Pooling Basics Fall 2016 Recommended Sessions for Pooling Basics Track: Pooling Basics Session #1a Monday, October 3, 1:45-3:00pm Pooling Basics Session #1b Monday, October 3, 3:00-4:00pm Pooling Basics Session #1c Monday, October 3, 4:00-5:00pm Pooling Basics Session #2a Tuesday, October 4, 10:00-11:00am Pooling Basics Session #2b Tuesday, October 4, 11:00-12:15pm Presentation Description Over the course of two days, solidify your pooling basics knowledge with several sessions to recap the course work you have already been through. Basics sessions will coverage Underwriting, Actuarial Science, the Claims Function, Financial Reporting, Auditing, and Risk Management. We will even dabble in Pooling’s historical background make some guesses as to it’s future. There will be plenty of time for Questions & Answers for the Pooling experts lined up to dispense their knowledge and experience. Presentation Software http://prezi.com/dcjl7yrankbc/?utm_campaign=share&utm_medium=copy&rc=ex0share Table of Contents Recommended Sessions for Pooling Basics Track: 1 Presentation Description 1 Presentation Software 1 Presenters 2 History of Insurance in 60 seconds 3 Pooling Background Material 4 Pooling Basics Session #1a – Underwriting 9 Pooling Basics Session #1b – The Life of a Claim 11 Pooling Basics Session #1c – Actuarial Science 13 Pooling Basics Session #2a – Financial Reporting and Auditing 14 Pooling Basics Session #2b – Risk Management, The Future of Pooling, and Questions & Answers 18

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PoolingBasics Fall2016

RecommendedSessionsforPoolingBasicsTrack:PoolingBasicsSession#1a Monday,October3,1:45-3:00pmPoolingBasicsSession#1b Monday,October3,3:00-4:00pmPoolingBasicsSession#1c Monday,October3,4:00-5:00pmPoolingBasicsSession#2a Tuesday,October4,10:00-11:00amPoolingBasicsSession#2b Tuesday,October4,11:00-12:15pm

PresentationDescription

Overthecourseoftwodays,solidifyyourpoolingbasicsknowledgewithseveralsessionstorecapthecourseworkyouhavealreadybeenthrough.BasicssessionswillcoverageUnderwriting,ActuarialScience,theClaimsFunction,FinancialReporting,Auditing,andRiskManagement.WewillevendabbleinPooling’shistoricalbackgroundmakesomeguessesastoit’sfuture.TherewillbeplentyoftimeforQuestions&AnswersforthePoolingexpertslineduptodispensetheirknowledgeandexperience.

PresentationSoftwarehttp://prezi.com/dcjl7yrankbc/?utm_campaign=share&utm_medium=copy&rc=ex0share

TableofContentsRecommendedSessionsforPoolingBasicsTrack: 1

PresentationDescription 1

PresentationSoftware 1

Presenters 2

HistoryofInsurancein60seconds 3

PoolingBackgroundMaterial 4

PoolingBasicsSession#1a–Underwriting 9

PoolingBasicsSession#1b–TheLifeofaClaim 11

PoolingBasicsSession#1c–ActuarialScience 13

PoolingBasicsSession#2a–FinancialReportingandAuditing 14

PoolingBasicsSession#2b–RiskManagement,TheFutureofPooling,andQuestions&Answers 18

Presenters

JoelKress,AGRiPStaff [email protected];603.568.4880JoelKresscurrentlyservesasDirectorofSpecialProjectsforAGRiP.Amongsthisotherprojects,heisupdatingPoolingBasicstobeincludedinaholisticinitiativeknownas‘PoolingAcademy’.Althoughinitsinfancy,PoolingAcademywillwrapupalleducationalinitiativesinthepoolingsector,andstandardizetheeducationalrequirementsforthoseseekingpoolmanagement.

Previously,Mr.KressservedasUnderwritingManagerforGovernmentEntitiesMutual,Inc.PCC,providingreinsuranceunderwritingandactuarialanalyticalservices,aswellascomputerprogrammingfortheclaimsmanagementinformationsystem.PrevioustoGEM,Mr.Kressworkedforanactuarialconsultingfirmfor5years.HehasreceivedtwoBachelorofSciencedegrees(AppliedMathematicsandMathematicalEducation)fromNorthCarolinaStateUniversity,andaMastersdegree(BusinessAdministration)fromSouthernNewHampshireUniversity.HealsoearnedthedesignationAssociateinReinsurance(ARe).

MujtabaDatoo,AONGlobalRiskConsulting [email protected];949-608-6332MujtabaDatooistheActuarialPracticeLeaderforAONGlobalRiskConsulting,leadingthepublicentitypractice.Hehasover30yearsexperienceprovidingactuarialserviceswithintheinsuranceandriskmanagementfields.Hehasspentover10,000hoursjustinthelastdecadepreparingactuarialreports,andthusqualifiesasanexpertaccordingtothe10,000-hourrulepopularizedbyMalcolmGladwellinhisbestsellingbook‘Outliers’.Mr.Datoohasextensiveexperienceinratemaking,lossreserve,andfundingstudiesforself-insuredworkerscompensationandliabilityprograms,particularlyforpoolingprograms.Hisexperiencehasincludedtenuresinacommercialcarrier,ratingbureaus,andconsulting.

Hehaspresentedbeforevariousorganizations,includingPRIMA,CAJPA,CASBO,PARMA,AGRiP,APTA,STRIMA,NLC,andConferenceofConsultingActuaries.AfrequentspeakertoPoolBoardshehaspresentedextensivelyonunderstandingactuarialreportsanditsfindings,financialmeasuresandcostallocations.HeisthecornerstoneofthefinancialbootcampsoftheAonPoolingConference.Hehasauthoredseveralarticlesonactuarialtopics,andaprimeronunderstandingyouractuarialreport–soontobepublished.Mr.DatooattendedColumbiaUniversityandholdstheprofessionaldesignationAssociateoftheCasualtyActuarialSociety(ACAS)andisaMemberoftheAmericanAcademyofActuaries(MAAA)andaFellowoftheConferenceConsultingActuaries(FCA).

ShawnBubb,MontanaSchoolBoardsAssociation/MSGIA [email protected];406.457.4500ShawnBubbhasbeenintheinsuranceindustrysince1994andpriortothatheworkedinthefinancialservicesindustryfor3years.Hehasastrongaccountingbackgroundholdingkeypositionssuchasinternalauditor,corporatecontroller,andinsuranceoperationsteamleaderfortheMontanaStateWCFund.Mr.BubbisagraduateofCarrollCollegeinHelena,MontanaandholdsundergraduatedegreesinAccountingandBusinessAdministration.HeisaCertifiedPublicAccount(CPA),CertifiedInternalAuditor(CIA),CIC(CertifiedInsuranceCounselor),CertifiedSchoolRiskManager(CSRM),andiscurrentlypursuinghisCharteredPropertyCausalityUnderwriter(CPCU)certification.Mr.Bubbhasworkedinthepoolingsectorsince2002.HeisapastpresidentofboththeMontanaWCSelfInsuranceAssociationboardofdirectorsandAssociationofGovernmentalRiskInsurancePools(AGRIP).FrankRamsey,WillisTowersWatson [email protected];8607594913FrankRamsayhasmorethan30yearsofexperienceinallaspectsofclaimsmanagementandconsulting.Histechnicalbackgroundincludesexperienceinprofessional(MPL,E&O,D&O,Lawyers)liability,generalliability,autoliability,workerscompensation,commercialandpersonallinespropertyclaims.Hehasmanagedasbestosandenvironmentalclaimissuesforamajorinsurerincludingthecoordinationandnegotiationofdefensecost-sharingagreements,lost

policyarrangements,casereserving,complexcoverageevaluation,legalcostmanagement,aswellasensuringtheconsistentapplicationofclaimandcoveragestandardsthroughoutvariousjurisdictions.Healsohasexperienceincededandassumedtreaty,facultative,proportionalandexcessoflossreinsuranceclaims.

