1 CHAPTER – 1 PROFILE OF THE COMPANY

Project Report Main

Dec 12, 2015

project report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

CHAPTER – 1

PROFILE OF THE COMPANY

2

1.1 Introduction to HDFC BANK Ltd.

The Housing Development Finance Corporation Limited (HDFC) was amongst the

first to receive an ‘in principle’ approval from the Reserve Bank of India (RBI) to set up a

bank in the private sector, as part of RBI’s liberalization of the Indian Banking Industry in

1994. The bank was incorporated in August 1994 in the name of ‘HDFC Bank Limited’,

with its registered office in Mumbai, India. HDFC Bank commenced operations as a

Scheduled Commercial Bank in January 1995.

HDFC Bank’s objective is to build sound customer franchises across distinct businesses

so as to be the preferred provider of banking services for target retail and wholesale

customer segments, and to achieve healthy growth in profitability, consistent with the

bank’s risk appetite. The bank is committed to maintain the highest level of ethical

standards, professional integrity, corporate governance and regulatory compliance. HDFC

Bank’s business philosophy is based on five core values: Operational Excellence,

Customer Focus, Product Leadership, Sustainability and People.

3

1.11 Company Information

S.no Particulars Details

1. Name HDFC Bank Ltd.

2. Logo

3. Address HDFC Bank Ltd., 9th Floor, Ansal Tower,

Rajouri Garden, New Delhi.

Tel: 7428122352

4. Registered Office HDFC Bank House, Senapati Bapat Marg,

Lower Parel (W), Mumbai - 400 013

Tel: +91 - 22 - 6652 1000

5. Branches 3,403 branches in 2,171 locations.

6. Website www.hdfcbank.com

7. E-Mail [email protected]

Table No – 1.1: Company Information and Contact Details

4

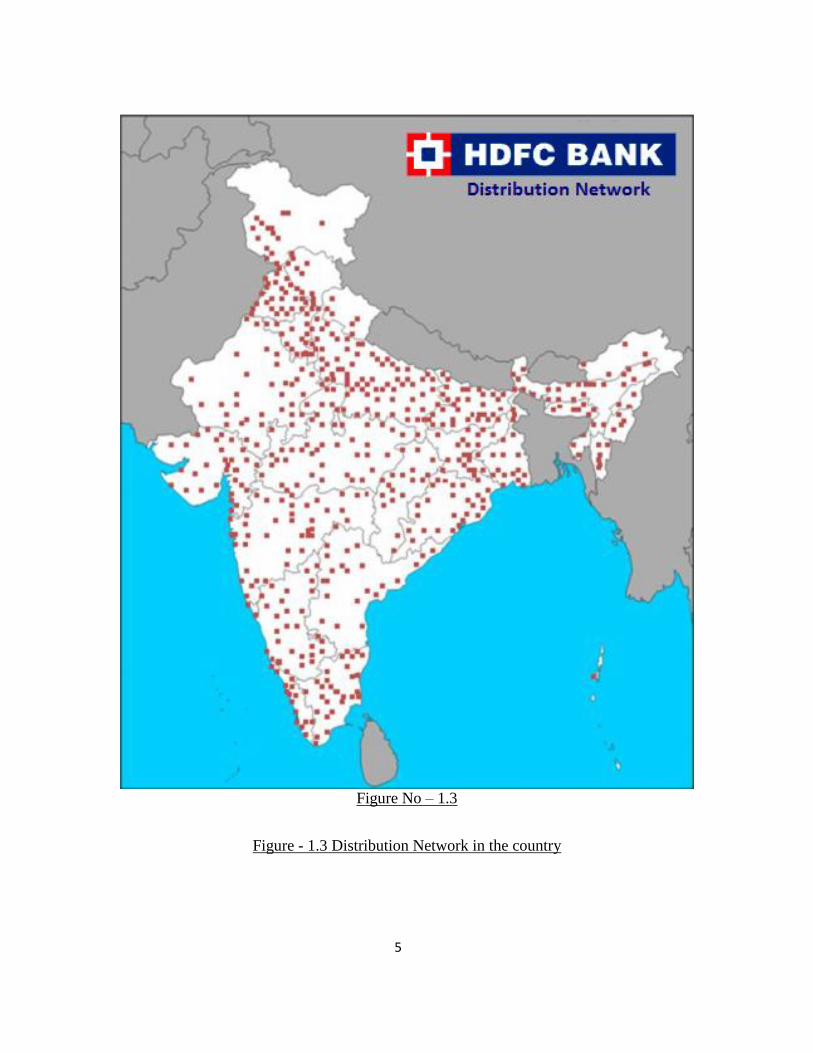

1.12 Distribution Network

HDFC Bank is headquartered in Mumbai. As of March 31, 2014, the Bank’s distribution

network was at 3,403 branches in 2,171 locations. All branches are linked on an online

real-time basis. Customers in over 1397 locations are also serviced through Telephone

Banking. The Bank’s expansion plans take into account the need to have a presence in all

major industrial and commercial centers, where its corporate customers are located, as well

as the need to build a strong retail customer base for both deposits and loan products. Being

a clearing / settlement bank to various leading stock exchanges, the Bank has branches in

centers where the NSE/BSE have a strong and active member base.

The Bank also has a network of 11,256 ATMs across India. HDFC Bank’s ATM network

can be accessed by all domestic and international Visa / MasterCard, Visa Electron /

Maestro, Plus / Cirrus and American Express Credit / Charge cardholders.

Figure No - 1.1 Figure No - 1.2

Figure - 1.1 & 1.2 Increase in Branches and Locations over the years

5

Figure No – 1.3

Figure - 1.3 Distribution Network in the country

6

1.2 Business Profile

HDFC Bank caters to a wide range of banking services covering commercial and

investment banking on the wholesale side and transactional / branch banking on the retail

side. The bank has three key business segments:

a. Wholesale Banking

b. Retail Banking

c. Treasury

1.21 Wholesale Banking

The Bank’s target market is primarily large, blue-chip manufacturing companies in the

Indian corporate sector and to a lesser extent, small & mid-sized corporates and agri-based

businesses. For these customers, the Bank provides a wide range of commercial and

transactional banking services, including working capital finance, trade services,

transactional services, cash management, etc. The bank is also a leading provider of

structured solutions, which combine cash management services with vendor and

distributor finance for facilitating superior supply chain management for its corporate

customers. Based on its superior product delivery / service levels and strong customer

orientation, the Bank has made significant inroads into the banking consortia of a number

of leading Indian corporates including multinationals, companies from the domestic

business houses and prime public sector companies. It is recognized as a leading provider

7

of cash management and transactional banking solutions to corporate customers, mutual

funds, stock exchange members and banks.

1.22 Retail Banking

The objective of the Retail Bank is to provide its target market customers a full range of

financial products and banking services, giving the customer a one-stop window for all

his/her banking requirements. The products are backed by world-class service and

delivered to customers through the growing branch network, as well as through alternative

delivery channels like ATMs, Phone Banking, Net Banking and Mobile Banking.

The HDFC Bank Preferred program for high net worth individuals, the HDFC Bank Plus

and the Investment Advisory Services programs have been designed keeping in mind

needs of customers who seek distinct financial solutions, information and advice on

various investment avenues. The Bank also has a wide array of retail loan products

including Auto

Loans, Loans against marketable securities, Personal Loans and Loans for Two-wheelers.

It is also a leading provider of Depository Participant (DP) services for retail customers,

providing customers the facility to hold their investments in electronic form. HDFC Bank

was the first bank in India to launch an International Debit Card in association with VISA

(VISA Electron) and issues the MasterCard Maestro debit card as well. The Bank launched

its credit card business in late 2001. By March 2013, the bank had a total card base (debit

and credit cards) of over 19.7 million.

8

The Bank is also one of the leading players in the “merchant acquiring” business with over

270,000 Point-of-sale (POS) terminals for debit / credit cards acceptance at merchant

establishments. The Bank is well positioned as a leader in various net based B2C

opportunities including a wide range of internet banking services for Fixed Deposits,

Loans, Bill Payments, etc.

1.23 Treasury

Within this business, the bank has three main product areas - Foreign Exchange and

Derivatives, Local Currency Money Market & Debt Securities, and Equities. With the

liberalization of the financial markets in India, corporates need more sophisticated risk

management information, advice and product structures. These and fine pricing on various

treasury products are provided through the bank’s Treasury team. To comply with

statutory reserve requirements, the bank is required to hold 25% of its deposits in

government securities. The Treasury business is responsible for managing the returns and

market risk on this investment portfolio.

1.3 HDFC Bank’s Vision and Mission

1.31 Vision of the Company

“To build a World-Class Indian Bank” By offering a wide of relevant products and

services.

a. Tailored Solutions for Customers.

b. Ensure Unmatched Customer Service.

9

c. Providing the Right Solution at Right Place.

d. Have Wide and Extensive Reach.

The delivery backbone for providing the above shall be by adopting world class

technology.

1.32 Mission and Core Values of the Company

Use Enabling Technology to provide valued added products and services to customers.

The Objective is to build sound customer franchises across distinct businesses so as to be

the preferred provider of banking services for target retail and wholesale customer

segments, and to achieve healthy growth in profitability, consistent with the bank’s risk

appetite. The bank is committed to maintain the highest level of ethical standards,

professional integrity, corporate governance and regulatory compliance.

In order to achieve the above said mission bank follows certain values.

The Bank’s Five Core Values are:

(a) Customer Focus: To Achieve sustainable competitive advantage. HDFC Bank relies not

only on strong customer service, but also on measuring customer experience. The Bank

has invested in CRM Technology which provides triggers for selling various products

depending on the customer profile. The Relationship Manager is a trusted advisor to the

customer – he/she has the best interest of the customer and can advise competitor product,

if the Bank’s product does not fit Customer needs.

10

(b) Operational Excellence: With a dedicated team to monitor quality and service standards,

several of HDFC Bank’s process segments, including HR Operations are ISO certified.

Over 2200 quality improvement projects, aimed at improving operational excellence have

been successfully implemented. Over 550 employees have qualified for Six Sigma

Certification and over 80 have earned the yellow belt.

(c) Product Leadership: HDFC Bank has consistently developed innovative products and

services that attract its targeted customers. Focusing on high earnings growth and low

volatility, HDFC Bank continues to develop and distribute products / services that reduce

cost of funds, by leveraging its extensive branch network. The Bank actively tracks the

performance of various products and depending on the feedback received, tweaks product

features, to better address the customer needs.

(d) Sustainability: HDFC Bank recognize Social and Environmental aspects as essential

elements of a Sustainable business philosophy and is committed to enhance its

performance on these fronts.

(e) People: People are the Bank’s greatest strength. HDFC Bank believes that the ultimate

identity and success of Bank will reside in the exceptional quality of its people and their

extraordinary efforts. For this reason, the Bank is committed to hiring, developing,

motivating and retaining the best people in the industry.

People Value can be defined as: (Professionalism, Respect for Individual,

“Can Do” Attitude, and Employee Care)

11

1.4 Product Range under Business Banking Mortgages

1.41 Loan against Property- LAP

It is a loan given on the basis of the market value of the property held by the applicant and

Restricted by repayment capacity. The property acts as a collateral and is oral mortgaged

as against the loan facility. Simple tool of raising credit against existing property for all

personal and business needs of a customer. (Loan can be easily processed once a Do-ability

Check is done)

1.42 Loan to Purchase Commercial Property- LCP

It is also a loan which is provided to applicant where he/she wants to buy a commercial

property for business

1.43 Overdraft against property- DOD

An Overdraft facility offered against self-occupied Residential & Commercial Property.

Considering the eligibility of the customer, line of credit is provided to the customer with

easy re-payment option.

1.44 Loan against Rental Receivables- LARR

Lease Rental Discounting of Commercial Property where the tenant is a reputed Corporate.

Only Commercial Property as considered as collateral.

12

1.5 Size of Organization

1.51 Size of Manpower

The Bank has branches in over five hundred cities covering a wide geographical area of

the country. Employees come from varied cultural, social and ethnic backgrounds.

Employees are Bank’s greatest assets. As of 31 March 2014, 50,906 employees were part

of the HDFC Bank. The follow a non-discrimination policy with regards to employment

and have employees with varied degrees of disabilities in certain functions of the bank.

