Basic Finance Peter Ouwehand Department of Mathematical Sciences University of Stellenbosch November 2010 P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 1 / 30

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Basic Finance

Peter Ouwehand

Department of Mathematical SciencesUniversity of Stellenbosch

November 2010

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 1 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations use

I Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;

I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;

I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;

I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;

I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;

I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

What is Finance?

Finance: ”The study of how people allocate scarce resources overtime.”

Individuals and corporations useI Savings accounts;I Mortgages;I Pension funds;I Annuities;I Stock market;

The outcomes — the costs and benefits — of financial decisions areusually:

I spread over time;I uncertain, i.e. subject to risk;

To make intelligent investment and consumption decisions, individualsmust be able to value and compare different risky cashflows overtime.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 2 / 30

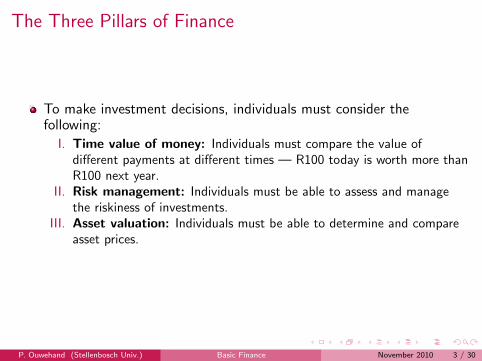

The Three Pillars of Finance

To make investment decisions, individuals must consider thefollowing:

I. Time value of money: Individuals must compare the value ofdifferent payments at different times — R100 today is worth more thanR100 next year.

II. Risk management: Individuals must be able to assess and managethe riskiness of investments.

III. Asset valuation: Individuals must be able to determine and compareasset prices.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 3 / 30

The Three Pillars of Finance

To make investment decisions, individuals must consider thefollowing:

I. Time value of money: Individuals must compare the value ofdifferent payments at different times — R100 today is worth more thanR100 next year.

II. Risk management: Individuals must be able to assess and managethe riskiness of investments.

III. Asset valuation: Individuals must be able to determine and compareasset prices.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 3 / 30

The Three Pillars of Finance

To make investment decisions, individuals must consider thefollowing:

I. Time value of money: Individuals must compare the value ofdifferent payments at different times — R100 today is worth more thanR100 next year.

II. Risk management: Individuals must be able to assess and managethe riskiness of investments.

III. Asset valuation: Individuals must be able to determine and compareasset prices.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 3 / 30

The Three Pillars of Finance

To make investment decisions, individuals must consider thefollowing:

I. Time value of money: Individuals must compare the value ofdifferent payments at different times — R100 today is worth more thanR100 next year.

II. Risk management: Individuals must be able to assess and managethe riskiness of investments.

III. Asset valuation: Individuals must be able to determine and compareasset prices.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 3 / 30

The Three Pillars of Finance

To make investment decisions, individuals must consider thefollowing:

I. Time value of money: Individuals must compare the value ofdifferent payments at different times — R100 today is worth more thanR100 next year.

II. Risk management: Individuals must be able to assess and managethe riskiness of investments.

III. Asset valuation: Individuals must be able to determine and compareasset prices.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 3 / 30

The Time Value of Money 1

Which do you prefer? R1000 in hand today, or the promise of R1000in one year’s time.Why?

I Opportunity cost: You can invest the R1000 now, with theexpectation of receiving a greater sum in the future.

I Inflation: R1000 in one year’s time may buy fewer goods than R1000today.

I Risk/Uncertainty: You can’t be sure that you will actually receive theR1000 in one year’s time.

So borrowing isn’t free: The borrower must pay a premium to inducethe lender to part temporarily with his/her money — the interest.

The interest rate depends on many factors, e.g. inflation, moneysupply, credit rating, etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 4 / 30

The Time Value of Money 1

Which do you prefer? R1000 in hand today, or the promise of R1000in one year’s time.Why?

I Opportunity cost: You can invest the R1000 now, with theexpectation of receiving a greater sum in the future.

I Inflation: R1000 in one year’s time may buy fewer goods than R1000today.

I Risk/Uncertainty: You can’t be sure that you will actually receive theR1000 in one year’s time.

So borrowing isn’t free: The borrower must pay a premium to inducethe lender to part temporarily with his/her money — the interest.

The interest rate depends on many factors, e.g. inflation, moneysupply, credit rating, etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 4 / 30

The Time Value of Money 1

Which do you prefer? R1000 in hand today, or the promise of R1000in one year’s time.Why?

I Opportunity cost: You can invest the R1000 now, with theexpectation of receiving a greater sum in the future.

I Inflation: R1000 in one year’s time may buy fewer goods than R1000today.

I Risk/Uncertainty: You can’t be sure that you will actually receive theR1000 in one year’s time.

So borrowing isn’t free: The borrower must pay a premium to inducethe lender to part temporarily with his/her money — the interest.

The interest rate depends on many factors, e.g. inflation, moneysupply, credit rating, etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 4 / 30

The Time Value of Money 1

Which do you prefer? R1000 in hand today, or the promise of R1000in one year’s time.Why?

I Opportunity cost: You can invest the R1000 now, with theexpectation of receiving a greater sum in the future.

I Inflation: R1000 in one year’s time may buy fewer goods than R1000today.

I Risk/Uncertainty: You can’t be sure that you will actually receive theR1000 in one year’s time.

So borrowing isn’t free: The borrower must pay a premium to inducethe lender to part temporarily with his/her money — the interest.

The interest rate depends on many factors, e.g. inflation, moneysupply, credit rating, etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 4 / 30

The Time Value of Money 1

Which do you prefer? R1000 in hand today, or the promise of R1000in one year’s time.Why?

I Opportunity cost: You can invest the R1000 now, with theexpectation of receiving a greater sum in the future.

I Inflation: R1000 in one year’s time may buy fewer goods than R1000today.

I Risk/Uncertainty: You can’t be sure that you will actually receive theR1000 in one year’s time.

So borrowing isn’t free: The borrower must pay a premium to inducethe lender to part temporarily with his/her money — the interest.

