Analysis and Recommendation By Daniel Timianko HCR ManorCare SpinCo Investment Memorandum 5/16/16 1 Disclosure: This report contains speculative data and forward looking statements. Due to the impending spinoff, some details may be inaccurate and/or changed upon the completion of an initial public offering.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

-

Analysis and Recommendation By Daniel Timianko

HCR ManorCare SpinCo

Investment Memorandum

5/16/16 1

Disclosure: This report contains speculative data and forward looking statements. Due to the impending spinoff, some details may be inaccurate and/or changed upon the completion of an initial public offering.

-

Analysis and Recommendation By Daniel Timianko

EXECUTIVE SUMMARY THE PURPOSE OF THIS INVESTMENT MEMORANDUM IS TO ANALYZE AND OFFER STRATEGIC ADVISORY ON THE PROPOSED SPINOFF OF HCPS HCR MANORCARE PORTFOLIO OF SKILLED NURSING, POST-ACUTE CARE FACILITIES AND SENIOR HOUSING. OVERVIEW On May 9th 2016 HCP announced a plan to spinoff their skilled nursing facilities (SNF), post-acute care facilities (ACF), and select senior housing facilities. The new company, initially organized as a REIT, would own approximately 320 properties with about $485,000,000 of net operating income. Most, if not all, of the spun off assets will be managed by HCR ManorCare. HCP is a healthcare real estate investment trust. It invests in medical office buildings, hospitals, senior housing, life science facilities, and hospitals. HCP holds $23.5bn in real estate investments as of Q4 2015. HCP also participates in debt investments as a senior mortgage lender and as a junior lender. BUSINESS HCPs investment strategy is to raise mostly unsecured debt (92% of Total Debt) to develop and manage properties serving the health care industry nationwide and in the United Kingdom. The growth strategy of HCP lies in internal growth and accretive investments. Constant dividend growth makes HCP a very attractive investment in a low interest rate environment. The dividend can be grown through increasing portfolio NOI internally or acquiring more property to increase total cash flow. In the first quarter of 2016, HCP has spent $335m on developing new property or redeveloping current holdings. None of their CAPEX has been allocated to SNF. Additionally, HCP has acquired $364m of SNF, senior housing, life science, and medical office property this quarter. Maintaining dividend growth will be a challenge if 23% of portfolio NOI will be spun off. However, the combined dividends may continue to grow for yield hungry investors.

5/16/16 2

HCR ManorCare SpinCo

FINANCIAL HIGHLIGHTS HCP has grown to a $26.70 billion market capitalization real estate investment trust.HCPholds a BBB- credit rating, but is in danger of being further downgraded due to the leverage needed for the spinoff. Total debt is 41% of overall capital, leaving equity to be 59% of capital. The HCR ManorCare (HCRMC) portfolio has been challenging for HCP. Over the past 12 months, HCP renegotiated the master lease with HCRMC and impaired $836m of value. The spinoff is clearly a defensive tactic by HCP to insulate itself from further risk from one of its largest operators.

-

Analysis and Recommendation By Daniel Timianko

STOCK INFORMATION HCP has not been performing very successfully when benchmarked against the NAREIT Equity REIT Index. It has underperformed the NAREIT Equity REIT Total Return Index over the past two years. Beta investors, which are a majority of REIT common stock investors would have achieved higher returns by investing their capital in index funds instead of in HCP directly. HIGHLIGHTS HCP exhibited greater volatility than the NAREIT Equity REIT Index in part because of the $836m impairment on HCPs holdings related to HCR Manorcare in 2015. The 2H of 2015 was surprising for HCP investors because of a reported loss in FFO and -7% same store growth in HCPs SNF segment. Being an S&P 500 Dividend Aristocrat implies dividend strength for HCP. Unfortunately their annual dividend growth rate has slowed. After posting 5%, 3.8%, and 3.7% dividend growth in 2013, 2014, and 2015 respectively, 2016s dividend has grown only 1.8%. It is of the highest priority to maintain consistent dividend growth for HCP. Their HCR ManorCare holdings are inhibiting growth.

