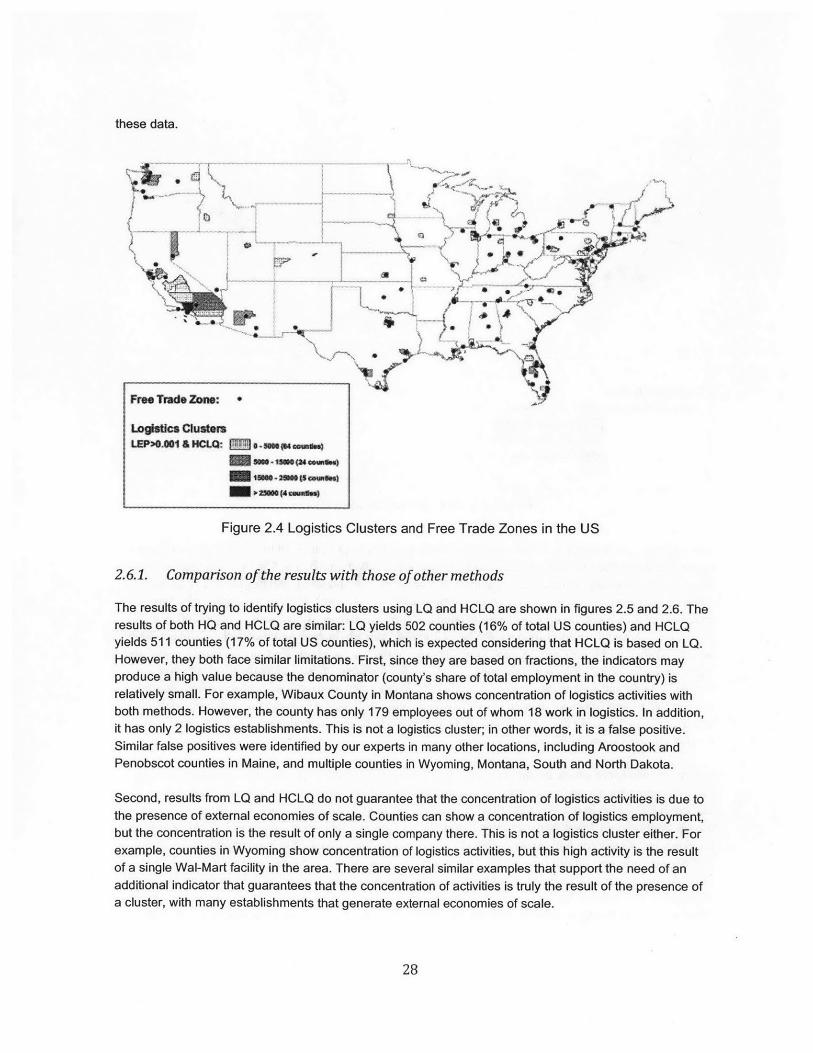

Construct validity considers a theoretical association between two concepts and then assesses whether

two indicators (one for each concept) are empirically associated (Adcock and Collier, 2001). It wasassessed by looking at the list of US Free Trade Zones (FTZs), compiled by the Import Administration of

the US International Trade Administration (International Trade Organization, 2011). Free Trade Zones

provide special customs and taxation reliefs to areas and facilities engaged in international trade. Bruns

(2009) and Thuermer (2008) have pointed out the conceptual relationship between logistics clusters and

FTZs. In this sense, most significant logistics clusters "should" have FTZs (since most of them should be

engaged in international trade). Comparing the list of identified logistics clusters (using as a criterion 30miles around the cluster's centroid) with the list of 358 FTZs, the overlap was 92%. Figure 2.4 depicts

27

[

..............

.IL

'Xiw

these data.

IFree Trade Zciw:

... ... ... .. .. ........ ...... .. ....................... .

..... ..... .....

...... ...... .. ........ ....... .....#

00 AMR~

.. .... ....- 1

\ aI k'*

Logisoca CluterLEP* 014 HCLQ: I -am#.s *..

