1 Environment-friendly tax structures for inclusive growth Giuseppe Nicoletti OECD Economics Department Rio+20 IMF side event on Tax and Subsidy Reform for a Greener Economy 21 Jun 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Environment-friendly tax structures for inclusive

growth

Giuseppe Nicoletti OECD Economics Department

Rio+20 IMF side event on Tax and Subsidy Reform for a Greener Economy

21 Jun 2012

2

Tax structures for inclusive green growth

Green taxes (or tradable permits) and elimination of environmentally harmful subsidies: – explicitly price environmental externalities, – increasing the cost of environmentally harmful behaviour – Improve competitiveness of clean technologies – Help equalise marginal abatement costs

As a result, they encourage – cleaner production and consumption – more efficient use of resources – Investment and innovation

… helping prevent future growth bottlenecks

3

Tax structures for inclusive green growth

Green taxes raise revenues which can be used to: – Make growth more inclusive – Help with fiscal consolidation in high-debt countries – Reduce more growth-distortive taxation

Shifting tax structures from income taxation towards alternative revenue sources can boost growth – More entrepreneurial incentives and to work, save and invest – 1% point shift in revenue share can increase GDP p.c. by

0.6-2.3%

A green tax reform can have environmental, social and economic benefits

4

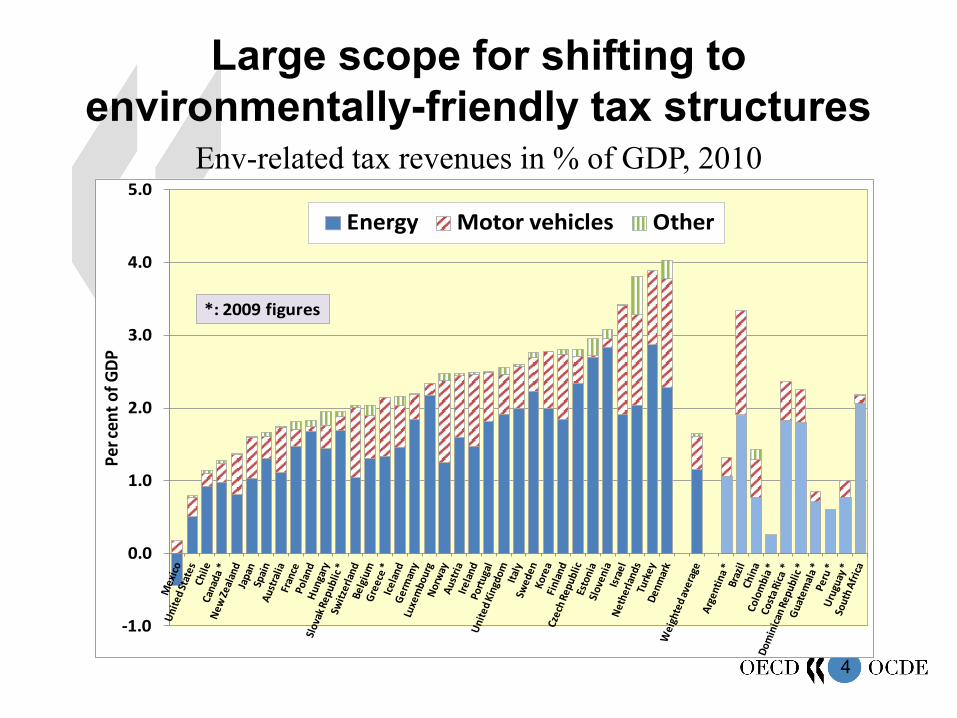

Large scope for shifting to environmentally-friendly tax structures

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Per c

ent o

f GD

P

Energy Motor vehicles Other

*: 2009 figures

Env-related tax revenues in % of GDP, 2010

5

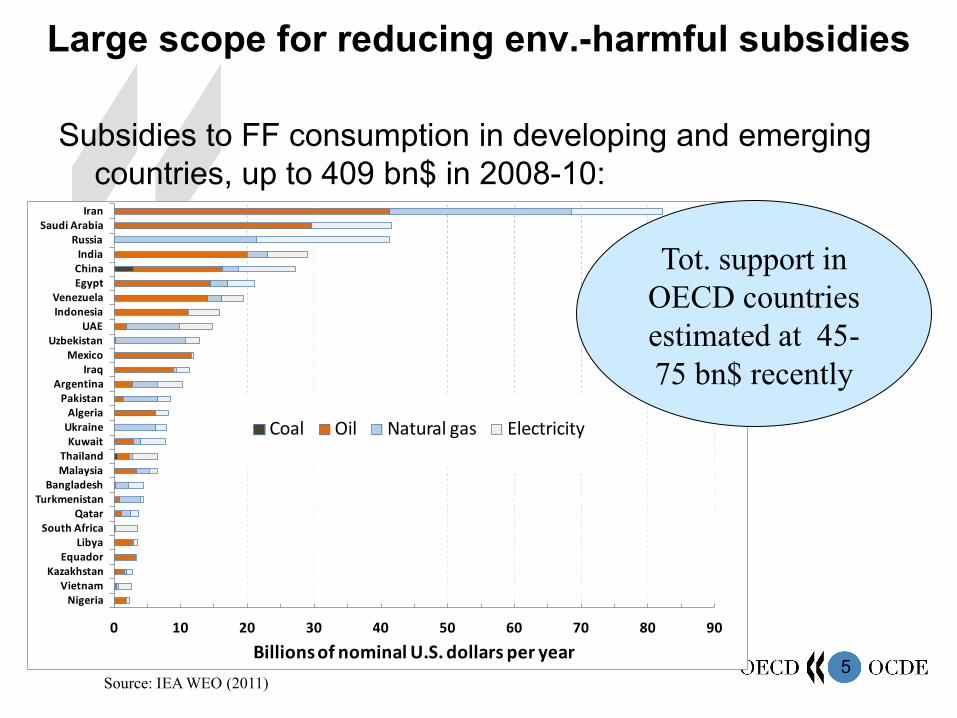

Large scope for reducing env.-harmful subsidies

Subsidies to FF consumption in developing and emerging countries, up to 409 bn$ in 2008-10:

0 10 20 30 40 50 60 70 80 90

NigeriaVietnam

KazakhstanEquador

LibyaSouth Africa

QatarTurkmenistan

BangladeshMalaysiaThailand

KuwaitUkraineAlgeria

PakistanArgentina

IraqMexico

UzbekistanUAE

IndonesiaVenezuela

EgyptChinaIndia

RussiaSaudi Arabia

Iran

Billions of nominal U.S. dollars per year

Coal Oil Natural gas Electricity

Source: IEA WEO (2011)

Tot. support in OECD countries estimated at 45-75 bn$ recently

6

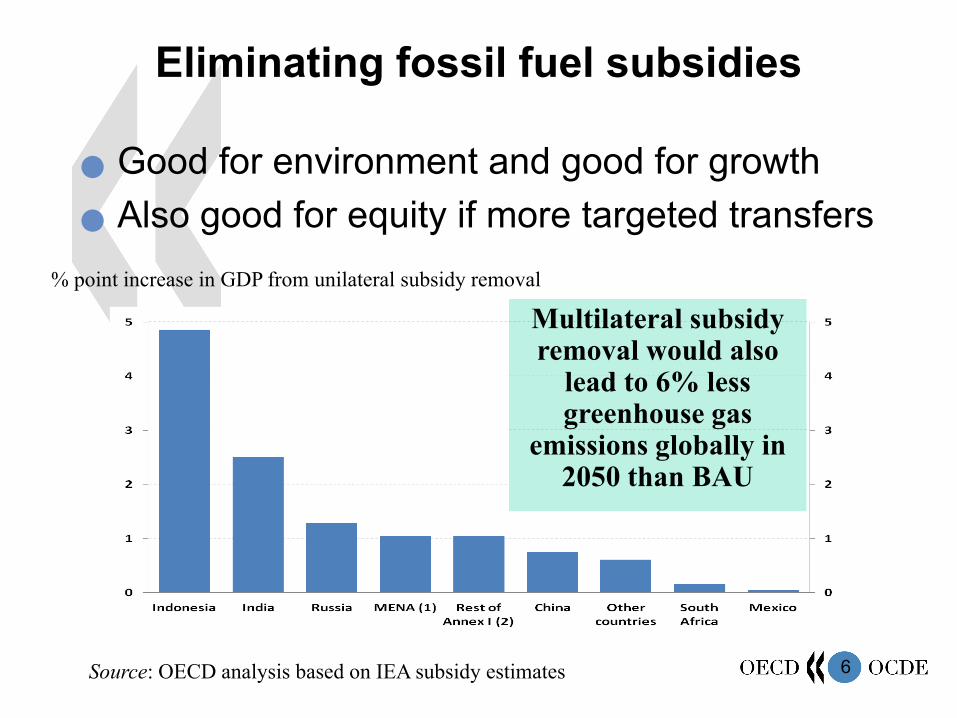

Eliminating fossil fuel subsidies

Good for environment and good for growth Also good for equity if more targeted transfers