The interest rate depends on many factors, e.g. inflation, moneysupply, credit rating, etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 4 / 30

The Time Value of Money 1

Which do you prefer? R1000 in hand today, or the promise of R1000in one year’s time.Why?

I Opportunity cost: You can invest the R1000 now, with theexpectation of receiving a greater sum in the future.

I Inflation: R1000 in one year’s time may buy fewer goods than R1000today.

I Risk/Uncertainty: You can’t be sure that you will actually receive theR1000 in one year’s time.

So borrowing isn’t free: The borrower must pay a premium to inducethe lender to part temporarily with his/her money — the interest.

The interest rate depends on many factors, e.g. inflation, moneysupply, credit rating, etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 4 / 30

The Time Value of Money 1

Which do you prefer? R1000 in hand today, or the promise of R1000in one year’s time.Why?

I Opportunity cost: You can invest the R1000 now, with theexpectation of receiving a greater sum in the future.

I Inflation: R1000 in one year’s time may buy fewer goods than R1000today.

I Risk/Uncertainty: You can’t be sure that you will actually receive theR1000 in one year’s time.

So borrowing isn’t free: The borrower must pay a premium to inducethe lender to part temporarily with his/her money — the interest.

The interest rate depends on many factors, e.g. inflation, moneysupply, credit rating, etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 4 / 30

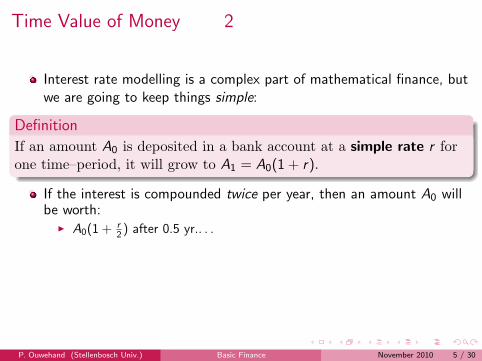

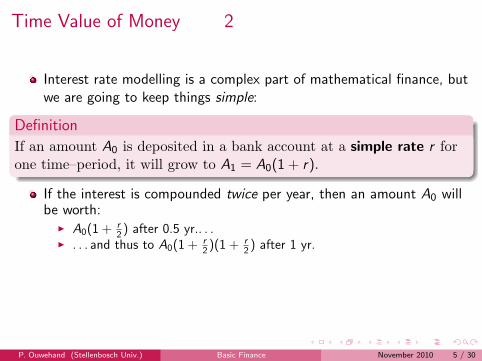

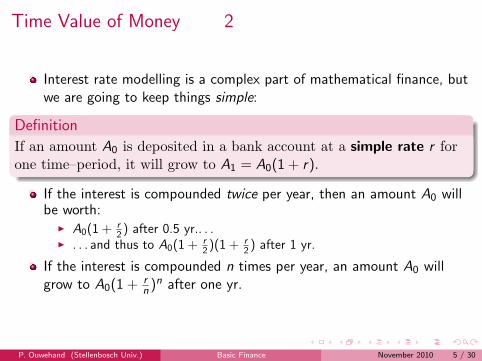

Time Value of Money 2

Interest rate modelling is a complex part of mathematical finance, butwe are going to keep things simple:

Definition

If an amount A0 is deposited in a bank account at a simple rate r forone time–period, it will grow to A1 = A0(1 + r).

If the interest is compounded twice per year, then an amount A0 willbe worth:

I A0(1 + r2 ) after 0.5 yr.. . .

I . . . and thus to A0(1 + r2 )(1 + r

2 ) after 1 yr.

If the interest is compounded n times per year, an amount A0 willgrow to A0(1 + r

n )n after one yr.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 5 / 30

Time Value of Money 2

Interest rate modelling is a complex part of mathematical finance, butwe are going to keep things simple:

Definition

If an amount A0 is deposited in a bank account at a simple rate r forone time–period, it will grow to A1 = A0(1 + r).

If the interest is compounded twice per year, then an amount A0 willbe worth:

I A0(1 + r2 ) after 0.5 yr.. . .

I . . . and thus to A0(1 + r2 )(1 + r

2 ) after 1 yr.

If the interest is compounded n times per year, an amount A0 willgrow to A0(1 + r

n )n after one yr.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 5 / 30

Time Value of Money 2

Interest rate modelling is a complex part of mathematical finance, butwe are going to keep things simple:

Definition

If an amount A0 is deposited in a bank account at a simple rate r forone time–period, it will grow to A1 = A0(1 + r).

If the interest is compounded twice per year, then an amount A0 willbe worth:

I A0(1 + r2 ) after 0.5 yr.. . .

I . . . and thus to A0(1 + r2 )(1 + r

2 ) after 1 yr.

If the interest is compounded n times per year, an amount A0 willgrow to A0(1 + r

n )n after one yr.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 5 / 30

Time Value of Money 2

Interest rate modelling is a complex part of mathematical finance, butwe are going to keep things simple:

Definition

If an amount A0 is deposited in a bank account at a simple rate r forone time–period, it will grow to A1 = A0(1 + r).

If the interest is compounded twice per year, then an amount A0 willbe worth:

I A0(1 + r2 ) after 0.5 yr.. . .

I . . . and thus to A0(1 + r2 )(1 + r

2 ) after 1 yr.

If the interest is compounded n times per year, an amount A0 willgrow to A0(1 + r

n )n after one yr.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 5 / 30

Time Value of Money 2

Interest rate modelling is a complex part of mathematical finance, butwe are going to keep things simple:

Definition

If an amount A0 is deposited in a bank account at a simple rate r forone time–period, it will grow to A1 = A0(1 + r).

If the interest is compounded twice per year, then an amount A0 willbe worth:

I A0(1 + r2 ) after 0.5 yr.. . .

I . . . and thus to A0(1 + r2 )(1 + r

2 ) after 1 yr.

If the interest is compounded n times per year, an amount A0 willgrow to A0(1 + r

n )n after one yr.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 5 / 30

Time Value of Money 2

Interest rate modelling is a complex part of mathematical finance, butwe are going to keep things simple:

Definition

If an amount A0 is deposited in a bank account at a simple rate r forone time–period, it will grow to A1 = A0(1 + r).

