Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

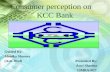

Portfolio 1

Sales

jindalongchul

Oil and Natural Gas Corporation Limited (ONGC)

• Incorporated on 23 June 1993

• A state-owned oil and gas company in India

• It contributes 77% of India‘s crude oil production and 81% of India‘s natural oil production

R S SharmaChairman &

Managing Director

R S SharmaChairman & Managing Director

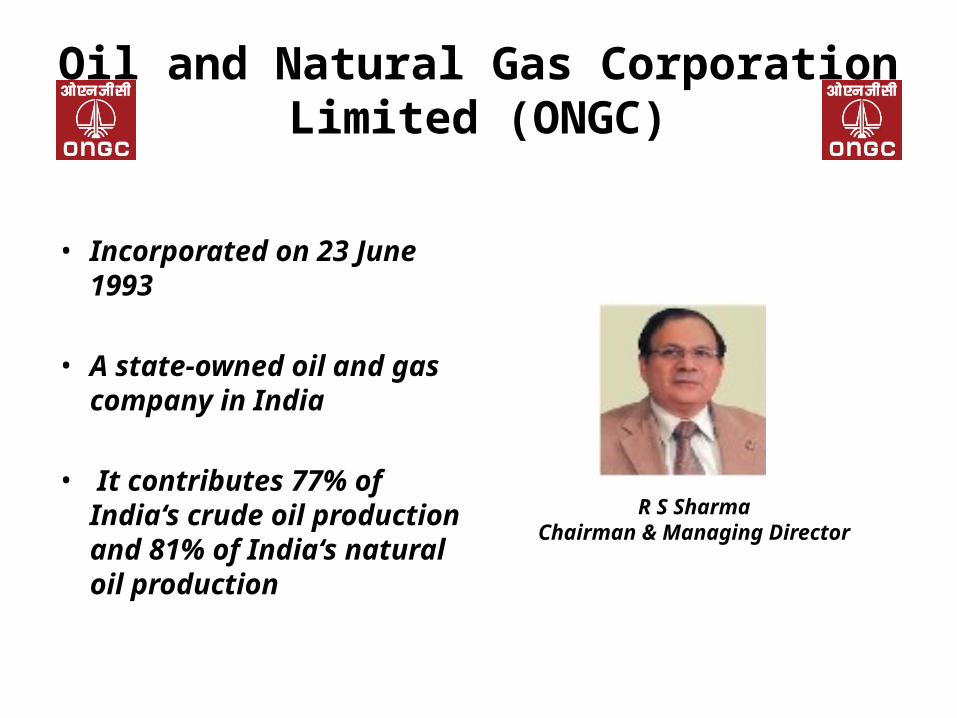

ONGC

Year Market Price Dividend (RS) (%)

2010 1098.5 15 150

2009 779.7 32 320

2008 981.35 32 320

2007 878.15 31 310

2006 864.27 38 380

2005 582.62 45 450

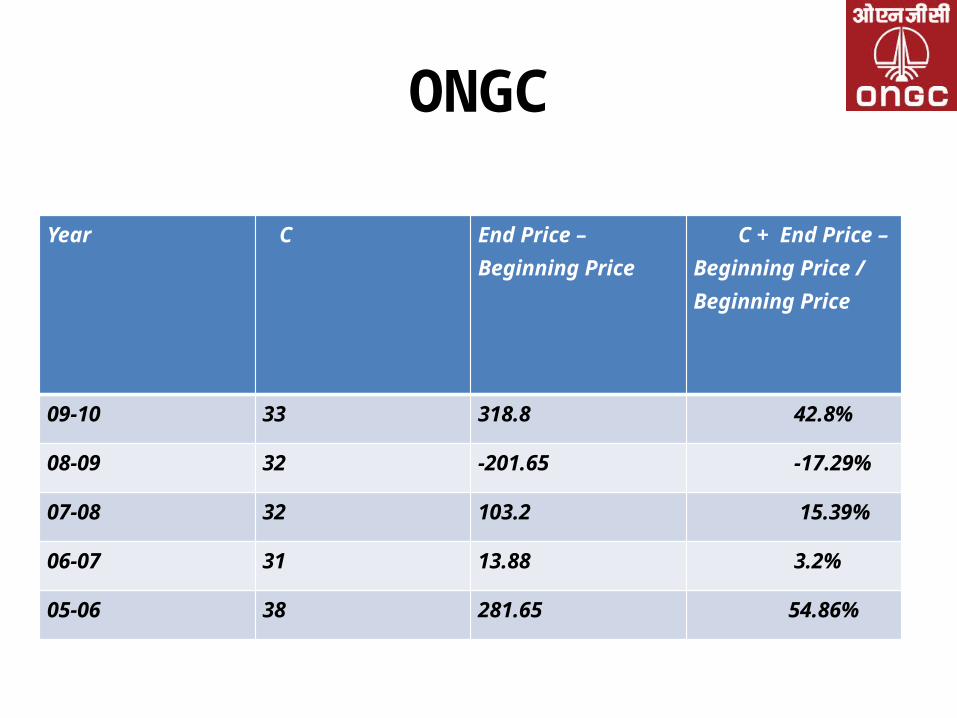

ONGC

Year C End Price – Beginning Price

C + End Price – Beginning Price / Beginning Price

09-10 33 318.8 42.8%

08-09 32 -201.65 -17.29%

07-08 32 103.2 15.39%

06-07 31 13.88 3.2%

05-06 38 281.65 54.86%

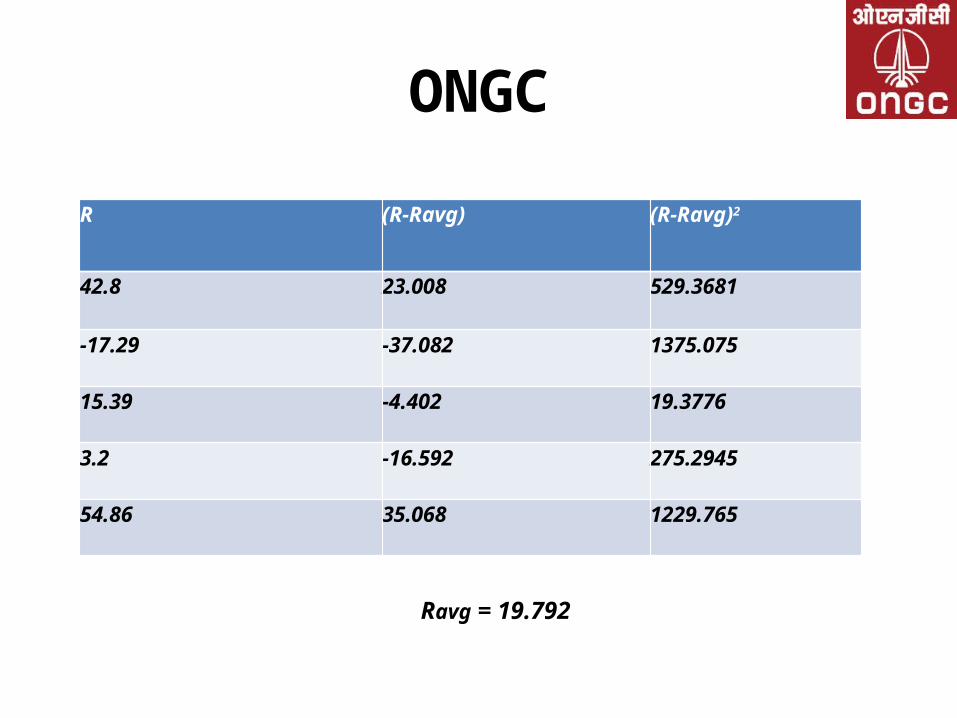

ONGC

R (R-Ravg) (R-Ravg)2

42.8 23.008 529.3681

-17.29 -37.082 1375.075

15.39 -4.402 19.3776

3.2 -16.592 275.2945

54.86 35.068 1229.765

Ravg = 19.792

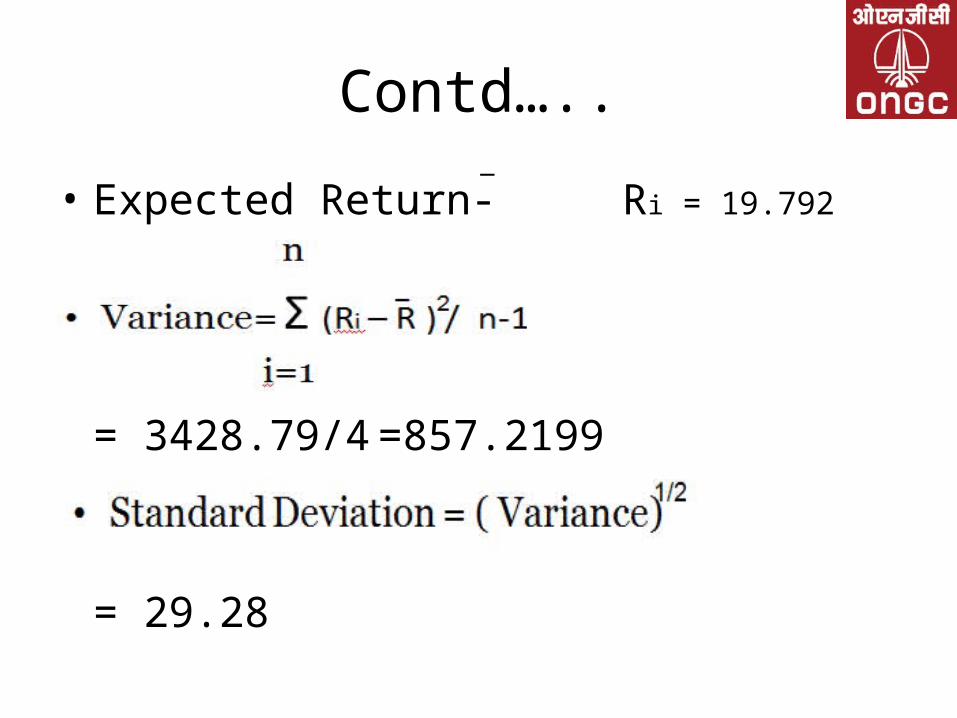

Contd…..

• Expected Return- Ri = 19.792

= 3428.79/4 =857.2199

= 29.28

_

Jindal Steel and Power Ltd.

