Chapter 1 INTRODUCTION 1.1 Background of the Study: In today’s context, just the knowledge about business and management theories does not limit into the prescribing books and syllabus by colleges and universities. It is necessary to have the real- time knowledge with theoretical aspects. Getting real-time knowledge with theoretical concept nowadays is about getting practical knowledge entering into the workplace, so that we may not face problems being into the workplace after our university degree. To bridge the gap between theoretical knowledge and practical aspects, internship has been taken as a pool and has become supportive to students also. Internship is the concept where one in course of learning, can put his/her theoretical knowledge into practical aspects. The Internship was carried out at Nepal Investment Bank Ltd. for the partial fulfillment of the Bachelors of Business Administration (BBA) program. The internship is to serve the purpose of acquainting th e st udents wi th the pr ac ti ce of knowle dge of the disc ip line of ba nking administration. This internship program enables the students to transform the academic knowledge learnt through the years into the practical real world environment where the organizations are facing tough competition with the effect of globalization. The practical approach of internship enables the students to learn what the organizations face in terms of employee diversity, develop interpersonal skills, obtain hands-on experience, the pressures that every organization face, the regulatory environments they have to work in and other variables that are prominent in the real working environment. The intern had the main objective of working in the banking industry and hence internship experience proved to be a nice platform to realize what the needs and the requirements for the jobs are in the banking industry. 1.2 Introduction to Banking Industry Bank is a fina ncia l inst itut ion. Fina ncial inst itut ion pla ys an imp ort ant role in accelerating development of the country. Mobilize saving and make investments in different enterprises of 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 1/40

Chapter 1

INTRODUCTION

1.1 Background of the Study:

In today’s context, just the knowledge about business and management theories does not limit into

the prescribing books and syllabus by colleges and universities. It is necessary to have the real-

time knowledge with theoretical aspects. Getting real-time knowledge with theoretical concept

nowadays is about getting practical knowledge entering into the workplace, so that we may not

face problems being into the workplace after our university degree.

To bridge the gap between theoretical knowledge and practical aspects, internship has been taken

as a pool and has become supportive to students also. Internship is the concept where one in course

of learning, can put his/her theoretical knowledge into practical aspects.

The Internship was carried out at Nepal Investment Bank Ltd. for the partial fulfillment of the

Bachelors of Business Administration (BBA) program. The internship is to serve the purpose of

acquainting the students with the practice of knowledge of the discipline of banking

administration. This internship program enables the students to transform the academic knowledge

learnt through the years into the practical real world environment where the organizations are

facing tough competition with the effect of globalization. The practical approach of internship

enables the students to learn what the organizations face in terms of employee diversity, develop

interpersonal skills, obtain hands-on experience, the pressures that every organization face, the

regulatory environments they have to work in and other variables that are prominent in the real

working environment. The intern had the main objective of working in the banking industry and

hence internship experience proved to be a nice platform to realize what the needs and the

requirements for the jobs are in the banking industry.

1.2 Introduction to Banking Industry

Bank is a financial institution. Financial institution plays an important role in accelerating

development of the country. Mobilize saving and make investments in different enterprises of

1

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 2/40

the National economic that consequently help in reducing poverty, rising employment

opportunities and thereby developing the society and country as a whole.

Bank is a financial intermediary between depositors and entrepreneurs.

The intermediation takes place when they accept deposits from general public, corporate bodies

and private organization and deploys that the deposit for profitable purpose in the form of loan

and advances. Bank is a financial service institution. Therefore, in between this intermediation,

bank gets some earning.

Bank is an establishment, which Wales to individuals such as an advances of the money as may

be requested and safety made to and to which individuals entrusts money when and required by

them for use.

“Banks are among one of the most important financial institutions in the economy and essential

business in thousand of local cities. Banks are those financial instituions that after the wide range

of financial services especially credit, saving and payments services and perform the widest range

of financial functions of any business firm in the economy. This multiplicity of bank services and

functions have led to banks being labeled ‘Financial Supermarkets’ and to such familiar

advertising slogans as your bank a full service financial institution.”

1.2.1 Historical Background of Banking System

Thus, the task of the Commercial bank in an under developed countries territory are almost self-

evident. Their purpose is to provide a collection point for saving of a relatively small average

amount from a large number of individual sources. So long as the means to utilize savings safely

and profitably are not available within an economy, funds will either be diverted abroad, sterilized

in useless hoards case are precious metals or more likely still will not accumulate at all.

In our country Nepal, the history of modern Banking system is very new. This becomes explicitwhen one compares Nepalese banking system with the banking system of other countries of the

world. But this does not mean that there was the complete absence of banking activities in Nepal.

Although, the banking in the form of money lending can be traced, bank in the reign of Gun Kam

Dev towards the end of eight century. According to the historical evidence in 423 A.D. Gun Kam

Dev, the king of Kathmandu had borrowed money to rebuild and to rule Kathmandu.

2

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 3/40

Another historical example as to the pre-modern banking system is found when Rana Prime

Minister Ranoddip Singh was administering Nepal is 1880 A.D. During his reign one financial

institution name by Tejarath was established to give loans facilities to the government staff and to

afford loans facilities to the public in general in the term of 5% on interest.

There is another financial institution specially established in 1991 for the future welfare of the

government staff it was “Sainik Dravya Kosha.” Staff of that period had to face much more

economic difficulties after retirement from his office. The need to regulate financial and

monetary system increased immensely resulting the establishment of Nepal Rastra Bank in 1956

A.D. In order to cater the demand of banking system, Rastriya Banijya Bank was established in

1966 A.D with 100% government ownership. In order to provide service to the agriculture sector,

Agriculture Development Bank was established in 1968.

The government of Nepal adopted liberal economic policy to accelerate country’s growthand

development. Foreign investment and participation of private sector were encouraged. The

government then enacted “Joint Venture Banking” policy. Commercial banks should operate

under the Commercial Bank Act 2031, Nepal Rastra Act 2058 and Company Act 2053 and

Contract Act 2056. Nepal Arab Bank Ltd. (currently known as NABIL) is the first bank

established in joint investment in Nepal in 2041 B.S. A year later Nepal Indosuez Bank Ltd.

currently renamed as Nepal Investment Bank Ltd. was set up. With the passage of time several

other joint venture and private bank has been established.Nepal Industrial Development

Corporation (NIDC) and Agricultural Development Bank(ADB) was only two development

banks established before the enactment of Nepal Development Bank Act in 2052 B.S. After the

introduction of Nepal Development Act 2052 many development banks have been set up.

1.2.2 Commercial Banking in Nepal

The Nepalese financial sector is composed of banking sector and non-banking sector. Banking

sector comprises Nepal Rastra Bank (NRB) and commercial banks. The non-banking sector

includes development banks, micro development bank, finance companies, cooperative financial

institutions, non-government organization (NGO) performing limited banking activities. Other

financial institution comprise of insurance companies, employee’s provident fund, citizen

investment trust, postal saving offices and Nepal stock exchange. There is tremendous growth in

the number of financial institution in Nepal in the last two decades. At the beginning of 1980s

3

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 4/40

when financial sector was not liberalized, there were only two commercial banks and two

development banks performing banking activities in Nepal. There were no micro-credit

development banks, finance companies, cooperatives and NGOs with limited banking transactions.

After the liberalization of the financial sector, financial sector has made a hallmark progress both

in terms of the number of financial institutions and beneficiaries of financial services.

Nowadays, there are 25 commercial banks operating in Nepal, out of them 9 are joint venture with

foreign bank. On the other hand a lot of financial cooperatives are also operating. With the

increasing number of commercial banks, competition among themselves has also become more

complex. In today’s dynamic environment, the commercial banks are trying to introduce and

establish themselves differently from other banks by providing special services and attractive

schemes to its customers.