Multilateral subsidy removal would also

lead to 6% less greenhouse gas

emissions globally in 2050 than BAU

% point increase in GDP from unilateral subsidy removal

Source: OECD analysis based on IEA subsidy estimates

7

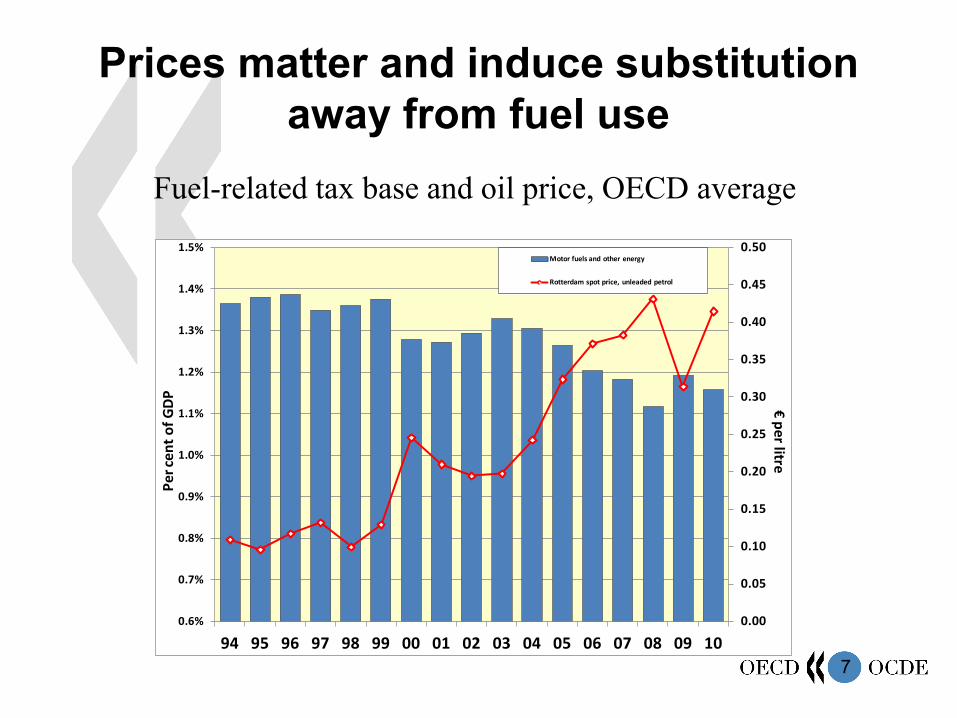

Prices matter and induce substitution away from fuel use

Fuel-related tax base and oil price, OECD average

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.6%

0.7%

0.8%

0.9%

1.0%

1.1%

1.2%

1.3%

1.4%

1.5%

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

€per litre

Per c

ent

of G

DP

Motor fuels and other energy

Rotterdam spot price, unleaded petrol

8

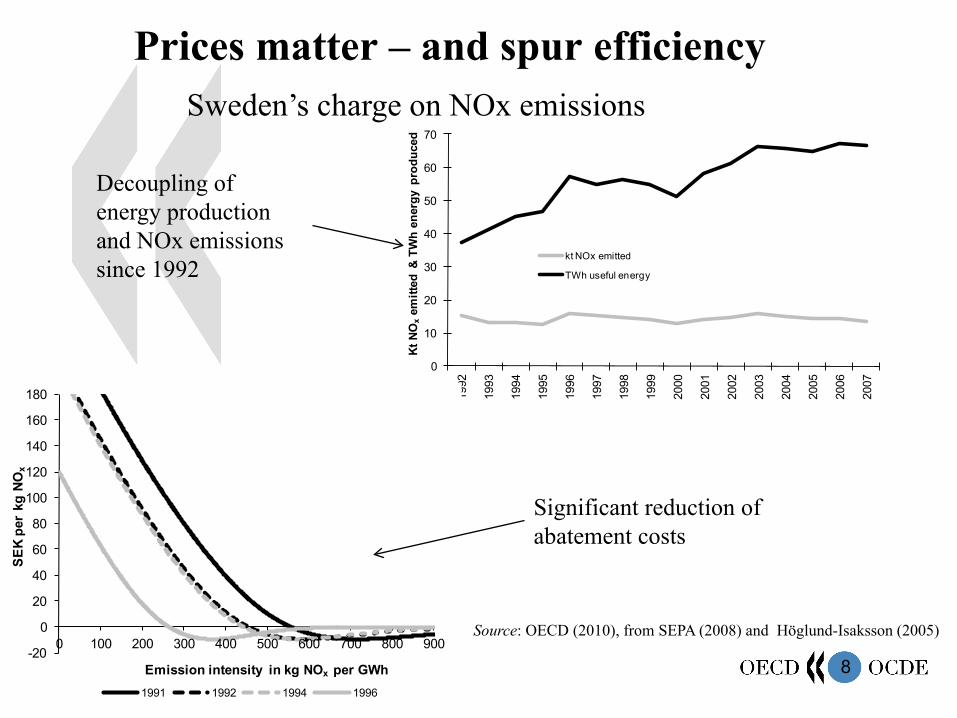

Prices matter – and spur efficiency

0

10

20

30

40

50

60

70

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Kt N

Ox

emitt

ed &

TW

h en

ergy

pro

duce

d

kt NOx emitted

TWh useful energy

-20

0

20

40

60

80

100

120

140

160

180

0 100 200 300 400 500 600 700 800 900

SEK

per

kg N

Ox

Emission intensity in kg NOx per GWh1991 1992 1994 1996

Decoupling of energy production and NOx emissions since 1992

Sweden’s charge on NOx emissions

Significant reduction of abatement costs

Source: OECD (2010), from SEPA (2008) and Höglund-Isaksson (2005)