• Jindal Steel & Power Limited (JSPL) forms a part of the Jindal Group

• Incorporated in 1979

• Expansion Projects in Chattisgarh, jharkhand, Odisha

Mr. Naveen JindalExecutive Vice Chairman & Managing Director

Smt. Savitri JindalChairperson

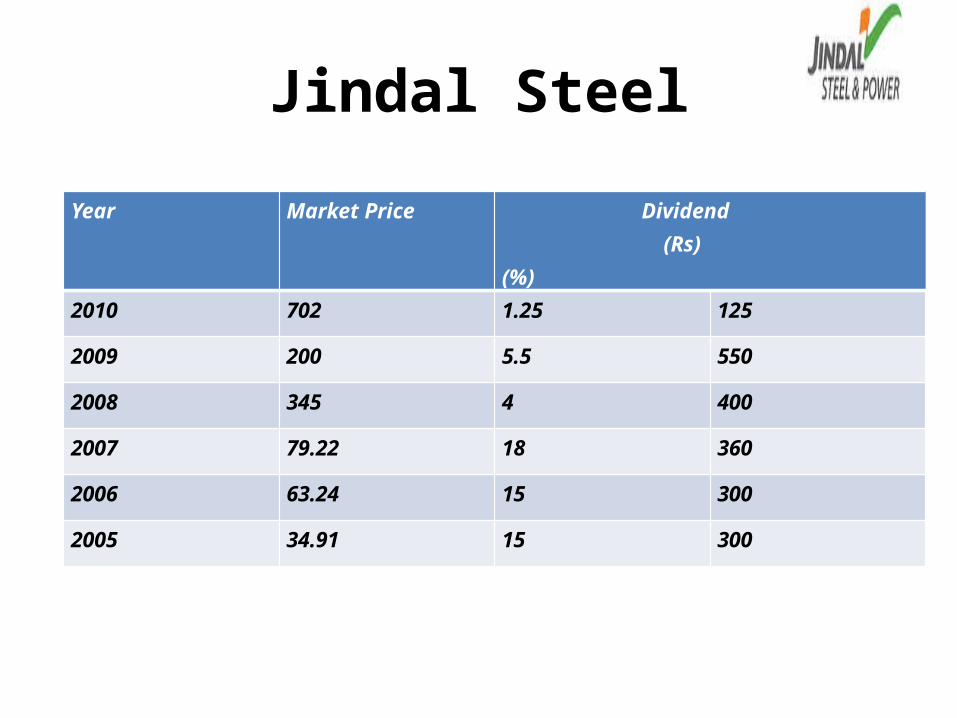

Jindal Steel

Year Market Price Dividend (Rs) (%)

2010 702 1.25 125

2009 200 5.5 550

2008 345 4 400

2007 79.22 18 360

2006 63.24 15 300

2005 34.91 15 300

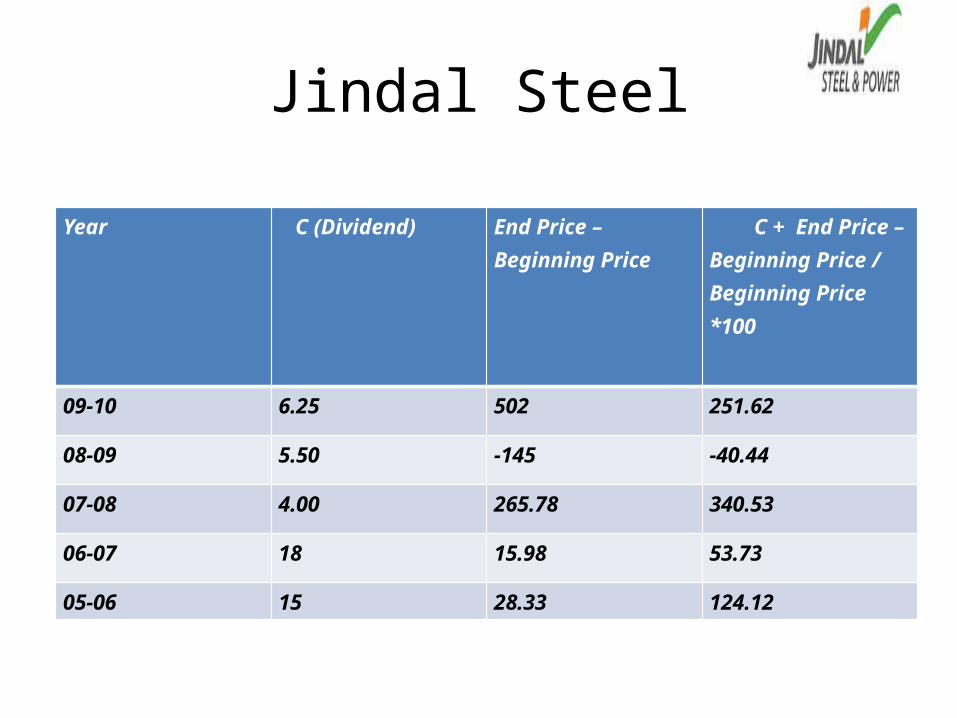

Jindal Steel

Year C (Dividend) End Price – Beginning Price

C + End Price – Beginning Price / Beginning Price *100

09-10 6.25 502 251.62

08-09 5.50 -145 -40.44

07-08 4.00 265.78 340.53

06-07 18 15.98 53.73

05-06 15 28.33 124.12

Jindal Steel

R (R-Ravg) (R-Ravg)2

251.62 105.72 11176.72

-40.44 -186.34 34722.6

340.53 194.63 37880.84

53.73 -92.17 8495.31

124.12 -21.78 474.37

Ravg = 145.912

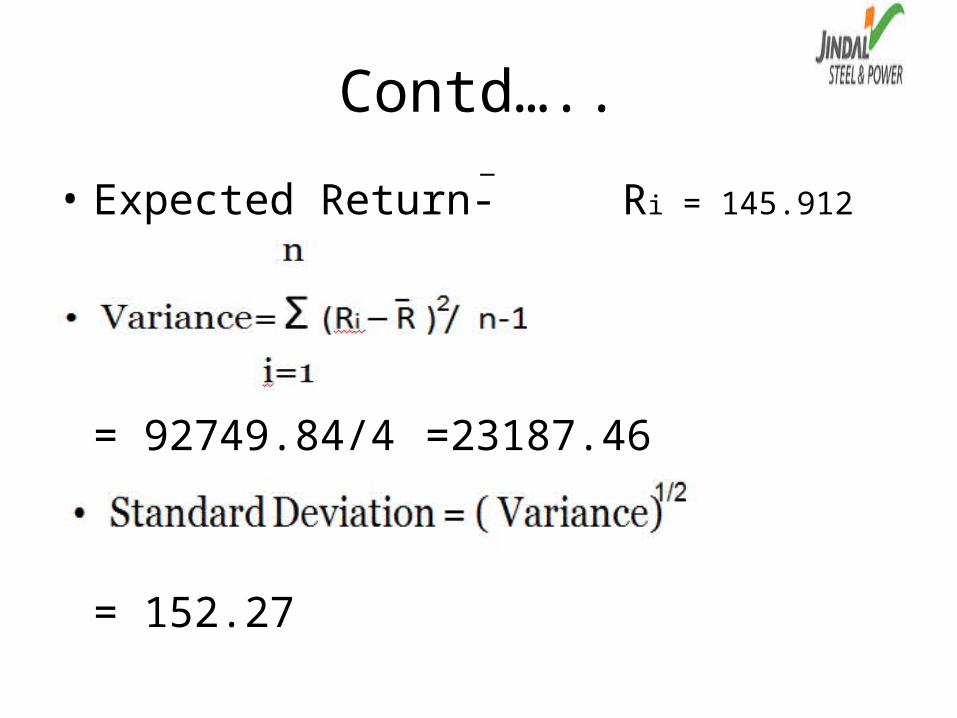

Contd…..

• Expected Return- Ri = 145.912

= 92749.84/4 =23187.46

= 152.27

_

Hindustan Unilever Limited

• HUL is Founded in 1933

• HUL is India's largest Fast Moving Consumer GoodsCompany

• Touching the lives of two out of three Indians with over 20 distinct categories

Mr. Nitin Paranjpe – CEO and Managing Director

Mr. Harish Manwani – Chairman

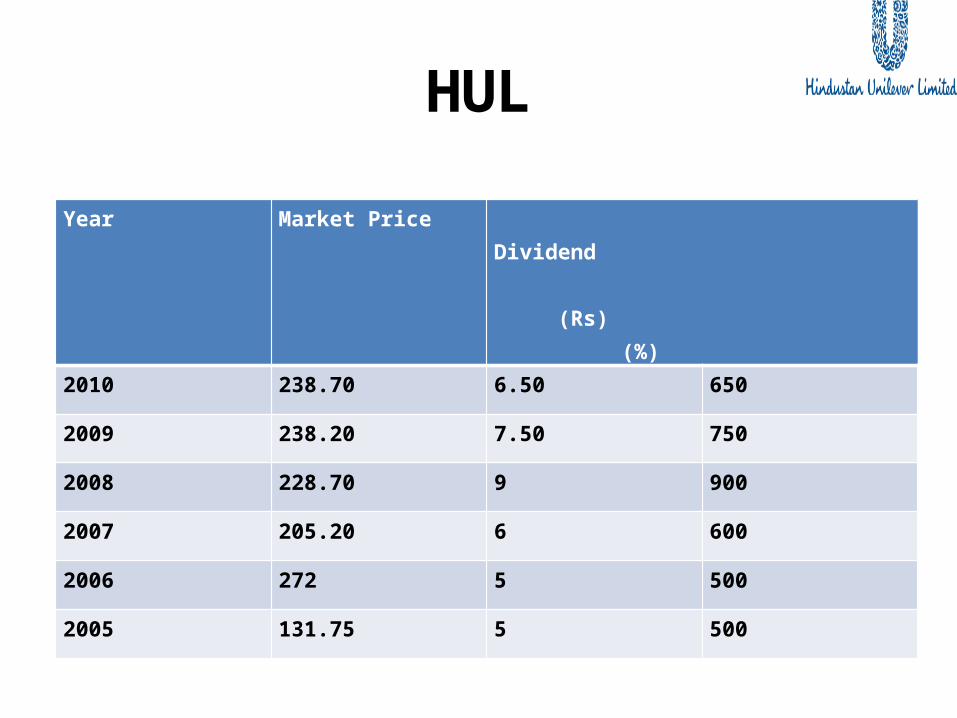

HUL

Year Market Price Dividend (Rs) (%)