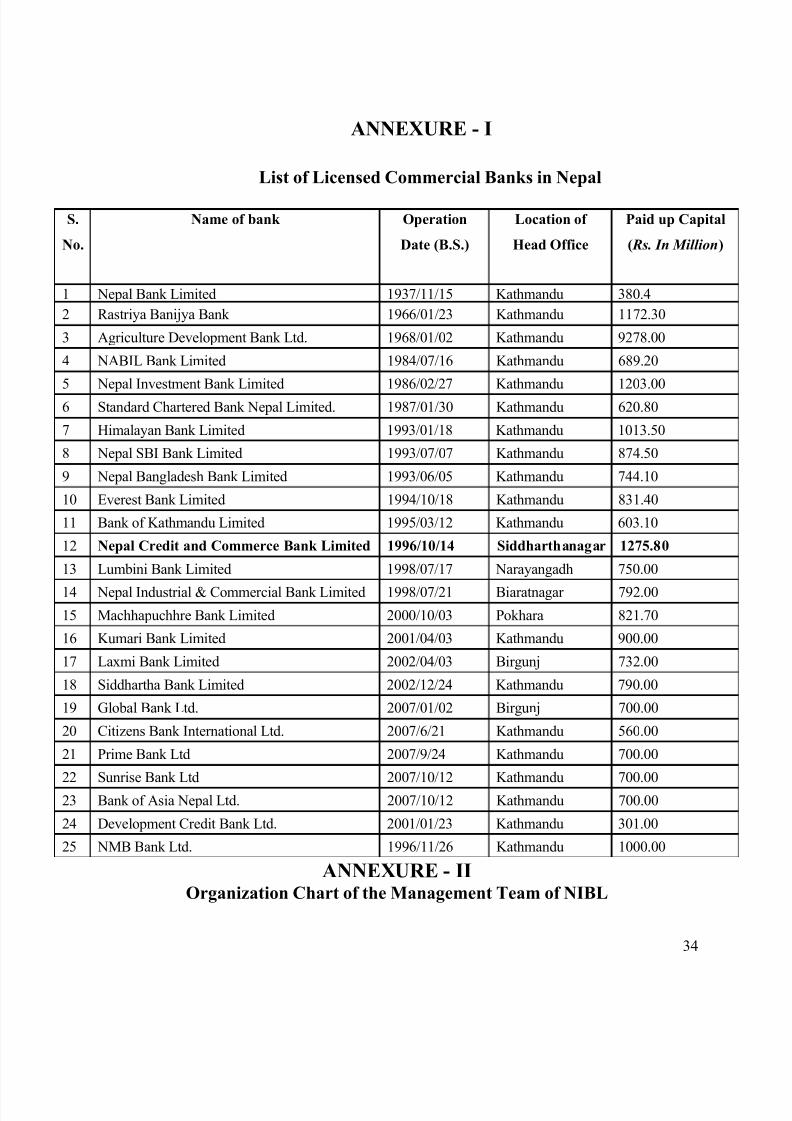

In Nepal up to now, there are 25 commercial banks in operation which is shown in ANNEXURE

I.

1.2 Introduction of company/organization

Nepal Investment Bank Ltd. (NIBL), previously Nepal Indosuez Bank Ltd., was established in

1986 as a joint venture between Nepalese and French partners. The French partner (holding 50% of

the capital of NIBL) was Credit Agricole Indosuez, a subsidiary of one the largest banking group

in the world.

With the decision of Credit Agricole Indosuez to divest, a group of companies comprising of

bankers, professionals, industrialists and businessmen, had acquired on April 2002 the 50%

shareholding of Credit Agricole Indosuez in Nepal Indosuez Bank Ltd.

The name of the bank has been changed to Nepal Investment Bank Ltd. upon approval of bank’s

Annual General Meeting, Nepal Rastra Bank and Company Registrar’s office with the followingshareholding structure.

Table 1 Shareholding Structure of NIBL

Owners percentage

Group of companies 50

Rastriya Banijya Bank 15

4

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 5/40

Rastriya Beema Sansthan 15

General Public 20

1.2.1 Mission/Objectives/Goals of the company

1.3.1.1 Mission

To be the leading Nepali bank, delivering world class service through the blending of state-of-the-

art technology and visionary management in partnership with competent and committed staff, to

achieve sound financial health with sustainable value addition to all our stakeholders.

NIBL is committed to do this mission while ensuring the highest levels of ethical standards,

professional integrity, corporate governance and regulatory compliance.

1.3.1.2 Purpose

To be the most preferred provider of Financial Services in Nepal.

1.3.1.3 Objective:

• To increase our market share by following a disciplined growth strategy.

•

To leverage our technology platform and pen scalable systems to achieve cost-effectiveoperations, efficient MIS, improved delivery capability and high service standards.

• To develop innovative products and services that attracts our targeted customers and market

segments.

• To continue to develop products and services that reduce our cost of funds.

• To maintain a high quality assets portfolio to achieve strong and sustainable returns and to

continuously build shareholders’ value.

• To explore new avenues for growth and profitability.

1.3.1.4 Goals:

• To provide excellent customer service by personalizing the service to gain the

confidence of the customers.

5

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 6/40

• To to deliver extraordinary outcome by the use of resources available through the

professional management team of the bank.

1.3.2 Analysis of Mission, Objectives and Goals

Mission, objectives and goals of NIBL are closely interlinked with each other. Objectives and

goals are set so as to acheive the mission of the bank. Moreover to acheive the above mission,

objectives and goals NIBL has certain core values and ethical principles. These core values

and ethical principles include-

• customer focus

• quality

• honesty and integrity

• belief in their people

• teamwork

• good corporate governance

• corporate social responsibility

With the matching mission, objectives and goals and with the use of these core values and

ethical principles, NIBL has been successful to make a significant position in the banking

industry of Nepal.

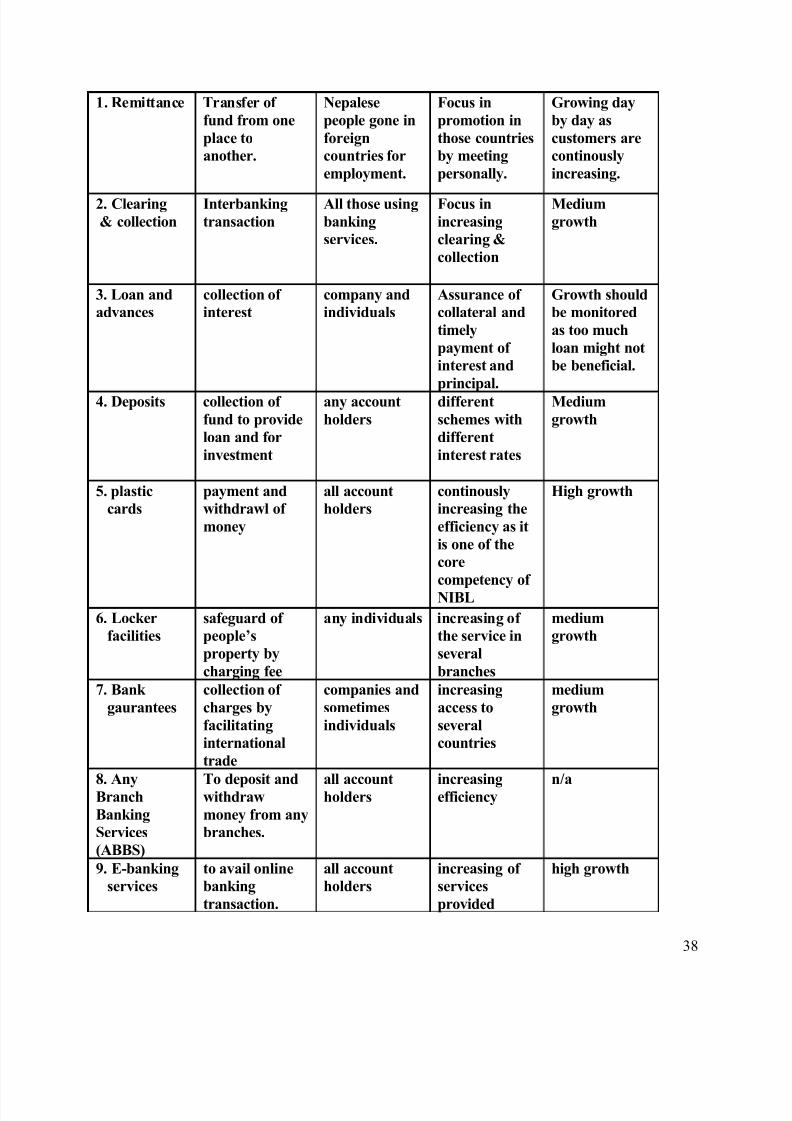

1.3.3Major Products of NIBL.

NIBL aims to provide comprehensive range of flexible and innovative products products

and services. To meet the changing needs of customers NIBL is making constant effort in

providing customer focused products. Major products and services provided by NIBL and

their analysis in terms of their purpose, target market, strategies and growth is as follows.