5/16/16 3

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

HISTORY OF HCP AND HCR MANORCARE

HCP began its relationship with The Carlyle Groups HCR ManorCare through purchasing a subordinate loan from the buyout in 2007 with a face value of $1.0 billion. In August 2009, HCP purchased $720 million of HCRMC senior debt secured by its property portfolio. In December 2010, Carlyle sold 338 SNF, assisted living, and post-acute care facilities for $6.1bn to HCP. This sale included a right to purchase a 9.9% interest in the operating company for $95 million, which HCP exercised.

HCP provided: $3.528bn in cash $1.72bn in reinvested debt held

by HCP $852 million in HCP common

stock

5/16/16 4

HCR ManorCare SpinCo

Upon sale of the portfolio, HCP and HCRMC negotiated a triple net master lease:

Annual rent increases of 3.5% for 5 years, 3% thereafter.

There is one extension option after 13-17 years depending on pool.

Rent increases are fair market value or 3% annual ranging from 10-18 additional years.

On April 1st, 2015 HCP and HCRMC renegotiated their master lease:

HCP reduced annual rent by $68 million to $473 million with contractual increasing 3% annually.

HCRMC transfers fee ownership in 9 new post-acute facilities to HCP. If properties cannot be transferred, HCP will retain a lease receivable of equal value.

HCP receives a lease receivable of $250 million in the event of capital or liquidity events or end of the initial master lease term. The receivable increases 3% annually from 2016-2018, 4% in 2019, 5% in 2020, and 6% from 2021 thereafter.

-

Analysis and Recommendation By Daniel Timianko

OTHER NOTES REGARDING THE HCRMC PORTFOLIO In December 2015, HCP reduced the carrying value of its 9.9% equity interest

in HCRMCs operating business to $0. As part of the Master Lease restructuring in Q1 2015, HCRMC has agreed to

sell 50 non-strategic facilities. As of Q1 2016, 33 facilities have been sold. HCRMC has agreed to sell 9 SNF facilities to HCP for $275m, 7 have closed. HCP has increased its lease receivable by $275m in the form of a deferred

rent obligation in exchange for a reduction in current rent. HCRMC leases are structured as capital leases. The leases can stipulate a

bargain purchase option, long term lease for 75% of economic life of property, or ownership transfer to lessee at end of lease.

5/16/16 5

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

5/16/16 6

76%

24%

Portfolio Mix

CON States

NO CON States

0

10

20

30

40

50

60

SNF

0

2

4

6

8

10

12

Senior Housing

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

HCR ManorCare SpinCo

5/16/16 7

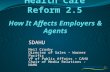

PORTFOLIO COMMENTARY Location Analysis: As illustrated on the previous page, the HCRMC portfolio is separated into two property types. Ohio and Pennsylvania are the two largest markets followed by Florida in senior housing and Michigan for SNF. Very few of the properties are located in high barrier major with above average price appreciation. Chicago, Philadelphia, and Detroit are the top 3 MSAs. Certificate of Need: A certificate of need is a state law that requires new construction of healthcare facilities to only be built when need is determined. The highly regulated nature of these types of facilities allows the established operators to have a higher barrier of entry for newly built facilities. These laws are intended to limit healthcare price inflation. This should help with portfolio occupancy. Leasing: Of the 320 properties being transferred into a separate company, all of them are master-leased by HCR ManorCare. This pools all of the properties into one lease. All of the leases are NNN, meaning the landlord is responsible for little or no property level expenses, insurance, or taxes. Quality: Further research must be done on a property-by-property basis to evaluate the condition of the properties and compare them to replacement cost. The average age of post-acute facilities in HCPs portfolio is 34 years old. Remember that the useful life of commercial property according to the IRS is 39 years. Vacancy: Even though the properties are master-leased by HCR ManorCare, vacancy should be measured by the tenants performance. HCRMCs portfolio wide occupancy is 83.9%. Look nearby for the proper metrics in measuring portfolio performance. HCRs senior housing properties underperform. Fixed Charge Coverage Ratio: As you can see to the right, the EBITDAR fixed charge coverage ratio for HCR is near 1X. This means that HCRMC is in danger of not paying their rent and interest expense this quarter. HCP has renegotiated its master lease to reduce HCRMCs rental obligations. Continued poor performance by HCRMC will lead to further impairment.