2010 238.70 6.50 650

2009 238.20 7.50 750

2008 228.70 9 900

2007 205.20 6 600

2006 272 5 500

2005 131.75 5 500

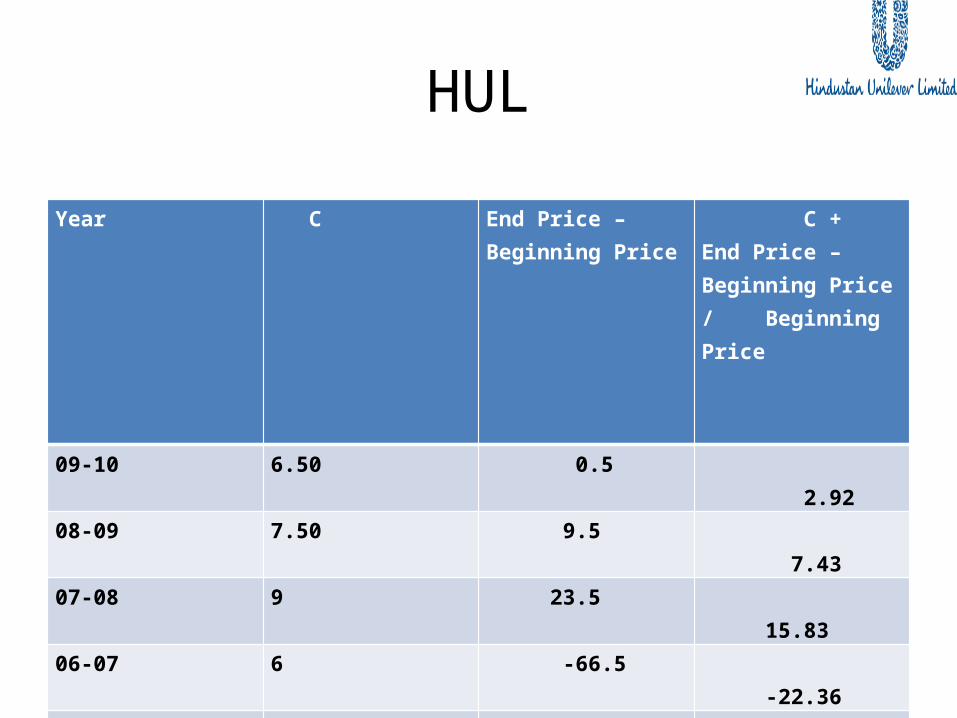

HUL

Year C End Price – Beginning Price

C + End Price – Beginning Price / Beginning Price

09-10 6.50 0.5 2.92

08-09 7.50 9.5 7.43

07-08 9 23.5 15.83

06-07 6 -66.5 -22.36

05-06 5 140.25 110.24

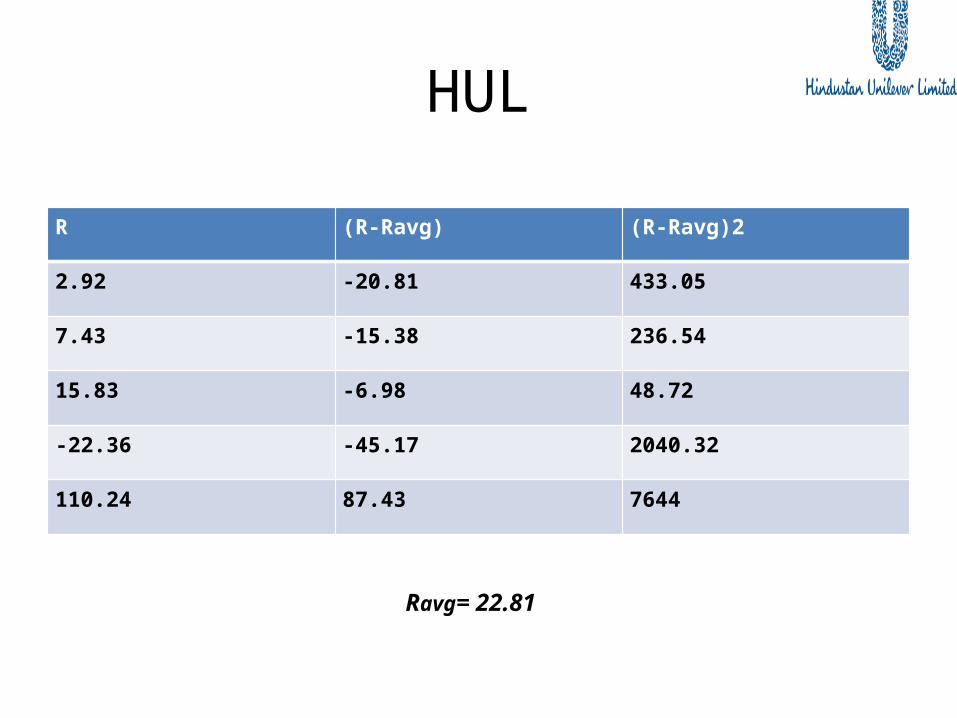

HUL

R (R-Ravg) (R-Ravg)2

2.92 -20.81 433.05

7.43 -15.38 236.54

15.83 -6.98 48.72

-22.36 -45.17 2040.32

110.24 87.43 7644

Ravg= 22.81

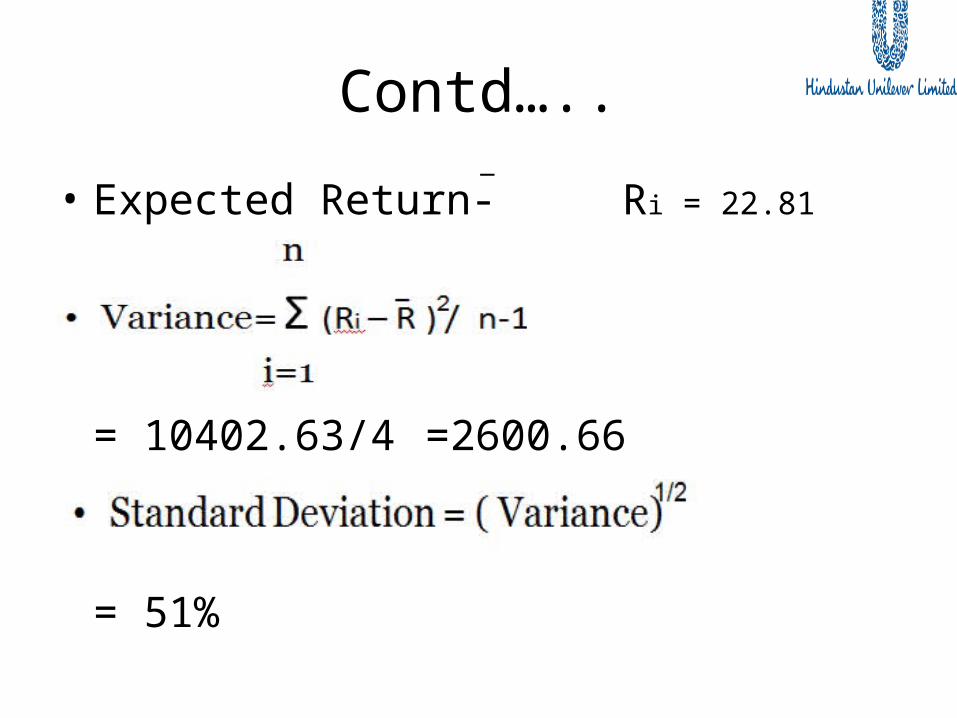

Contd…..

• Expected Return- Ri = 22.81

= 10402.63/4 =2600.66

= 51%

_

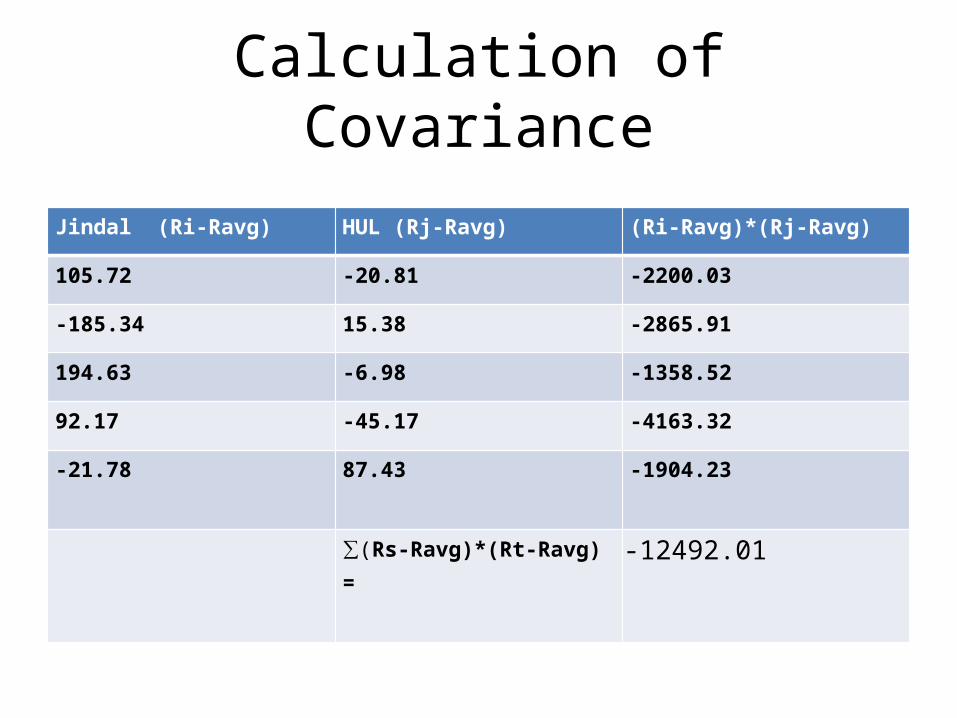

Calculation of Covariance

Jindal (Ri-Ravg) HUL (Rj-Ravg) (Ri-Ravg)*(Rj-Ravg)

105.72 -20.81 -2200.03

-185.34 15.38 -2865.91

194.63 -6.98 -1358.52

92.17 -45.17 -4163.32

-21.78 87.43 -1904.23

∑(Rs-Ravg)*(Rt-Ravg) = -12492.01

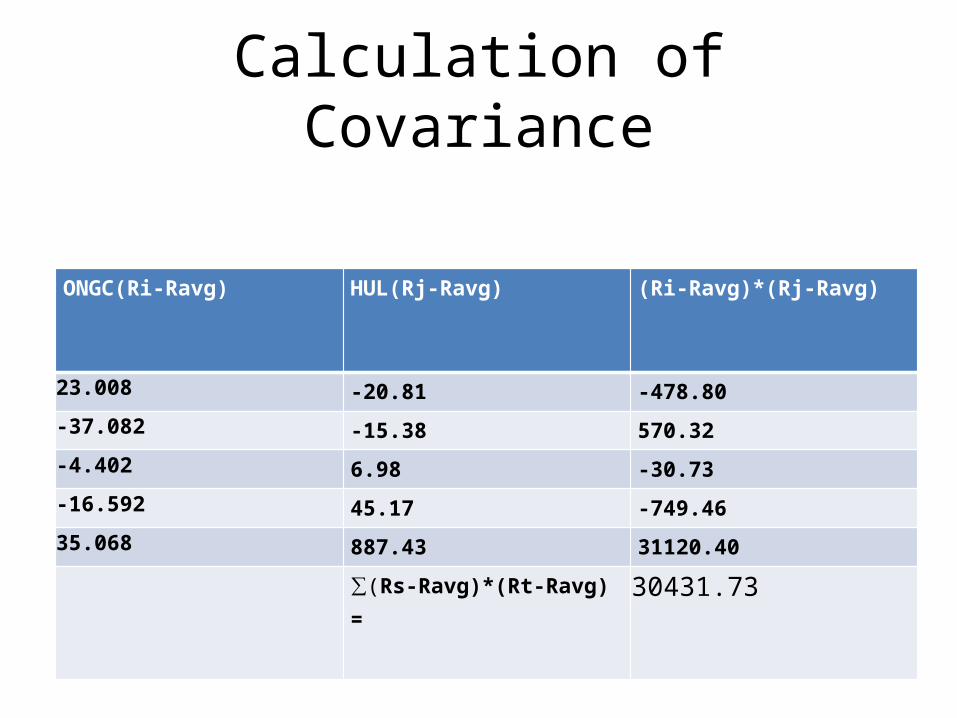

Calculation of Covariance

ONGC(Ri-Ravg) HUL(Rj-Ravg) (Ri-Ravg)*(Rj-Ravg)

