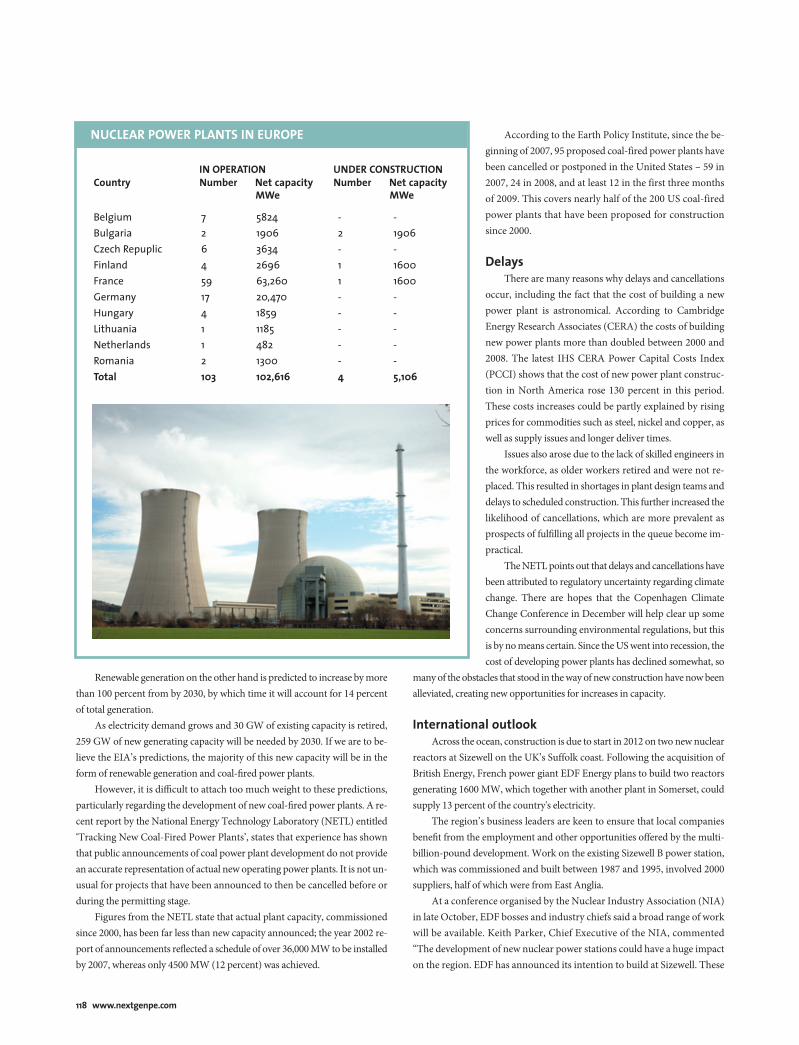

www.nextgenpe.com • Q4 2009 BALANCING THE LOAD Page 50 A PERFECT FIT Page 98 ENERGIZING THE FUTURE Page 117 Will the pressure of public opinion dissolve the Obama Administration’s atomic plans? Page 32 PRACTICAL MATTERS Michael Morris tackles the issue of renewable energy Page 40 SMART POLITICS Making funding decisions about the intelligent grid Page 44 RENEWED INTEREST The transatlantic future of alternative energy sources Page 80 Meltdown Nuclear

P&E US 8

Mar 27, 2016

Power & Enrgy US magazine. Issue 8. November 2009. The problems with Obama's nuclear plans, and why this is a pivotal time for the development of renewable energy policies.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.nextgenpe.com • Q4 2009

BALANCING THE LOAD Page 50 A PERFECT FIT Page 98 ENERGIZING THE FUTURE Page 117

Will the pressure of public opiniondissolve the Obama Administration’s

atomic plans? Page 32

PRACTICAL MATTERSMichael Morris tackles theissue of renewable energy

Page 40

SMART POLITICSMaking funding decisionsabout the intelligent grid

Page 44

RENEWED INTERESTThe transatlantic future ofalternative energy sources

Page 80

MeltdownNuclear

COVER NG P&E8 viz2_nov09 06/11/2009 09:52 Page 1

PVP_DPS_AD.indd 1PVP_DPS_AD.indd 1 3/11/09 10:55:353/11/09 10:55:35

PVP_DPS_AD.indd Sec1:1PVP_DPS_AD.indd Sec1:1 3/11/09 10:55:383/11/09 10:55:38

ITRON_DPS_AD.indd 2ITRON_DPS_AD.indd 2 3/11/09 10:44:533/11/09 10:44:53

ITRON_DPS_AD.indd 3ITRON_DPS_AD.indd 3 3/11/09 10:44:553/11/09 10:44:55

MSE_AD.indd 4MSE_AD.indd 4 3/11/09 10:50:113/11/09 10:50:11

With December’s UN Cli-mate Change Conference in Copenhagen looming, and as we grow ever more

aware of our eff ect on the environment, the pressure to develop new sources of renewable energy increases.

Th anks in part to this trend, nuclear power is currently undergoing a well-documented revival, both here in the US and abroad. Oft en billed as an environmentally friendly option because of its zero carbon emissions, nuclear has been hailed as the potential savior of coun-tries keen to cut back on CO2 while keeping their power-hungry populations happy.

Nuclear seems the obvious choice for a fl edgling government seeking popular support – which explains the positive spin put on it by President Obama, who even mentioned it in his presidential acceptance speech.

But nuclear comes with some not-so-hid-den downsides. Th ose with long memories will still be haunted by visions of Th ree Mile Island

and Chernobyl. And quite apart from the potential for a leak or ‘core damage incident’ – admittedly mitigated by improvements in technology and safety since the 1970s and ’80s – there is the problem of storing the radioactive waste produced by the nuclear fi ssion process.

Th ese issues are serious enough to make the reintroduction of nuclear power contro-versial in some quarters, resulting in a dilem-ma for Obama and his team: how to appease both sides? Th e apparent answer is to talk up the positive aspects of new nuclear while hold-ing back on handing out any actual cash for its development. As Associate Editor Natalie Brandweiner discovers in her in-depth look at the new administration’s nuclear policies, such a delicate juggling act can be a hard one to keep up.

Elsewhere in this issue, American Elec-tric Power CEO Michael Morris outlines his stance on renewable energy sources. In his view, our current generation and transmis-sion system must be restructured if we are to

FROM THE EDITOR

Climate crunch

reach our ultimate goal of becoming greener and less dependent on fossil fuels. He warns, however, that those who believe we can do this without spending any extra money are fooling themselves.

We also take a look at the latest news on the smart grid, oft en touted as an essential ele-ment in our drive toward increased energy ef-fi ciency. Will governmental wrangling thwart its development?

Unless we can work things out at a politi-cal level, all the eff ort we put into reducing our environmental impact will go to waste. Th at’s why events like Copenhagen are so important – without them, the future of our planet may hang in the balance.

Marie Shields, Editor

Why this is a pivotal time for the development of renewable energy policies.

5

“Solar energy presents a little more complex picture than traditional renewable sources” Mike Taylor, Director of Research and Education, Solar Electric Power Association (p90)

“There is great promise in technologies around traditional pulverized coal”Chris Hobson, SVP and Chief Environmental Offi cer, Southern Company (p94)

“Politicians always want to sell happy dust, the whole notion that we can do this without any pain. But you know it’s not true”Michael Morris, CEO American Electric Power (p38)

EDITORS NOTE.indd 5EDITORS NOTE.indd 5 6/11/09 13:22:426/11/09 13:22:42

AT&T_DPS_AD.indd 6AT&T_DPS_AD.indd 6 3/11/09 10:35:063/11/09 10:35:06

AT&T_DPS_AD.indd 7AT&T_DPS_AD.indd 7 3/11/09 10:35:073/11/09 10:35:07

BPSolar_AD.indd 8BPSolar_AD.indd 8 3/11/09 10:37:503/11/09 10:37:50

44

Keeping it realMichael Morris takesa pragmatic approachto renewable energy

80

32

38

Power playPolitics and the smart grid

Sustainable energyshowdownHow renewables are shaping up inthe US and Europe

CONTENTS9

Sleight of handIs the Obama Administration’s supportfor nuclear power merely an illusion?

CONTENTS_nov09 05/11/2009 15:01 Page 9

RAMMOUNT_AD.indd 10RAMMOUNT_AD.indd 10 3/11/09 10:58:053/11/09 10:58:05

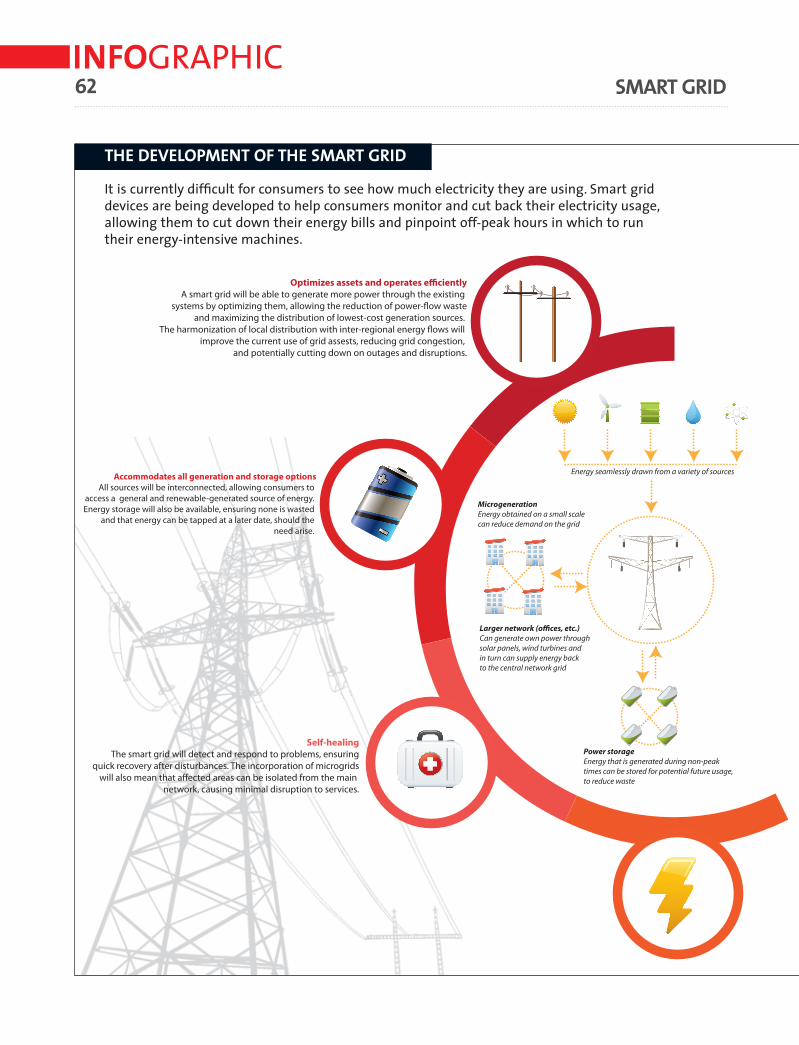

SMART GRID50 Balancing the loadMark Case outlines BGE’s smart grid program

56 Rise of the machinesHow Southern California Edison is deployingcutting-edge technologies

76 Risk assessmentAnnabelle Lee on security within the smartgrid infrastructure

RENEWABLES84 Pushing the boundaries AEP uses technological innovation to diversifyits fuel mix