Leasing Metrics (12 Months Trailing) EBITDAR: $503.2m EBITDARM: $517.4m EBITDAR FIXED CHARGE COVERAGE RATIO: 1.03X EBITDARM FCCR: 1.06X Senior Housing 1Q Cash NOI: $16.8m Investment:$1.17bn Quarterly Yield: 1.4% Vacancy: 16.1% Portfolio Vacancy (Excluding HCR): 12.5% SNF/Acute Care 1Q Cash NOI: $96.1m Investment: $3.94bn Quarterly Yield: 2.5% Vacancy: 16.4% SNF Portfolio Vacancy (Excluding HCR): 15.8%

-

Analysis and Recommendation By Daniel Timianko

SELECTED FINANCIAL HIGHLIGHTS FROM HCR MANORCARES OPERATIONS ($ in thousands) Q1 2016: Portfolio NOI: $112,988 Occupancy: 83.6% Total Units: 36,966 NOI Growth: (13%) Q1 2015: Portfolio NOI: $130,709 Occupancy: 83.6% Total Units: 36,966 NOI Growth: 3% Q1 2014: Portfolio NOI:$126,539 Occupancy: 84.3% Total Units: 39,724 NOI Growth: (14%) Q1 2013: Portfolio NOI:$144,350 Occupancy: 85.5% Total Units: 41,384

5/16/16 8

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

CONCLUSIONS FROM FINANCIAL AND PORTFOLIO ANALYSIS HCPs investment in HCRMC is very difficult to value considering that HCP holds an equity interest in the operating company while also being a liability on HCRMCs balance sheet. Separating HCP from its holdings in HCRMC better positions HCP to focus on its private pay portfolio and to maintain its identity as a real estate company. The newly spun off company is technically a hybrid between a real estate company and an operating company. Maximizing the value of its real estate holdings will minimize the value of its operating business. However, adding value to the operating business will increase the value of HCRMCs real estate. Establishing an identity for the SpinCo is the number one priority. One metric to be explored is the value of the 9.9% equity interest in HCRMCs operating business. While it was purchased for $95m originally, the value today will help us decide strategic options. HCP has impaired the value of the equity interest in HCRMC to $0. Additionally, HCP impaired $1.3bn related to HCRMC leases. HCRMC assets are valued at $5.1bn currently. Over the next few pages I will analyze the strengths and weaknesses of the proposed SpinCo and then propose some opportunities to create value as well as describe threats facing the new company.

5/16/16 9

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

5/16/16 10

HCR ManorCare SpinCo

SWOT ANALYSIS STRENGTHS HCRMC has a national platform in many high barrier to entry health care markets. HCP trades at a premium to net asset value, making the timing for a spinoff ripe. New SpinCo has a $525m corporate lease receivable in the event of a capital or liquid event.

The receivable increases annually. There is precedence for a skilled nursing/post-acute facility spinoff from Ventas. The new REIT is

called Care Capital Properties. There are strong demographics for senior housing and health care facilities. Baby boomer

retirement will increase demand for properties being spun off. Since HCP uses unsecured debt, the properties being spun off are mostly unencumbered. The single master lease has cross-default protections. WEAKNESSES There are multiple lawsuits pending against HCRMC for improper billing practices. Due to the passage of the Affordable Care Act, many of the patients in the skilled nursing

facilities have migrated to managed care health plans that reimburse less. It is having a significant impact on HCRMCs revenues.

Care Capital Properties has lost significant equity value since its IPO. There will be low investor appetite for a SNF REIT.

HCRMC is struggling to pay its fixed charges. The spinoff is viewed by the public as cut and run by HCP.