1.52 Turnover and Financials

(a) Profit and Loss Account: Year ended March 31, 2014

For the year ended March 31, 2014, the Bank earned total income of `49,055.17’ crores.

Net revenue for the year ended March 31, 2014 were `26,402.27’ crores, up by 16.49%

over 22,663.7 crores for the year ended March 31, 2013. The Banks Net Profit for the

year ended March 31, 2014 was `8478’ crores, up 26.04%, over the year 2013.

Figure No - 1. 4

Figure – 1.4 Increase in Net Profit over the years

13

(b) Balance Sheet: As of March 31, 2014

The Bank’s total balance sheet size increased by 22.8% to Rs 491,600 crores as of March

31, 2014 from Rs 400,332 crores as of March 31, 2013. Total net advances as of March

31, 2014 were Rs 303,000 crores, an increase of 26.4% over March 31, 2013. Total

Deposits were Rs 367,337.5 crores, an increase of 24% over March 31, 2013.

Figure No - 1.5

Figure No - 1.6

Figure - 1.5 & 1.6 Increase in Balance Sheet and Advances over the years

Figure No - 1.7 Figure No - 1.8

Figure - 1.7 & 1.8 Increase in Deposits and Saving Deposits over the years

14

1.6 Organisation Structure of the Company

Mr. C.M. Vasudev has been appointed as the Chairman of the Bank with effect from 6th

July 2010 subject to the approval of the shareholders. Mr. Vasudev has been a Director of

the Bank since October 2006. A retired IAS officer, Mr. Vasudev has had an illustrious

career in the civil services and has held several key positions in India and overseas,

including Finance Secretary, Government of India, Executive Director, World Bank and

Government nominee on the Boards of many companies in the financial sector.

The Bank’s Managing Director, Mr. Aditya Puri, has been a professional banker for

over 25 years and before joining HDFC Bank in 1994 was heading Citibank's operations

in Malaysia. The Bank's Board of Directors comprises of eminent individuals with a wealth

of experience in public policy, administration, industry and commercial banking. Senior

executives representing HDFC are also on the Board.

Senior banking professionals with substantial experience in India and abroad, head various

businesses and functions and report to the Managing Director. Given the professional

expertise of the management team and the overall focus on recruiting and retaining the

best talent in the industry, the bank believes that its people are a significant competitive

strength.

15

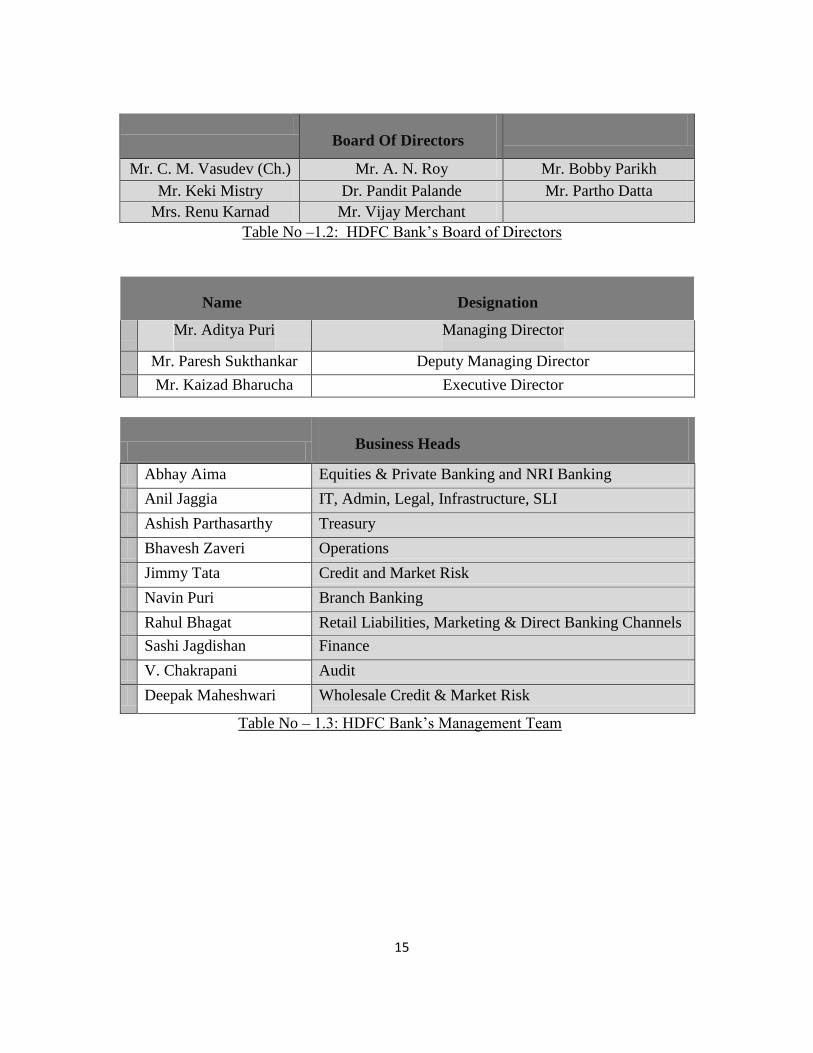

Board Of Directors

Mr. C. M. Vasudev (Ch.) Mr. A. N. Roy Mr. Bobby Parikh

Mr. Keki Mistry Dr. Pandit Palande Mr. Partho Datta

Mrs. Renu Karnad Mr. Vijay Merchant

Table No –1.2: HDFC Bank’s Board of Directors

Name Designation

Mr. Aditya Puri Managing Director

Mr. Paresh Sukthankar Deputy Managing Director

Mr. Kaizad Bharucha Executive Director

Business Heads

Abhay Aima Equities & Private Banking and NRI Banking

Anil Jaggia IT, Admin, Legal, Infrastructure, SLI

Ashish Parthasarthy Treasury

Bhavesh Zaveri Operations

Jimmy Tata Credit and Market Risk

Navin Puri Branch Banking

Rahul Bhagat Retail Liabilities, Marketing & Direct Banking Channels

Sashi Jagdishan Finance

V. Chakrapani Audit

Deepak Maheshwari Wholesale Credit & Market Risk

Table No – 1.3: HDFC Bank’s Management Team

16

1.7 Market Position of HDFC Bank

HDFC Bank is one of the Top Four banks in India along with State Bank Of India, Axis

Bank and ICICI Bank. However as per the “The Business Today-KPMG Best Bank 2013

study” HDFC Bank has emerged as the best large bank because of good asset quality,

high loan growth, a healthy capital adequacy ratio and an improvement in returns on capital

employed.

Figure – 1.9: HDFC ranks first amongst Top Performing Banks in Country

17

1.8 Leadership Initiatives

a. During the Internship session there were many occasions when client meetings

happened and initiatives were taken to be the active participant of the conversation and also there was regular interaction with the employees of the Organization.

b. Telephonic conversation with clients to get their feedback about the services.

c. Client visits with the Banks Representative to get a fair idea about quoting for a product.

Names of Employees

S.no Particulars Details

1 Amit Munjal Sales Manager (Internship Mentor)

2 Nikhil Rahi Area Sales Manager

3 Nirmal Kalra Credit Manager

4 Mahinder Seth Branch Manager

Table No – 1.4: Interaction with Employees

1.9 Sources of Data Collection

1.91 Primary Data Source

Primary Data was gathered by asking and collecting information from the Internship

Mentor Mr. Amit Munjal and also by communicating with other employees.

18

Personal Observation also played an important role to get to know about organization’s

internal environment and client dealing.

1.92 Secondary Data Source

a. Data collected from hdfcportal a knowledge center available within the

organization’s intranet.

b. Help of Online material from www.hdfcbank.com

http://businesstoday.intoday.in/ (KPMG Report)

c. Annual Report of HDFC BANK year 2013-2014 & 2012-2013.

19

CHAPTER – 2

SWOT ANALYSIS

20

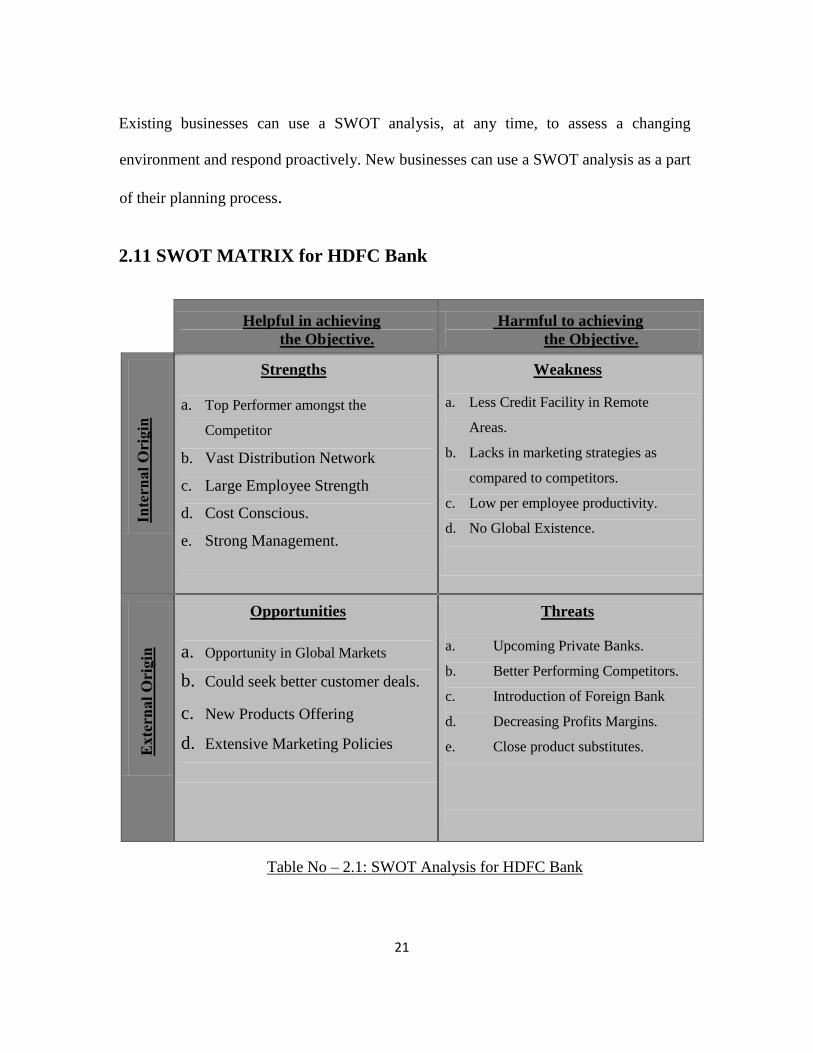

2. SWOT ANALYSIS

S.W.O.T. is an acronym stands for Strengths, Weaknesses, Opportunities, and Threats.

SWOT analysis is an organized list of a business’s greatest strengths, weaknesses,

opportunities, and threats. A SWOT analysis can be carried out for a product, place,

industry or person. It involves specifying the objective of the business venture or project

and identifying the internal and external factors that are favorable and unfavorable to

achieve that objective.

The technique is credited to Albert Humphrey, who led a convention at the Stanford

Research Institute (now SRI International) in the 1960s and 1970s using data from

Fortune 500 companies. The degree to which the internal environment of the firm

matches with the external environment is expressed by the concept of strategic fit.

Setting the objective should be done after the SWOT analysis has been performed. This

would allow achievable goals or objectives to be set for the organization.

Strengths: are the characteristics of the business that give it an advantage over others.

Weaknesses: are the characteristics that place the business or project at a disadvantage

relative to others.

Opportunities: elements that the project could exploit to its advantage

Threats: elements in the environment that could cause trouble for the business or project

21

Existing businesses can use a SWOT analysis, at any time, to assess a changing

environment and respond proactively. New businesses can use a SWOT analysis as a part

of their planning process.

2.11 SWOT MATRIX for HDFC Bank

Helpful in achieving

the Objective.

Harmful to achieving

the Objective.

Strengths

a. Top Performer amongst the

Competitor

b. Vast Distribution Network

c. Large Employee Strength

d. Cost Conscious.

e. Strong Management.

Weakness

a. Less Credit Facility in Remote

Areas.

b. Lacks in marketing strategies as

compared to competitors.

c. Low per employee productivity.

d. No Global Existence.