Inadditiontohisconsultingrole,Mr.RamseyleadstheWillisTowersWatsonClaimsManagementpractice,overseeingthedeliveryoftheclaimpractice’sproductsandservices,managingclientrelationships,andpeoplemanagement.Mr.RamseyearnedaB.A.fromEasternConnecticutStateUniversity.HeholdstheSeniorClaimLawAssociatedesignationandisamemberoftheLossExecutivesAssociation.

HistoryofInsurancein60seconds(settothemusicofapopularsong)

Lloyd’sofLondon,teatime,cargoships,maritime;BarnbuildingAmish,Franklin’sFireMutuals;Homesteaderstakearisk,farmers’cropstakeahit;Insurancesalesmengetawrap,sellingonebigmoneytrap.

Exclusions,exclusionseverywhere,regulatorsonatear;ActsofGoddon’tyousay,NFIPsavestheday;Asbestos,blacklungdisease,toxicdumpingkillingtrees;UnderwritersoffScot-free,who’llactuallypayforme.

Wedidn’tstartthe(insurable)fireItwasalwaysburningSincetheworld’sbeenturningWedidn’tstartthe(insurable)fireNo,wedidn’tlightitButwetriedto(compensate)foritStripSearches,eminentdomain,MirandaRightsaresuchapain;HurricaneAndrew,Northridgeearthquake;EliotSpitzerkillsfinite,contingentcommissionsgoodnight;Medicalandsocialinflationequalspremiumescalation;Katrinarainsdownforaweek,NewOrleansspringsaleak;Lehman,AIGcrashes,GreatRecessionlashes;InvestorseyeInsuranceprofit,softmarketbeyondalllogic;UnderwritersoffScot-free,who’llactuallypayforme;Wedidn’tstartthe(insurable)fireItwasalwaysburningSincetheworld’sbeenturningWedidn’tstartthe(insurable)fireNo,wedidn’tlightitButwetriedto(compensate)forit

PoolingBackgroundMaterial

PoolingBasics–FillingthePool

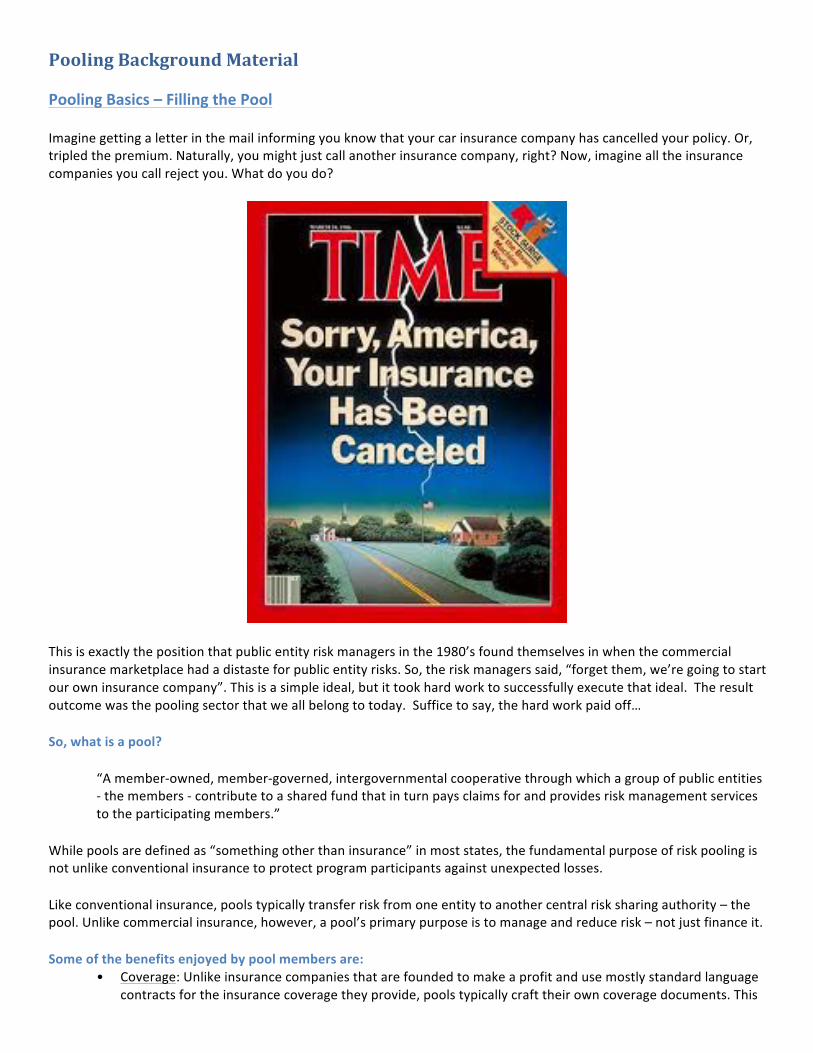

Imaginegettingaletterinthemailinformingyouknowthatyourcarinsurancecompanyhascancelledyourpolicy.Or,tripledthepremium.Naturally,youmightjustcallanotherinsurancecompany,right?Now,imaginealltheinsurancecompaniesyoucallrejectyou.Whatdoyoudo?

Thisisexactlythepositionthatpublicentityriskmanagersinthe1980’sfoundthemselvesinwhenthecommercialinsurancemarketplacehadadistasteforpublicentityrisks.So,theriskmanagerssaid,“forgetthem,we’regoingtostartourowninsurancecompany”.Thisisasimpleideal,butittookhardworktosuccessfullyexecutethatideal.Theresultoutcomewasthepoolingsectorthatweallbelongtotoday.Sufficetosay,thehardworkpaidoff…

So,whatisapool?

“Amember-owned,member-governed,intergovernmentalcooperativethroughwhichagroupofpublicentities-themembers-contributetoasharedfundthatinturnpaysclaimsforandprovidesriskmanagementservicestotheparticipatingmembers.”

Whilepoolsaredefinedas“somethingotherthaninsurance”inmoststates,thefundamentalpurposeofriskpoolingisnotunlikeconventionalinsurancetoprotectprogramparticipantsagainstunexpectedlosses.

Likeconventionalinsurance,poolstypicallytransferriskfromoneentitytoanothercentralrisksharingauthority–thepool.Unlikecommercialinsurance,however,apool’sprimarypurposeistomanageandreducerisk–notjustfinanceit.

Someofthebenefitsenjoyedbypoolmembersare:• Coverage:Unlikeinsurancecompaniesthatarefoundedtomakeaprofitandusemostlystandardlanguage

contractsfortheinsurancecoveragetheyprovide,poolstypicallycrafttheirowncoveragedocuments.This

providesthememberswiththeavailabilityofcoverage,terms,andlimitswhicharebestsuitedtoaddresstherisksofthemembers.

• Services:Riskmanagementistypicallyseenasadetractionfromaninsurancecompany’sbottomline.Thepoolingcommunityhascommittedmuchmorelaborandcapitaltoreduce,mitigate,andpreventlossesfromhappening.Thesecustomizedriskmanagementservicesareprovidedtomeetyourmembers’riskmanagementandadministrationneeds.