The major pproducts and services of NIBL is shown in ANNEXURE

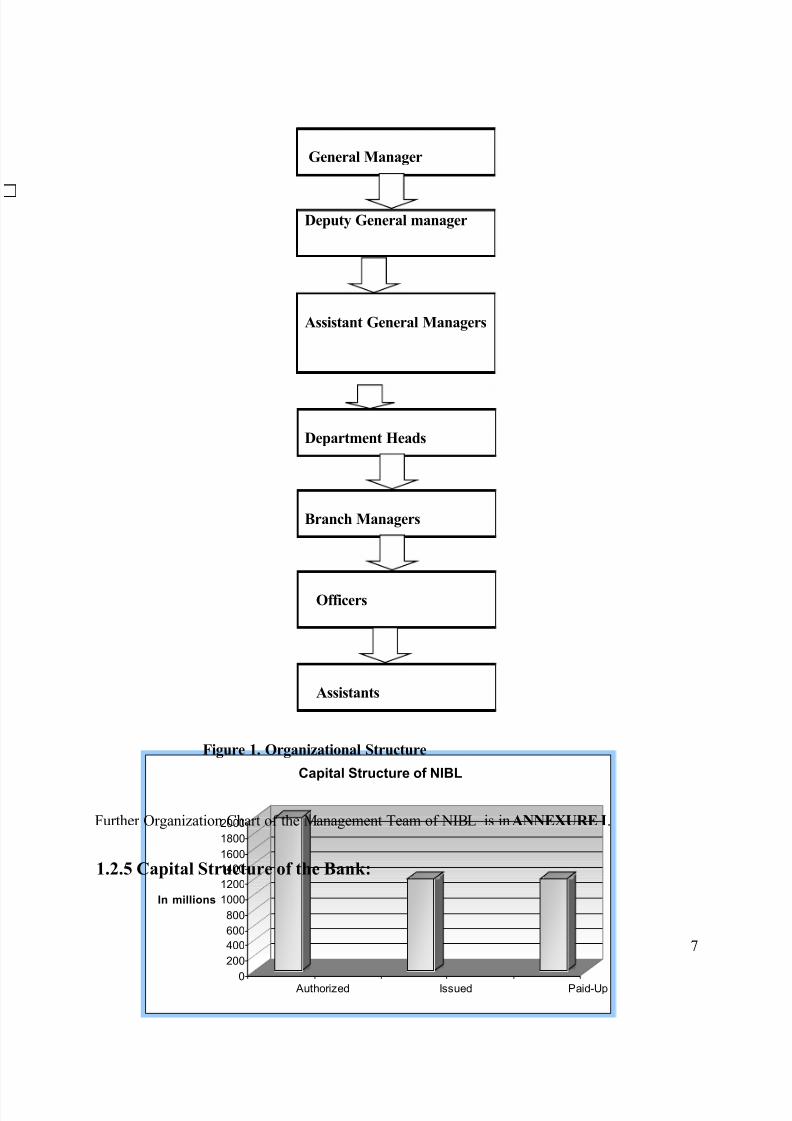

1.2.4 Organizational Structure of NIBL

6

Chairman/CED

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 7/40

0

200

400

600

800

1000

1200

1400

1600

1800

2000

In millions

Authorized Issued Paid-Up

Capital Structure of NIBL

Figure 1. Organizational Structure

Further Organization Chart of the Management Team of NIBL is in ANNEXURE I.

1.2.5 Capital Structure of the Bank:

7

General Manager

Deputy General manager

Assistant General Managers

Department Heads

Branch Managers

Officers

Assistants

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 8/40

Figure 1: Capital Structure of NIBL

The above table that the paid up capital structure of NIBL comprises of Rs.1,203,915,400 of Issued capital

and Paid up capital and Rs.2,000,000,000 of authorized capital of the Bank till the year FY 2009/2010.

1.3 Objective of the Study:

The main objective of this report is to study and examine the trend of financial status of Nepal

Investment Bank Limited; however there is some other objectives concerning with this

project.They are as follows:

• To analyze the financial performance of Nepal Investment Bank Limited in terms

of Liquidity, Earning, Asset Quality and Capital Adequacy.

• To analyse the financial statements of the corporation to it’s true financial position

by the use of ratios.

• To know about fund collection and mobilization in banking system.

• To know the market position of Nepal Investment Bank Limited.

• To identify the contribution of Nepal Investment Bank Limited in Nepalese

economy.

1.4 Methodology of data collection

8

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 9/40

The information required for the preparation of the study report was collected from various

primary and secondary sources. Since not all data collected from secondary sources (as in past

annual reports of NIBL and brochures) can be relied upon for up-to-date and reliable information

both primary, as well as secondary information has been used to prepare this report.

• Primary Source of Information:

The primary information for the report is collected through direct participation of the

intern. The major data collection is done through interview. Where the intern becomes the

interviewer and the bank’s staff or any other personnel to whom the questions are asked

become the interviewee. The questionnaire is prepared before hand for adequacy and to

avoid time loss.

• Secondary Source of Information:

Secondary data i.e. annual reports of the organization for last five years has been

taken into consideration as the main source of data for the purpose of financial

performance analysis. Various publications of Nepal Rastra Bank about banking

and financial statistics and unified directives are also taken for the study. Moreover

informal interactions and structured interviews is also done with different

professionals of accounting and finance in NIBL during the internship period.Various ratios has been calculated for last five years then they are presented by

using respective tables and bar-chart. Interpretation for the findings of each ratios

is also given at last. Also the necessary suggestions have been provided to the

organization so that they know their weakpoints and try to ensure the correction.

1.5 Scope and limitation of Financial Analysis

Scope/Extent of the Study

This report does emphasize the financial position of NIBL.Its scope can be defined as follows:

- Useful to analyze the financial growth trend of NIBL with 5 years.

- Useful to gain knowledge about parameters and techniques regarding ratio analysis.

9

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 10/40

- This study is useful in judging NIBL’s efficiency in terms of its operations and

management.

- This study is also useful in locating weakness on specific operation eventhough overall

performance may be quite good.

- Useful to analyze financial statement over last 5 years.

Limitations/Constraints of Study

- This study is based on the annual report and ratios are calculated as per balance sheet

in the annual report. So, the figures as per the blaance sheet date may not be

indicative of the year round position.

- The study is based on the comparision of ratios with past trends, but it may not give

correct picture due to the change in accounting policies.

- Financial ratio comparision with past trend does not consider the impact of inflation.

Chapter 2

10

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 11/40

Data presentation and Analysis

2.1 Introduction of Financial Analysis

There are several categories of financial service providers active in formal and informalsectors in Nepal. Apart from the commercial banks, the financial system has outgrown to

include development banks, microfinance development banks, finance companies, nongovernment

micro-credit institutions, and non-government cooperative societies.

Nepalese financial market grew largely after late 90s of 20th century. Banks and financial

institutions have been raised tremendously.Now there are commercial banks, finance

compannies and cooperatives. As all those financial institutions run mainly through deposit

collection from customers and by mobilizing the deposit to provide credit,they all are

competing with each other to make them survive and prospher.

In this scenario, I choose to analyze the financial performance of Nepal Investment Bank Limited

over past 5 years to show its effectivness over the years.

11

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 12/40

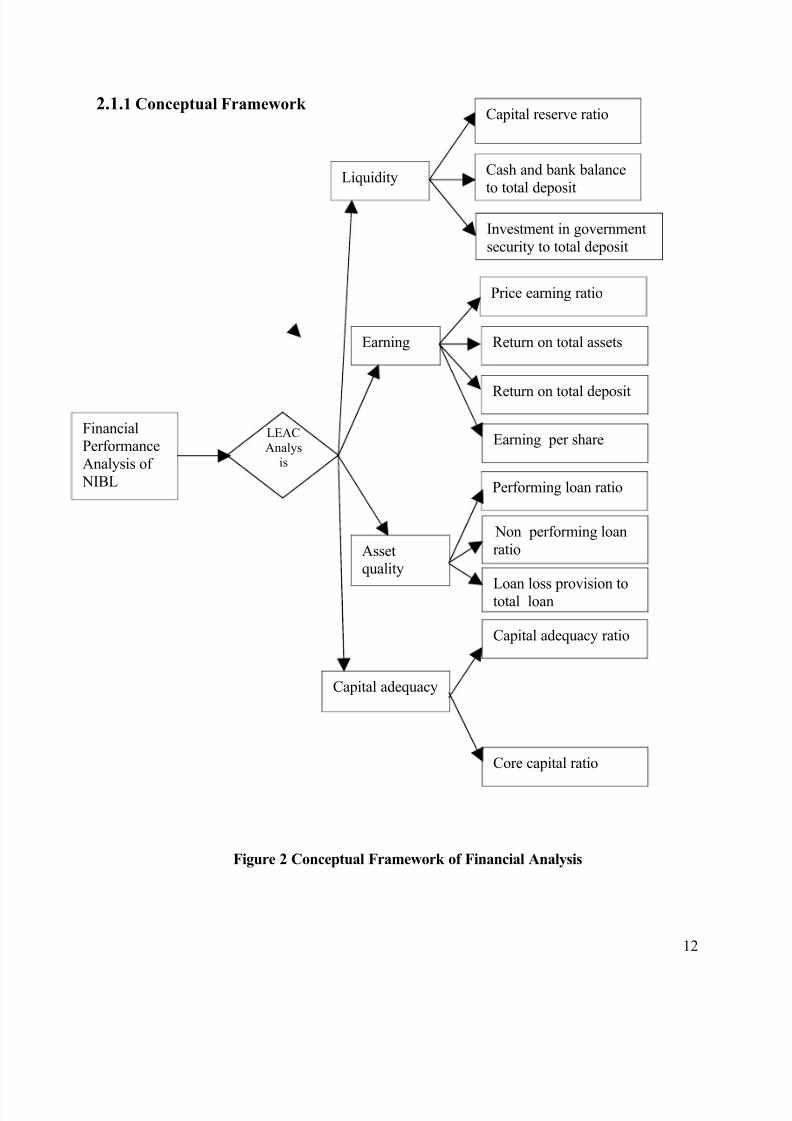

2.1.1 Conceptual Framework

Figure 2 Conceptual Framework of Financial Analysis

12

FinancialPerformance

Analysis of

NIBL

LEAC

Analysis

Liquidity

Earning

Assetquality

Capital adequacy

Cash and bank balance

to total deposit

Investment in government

security to total deposit

Price earning ratio

Return on total assets

Return on total deposit

Earning per share

Performing loan ratio

Non performing loan

ratio

Loan loss provision tototal loan

Capital adequacy ratio

Core capital ratio

Capital reserve ratio

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 13/40

Financial performance analysis of NIBL is done through LEAC analysis which means the analysis

of the degree of liquidity, earning capacity, asset quality and capital adequacy. The analysis of

these four factors is done through the calculation and interpretation of the ratios over last five years

from the respective financial statements to each of the factors.