90 Saving up the sunHow do issues of storage affect solar energy’sviability?

94 The case for carbonWhy Chris Hobson supports clean coal

98 A perfect fitRhone Resch looks at solar’s place in theenergy puzzle

102 Tapping the sourceHow to get in on the flow of money for newprojects in renewable energy

104 Adding value to the gridBrad Roberts on the latest energy storagetechnologies

84

50

Pushing the boundaries Balancing the load

66Smart grid

CONTENTS11

G O L D S P O N S O R S

INDUSTRY INSIGHT

60 David Wilkinson, RAMMounting Systems78 Jeff Newman, Enfora

ASK THE EXPERT

48 Alex Brisbourne, Kore Telematics

CONTENTS_nov09 05/11/2009 15:01 Page 11

TELUS_B2B_AD.indd 75TELUS_B2B_AD.indd 75 3/11/09 11:00:423/11/09 11:00:42

CONSTRUCTION117 Energizing the futureA round-up of current power plantconstruction projects

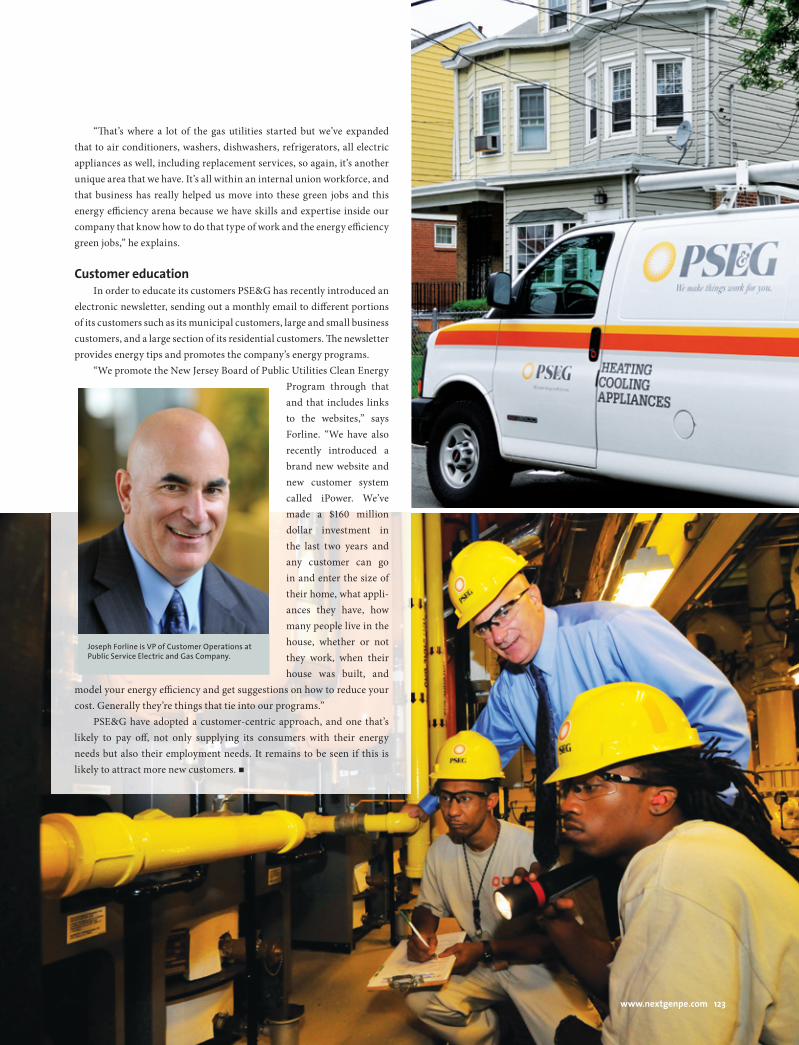

CUSTOMER OPERATIONS122 Saving money through energyefficiencyJoseph Forline explains how PSE&G is givingback to its customers

90

114

Saving up the sun

Looking for a new breed of CEO

A perfect fit

98

Green leader: Denmark

124 Comment: Climate change 126 Regional focus: Denmark 128 Photo finish

108 Renewable recoveryThe future is bright for green energy, saysMike Eckhart

110 Gridlock?What the Golden State is doing to overcomeits transmission infrastructure challenges

114 Looking for a new breed of CEOAnita Hoffmann examines the CEO talent inthe cleantech sector

IN THE BACK

CONTENTS13

ROUNDTABLE

66 Smart gridWith AT&T’s Kevin Jones, MalcolmUnsworth of Itron, Jim Hanson ofMotorola Inc., Andrew A. Bochman ofIBM’s Ounce Labs, Allan Breitmayerof Sierra Wireless and TELUS BusinessSolutions’ Roland Labuhn

EXECUTIVE INTERVIEW

88 Nancy Hartsoch, SolFocus97 Gregg Patterson, PVPowered, Inc.121 Alan Saunders, Autodesk

CONTENTS_nov09 05/11/2009 15:01 Page 13

Chairman/Publisher SPENCER GREENDirector of Projects ADAM BURNSEditorial Director HARLAN DAVIS

Worldwide Sales Director OLIVER SMART

Editor MARIE SHIELDS,Managing Editor BEN THOMPSON

Associate Editor NATALIE BRANDWEINERDeputy Editors REBECCA GOOZEE, DIANA MILNE, JULIAN ROGERS,

STACEY SHEPPARD, HUW THOMAS

Creative Director ANDREW HOBSONDesign Directors ZÖE BRAZIL, SARAH WILMOTT

Associate Design Directors MICHAEL HALL, CRYSTAL MATHER, CLIFF NEWMAN

Assistant Designer CATHERINE WILSON

Online Director JAMES WESTOnline Editor JANA GRUNE

Project Director HEATHER BRIDEN

Senior Project Director BROOKE THORPE

Sales Executives DDANIEL SULLIVAN, ANGELA BYRNE, LAUREN MITTLEBERG,

RYAN GOLTZMAN, MELISSA LUONGO

Finance Director JAMIE CANTILLON

Production Coordinators HANNAH DUFFIE, LAUREN HEAL,

RENATA OKRAJNI

Director of Business Development RICHARD OWEN

Operations Director JASON GREEN

Operations Manager BEN KELLY

Subscription Enquiries +44 117 9214000. www.nextgenpe.com

General Enquiries [email protected]

(Please put the magazine name in the subject line)

Letters to the Editor [email protected]

Next Generation Power and Energy Trump Building, Floor 5 , 40 Wall Street, New York NY 10005, USA

Tel: +1 212 920 8181. Fax: +1 212 796 7010. E-mail: [email protected]

Legal InformationThe advertising and articles appearing within this publication refl ect the opinions

and attitudes of their respective authors and not necessarily those of the publisher or editors. We are not to be held accountable for unsolicited manuscripts, transparencies or

photographs. All material within this magazine is ©2009 NG P&E.

GDS InternationalGDS Publishing, Queen Square House, 18-21 QueenSquare, Bristol BS1 4NH.

+44 117 9214000. [email protected]

Find Out MoreContact NGU at (+1) 212 920 8181

www.ngusummitna.com

The NGU Summit is a three-day critical information gathering of the most infl uential and important CIO’s from across America.

NGU Summit US 2010

Four Seasons, Las Colinas, Texas10-12th May 2010

A Controlled, Professional & Focused EnvironmentThe NGU Summit is an opportunity to debate, benchmark and learn from other industry leaders. It is a C-level event reserved for 100 participants that includes expert workshops, facilitated roundtables, peer-to-peer networking, and coordinated technology meetings.

A Proven FormatThis inspired and professional format has been used by over 100 executives as a rewarding platform for discussion and learning.

“Two of the most productive days I have ever spent at a conference. High caliber participants who were fully engaged in discussions of very relevant topics” Barbara Siehr, VP Energy Delivery, Customer Services, Alliant Energy

“NGU is a unique conference for offering undivided attention of potential customers or leading consultants as part of their seminar package.” Ali Nourai, Manager Distributed Energy Resources, AEP

CREDITS.indd 14CREDITS.indd 14 5/11/09 15:02:375/11/09 15:02:37

SUNGUARD_AD.indd 65SUNGUARD_AD.indd 65 3/11/09 11:37:203/11/09 11:37:20

UPFRONT16

Addressing the media on the fi nal day of the two-week long Bangkok talks on

climate change, Executive Secre-tary of the United Nations Frame-work Convention on Climate Change Yvo de Boer called the talks “constructive” and said he believed all the ingredients were there for a successful outcome for the Climate Change Conference in Copenhagen in December.

“Whatever the atmosphere at the moment, I think signifi cant advances have been made here to get us close to something which can serve as the basis for agree-ment in Copenhagen,” de Boer said at the conclusion of the talks.

However, he also pointed out that while countries’ negotiators have shown rapid progress on concrete ways to implement the

mandate, he believes they are still clinging to long-held diff erences. De Boer stressed the urgency of raising ambitions and bridging this divide.

“Th is session has been char-acterized by real advances and real work to put together impor-tant parts of the architecture of the Copenhagen agreement but you can only take good faith so far. . . . Th e stark reality out there is that unless we see an advance on those key political issues, it is very diffi cult for negotiators in this process to continue their work in good faith,” he said.