If the interest is compounded twice per year, then an amount A0 willbe worth:

I A0(1 + r2 ) after 0.5 yr.. . .

I . . . and thus to A0(1 + r2 )(1 + r

2 ) after 1 yr.

If the interest is compounded n times per year, an amount A0 willgrow to A0(1 + r

n )n after one yr.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 5 / 30

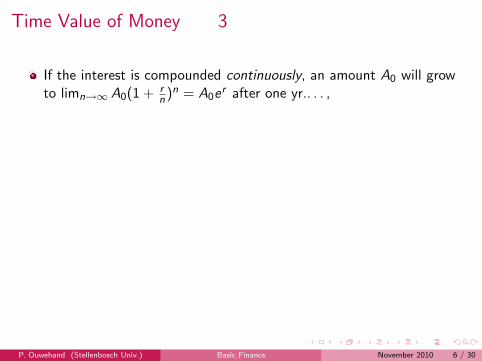

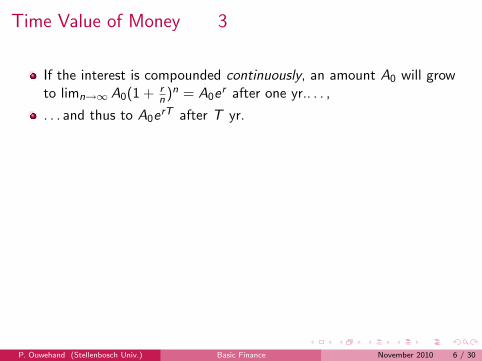

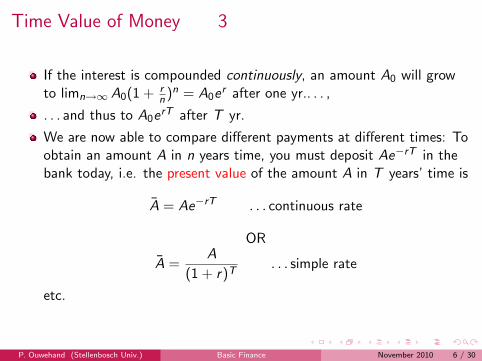

Time Value of Money 3

If the interest is compounded continuously, an amount A0 will growto limn→∞ A0(1 + r

n )n = A0er after one yr.. . . ,

. . . and thus to A0erT after T yr.

We are now able to compare different payments at different times: Toobtain an amount A in n years time, you must deposit Ae−rT in thebank today, i.e. the present value of the amount A in T years’ time is

A = Ae−rT . . . continuous rate

OR

A =A

(1 + r)T. . . simple rate

etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 6 / 30

Time Value of Money 3

If the interest is compounded continuously, an amount A0 will growto limn→∞ A0(1 + r

n )n = A0er after one yr.. . . ,

. . . and thus to A0erT after T yr.

We are now able to compare different payments at different times: Toobtain an amount A in n years time, you must deposit Ae−rT in thebank today, i.e. the present value of the amount A in T years’ time is

A = Ae−rT . . . continuous rate

OR

A =A

(1 + r)T. . . simple rate

etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 6 / 30

Time Value of Money 3

If the interest is compounded continuously, an amount A0 will growto limn→∞ A0(1 + r

n )n = A0er after one yr.. . . ,

. . . and thus to A0erT after T yr.

We are now able to compare different payments at different times: Toobtain an amount A in n years time, you must deposit Ae−rT in thebank today, i.e. the present value of the amount A in T years’ time is

A = Ae−rT . . . continuous rate

OR

A =A

(1 + r)T. . . simple rate

etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 6 / 30

Time Value of Money 3

If the interest is compounded continuously, an amount A0 will growto limn→∞ A0(1 + r

n )n = A0er after one yr.. . . ,

. . . and thus to A0erT after T yr.

We are now able to compare different payments at different times: Toobtain an amount A in n years time, you must deposit Ae−rT in thebank today, i.e. the present value of the amount A in T years’ time is

A = Ae−rT . . . continuous rate

OR

A =A

(1 + r)T. . . simple rate

etc.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 6 / 30

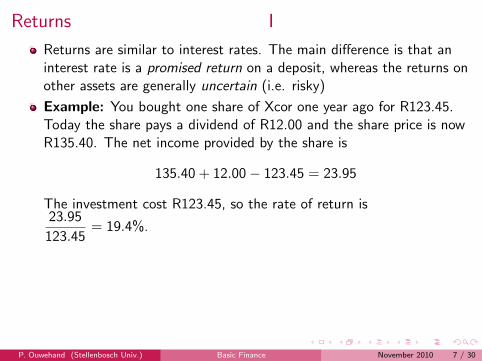

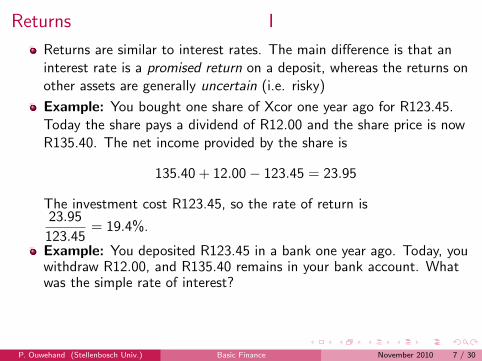

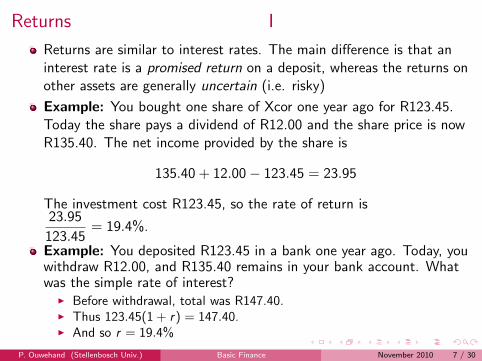

Returns I

Returns are similar to interest rates. The main difference is that aninterest rate is a promised return on a deposit, whereas the returns onother assets are generally uncertain (i.e. risky)

Example: You bought one share of Xcor one year ago for R123.45.Today the share pays a dividend of R12.00 and the share price is nowR135.40. The net income provided by the share is

135.40 + 12.00− 123.45 = 23.95

The investment cost R123.45, so the rate of return is23.95

123.45= 19.4%.