23.008 -20.81 -478.80

-37.082 -15.38 570.32

-4.402 6.98 -30.73

-16.592 45.17 -749.46

35.068 887.43 31120.40

∑(Rs-Ravg)*(Rt-Ravg) = 30431.73

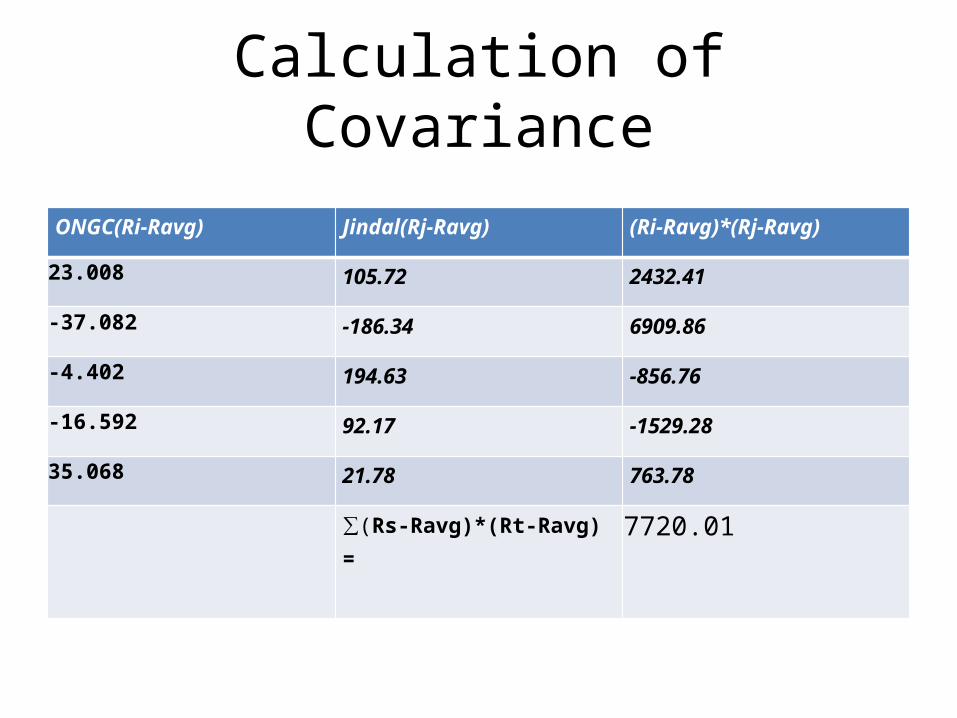

Calculation of Covariance

ONGC(Ri-Ravg) Jindal(Rj-Ravg) (Ri-Ravg)*(Rj-Ravg)

23.008 105.72 2432.41

-37.082 -186.34 6909.86

-4.402 194.63 -856.76

-16.592 92.17 -1529.28

35.068 21.78 763.78

∑(Rs-Ravg)*(Rt-Ravg) = 7720.01

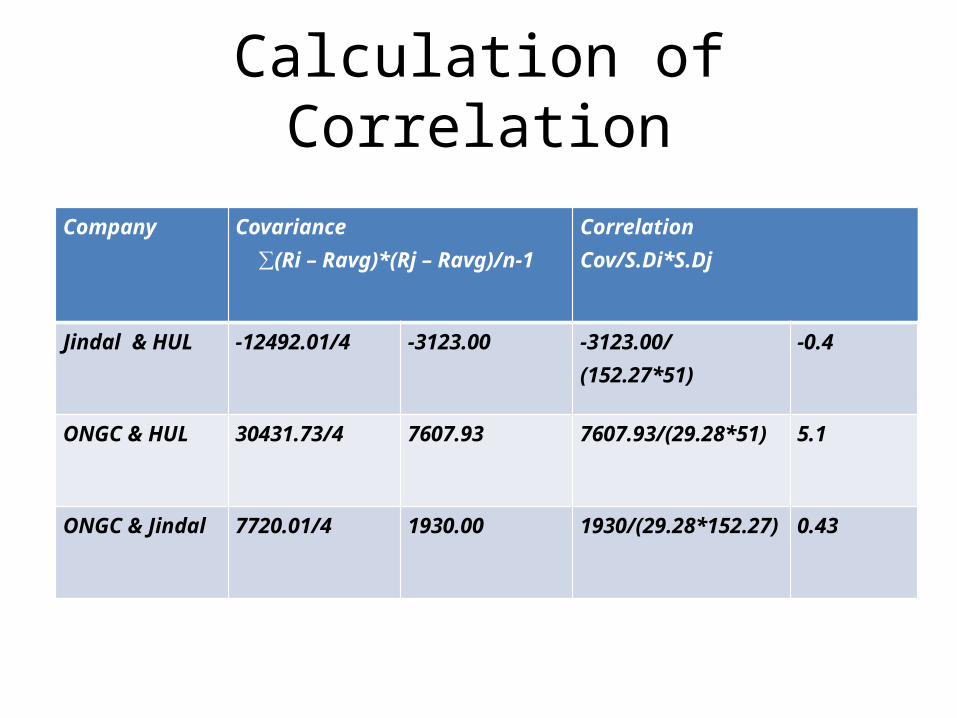

Calculation of Correlation

Company Covariance ∑(Ri – Ravg)*(Rj – Ravg)/n-1

Correlation Cov/S.Di*S.Dj

Jindal & HUL -12492.01/4 -3123.00 -3123.00/(152.27*51) -0.4

ONGC & HUL 30431.73/4 7607.93 7607.93/(29.28*51) 5.1

ONGC & Jindal 7720.01/4 1930.00 1930/(29.28*152.27) 0.43

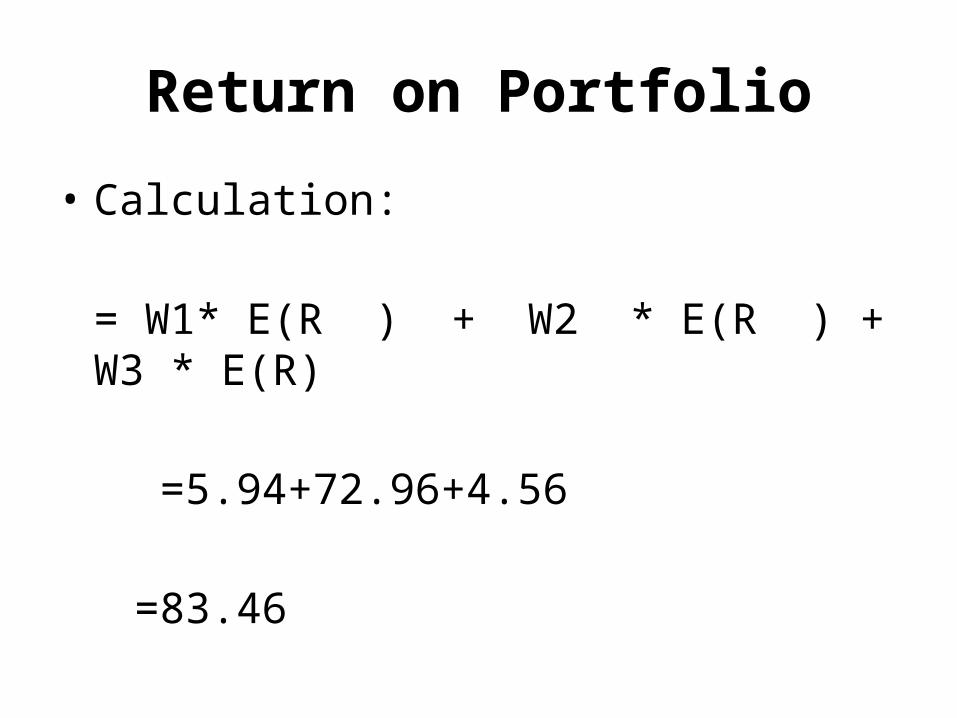

Return on Portfolio

• Calculation:

= W1* E(R ) + W2 * E(R ) + W3 * E(R)

=5.94+72.96+4.56

=83.46

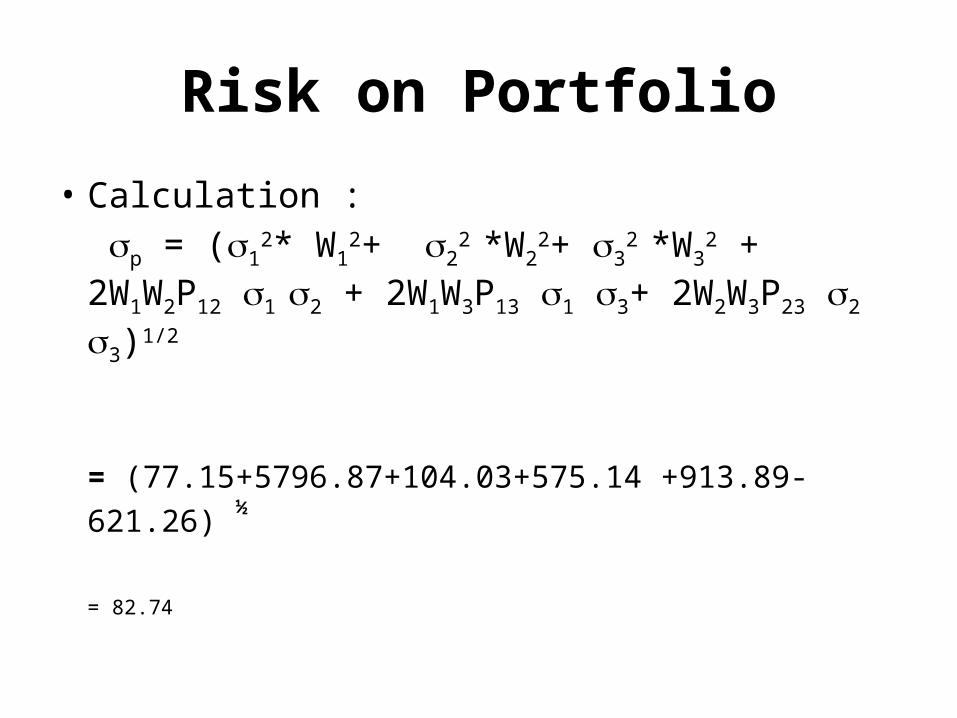

Risk on Portfolio

• Calculation : p = (1

2* W12+ 2

2 *W22+ 3

2 *W32 + 2W1W2P12

1 2 + 2W1W3P13 1 3+ 2W2W3P23 2 3)1/2

= (77.15+5796.87+104.03+575.14 +913.89-621.26) ½

= 82.74

Portfolio 2

• Reliance Capital Limited (RCL) is a Non-Banking Financial Company

(NBFC)

• RCL has a net worth of over Rs ‘8000 crore and over 165,000'

shareholders.

• It is headed by Anil Ambani and is a part of the Reliance ADA Group.

• Reliance Capital ranks among the top 3 private sector financial services and

banking companies, in terms of net worth.

• Reliance Capital has interests in asset management and mutual funds, life

and general insurance, private equity and proprietary investments, stock

broking, depository services, distribution of financial products, consumer

finance and other activities in financial services.