During the sessions in Bang-kok, negotiators resolved about half of the 2500 points of conten-tion in the 200-page negotiating text, including determining ways to help poor countries to adapt to the eff ects of climate change,

transfer cleaner technology and collect and distribute funds to assist the poorest nations.

However, rich and poor na-tions ended the week further apart on at least one issue. Th e European Union and the United States made it clear that they wanted to put a new treaty in place of the Kyoto Protocol, causing delegates from developing nations to walk out. Th ey accused the economically powerful countries of wanting to “kill off ” Kyoto, despite the em-phasis it places on encouraging development in poorer areas.

China, along with the major-ity of developing nations, insists that industrialized countries cut emissions by at least 40 percent of 1990 levels by 2020, the frame-

work of which was decided by the Kyoto Protocol in 1997.

Targets for emissions cuts by developed countries still fall short of their required levels, although they are creeping upwards, mostly

as the result of the introduc-tion of more ambitious

goals by Japan’s new government. Th e World Resources Institute calculates that the targets

amount to cuts of about 10 to 24 percent

below 1990 levels by 2020. By contrast, scientists have said that cuts of 25 to 40 percent are needed to have a real eff ect on global warming.

Oil-rich Norway provided the one bright spot in Bangkok by promising a 40 percent cut if agreement is reached in Copenha-gen. Observers saw this as a moral gesture more than a practical one,

THE BRIEF

Cuts of

are needed to have a real

effect on global warming

25% to 40%

BANGKOK CLIMATE CHANGE TALKS

United Nations climate chief Yvo de Boer

UPFRONT.indd 16UPFRONT.indd 16 5/11/09 16:37:465/11/09 16:37:46

UPFRONT17

because it would have little impact on total emissions from the indus-trialized world, given Norway’s small size.

Th ere was also no break-through on how much money to give to the world’s poorest coun-tries in order to help them prevent global warming, despite a proposal by British Prime Minister Gordon Brown this summer for an amount rising to $100 billion a year.

Th e Philippines’ Bernarditas Muller commented: “We are ex-tremely concerned by the lack of numbers and clear funding com-mitments by the developed world.” Su Wei, China’s chief negotiator, said, “We came here with hope and confi dence, but have to leave with disappointment and deep concern.”

Su, who is Director of the Cli-mate Change Policy Department of the Chinese National Development and Reform Commission, said some developed countries adopted a “passive attitude” in combating climate change during the talks. “Th ey neither off ered satisfactory plans on their own emissions cuts, capital and technological transfer to developing countries, nor re-sponded positively to developing nations’ suggestions on these as-pects,” he added.

“Th e talks involved a confl ict of interests, so they could not run smoothly,” Qi Jianguo, an eco-nomic and environmental policy researcher at the Chinese Academy of Social Sciences, told the Chinese news agency Xinhua.

Many eyes are now on Presi-dent Obama, in the hope that he will travel to Copenhagen in De-cember aft er receiving his Nobel Peace Prize in Oslo. His attendance would ensure a level of attention that could make all the diff erence to the talks’ success.

THE BRIEF

NEWS IN PICTURES

Solar panels on a yurt in Tajikistan. A small panel can save a family up to one dollar per day on the cost of kerosene.

A student cleans solar panels to maximize energy effi ciency during the Department of Energy Solar Decathlon in Washington, DC.

A maze of electrial wires above a street in Shanghai China. China recently overtook the US as the world’s biggest emitter of CO2.

A full moon next to a wind energy turbine near Filsum, Germany. The country is a leader in installed wind capacity, with 25 GW.

NEWS IN PICTURES

UPFRONT.indd 17UPFRONT.indd 17 5/11/09 16:37:535/11/09 16:37:53

UPFRONT18 PROFILE

LISA JACKSON, ADMINISTRATOR, ENVIRONMENTAL PROTECTION AGENCY

Currently serving as the Administrator of the Environmental Protection Agency (EPA), Jackson is regarded as one of the most pow-erful women in US environmental politics. Offi cially nominated by President Obama in December 2008, she was confi rmed through unanimous consent of the US Senate in January 2009.

Beginning her career with the EPA in 1986, Jackson has always been at the forefront of environmental strategies. During her tenure at the EPA, she worked on the federal Super-fund program, developing hazardous waste clean-up regulations and overseeing proj-ects throughout New Jersey, later becoming Deputy Director and Acting Director of the region’s enforcement division.

Delving further into politics, Jackson joined the New Jersey Department of Environmental Protection (DEP) in 2002 as Assistant Com-

missioner of Compliance and Enforcement and headed numerous programs such as land use regulation, water supply and geological surveys. Most notable was the department’s creation of standards for the Highlands Water Protection and Planning Act.

Becoming Commissioner of Environmental Protection was the logical next step for Jack-son, and she led a team of 2990 professionals responsible for protecting New Jersey’s natural and historic resources. She actively aimed to aid those communities that had long been ne-glected, and led numerous compliance sweeps on areas heavily aff ected by pollution, such as Camden and Patterson. Opinion regarding strong enforcement was divided at that time, and she received much criticism from those working on toxic clean-ups at the local level.

She became Chief of Staff to the Governor of New Jersey, handling all state operations

and political liaisons for the governor, before being appointed to her federal posi-tion by the President. In her role at the EPA, she is currently attempting to push through the Clean Air Act. Th e act declares CO2 to be a public health threat and paves the way for the government to impose taxes on US businesses producing large amounts of CO2. It is expected to provide the basis for cap and trade.

The suppression of a report in June brought Jackson under question. It was alleged she was involved in withholding data written by Alan Carlin that was unsupportive of climate change. Senator John Barrosso of Wyomng has also accused her of taking de-cisions based “more on political calculations than scientifi c ones”. Combine that with damning reports from DEP employees, and her time in federal government is likely to be a colorful one.

UPFRONT.indd 18UPFRONT.indd 18 5/11/09 16:37:595/11/09 16:37:59

UPFRONT19

FAST FACT

GOAL WITHIN REACH HITTING THE OCEAN FLOOR

Source:

Th e Obama Administration has not given up trying to get approval of its climate policy in the Senate before the UN Climate conference in Copenhagen in December. Carol Browner, White House Adviser on Energy and Environment, says that it is still possible to get a political mandate from the Senate in time.

“Th is administration from day one has been about taking action and we are still working very, very hard to get a bill out of the Senate,” she says.

She believes it is still possible for the Senate to pass energy and climate legisla-tion this year, even as a debate over the US healthcare system dominates the Congres-sional calendar.

“We haven’t given up trying. Th ere are still windows where time could come available…We feel very, very confi dent that we can work with the rest of the world to take signifi cant steps forward in Copen-hagen,” Browner said in an interview with Bloomberg News.

Maldives government offi cials literally took a dive in October to raise awareness about climate change. Members of the cabinet staged a meeting six meters under a lagoon to highlight the threat of global warming to the lowest-lying country in the world.

President Mohammed Nasheed and 13 others pulled on scuba gear and commu-nicated via hand signals while seated around a table in the lagoon on the island of Girifushi. Th e meeting aimed to draw attention to fears that rising sea levels caused by polar ice cap melt could swamp this Indian Ocean archipelago within the next 100 years. Th e islands are currently only an average of 2.1 meters above sea level.

The proportion of renewable energy in Denmark is to be increased to

rising to

“What we are trying to make people re-alize is that the Maldives is a frontline state. Th is is not merely an issue for the Maldives but for the world,” Nasheed said.

Against a backdrop of coral, the Presi-dent, Vice President, Cabinet Sec-

retary and 11 ministers signed a document calling on all

nations to cut their carbon dioxide emissions.

Nasheed had already announced plans for a

fund to buy a new home-land for his people if the 1192

low-lying coral islands are sub-merged. He has promised to make the

Maldives, with a population of 350,000, the world’s fi rst carbon-neutral nation within a decade.

President Obama’s visit to China in mid-November will not lead to an agreement on countering global warming, according to Todd Stern, the US special envoy for climate change. However, he says Obama will work with Chinese President Hu Jintao toward facilitating an agreement at the interna-tional meeting.

“It’s never been an eff ort on our side to work toward a separate deal, but we’re going

to be trying to make as much progress as possible,” Stern says. “We’re pushing them and they’re pushing us.”

“All of us have to take responsibility for our own countries and for the sake of all mankind. Th is is not a matter of saying, only if other countries take certain measures will we take certain measures. It is not that kind of future,” Xie Zhenhua, China’s top climate envoy, told reporters.

NO US-CHINA PACT

20% in 201130% in 2020

The islands are only an average of

above sea level2.1 meters

UPFRONT.indd 19UPFRONT.indd 19 5/11/09 16:38:045/11/09 16:38:04

UPFRONT20

Th e Desertec Industrial Initiative, a $400 billion plan to provide Europe with solar power from the Sahara, has reached fur-ther development following the formation of 12 companies to carry out the work. Th e German-led, project brings together major players in the industry such as Siemens, E.ON and Deutsche Bank.

Th e initiative has set a target to provide 15 percent of Europe’s electricity by 2015, with solar power being generated as soon as 2015. Th e technology being used is not inno-vative, it is already being used in the deserts of California and Nevada, but it is receiving huge media attention for the scale of the proj-ect, which also has plans to connect North Africa to this European grid.

Th e French government is becoming doubt-ful as to the purchase of half of US nuclear energy company Constellation. State-con-trolled French operator EDF announced its bid for Constellation last December, but it has since emerged that the government is keen to continue its presence in Europe following its buyout of British Energy in late 2008. Th e Financial Times reported the government’s change in enthusiasm for the American takeover, stating that regulatory diffi culties in the US have delayed the $4.5 billion deal and quotes a senior offi cial questioning EDF’s progression with Constellation.

However, a French government offi cial who stated that a deal between the two has been authorized denied the report.

London’s mayor, Boris Johnson, is consider-ing a new project to save at least $147 million in refuse collection. Following a report by the London assembly, it emerged that the waste generated by Londoners could be used to gen-erate enough electricity to power up to two million homes and provide heat for 625,000 houses. Th e amount of money being spent on sending waste to landfi ll is increasing follow-ing rising taxes.