To analyze liquidity cash reserve ratio (CRR), cash and bank balance to total deposit ratio and

investment in government security to total deposit ratio are calculated. Earning capacity of bank is

measured in terms of price earnings ratio (PE ratio), return on total assets (ROA), return on total

deposit and earning per share ( EPS). Asset quality has been analyzed through the use of

performing loan ratio and loan loss provision to total loan. The degree of capital adequacy has been

measured through capital adequacy ratio and core capital ratio. Analysis of all these ratios has

provided quite clear financial performance of NIBL.

Commercial bank management concept is helpful in preparing the main presentation part

of the project, i.e. LEAC analysis. Moreover the concept of accounting and corporate finance

are equally important for financial ratio and performance analysis.

These two important terms are discussed as follows:

• Financial ratio analysis-

Ratio primarily means the arithemetical relationship between two figures. Ratio is computed

by dividing one item of relation with another. Financial ratio analysis involves a study of the

relationship between income statement and balance sheet accounts, the change in theseratios over a period of time provides the performance of the firm within that time. Also

financial ratios calculated within corresponding years for multiple years such 5 years or 10

years suggest the trend of financial performance over those years.

• Financial performance analysis-

Financial performance analysis refers to an assessment of the viability, stability, and

profitability of a business. Financial analyst often assess the firms performance on the basis

of profitability, solvency, liquidity and stability. Past performance are used to perform the

financial performance analysis and future performance target is set on that basis and then

activities are planned to meet the target.

2.2 Presentation and analysis of data

The main analytical presentation and the major findings of report constitutes this section.

13

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 14/40

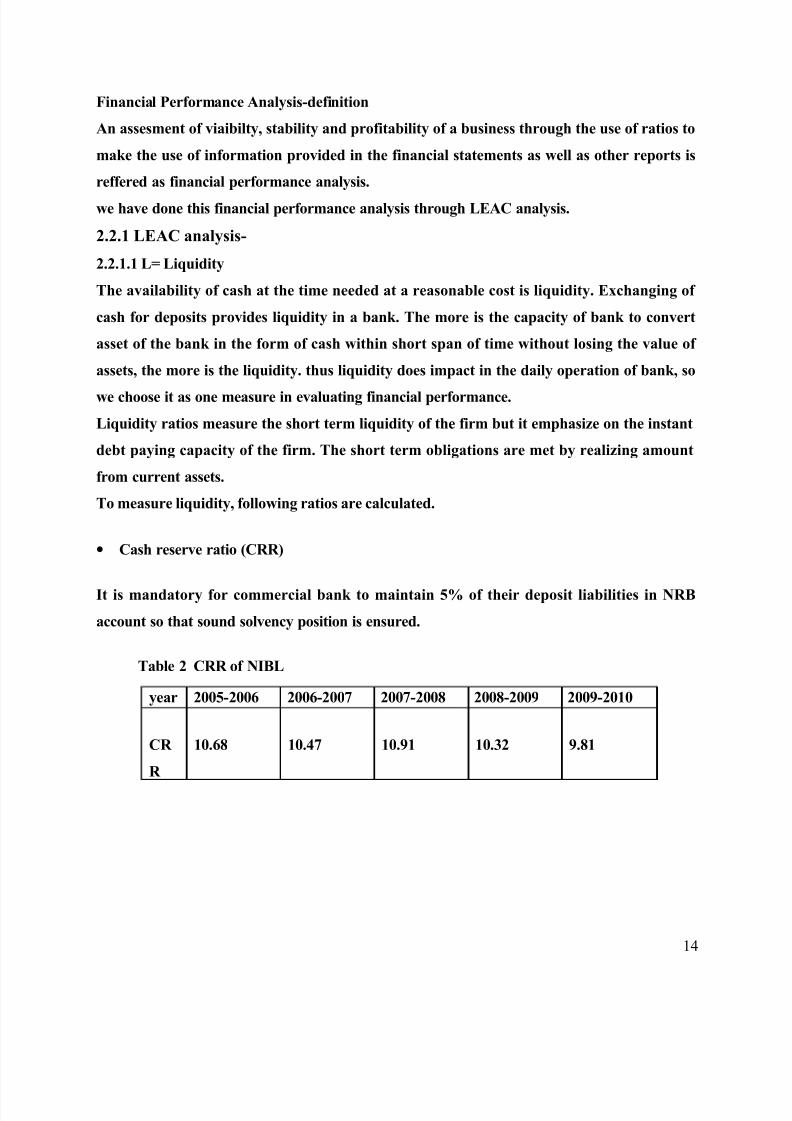

Financial Performance Analysis-definition

An assesment of viaibilty, stability and profitability of a business through the use of ratios to

make the use of information provided in the financial statements as well as other reports is

reffered as financial performance analysis.

we have done this financial performance analysis through LEAC analysis.

2.2.1 LEAC analysis-

2.2.1.1 L= Liquidity

The availability of cash at the time needed at a reasonable cost is liquidity. Exchanging of

cash for deposits provides liquidity in a bank. The more is the capacity of bank to convert

asset of the bank in the form of cash within short span of time without losing the value of

assets, the more is the liquidity. thus liquidity does impact in the daily operation of bank, so

we choose it as one measure in evaluating financial performance.

Liquidity ratios measure the short term liquidity of the firm but it emphasize on the instant

debt paying capacity of the firm. The short term obligations are met by realizing amount

from current assets.

To measure liquidity, following ratios are calculated.

• Cash reserve ratio (CRR)

It is mandatory for commercial bank to maintain 5% of their deposit liabilities in NRB

account so that sound solvency position is ensured.

Table 2 CRR of NIBL

year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

CR

R

10.68 10.47 10.91 10.32 9.81

14

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 15/40

Figure 3 Bar-chart presenting CRR

From the above figure and table it can be seen that NIBL is able to maintain much higher

cash reserve ratio than obligated by NRB. But very higher CRR ratio has also negative effect,

like, cash remain idle and the bank may not be able to grab the opportunity from the

potential profitable sector.

• Cash and Bank Balance to Total Deposit

- shows the percent of deposit maintained as liquid assets.

- maintained to meet any unexpected demand of depositors.

- higher ratio means greater ability to meet an unexpected demand of

depositors.

- but keeping idle cash is not desirable so very high ratio can produce negative

results.

- so this ratio is only maintained to measure the banks ability to meet the

immediate obligation.

cash and bank balance to total deposit of NIBL=cash and bank balance/total deposit

15

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 16/40

Table 3 cash and bank balance to total deposit of NIBL

Figure 4 Bar-chart presenting cash and bank balance to total deposit of NIBL

The cash and bank balance to total deposit ratio of NIBL was in increasing trend since 2005

to 2009 but in fiscal year 2008-2009 it has increased to much higher value of 16.95. But very

higher ratio is also not beneficial so the bank lowered its ratio to 13.61.

•Investment in government securities to total deposits

Government securities are liquid assets which can easily be converted into cash so

every commercial invest their certain amount in government securities.

16

year 2005-

2006

2006-

2007

2007-

2008

2008-

2009

2009-

2010

cash and bank

balance to

deposit

9.97 10.89 12.48 16.95 13.61

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 17/40

Table 4 Investment in government securities to total deposits

year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010NIBL 13.35 10.35 7.87 5.42 6.12

Figure 5 Investment in government securities to total deposits

This shows that investment in government securities to total deposit is in decreasing trend.

2.2.1.2 E=Earning

Earning is what considered to be the ultimate goal of commercial bank. Everyone’s focus is

at earning at the year end. Interest on loan, return on income, charges on different service

provided to the customers etc are the major constituent of earning of a bank.