Opportunities

a. Opportunity in Global Markets

b. Could seek better customer deals.

c. New Products Offering

d. Extensive Marketing Policies

Threats

a. Upcoming Private Banks.

b. Better Performing Competitors.

c. Introduction of Foreign Bank

d. Decreasing Profits Margins.

e. Close product substitutes.

Table No – 2.1: SWOT Analysis for HDFC Bank

22

2.12 Strengths

(a) Top Performer amongst the Competitor:

HDFC Bank has emerged as the best large bank because of good asset quality, high loan

growth, a healthy capital adequacy ratio and an improvement in returns on capital

employed

(b) Vast Distribution Network:

Bank’s distribution network was at 3,403 branches in 2,171 locations.

(c) Large Employee Strength:

Bank has huge employee base of 69,065 people as of 31st March 2013.

(d) Cost Conscious:

Bank has its unique cost management practices which helps in controlling the operating

cost within defined budgetary parameters.

(e) Strong Management:

Senior banking professionals with substantial experience in India and abroad, head various

businesses and functions

23

2.13 Weakness

(a) Less Credit Facility in Remote Areas

Bank is conservative in providing credit facility in rural areas as compared to the urban

area.

(b) Lacks in marketing strategies as compared to competitors:

Bank does not follow extensive marketing techniques as competitor banks do.

(c) Low per employee productivity:

Even after having a huge employee base, per employee productivity is not adequate

(d) No Global Existence:

HDFC Bank operates with in the country it only have 2 Branches outside the nation.

2.14 Opportunities

(a) Opportunity in Global Markets:

HDFC Bank can achieve new horizons in global markets looking at the performance within

the country.

(b) Could seek better customer deals:

Bank could come up with fairer customer deals to increase their existing and prospect

customers.

24

(c) New Products Offering:

Newer products with more benefits to customer will help the bank to survive the

competition in terms of close substitute products.

(d) Extensive Marketing Policies:

Extensive marketing policies can be adopted to reach out the masses.

2.15 Threats

(a) Upcoming Private Banks:

Entry of new private banks into the market may act as a threat to the Bank.

(b) Better Performing Competitors:

Competitors like ICICI Bank and Axis Bank is not far behind. Their performance is also

improving.

(c) Introduction of Foreign Bank:

Entry of big foreign Banking players in Indian market will be a threat to the bank

(d) Decreasing Profits Margins:

Bank is performing well however its profits margin are increasing but at a decreasing rate

and that can be seen in the financials of the Bank.

25

(e) Close product substitutes:

Customer while opting for Banking products or services easily substitute their choice

having very small variation in interest rates

2.2 Best Practices in Different Functional Areas

2.21 Human Resource

Human Resources Development has been a key and constant focus area for bank. The

human resources agenda, that includes within its gamut the attraction and retention of

talent, skills development, reward and recognition, performance management and

employee engagement are realized through a number of key initiatives, systems and

processes.

a) Employee Development: Performance Management is one of the most critical

dimensions pertaining to the management of human resources and the Organization has a

comprehensive Performance Management System (PMS) to assess performance. The PMS

facilitates the differentiation between the various categories of performance. Higher

rewards for higher levels of performance have been a fundamental philosophy of bank.

Employee development and growth is realized through an array of functional and

behavioral programs that bank conducts throughout the year as well as on the job training.

26

b) Rewards and Recognition: Rewards and Recognition play a key role to attract, retain

and engage employees. Bank is committed to ensure that employees are competitively

positioned vis-à-vis market with respect to both fixed as well as variable pay.

2.22 Information Technology

HDFC Bank operates in a highly automated environment in terms of information

technology and communication systems.

All the bank’s branches have online connectivity, which enables the bank to offer speedy

funds transfer facilities to its customers. Multi-branch access is also provided to retail

customers through the branch network and Automated Teller Machines (ATMs). The Bank

has made substantial efforts and investments in acquiring the best technology available

internationally, to build the infrastructure for a world class bank. In terms of core banking

software, the Corporate Banking business is supported by Flexcube, while the Retail

Banking business by Finware, both from i-flex Solutions Ltd. The systems are open,

scalable and web-enabled.

The Bank has prioritized its engagement in technology and the internet as one of its key

goals and has already made significant progress in web-enabling its core businesses. In

each of its businesses, the Bank has succeeded in leveraging its market position, expertise

and technology to create a competitive advantage and build market share.

27

2.23 SLI Initiative-Sustainable Livelihood Initiative:

Bank is committed to reaching out to the unbanked and under banked people at the bottom

of the pyramid, particularly in rural India and bringing them into the banking fold.

Bank’s Sustainable Livelihood Initiative has helped empower thousands of people,

particularly women, in rural parts of India.

Through this initiative, the Bank reaches out to the un-banked and under-banked segment

of the population and in doing so, helps as many people as possible at the bottom of the

pyramid by providing them with livelihood training and finance.

It involves a holistic approach- from offering training and enhancing occupation skills to

providing credit counseling, financial literacy and market linkages – which financially

empowers people and brings them into the banking fold. About 9 lac families were covered

this year and about 27 lac families have so far benefitted from this initiative.

2.24 Corporate Governance

The Bank believes in adopting and adhering to the best recognized corporate governance

practices and continuously benchmarking itself against each such practice. The Bank

understands and respects its fiduciary role and responsibility towards its shareholders and

strives hard to meet their expectations. The Bank believes that best board practices,

transparent disclosures and shareholder empowerment are necessary for creating

shareholder value.

28

The Bank has infused the philosophy of corporate governance into all its activities. The

philosophy on corporate governance is an important tool for shareholder protection and

maximization of their long term values. The cardinal principles such as independence,

accountability, responsibility, transparency, fair and timely disclosures, credibility,

sustainability etc. serve as the means for implementing the philosophy of corporate

governance in letter and spirit.

2.3 Deviations

a. Even after having strong HR Policies job security is a concern for employees.

b. Customer Satisfaction is always treated as the main focus of any Organization in books

however in real life scenario completion of targets on time is a bigger priority

29

CHAPTER – 3

DATA COLLECTION & PRESENTATION

30

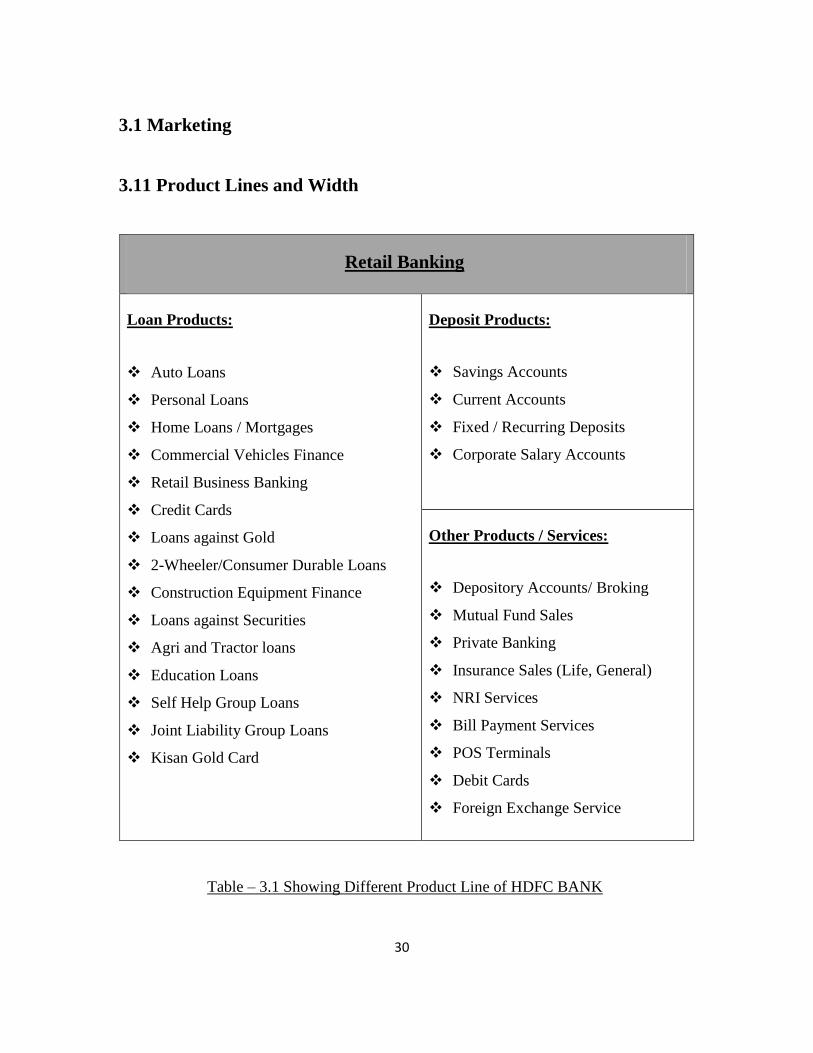

3.1 Marketing

3.11 Product Lines and Width

Retail Banking

Loan Products:

Auto Loans

Personal Loans

Home Loans / Mortgages

Commercial Vehicles Finance

Retail Business Banking

Credit Cards

Loans against Gold

2-Wheeler/Consumer Durable Loans

Construction Equipment Finance

Loans against Securities

Agri and Tractor loans

Education Loans

Self Help Group Loans

Joint Liability Group Loans

Kisan Gold Card

Deposit Products:

Savings Accounts

Current Accounts

Fixed / Recurring Deposits

Corporate Salary Accounts

Other Products / Services:

Depository Accounts/ Broking

Mutual Fund Sales

Private Banking

Insurance Sales (Life, General)

NRI Services

Bill Payment Services

POS Terminals

Debit Cards

Foreign Exchange Service

Table – 3.1 Showing Different Product Line of HDFC BANK

31

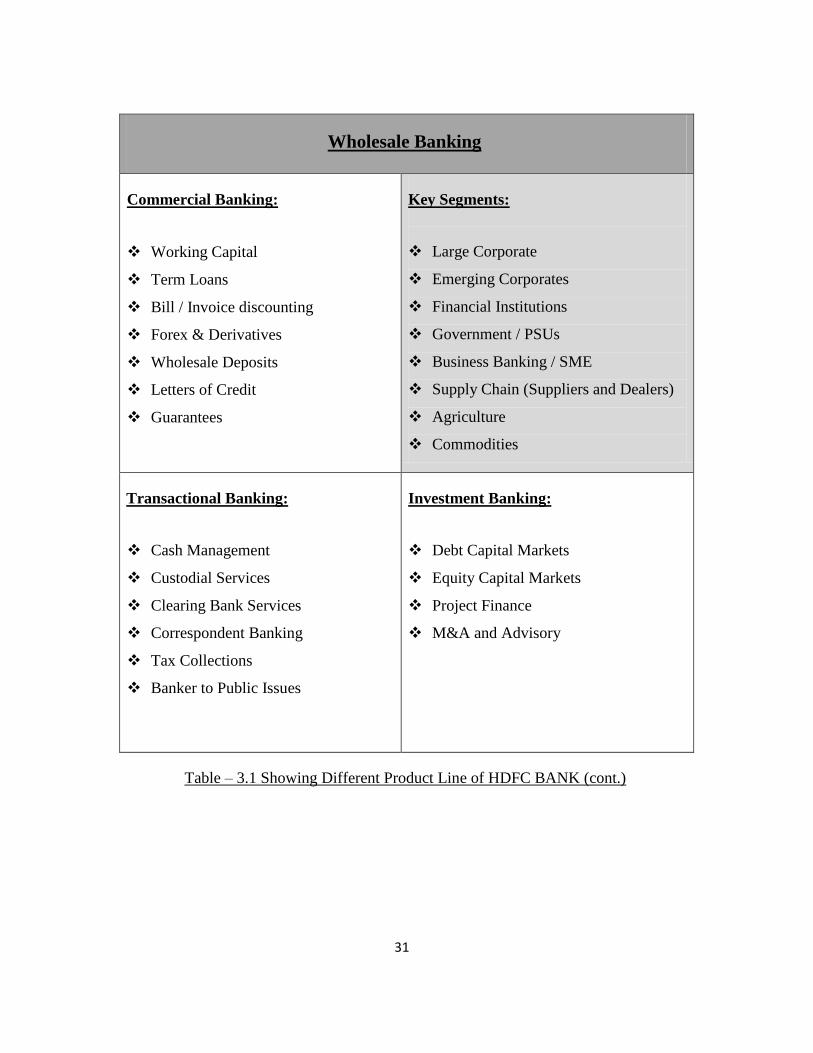

Wholesale Banking

Commercial Banking:

Working Capital

Term Loans

Bill / Invoice discounting

Forex & Derivatives

Wholesale Deposits

Letters of Credit

Guarantees

Key Segments:

Large Corporate

Emerging Corporates

Financial Institutions

Government / PSUs

Business Banking / SME

Supply Chain (Suppliers and Dealers)

Agriculture

Commodities

Transactional Banking:

Cash Management

Custodial Services

Clearing Bank Services

Correspondent Banking

Tax Collections

Banker to Public Issues

Investment Banking:

Debt Capital Markets

Equity Capital Markets

Project Finance

M&A and Advisory

Table – 3.1 Showing Different Product Line of HDFC BANK (cont.)