= -=Wowman.) II

Figure 2.4 Logistics Clusters and Free Trade Zones in the US

2.6.1. Comparison of the results with those of other methods

The results of trying to identify logistics clusters using LQ and HCLQ are shown in figures 2.5 and 2.6. Theresults of both HQ and HCLQ are similar: LQ yields 502 counties (16% of total US counties) and HCLQyields 511 counties (17% of total US counties), which is expected considering that HCLQ is based on LQ.However, they both face similar limitations. First, since they are based on fractions, the indicators mayproduce a high value because the denominator (county's share of total employment in the country) isrelatively small. For example, Wibaux County in Montana shows concentration of logistics activities withboth methods. However, the county has only 179 employees out of whom 18 work in logistics. In addition,it has only 2 logistics establishments. This is not a logistics cluster; in other words, it is a false positive.Similar false positives were identified by our experts in many other locations, including Aroostook andPenobscot counties in Maine, and multiple counties in Wyoming, Montana, South and North Dakota.

Second, results from LQ and HCLQ do not guarantee that the concentration of logistics activities is due tothe presence of external economies of scale. Counties can show a concentration of logistics employment,but the concentration is the result of only a single company there. This is not a logistics cluster either. Forexample, counties in Wyoming show concentration of logistics activities, but this high activity is the resultof a single Wal-Mart facility in the area. There are several similar examples that support the need of anadditional indicator that guarantees that the concentration of activities is truly the result of the presence ofa cluster, with many establishments that generate external economies of scale.

28

.4....

LQ E pfauam

Figure 2.5. Concentration of Logistics activities using LQ, 2008

. ........

0'q

CD...... ....