-

Analysis and Recommendation By Daniel Timianko

OPPORTUNITIES Opportunity 1: Stabilize and Consolidate The SNF REIT subsector is dominated by Omega Healthcare. There are few other significantly sized pure play SNF REITs. Such a highly dispersed field presents an opportunity for consolidation among some of the smaller REITs. The long term goal of SpinCo can be to grow to the largest SNF pure play REIT by combining with a number of the small/mid cap SNF REITs like CCP or CTRE. This opportunity can precede or succeed stabilization for the SpinCo. If SpinCo can raise capital at a favorable cost, it can diversify through a merger or an acquisition. To receive the best valuation for SpinCo, fixing the current holdings would be preferable. Opportunity 2: Taking an Active Role in Operations The operating entity of HCRMC has seen little success. Revenue has fallen, lawsuits have been filed, leases have been restructured, and confidence is gone. With a 9.9% ownership in the operating entity, SpinCo can assist in the turnaround process. Besides lowering fixed charges, SpinCo can help HCRMC diversify from the reimbursement/managed care sources of revenue to private pay sources. It can introduce cost cutting measures and cull the leases that are not profitable. Since HCRMC is a private company, their financials are not open to the public. Perhaps SpinCo can take a role in restructuring any existing debt that will help HCRMC succeed operationally. Opportunity 2A: Transforming HCRMC In addition to the suggestions in Opportunity 2, SpinCo can enter a joint venture with HCRMC to transform the facilities into higher-end private pay facilities. Many of the risks inherent in managed care will be mitigated or supplemented by private pay facilities in the same location. This opportunity is extremely risky and requires a lot of capital and patience for results. If SpinCos management believes strongly that the status quo will lead to bankruptcy, then this Opportunity may be most logical.

5/16/16 11

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

Opportunity 3: Takeover of HCRMC If SpinCo feels their 9.9% interest in HCRMC will become a liability with current management, then the next round of rent concession negotiations can include a controlling interest in the HCRMC operating entity. This control will allow SpinCo to pursue all strategic options including: a sale, default on leases to vacate properties, cost cutting measures, or merging with another operator. A highest and best use analysis should be explored to search for any hidden value in the properties. Opportunity 4: Passive Stability This strategy recommends further rent concessions and allowing HCRMC the flexibility to fix their business. Taking a passive strategy on the portfolio will be supplemented by an active strategy in making accretive investments in SNF or senior housing properties. The strategy is to diversify away from the HCRMC portfolio. This strategy might cause a conflict of interest with HCP because it will still maintain an interest in SNF. SpinCo and HCP might compete for the same private pay properties for acquisition. THREATS Continued contraction in revenue for HCRMC. Inability to raise funds on a favorable cost of capital basis for new REIT. HCRMC bankruptcy. Increased regulation in the SNF/ACF sector that will decrease profit margins and health ratios. Lawsuits damage HCRMCs brand. Larger macro-economic events that will decrease spending on health care and GDP. Lack of diversity in the portfolio. Pure Play REITs fall out of favor for more diversified and better capitalized REITs. Changes in patient management make SNF and ACF fall out of favor. Changing the use may be

difficult. Long lease maturities.

5/16/16 12

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

HCR ManorCare SpinCo

Recommended Capital Offerings EQUITY The market value of equity has yet to be priced. Pricing it can be reached through comparable analysis in price-to-AFFO or NAV. The most simple comparison is CCP. CCP trades at an 8X multiple. Omega trades at a 10X multiple (projected). HCP currently trades at a 13X multiple. NAV is more of an art and can be assessed post spin when all parts of the capital stack are raised. DEBT SpinCo must raise debt in order to control the costs of capital. Unsecured corporate debt may be cheaper, but it leaves all corporate assets liable in the event of default. However, the initial spin will almost exclusively hold properties under a master lease. So the performance of all properties are connected regardless. Exploring a portfolio-wide debt offering privately may also raise the capital needed. Establishing a credit facility for quick access to capital is important. Also accessing the senior bond market will control the cost of capital. PREFERRED Offering preferred stock may increase investor appetite for SpinCo because of its fixed dividends and low volatility. However, any new equity offering might undervalue SpinCo significantly.