9

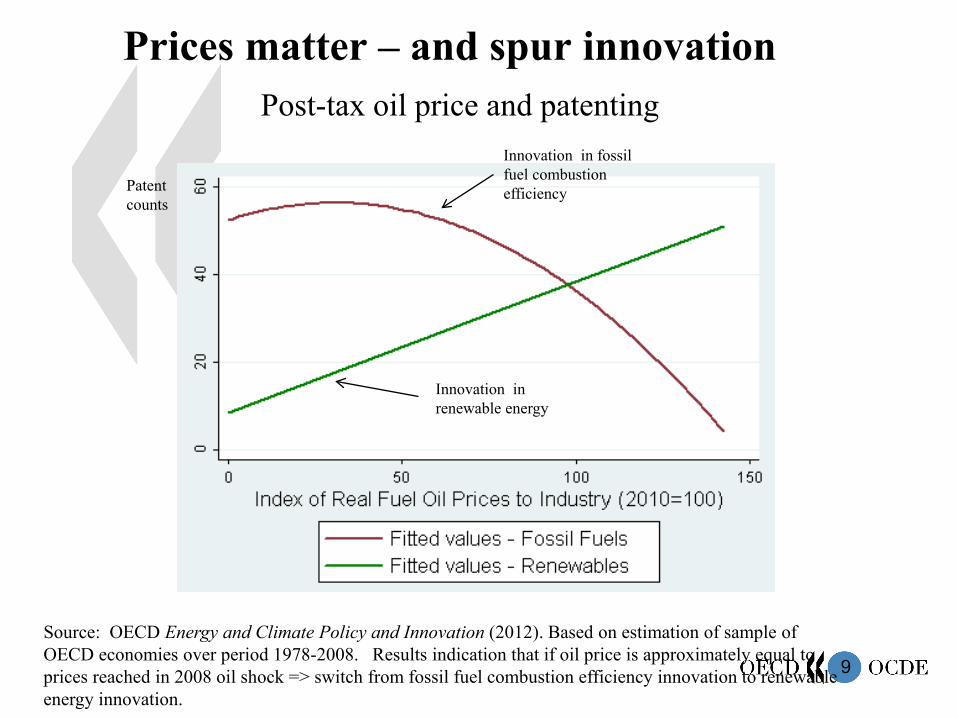

Prices matter – and spur innovation

Source: OECD Energy and Climate Policy and Innovation (2012). Based on estimation of sample of OECD economies over period 1978-2008. Results indication that if oil price is approximately equal to prices reached in 2008 oil shock => switch from fossil fuel combustion efficiency innovation to renewable energy innovation.

Patent counts

Innovation in fossil fuel combustion efficiency

Innovation in renewable energy

Post-tax oil price and patenting

10

Principles of good green fiscal reform

Tax=marginal social damage of environmental externality

For same externality, tax uniformly across different emission sources

Cost-effectiveness and environmental integrity

But principles rarely complied with: e.g. diesel vs gasoline, implicit CO2 taxation, biofuel subsidies

Cost-benefit or multi-criteria analysis important to design green fiscal reform

11

Why is green fiscal reform difficult? Uncertainties related to the valuation of effects

Proxy, measurement, monitoring and enforcement problems

Market instruments require well-functioning markets

Opacity on who pays and who benefits from subsidies

High “visibility” of taxation relative to other green policies (direct real

income losses)

Potential regressivity of some green taxes

Compet. issues for globally traded and public goods (e.g.GHG)

Need to design socially conscious and inclusive green fiscal reform

12

Green taxes and inclusive growth

Additional revenues can be used to offset possible regressive effects of rebalanced tax and subsidy structure – Compensate households for increase in prices – Target transfers to low-incomes

Better pricing of ecosystem services can alleviate poverty in various ways: – Improved health from reduced pollution – Safer reliance on natural resources on which livelihoods of

poor hinge – Revenues can finance improved access to basic services

Recycling revenues to reduce labour income taxation can also push up employment, though not by much

13

Thank you!

For more details: www.oecd.org/rio+20 www.oecd.org/env/taxes www.oecd.org/env/policies/database

Related Documents