10 C JcP

LVI A

Figure 2.6. Concentration of Logistics activities using HCLQ, 2008

29

HCLQ: M s-sNO 4w7 anmS)- NW-seepwnw

- oeasss.e.- flu-peo-SIs

al

Mason

= 4%

z

2.7. Results: Trends and Dynamics

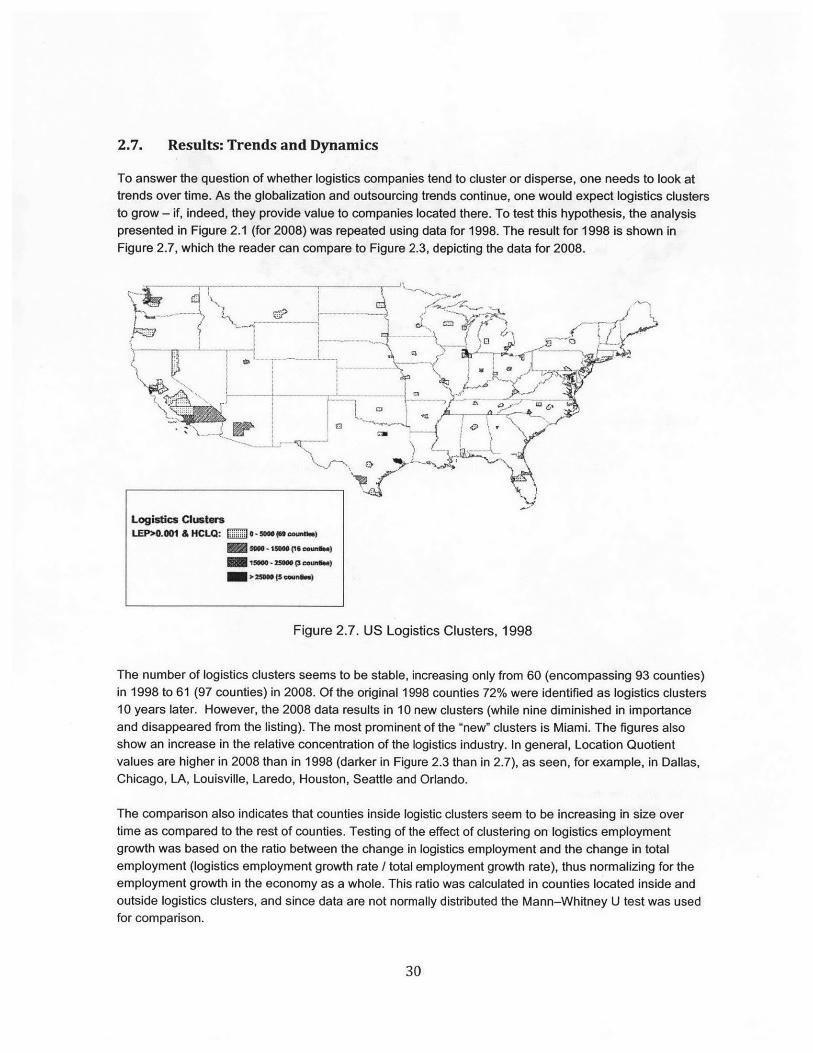

To answer the question of whether logistics companies tend to cluster or disperse, one needs to look attrends over time. As the globalization and outsourcing trends continue, one would expect logistics clustersto grow - if, indeed, they provide value to companies located there. To test this hypothesis, the analysispresented in Figure 2.1 (for 2008) was repeated using data for 1998. The result for 1998 is shown inFigure 2.7, which the reader can compare to Figure 2.3, depicting the data for 2008.

LEP> .C-...... ... .

PZZ-7 ~ ~4, .....

Figrei.7.USicgsticlCusstsr99

The number of logistics clusters seems to be stable, increasing only from 60 (encompassing 93 counties)in 1998 to 61 (97 counties) in 2008. Of the original 1998 counties 72% were identified as logistics clusters10 years later. However, the 2008 data results in 10 new clusters (while nine diminished in importanceand disappeared from the listing). The most prominent of the "new" clusters is Miami. The figures alsoshow an increase in the relative concentration of the logistics industry. In general, Location Quotientvalues are higher in 2008 than in 1998 (darker in Figure 2.3 than in 2.7), as seen, for example, in Dallas,Chicago, LA, Louisville, Laredo, Houston, Seattle and Orlando.

The comparison also indicates that counties inside logistic clusters seem to be increasing in size overtime as compared to the rest of counties. Testing of the effect of clustering on logistics employmentgrowth was based on the ratio between the change in logistics employment and the change in totalemployment (logistics employment growth rate / total employment growth rate), thus normalizing for theemployment growth in the economy as a whole. This ratio was calculated in counties located inside andoutside logistics clusters, and since data are not normally distributed the Mann-Whitney U test was usedfor comparison.

30

The Mann-Whitney U test or Wilcoxon rank sum test is a non-parametric statistical hypothesis test used

to assess whether one of two samples of independent observations tends to have larger values than theother (Corder and Foreman, 2009). The test is a non-parametric analog to the independent samples t-test(see e.g. Cooper and Schindler, 2003) and can be used when it cannot be assumed that the dependentvariable is normally distributed (it is only assumed that the variable is ordinal).

Several studies have applied the Wilcoxon Rank Sum Test (WRST) to compare the distribution ofdifferent responses or validate the effectiveness of a policy. In the field of transportation studies, Rosneret al. (2003) points that the WRST is frequently used when comparing measures of location because"...the underlying distributions are far from normal or not known in advance" (Rosner et al., 2003). VanAuken and Crum (1985) used it to study the effect of the motor carrier act of 1980, and Xenias andWhitmarsh (2013) used it to analyze the differences in opinion between two groups (experts and theBritish public) regarding the sustainability of the transportation network.

This approach is more convenient than other tests because "it is easier to enter ranks into a program forparametric analysis than it is to find or write a program for a nonparametric analysis" (Conover and Iman,

1981). When studying clustering effects, the use of parametric techniques tends to underestimate the p-values and reduce the range of the confidence interval, which is why nonparametric techniques arepreferred over the F-tests and t-tests that are sensitive to the non-normality of the data. Sawilowsky(2005) claimed that it is a mistake to choose the t-test over the WRST when the interest is to test the shiftin location parameters, because it can be non-robust. Even if normality assumptions are nearly met bythe data, t-tests have a smaller power than the Wilcoxon rank sum test (De Winter and Dodou, 2010).When the data is non-normal its efficiency can exceed that of the t test by 100% (Meeter, 1968).