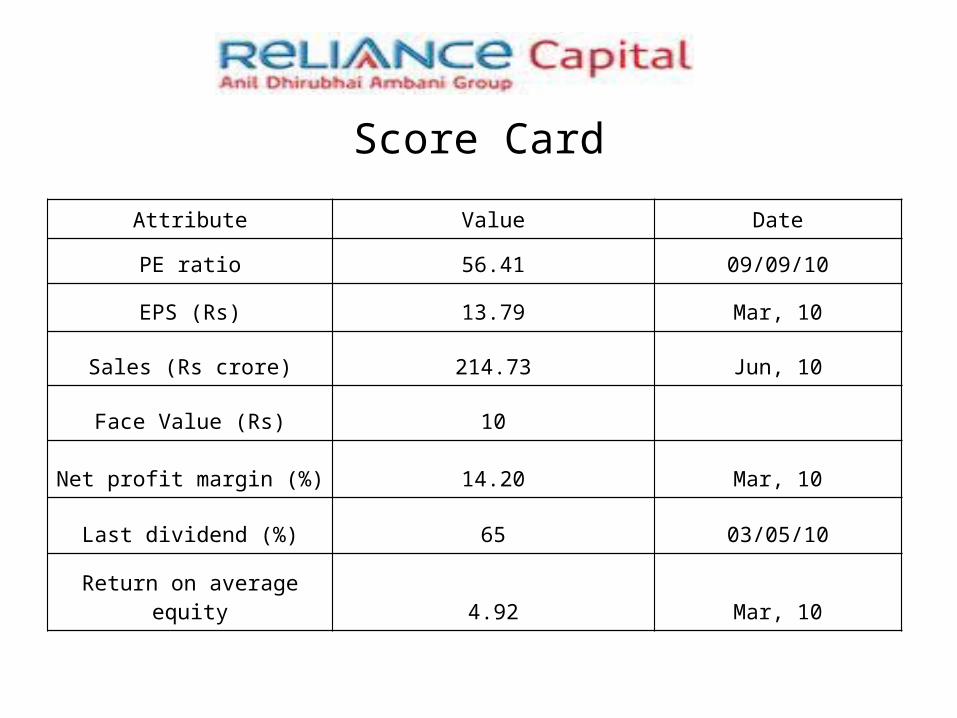

Attribute Value Date

PE ratio 56.41 09/09/10

EPS (Rs) 13.79 Mar, 10

Sales (Rs crore) 214.73 Jun, 10

Face Value (Rs) 10

Net profit margin (%) 14.20 Mar, 10

Last dividend (%) 65 03/05/10

Return on average equity 4.92 Mar, 10

Score Card

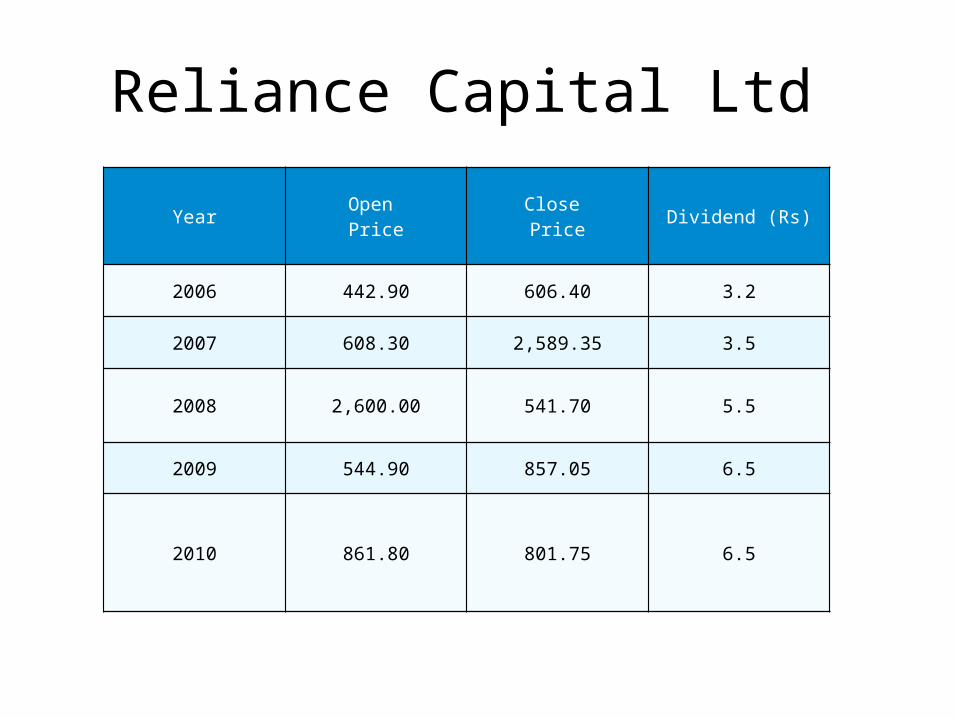

Reliance Capital Ltd

Year Open Price

Close Price Dividend (Rs)

2006 442.90 606.40 3.2

2007 608.30 2,589.35 3.5

2008 2,600.00 541.70 5.5

2009 544.90 857.05 6.5

2010 861.80 801.75 6.5

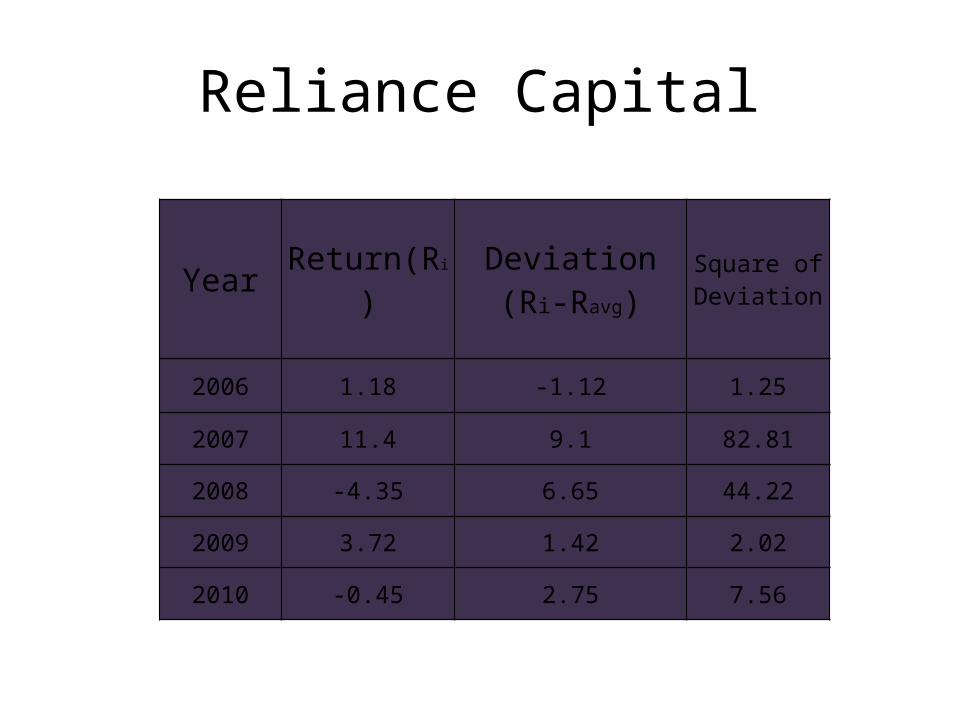

Reliance Capital

Year Return(Ri) Deviation(Ri-Ravg)

Square of Deviation

2006 1.18 -1.12 1.25

2007 11.4 9.1 82.81

2008 -4.35 6.65 44.22

2009 3.72 1.42 2.02

2010 -0.45 2.75 7.56

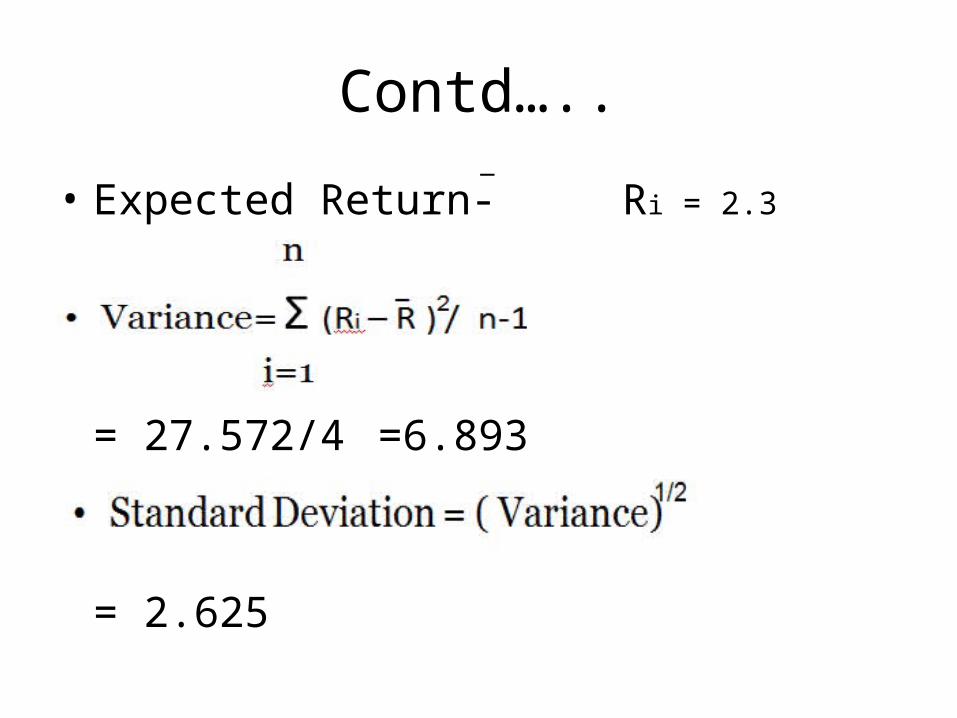

Contd…..

• Expected Return- Ri = 2.3

= 27.572/4 =6.893

= 2.625

_

• Type- Public. Founded-1945.

• Founder(s) JRD Tata

• Headquarters Mumbai, Maharashtra, India

• Key people Ratan Tata, Chairman

Ravi Kant, Vice Chairman

• Revenue $14.250 billion (2009)

• Operating income $10.40 billion

• Net income $1.198 billion

• Total assets $15.430 billion

• Total equity $763 million

• Parent Tata Group Subsidiaries- Jaguar, Land Rover, TDCV Hispano

Carrocera.

Tata Motors Ltd.