32

Treasury

Products / Segments:

Foreign Exchange

Debt Securities

Derivatives

Equities

Other Functions:

Asset Liability Management

Statutory Reserve Management

Table – 3.1 Showing Different Product Line of HDFC BANK (cont.)

3.12 Channel Management

The Bank has a distribution network of 3,403 branches in 2,171 locations. All branches

are linked on an online real-time basis. Handling Customer base of over 28 million, new

customer acquisition of 3 million in FY 2014.

(a) Classification of Branches on the Basis of Locations

Figure – 3.1 Showing Distribution of Branches over the Years

(cont.)

33

3.13 Customer Relationship Management

HDFC bank uses CRM technology when interacting with the customers. They are as

follows; Call center Automation, Data warehousing, Email Management, Field Service

Automation, and Marketing Automation.

(a) The bank selected CRMnext's solution in 2008 which promised to fulfill the bank’s

needs. Including the following

i. Creating a unified customer view by collating and massaging data from various

sources including the data warehouse.

ii. Controlling customer information based on the role of users.

iii. Enabling aces to single view across various channels like branch, phone banking,

etc.

iv. Ensuring information availability at al customer touch points to boost the quality

of interactions.

(b) Cross Selling Capability The platform operates across all channels, providing global

visibility and status of offers. Various systems integrated to provide event based

triggering such as large deposits, channel usage, etc. Marketing team continuously

generates cross-sell offers and next best products to be sold and provides one stop

solution for all customer needs.

34

3.14 Major Competitors (in Private Sector)

BASIS ICICI BANK YES BANK AXIS BANK

Marketing

Outlook

Aggressive Marketing Knowledge banking

approach

Rebranding from

previous UTI

CRM as

Focus Area

Marketing and

competitive sales

approach

To have more

interactive

approach.

To have broader

markets

Online

Popularity

It is now ranked as

2nd

Establishing market

through Social

networking sites

Following

footsteps of others

Market

Segment

Bank young stars,

bank @campus, and

women account

Retail segment

As a preferred

partner in

progress.

Table – 3.2 Major Competitors of Bank

35

3.14 Environmental Responsibility

Your Bank regards climate change mitigation and environmental improvements as

essential elements of a sustainable business. This belief embodies the Bank’s approach on

reduction of carbon emissions. The Bank has taken various steps to manage GHG emission,

through multichannel delivery such as ATMs, PhoneBanking, NetBanking and

MobileBanking which have cut down customers' need to commute to our branches. Bank

has ensured that many of its major locations have energy efficient lighting systems in place.

Bank has also adopted a ‘Phase-out’ policy to replace inefficient lighting options and have

also started incorporating the use of unconventional energy sources to power our ATMs in

areas with fluctuating power supply. Promotion of video conference and video chatting on

IP phone has also resulted in reducing travelling and fuel consumption; Bank has also

introduced server and desktop Virtualization thereby reducing Power Consumption.

Bank performs some of the following practices to lead a better environment:

a) Reducing the Use of Paper

b) Energy Conservation

c) Exploring Renewable Energy

d) Managing Waste

e) Green Procurement

36

3.2 Human Resource Management

HDFC Bank is a young and dynamic bank, with a youthful and enthusiastic team

determined to accomplish the vision of becoming a world-class Indian bank. Believing

that the ultimate identity and success of bank will reside in the exceptional quality of

people and their extraordinary efforts. For this reason, HDFC is committed to hiring,

developing, motivating and retaining the best people in the industry

Bank’s Total employee strength is 69,065 as of 31st March 2013.Which is a big advantage

to the Bank.

Recruiting and selecting the right people is paramount to the success of the HDFC BANK

LTD. and its ability to retain a workforce of the highest quality. This recruitment and

selection policy sets out the procedure to ensure that the best people are recruited on merit

and that are the recruitment process is free from bias and discrimination.

3.12 Recruitment & Selection Process

(a) Candidate sourcing:

The hiring manager along with the Human Resource Department would decide the channel

/ source to use based on the nature of the recruitment.

37

The following sources of recruitment may be considered.

i. Internal Sources

Whenever any vacancy arises, the possibility of fulfilling the requirement internally via

reassignment and relocation, re-allocation of the responsibilities or internal promotion will

be explored by the hiring function along with the HR Department. Internal job postings to

explore internal candidates.

Employee Referrals – HDFC encourages employees to refer suitable candidates for open

positions.

ii. External Sources

Recruitment agencies, External job postings, College / campus requirement, Requirement

advertisements.

(c) Interview Process

i. All candidates are required to undergo a face to face interview with the interview

panel before selection.

ii. Interviews may be conducted at a place at mutually convenient locations and time

in an effort to maintain confidentiality of the hiring effort.

iii. One on one meeting shall be preferred as the interview format, however

depending on the constraints panel interviews / telephone / video conference

screening could be used.

38

iv. For recruitment at junior levels, job fairs, universities etc, where large volume of

candidates, HDFC will use recruitment tests for purpose of short listing. The

candidate may be tested on the basic aptitude, analytical skills or other skills

required for the job of the candidates.

v. The interview process will focus on the evaluating the candidates suitability in

terms of the job description and fit within the organization.

vi. Each interviewer will complete the interview feedback form and submit it to HR.

HR will compile the results from a various interviews and provide these to the

line manager for the final decision.

(d) Pre-Employment Check

i. This will include both a professional reference check as well as the background

check.

ii. Professional reference check will be completed by the hiring manager. HDFC

will request contact information for 2 references from the candidate, and check

the quality of previous work experience and key personal

characteristics/conduct/ previous record etc.

iii. For key positions in areas, HDFC will also perform a background check to assess

the integrity / conduct of the candidate.

39

iv. The following information regarding the candidate will be verified:

Proof of educational qualifications, Any professional certificate that is essential

to the job

v. Address and Passport Details.

vi. Date of birth Proof of previous employment (service certificate)

Any negative feedback and comment in the reference check will be investigated

by HR and if found genuine shall be a cause for disqualification of the candidate

or dismissal from employment.

(e) Offer Process

i. Once the hiring decision is finalized, HR will prepare an offer / fitment as per

the compensation structure and grade and keeping in mind the internal equity.

ii. The offer would be communicated to the selected candidates by the hiring

manager along with HR. The candidate will sign the contract letter to formally

accept employment from the organization.

(f) Probation Policy

Probation is a trial that is mutual opportunity for the employee and HDFC to confirm

suitability for continued employment. The probation period is to establish a stronger

understanding of mutual capabilities, expectations and understanding which may include

40

functional training. The employee must demonstrate suitability for continued employment.

An assessment will be based on factors related to work performance, work habits,

productivity, attitude and compatibility, attendance and punctuality, and any other matter

that is linked to job performance and expectations.

All new hires will be placed on probation for a period of 6 months from the date of joining

HR will initiate the confirmation process by sending an appraisal form to the immediate

supervisor before the completion of probationary period.

The appraisal form will need to be approved by the supervisor’s leadership

all letters of confirmation or extension of probation will be signed by the HR head and

will be stored in employee file for records.

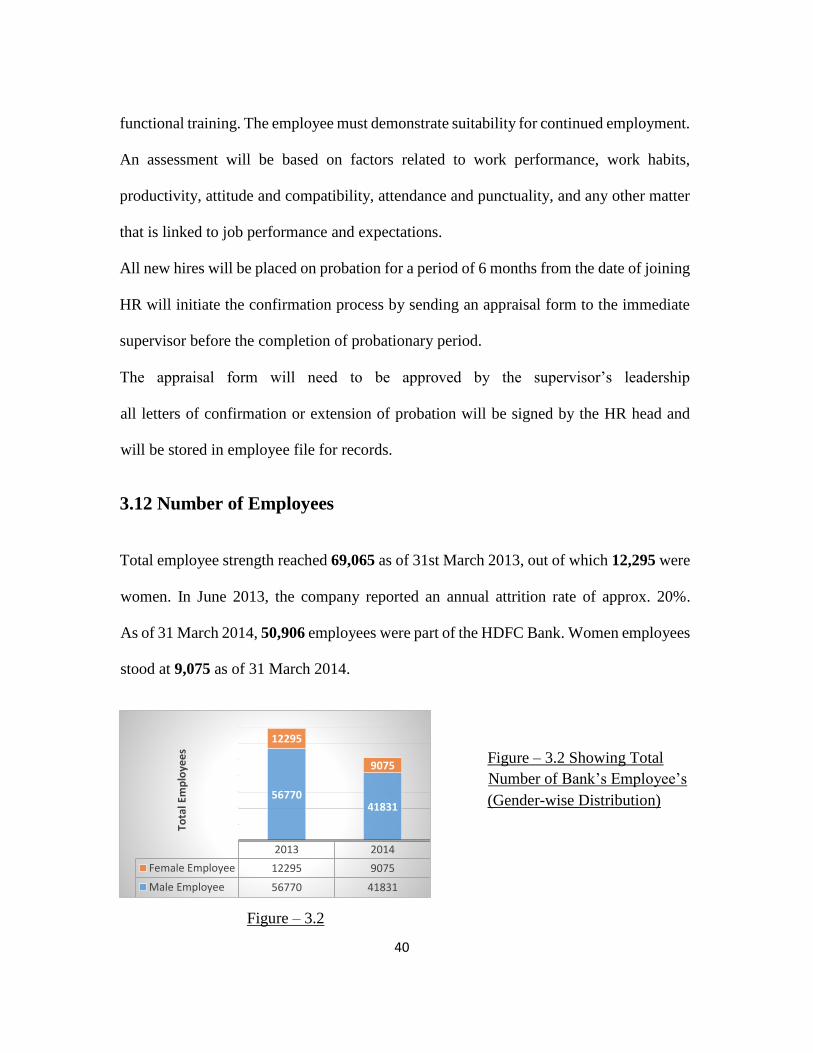

3.12 Number of Employees

Total employee strength reached 69,065 as of 31st March 2013, out of which 12,295 were

women. In June 2013, the company reported an annual attrition rate of approx. 20%.

As of 31 March 2014, 50,906 employees were part of the HDFC Bank. Women employees

stood at 9,075 as of 31 March 2014.

Figure – 3.2 Showing Total

Number of Bank’s Employee’s

(Gender-wise Distribution)

2013 2014

Female Employee 12295 9075

Male Employee 56770 41831

5677041831

12295

9075

Tota

l Em

plo

yee

s

Figure – 3.2

41

Figure – 3.3 Showing Decrease

in Number of Employees over

the past year

Figure – 3.3

Total Number of Bank’s Employees reduced from 69,065 to 50,906 as per the Business

Responsibility Report for year 2013 and 2014. Which shows that 18,159 employees left

the organization and the annual attrition rate was reported at 26% approx.