Financial statements are viewed to know about earning of any institution. Retaining a certain

portion of earning every year helps gradually to grow capital fund of the institution.Following ratios are calculated to test earning capacity of NIBL.

•Price earning ratio

- It presents the investor judgement on expectation about the growth in banks

earning.

17

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 18/40

- It measures how the market is responding to use the earning performance of

the bank.

- The higher ratio indicates the greater confident of investors in banks future.

price earning ratio = market price per share / earning per share

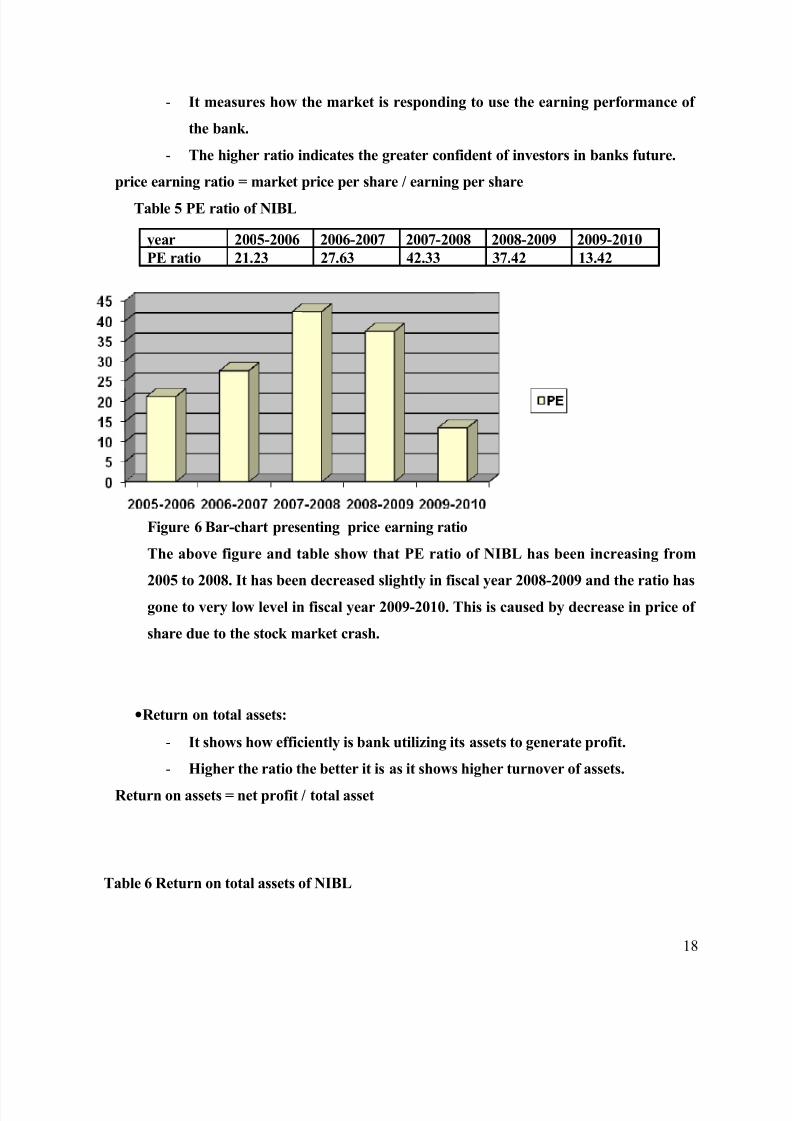

Table 5 PE ratio of NIBL

year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

PE ratio 21.23 27.63 42.33 37.42 13.42

Figure 6 Bar-chart presenting price earning ratio

The above figure and table show that PE ratio of NIBL has been increasing from

2005 to 2008. It has been decreased slightly in fiscal year 2008-2009 and the ratio has

gone to very low level in fiscal year 2009-2010. This is caused by decrease in price of

share due to the stock market crash.

•Return on total assets:

- It shows how efficiently is bank utilizing its assets to generate profit.

- Higher the ratio the better it is as it shows higher turnover of assets.

Return on assets = net profit / total asset

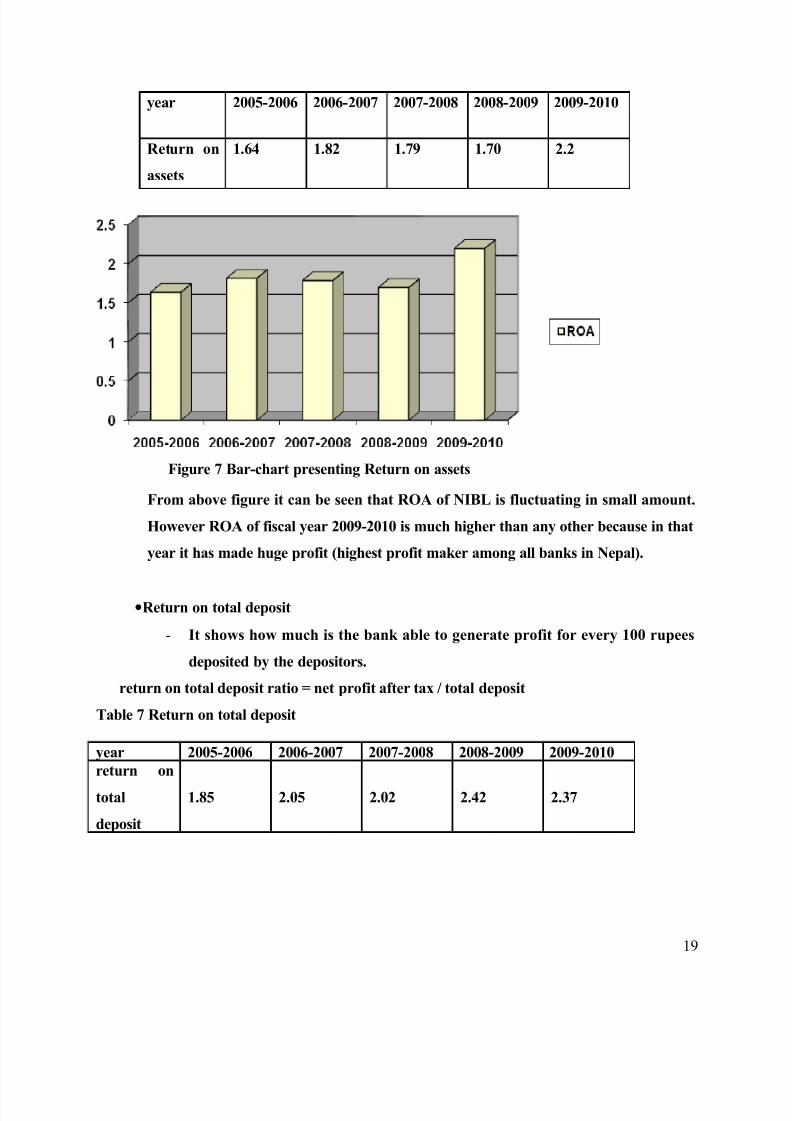

Table 6 Return on total assets of NIBL

18

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 19/40

year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

Return on

assets

1.64 1.82 1.79 1.70 2.2

Figure 7 Bar-chart presenting Return on assets

From above figure it can be seen that ROA of NIBL is fluctuating in small amount.

However ROA of fiscal year 2009-2010 is much higher than any other because in that

year it has made huge profit (highest profit maker among all banks in Nepal).

•Return on total deposit

- It shows how much is the bank able to generate profit for every 100 rupees

deposited by the depositors.