Currently, more than half of the capital’s waste ends up in landfi ll, with only 22 percent of it being recycled; non-recyclable rubbish, such as food, could be converted into energy. Creating gas from the rubbish could be used for heating or for generating electricity and could cut London’s CO2 emissions by 1.2 mil-lion tones.

INTERNATIONAL NEWS

SAHARA SOLAR NUCLEAR TAKEOVER RUBBISH RE-USE

UPFRONT.indd 20UPFRONT.indd 20 5/11/09 16:40:195/11/09 16:40:19

UPFRONT21INTERNATIONAL NEWS

COAL GASIFICATION TOKYO MOTOR SHOW SOLAR FOCUS

In a bid to develop its clean coal technolo-gies, India is undertaking a collaborative eff ort with Coal India Ltd (CIL) and receiving support from its peers. CIL and GAIL (India) Ltd are working together to develop a surface coal gasifi cation project at Talcher coalfi eld in Orissa for the production of ammonium nitrate and urea.

GAIL had organized a study by Udhe India to examine the potential of the project. It was estimated that the project would con-sume 5000 tons of coal a day to produce 7.76 mscmd of synthesis gas (equivalent to 3000 tons a day of ammonia) to produce 3500 tons of urea a day.

CIL is also working with ONGC for un-derground coal gasifi cation projects.

Th e two are working on the development, operation and R&D activities. Th e pilot site at Vastan, Gujarat, has been obtained and its design has been fi rmed up, and the project is expected to commence production next year.

Th e 41st showcasing of innovative concepts and new production cars from the world’s major auto manufacturers took place in Tokyo between October 21-November 4. Th e eff ects of the recession were present, with only Lotus, Caterham and Alpina making the journey from Europe. Most notable was the innovative yet cautious approach to plug-in hybrid vehicles.

Toyota displayed its Plug-In Prius Hybrid, run on lithium-ion battery technol-ogy and emitting just 42g/km of CO2 or less. However, remaining cautious of public opin-ion, the vehicle is due to go on a limited trial next year.

Renault, also exhibiting at the show, has stated that 20 percent of its entire production will be battery electric vehicles by 2012.

Th e Japanese government has launched a new program to encourage the purchase of surplus solar electricity. Power companies will now be purchasing the surplus electric-ity produced by solar power generations in homes, schools and hospitals at a much higher rate.

Starting in April, the utility companies will collect a monthly sub-charge from every household and organization to cover the rise in costs. However, critics are doubtful about this move and believe it will only weaken cus-tomer sentiment.

Th is is the latest of Japan’s attempts to make photovoltaic generation, which pro-duces less carbon emissions than fossil fuels, is popular and demonstrates the country’s commitment to fi ghting global warming.

UPFRONT.indd 21UPFRONT.indd 21 5/11/09 16:40:355/11/09 16:40:35

UPFRONT22

KEVIN MCCULLOUGH, CHIEF OPERATING OFFICER, RWE ENERGY

Being a very carbon-heavy industry and a very carbon-heavy player within the energy sector, arguably we needed to do something more fundamental around weaning ourselves away from the carbon-based technologies.

The winners going forward in any business sector are always those that can be innova-tive and move quickly, and because we were a little later than most of our competitors in getting into large volume renewables, we had to make some fairly bold moves fairly quickly.

We live in a world at the moment where we take poverty for granted and we have to do something about that. Th e vast majority only minimally change their lifestyles towards energy, and there is no real solution going for-ward that involves low carbon and low price, and that’s the reality.

Onshore wind is now beginning to find parity with gas turbine plants. Off shore wind

is in a diff erent league. It’s at least 50 percent more expensive than onshore wind in pure capital of cost because of the amount of in-frastructure that sits beneath the waves.

We see real strength as a portfolio as opposed to a single party player. I don’t believe that with the technology available today we will be 100 percent renewable. Th ere is certainly the potential, but probably only on a project by project basis.

You’re already seeing, on a larger scale, utili-ties using their carbon footprint or their sus-tainability impact very cleverly to competitive advantage. Th ere’s no reason that I can fore-see why that wouldn’t be just as practically

applied in a smaller environment, ultimately to a very small scale.

Nuclear was born out of the Cold War. It was built eff ectively for weapons grade plu-

tonium with heat as a huge byproduct that some clever people thought we can build energy from, and of course more clever uses of that nuclear technology became civil nuclear reactors.

Consumers need to be continually educated, but so do the utilities that serve them because our consumers are our absolute lifeblood, and you ignore your consumer at your peril. We’re living in an age now where consumers has never been as informed as they are today.

“Our consumers are our absolute lifeblood, and you ignore your consumer at your peril”

UPFRONT.indd 22UPFRONT.indd 22 5/11/09 16:40:415/11/09 16:40:41

UPFRONT23

FROM THE VAULT

CLEAN VEHICLES

In the Q1 2009 issue of Power & Energy, Ralph Izzo, CEO of Public

Service Enterprise Group, examines the diffi cult state of the US utility

industry in relation to the heightened federal focus on reducing green-

house gas emissions and the recent global fi nancial crisis.

Go to www.nextgenpe.com, click on ‘Previous issues’ in the left column,

choose ‘Issue 6, February 2009’ and scroll down to ‘Cover stories’ to

read about PSEG Global’s strategic efforts to face the enormous chal-

lenges created by climate change.

BIOFUEL COULD HARM WATER

A new study by researchers at Rice University in Houston, Texas has found that expanded production of crops to produce biofuels could damage water resources. Th e research suggests that policy makers should take into account what they call the “water footprint” when encouraging biofuel development.

Th e study, called ‘Th e Water Footprint of Biofuels: A Drink or Drive Issue?’, suggests that by using too much water to produce fuel, we might end up with not enough water to drink or to grow food.

According to the lead author of the study, Pedro Alvarez, Rice University Professor of Civil and Environmental Engineering, the water footprint consists of two elements. “Water shortages caused by a signifi cant increase in fuel crop irrigation, and increased water pollution from related agro-chemical drainage and increased erosion and so on. Th e two impacts we refer to as the ‘water footprint,’” he says.

Alvarez says there are good reasons to continue programs to produce biofuels, such as reducing the need for imported oil and diversifying our sources of energy. But he says policymakers should provide incentives to producers to use crops that use less water and have less impact on the environment in the form of runoff of pesticides, fertilizers and other chemicals.

NEW SOLAR RESOURCES

Energy Secretary Steven Chu announced in early November that the Department of Energy is providing up to $5.5 million in funding from the American Recovery and Reinvestment Act to support the X PRIZE Foundation’s work to inspire a new genera-tion of energy effi cient vehicles.

As part of the Automotive X PRIZE competition, teams design innovative, commercially viable, high-effi ciency vehicles that will help break the dependence on oil and stem the eff ects of climate change. Th e funding will provide technical assistance and expand national education and outreach eff orts for the competition. Th e award also supports President Obama’s Strat-egy for American Innovation, which calls on federal agencies to increase their use of prizes as a tool for promoting technological advances.

To help utilities rise to the chal-lenge of adopting solar power at a large scale, the Solar Electric Power Association (SEPA) un-veiled a new web portal and da-tabase last week at Solar Power International. SEPA says that its new site lets utilities explore op-tions, fi nd resources and think strategically about how their utility peers across the country are moving forward.

Th e site aims to help utilities make business decisions about

solar power by providing “intel-ligent navigation” of industry reports, events, online tools and market data that can be fi ltered by technology, application and employee type, SEPA said. Highlights include the Solar Toolkit, a one-stop window into the site’s technical content.

Th e site also off ers data and maps on the largest solar projects, as well as streaming online webinars from past SEPA events.

Source: voanews.com

Source: renewableenergyworld.com

UPFRONT.indd 23UPFRONT.indd 23 5/11/09 16:40:475/11/09 16:40:47

UPFRONT24

BACK TO THE LAB

The US Department of Energy researches and develops its national science interests through a system of facilities and laboratories, which it oversees. The National Laboratories and Technology Centers are federally funded but administered and staffed by private corporations and universities. In the second of an ongoing series, Power & Energy examines the 17 national laboratories and the varying ways in which they impact the country’s energy usage.

PROJECT FOCUS

A SCIENCE, TECHNOLOGY AND ENERGY laboratory, the main focus of the National Energy Technology Lab is to advance the national, economic and energy security of the US, which it does through onsite and contracted research.

The laboratory develops technologies to resolve the constraints imposed on decreasing fossil fuels, and ensures responsible supplies of energy for the nation’s growing economy. It is the only lab devoted to research into fossil energy technology and incorporates a number of national goals, such as carbon sequestration and producing hydrogen fuel from coal. It currently employs more than 1200 people at each of the fi ve laboratory sites.

NATIONAL ENERGY TECHNOLOGY LAB

LOCATED IN LONG ISLAND, New York, Brookhaven was established in 1947 and originally owned by the Atomic Energy Commission. First operated as a nuclear research facility, Brookhaven’s activities have vastly expanded to include environmental and energy research, neurosciences and medical imaging, and structural biology.

The lab’s motto is ‘passion for discovery’, and it has six Nobel Prizes to back up its promise. Co-located within the laboratory is the uptown New York forecast offi ce of the National Weather Service.

BROOKHAVEN NATIONAL LAB

UPFRONT.indd 24UPFRONT.indd 24 5/11/09 16:43:035/11/09 16:43:03

UPFRONT25PROJECT FOCUS

OFFICIALLY KNOWN as the Thomas Jefferson National Accelerator Facility, it was founded in 1984 and is operated by Jefferson Science Associates, LLC. The lab’s main research facility is the Continuous Electron Beam Accelerator Facility (CEBAF) accelerator, and the nuclear physics program is carried out at three end stations, with plans to introduce a fourth. There are plans to double the electron beam to 12 GeV.

The Jefferson Lab also boasts the world’s most powerful free electron laser, at more than 14 kW.

JEFFERSON NATIONAL ACCELERATOR LAB

SITUATED AT THE SAVANNAH River site near Aiken, South Carolina, the laboratory carries out research and development incorporating environmental remediation, technologies for the hydrogen economy, handling of hazardous materials, and technologies for the prevention of nuclear proliferation.