• Financialsavings:Reducedlosses,loweroverhead,leverageinthepurchaseofcatastropheinsurance(or“reinsurance”),andinvestmentincomethataccruestothemember-owners,allallowapooltoofferlowercostsoverthelongrunthancommercialinsurance.

• Budgetarystability:Thefinancialadvantages,togetherwithprudentfundingandmembercommitment,hasprovidedgreaterbudgetarystabilitytomembers.Thecommercialinsurancemarket,however,vacillatesgreatlydependingonanumberofinternalandexternalfinancialconditions.

Formations

Poolsareorganizeddifferentlyineachstate–afunctionofstatelaw.Theinitialformationanditsincorporatingdocumentsdeterminehowyourpoolinteractswithitsmembershipandregulators,andgenerallydoesnotallowforinterstatemembership.

Dependingwhereyoulivearoundthecountry,poolsmightbecalledJointPowersAuthorities,InterlocalAgreements,Trusts,Reciprocals,Funds,RiskRetentionGroups,andevenMutualInsuranceCompaniesandCaptiveInsuranceCompanies.Alloftheseareslightlydifferentinorganizationandregulatoryrequirements,butgenerallytheyallfunctionsimilarlytoyourownpool.

FoundationDocuments

Regardlessofpoolformationtype,youshouldhavemanyofthesamecorelegaldocuments.Thosearethepool’s‘Bylaws’andits‘MembershipAgreement’,whichsetforththeresponsibilitiesandrelationshipbetweenthepoolandeachmember.

Amongallthosegoverningdocuments,therecontainsprovisionswhichshouldaddressatleastthefollowing:• Membershipeligibilitycriteria• Obligationsofmembers• Membershiptermination• Powersanddutiesofgoverningbodies• Ownershipanduseanddistributionofassets• Assessments• Professionalcertifications(includingactuarialreviewsandfinancialaudits)• Governancepoliciesprovidingaframeworkforoperationalissue(i.e.targetsurplus,fundingcriteria,etc.)

Regulations

Themethodofpoolingregulationvariesfromstatetostate.Eachstatehastheauthoritytoregulatemunicipalinsuranceandriskpooling,mostoftendisparatelyso.Accordingly,it’scrucialtoknowyourstate’sregulationstoensurecomplianceandtheabilitytocontinueoperations.Evenlargely“unregulated”poolsneedtounderstandtheauthorityunderwhichtheyoperate,andbeawarethat,whileastatemaynotexercisemuchregulatoryoversighttoday,thatconveniencecouldchangetomorrow.

CoverageDocumentandLinesofBusiness

Intheinsuranceindustry,organizationssuchastheISO(“InsuranceServicesOffices”)promulgatestandardizedcoveragelanguagethat,intheory,helpsregulatorswiththeapprovalprocess,andleadstowardmoreconsistentcoverageinterpretations.Nevertheless,disputesarise,andwhentheydo,thereisahugebodyofcourtcaselawtofallbackon.

Sincemostpoolsaren’ttechnicallyinsurers,theircoveragedocumentsarenot“insurancedocuments”;theyaremanuscriptcontractsbetweenthepoolandthemember,andgenerallyinterpretedunderContractLaw,ratherthanInsuranceLaw.Mostpoolsrefertotheircoveragedocumentsasthe“MemorandumofCoverage”,oran“MOC”.

WhetherISOformsormanuscriptcontracts,MOC’sshouldincludecertainsectionsthatallowforconsistentunderstandingandinterpretation.Theseinclude:

• Declarations:Also,referredtoasthe“DEC”page,thisusuallysinglepagequicklyoutlinesthespecificcoverage,limitdeductibles,andendorsementsthateachparticularmemberhaspurchased.

• Definitions:Identifiesandclearlydefineskeytermsforpurposesofthatparticularcoverage.• CoverageAgreement:Thebodyoftheagreementthatexplainswhattheexactcoverageasitisintended.• Conditions:Requirementsofthememberintheeventofaclaim,suchascooperatingwiththeinvestigation,

andtakingstepstominimizetheloss.• Exclusions:Clearlyexpressedrestrictionstotheintendedcoverage,someofwhichmaybequitestandard

(suchasasbestos,orlossescausedbywar),andsomewhichmaybespecifictothatpool(suchassubsidence,forapoolwithcoastalexposure).

• Endorsements:Standardormanuscript,theseareaddedtoanindividualmember’sMOCtochange,add,ordetractcoverage.Endorsementsarenegotiatedandagreeduponbyboththememberandthepool.

Ingeneral,thereareeighttypesofcoveragepoolsmightoffer:• Property• Boiler&Machinery(or,EquipmentBreakdown)• Crime&Fidelity• Liability• AutoLiability• Workers’Compensation• HealthorEmployeeBenefits• UnemploymentInsurance

WhataretheBasicDutiesofaPoolBoardMember?

Thelegalstructureofthepoolanditsboard–whetherdirectorsortrustees–presentslegalnuancesintherolesandresponsibilitiesofboardmembersthatarepool-specific.Thereare,however,somegeneralcharacteristicsthathelpensuretheboardpromotesthecooperativeculturethatisinstrumentaltoapool’ssuccess:

• Asamemberoftheboard,yourdutyistothepool–NOTtothememberyourepresent• Youarenotexpectedtobeatechnicalexpert,butyouareexpectedtoengagetechnicalexpertisewhen

needed,andtoalwaysactingoodfaith• Youareexpectedtodeliberateanddebatewithyourcolleaguesontheboard,butonceactionistaken,you

mustsupportthataction.Inotherwords,“TheBoardspeakswithonevoice.”