return on total deposit ratio = net profit after tax / total deposit

Table 7 Return on total deposit

19

year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

return on

total

deposit

1.85 2.05 2.02 2.42 2.37

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 20/40

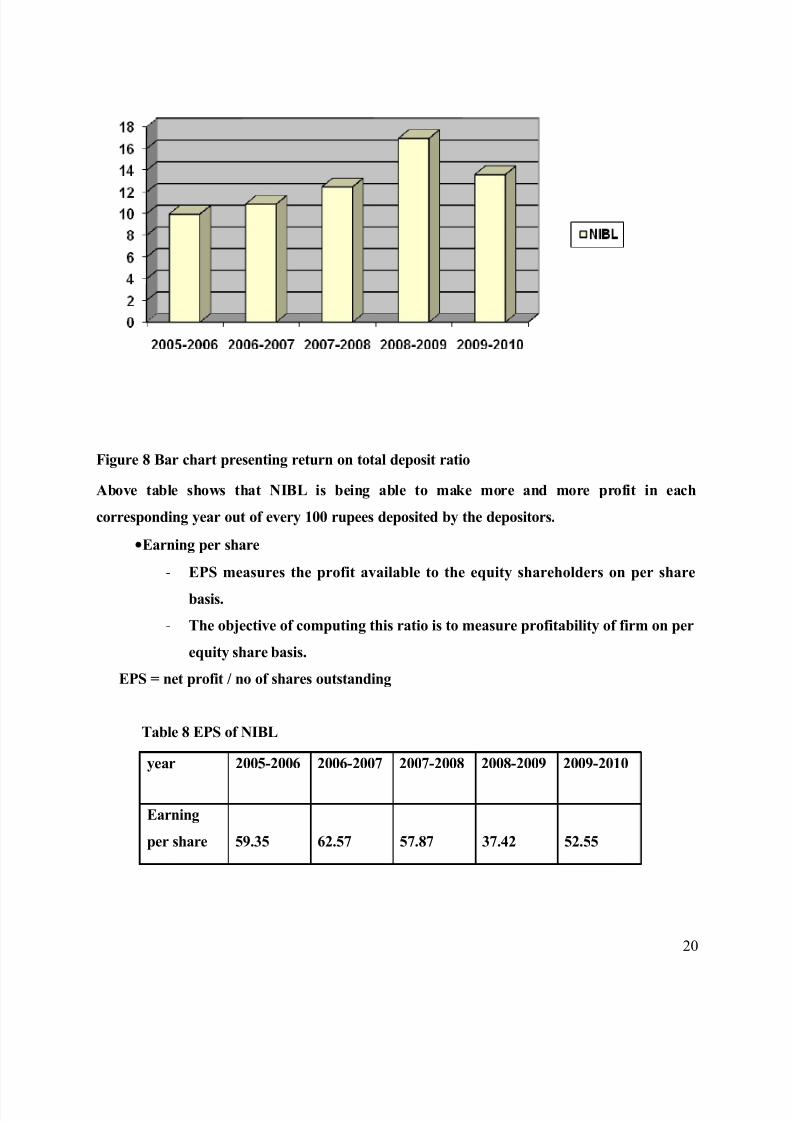

Figure 8 Bar chart presenting return on total deposit ratio

Above table shows that NIBL is being able to make more and more profit in each

corresponding year out of every 100 rupees deposited by the depositors.

•Earning per share

- EPS measures the profit available to the equity shareholders on per share

basis.

- The objective of computing this ratio is to measure profitability of firm on per

equity share basis.

EPS = net profit / no of shares outstanding

Table 8 EPS of NIBL

year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

Earning

per share 59.35 62.57 57.87 37.42 52.55

20

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 21/40

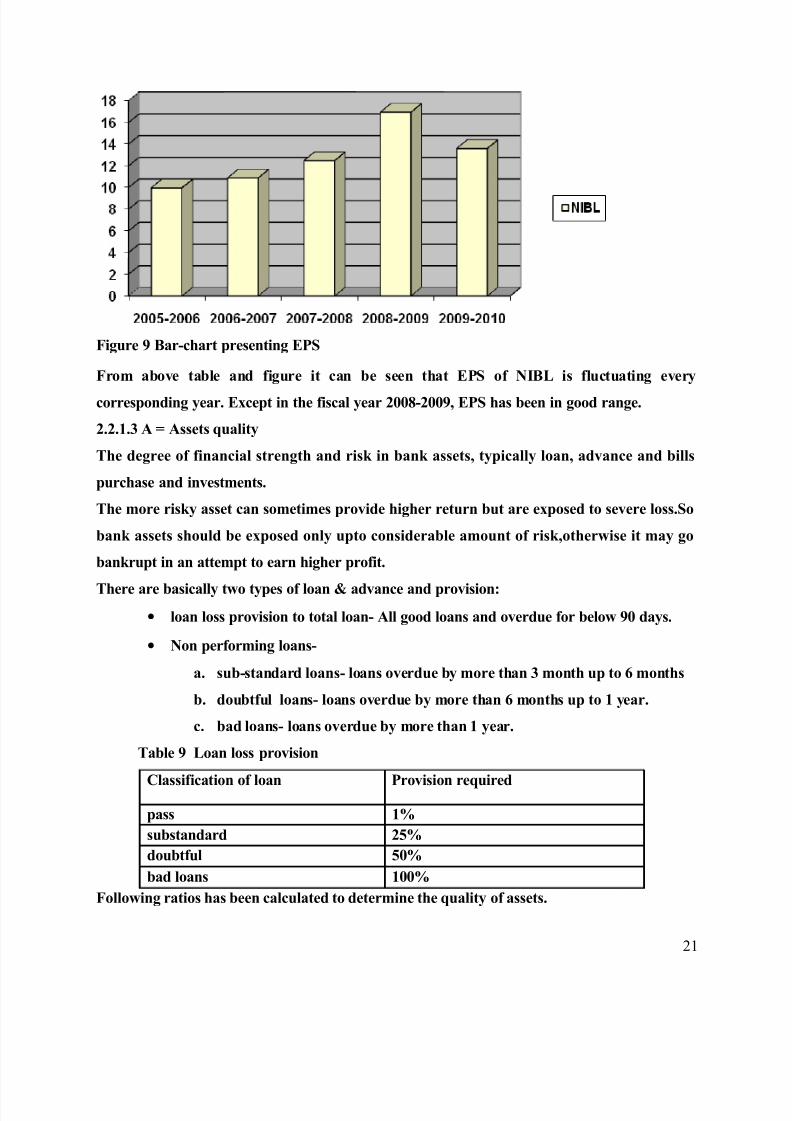

Figure 9 Bar-chart presenting EPS

From above table and figure it can be seen that EPS of NIBL is fluctuating every

corresponding year. Except in the fiscal year 2008-2009, EPS has been in good range.

2.2.1.3 A = Assets quality

The degree of financial strength and risk in bank assets, typically loan, advance and bills

purchase and investments.

The more risky asset can sometimes provide higher return but are exposed to severe loss.So

bank assets should be exposed only upto considerable amount of risk,otherwise it may go

bankrupt in an attempt to earn higher profit.

There are basically two types of loan & advance and provision:

• loan loss provision to total loan- All good loans and overdue for below 90 days.

• Non performing loans-

a. sub-standard loans- loans overdue by more than 3 month up to 6 months

b. doubtful loans- loans overdue by more than 6 months up to 1 year.

c. bad loans- loans overdue by more than 1 year.

Table 9 Loan loss provision

Classification of loan Provision required

pass 1%

substandard 25%

doubtful 50%

bad loans 100%

Following ratios has been calculated to determine the quality of assets.

21

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 22/40

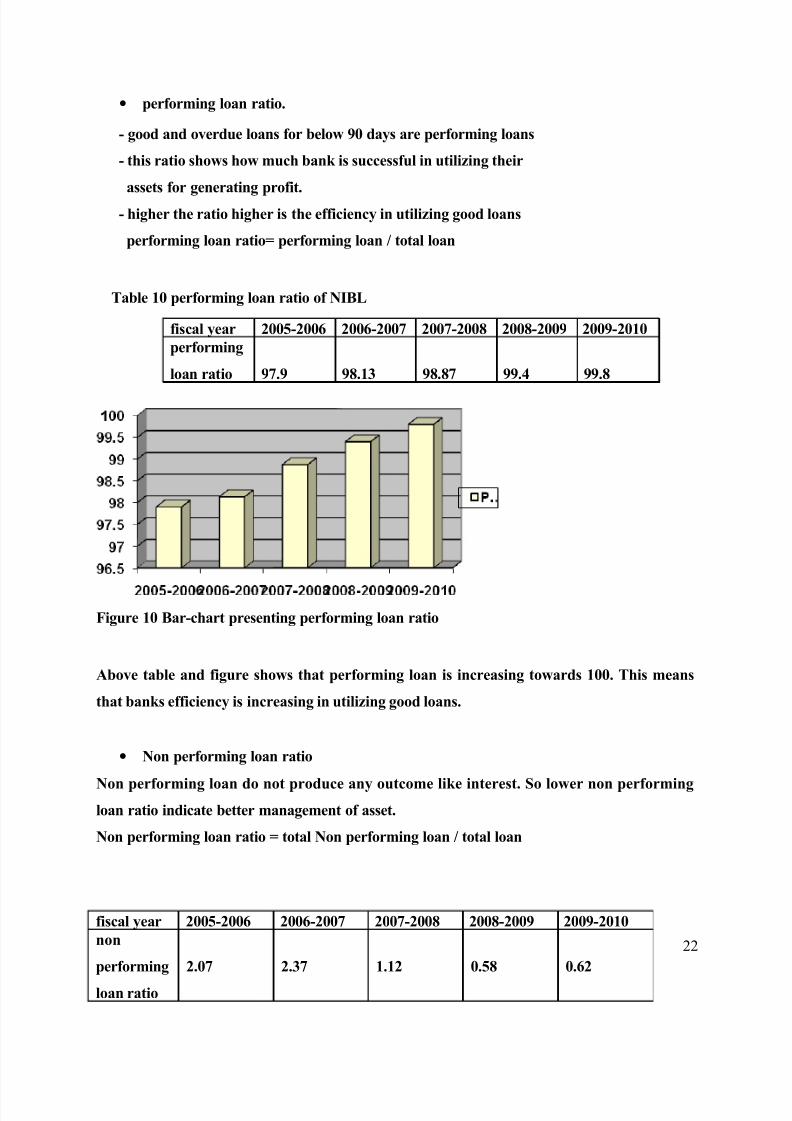

• performing loan ratio.