5/16/16 13

60%

30%

10%

0%

Proposed Capital Structure

Common Stock

Mortgage Debt

Credit Facility

Unsecured Debt

-

Analysis and Recommendation By Daniel Timianko

RATIO ANALYSIS When pursuing an initial public offering, management needs to be cognizant of how the rating agencies will issue a credit rating based on certain metrics. The image to the right is a sample of ratio performance for each credit rating. Most REITs aim for an investment grade credit rating of BBB, very few REITs have an A rating. With easy to understand cash flows from the spun off properties, maintaining an investment grade rating depends on raising a conservative amount of debt and growing revenues. The challenge for SpinCo will be to maintain the level of revenue from the HCRMC master lease. The debt capital raised upon becoming public must provide ample returns because the inherited portfolio requires defensive management. The picture to the right should set the goals of performance.

5/16/16 14

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

SECTOR OUTLOOK As a company having a stake in a healthcare operating company and as a healthcare property owner, keeping up with trends in this space is essential. The healthcare economy receives much attention in the media and in government. It is a closely monitored sector because of its cost, ethics, and impact on American families. TRENDS IN SNF/ACF -The Centers for Medicare and Medicaid have increased reimbursements by 2.1% in 2017. -The Affordable Care Act has migrated millions of patients to lower reimbursement managed care plans. -Patients are becoming more dependent on the ADL scale, requiring more attention from nurses. -Long-term care facilities are not covered by Medicare or many private insurers. SNF are an attractive option to control costs. WHAT IS THE COMPETITION SAYING? We remain as bullish as ever on the skilled nursing space. As has been the case for the last 15 years, the skilled operators, who are nimble, talented, sophisticated and committed to quality care, will be able to capitalize on the increasing demand for transparency, quality, data and collaboration with the acute hospitals, managed care organizations, home health providers and other stakeholders in their local markets. David Sedgwick, VP of Operations of CareTrust REIT on Q1 2016 Earnings Call. All of the change in healthcare (are) designed to do two things, improve quality and reduce cost. It is an undisputable fact that there is no lower cost facility based setting than skilled nursing in which to provide high levels of care. A hospital stay can cost anywhere from $2,000 to $4,000 per day versus $500 per days in the skilled nursing facilities. The potential savings in the skilled nursing facility are dramatic and compelling compared with any other portion of the healthcare continue and with advances in technology and care our nursing homes are increasingly able to provide high quality care for more complex post-acute conditions. All of this supports that the demand for skilled nursing services will only continue to increase. So I think there is a lot of good news about the future of the skilled nursing industry which is not getting much (of) your time. -Raymond Lewis, CEO of Care Capital Properties on Q1 2016 Earnings Call

5/16/16 15

HCR ManorCare SpinCo

-

Analysis and Recommendation By Daniel Timianko

Concluding Thoughts With a fully impaired operating business and a below basis property portfolio, the new SpinCo has many challenges ahead. Value can be created in the property portfolio as a result of repairing HCRMCs operating business. The role in which to play should be decided on a thorough understanding of the potential value of HCRMC. HCP has attempted to insulate itself from the issues at HCRMC, but the SpinCo may not have that luxury. With an entire portfolio so intimately connected to one tenant, the fate of the operating business has an outsized impact on the new REIT. The strategies presented, besides Opportunity 3, will be successful if HCRMC returns to profitability. Further analysis of HCRMC is needed to decide whether its poor performance is due to current management or sector risk. From my reading, it seems that there is a place for skilled nursing facilities in the healthcare landscape. In the case of poor management, SpinCo has a strategy to take an active role in the operating business. If the whole sector is falling out of favor, SpinCo will have to transform the use of the portfolio or consolidate with a peer because the basis of the investment in SNF and ACF is extremely overvalued today.

All in all, SpinCo must take a position on its confidence in the current management of HCRMC and the long-term value of SNF/ACF. SpinCo can then act accordingly to create shareholder value.

5/16/16 16

HCR ManorCare SpinCo

Related Documents