Example: You deposited R123.45 in a bank one year ago. Today, youwithdraw R12.00, and R135.40 remains in your bank account. Whatwas the simple rate of interest?

I Before withdrawal, total was R147.40.I Thus 123.45(1 + r) = 147.40.I And so r = 19.4%

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 7 / 30

Returns I

Returns are similar to interest rates. The main difference is that aninterest rate is a promised return on a deposit, whereas the returns onother assets are generally uncertain (i.e. risky)

Example: You bought one share of Xcor one year ago for R123.45.Today the share pays a dividend of R12.00 and the share price is nowR135.40. The net income provided by the share is

135.40 + 12.00− 123.45 = 23.95

The investment cost R123.45, so the rate of return is23.95

123.45= 19.4%.

Example: You deposited R123.45 in a bank one year ago. Today, youwithdraw R12.00, and R135.40 remains in your bank account. Whatwas the simple rate of interest?

I Before withdrawal, total was R147.40.I Thus 123.45(1 + r) = 147.40.I And so r = 19.4%

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 7 / 30

Returns I

Returns are similar to interest rates. The main difference is that aninterest rate is a promised return on a deposit, whereas the returns onother assets are generally uncertain (i.e. risky)

Example: You bought one share of Xcor one year ago for R123.45.Today the share pays a dividend of R12.00 and the share price is nowR135.40. The net income provided by the share is

135.40 + 12.00− 123.45 = 23.95

The investment cost R123.45, so the rate of return is23.95

123.45= 19.4%.

Example: You deposited R123.45 in a bank one year ago. Today, youwithdraw R12.00, and R135.40 remains in your bank account. Whatwas the simple rate of interest?

I Before withdrawal, total was R147.40.I Thus 123.45(1 + r) = 147.40.I And so r = 19.4%

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 7 / 30

Returns I

Returns are similar to interest rates. The main difference is that aninterest rate is a promised return on a deposit, whereas the returns onother assets are generally uncertain (i.e. risky)

Example: You bought one share of Xcor one year ago for R123.45.Today the share pays a dividend of R12.00 and the share price is nowR135.40. The net income provided by the share is

135.40 + 12.00− 123.45 = 23.95

The investment cost R123.45, so the rate of return is23.95

123.45= 19.4%.

Example: You deposited R123.45 in a bank one year ago. Today, youwithdraw R12.00, and R135.40 remains in your bank account. Whatwas the simple rate of interest?

I Before withdrawal, total was R147.40.I Thus 123.45(1 + r) = 147.40.I And so r = 19.4%

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 7 / 30

Returns I

Returns are similar to interest rates. The main difference is that aninterest rate is a promised return on a deposit, whereas the returns onother assets are generally uncertain (i.e. risky)

Example: You bought one share of Xcor one year ago for R123.45.Today the share pays a dividend of R12.00 and the share price is nowR135.40. The net income provided by the share is

135.40 + 12.00− 123.45 = 23.95

The investment cost R123.45, so the rate of return is23.95

123.45= 19.4%.

Example: You deposited R123.45 in a bank one year ago. Today, youwithdraw R12.00, and R135.40 remains in your bank account. Whatwas the simple rate of interest?

I Before withdrawal, total was R147.40.

I Thus 123.45(1 + r) = 147.40.I And so r = 19.4%

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 7 / 30

Returns I

Returns are similar to interest rates. The main difference is that aninterest rate is a promised return on a deposit, whereas the returns onother assets are generally uncertain (i.e. risky)

Example: You bought one share of Xcor one year ago for R123.45.Today the share pays a dividend of R12.00 and the share price is nowR135.40. The net income provided by the share is

135.40 + 12.00− 123.45 = 23.95

The investment cost R123.45, so the rate of return is23.95

123.45= 19.4%.

Example: You deposited R123.45 in a bank one year ago. Today, youwithdraw R12.00, and R135.40 remains in your bank account. Whatwas the simple rate of interest?

I Before withdrawal, total was R147.40.I Thus 123.45(1 + r) = 147.40.

I And so r = 19.4%

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 7 / 30

Returns I

Returns are similar to interest rates. The main difference is that aninterest rate is a promised return on a deposit, whereas the returns onother assets are generally uncertain (i.e. risky)

Example: You bought one share of Xcor one year ago for R123.45.Today the share pays a dividend of R12.00 and the share price is nowR135.40. The net income provided by the share is

135.40 + 12.00− 123.45 = 23.95

The investment cost R123.45, so the rate of return is23.95

123.45= 19.4%.

Example: You deposited R123.45 in a bank one year ago. Today, youwithdraw R12.00, and R135.40 remains in your bank account. Whatwas the simple rate of interest?

I Before withdrawal, total was R147.40.I Thus 123.45(1 + r) = 147.40.I And so r = 19.4%

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 7 / 30

Returns II

Fundamental relationship in finance:

E[Return] = f (Risk)

where f is an increasing function.

Shares are riskier investments than deposits. Thus the expectedreturn on a share should be greater than the interest offered by abank account.

Note that returns can be negative, whereas interest rates must bepositive.

The return on an investment is roughly the percentage by which itsvalue has increased in one year, i.e.

Return =Final Price + Interim Cashflows – Initial Price

Initial Price

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 8 / 30

Returns II

Fundamental relationship in finance:

E[Return] = f (Risk)

where f is an increasing function.

Shares are riskier investments than deposits. Thus the expectedreturn on a share should be greater than the interest offered by abank account.

Note that returns can be negative, whereas interest rates must bepositive.

The return on an investment is roughly the percentage by which itsvalue has increased in one year, i.e.

Return =Final Price + Interim Cashflows – Initial Price

Initial Price

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 8 / 30

Returns II

Fundamental relationship in finance:

E[Return] = f (Risk)

where f is an increasing function.