- good and overdue loans for below 90 days are performing loans

- this ratio shows how much bank is successful in utilizing their

assets for generating profit.

- higher the ratio higher is the efficiency in utilizing good loans

performing loan ratio= performing loan / total loan

Table 10 performing loan ratio of NIBL

fiscal year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

performing

loan ratio 97.9 98.13 98.87 99.4 99.8

Figure 10 Bar-chart presenting performing loan ratio

Above table and figure shows that performing loan is increasing towards 100. This means

that banks efficiency is increasing in utilizing good loans.

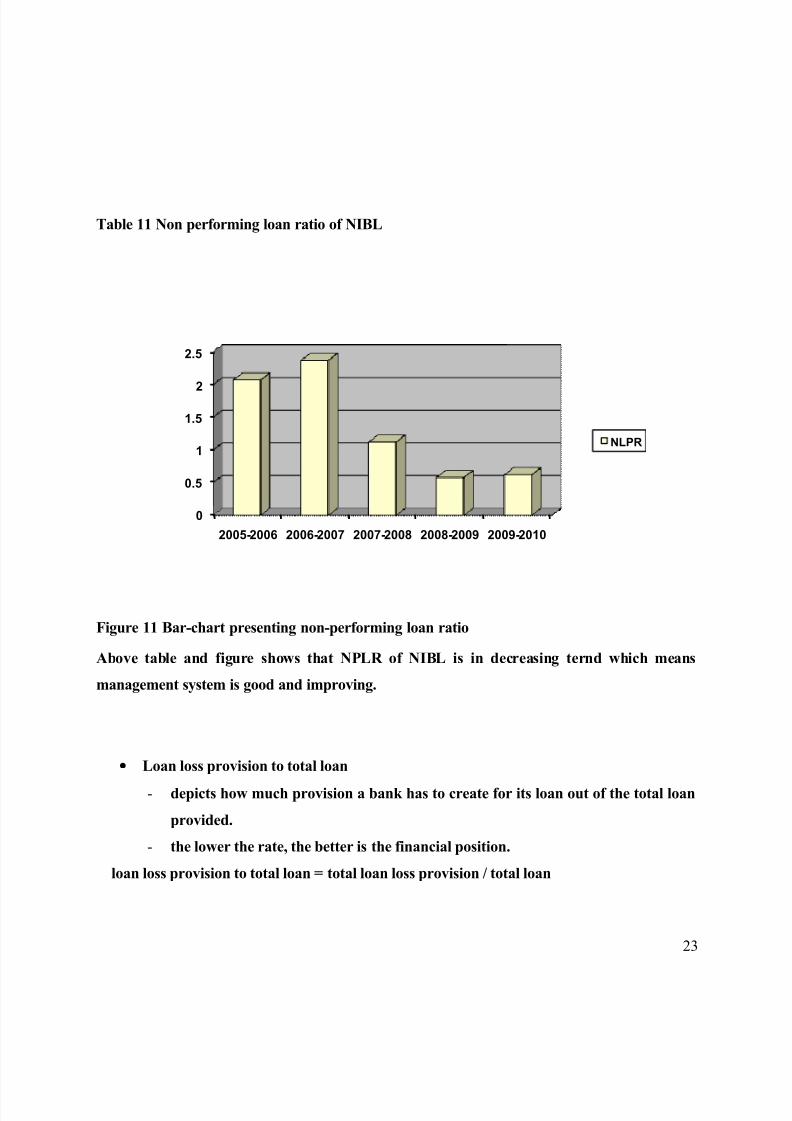

• Non performing loan ratio

Non performing loan do not produce any outcome like interest. So lower non performing

loan ratio indicate better management of asset.

Non performing loan ratio = total Non performing loan / total loan

22

fiscal year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

non

performing

loan ratio

2.07 2.37 1.12 0.58 0.62

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 23/40

Table 11 Non performing loan ratio of NIBL

0

0.5

1

1.5

2

2.5

2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

NLPR

Figure 11 Bar-chart presenting non-performing loan ratio

Above table and figure shows that NPLR of NIBL is in decreasing ternd which means

management system is good and improving.

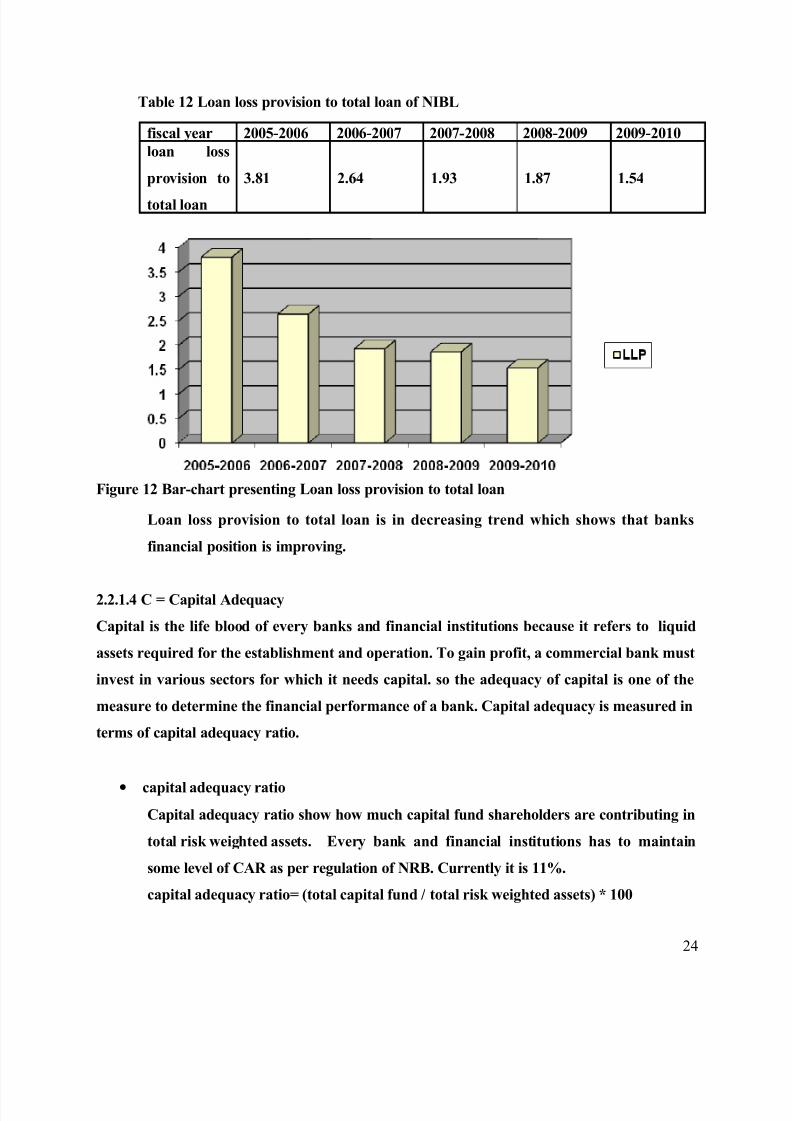

• Loan loss provision to total loan

- depicts how much provision a bank has to create for its loan out of the total loan

provided.

- the lower the rate, the better is the financial position.

loan loss provision to total loan = total loan loss provision / total loan

23

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 24/40

Table 12 Loan loss provision to total loan of NIBL

fiscal year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

loan loss

provision to

total loan

3.81 2.64 1.93 1.87 1.54

Figure 12 Bar-chart presenting Loan loss provision to total loan

Loan loss provision to total loan is in decreasing trend which shows that banks

financial position is improving.

2.2.1.4 C = Capital Adequacy

Capital is the life blood of every banks and financial institutions because it refers to liquid

assets required for the establishment and operation. To gain profit, a commercial bank must

invest in various sectors for which it needs capital. so the adequacy of capital is one of the

measure to determine the financial performance of a bank. Capital adequacy is measured in

terms of capital adequacy ratio.