The null hypothesis was that there was no difference in the ratio of logistics employment growth to totalemployment growth between counties inside and outside logistics clusters, versus the alternativehypothesis that there was a difference:

HO: (logistics employment growth rate inside logistics clusters

total employment growth rate inside logistics clusters

(logistics employment growth rate outside logistics clusters

\ total employment growth rate outside logistics clusters)

Versus

H: (logistics employment growth rate inside logistics clusters

total employment growth rate inside logistics clusters

(logistics employment growth rate outside logistics clusters

k total employment growth rate outside logistics clusters )

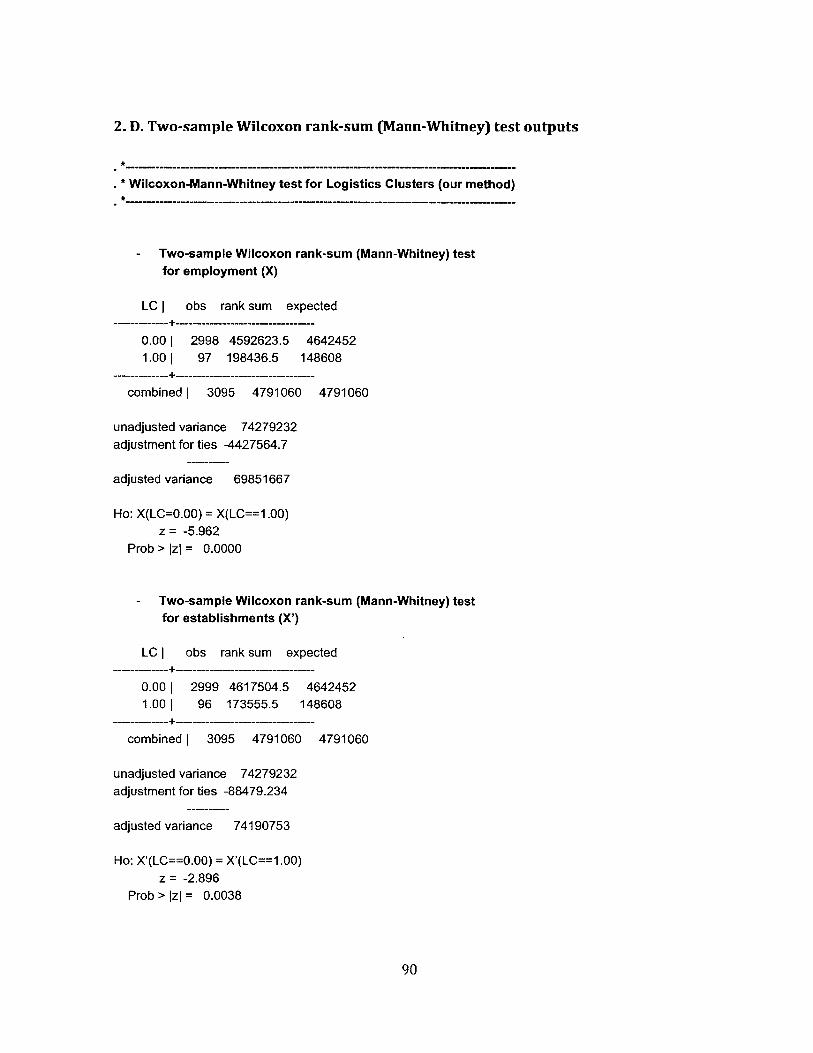

The results suggest that there is a statistically significant difference between the underlying distributionsof employment growth inside and outside logistics clusters (z = -5.962, p = 0.0000). The employmentgrowth inside logistics clusters was higher since the actual rank sums were higher than the expected ranksums under the null hypothesis. Appendix D presents the outputs of the statistical tests using STATA.

31

Due to the importance of external economics to the clustering phenomenon, an additional test examinedthe difference in the ratio between the change in logistics establishments and the change of totalestablishments (to account for changes in the whole economy) between counties located inside andoutside logistics clusters (logistics establishments' growth rate / total establishments growth rate). Theresults show that the null hypothesis of a similar growth rate (z = -2.896, p = 0.0038) can be rejected,leading to a conclusion (with 99% confidence) that there has been a difference in growth. The number ofestablishments inside logistics clusters grew at a higher rate in counties located outside clusters becausethe actual rank sums were higher than the expected rank sums under the null hypothesis (see Appendix2.D).