Tata Motors Ltd

Attribute Value DatePE ratio 26.14 13/09/10EPS (Rs) 39.26 Mar, 10

Sales (Rs crore) 10,416.26 Jun, 10Face Value (Rs) 10

Net profit margin (%) 6.28 Mar, 10

Last bonus 3:5 28/09/95Last dividend (%) 150 27/05/10

Return on average equity 14.96 Mar, 10

Score Card

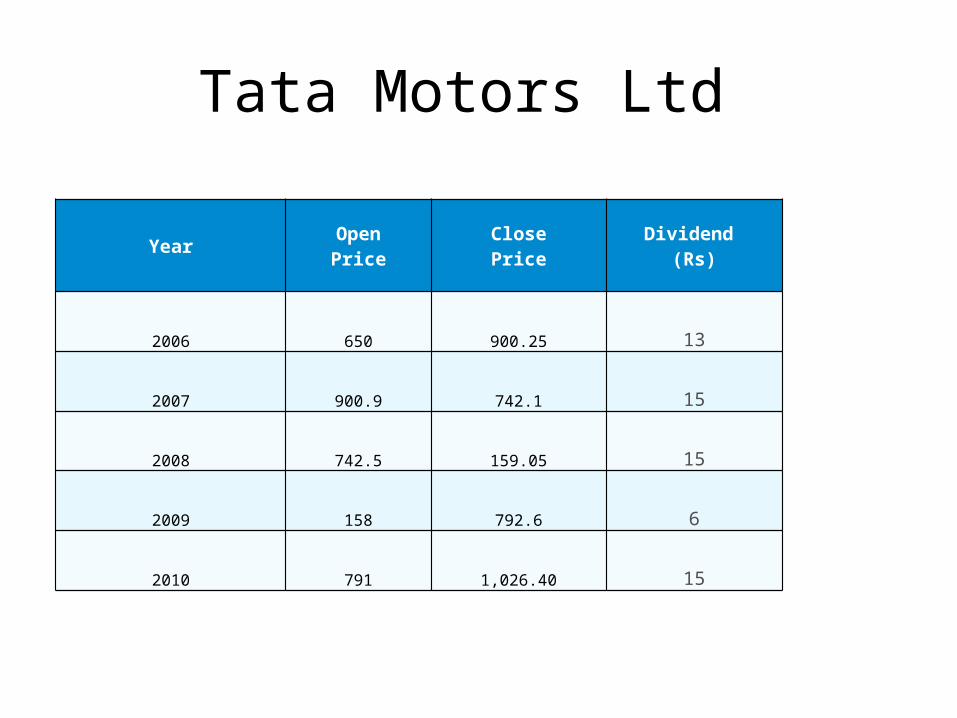

Tata Motors Ltd

Year OpenPrice

ClosePrice

Dividend (Rs)

2006 650 900.25 13

2007 900.9 742.1 15

2008 742.5 159.05 15

2009 158 792.6 6

2010 791 1,026.40 15

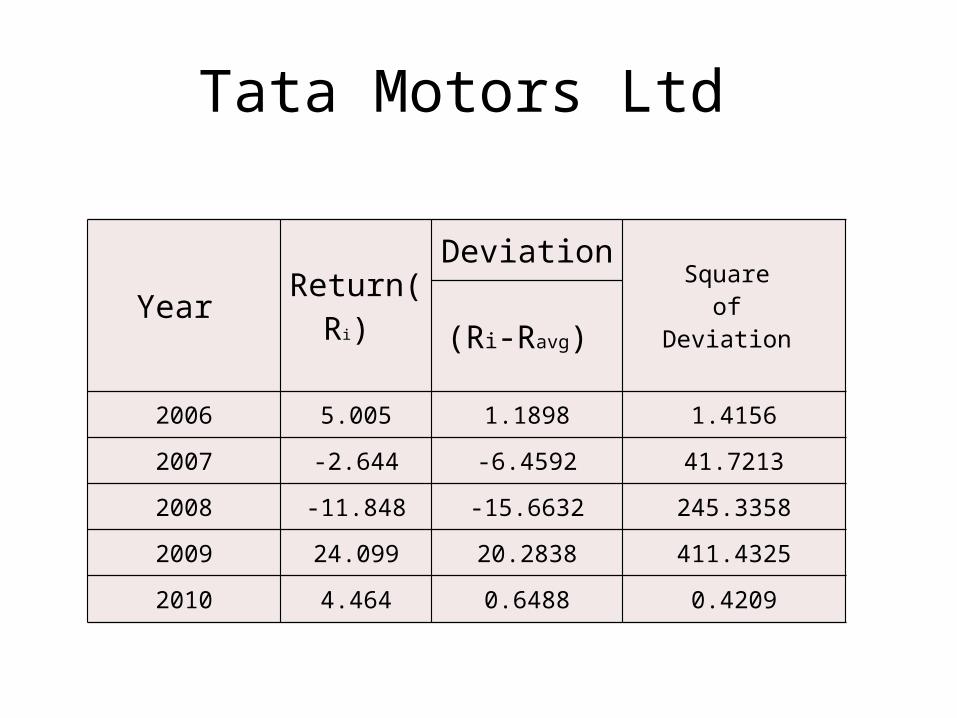

Tata Motors Ltd

Year Return(Ri)

DeviationSquare

of Deviation (Ri-Ravg)

2006 5.005 1.1898 1.4156

2007 -2.644 -6.4592 41.7213

2008 -11.848 -15.6632 245.3358

2009 24.099 20.2838 411.4325

2010 4.464 0.6488 0.4209

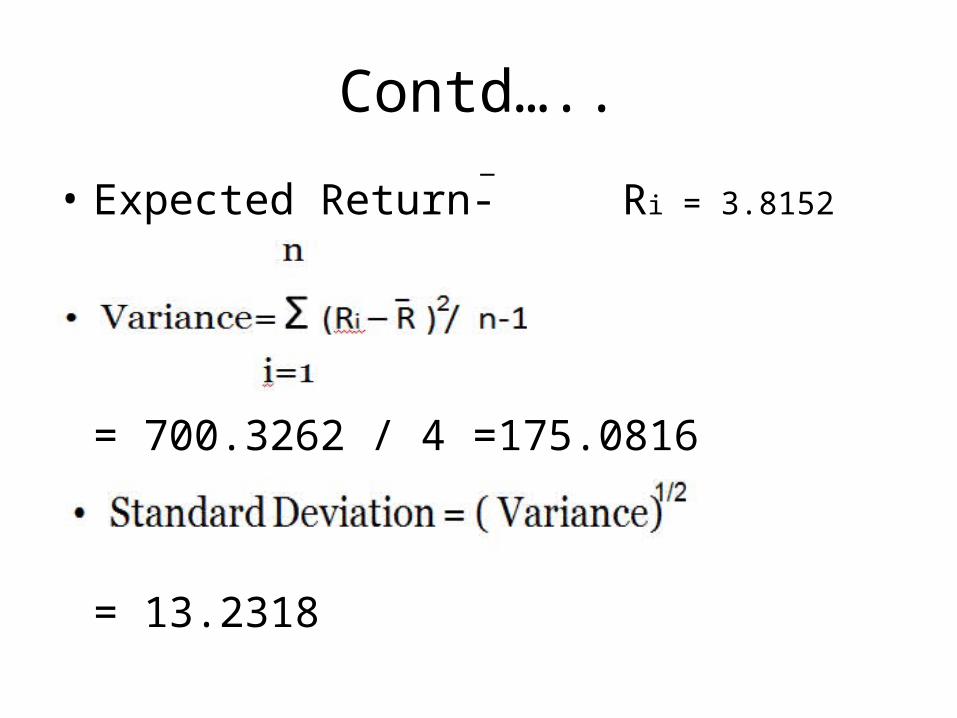

Contd…..

• Expected Return- Ri = 3.8152

= 700.3262 / 4=175.0816

= 13.2318

_

• Founded on April 5, 1974

• This group has grown to become a major player in the Financial Services

space.

• It was founded by 3 people. Mr. R. Thyagarajan, Mr. AVS Raja and Mr. T.

Jayaraman.

• Helping Create Wealth. Empowering people through prosperity. The

relentless pursuit of this mission, since their inception in 1974 has given the

Shriram Group their raison d'être and our distinct identity.

• The Group’s reputation for effectiveness, transparency and integrity has

helped it to become one of India’s largest Financial Services Network.