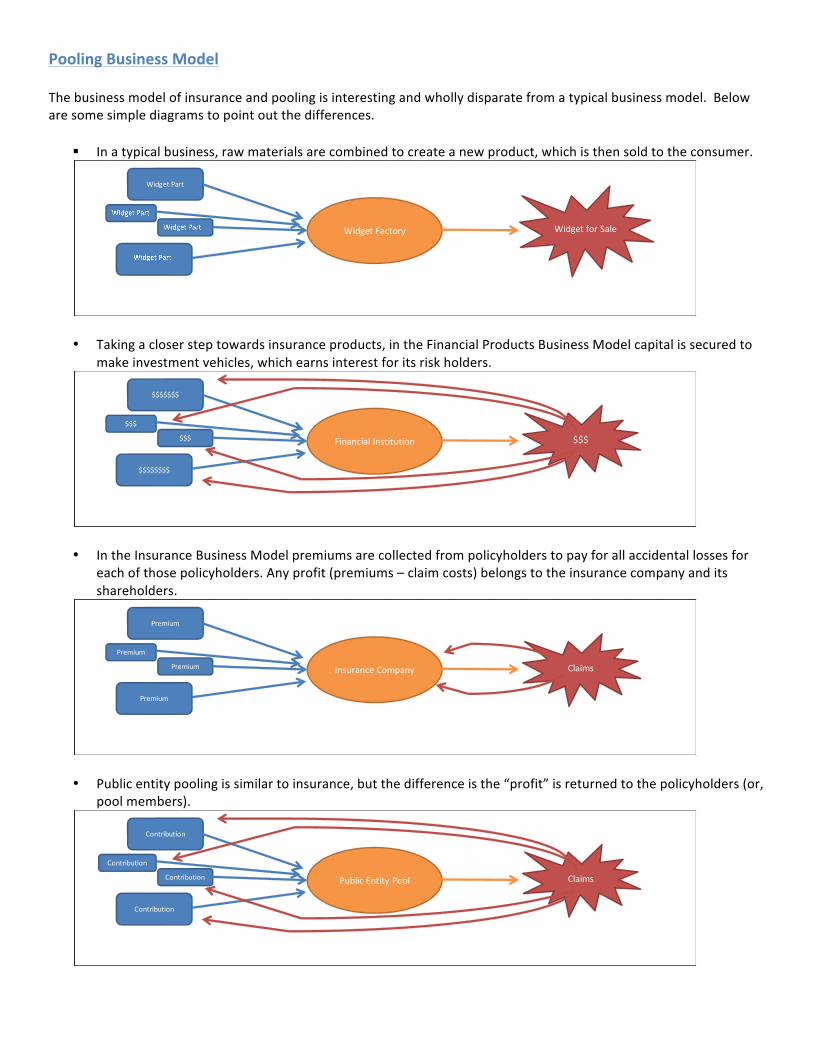

PoolingBusinessModel

Thebusinessmodelofinsuranceandpoolingisinterestingandwhollydisparatefromatypicalbusinessmodel.Belowaresomesimplediagramstopointoutthedifferences.

§ Inatypicalbusiness,rawmaterialsarecombinedtocreateanewproduct,whichisthensoldtotheconsumer.

• Takingaclosersteptowardsinsuranceproducts,intheFinancialProductsBusinessModelcapitalissecuredtomakeinvestmentvehicles,whichearnsinterestforitsriskholders.

• IntheInsuranceBusinessModelpremiumsarecollectedfrompolicyholderstopayforallaccidentallossesforeachofthosepolicyholders.Anyprofit(premiums–claimcosts)belongstotheinsurancecompanyanditsshareholders.

• Publicentitypoolingissimilartoinsurance,butthedifferenceisthe“profit”isreturnedtothepolicyholders(or,poolmembers).

WidgetPart

WidgetFactory WidgetforSale

$$$$$$$

$$$

$$$

$$$$$$$$

Financial Institution $$$

Premium

Premium

Premium

Premium

Insurance Company Claims

Contribution

Contribution

Contribution

Contribution

Public EntityPool Claims

Additionally,therearesomeinterestingaspectstothebusinessmodelofinsurancecompaniesandpublicentitypoolsversusthetraditionalbusinessmodel.Inmostbusinesses,youmakeaproductsuchasawidget.Thecostofmakingthatwidgetisknown,becauseyouhavetospendalmostallofthecostofmakingthatwidgetbeforeyousellittoaconsumer.Whenyousellthewidget,youaddupallthecoststomakeit,putinalittleprofit,andchargethecustomerthatprice.

Forinsuranceandpoolingcontracts,youchargethecustomerfirstintheformofpremiumsorcontributions,andthenyearsanddecadeslateryoufindouthowmuchthatproductcosts.Thatunknowncostforallthoseyearsanddecadesisreserves,whichareestimatedbytheclaimsstaffandanactuary.Likeallpredictions,theestimatesareneverassumedtobeentirelycorrect.Thoseunknownestimateshavetobebookedonourbalancesheetandincomestatement.Fortunately(quiteliterally),thereisabenefittothisbusinessmodel.Allthosebookedreservessittingonyourbalancesheetcanbeinvestedtogenerateinvestmentincome.Thisinvestmentincomecanusedtoeithergarneradditional“profit”ortolowerthecostofpremiums/contributions.

PoolingBasicsSession#1a–Underwriting

Monday,October3,1:45-3:00pm

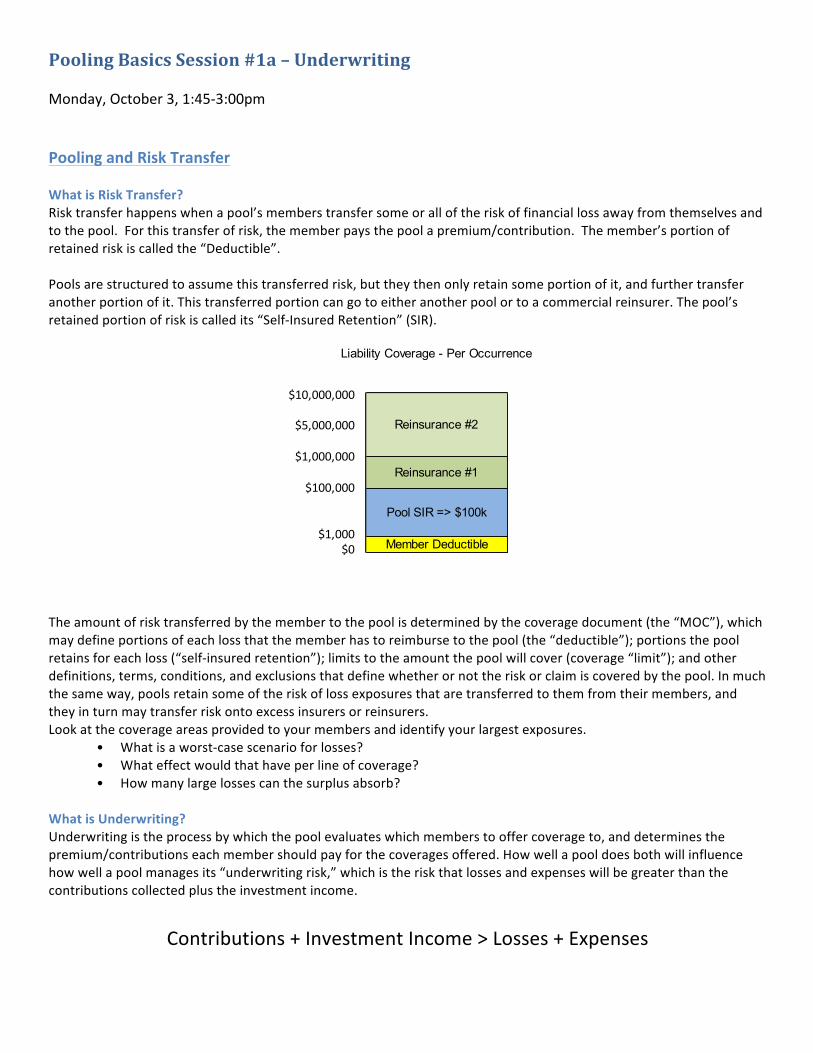

PoolingandRiskTransferWhatisRiskTransfer?Risktransferhappenswhenapool’smemberstransfersomeoralloftheriskoffinanciallossawayfromthemselvesandtothepool.Forthistransferofrisk,thememberpaysthepoolapremium/contribution.Themember’sportionofretainedriskiscalledthe“Deductible”.Poolsarestructuredtoassumethistransferredrisk,buttheythenonlyretainsomeportionofit,andfurthertransferanotherportionofit.Thistransferredportioncangotoeitheranotherpoolortoacommercialreinsurer.Thepool’sretainedportionofriskiscalledits“Self-InsuredRetention”(SIR).

Theamountofrisktransferredbythemembertothepoolisdeterminedbythecoveragedocument(the“MOC”),whichmaydefineportionsofeachlossthatthememberhastoreimbursetothepool(the“deductible”);portionsthepoolretainsforeachloss(“self-insuredretention”);limitstotheamountthepoolwillcover(coverage“limit”);andotherdefinitions,terms,conditions,andexclusionsthatdefinewhetherornottheriskorclaimiscoveredbythepool.Inmuchthesameway,poolsretainsomeoftheriskoflossexposuresthataretransferredtothemfromtheirmembers,andtheyinturnmaytransferriskontoexcessinsurersorreinsurers.Lookatthecoverageareasprovidedtoyourmembersandidentifyyourlargestexposures.