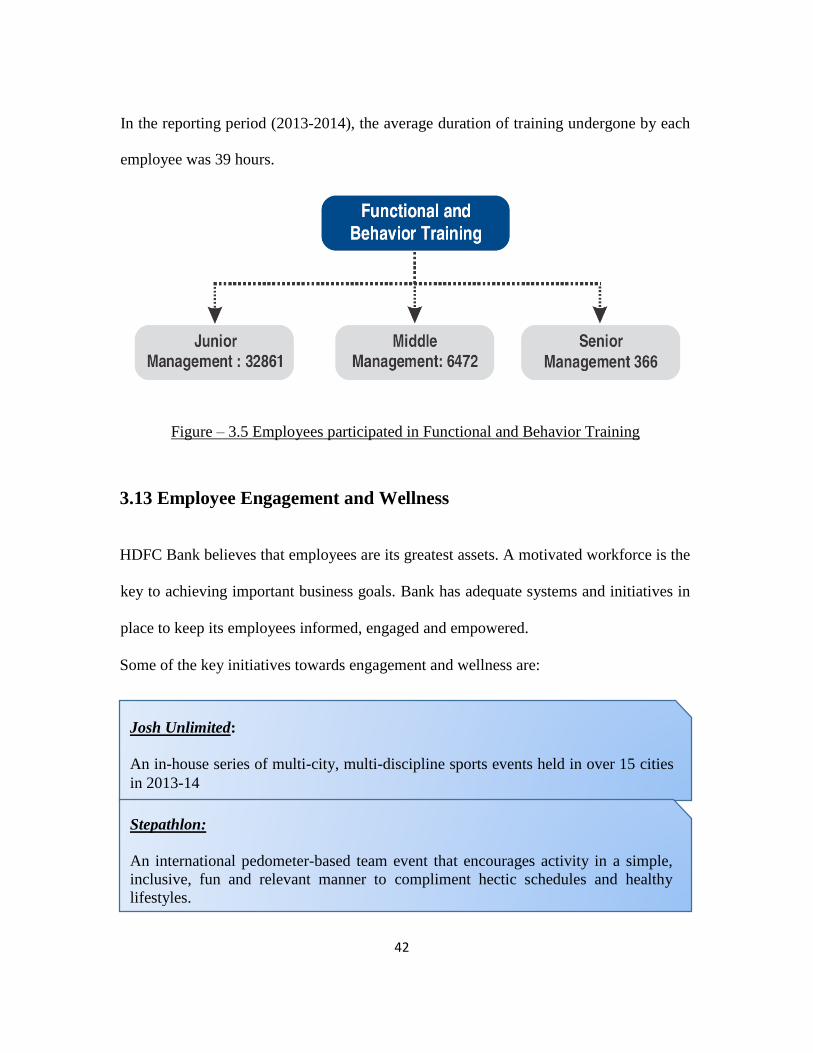

3.13 Employee Training and Development

To enhance the learning and

development of employees,

bank conduct trainings in

Technical as well as

Behavioral aspects. Focused

sessions on technical and

functional training were

conducted through the year where employees were trained in aspects of innovative

banking operations and behavioral solutions such as effective planning & decision making

69,065

50,906

2013 2014

Tota

l Em

plo

yees

Total Employees

Total Employees Linear (Total Employees)

Figure – 3.4 Employees Trained with Technical Skills

42

In the reporting period (2013-2014), the average duration of training undergone by each

employee was 39 hours.

Figure – 3.5 Employees participated in Functional and Behavior Training

3.13 Employee Engagement and Wellness

HDFC Bank believes that employees are its greatest assets. A motivated workforce is the

key to achieving important business goals. Bank has adequate systems and initiatives in

place to keep its employees informed, engaged and empowered.

Some of the key initiatives towards engagement and wellness are:

Josh Unlimited:

An in-house series of multi-city, multi-discipline sports events held in over 15 cities

in 2013-14

Stepathlon:

An international pedometer-based team event that encourages activity in a simple,

inclusive, fun and relevant manner to compliment hectic schedules and healthy

lifestyles.

43

Figure – 3.6 Employees Engagement and Wellness Initiatives by Bank

3.13 Employee Benefits

(a) Gratuity

The Bank provides for gratuity to all employees. The benefit is in the form of lump sum

payment to vested employees on resignation, retirement, death while in employment or on

termination of employment of an amount equivalent to 15 days basic salary payable for

each completed year of service. Vesting occurs upon completion of five years of service.

Sensations:

An 'In-house Musical Band' where employees across locations & functions come

together to share their passion for music & form their bands

Other Wellness/Diversity Initiatives:

• Celebrations during Diwali/ Christmas, Special workshops during Women's day

• Creating forums for employees to connect

Health and Wellness:

Providing complete health check-up packages for Bank’s employees

HDFC Bank Voice Hunt Contest:

A platform for all the employees of the Bank who are passionate about singing, to

showcase their talent on a National Level

44

The Bank makes contributions to funds administered by trustees and managed by insurance

companies for amounts notified by the said insurance companies.

(b) Leave Encashment

The Bank does not have a policy of encashing unavailed leave for its employees, except

for certain eLKB employees under Indian Banks’ Association (‘IBA’) structure. The Bank

provides for leave encashment / compensated absences based on an independent actuarial

valuation at the balance sheet date, which includes assumptions about demographics, early

retirement, salary increases, interest rates and leave utilisation.

(c) Superannuation

Employees of the Bank, above a prescribed grade, are entitled to receive retirement benefits

under the Bank’s Superannuation Fund. The Bank contributes a sum equivalent to 13% of

the employee’s eligible annual basic salary (15% for the Managing Director, Executive

Directors and for certain eligible erstwhile Centurion Bank of Punjab (‘eCBoP’) staff) to

insurance companies, which administer the fund. The Bank has no liability for future

superannuation fund benefits other than its contribution, and recognises such contributions

as an expense in the year incurred, as such contribution is in the nature of defined

contribution.

45

(d) Provident fund

In accordance with law, all employees of the Bank are entitled to receive benefits under

the provident fund. The Bank contributes an amount, on a monthly basis, at a determined

rate (currently 12% of employee’s basic salary). Of this, the Bank contributes an amount

equal to 8.33% of employee’s basic salary up to a maximum salary level of ` 6,500/- per

month, to the Pension Scheme administered by the Regional Provident Fund Commissioner

(‘RPFC’). The balance amount is contributed to a fund set up by the Bank and administered

by a board of trustees.

3.3 Finance

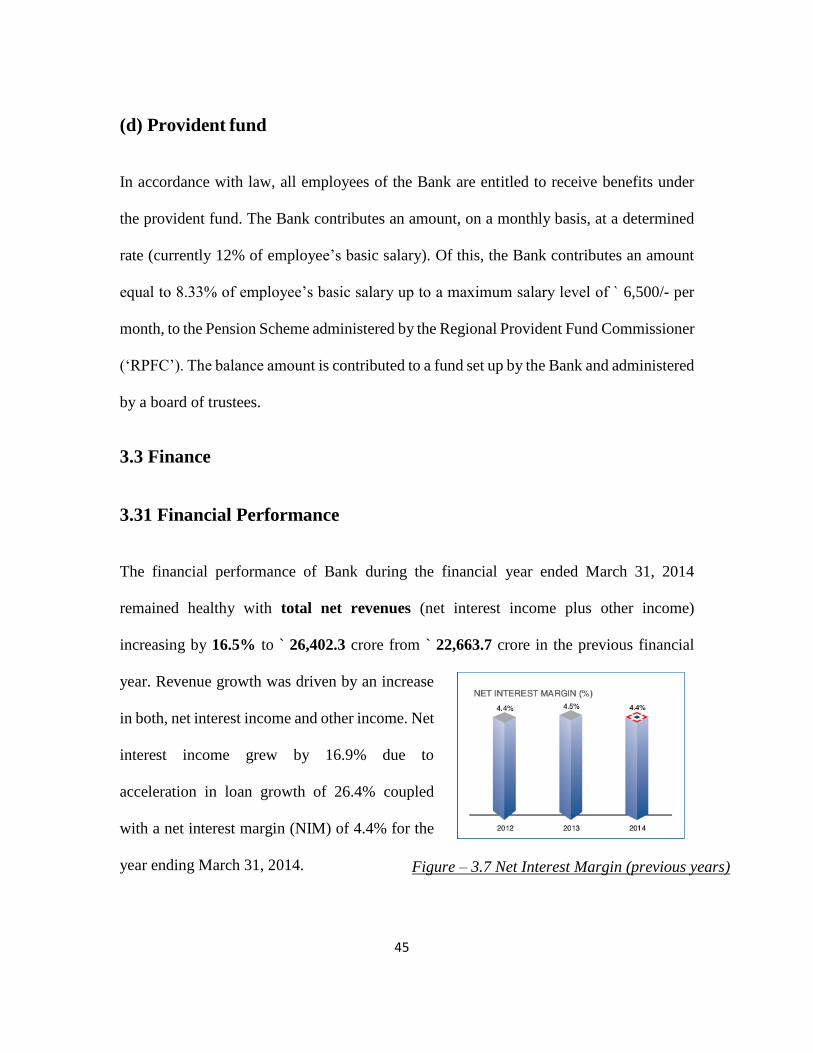

3.31 Financial Performance

The financial performance of Bank during the financial year ended March 31, 2014

remained healthy with total net revenues (net interest income plus other income)

increasing by 16.5% to ` 26,402.3 crore from ` 22,663.7 crore in the previous financial

year. Revenue growth was driven by an increase

in both, net interest income and other income. Net

interest income grew by 16.9% due to

acceleration in loan growth of 26.4% coupled

with a net interest margin (NIM) of 4.4% for the

year ending March 31, 2014. Figure – 3.7 Net Interest Margin (previous years)

46

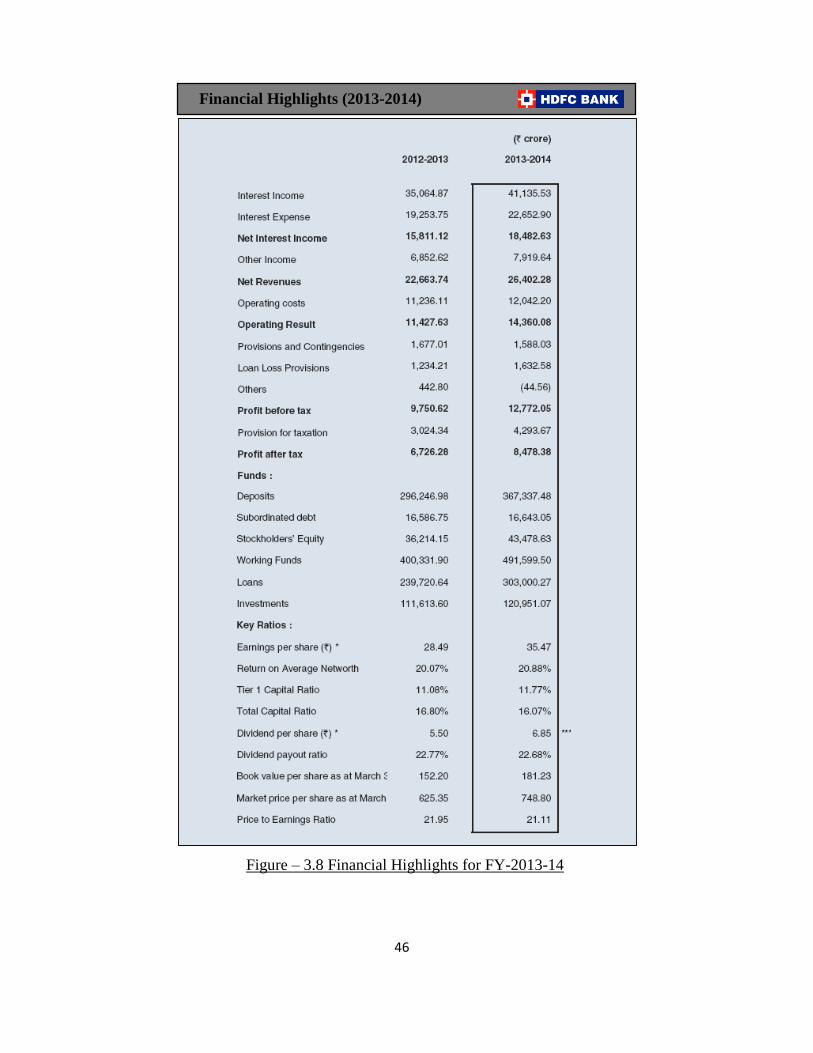

Figure – 3.8 Financial Highlights for FY-2013-14

Financial Highlights (2013-2014)

47

Other income grew 15.6% over that in the previous year to ` 7,919.6 crore during the

financial year ended March 31, 2014. The largest component of other income was fees and

commissions, which increased by 11.0% to ` 5,734.9 crore with the primary drivers being

commissions on debit and credit cards, transactional charges, fees on deposit accounts,

processing fees on retail assets and

commission on distribution of

Insurance products. Foreign exchange

and derivatives revenues were `

1,401.1 crore, gain on revaluation /

sale of investments were ` 110.5 crore

and recoveries from written-off

accounts were ` 622.6 crore in the

financial year ended March 31, 2014. Figure – 3.9 Rise in Other Income

Operating (non-interest) expenses increased from ` 11,236.1 crore in the previous

financial year to ` 12,042.2 crore in the year under consideration. During the year, Bank

opened 341 new branches and 513 ATMs which resulted in higher infrastructure and

staffing expenses. Staff expenses also increased on account of annual wage revisions. Cost

to income ratio was at 45.6% for the year ended March 31, 2014, as against 49.6% for the

previous year.