The labs focuses on, and has vast amount of experience in, the domain of nuclear waste and hydrogen storage, following its initial creation to support the production of tritium and plutonium during the Cold War.

SAVANNAH RIVER NATIONAL LAB

SPECIFIED FOR RESEARCH regarding plasma physics and nuclear fusion science, the lab is located in New Jersey. It originated out of the Cold War project Matterhorn, a project to control thermonuclear reactions, and was renamed the Princeton Plasma Physics Lab following the project’s declassifi cation in 1961.

Its primary goal is to develop fusion as an energy source and its current major research projects and experiments include a Tokamak Fusion Test Reactor and the National Spherical Torus Experiment.

PRINCETON PLASMA PHYSICS LAB

UPFRONT.indd 25UPFRONT.indd 25 5/11/09 16:43:045/11/09 16:43:04

UPFRONT26

SMART GRID PROGRAM

OG&E has entered into agreements with General Electric Energy (GE) and Silver Spring Networks to handle key aspects of its Positive Energy Smart Grid Program to begin in Norman, Oklahoma next year.

As part of the Norman deployment, 2000 to 3000 customers will be recruited

to receive information in almost real time regarding the price of electricity by time of day and the amount being used.

Th e smart grid pro-gram will provide customers with more information to help manage their energy use and save money, without compromis-ing their lifestyles. It also will help OG&E maintain reasonable electricity rates and continue reliable delivery of electricity to its customers, the utility said.

GE will provide Norman with 42,000 smart meters that will measure electricity use in the home or business and transmit the information to OG&E for billing and service monitoring. Th e information will be communicated via Silver Spring Net-works’ Smart Energy Network, a secure, IP-based network.

FAST FACT

If

smart meters are installed over the next 10 years, they could produce a quadrillion bytes of information

140 million

UTILITY BALANCE SHEETS STRAINED

US ENERGY CONSUMPTION (QUADRILLION BTU)

Share values among America’s utility, gas and power companies have outperformed the broader market since the fi nancial crisis began last year. Maintaining this perfor-mance, however, might become more dif-fi cult in the months ahead, according to a report published in the September issue of Public Utilities Fortnightly magazine.

Th e fi ft h-annual Fortnightly 40 study, sponsored by Accen-ture, ranked the four-year shareholder value perfor-mance of US investor-owned utilities (IOUs) and other companies active in electric power and gas industries. Th e C Th ree Group of Atlanta, which along with Public Utilities Fortnightly devel-oped the F40 fi nancial model, analyzed the annual reports of 85 companies to compare a series of shareholder-value metrics – such as profi t margin, dividend yield, return on equity (ROE), return on assets (ROA) and sustainable growth.

Companies leading the F40 ranking

this year included DPL, Energen and PPL. Ranked among the top 40 for the fi rst time was NRG (32), and returning to the rank-ing aft er a year’s absence were Mirant (21) and AES (37) – three companies with heavy exposure in wholesale power markets. Con-versely, Alliant and Northwest Natural Gas

slipped to the bottom of the F40 aft er ranking in the high 20s last

year.Th e F40 metrics – com-

bined with supplementary 2009 data – showed the in-dustry remains fi nancially

robust despite a substantial decline in stock prices. Cap-ex

spending among the Fortnightly 40 companies grew by nearly 30 percent in 2008, topping $49 billion, and the entire industry’s cap-ex increased 17 percent to nearly $94 billion. At the same time, equity returns among the top 40 companies de-clined only slightly, from 15.4 percent in FY2007 to 14.6 percent in 2008.

Source: www.fortnightly.com

ENERGY SOURCE 2008

FOSS

IL FU

ELS

- 8

3.43

6

COAL

- 2

2.42

1

COAL

CO

KE N

ET IM

PORT

S -

0.0

40

NAT

URAL

GAS

- 2

3.83

8

PETR

OLE

UM -

37.

137

ELEC

TRIC

ITY

NET

IMPO

RTS

- 0

.113

NUC

LEAR

ELE

CTRI

C PO

WER

- 8

.455

REN

EWAB

LE E

NER

GY -

7.3

01

BIO

MAS

S -

3.88

4

BIO

FUEL

S -

1.41

3

Cap-ex spending grew by nearly

in 200830%

Source: renewableenergyworld.com

UPFRONT.indd 26UPFRONT.indd 26 6/11/09 09:22:466/11/09 09:22:46

TeamQuest.indd 1TeamQuest.indd 1 3/11/09 15:03:433/11/09 15:03:43

UPFRONT28

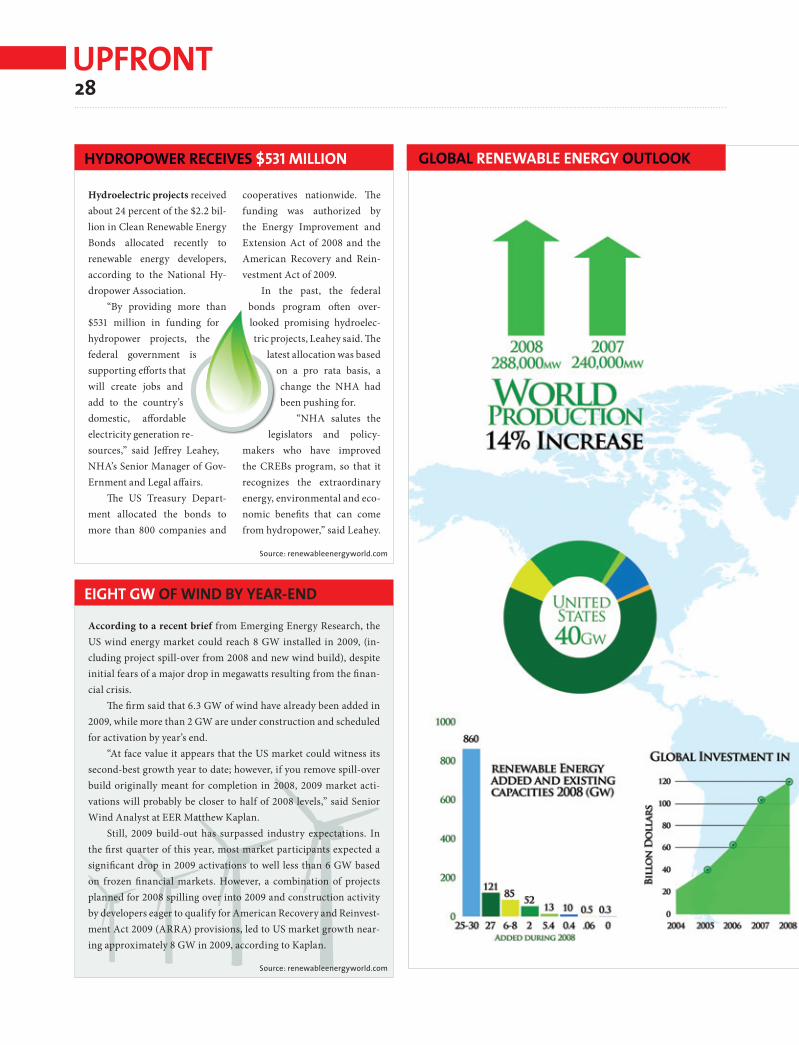

GLOBAL RENEWABLE ENERGY OUTLOOKHYDROPOWER RECEIVES $531 MILLION

Hydroelectric projects received about 24 percent of the $2.2 bil-lion in Clean Renewable Energy Bonds allocated recently to renewable energy developers, according to the National Hy-dropower Association.

“By providing more than $531 million in funding for hydropower projects, the federal government is supporting eff orts that will create jobs and add to the country’s domestic, aff ordable electricity generation re-sources,” said Jeff rey Leahey, NHA’s Senior Manager of Gov-Ernment and Legal aff airs.

Th e US Treasury Depart-ment allocated the bonds to more than 800 companies and

cooperatives nationwide. Th e funding was authorized by the Energy Improvement and Extension Act of 2008 and the American Recovery and Rein-vestment Act of 2009.

In the past, the federal bonds program oft en over-looked promising hydroelec-tric projects, Leahey said. Th e

latest allocation was based on a pro rata basis, a change the NHA had been pushing for.

“NHA salutes the legislators and policy-

makers who have improved the CREBs program, so that it recognizes the extraordinary energy, environmental and eco-nomic benefi ts that can come from hydropower,” said Leahey.

EIGHT GW OF WIND BY YEAR-END

Source: renewableenergyworld.com

According to a recent brief from Emerging Energy Research, the US wind energy market could reach 8 GW installed in 2009, (in-cluding project spill-over from 2008 and new wind build), despite initial fears of a major drop in megawatts resulting from the fi nan-cial crisis.

Th e fi rm said that 6.3 GW of wind have already been added in 2009, while more than 2 GW are under construction and scheduled for activation by year’s end.

“At face value it appears that the US market could witness its second-best growth year to date; however, if you remove spill-over build originally meant for completion in 2008, 2009 market acti-vations will probably be closer to half of 2008 levels,” said Senior Wind Analyst at EER Matthew Kaplan.

Still, 2009 build-out has surpassed industry expectations. In the fi rst quarter of this year, most market participants expected a signifi cant drop in 2009 activations to well less than 6 GW based on frozen fi nancial markets. However, a combination of projects planned for 2008 spilling over into 2009 and construction activity by developers eager to qualify for American Recovery and Reinvest-ment Act 2009 (ARRA) provisions, led to US market growth near-ing approximately 8 GW in 2009, according to Kaplan.

is

-

lat

leg

Source: renewableenergyworld.com

UPFRONT.indd 28UPFRONT.indd 28 5/11/09 16:52:365/11/09 16:52:36

UPFRONT29

UPFRONT.indd 29UPFRONT.indd 29 5/11/09 16:46:015/11/09 16:46:01

UPFRONT30

Heidrick & Struggles 114

Idaho National Laboratory 32

Itron 2, 66

Kore Telematics 48, 49

Land Agent Services LLC 101

meettheboss.com 125

Motorola 66, 72

MSE Power Systems 4, 116

National Energy Technology Laboratory 24

National Institute of Standards and

Technology 76

Nuclear Energy Institute 32

Oak Ridge National Laboratory 44

Oliver Wyman 44

Ounce Labs, an IBM company 66, 68, OBC

PowerMand 53

Princeton Plasma Physics Laboratory 24

PSE&G 122

PV Powered, Inc IFC, 97

RAM Mounting Systems 10, 60, 61

S&C Electric Company 104

Savannah River National Laboratory 24

Sensus 54

Sierra Wireless 66, 70

COMPANY INDEX Q4 2009 Companies in this issue are indexed to the fi rst page of the article in which each is mentioned.