These tests support the assertion that the growth of logistics operations, in terms of employment andestablishments, was higher for counties located inside the identified clusters between 1998 and 2008,than for counties outside clusters. A comparison of Figure 2.7 to Figure 2.3 is in line with this finding. Asmentioned above, the relative concentration of the logistics industry increased between 1998 and 2008and in general - HCLQ values are higher in 2008. Some existing clusters seem to be expanding even toneighboring counties. That was the case, in particular, in Dallas, Atlanta and Allentown/Harrisburg (PA).For instance, in Atlanta, logistics operations were agglomerated in Chatham and Clay counties in 1998,and ten years later they extended to three additional counties (Decatur, Franklin and Worth). In theAllentown/Harrisburg region the logistics industry was concentrated in York, Luzerne, Lehigh, Lancaster,Delaware and Berks counties in 2008, while this concentration was observed only in York in 1998.Naturally, the decline of logistics activities in some Mid-West areas may be a reflection of the decreasingmanufacturing activities in the US heartland, while the increase in other areas is likely rooted in theincreased cross country trade flows, and in particular, imports.

32

Chapter 3

Relationship between freight accessibilityand logistics employment in US counties 3

3.1. Introduction

One of the key factors to a region's economic performance is a reliable and efficient transportationinfrastructure. "A well-developed transportation system provides adequate access to the region, which inturn is a necessary condition for the efficient operation of the manufacturing, retail, labor, and housingmarkets" (Ozbay et al., 2006, p.3). The accessibility of a location is, naturally, an important factor for thelocation decision of logistics companies (such as third party logistics service providers, warehouses,motor carriers, and the logistics/distribution operations of retailers, distributors and manufacturers). Betteraccessibility results in lower transportation costs and a shorter time to the market (Limbo and Venables,2001), which have a direct impact on the cost and service level that logistics operations enjoy. Therefore,logistics employment is expected to be concentrated in areas that are highly accessible. Hence, it is notsurprising that improvements to the road network significantly affect the location of agglomerations oflogistics firms (Taniguchi et al., 1999), that logistics clusters in the US are primarily developed close tomajor airports and seaports and in central areas such as Chicago, Kansas City and Dallas (Rivera et al.,2014), or that logistics establishments in the Netherlands relocate relatively often in areas with intermodalterminals (Van den Heuvel et al., 2013). This chapter analyzes whether there is a general relationbetween freight accessibility and logistics employment. This topic may be especially relevant givenHesse's (2008) argument that logistics investments may accelerate economic development of areas. Thisargument is also advanced by Sheffi (2012), who demonstrates that logistics clusters attractmanufacturing sub-clusters.

Several studies have found that accessibility is an important factor for urbanization (population andemployment growth, see e.g. Jiwattanakulpaisarn et al., 2010; Song et al., 2012). However, therelationship between freight accessibility and logistics employment has hardly been studied. Such ananalysis requires a measure of freight accessibility. Although freight accessibility is important for locationdecisions of companies (Porter and Rivkin, 2012), limited efforts have been put in developing freightaccessibility measures. This chapter addresses these gaps; a freight accessibility index is developed and

the relationship between freight accessibility and logistics employment is analyzed.

3 The content of this chapter has also been presented in Van den Heuvel et al. (2014). Besides Liliana Rivera andYossi Sheffi this paper was coauthored by Fran Van de Heuvel, Peter de Langen, Jan Fransoo, Karel van Donselaar,and Ad de Jong from the Eindhoven University of Technology.

33

The remainder of this chapter is structured as follows. Section 3.2 presents an overview of the relevantliterature on the relationship between accessibility and employment, while Section 3.3 reviews theacademic literature on accessibility measures. Section 3.4 presents an accessibility measure especiallydeveloped for freight transport. Using data at the county level in the US, Section 3.5 presents the analysisinto the relation between freight accessibility and logistics employment per county, based on a PartialLeast Squares model. Finally, Section 3.6 concludes the chapter and discusses options for furtherresearch.

3.2. Relationship between accessibility and employment