2013 2014

Other Income 6,852.62 7,919.64

6,852.62

7,919.64

6,200.00

6,400.00

6,600.00

6,800.00

7,000.00

7,200.00

7,400.00

7,600.00

7,800.00

8,000.00

Other Income

48

Total provisions and contingencies were ` 1,588 crore for the financial year ended March

31, 2014 as compared to ` 1,677.0 crore during the previous year. Bank’s provisioning

policies for specific loan loss provisions remain higher than regulatory requirements. The

coverage ratio based on specific provisions alone without including general and floating

provisions was 176% as on March 31, 2014. Bank made general provisions of ` 221.3 crore

during the financial year ended March 31, 2014.

Bank’s Profit Before Tax was` 12,772.1 crore, an increase of 31.0% over the year ended

March 31, 2013. With the effective tax rate for the year at 33.6% as against 31.0% for the

previous year.

The Bank posted total income and net profit of ` Rs. 49,055.2 crore and ` Rs. 8,478.4 crore

respectively for the financial year ended March 31, 2014 as against ` Rs. 41,917.5 crore

and ` Rs. 6,726.3 crore respectively in the previous year.

Figure – 3.10 Rise in PAT (Net Profit)

49

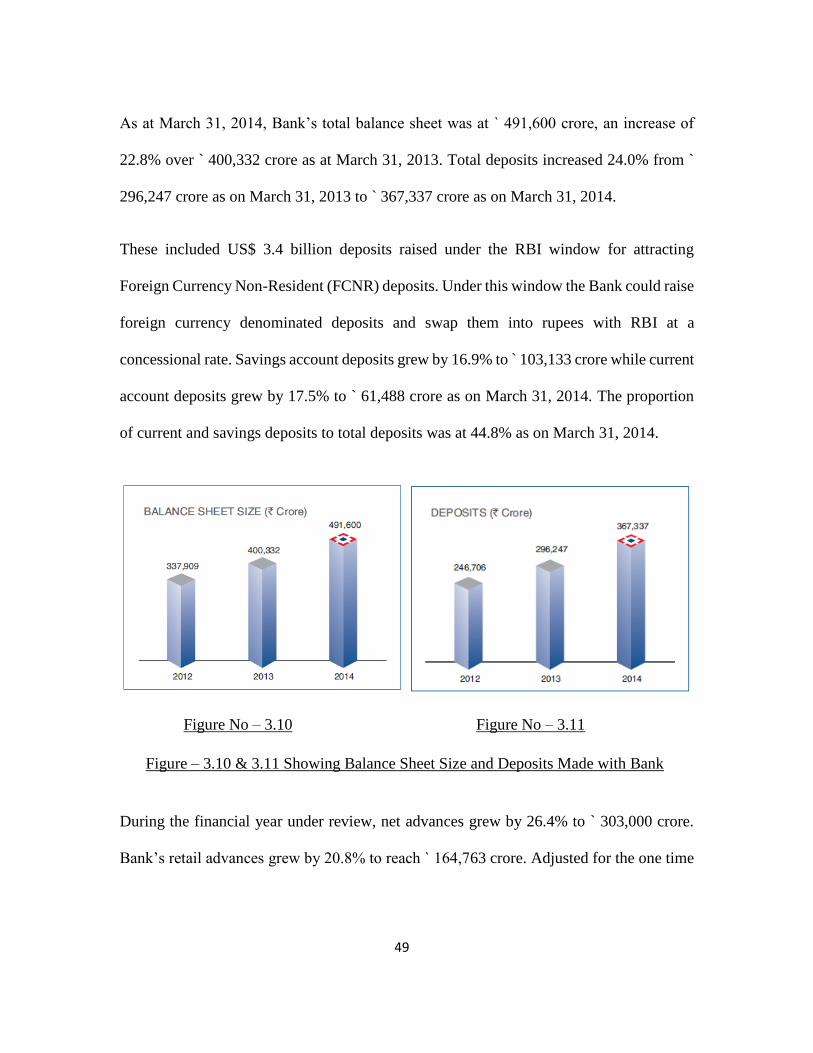

As at March 31, 2014, Bank’s total balance sheet was at ` 491,600 crore, an increase of

22.8% over ` 400,332 crore as at March 31, 2013. Total deposits increased 24.0% from `

296,247 crore as on March 31, 2013 to ` 367,337 crore as on March 31, 2014.

These included US$ 3.4 billion deposits raised under the RBI window for attracting

Foreign Currency Non-Resident (FCNR) deposits. Under this window the Bank could raise

foreign currency denominated deposits and swap them into rupees with RBI at a

concessional rate. Savings account deposits grew by 16.9% to ̀ 103,133 crore while current

account deposits grew by 17.5% to ` 61,488 crore as on March 31, 2014. The proportion

of current and savings deposits to total deposits was at 44.8% as on March 31, 2014.

During the financial year under review, net advances grew by 26.4% to ` 303,000 crore.

Bank’s retail advances grew by 20.8% to reach ` 164,763 crore. Adjusted for the one time

Figure – 3.10 & 3.11 Showing Balance Sheet Size and Deposits Made with Bank

Figure No – 3.10 Figure No – 3.11

50

increase in FCNR deposits swapped with RBI under the special window and the related

foreign currency loans, core deposits and advances growth for the year ended March 31,

2014 was 16.9% and 21.8% respectively. The Bank had a market share of approximately

4.4% and 4.7% in total domestic system deposits and advances respectively.

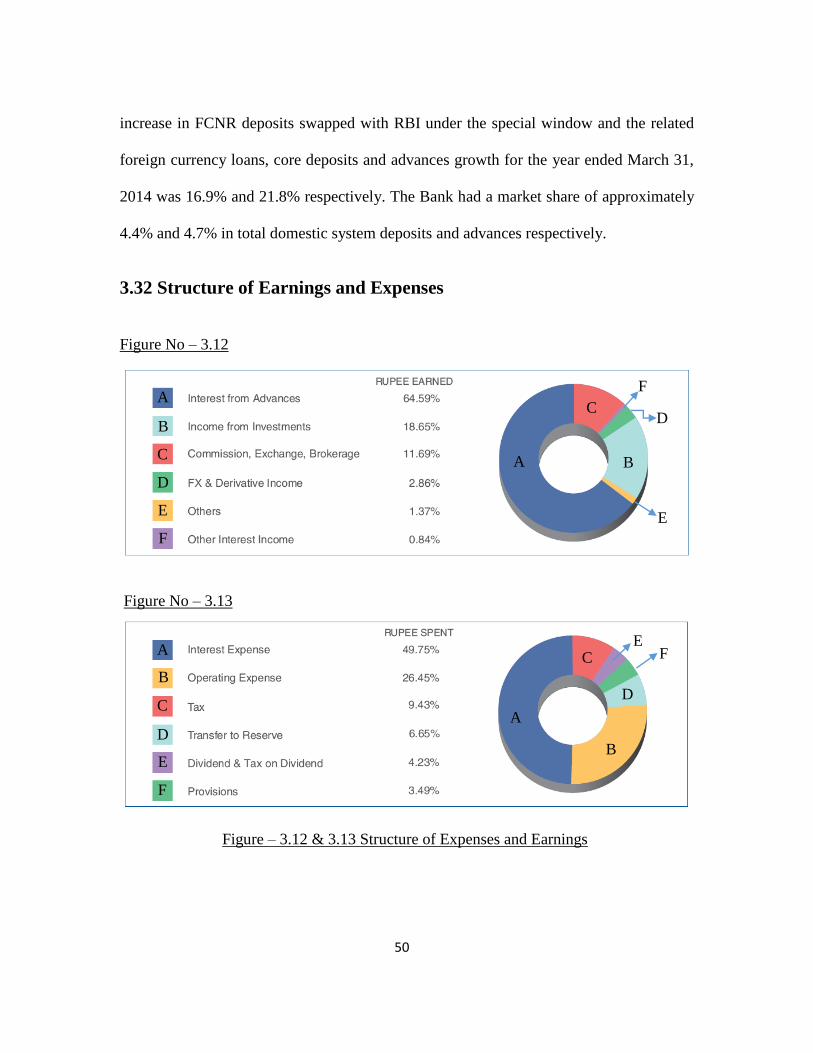

3.32 Structure of Earnings and Expenses

Figure No – 3.12

Figure No – 3.13

Figure – 3.12 & 3.13 Structure of Expenses and Earnings

A

B

C

D

E

F

A B

C D

E

F

A

B

C

D

E

F

A

B

D

C E

F

51

3.33 Capital Structure

As on March 31, 2014 the authorized share capital of the Bank is Rs. 550 crore. The paid-

up capital as on the said date is Rs 4,798,100,870/- (2,399,050,435) equity shares of Rs.

2/- each). The HDFC Group holds 22.64 % of the Bank's equity and about 16.97 % of the

equity is held by the ADS / GDR Depositories (in respect of the bank's American

Depository Shares

(ADS) and Global

Depository Receipts

(GDR) Issues). 34.11 %

of the equity is held by

Foreign Institutional

Investors (FIIs) and the

Bank has 422,314

shareholders. Figure – 3.14 Shareholding Pattern

The shares are listed on the Bombay Stock Exchange Limited and The National Stock

Exchange of India Limited. The Bank's American Depository Shares (ADS) are listed on

the New York Stock Exchange (NYSE) under the symbol 'HDB' and the Bank's Global

Depository Receipts (GDRs) are listed on Luxembourg Stock Exchange under ISIN No

US40415F2002.

HDFC Group23%

ADS / GDR Depositories

17%FII's34%

Others26%

SHAREHOLDING PATTERN

HDFC Group ADS / GDR Depositories FII's Others

52

3.34 Earnings per Share (EPS)

Basic and Diluted earnings per equity share have been calculated based on the net profit

after taxation of 8,743.49 crore (previous year: ` 6,869.64 crore) and the weighted average

number of equity shares outstanding during the year of 2,390,289,717 (previous year:

2,360,960,867)

Basic earnings per share (as reported) as on March 31, 2014 is 35.47

Figure – 3.15 Earning per Share over the years

3.35 Dividends

Bank has had a dividend policy that balances the dual objectives of appropriately rewarding

shareholders through dividends and retaining capital in order to maintain a healthy capital

adequacy ratio to support future growth. It has had a consistent track record of moderate

but steady increase in dividend declarations over its history with the dividend payout ratio

ranging between 20% and 25%.

53

Consistent with this policy and in recognition of the overall performance during this

financial year, directors were pleased to recommend a dividend of ` 6.85 per equity share

of ` 2 for the year ended March 31, 2014 as against ` 5.50 per equity share of ` 2 for the

previous year ended March 31, 2013. This dividend shall be subject to tax on dividend to

be paid by the Bank.

Figure – 3.15 Dividends per Share over the years

3.4 Information Technology

Bank had successfully completed the program to refresh its Retail Core Banking System

to the latest technology platform. Continuing with the program from the previous financial

year, Bank migrated the remaining 60% of the Retail Accounts to this new technology

platform during the financial year ended March 31, 2014. This new Retail Core Banking

System is deployed on a more robust architecture, enabling Bank to provide more features

to its customers and respond faster to business and market needs.

54

Bank continues to make substantial investments in its technology platforms and systems

and spread its electronically linked branch network. Bank’s direct banking platforms

continue to be stable and robust, supporting ever increasing transaction volumes, as

customers adopt newer self-service technologies.

Over 215,000 of your Bank’s Point-of

Sale terminals have been made safer

and more secure, following

implementation of RBI’s security and

encryption mandates. Also, Rupay

cards are now accepted on these

terminals and at Internet merchants

enlisted with Bank.

Bank continuously seek to improve environmental performance by promoting the use of

energy efficient and environment friendly technologies as detailed below:

Figure – 3.16 POS Terminals installed over the years

IT Enabled Communication:

Video Conference and Video Chatting on IP phone reduces travelling cost and time.