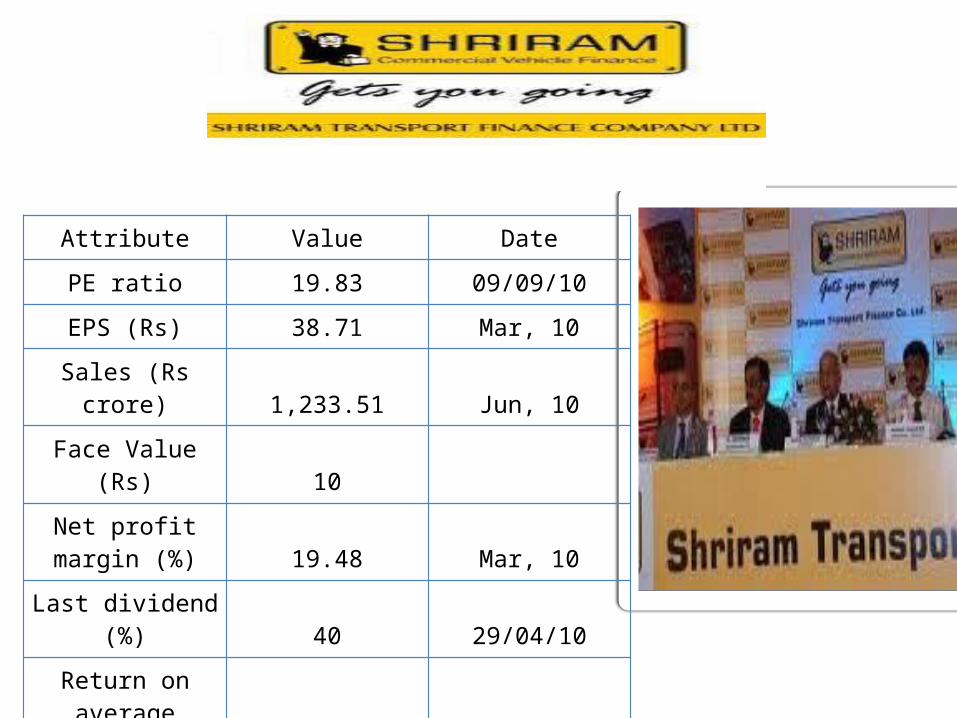

Attribute Value DatePE ratio 19.83 09/09/10EPS (Rs) 38.71 Mar, 10

Sales (Rs crore) 1,233.51 Jun, 10Face Value (Rs) 10

Net profit margin (%) 19.48 Mar, 10

Last dividend (%) 40 29/04/10Return on average

equity 22.99 Mar, 10

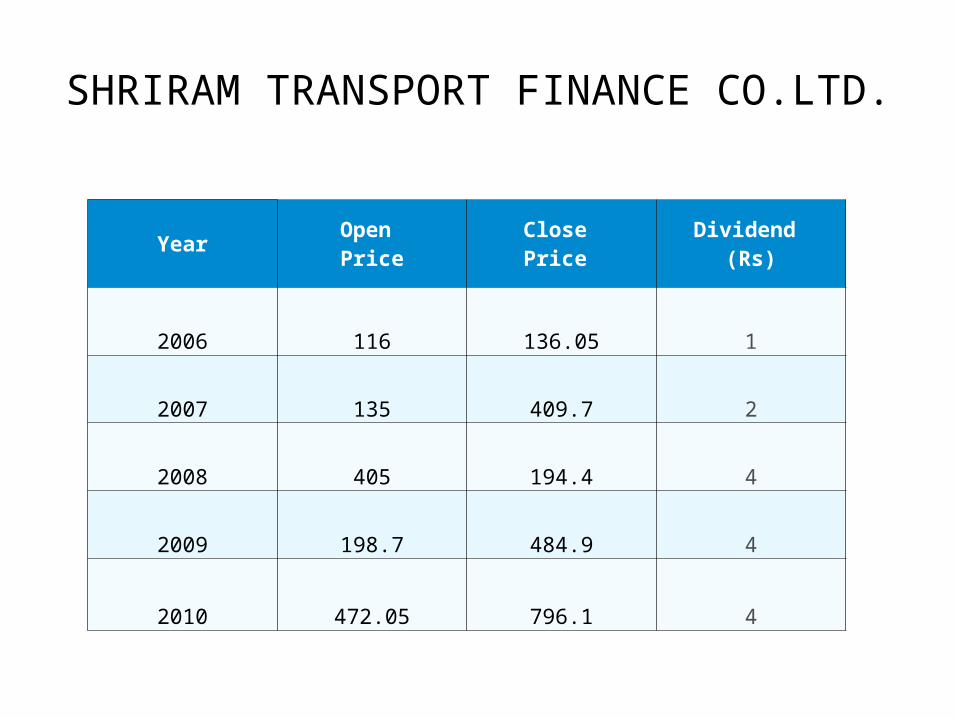

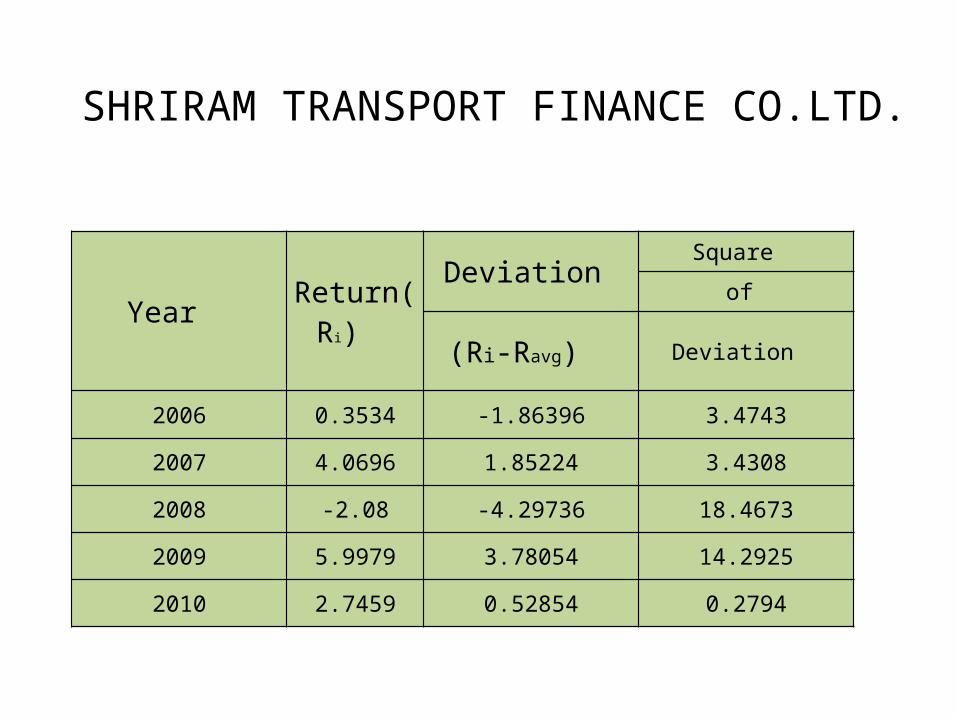

SHRIRAM TRANSPORT FINANCE CO.LTD.

Year Open Price

Close Price

Dividend (Rs)

2006 116 136.05 1

2007 135 409.7 2

2008 405 194.4 4

2009 198.7 484.9 4

2010 472.05 796.1 4

Year Return(Ri) Deviation Square

of

(Ri-Ravg) Deviation

2006 0.3534 -1.86396 3.4743

2007 4.0696 1.85224 3.4308

2008 -2.08 -4.29736 18.4673

2009 5.9979 3.78054 14.2925

2010 2.7459 0.52854 0.2794

SHRIRAM TRANSPORT FINANCE CO.LTD.

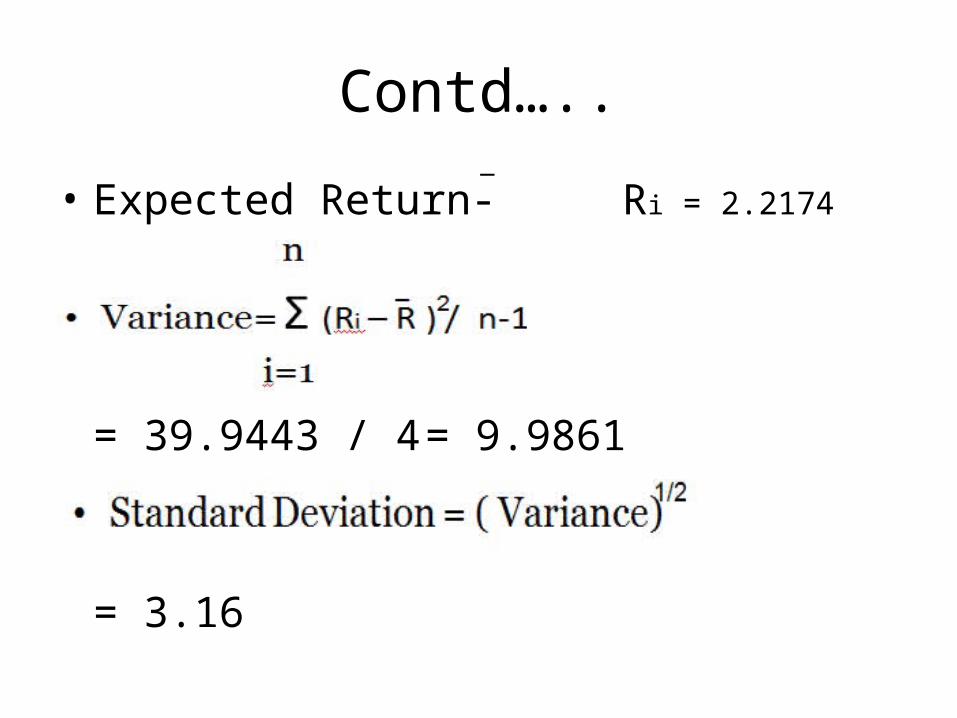

Contd…..

• Expected Return- Ri = 2.2174

= 39.9443 / 4 = 9.9861

= 3.16

_

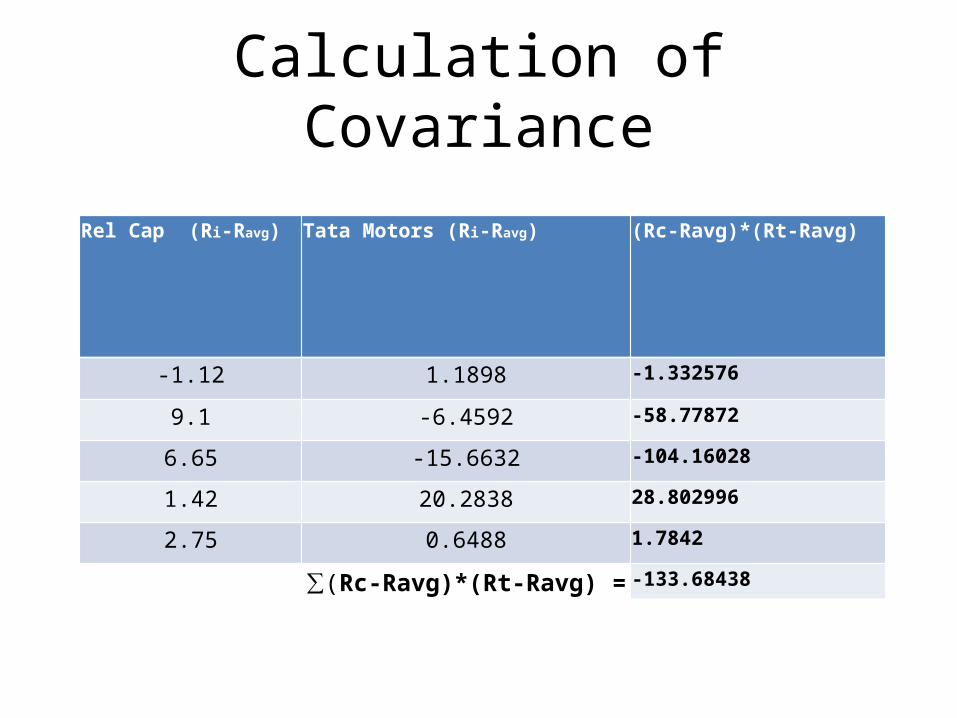

Calculation of Covariance

Rel Cap (Ri-Ravg) Tata Motors (Ri-Ravg) (Rc-Ravg)*(Rt-Ravg)

-1.12 1.1898 -1.332576

9.1 -6.4592 -58.77872

6.65 -15.6632 -104.16028

1.42 20.2838 28.802996

2.75 0.6488 1.7842

∑(Rc-Ravg)*(Rt-Ravg) = -133.68438

Calculation of Covariance

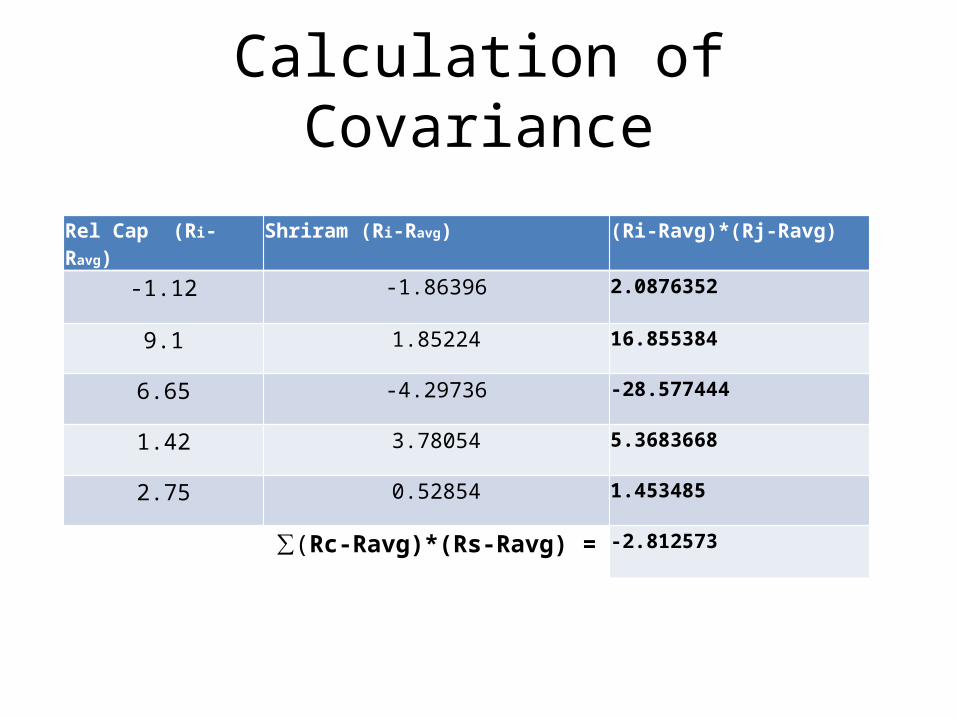

Rel Cap (Ri-Ravg) Shriram (Ri-Ravg) (Ri-Ravg)*(Rj-Ravg)