Shares are riskier investments than deposits. Thus the expectedreturn on a share should be greater than the interest offered by abank account.

Note that returns can be negative, whereas interest rates must bepositive.

The return on an investment is roughly the percentage by which itsvalue has increased in one year, i.e.

Return =Final Price + Interim Cashflows – Initial Price

Initial Price

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 8 / 30

Returns II

Fundamental relationship in finance:

E[Return] = f (Risk)

where f is an increasing function.

Shares are riskier investments than deposits. Thus the expectedreturn on a share should be greater than the interest offered by abank account.

Note that returns can be negative, whereas interest rates must bepositive.

The return on an investment is roughly the percentage by which itsvalue has increased in one year, i.e.

Return =Final Price + Interim Cashflows – Initial Price

Initial Price

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 8 / 30

Returns II

Fundamental relationship in finance:

E[Return] = f (Risk)

where f is an increasing function.

Shares are riskier investments than deposits. Thus the expectedreturn on a share should be greater than the interest offered by abank account.

Note that returns can be negative, whereas interest rates must bepositive.

The return on an investment is roughly the percentage by which itsvalue has increased in one year, i.e.

Return =Final Price + Interim Cashflows – Initial Price

Initial Price

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 8 / 30

Returns III

Shares with a higher expected return are therefore riskier than shareswith a low expected return.

I If two shares had the same risk, but different expected returns,everyone would buy the share with the higher return (and short theshare with the lower return).

I This would drive the price of the “high return” share up, thus loweringits return.

The riskiness of a share is measured by a quantity called volatility: Itis the standard deviation of annualized returns.

Returns may also be measured as discretely– or continuouslycompounded.

Returns on bonds are called yields.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 9 / 30

Returns III

Shares with a higher expected return are therefore riskier than shareswith a low expected return.

I If two shares had the same risk, but different expected returns,everyone would buy the share with the higher return (and short theshare with the lower return).

I This would drive the price of the “high return” share up, thus loweringits return.

The riskiness of a share is measured by a quantity called volatility: Itis the standard deviation of annualized returns.

Returns may also be measured as discretely– or continuouslycompounded.

Returns on bonds are called yields.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 9 / 30

Returns III

Shares with a higher expected return are therefore riskier than shareswith a low expected return.

I If two shares had the same risk, but different expected returns,everyone would buy the share with the higher return (and short theshare with the lower return).

I This would drive the price of the “high return” share up, thus loweringits return.

The riskiness of a share is measured by a quantity called volatility: Itis the standard deviation of annualized returns.

Returns may also be measured as discretely– or continuouslycompounded.

Returns on bonds are called yields.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 9 / 30

Returns III

Shares with a higher expected return are therefore riskier than shareswith a low expected return.

I If two shares had the same risk, but different expected returns,everyone would buy the share with the higher return (and short theshare with the lower return).

I This would drive the price of the “high return” share up, thus loweringits return.

The riskiness of a share is measured by a quantity called volatility: Itis the standard deviation of annualized returns.

Returns may also be measured as discretely– or continuouslycompounded.

Returns on bonds are called yields.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 9 / 30

Returns III

Shares with a higher expected return are therefore riskier than shareswith a low expected return.

I If two shares had the same risk, but different expected returns,everyone would buy the share with the higher return (and short theshare with the lower return).

I This would drive the price of the “high return” share up, thus loweringits return.

The riskiness of a share is measured by a quantity called volatility: Itis the standard deviation of annualized returns.

Returns may also be measured as discretely– or continuouslycompounded.

Returns on bonds are called yields.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 9 / 30

Returns III

Shares with a higher expected return are therefore riskier than shareswith a low expected return.

I If two shares had the same risk, but different expected returns,everyone would buy the share with the higher return (and short theshare with the lower return).

I This would drive the price of the “high return” share up, thus loweringits return.

The riskiness of a share is measured by a quantity called volatility: Itis the standard deviation of annualized returns.

Returns may also be measured as discretely– or continuouslycompounded.

Returns on bonds are called yields.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 9 / 30

Returns III

Shares with a higher expected return are therefore riskier than shareswith a low expected return.

I If two shares had the same risk, but different expected returns,everyone would buy the share with the higher return (and short theshare with the lower return).

I This would drive the price of the “high return” share up, thus loweringits return.

The riskiness of a share is measured by a quantity called volatility: Itis the standard deviation of annualized returns.

Returns may also be measured as discretely– or continuouslycompounded.

Returns on bonds are called yields.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 9 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.

I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I shares

I bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bonds

I derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments I

Traders in a financial market exchange securities for money.

Securities are contracts for future delivery of goods or money, e.g.I sharesI bondsI derivatives

One distinguishes between underlying (primary) and derivative(secondary) instruments.

Examples of underlying instruments are shares, bonds, currencies,interest rates, and indexes.

A derivative is a financial instruments whose value is derived from anunderlying asset.

Examples of derivatives are forward contracts, futures, options, swapsand bonds.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 10 / 30

Markets and Instruments II

One also distinguishes between primary and secondary markets.Securities are issued for the first time on the primary market, andthen traded on the secondary market. The secondary market providesimportant liquidity.

Borrowing and lending is done in fixed–income markets. The moneymarket is for very short–term debt (maturities ≤ 1 yr.)

Finally, we distinguish between the spot market and the forwardmarket.

I Most transactions are spot transactions: Pay now, and receive goodsnow.

I To hedge/speculate on future market movements, it is possible to sellgoods for delivery in the future. Forward and futures contracts arederivatives which make this possible.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 11 / 30

Markets and Instruments II

One also distinguishes between primary and secondary markets.Securities are issued for the first time on the primary market, andthen traded on the secondary market. The secondary market providesimportant liquidity.

Borrowing and lending is done in fixed–income markets. The moneymarket is for very short–term debt (maturities ≤ 1 yr.)

Finally, we distinguish between the spot market and the forwardmarket.

I Most transactions are spot transactions: Pay now, and receive goodsnow.