• Whatisaworst-casescenarioforlosses?• Whateffectwouldthathaveperlineofcoverage?• Howmanylargelossescanthesurplusabsorb?

WhatisUnderwriting?Underwritingistheprocessbywhichthepoolevaluateswhichmemberstooffercoverageto,anddeterminesthepremium/contributionseachmembershouldpayforthecoveragesoffered.Howwellapooldoesbothwillinfluencehowwellapoolmanagesits“underwritingrisk,”whichistheriskthatlossesandexpenseswillbegreaterthanthecontributionscollectedplustheinvestmentincome.

Contributions+InvestmentIncome>Losses+Expenses

Liability Coverage - Per Occurrence

Reinsurance #2

Reinsurance #1

Pool SIR => $100k

Member Deductible

$10,000,000

$5,000,000

$1,000,000

$100,000

$1,000$0

Herearesomegenerally-accepteduniversalunderwritinggoals:• Determinethetypesofriskthepooliswillingtoaccept,bydefiningthetypesofpublicentities,including

“demographics”likegeography,size,andmanagementstructure.Thisistheclassicdiversityversushomogeneityofriskdebate.

• Establishmember-specificunderwritingandratingcriteria,whichcapturesmostofyourintendedmarket,rewardingthegoodrisksandeliminating/minimizingthebadrisks.

• Makesurethattheguidelinesyouuseareappliedconsistently,asunfairdiscriminationinhowyouselectandpricememberswillleadtoconflictandevenlawsuitswithinthepool.

• Knowwhattheriskofcatastrophiclossesmaybeandhowitmightvaryforcertainmembers.Avoidexcessivesubsidizationofcertainmembersattheexpenseofothers.

Calculatingthepremiumorcontributionsofeachmemberisamarriagebetweenactuaryandunderwriter.Generally,mostratingsystemsincorporatingthesestepsinoneformoranother:

• Experiencerating• Exposurerating• Premiumallocation• Schedulerating

DifferencesofInsuranceandPoolingUnderwritingWhileinsuranceandpoolingunderwritingaresimilar,theydohavethreedistinctdifferences.Theseare:

• Communityrating• Useofdataanalytics• Howtheyacceptorrejectrisk

UnderwritingBiasItisimpossibletoremovebiasfromourlives,andthisistrueforunderwriters.Therearemanybiasestoavoid(https://en.wikipedia.org/wiki/List_of_cognitive_biases)tobecomecompletelyobjective,asnobleasthatgoalis.Relatedtobiasesistheconceptofdiscrimination,andbystatelawtherearecertaindiscriminationswecannotusewhileunderwriting(gender,race,religion,etc).But,essentially,thejoboftheunderwriteristofindadiscriminatorybasisamongthepolicyholderstowardsrisk.Ifyouhavetwoschoolsthatyouareunderwriting,andoneschoolisthoughttobetwiceasriskyastheother.Intuitively,youshouldchargethefirstschooltwiceasmuchcontributionasthesecond,right?But,whatbasisareyoumakingthatdeterminationof“twicetherisk”,absentanylossdata.Ifthefirstschoolhadtwiceasmanystudents,thenyoucouldmakearationalargumentthatitwouldbetwiceasrisky.But,ifyouweretoassesstherisklevelagainstaprotectedclass(forinstance,thefirstschoolisAllBoysandthesecondschoolisAllGirls),thenthatisillegal.So,underwritersneedtomakeasobjectiveselectorstoriskaspossible.Onecommonbiasis‘IngroupBias’,whichisthetendencytogivepreferentialtreatmenttootherstheyperceivetobemembersoftheirowngroup.So,backtotheschoolexample,perhapsevenwithtwiceasmanystudentsthefirstschoolgetsthesamepremiumasthesecondschool,merelybecauseitresidesinthesametownastheunderwriterlives.

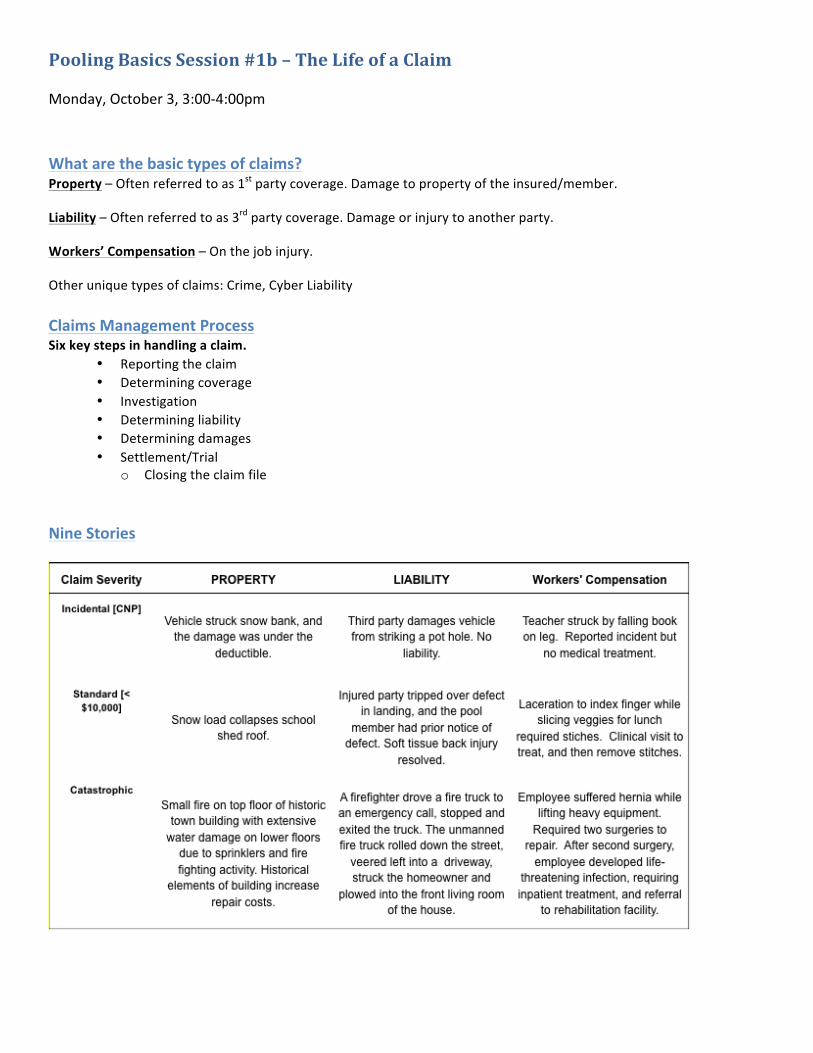

PoolingBasicsSession#1b–TheLifeofaClaim

Monday,October3,3:00-4:00pm

Whatarethebasictypesofclaims?Property–Oftenreferredtoas1stpartycoverage.Damagetopropertyoftheinsured/member.

Liability–Oftenreferredtoas3rdpartycoverage.Damageorinjurytoanotherparty.

Workers’Compensation–Onthejobinjury.

Otheruniquetypesofclaims:Crime,CyberLiability

ClaimsManagementProcessSixkeystepsinhandlingaclaim.