Alstom 38

American Council on

Renewable Energy 108

American Electric Power 32, 38, 84

American Wind Energy Association 80, 110

AT&T 6, 66

Autodesk 121

Baltimore Gas and Electric 50

BP Solar 8

Brookhaven National Laboratory 24

California Energy Commission 110

CH2M HILL 37, 119

Cinterion 64

Conergy 93

Current 31

Duff & Phelps 102

Electricity Storage Association 104

Energy Storage and Power LLC 107

Enfora 78, 79

European Photovoltaic Industry

Association 80

European Renewable Energy Council 80

Exelon 32

Get Wireless 59

Solar Electric Power Association 90

Solar Energy Industries

Association 98, 110

SolFocus 88, 89, IBC

Southern California Edison 56

Southern Company 94

SunGard 15

Teamquest 27

TELUS Business Solutions 12, 66, 75

Thomas Jefferson National

Accelerator Facility 24

University of Massachusetts 80

DOE AWARDS FUNDING FOR GEOTHERMAL ENERGY

Energy Secretary Steven Chu has an-nounced up to US $338 million in Re-covery Act funding for the exploration and development of new geothermal fi elds and research into advanced geo-thermal technologies.

Th ese grants will support 123 projects in 39 states, with recipients including private industry, academic institutions, tribal entities, local governments, and the DOE’s national laboratories. Th e grants will be matched more than one-for-one with an additional $353 million in private and non-federal cost-share funds.

Th e grants are for identifying and developing new geothermal fi elds and reducing the upfront risk associ-ated with geothermal development through innovative exploration and drilling projects and data development

and collection. In addition, the grants will support the deploy-ment and creative fi nancing approaches for ground source heat pump demonstration projects across the country.

“Th e United States is blessed with vast geothermal energy re-sources, which hold enormous potential to heat our homes and power our economy,” said Secretary Chu. “Th ese investments in America’s technological innovation will allow us to capture more of this clean, carbon free energy at a lower cost than ever before. We will create thousands of jobs, boost our economy and help to jumpstart the geothermal industry across the United States.”

Source: renewableenergyworld.com

CLIMATE SUPPORT

More than a dozen leading US corporations, includ-ing Public Service Enter-prise Group (PSEG), DB Climate Change Advisors (Deutsche Bank Group), Gap Inc. and National Grid, have announced the launch of a new initiative to support Congressional action on clean energy and climate change legislation.

Th e goal of the new group, called American Businesses for Clean Energy (ABCE), is to off er a platform for leading US businesses to express their support for meaningful and eff ective legislation that will drive clean tech-nology innovation, create jobs and address the threat of global climate change.

ABCE’s offi cial mes-sage is: “We are businesses from a broad cross-section of American industry that support Congressional action to enact clean energy and climate legislation that will signifi cantly reduce greenhouse gas emissions. Now is the time to act.”

Some of the fi rst signa-tories to the ABCE pledge of support include Aspen Skiing Company, Avista, Calpine Corporation, Con-servation Services Group, DB Climate Change Ad-visors (Deutsche Bank Group), FPL Group, Gap Inc., National Grid, New York Power Author-ity, PNM Resources, and Public Service Enterprise Group.

UPFRONT.indd 30UPFRONT.indd 30 5/11/09 16:46:395/11/09 16:46:39

CURRENT OpenGrid™ — Delivering Real Smart Grid Results Today

SYSTEM OPTIMIZATION

DISTRIBUTION MANAGEMENT

SENSING & COMMUNICATIONS

OPENGRID

www.currentgroup.com 866.427.0602

Current.indd 1Current.indd 1 3/11/09 15:01:503/11/09 15:01:50

32 www.nextgenpe.com

COVER STORY

Now you see it...

Cover Story:4August 5/11/09 15:19 Page 32

www.nextgenpe.com 33

you don’tHe hails nuclear as the answer toAmerica’s carbon-emitting problemand the future of energy self-sufficiency, but without thelegislation to back up his rhetoric, arePresident Obama’s nuclear policiesnothing more than an act of illusion?

By Natalie Brandweiner

now

In recent years, nuclear has been dressed up and re-branded asthe savior of the global energy crisis. Governments are finallytaking notice of diminishing energy resources and beginning tofeel the power of lobbying efforts calling for a reduction in car-bon emissions. Public opinion is no longer as drowsy as it pre-viously has been – the average energy consumer is now wakingup to the effects of individual usage on global warming. Being‘green’ is the new scene.

The previous stigmas of safety and reliability have been washed over andnuclear has re-emerged as America’s answer to the fuel crisis. PresidentObama is carrying the torch for its revival and canvassing in its support, withEnergy Secretary Steven Chu in tow, but the accumulation of this into policynever seems to appear. There is still so much to see of Obama’s tenure, but sofar his legislation for nuclear’s dominance is nowhere to be seen. In fact, nu-clear features as a side note in many of his energy speeches. Promises of fund-ing and plant construction continue to be made, but it seems that the USgovernment is shying away from actual legislation.

Public opinionGlobal opinion has changed. The UN Climate Change Conference

scheduled for Copenhagen in December 2009 is set to reorganize the frame-work for climate change mitigation and millions across the globe will bewatching the outcome. The Nuclear Energy Institute (NEI) is regarded as thebiggest nuclear lobbying group in the US: according to its website it “developspolicy on key legislative and regulatory issues affecting the industry.” The NEIboard represents 27 nuclear utilities, plant designers and engineering firms inefforts to expand the nuclear industry, and for the entirety of 2007 spent $1.3million lobbying the US federal government. It has targeted this towards build-ing public support, running ads to highlight the nuclear benefits.

Cover Story:4August 5/11/09 15:19 Page 33

34 www.nextgenpe.com

Bush and facing criticisms for favoring Texan companies and amounting tonothing more than a broad collection of subsidies for US energy companies,the legislation highlights nuclear as an “innovative technology” and autho-rizes cost-overrun support of up to $2 billion for six new power plants. Obamavoted ‘yes’ on the bill and carried through his support into his own presiden-cy, including nuclear as part of his energy policy. During his acceptancespeech he announced, “As President, I will tap our natural gas reserves, investin clean coal technology and find ways to safely harness nuclear power.”However, implementing his promises into policy is quite a different story.

The Obama Administration has ramped up the move towards renew-ables, but this alone cannot produce the energy that the country needs. A re-cent study by the Nature Conservancy, a conservation organization of morethan one million members, shows that new energy production, specificallybiofuels and wind power, is likely to consume a landmass larger thanNebraska. Nuclear sets itself apart as being a producer of low-carbon elec-tricity without excessivie intringement upon the country’s landscape, but thefederal policy to support engagement with nuclear never materializes.

The Office of Nuclear Energy offers two program goals for nuclear ad-vancement: the development of new nuclear generation technologies and the

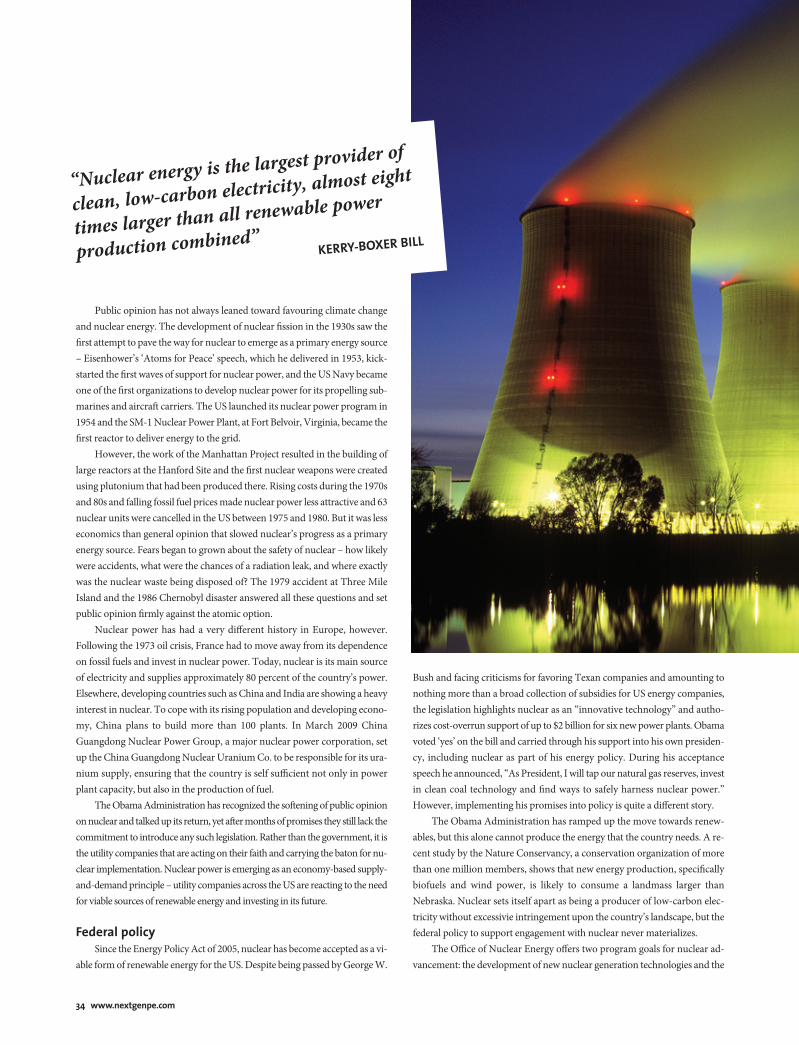

“Nuclear energy is the largest provider of

clean, low-carbon electricity, almost eight

times larger than all renewable power

production combined”KERRY-BOXER BILL

Public opinion has not always leaned toward favouring climate changeand nuclear energy. The development of nuclear fission in the 1930s saw thefirst attempt to pave the way for nuclear to emerge as a primary energy source– Eisenhower’s ‘Atoms for Peace’ speech, which he delivered in 1953, kick-started the first waves of support for nuclear power, and the US Navy becameone of the first organizations to develop nuclear power for its propelling sub-marines and aircraft carriers. The US launched its nuclear power program in1954 and the SM-1 Nuclear Power Plant, at Fort Belvoir, Virginia, became thefirst reactor to deliver energy to the grid.