I To hedge/speculate on future market movements, it is possible to sellgoods for delivery in the future. Forward and futures contracts arederivatives which make this possible.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 11 / 30

Markets and Instruments II

One also distinguishes between primary and secondary markets.Securities are issued for the first time on the primary market, andthen traded on the secondary market. The secondary market providesimportant liquidity.

Borrowing and lending is done in fixed–income markets. The moneymarket is for very short–term debt (maturities ≤ 1 yr.)

Finally, we distinguish between the spot market and the forwardmarket.

I Most transactions are spot transactions: Pay now, and receive goodsnow.

I To hedge/speculate on future market movements, it is possible to sellgoods for delivery in the future. Forward and futures contracts arederivatives which make this possible.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 11 / 30

Markets and Instruments II

One also distinguishes between primary and secondary markets.Securities are issued for the first time on the primary market, andthen traded on the secondary market. The secondary market providesimportant liquidity.

Borrowing and lending is done in fixed–income markets. The moneymarket is for very short–term debt (maturities ≤ 1 yr.)

Finally, we distinguish between the spot market and the forwardmarket.

I Most transactions are spot transactions: Pay now, and receive goodsnow.

I To hedge/speculate on future market movements, it is possible to sellgoods for delivery in the future. Forward and futures contracts arederivatives which make this possible.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 11 / 30

Markets and Instruments II

One also distinguishes between primary and secondary markets.Securities are issued for the first time on the primary market, andthen traded on the secondary market. The secondary market providesimportant liquidity.

Borrowing and lending is done in fixed–income markets. The moneymarket is for very short–term debt (maturities ≤ 1 yr.)

Finally, we distinguish between the spot market and the forwardmarket.

I Most transactions are spot transactions: Pay now, and receive goodsnow.

I To hedge/speculate on future market movements, it is possible to sellgoods for delivery in the future. Forward and futures contracts arederivatives which make this possible.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 11 / 30

Markets and Instruments II

One also distinguishes between primary and secondary markets.Securities are issued for the first time on the primary market, andthen traded on the secondary market. The secondary market providesimportant liquidity.

Borrowing and lending is done in fixed–income markets. The moneymarket is for very short–term debt (maturities ≤ 1 yr.)

Finally, we distinguish between the spot market and the forwardmarket.

I Most transactions are spot transactions: Pay now, and receive goodsnow.

I To hedge/speculate on future market movements, it is possible to sellgoods for delivery in the future. Forward and futures contracts arederivatives which make this possible.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 11 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.I Shareholders own a corporation. Directors act in the shareholders’

best interest.I Public limited companies are listed on a stock exchange. Ownership is

easily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.I On the ex-dividend date, the share price decreases by the amount of

the dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.

I Shareholders own a corporation. Directors act in the shareholders’best interest.

I Public limited companies are listed on a stock exchange. Ownership iseasily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.I On the ex-dividend date, the share price decreases by the amount of

the dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.I Shareholders own a corporation. Directors act in the shareholders’

best interest.

I Public limited companies are listed on a stock exchange. Ownership iseasily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.I On the ex-dividend date, the share price decreases by the amount of

the dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.I Shareholders own a corporation. Directors act in the shareholders’

best interest.I Public limited companies are listed on a stock exchange. Ownership is

easily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.I On the ex-dividend date, the share price decreases by the amount of

the dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.I Shareholders own a corporation. Directors act in the shareholders’

best interest.I Public limited companies are listed on a stock exchange. Ownership is

easily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.I On the ex-dividend date, the share price decreases by the amount of

the dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.I Shareholders own a corporation. Directors act in the shareholders’

best interest.I Public limited companies are listed on a stock exchange. Ownership is

easily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.

I On the ex-dividend date, the share price decreases by the amount ofthe dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.I Shareholders own a corporation. Directors act in the shareholders’

best interest.I Public limited companies are listed on a stock exchange. Ownership is

easily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.I On the ex-dividend date, the share price decreases by the amount of

the dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments III

Equity: Stocks, shares. Ownership of a small piece of a company.I Shareholders own a corporation. Directors act in the shareholders’

best interest.I Public limited companies are listed on a stock exchange. Ownership is

easily transferred. The shareholders share the profits of the company,but have limited liability: At most, they can lose their investment.

Most shares pay regular dividends, whose amount varies according toprofitability and opportunities for growth.

I A share may be bought cum– or ex–dividend.I On the ex-dividend date, the share price decreases by the amount of

the dividend.

Occasionally a company announces a stock split: Suppose, forexample, that you own a single stock whose current price is R600.00.After a 3–for–1 stock split you will own 3 shares each valued atR200.00.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 12 / 30

Markets and Instruments IV

Short selling: Selling a share you don’t own, hoping to pick them upmore cheaply later on.

I Your broker borrows the share from a client.I You may now sell these shares, even though you don’t own them.I Later, you buy the shares in the market and return them to your

broker, who returns them to the other client. You also pay anydividends that were issued in the interim.

Commodities: Raw materials such as metals, oil, agriculturalproducts, etc. These are often traded by people who have no need forthe material, but are speculating on the direction of the commodity.Most of this trading is done in the futures market, and contracts areclosed out before the delivery date.

Currencies: FOREX.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 13 / 30

Markets and Instruments IV

Short selling: Selling a share you don’t own, hoping to pick them upmore cheaply later on.

I Your broker borrows the share from a client.I You may now sell these shares, even though you don’t own them.I Later, you buy the shares in the market and return them to your

broker, who returns them to the other client. You also pay anydividends that were issued in the interim.

Commodities: Raw materials such as metals, oil, agriculturalproducts, etc. These are often traded by people who have no need forthe material, but are speculating on the direction of the commodity.Most of this trading is done in the futures market, and contracts areclosed out before the delivery date.

Currencies: FOREX.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 13 / 30

Markets and Instruments IV

Short selling: Selling a share you don’t own, hoping to pick them upmore cheaply later on.

I Your broker borrows the share from a client.

I You may now sell these shares, even though you don’t own them.I Later, you buy the shares in the market and return them to your

broker, who returns them to the other client. You also pay anydividends that were issued in the interim.