• Reportingtheclaim• Determiningcoverage• Investigation• Determiningliability• Determiningdamages• Settlement/Trial

o Closingtheclaimfile

NineStories

ReportingtheClaimKeycomponents:

- Timelyreporting- Adequateinformation(who,what,when,where,howorwhy)- Preventfurtherlossordamage

DeterminingCoverageKeycomponents:

- Whattypeofaclaim(property,liability,crime,cyber,workerscompensation,etc.)- Reviewcoveragedocument(s),reinsurance/excess- Reviewschedule(property)- Ifnocoverageorlimitedcoverage,denyclaimorinvestigateunderareservationofrights

InvestigationKeycomponents:

- Contactallpartiesinvolved,getstatements- Obtainalldocumentation,policereports,incidentreports,medicalreports- Phonevs.facetoface

DeterminingLiabilityKeycomponents:

- Negligence(atfaultparty/parties)- Comparativenegligence(lawsdifferfromstatetostate)- WorkersComp(state’sdefinitionoftheemployer’sresponsibilitytoanemployeeforinjuriesthatariseinthe

courseofemployment)- Subrogation(propertyclaims)

DeterminingDamagesKeyComponents:

- Obtainandevaluateallinvoices,bills,documents- Reasonableness- Property(actualcashvaluevs.replacementcost)- Generaldamages(painandsuffering,mentaloremotionaldistress)- Specialdamages(medicalbills,treatment,costtorepair)

Settlement/Trial

- Settlementauthoritylevels- Negotiatesettlementdirectlywithmember/claimant/attorney- ObtainProofofLoss(property)orReleaseofClaim- Mediation/Arbitration- Trial- WorkCompclaimstendtoremainopenforlongerperiodsoftime- Paymentofclaim/closingfile

Otherconsiderations:Reservepractices

BoardofDirectorsresponsibilitiesinclaims

Litigation–prosandcons,cost(financially/emotionally/reputational)

Independentclaimsaudits

PoolingBasicsSession#1c–ActuarialScience

Monday,October3,1:45-3:00pm

TheProbabilitiesandStatisticsofPredictingtheFutureActuariesplayavitalroleintheoperationandsuccessofpoolsbyprovidinganalysiscrucialtothefinancialviabilityofpools.Quitesimply,whenapooloffersitsproduct–indemnificationcoverage–itcannotknowforsurewhatitsfinalcostfortheproduct–theclaimsitwillpay,andwhenitwillpaythem–willbe.Thatiswhereactuariescomein.Actuariesaretrainedintriedandprovenstatisticalmethodsofmakingfuture“guesses”asaccurateaspossible.Thepool’sactuaryshouldalsobeinvolvedinestablishingthefundingrequirementsfortheupcomingyear,orthe“rates”thepoolwillchargemembers.Thisinvolvesprojectionsoffuturelosses,basedonpastexperienceandwhetherotherchangesareoccurring(suchaschangesincoverages,thelitigationenvironment,orbenefitslevelsinworkers'compensation)andaddingothercosts,suchasadministrativeexpensesandreinsurancecosts.Actuariesusemathematics,statistics,economics,andfinancetoanalyzethefinancialconsequencesofrisk.Inthiscase,therisksanalyzedarerelatedtothecoveragesor“riskscovered”bypools.

FundingStudiesSo,howdoyoufundforalossthathasyettooccur?Or,inbusinessterms,howdoyoupriceaproductyouaresellingtoday,whenyoudon’tknowtheultimateproductioncostsformanyyears(orevendecades)?Anactuaryconductsalossprojectionanalysis,whichisanestimateoftheretainedlossesthatwilloccurduringaspecifictimeperiodinthefuture,basedonthecoverageprovidedbythepooltoitsmembers.Inordertoprojectthelossesforthecomingperiod,anactuarywillreviewthehistoricallossesandexposuresassociatedwithpreviousperiods.Heorshewillalsoaskforinputfrommanagementonwhatmightbedifferentnextyear,intermsofchangingmembershiporcoverages,forexample.Anactuarywillfirstestimatetheultimatelossesforeachofthepreviousperiodsbasedonseveralactuarialmethods.Theincurredandpaidlossdevelopmentmethodsarethemostcommonandbasicmethodsused.ReserveStudiesAnactuarialreserveanalysisestimatesapool’soutstandingliabilitiesresultingfromtherisktransfercontractstheyhavewritteninthepast.Oneuniquecharacteristicofrisktransferproductsisthattheproductsarepricedbeforethepolicyiswritten,butthefinalcostmaynotbeknownforsometimesdecadeslater.Forpropertyrisks,itmayonlybefiveyears–yourbuildingburnsdown,youbuildanotherone.But,forworkers’compensation,aninjuredworkermighthavealifetimeofbenefits.Theliabilitiestobefundedconsistoftwocomponents:

1.Casereservesarethereserveamountsshownonthelossrun.Theyaretypicallyestimatedbyaclaimadjuster,lawyer,orotherinsuranceprofessional.Theyrepresenttheamountofmoneyestimatedforfuturepaymentsrelatedtoaparticularclaim.

2.IBNRreservescanbethoughtofascomposedoftwofurtherparts–PureIBNRreservesandreservesfordevelopmentonknownclaims.

• PureIBNRreservesaretheestimatedamountneededforclaimsthathavehappenedbuthavenotbeenreportedtothepoolyet.

• Reservesfordevelopmentonknownclaimsareestimatedadditionalamountsneededtoultimatelysettleknownclaimsinadditiontothecurrentcasereserves.

PoolingBasicsSession#2a–FinancialReportingandAuditing

Tuesday,October4,10:00-11:00am

BalanceSheetandIncomeStatementBasics

Animportantpartofanyorganizationisitsfinancialhealth.Twokeycomponentsofassessingandreportingfinancialhealtharebalancesheetsandincomestatements.Wewillexplainthebasicsofeachandhowtheyinterrelate.