Virtualization of Systems:

Server and desktop virtualization reducing power consumption

55

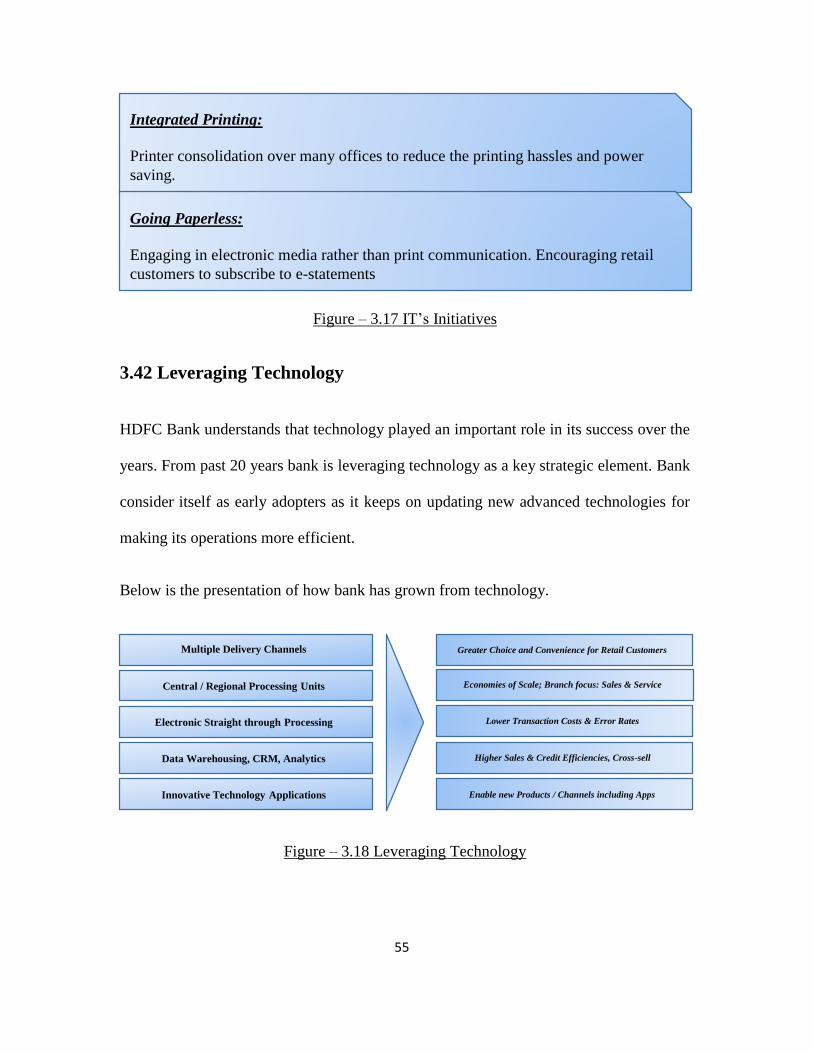

Figure – 3.17 IT’s Initiatives

3.42 Leveraging Technology

HDFC Bank understands that technology played an important role in its success over the

years. From past 20 years bank is leveraging technology as a key strategic element. Bank

consider itself as early adopters as it keeps on updating new advanced technologies for

making its operations more efficient.

Below is the presentation of how bank has grown from technology.

Figure – 3.18 Leveraging Technology

Integrated Printing:

Printer consolidation over many offices to reduce the printing hassles and power

saving.

Going Paperless:

Engaging in electronic media rather than print communication. Encouraging retail

customers to subscribe to e-statements

Multiple Delivery Channels

Central / Regional Processing Units

Electronic Straight through Processing

Data Warehousing, CRM, Analytics

Innovative Technology Applications

Greater Choice and Convenience for Retail Customers

Economies of Scale; Branch focus: Sales & Service

Lower Transaction Costs & Error Rates

Higher Sales & Credit Efficiencies, Cross-sell

Enable new Products / Channels including Apps

56

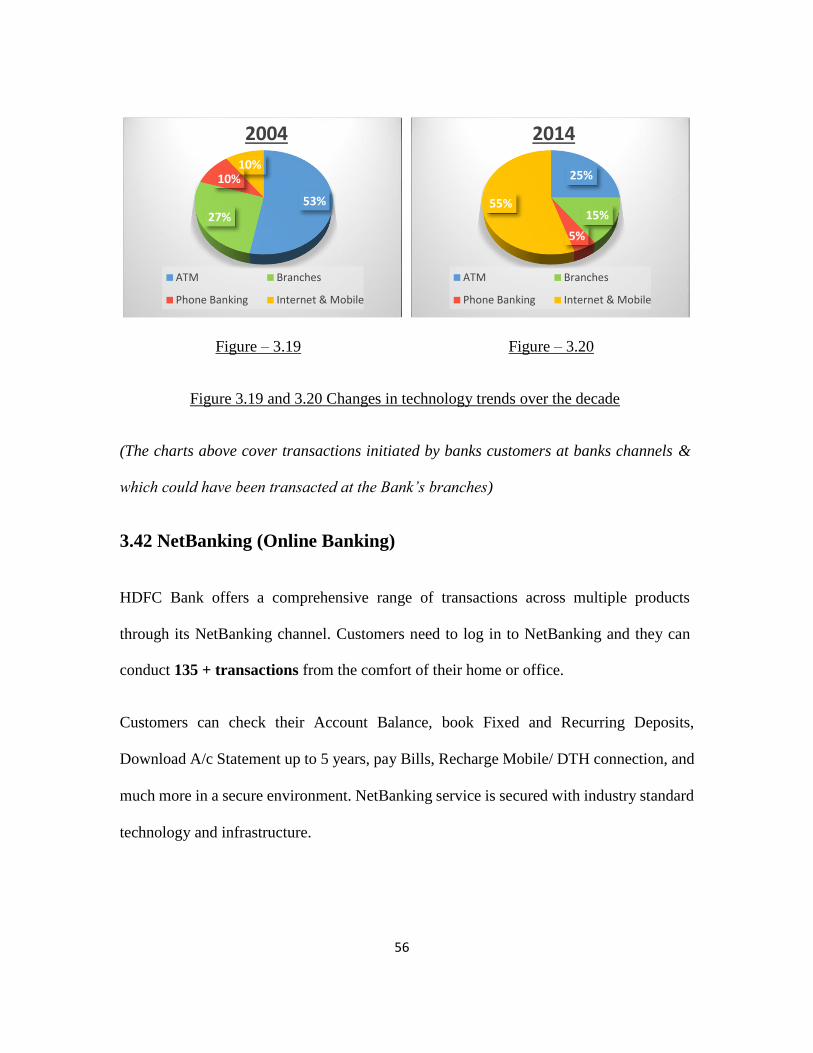

Figure – 3.19 Figure – 3.20

Figure 3.19 and 3.20 Changes in technology trends over the decade

(The charts above cover transactions initiated by banks customers at banks channels &

which could have been transacted at the Bank’s branches)

3.42 NetBanking (Online Banking)

HDFC Bank offers a comprehensive range of transactions across multiple products

through its NetBanking channel. Customers need to log in to NetBanking and they can

conduct 135 + transactions from the comfort of their home or office.

Customers can check their Account Balance, book Fixed and Recurring Deposits,

Download A/c Statement up to 5 years, pay Bills, Recharge Mobile/ DTH connection, and

much more in a secure environment. NetBanking service is secured with industry standard

technology and infrastructure.

53%27%

10%10%

2004

ATM Branches

Phone Banking Internet & Mobile

25%

15%

5%

55%

2014

ATM Branches

Phone Banking Internet & Mobile

57

CHAPTER – 4

FUNCTIONAL ANALYSIS

58

4. Functional Analysis of HDFC Bank Ltd.

HDFC Bank began operations in 1995 with a simple mission: to be a "World-class Indian

Bank". At early stage bank realized that product quality and service excellence would help

it to reach its objective. Today HDFC Bank is proud to say that it is well on its way towards

that objective.

In the past years, awards and recognition were conferred upon Bank by leading domestic

and international organizations. Some of them are:

a. Business Today-KPMG Bank Survey: Best Bank

b. Business Standard: Aditya Puri (Banker of the Year)

c. Forbes Asia: Fab 50 Companies (7th time) , Best Bank in India

d. GUINNESS WORLD RECORD: Largest Blood Donation Drive

e. IBA Innovation Awards: Most Innovative use of Technology

The key to Bank’s initial success probably lay in the fact that HDFC preferred the solid

conservatism of the tried and tested to the new. This often meant that other banks pioneered

new ideas, but HDFC Bank could jump in once a concept was proven. It took very few big

risks. HDFC Bank started off steadily and safely and that’s why it managed to become one

of the largest bank of the country with a huge customer base.

59

4.1 Inferences from different Functional Areas

4.11 Marketing

HDFC Bank is one of the best private bank in India. Bank’s efficient marketing strategies

and core values including Operational Excellence, Customer Focus, Product Leadership,

People and Sustainability helped it to achieve this position which it is holding today.

HDFC Bank focuses on delivering excellence to its customer by providing them value

added products and services. Bank has positioned itself in a best possible manner using its

quick adaptability in market.

Following are the highlights of bank’s Marketing Practice’s and Strategies

a. Huge Distribution Network across the nation enables the bank to reach out the

customer easily. Which acts as a competitive advantage to the bank. Network

includes Branches and ATM’s both.

b. Bank keeps on developing new innovative products and services that attracts the

targeted customers and provides the product leadership in market.

c. HDFC Bank exercises the Cross Selling of products which provides its customer a

one stop solution for all their financial requirements.

d. Strong relationship and engaging with stakeholders on a consistent and continuous

basis is essential for healthy business growth. Bank acknowledge and value the role

60

played by its stakeholders – both internal and external, which has helped HDFC

Bank to maintain its position among the leaders in the financial sector.

e. Bank uses Customer Relationship Management Technology to retain a huge

customer base. It helps to understand customer needs and also helps in providing

different solutions accordingly.

f. Bank has an effective systems that ensure transparency and accuracy in-line with

the Corporate Communications Policy. Complete and correct information is passed

onto customers to help them make informed decisions.

g. Bank takes many initiative as a part of Social Responsibility including

environmental responsibility.

4.12 Human Resource

An organization cannot build a good team of working professionals without good Human

Resources. The key functions of the Human Resources Management (HRM) team include

recruiting people, training them, performance appraisals, motivating employees as well as

workplace communication, workplace safety, and much more.

HDFC Bank has a youthful and enthusiastic team which is considered as one of the main

success factor for bank. Some of the Human Resource highlights are:

61

a. Human resource department of HDFC Bank is committed to hiring, developing,

motivating and retaining the best people in the industry

b. Bank has large employee base which helps the bank to facilitate its large operation

network.

c. HDFC Bank maintains a gender-inclusive environment and ensure the safety of

female employees. All cases of harassment are treated with great sensitivity and are

escalated in time for resolution

d. Bank regularly conducts Technical and Behavioral training sessions to enhance the

learning and development of the employees.

e. Bank takes adequate initiative to motivate its employees by engaging them into

different wellness and development activities.

4.13 Finance

It is impossible for an organization to achieve long-term and short-term goals without

effectively managing finances. It is significant for business growth, market competition,

and to keep business operational and maintain your customer base.

Here are some Highlights of Banks Finances and Financial Performance

a. The Financial Performance of HDFC Bank during Financial year 2013-2014

remained healthy.

62

b. Bank recorded a growth of 16% approx. in its total income which led to the

increase in its profits.

c. HDFC Bank has emerged as the best large bank because of good asset quality, high

loan growth, a healthy capital adequacy ratio and an improvement in returns on

capital employed

d. Financial Performance of subsidiary companies, HDFC SECURITIES LIMITED

and HDB FINANCIAL SERVICES LIMITED remained also strong.

4.14 Information Technology

Information Technology played a very important role in the success of HDFC Bank and

its existence as a one of the top bank in the country. Information Technology has always

been one of the key strategies of HDFC Bank.

Bank has always adopted to new technology in order to gain maximum efficiency.

Following are some highlights of Information Technology at HDFC

a. Bank is leveraging technology as a key strategic element from past 20 years.

b. Bank always seek to improve its performance by promoting the use of latest

technologies.

c. All the bank’s branches and ATM’s have online connectivity, which enables the

bank to offer speedy funds transfer facilities to its customers.