However, the work of the Manhattan Project resulted in the building oflarge reactors at the Hanford Site and the first nuclear weapons were createdusing plutonium that had been produced there. Rising costs during the 1970sand 80s and falling fossil fuel prices made nuclear power less attractive and 63nuclear units were cancelled in the US between 1975 and 1980. But it was lesseconomics than general opinion that slowed nuclear’s progress as a primaryenergy source. Fears began to grown about the safety of nuclear – how likelywere accidents, what were the chances of a radiation leak, and where exactlywas the nuclear waste being disposed of? The 1979 accident at Three MileIsland and the 1986 Chernobyl disaster answered all these questions and setpublic opinion firmly against the atomic option.

Nuclear power has had a very different history in Europe, however.Following the 1973 oil crisis, France had to move away from its dependenceon fossil fuels and invest in nuclear power. Today, nuclear is its main sourceof electricity and supplies approximately 80 percent of the country’s power.Elsewhere, developing countries such as China and India are showing a heavyinterest in nuclear. To cope with its rising population and developing econo-my, China plans to build more than 100 plants. In March 2009 ChinaGuangdong Nuclear Power Group, a major nuclear power corporation, setup the China Guangdong Nuclear Uranium Co. to be responsible for its ura-nium supply, ensuring that the country is self sufficient not only in powerplant capacity, but also in the production of fuel.

The Obama Administration has recognized the softening of public opinionon nuclear and talked up its return, yet after months of promises they still lack thecommitment to introduce any such legislation. Rather than the government, it isthe utility companies that are acting on their faith and carrying the baton for nu-clear implementation. Nuclear power is emerging as an economy-based supply-and-demand principle – utility companies across the US are reacting to the needfor viable sources of renewable energy and investing in its future.

Federal policySince the Energy Policy Act of 2005, nuclear has become accepted as a vi-

able form of renewable energy for the US. Despite being passed by George W.

Cover Story:4August 6/11/09 09:03 Page 34

www.nextgenpe.com 35

maintenance, enhancement and safeguarding of America’s nuclear infra-structure. Its first goal, as stated on the Department of Energy’s website, is todevelop technologies that “foster the diversity of the domestic energy supplythrough public-private partnerships that are aimed in the near-term at the de-ployment of advanced, proliferation-resistant light water reactor and fuelcycle technologies and in the longer-term at the development and deploymentof next-generation advanced reactors and fuel cycles.”

On June 16 this year, Steven Chu followed up on the DOE’s emphasis of de-velopment, announcing funding of $9 million for nuclear energy university pro-gram awards. The Nuclear Energy Universities Program will provide scholarshipsand fellowships to 86 US nuclear science and engineering students. The fundingis being made available to support the country’s energy research infrastructure,but what about the powering of the infrastructure itself?

On September 18, Chu flew the flag for nuclear once again and an-nounced that $40 million in funding would be made available to support de-sign and planning for the Next Generation Nuclear Plant (NGNP): plantswhich will use high temperature, gas-cooled reactor technologies to integratemultiple industrial applications in one plant or facility, such as generatingelectricity while refining petroleum.

Kerry-Boxer BillClaimed by John Kerry to be a“pollution reduction bill”, the issueof cap and trade is avoided;instead the bill looks at nuclearworker training, federalprocurement of water-efficientproducts, green jobs, climatechange adaptation programs andflood control. The bill emphasizesthe need for the Secretary ofHealth and Human Services tocreate a strategic plan for healthissues caused by climate change– waterborne diseases, tropicaldiseases, pulmonary effects,cardiovascular effects, air pollutionhealth effects, hazardous algalblooms, mental and behavioralhealth impacts of climate change,the health of refugees, theimplications for communitiesvulnerable to climate change, andlocal and community-based healthinterventions.

“Support for new developments in nuclear technologies will be critical tomeeting our energy, climate and security goals for years to come,” says Chu.“Next Generation Nuclear Plants hold the promise of safe, cost-effective, zero-emissions energy for major US industries that are some of the largest energyconsumers in the country.”

The NGNP project is expected to be comprised of two phases, with theconstruction of a demonstration plant expected in 2012. Applications are to bemade to the DOE, with two awards being announced in February 2010 and bothsupporting a unique reactor concept. This follows an already long-standingagreement for the involvement of Idaho National Laboratory to build a full-scale,300MW prototype. However, before anticipation runs too high, is worth notingthat the construction of the plant is not planned to begin until 2016.

The Nuclear Regulatory Commission (NRC) published an NGNP li-censing strategy in 2009 laying out a process, but includes no actual details re-garding design for the reactors, and it is expected that it will be at least 2014before the NGNP is ready with a reactor design for the NRC review. TheObama Administration hails itself as bringing the next generation of nuclearpower, promising research funds and new developments, but when strippedback to the finer details, the likelihood of any progress being made during thecurrent president’s tenure seems exceptionally small.

It is not only the construction of nuclear power plants that the govern-ment is failing in its support. The catastrophic case of the Yucca MountainRepository was also a stop-start, before being completely rejected by theObama Administration. Proposed as a storage facility for nuclear fuel andother radioactive waste, it was approved in 2002 under the BushAdministration but all funding was stopped earlier this year. Chu stated thatit is “no longer an option for storing nuclear waste,” prompting concerns overplans for nuclear waste disposal.

Obama’s team do not want to lose face by ignoring public interest in nu-clear, but are reluctant to implement a potentially damaging policy. His nu-clear policy is proving to be nothing more than a brilliantly streamlined PRspin: extolling the benefits of nuclear but without feeling the effects shouldanything go wrong. Nuclear has certainly moved away from its previous stig-mas, but not completely. For many it still remains a controversial policy.

John Keeley at the NEI confirms this viewpoint. He believes that al-though there may be a lot happening behind the scenes, it is unlikely wewill see nuclear policy made into legislation any time soon. He notes thecurrent federal focus on healthcare reform and the need for the ObamaAdministration to heavily hone in on the criticisms they are currently fac-ing. “Healthcare is the driver now,” says Keeley. He also notes the Senateelections that are due next year – in times of electoral campaigns it is rareto see controversial legislation introduced for fear of political fallout.

Lack of supportKeeley also points to the shortfalls of support for nuclear energy in the

Kerry-Boxer bill. The only promise Barbara Boxer seems to have kept in an-nouncing new legislation on nuclear power is the announcement having ‘nu-clear’ in the title. The bill actually does very little to address nuclear policy, optingto include it as a side note on the end of stipulations for natural gas, coal and re-newable energy.

The report cites nuclear’s pivotal role, yet fails to make any serious com-mitments for the future: “Nuclear energy is the largest provider of clean, low-carbon electricity, almost eight times larger than all renewable power

Cover Story:4August 5/11/09 15:19 Page 35

production combined, excluding hydroelectric power.” The bill includes a gener-ic goal to expand the nuclear energy workforce and concentrate more researchinto nuclear safety and disposal, but none of this is partnered with a firm set ofallocated funds. Chu has sided with this argument and stated that in response hewill push for billions of dollars to secure funds to cut greenhouse gas emissions.

The response to the bill has been overwhelmingly critical. The bill cameabout as a result of the lobbying done by conservationist Lamar Alexander,who spoke on the importance of nuclear, not just for a greener future but alsoto secure more votes for the energy and climate bill. Fellow Republican JohnMcCain also staunchly spoke out against the bill, saying, “I’m not going to bepart of any agreement that I know is not going to succeed in reducing green-house gas emissions, and that means it has to be nuclear power. We need tobuild 100 nuclear power plants in the next 20 years. We have to, otherwisewe’re not going to reduce greenhouse gas emissions.”

The principle of outside looking in springs to mind, however. WouldRepublicans introduce such a controversial policy if they were in power?Obama’s Administration is quick to note the environmental benefits of nu-clear but slow to implement it because of the fear of failure. The politics of in-troducing nuclear as a primary energy source continue to get in the way – thecontroversy surrounding the safety of it, the problems with storage and a pos-sible electoral defeat should anything go wrong.

Facing increasing criticism for his lack of commitment, Obama may nowhave given up on glossing over the shortcomings of his nuclear legislation.During the UN climate summit on September 22 he failed to mention nuclearenergy even once, an omission that was made more apparent by the Chinesepresident’s discussion of nuclear as a primary energy source. HuJintao cited statistics and targets for his energy plan, committing tobuilding 132 GW of new nuclear plants.

Utility policyInstead of instigating nuclear legislation, the current adminis-

tration seems to be warming the waters for the utilities to dive inand make the first move, be it successful or not. Its vague pledgesfor government funding for nuclear programs have got the utili-ties fired up and competing for the prize, each attempting to be atthe cutting edge of nuclear technology.

One utility that has long established its support for nuclear technology isExelon. It has the largest nuclear fleet in the US with 17 generating units, whichproduced a record 132.3 million net megawatt-hours of electricity in 2007. Thecompany has done away with safety fears and gained public confidence in its op-erations with its unbeatable statistics – during the same year, as production in-creased, the fleet recorded its lowest industry safety accident rate.

In a previous interview with Power & Energy, Helen Howes, Exelon’s VPof Environment, Health and Safety, said she believed the growing public de-

mand to increase the supply of nuclear energy is proof enough thatconsumers no longer have the critical attitude towards nuclear thatthey once did.

“What we’re seeing now is an evolution of thinking regardingthe value of nuclear as a contributor to the solution,” she said.There are still a number of those who are anti-nuclear, that’s in-evitable, but the value of nuclear as a climate change strategy is

being more and more acknowledged. It’s certainly not done so as the only op-tion, but it’s raised its status to be one of a number of options on the table.”

American Electric Power (AEP) is another utility that is pushing nuclear.With a majority of its fleet being traditional coal-fired generation, the com-pany understands the need to expand its resource mix and create a balancedportfolio to suit both the climate and changing consumer needs. Nick Akins,EVP of Generation, explains that nuclear is a huge focus for AEP, who are ex-ploring other forms of base load technology. “It’s a priority for us to be ableto uprate our nuclear station: we have plans on uprating nuclear by 400- to500-megawatts and that is a relatively small cost, at least a lesser cost than anew coal-fired station,” he says.