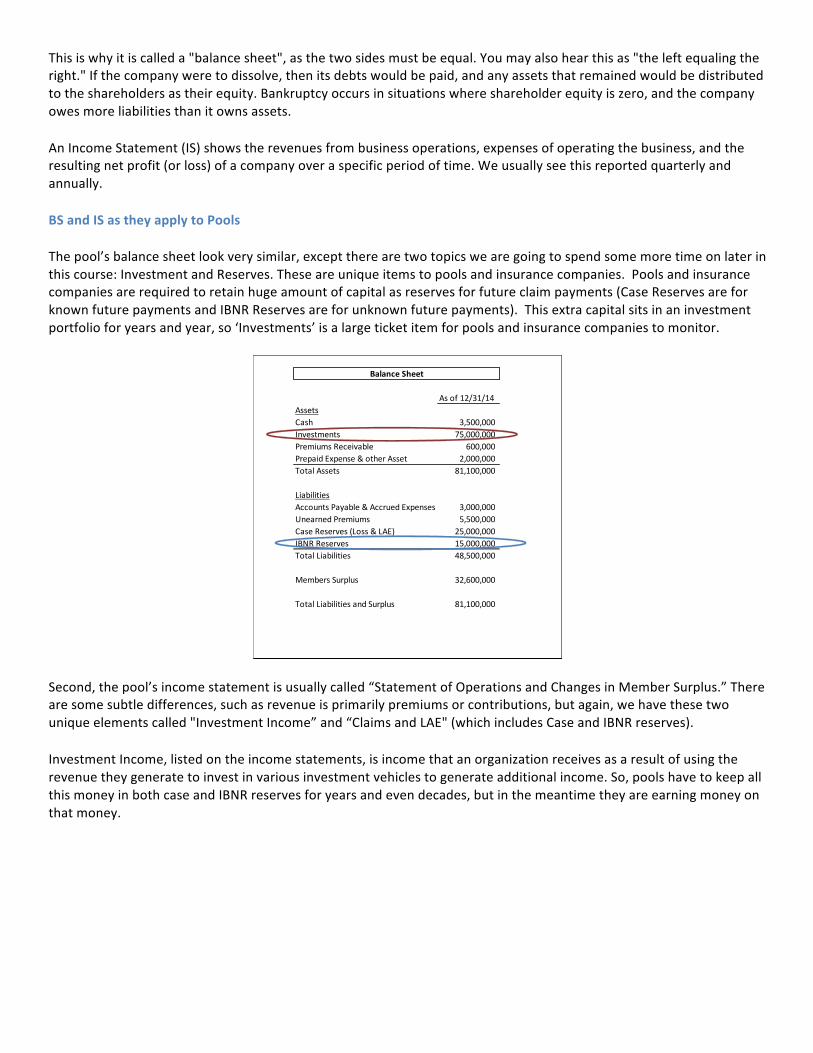

ABalanceSheet(BS)isastatementofacompany’sfinancialpositionataparticularmomentintime.Thisfinancialreportshowsthetwosidesofacompany’sfinancialsituation:whatitownsandwhatitowes.Whatthecompanyowns,calledits"assets,"isalwaysequaltothecombinedvalueofwhatthecompanyowes,calledits"liabilities,"andthevalueofitsshareholders’equity.

Assets=Liabilities+ShareholderEquity

Thisiswhyitiscalleda"balancesheet",asthetwosidesmustbeequal.Youmayalsohearthisas"theleftequalingtheright."Ifthecompanyweretodissolve,thenitsdebtswouldbepaid,andanyassetsthatremainedwouldbedistributedtotheshareholdersastheirequity.Bankruptcyoccursinsituationswhereshareholderequityiszero,andthecompanyowesmoreliabilitiesthanitownsassets.

AnIncomeStatement(IS)showstherevenuesfrombusinessoperations,expensesofoperatingthebusiness,andtheresultingnetprofit(orloss)ofacompanyoveraspecificperiodoftime.Weusuallyseethisreportedquarterlyandannually.

BSandISastheyapplytoPools

Thepool’sbalancesheetlookverysimilar,excepttherearetwotopicswearegoingtospendsomemoretimeonlaterinthiscourse:InvestmentandReserves.Theseareuniqueitemstopoolsandinsurancecompanies.Poolsandinsurancecompaniesarerequiredtoretainhugeamountofcapitalasreservesforfutureclaimpayments(CaseReservesareforknownfuturepaymentsandIBNRReservesareforunknownfuturepayments).Thisextracapitalsitsinaninvestmentportfolioforyearsandyear,so‘Investments’isalargeticketitemforpoolsandinsurancecompaniestomonitor.

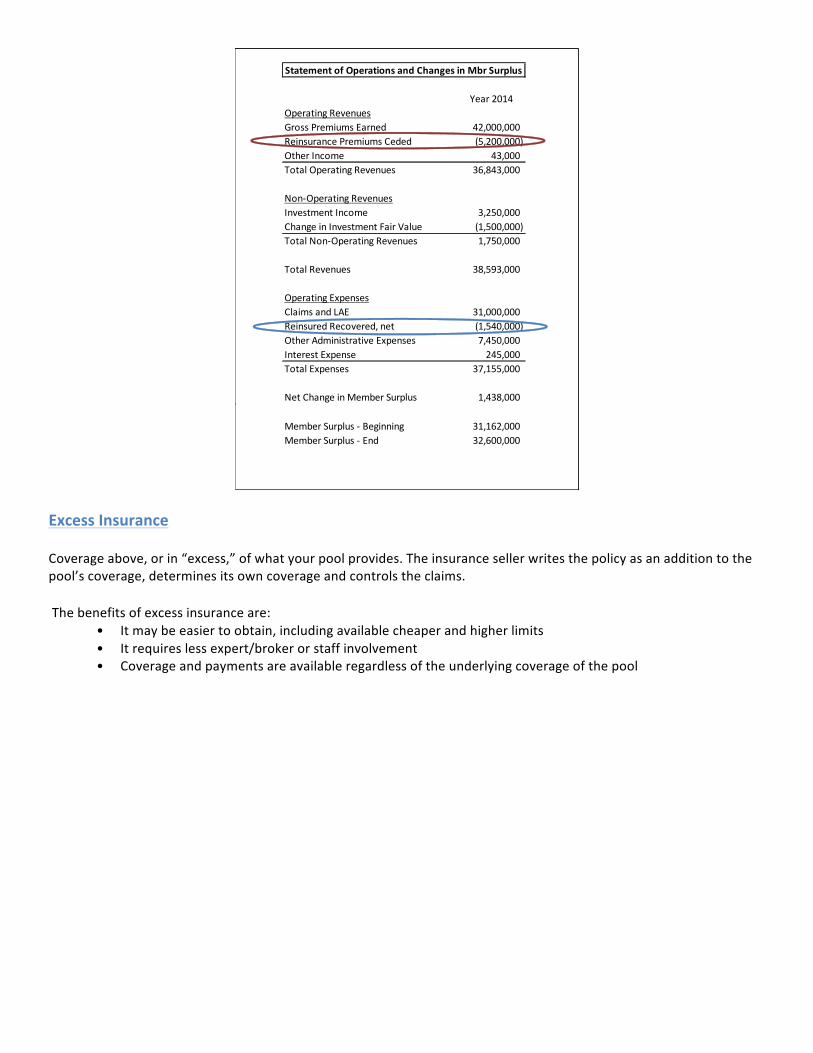

Second,thepool’sincomestatementisusuallycalled“StatementofOperationsandChangesinMemberSurplus.”Therearesomesubtledifferences,suchasrevenueisprimarilypremiumsorcontributions,butagain,wehavethesetwouniqueelementscalled"InvestmentIncome”and“ClaimsandLAE"(whichincludesCaseandIBNRreserves).

InvestmentIncome,listedontheincomestatements,isincomethatanorganizationreceivesasaresultofusingtherevenuetheygeneratetoinvestinvariousinvestmentvehiclestogenerateadditionalincome.So,poolshavetokeepallthismoneyinbothcaseandIBNRreservesforyearsandevendecades,butinthemeantimetheyareearningmoneyonthatmoney.

Asof12/31/14AssetsCash 3,500,000Investments 75,000,000PremiumsReceivable 600,000PrepaidExpense&otherAsset 2,000,000TotalAssets 81,100,000

LiabilitiesAccountsPayable&AccruedExpenses 3,000,000UnearnedPremiums 5,500,000CaseReserves(Loss&LAE) 25,000,000IBNRReserves 15,000,000TotalLiabilities 48,500,000

MembersSurplus 32,600,000

TotalLiabilitiesandSurplus 81,100,000

BalanceSheet

Reinsurance

Reinsuranceisessentially“insuranceforinsurancecompanies,”or,inourcase,“insuranceforpools”.Thepool’scoveragedocumentdefinescoverage,andthereinsurer“followstheform”ofthepool’scoveragedocument.Typically,controloftheclaimremainswiththepoolaswell,andthereinsurer“followsthefortunes”ofthepoolintermsofhowtheclaimisresolved.