63

d. Bank has taken various technology initiatives and same has been applied amongst

the employees

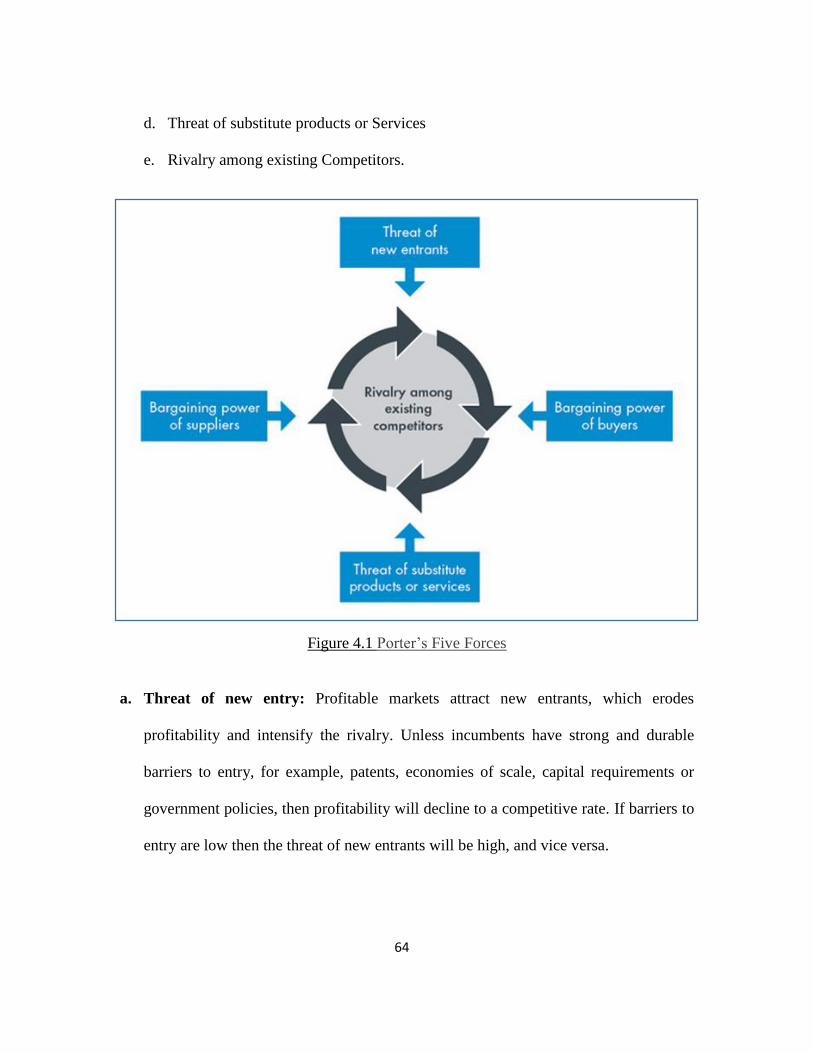

4.2 Porter’s Five Forces Model

Porter's Five Forces of Competitive Position Analysis were developed in 1979 by Michael

E Porter of Harvard Business School as a simple framework for assessing and evaluating

the competitive strength and position of a business organization.

This theory is based on the concept that there are five forces that determine the competitive

intensity and attractiveness of a market. Porter’s five forces help to identify where power

lies in a business situation. This is useful both in understanding the strength of an

organization’s current competitive position, and the strength of a position that an

organization may look to move into.

Porter’s five forces helps to understand whether new products or services are potentially

profitable. By understanding where power lies, the theory can also be used to identify

areas of strength, to improve weaknesses and to avoid mistakes.

Five Forces that act together to determine the nature of competition within an industry are

follows:

a. Threat of new Entrants

b. Bargaining power of Supplier

c. Bargaining power of Buyers

64

d. Threat of substitute products or Services

e. Rivalry among existing Competitors.

Figure 4.1 Porter’s Five Forces

a. Threat of new entry: Profitable markets attract new entrants, which erodes

profitability and intensify the rivalry. Unless incumbents have strong and durable

barriers to entry, for example, patents, economies of scale, capital requirements or

government policies, then profitability will decline to a competitive rate. If barriers to

entry are low then the threat of new entrants will be high, and vice versa.

65

b. Supplier power: An assessment of how easy it is for suppliers to drive up prices. This

is driven by the: number of suppliers of each essential input; uniqueness of their product

or service; relative size and strength of the supplier; and cost of switching from one

supplier to another.

c. Buyer power: An assessment of how easy it is for buyers to drive prices down. This is

driven by the: number of buyers in the market; importance of each individual buyer to

the organization; and cost to the buyer of switching from one supplier to another. If a

business has just a few powerful buyers, they are often able to dictate terms.

d. Threat of substitution: Where close substitute products exist in a market, it increases

the likelihood of customers switching to alternatives in response to price increases. This

reduces both the power of suppliers and the attractiveness of the market.

e. Competitive rivalry: The main driver is the number and capability of competitors in

the market. Many competitors, offering undifferentiated products and services, will

reduce market attractiveness.

4.21 Porter’s Five Force Model for HDFC BANK Ltd.

a. Threat of New Entrants: As a part of on-going banking sector reforms, New Licenses

would be issued to a few new players shortly. And yet the fact remains that anyone

and everyone cannot start up a bank. Nevertheless, there are services, such as internet

bill payment, on which entrepreneurs can capitalize.

66

Bank is fearful of being squeezed out of the payments business, because it is good

source of fee-based revenue. Another drift that poses a threat is companies offering

other financial services e.g.; an insurance company offering mortgage and loan

services. As far as regional banks are concerned the possibility of a mega bank

entering into the market poses a real threat to HDFC Bank.

b. Supplier power: The providers of capital might not posture a gigantic hazard, but the

threat of suppliers luring away human capital does. Retention of talent becomes

difficult in a situation wherein a talented individual working in bank may be stolen

away by other bigger banks, investment firms, etc.

c. Buyer power: One single retail customer may not really pose much of a threat to the

Bank, but one major factor affecting the power of buyers is relatively high switching

costs. If a person has a mortgage, car loan, credit card, checking account and mutual

funds with one particular bank, it can be extremely tough for that person to switch to

another bank. In an attempt to lure in customers, competitor banks try to lower the

price of switching, but many people would still rather stick with their current Bank.

On the other hand, large corporate clients have banks running after them, offering

innovative plans and schemes. Financial institutions - by offering better exchange

rates, more services, and exposure to foreign capital markets - work extremely hard to

get high-margin corporate customers.

67

d. Threat of substitution: Our market, as is well known, has a parallel economy based

on black money and grey operators. Even if, for a moment, we discard such realities,

there would still be plenty of substitutes in the banking industry. Banks offer a suite

of services over and above taking deposits and lending money, but whether it is

insurance, mutual funds or fixed income securities, chances are there is a non-banking

financial services company that can offer similar services.

On the lending side of the business, banks are seeing competition rise from

unconventional companies that offer preferred financing to customers who buy big

items. If a company is offering 0% financing, why would anyone want to get a loan

from the bank for the same commodity and pay expensive interest?

e. Competitive rivalry: The banking sector is highly competitive. The financial services

industry has been around for a good amount of time and simply put across, anyone

and everyone who needs banking services, already has the access to such services.

Banks, therefore, have no choice but to make attempts to lure clients away from their

competitors.

A bank may do so by offering lower financing, preferred rates and investment services

but such an action may cause banks to experience pretty lower profit margins. In such

a scenario, concerned bank(s) have an incentive to take on high-risk projects. In the

long run, we're likely to see more consolidation in the banking industry. Big fish may,

logically, prefer to digest smaller fish rather than spending or cutting on own margins.

68

The Indian banking sector is linked to the world economy but the Indian banking

system has had no direct exposure to the sub-prime mortgage assets or to the failed

institutions. It has very limited off-balance sheet activities or securitized assets. In fact,

our banks continue to remain safe and healthy. The Indian banking sector has been

well shielded by the central bank and has managed to sail through most of the crisis

with relative ease. It is hoped that the trend would continue for a foreseeable future.

4.22 In a Nutshell

It is true that banks have been under tremendous pressure, especially during the present

fiscal. It is wrong to see such a trend in isolation as a host of factors have been contributing

to such a trend. With new RBI Governor at the helm of affairs, banking industry is

optimistic even though the pressure would continue for a while. Even though SBI remains

the biggest of all, banks like HDFC and AXIS Bank have been successful in leading with

their operational efficiencies and resultant productivity. The future that envisages growth

of the nation, cannot ignore a parallel growth of banking sector and that being something

inevitable, future looks bright for the industry despite present hiccups and glitches.

69

CHAPTER – 5

SUMMARY & CONCLUSIONS

70

5.1 Findings

a. HDFC Bank is among the top banks in the private sector domain. The bank boasts of

a huge amount of operational efficiencies for over the years.

b. Having strong competitors like ICICI Bank, AXIS Bank and Kotak Mahindra Bank,

HDFC Bank has managed its customer base and market share very competently.

c. Bank has a very strong market reputation which holds the loyalty factor within its

customers.

d. Bank doesn’t runs after the sales as it follows a conservative approach which

eventually reduces the risk of losses.

e. Bank’s enormous distribution network is well positioned in India which makes HDFC

Bank easily accessible by customers from different parts of the country.

f. Bank provides variety of financial products and services which targets different

customer segments in the market and which also provides competitive advantage to

bank.

g. Bank has got a very good asset quality, high loan growth and good coverage ratios and

that’s what makes HDFC Bank the best performer among other private banks.

h. Bank recorded a consistent growth in its total income over the year which has also

increased the profit margins.

i. As explained in previous chapter, the bank has positive net interest margins (NIMs) of

almost 4.5% and it is felt and believed that it would be able to maintain that for the

foreseeable future, especially so when the worst appears to be over.

71

j. The Bank’s stock has been giving healthy returns in terms of appreciation. Even

though it may not be the sector leader as far as dividend is concerned, it has been

consistent nevertheless.

k. HDFC Bank has large employee base which helps the bank to facilitate its operations

and also enhances the productivity of the Bank.

l. HDFC Bank acknowledge the roles of internal and external stakeholders and it also

maintains the communication with both.

m. HDFC Bank keeps on taking initiatives for employee’s wellness and their development

and it also works for the development of the society and protection of environment.

n. Technology is a key strategy for bank, technology has played an important role in

overall growth of bank, Bank always welcome new and advanced technologies for

improving its efficiency.

5.2 Learnings

HDFC Bank is one of the prestigious organizations of the country where carrying out a

management internship is really a big opportunity. It has been a wonderful experience

working with HDFC Bank where the researcher had given a chance to work as a part of

the Organization.

This practical exposure gave an opportunity to the researcher to put the previous

educational knowledge gained so far into use and enhance the existing knowledge by

facing the real life corporate world.

72

The whole Training tenure was full of opportunities and learnings for the researcher.

a. Being a management intern researcher worked with Mortgage Team of HDFC

Bank which looks after the Sales of Mortgage Loan Products.

b. The researcher was allotted with all major responsibilities that are usually being

done by other employees.

c. Researcher learned how to interact with clients during different client meetings

which is really essential for a marketing personnel.

d. Researcher has gained knowledge about different Mortgage products so as to

offer the right product to the clients.

e. Follow-ups of sales lead by making calls to the team members was also done by

researcher during the training period.

f. Researcher interacted with different Branch Manager’s in regards to the sales data

and sales leads of their respective branches.

g. Interaction with other employees of the organization also helped the researcher to

know more about the work culture and organization’s internal environment.

h. HDFC Bank’s knowledge center enabled researcher to learn about organizations

code of conduct, rules and governance.

73

i. Researcher participated in monthly sales closing which takes place at the end of

every month where reports are prepared for the business generated during the

month.

j. Researcher also learned the effectiveness of cross-selling in banking industry as it

does not only helps in increasing the sales but also helps to retain customers by

providing them one-stop solution for their needs.

5.3 Suggestions

a. More training opportunities must be given to management students to peruse their

training in HDFC Bank.

b. HDFC Bank is a great platform for trainees for exposure to the corporate world.

c. Different functional departments of the organization may help an intern to

improve his/her functional skills.

d. HDFC is the right place for an intern to learn customer interaction and client

dealings which is an essential for a management learner.

e. Bank’s internal environment improves the practical as well as conceptual

learnings.

f. Dedicated workforce motivates the trainee and boosts up the morale.

Related Documents