However, Exelon and AEP are two of America’s largest utility companies,with reported revenues in 2008 of $18.9 million and $13.3 million respectively.The average cost of building a new nuclear power plant is approximately $7 bil-lion, which is virtually unachievable without the help of government funding;maintaining the plant also brings high costs.

The only recent nuclear funding other than Chu’s long-term applica-tions for $40 million has been for the Idaho National Laboratory.Republican Mike Simpson, whose district stretches across Idaho and in-cludes the lab, recently announced an increase of $33 million in fundingfor research, equipment purchases and the advanced test reactor’s oper-ation as a national scientific user facility.

President Obama’s energy policies contain promising nods to anAmerican future where nuclear plays an important role in a dramaticallyreduced carbon emissions rate, but none of this is backed up by legisla-tion. As the NEI’s John Keeley suggests, while there may be much goingon behind the scenes, nuclear’s future, right now, does not seem concreteor certain.

This lack of federal commitment raises questions of government uncer-tainty and doubt. Perhaps they are concentrating on changing attitudes ofanti-campaigners to avoid a bombardment of attacks and criticisms shouldanything go wrong, or perhaps they are sitting back, waiting for a Republicangovernment to storm full steam ahead and make their mistakes for them.Only time will tell – but for now, it appears that the shining future of nucleargeneration outlined in Obama’s speeches will be funded not by the govern-ment but by the utility companies themselves. �

36 www.nextgenpe.com

“We’re seeing an evolution of thinking

regarding the value of nuclear as a

contributor to the solution”HELEN HOWES

“Support for new developments in nucleartechnologies will be critical to meeting ourenergy, climate and security goals foryears to come” STEVEN CHU

Cover Story:4August 5/11/09 15:19 Page 36

CH2MHill_AD.indd 121CH2MHill_AD.indd 121 3/11/09 10:39:053/11/09 10:39:05

38 www.nextgenpe.com

THE BIG INTERVIEW

Keeping it realMichael Morris, CEO of America’s largest electricity

generator, tells Natalie Brandweiner about his pragmatic approach to building our renewable energy future.

MORRIS ED P38-43.indd 38MORRIS ED P38-43.indd 38 5/11/09 15:58:375/11/09 15:58:37

www.nextgenpe.com 39

He notes the current activities of Senator Jeff Bingaman and the work he is currently undertaking with one of the principal committees in the Senate as a move towards this, describing it as, “A pushback from the Republicans, oddly enough.

“It’s a states’ rights issue versus federal government intervention. It’s the cost allocation. Why would somebody in New Jersey want to pay for a transmission line built in North Dakota to bring wind to the Twin Cities? Th at’s no diff erent from asking why would someone in Columbus want to pay for a bridge spanning Tampa Bay in Florida? But that’s the way the federal policy has always worked.

“Governor Pataki has been helping us on this issue, and he’s got two great analogies that are absolutely irrefutable. At the turn of the 20th century, De Witt Clinton, the mayor of New York City, suggested that they fund the Erie Canal. He had no idea it would make New York the fi nancial capital of the world for decades, and it has.

“Dwight Eisenhower, when he was President, for diff erent reasons believed very strongly in putting together an interstate highway system. He had no idea it would make California the eighth largest economy in the world, but it did. So the point here is if we built the electric grid in the same way we built the interstate highway system, we would build out a technology-enhanced greener footprint that is a less carbon in-tensive, less costly undertaking for the country, which would allow us to continue to have technological advantages over all the countries that we compete against.”

Shareholder growthAddressing AEP growth at a recent shareholder meeting, Michael

Morris said that actions taken in late 2008 and early 2009 were aimed at assuring the company’s stability in these weak economic conditions and have it positioned to resume growth when the economy recovers. BP CEO Tony Hayward recently faced the task of publicly denying that the com-pany had turned its back on renewables, as it reported a loss of 53 percent in second quarter profi ts. Renewable energy is not a fast ensurer of ROI, and so how can Morris be so sure that his investments are sturdy?

“Well, there’s a lot of credit here to the fi nance committee of the board of directors as well as our Chief Financial Offi cer and those inside of the fi nance group that we were early to move to take down lines of credit that we had negotiated back in the 2005/2006 timeline,” he replies. “We were fearful. We are an A2P2 credit rated utility as it pertains to commercial paper. Companies like ours and other utilities around the United States depend substantially on commercial paper to fund the day-to-day opera-tions of a business for paycheck, to pay for coal as it’s delivered, to pay the transporters, their bills as they send them to us, the entire business.

According to recent forecasts, the US energy grid will be adding 20 percent more users in the next 10 years. With its 39,000 miles of territory, Ameri-can Electric Power will have a major role to play, and AEP CEO Michael Morris believes the grid to currently be in a state to handle these demands. He

notes the mistakes made by previous energy growth forecasts, and the likelihood that those being made now have just as much potential for inaccuracy. “Whether they’re wrong on the high side or wrong on the low side is important, but if they miss it by a small amount, the grid will be fi ne,” he says.

“Th ere are some very important subsets, though, to what we need to do. When we had the 2003 outage, a lot of people said we had a Th ird World grid. Th at just isn’t accurate. What we have is a very bifurcated grid. It was not built regionally, it was built very locally as each utility served their own needs, and ultimately over time we have knitted that together.

“Th e American Electric Power 765 backbone grid serves 10 percent of all the energy that fl ows through the Eastern Interconnect, which is everything east of the Rocky Mountain region. American Electric Power’s transmission grid also handles about 10 percent of all the electricity that fl ows across Texas, so we will be a major player, no matter how this unfolds. Th erefore, it’s very important to our customers, very important to the states we serve and very important to our shareholders because we see it as a real potential growth opportunity in an earning sense,” Morris explains.

However, the question as to whether the grid should be regulated at federal or state level is no longer the primary issue. During the 1930s the interstate gas companies were forced to abide by federal regulation while the electric companies, under the Federal Power Act, chose to be contin-ually regulated by the states. Th is was then hard to change because of the footprint already established within the utility industry, says Morris.

“Th e benefi t of an interstate electric transmission grid will be to the benefi t of everyone who lives in the country, so why shouldn’t you spread it across the entirety of the gigawatt hours that the system is able to handle? If you do that and you have federal control over it, you’ll see a tremendous amount of transmission capacity added to the system, which will bring renewables into play and also change the way that we build power production facilities.

“You take a region of the country where you think you may need four or fi ve stations to be built. If the grid were truly interconnected, you might only need to build two or three of those stations. Today a new clean coal plant or a new nuclear station may cost as much as $7 billion. Build three of them instead of fi ve and you’ve saved the US economy a tremendous amount of money. So, yes, it should be federally regulated.”

New infrastructureMorris fully endorses the restructuring of the current generation

and transmission system and advocates the benefi ts it can provide. Surely such an overhaul and those jobs created would also provide federal bene-fi ts, helping President Obama reach his self-set target of creating fi ve mil-lion new green collar jobs. “If we’re ultimately going to make the country greener and less dependent on fossil-based fuels, it’s essential. Federal legislative control and cost allocation authority will take down the barri-ers that are holding back the capital investment needed,” he adds.

“Almost everywhere where I bump into politicians, they always want

to sell happy dust, the whole notion that we can do this without any

pain. Wouldn’t you love to believe that? But you know it’s not true”

MORRIS ED P38-43.indd 39MORRIS ED P38-43.indd 39 5/11/09 15:58:415/11/09 15:58:41

40 www.nextgenpe.com

to that same conclusion. I received enough emails back from the folks in this company that led me to believe they understood that. Was anybody happy, me included? No, of course not. Everyone thinks every year you ought to make more money, but the truth is that saved us a tremendous amount of revenue going forward. Th e 2008 plan did pay off , and we were honest about it, and we calculated the incentive compensation that everyone earned and everyone got it.

“Th ere are 21,640 men and women who have dedicated their lives to keeping the lights on in the 11 states that we do business. Th ey're bright people. Th ey want to be told the truth, and that’s what we do,” he explains.

In the mix Morris was recently quoted as saying of the energy mix, “Th ere is an issue here that is larger than many of us think. Th ere are answers, but the cost of energy is going to go up. I hate it when I hear Democrats and Republicans saying we need wind, we need solar, we need nuclear, and costs will come down. Th e politicians think it is going to be free. It isn’t.” It’s not a comfortable message for these times of increased focus on the benefi ts of renewables.

“Th e American people are bright, and all you need to do is tell them the truth. Politicians on both sides of the aisle – at the local level, at the state level, at the federal level – almost everywhere I bump into politi-cians, they always want to sell happy dust, the whole notion that we can do this without any pain. It’s like the commercials on TV: ‘You can lose 30 pounds and eat all the chocolate cake you like.’ Wouldn’t you love to believe that? But you know it’s not true.”

He notes the Energy Information Administration and the data they release as being “typically wrong.” Statistics such as ‘Wind is 15 cents a kilowatt hour; biomass is 12 cents a kilowatt hour; a well-run fossil plant with all of the paraphernalia, even with carbon capture, is approxi-mately six or seven cents a kilowatt hour.’ As the expenses of functioning the way we have been continue to increase, Morris emphasizes that the

“Worried that that might not sustain through an ex-tended credit crunch if it came, we took down those lines of credit. And what was predicted to happen did. A2P2 com-mercial paper was unavailable toward the latter part of the fourth quarter of 2008 and totally unavailable in the fi rst half of Q1 2009. Th at’s beginning to ease some now, but that gave us some fi nancial fl exibility.

“We then moved quickly into the equity markets in Q1 2009 to take advantage of what we saw as an opportunity to put additional equity into the system, help to balance out the debt-equity ratio in our balance sheet and support more strongly the notion that our ratings from the three principal rating agencies are not only right but sustainable now and into the near-term future.

“As many people know from our earnings call and up-dates, we’ve cut our capital budget to $1.8 billion for 2010. If times were diff erent, we would have that capital investment up in the $2.5 billion to $3 billion range because that’s the kind of money that needs to be spent on the system to make sure that we continue to provide reliable, cost-eff ective power to our customers,” he asserts.