Commodities: Raw materials such as metals, oil, agriculturalproducts, etc. These are often traded by people who have no need forthe material, but are speculating on the direction of the commodity.Most of this trading is done in the futures market, and contracts areclosed out before the delivery date.

Currencies: FOREX.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 13 / 30

Markets and Instruments IV

Short selling: Selling a share you don’t own, hoping to pick them upmore cheaply later on.

I Your broker borrows the share from a client.I You may now sell these shares, even though you don’t own them.

I Later, you buy the shares in the market and return them to yourbroker, who returns them to the other client. You also pay anydividends that were issued in the interim.

Commodities: Raw materials such as metals, oil, agriculturalproducts, etc. These are often traded by people who have no need forthe material, but are speculating on the direction of the commodity.Most of this trading is done in the futures market, and contracts areclosed out before the delivery date.

Currencies: FOREX.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 13 / 30

Markets and Instruments IV

Short selling: Selling a share you don’t own, hoping to pick them upmore cheaply later on.

I Your broker borrows the share from a client.I You may now sell these shares, even though you don’t own them.I Later, you buy the shares in the market and return them to your

broker, who returns them to the other client. You also pay anydividends that were issued in the interim.

Commodities: Raw materials such as metals, oil, agriculturalproducts, etc. These are often traded by people who have no need forthe material, but are speculating on the direction of the commodity.Most of this trading is done in the futures market, and contracts areclosed out before the delivery date.

Currencies: FOREX.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 13 / 30

Markets and Instruments IV

Short selling: Selling a share you don’t own, hoping to pick them upmore cheaply later on.

I Your broker borrows the share from a client.I You may now sell these shares, even though you don’t own them.I Later, you buy the shares in the market and return them to your

broker, who returns them to the other client. You also pay anydividends that were issued in the interim.

Commodities: Raw materials such as metals, oil, agriculturalproducts, etc. These are often traded by people who have no need forthe material, but are speculating on the direction of the commodity.Most of this trading is done in the futures market, and contracts areclosed out before the delivery date.

Currencies: FOREX.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 13 / 30

Markets and Instruments IV

Short selling: Selling a share you don’t own, hoping to pick them upmore cheaply later on.

I Your broker borrows the share from a client.I You may now sell these shares, even though you don’t own them.I Later, you buy the shares in the market and return them to your

broker, who returns them to the other client. You also pay anydividends that were issued in the interim.

Commodities: Raw materials such as metals, oil, agriculturalproducts, etc. These are often traded by people who have no need forthe material, but are speculating on the direction of the commodity.Most of this trading is done in the futures market, and contracts areclosed out before the delivery date.

Currencies: FOREX.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 13 / 30

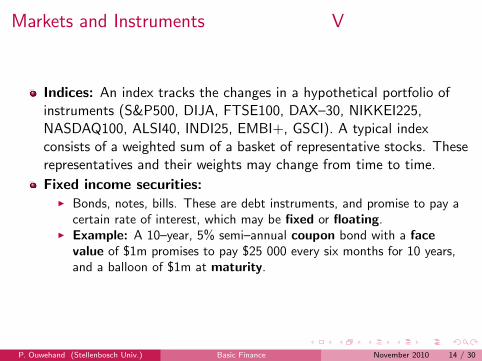

Markets and Instruments V

Indices: An index tracks the changes in a hypothetical portfolio ofinstruments (S&P500, DIJA, FTSE100, DAX–30, NIKKEI225,NASDAQ100, ALSI40, INDI25, EMBI+, GSCI). A typical indexconsists of a weighted sum of a basket of representative stocks. Theserepresentatives and their weights may change from time to time.

Fixed income securities:I Bonds, notes, bills. These are debt instruments, and promise to pay a

certain rate of interest, which may be fixed or floating.I Example: A 10–year, 5% semi–annual coupon bond with a face

value of $1m promises to pay $25 000 every six months for 10 years,and a balloon of $1m at maturity.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 14 / 30

Markets and Instruments V

Indices: An index tracks the changes in a hypothetical portfolio ofinstruments (S&P500, DIJA, FTSE100, DAX–30, NIKKEI225,NASDAQ100, ALSI40, INDI25, EMBI+, GSCI). A typical indexconsists of a weighted sum of a basket of representative stocks. Theserepresentatives and their weights may change from time to time.

Fixed income securities:I Bonds, notes, bills. These are debt instruments, and promise to pay a

certain rate of interest, which may be fixed or floating.I Example: A 10–year, 5% semi–annual coupon bond with a face

value of $1m promises to pay $25 000 every six months for 10 years,and a balloon of $1m at maturity.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 14 / 30

Markets and Instruments V

Indices: An index tracks the changes in a hypothetical portfolio ofinstruments (S&P500, DIJA, FTSE100, DAX–30, NIKKEI225,NASDAQ100, ALSI40, INDI25, EMBI+, GSCI). A typical indexconsists of a weighted sum of a basket of representative stocks. Theserepresentatives and their weights may change from time to time.

Fixed income securities:

I Bonds, notes, bills. These are debt instruments, and promise to pay acertain rate of interest, which may be fixed or floating.

I Example: A 10–year, 5% semi–annual coupon bond with a facevalue of $1m promises to pay $25 000 every six months for 10 years,and a balloon of $1m at maturity.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 14 / 30

Markets and Instruments V

Indices: An index tracks the changes in a hypothetical portfolio ofinstruments (S&P500, DIJA, FTSE100, DAX–30, NIKKEI225,NASDAQ100, ALSI40, INDI25, EMBI+, GSCI). A typical indexconsists of a weighted sum of a basket of representative stocks. Theserepresentatives and their weights may change from time to time.

Fixed income securities:I Bonds, notes, bills. These are debt instruments, and promise to pay a

certain rate of interest, which may be fixed or floating.

I Example: A 10–year, 5% semi–annual coupon bond with a facevalue of $1m promises to pay $25 000 every six months for 10 years,and a balloon of $1m at maturity.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 14 / 30

Markets and Instruments V

Indices: An index tracks the changes in a hypothetical portfolio ofinstruments (S&P500, DIJA, FTSE100, DAX–30, NIKKEI225,NASDAQ100, ALSI40, INDI25, EMBI+, GSCI). A typical indexconsists of a weighted sum of a basket of representative stocks. Theserepresentatives and their weights may change from time to time.