Thebenefitsofreinsuranceare:• Yourabilitytocontroltheinterpretationandapplicationofthecoveragedocumentissuedtothemember• Makingyourowncoveragedecisions• Adjustingyourownclaims

Year2014OperatingRevenuesGrossPremiumsEarned 42,000,000ReinsurancePremiumsCeded (5,200,000)OtherIncome 43,000TotalOperatingRevenues 36,843,000

Non-OperatingRevenuesInvestmentIncome 3,250,000ChangeinInvestmentFairValue (1,500,000)TotalNon-OperatingRevenues 1,750,000

TotalRevenues 38,593,000

OperatingExpensesClaimsandLAE 31,000,000ReinsuredRecovered,net (1,540,000)OtherAdministrativeExpenses 7,450,000InterestExpense 245,000TotalExpenses 37,155,000

NetChangeinMemberSurplus 1,438,000

MemberSurplus-Beginning 31,162,000MemberSurplus-End 32,600,000

StatementofOperationsandChangesinMbrSurplus

ExcessInsurance

Coverageabove,orin“excess,”ofwhatyourpoolprovides.Theinsurancesellerwritesthepolicyasanadditiontothepool’scoverage,determinesitsowncoverageandcontrolstheclaims.

Thebenefitsofexcessinsuranceare:• Itmaybeeasiertoobtain,includingavailablecheaperandhigherlimits• Itrequireslessexpert/brokerorstaffinvolvement• Coverageandpaymentsareavailableregardlessoftheunderlyingcoverageofthepool

Year2014OperatingRevenuesGrossPremiumsEarned 42,000,000ReinsurancePremiumsCeded (5,200,000)OtherIncome 43,000TotalOperatingRevenues 36,843,000

Non-OperatingRevenuesInvestmentIncome 3,250,000ChangeinInvestmentFairValue (1,500,000)TotalNon-OperatingRevenues 1,750,000

TotalRevenues 38,593,000

OperatingExpensesClaimsandLAE 31,000,000ReinsuredRecovered,net (1,540,000)OtherAdministrativeExpenses 7,450,000InterestExpense 245,000TotalExpenses 37,155,000

NetChangeinMemberSurplus 1,438,000

MemberSurplus-Beginning 31,162,000MemberSurplus-End 32,600,000

StatementofOperationsandChangesinMbrSurplus

PoolingBasicsSession#2b–RiskManagement,TheFutureofPooling,andQuestions&Answers

Tuesday,October4,11:00-12:15pmRiskManagementinthePoolingContext"Riskmanagement"isacorefunction–somewouldsayTHEcorefunction–ofpools.Mostdefinitionsofriskmanagementinvolvetheprocessoftheidentification,assessment,andtreatmentofrisk,where"risk"isuncertaintyandusuallyviewedasnegative,asinthepossibilityofloss,damage,orharm.Youwillhearreferencestoanumberofprograms,activitiesorfunctions,allofwhichareformsofriskmanagement.Someofthemorecommoninclude:

• Lossprevention:Referringtoeffortstokeepbadoutcomesfromhappeninginthefirstplace,oftenthroughbettertrainingofemployeestoavoidinjurytothemselvesorothers;adoptionandenforcementofgoodpoliciesforpublicofficialstofollow;wellnessprogramstoimproveemployeehealth;anduseofpreventivemaintenanceprogramsforpropertiesandpublicinfrastructure.

• Losscontrol:Referringtoeffortstoreducethesizeofanylossthatdoesoccur,throughpromptreporting,proactiveclaimmanagement,andpostincidentoraccidentreview.

• Safety:Mostcommonlyassociatedwithemployeeon-the-jobinjuryprevention,butalsoapplicabletocreatingandassuringsafeenvironmentsforthepublic,orsafeoperationofvehiclesorequipment.

• Training:Agrowingareaofactivityforpools,especiallyusingnewtechnologyforefficiency,andoftentoincludecomplianceissues.

Oneofthemostimportant,yetchallenging,aspectsofriskmanagementisdetermininghowmuchtoinvestinriskmanagementprogramsandservices(i.e.measuringtheireffectiveness).Howdoyouknowifthespecificinvestmentsactuallyhadanimpactonthelosscosts?Maybethereductionwouldhavehappenednomatterwhat.Maybeitisjustgoodluck.CreatingaCultureofRiskManagementPerformanceimprovementprotocols:Toencouragetherightbehavior–andforthebenefitoftherestofthemembership–poolsadoptprogramsthatrequirememberstomakechangesinordertostayinthepool,andevenrefuserenewal,ifnecessary.Thismightalsotaketheformofincentivizedpricingforthosemembersofthepoolsthatadheretostrictsafetypracticesorrecommendedchangestoexistingpolicies.Casestudies:Sharingthepositiveresultsofonememberwithothers,andleveragingpilotprogramsacrossthewholepoolmembership,isanaturalwayforpoolstoimprovetheirriskmanagementculture.Dataanalysis:Poolsnowhave20to40yearsofdata,andtoolstobetteranalyzethedata,tounderstandwhatworks,andwhatdoesn't,thatcanhelpthepoolengageitsmembersinthevalueofriskmanagement.TheFutureofPublicEntityPoolingWhatdoesthefuturehold?That’satoughquestion,butAGRiPhastakenthestepstoensurewestartthinkingaboutthefutureinadisciplinedway.ThroughourResidentFuturistRebeccaRyan,wecanbrieflytalkaboutfoursegmentsofthefuturethatwillaffectpooling(and,notinsignificantly,therestofourlives,aswell).GenerationalShiftsAstheBabyBoomergenerationmovestowardsretirement,theoriginalfoundersofthepoolingmovementwillbetakingalltheirinstitutionalknowledgewiththiswhentheyleavethepool.Additionally,anationwideshortageofGenerationX’erstoreplacethemwillleadanemployee’smarketforemployment.Poolswillhavetoremaincompetitivetoretainthebeststaffing,andcontinuetoinnovatetointerestyoungerworkers.

TechnologyThereisnodoubtthattechnologyhasandwillcontinuetochangeourlivesandourbusinessmodels.But,howso?Whocouldhavepredicted20yearsagohowtheInternetandsocialmediawouldfundamentallychangebusinessmodelscenturiesold?So,whatisnext?Noonecansayforcertain,butit’sagoodbettogoaskyourinternwhatheorshethinks…LeadershipChangesAsthepoolingstaffturnsoverinfavorofayounger,moretechnologicallymindedemployee,poolmanagementneedstocontinuetoengagenotonlythem,butthepoolmemberrepresentatives,aswell.On-sitemeetings,mailedflyers,andphysicallocationsarenolongerimportant.Newmanagersmustintegratenewmethodstoengagenewemployeesandconstituencies.Newmanagersmustharnessthepowerofinformationanddisseminateittoeveryoneseamlesslyandconstantly.CatastrophicWeatherIrregardlessofwhocausedit,thereislittledoubtthatweatherpatternsarechangingfromhistoricaldata.Patternsarebecomingmoreerraticandsevere,andcatastrophicweatherisplaguingareaswherepreviouslytherewasnone.Aspoolsgrapplewiththeseenormouslossevents,riskmanagersandunderwritershavetore-doubletheireffortsandre-thinkwhatwaspreviouslyimprobable.Moregenerally,poolsneedtoleadthechargeofinfluencingpublicentitiestore-thinktheirinfrastructure,maintainedproperties,andsocialservices.

Related Documents