-1.12 -1.86396 2.0876352

9.1 1.85224 16.855384

6.65 -4.29736 -28.577444

1.42 3.78054 5.3683668

2.75 0.52854 1.453485

∑(Rc-Ravg)*(Rs-Ravg) = -2.812573

Calculation of Covariance

Shriram (Ri-Ravg) Tata Motors (Ri-Ravg) (Rs-Ravg)*(Rt-Ravg)

-1.86396 1.1898 -2.217739608

1.85224 -6.4592 -11.96398861

-4.29736 -15.6632 67.31040915

3.78054 20.2838 76.68371725

0.52854 0.6488 0.342916752

∑(Rs-Ravg)*(Rt-Ravg) = 130.1553149

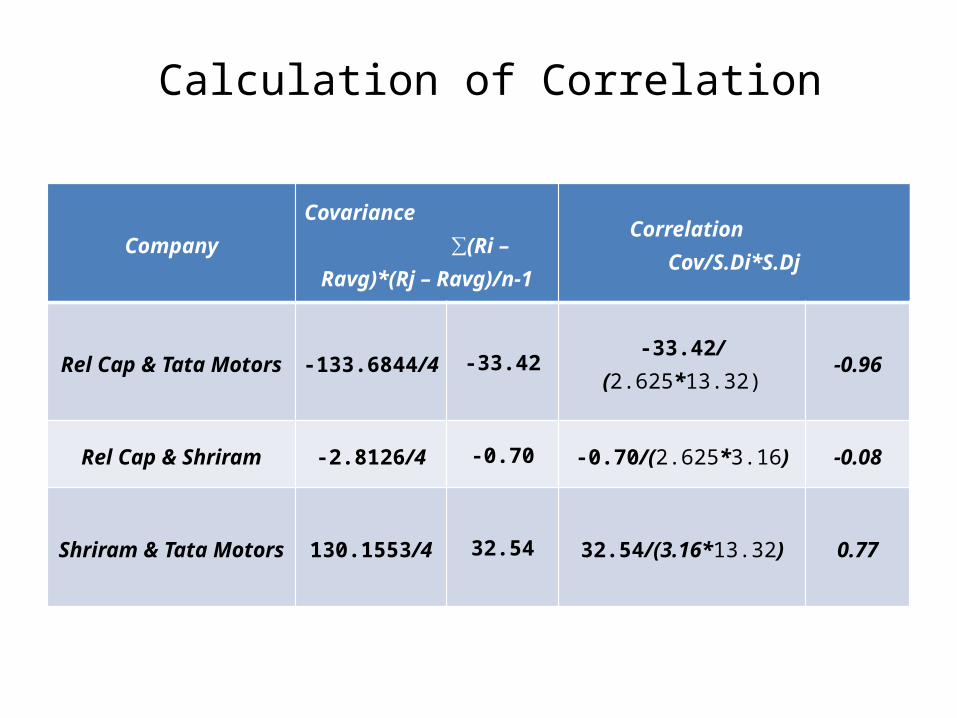

CompanyCovariance ∑(Ri – Ravg)*(Rj –

Ravg)/n-1Correlation Cov/S.Di*S.Dj

Rel Cap & Tata Motors -133.6844/4 -33.42 -33.42/(2.625*13.32) -0.96

Rel Cap & Shriram -2.8126/4 -0.70 -0.70/(2.625*3.16) -0.08

Shriram & Tata Motors 130.1553/4 32.54 32.54/(3.16*13.32) 0.77

Calculation of Correlation

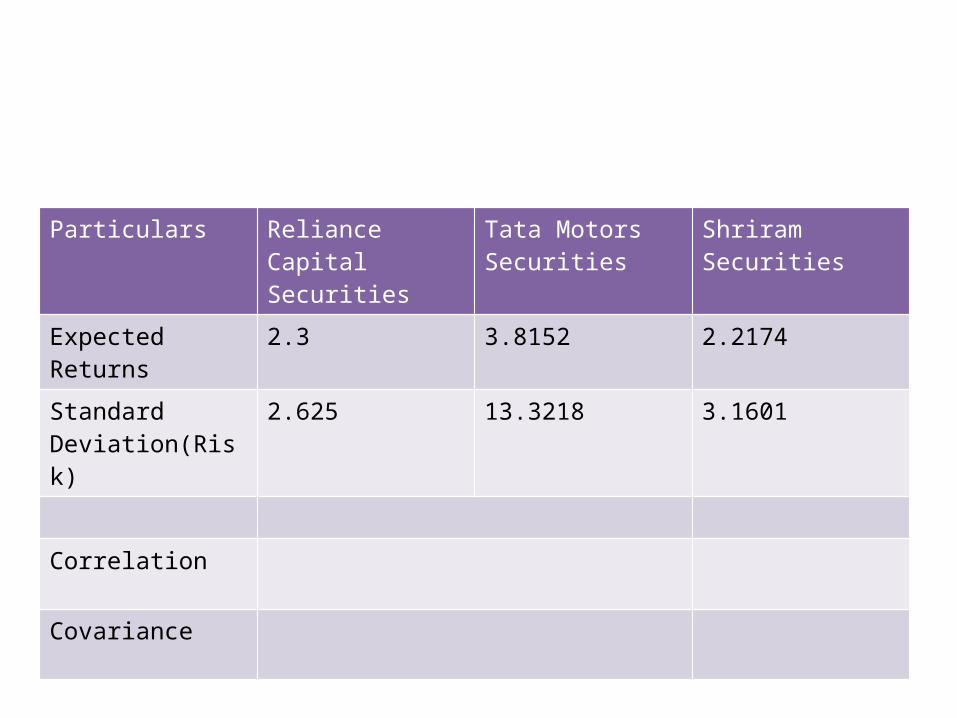

Particulars Reliance Capital Securities

Tata Motors Securities

Shriram Securities

Expected Returns 2.3 3.8152 2.2174

Standard Deviation(Risk)

2.625 13.3218 3.1601

Correlation

Covariance

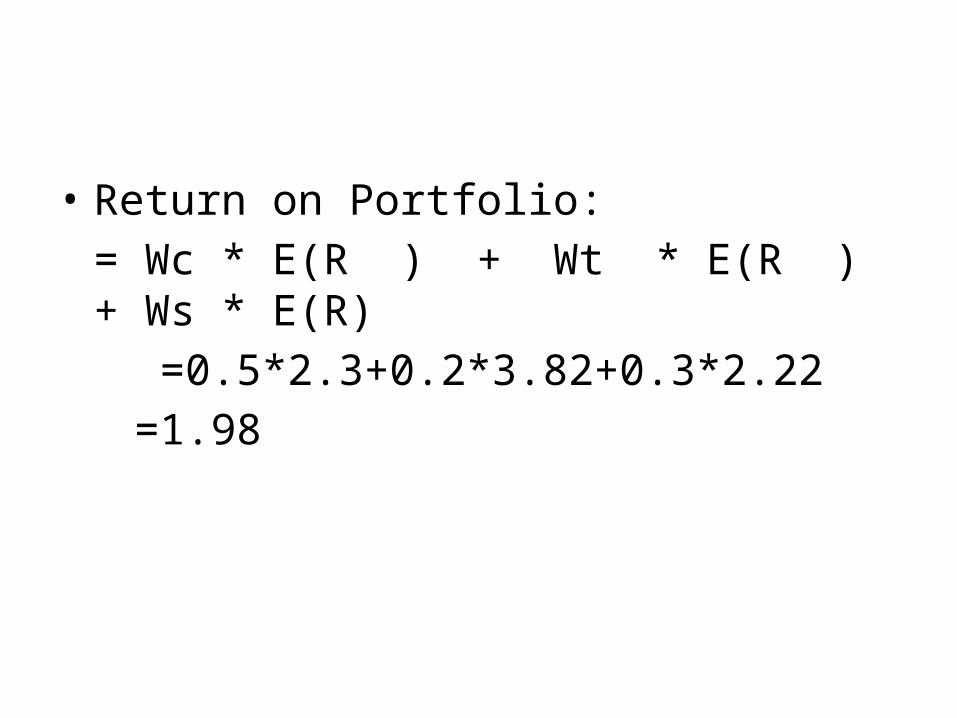

• Return on Portfolio:= Wc * E(R ) + Wt * E(R ) + Ws * E(R)

=0.5*2.3+0.2*3.82+0.3*2.22 =1.98

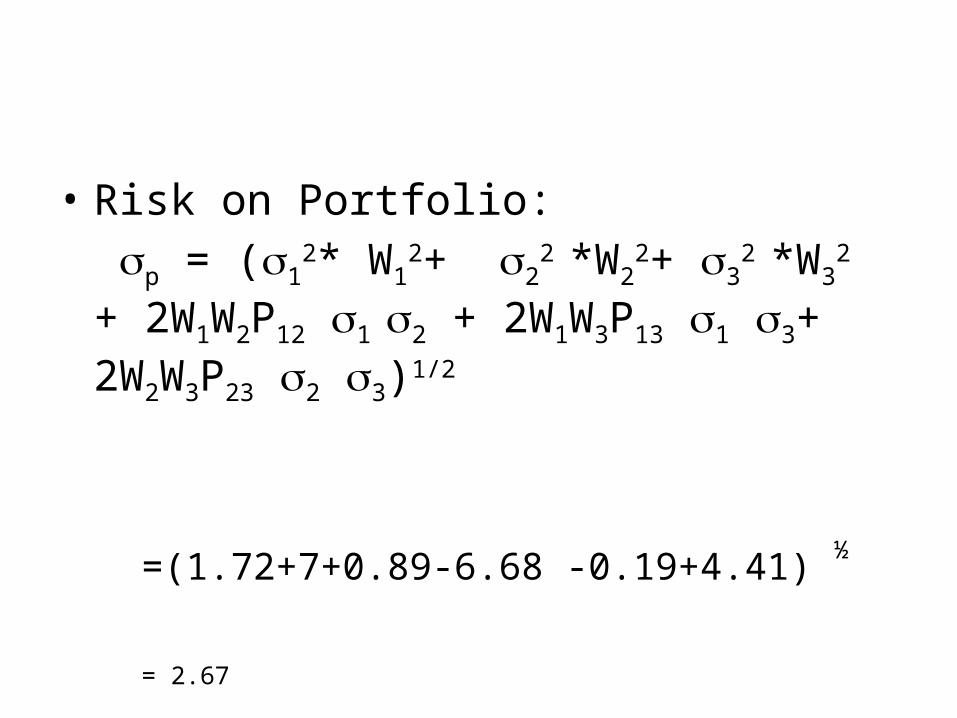

• Risk on Portfolio: p = (1

2* W12+ 2

2 *W22+ 3

2 *W32 +

2W1W2P12 1 2 + 2W1W3P13 1 3+ 2W2W3P23 2 3)1/2

=(1.72+7+0.89-6.68 -0.19+4.41) ½

= 2.67

Related Documents