Fixed income securities:I Bonds, notes, bills. These are debt instruments, and promise to pay a

certain rate of interest, which may be fixed or floating.I Example: A 10–year, 5% semi–annual coupon bond with a face

value of $1m promises to pay $25 000 every six months for 10 years,and a balloon of $1m at maturity.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 14 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.

I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.

I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.

I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.

I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:

I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.

I They can be used to speculate — to take on extra risk in the hope ofgreater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Derivative Securities

Individuals and corporations face risks, and many of these risks entailfinancial gain or loss. Often, gain or loss is a simple result of a changein the value of a market variable, such as a price or rate:

I Commodity prices: Oil, maize, wheat, wool, etc.I Interest rates.I The prices of stocks that make up a pension portfolio.I Foreign currency exchange rates.I . . .

A derivative security is a financial instrument whose value is derivedfrom another, underlying or primary, variable, such as a stock price,an interest rate, a commodity price, a forex rate, etc.

Derivatives are used to transfer risk:I They can be used to hedge — i.e. as insurance against adverse risk.I They can be used to speculate — to take on extra risk in the hope of

greater returns.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 15 / 30

Call Options

An option gives the holder the right, but not the obligation to buy or sellan asset.

A European call option gives the holder the right to buy an asset S (theunderlying) for an agreed amount K (the strike price or exercise price) ona specified future date T (maturity or expiry).

The party who undertakes to deliver the asset is called the writer ofthe option.

The buyer of a European call would exercise at time T only ifK < S(T ), for a profit of S(T )− K .

If the spot price is less than the strike, the holder would discard theoption: Why pay K if you can pay S(T ) < K ?

Thus the payoff to the holder is max{S(T )− K , 0} ≥ 0.

Unlike forward contracts, options cost money. You have to pay thewriter of an option a premium upfront to enter into the contract.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 16 / 30

Call Options

An option gives the holder the right, but not the obligation to buy or sellan asset.

A European call option gives the holder the right to buy an asset S (theunderlying) for an agreed amount K (the strike price or exercise price) ona specified future date T (maturity or expiry).

The party who undertakes to deliver the asset is called the writer ofthe option.

The buyer of a European call would exercise at time T only ifK < S(T ), for a profit of S(T )− K .

If the spot price is less than the strike, the holder would discard theoption: Why pay K if you can pay S(T ) < K ?

Thus the payoff to the holder is max{S(T )− K , 0} ≥ 0.

Unlike forward contracts, options cost money. You have to pay thewriter of an option a premium upfront to enter into the contract.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 16 / 30

Call Options

An option gives the holder the right, but not the obligation to buy or sellan asset.

A European call option gives the holder the right to buy an asset S (theunderlying) for an agreed amount K (the strike price or exercise price) ona specified future date T (maturity or expiry).

The party who undertakes to deliver the asset is called the writer ofthe option.

The buyer of a European call would exercise at time T only ifK < S(T ), for a profit of S(T )− K .

If the spot price is less than the strike, the holder would discard theoption: Why pay K if you can pay S(T ) < K ?

Thus the payoff to the holder is max{S(T )− K , 0} ≥ 0.

Unlike forward contracts, options cost money. You have to pay thewriter of an option a premium upfront to enter into the contract.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 16 / 30

Call Options

An option gives the holder the right, but not the obligation to buy or sellan asset.

A European call option gives the holder the right to buy an asset S (theunderlying) for an agreed amount K (the strike price or exercise price) ona specified future date T (maturity or expiry).

The party who undertakes to deliver the asset is called the writer ofthe option.

The buyer of a European call would exercise at time T only ifK < S(T ), for a profit of S(T )− K .

If the spot price is less than the strike, the holder would discard theoption: Why pay K if you can pay S(T ) < K ?

Thus the payoff to the holder is max{S(T )− K , 0} ≥ 0.

Unlike forward contracts, options cost money. You have to pay thewriter of an option a premium upfront to enter into the contract.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 16 / 30

Call Options

An option gives the holder the right, but not the obligation to buy or sellan asset.

A European call option gives the holder the right to buy an asset S (theunderlying) for an agreed amount K (the strike price or exercise price) ona specified future date T (maturity or expiry).

The party who undertakes to deliver the asset is called the writer ofthe option.

The buyer of a European call would exercise at time T only ifK < S(T ), for a profit of S(T )− K .

If the spot price is less than the strike, the holder would discard theoption: Why pay K if you can pay S(T ) < K ?

Thus the payoff to the holder is max{S(T )− K , 0} ≥ 0.

Unlike forward contracts, options cost money. You have to pay thewriter of an option a premium upfront to enter into the contract.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 16 / 30

Call Options

An option gives the holder the right, but not the obligation to buy or sellan asset.

A European call option gives the holder the right to buy an asset S (theunderlying) for an agreed amount K (the strike price or exercise price) ona specified future date T (maturity or expiry).

The party who undertakes to deliver the asset is called the writer ofthe option.

The buyer of a European call would exercise at time T only ifK < S(T ), for a profit of S(T )− K .

If the spot price is less than the strike, the holder would discard theoption: Why pay K if you can pay S(T ) < K ?

Thus the payoff to the holder is max{S(T )− K , 0} ≥ 0.

Unlike forward contracts, options cost money. You have to pay thewriter of an option a premium upfront to enter into the contract.

P. Ouwehand (Stellenbosch Univ.) Basic Finance November 2010 16 / 30

More Options

A European put option confers the right to sell an asset S for anagreed amount K at a specified future date T .

Similarly, an American call (put) option confers the right to buy (sell)an asset S for an agreed amount K , but at any time at or beforematurity T .

An Asian option has a payoff that depends on the average stock priceover a certain time period.

A knock–out barrier call will pay the same as a European call, butonly if the underlying asset price hasn’t crossed a predeterminedbarrier level.

The list of examples of derivatives is endless: Interest rate swaps,interest rate caps and floors, forward rate agreements, credit defaultswaps. . .