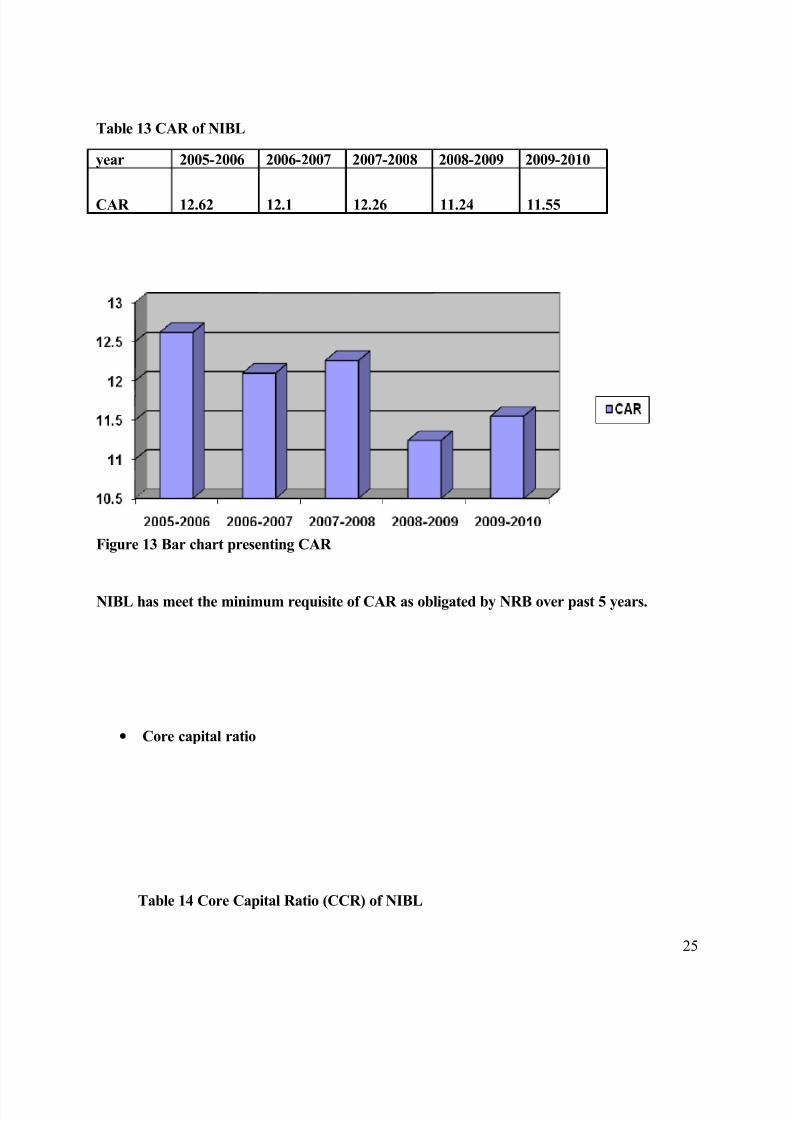

• capital adequacy ratio

Capital adequacy ratio show how much capital fund shareholders are contributing in

total risk weighted assets. Every bank and financial institutions has to maintain

some level of CAR as per regulation of NRB. Currently it is 11%.

capital adequacy ratio= (total capital fund / total risk weighted assets) * 100

24

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 25/40

Table 13 CAR of NIBL

year 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010

CAR 12.62 12.1 12.26 11.24 11.55

Figure 13 Bar chart presenting CAR

NIBL has meet the minimum requisite of CAR as obligated by NRB over past 5 years.

• Core capital ratio

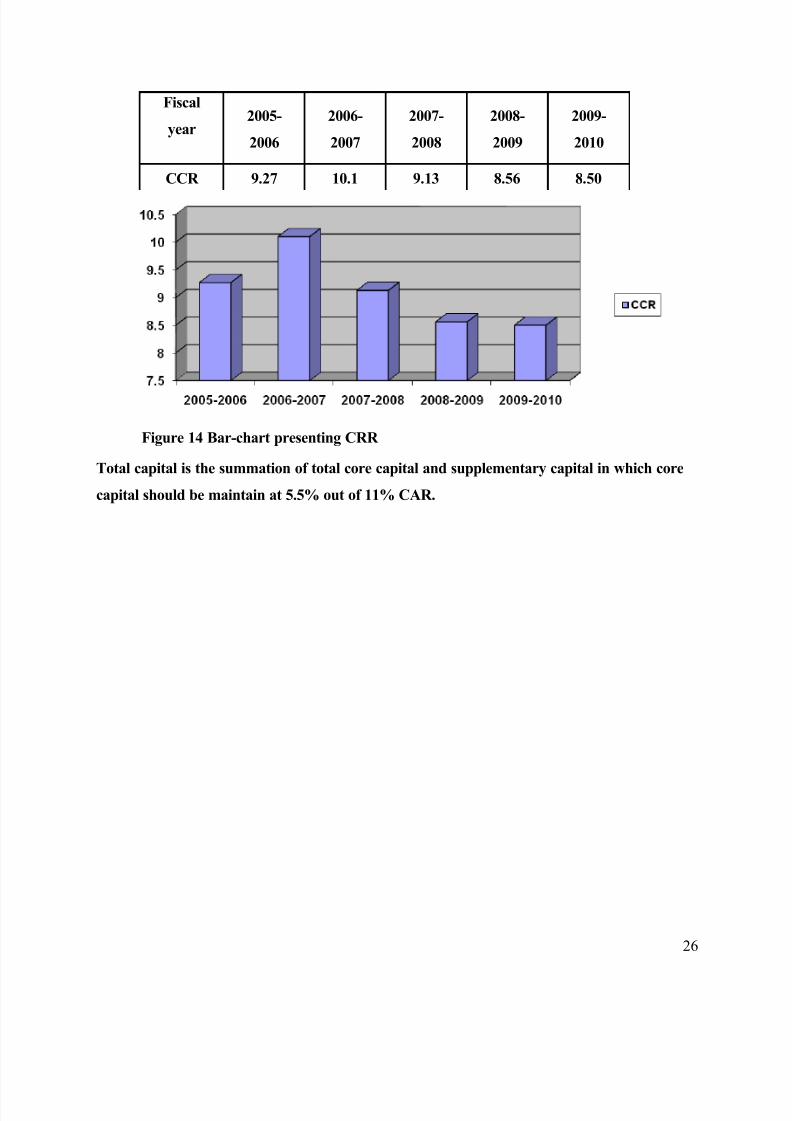

Table 14 Core Capital Ratio (CCR) of NIBL

25

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 26/40

Fiscal

year2005-

2006

2006-

2007

2007-

2008

2008-

2009

2009-

2010

CCR 9.27 10.1 9.13 8.56 8.50

Figure 14 Bar-chart presenting CRR

Total capital is the summation of total core capital and supplementary capital in which core

capital should be maintain at 5.5% out of 11% CAR.

26

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 27/40

Chapter 3

SUMMARY, CONCLUSION AND RECOMMENDATION

3.1 Summary:

The basic purpose of this internship is to get practical knowledge, so that we can utilize our

theoretical knowledge the real-time situation. The main objective of this internship is to get better

understanding of the operations of Customer Service Department and Marketing Department of

Nepal Investment Bank Ltd.

The internee approached Nepal Investment Bank Ltd. Nepal Investment Bank Ltd. (NIBL),

previously Nepal Indosuez Bank Ltd. From the establishment period Nepal Investment Bank has

done its best to prove itself as a best bank in the country.

This intern report is done by the internee for the partial fulfillment of Bachelor of Business

Administration (BBA) and the report is on “Financial Analysis Of NIBL”.

Financial performance analysis of NIBL is done through LEAC analysis which means the analysis

of the degree of liquidity, earning capacity, asset quality and capital adequacy. The analysis of

these four factors is done through the calculation and interpretation of the ratios over last five years

from the respective financial statements to each of the factors.To analyze liquidity cash reserve ratio(CRR), cash and bank balance to total deposit ratio and

investment in government security to total deposit ratio are calculated. Earning capacity of bank is

measured in terms of price earning ratio(PE ratio), return on total assets(ROA), return on total

deposit and earning per share( EPS). Asset quality has been analyzed through the use of

performing loan ratio and loan loss provision to total loan. The degree of capital adequacy has been

measured through capital adequacy ratio and core capital ratio. Analysis of all these ratios has

provided quite clear financial performance of NIBL.

3.2 Conclusions

The banking sector is regarded as fastest growing and leading sector in economy. It provides all

kind of financial and banking solutions to the people. NIBL is one of the leading commercial bank

27

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 28/40

serving the nation since 24 years. The has altogether 40 banking branches all over the Nepal. It has

tried to target international customer through the ATM and remittance service. Since its

establishment in 1986, NIBL has been able to successfully operate providing efficient service to its

customers. By being awarded as " Bank of the Year " in 2003, 2005 and 2008; the bank has gained

a reputation in the market.

From the analysis of the financial performance of NIBL we reach to the following

conclusions:

• NIBL has been seen very efficient in the collection of funds and in its mobilization to

earn profit.

• NIBL has excess amount of cash reserve to cope with the liquidity problem seen in

Nepalese financial market in recent years, which is shown by the higher CRR ratio of about 10% in every year of last 5 years.

• NIBL is constantly earning huge amount of profit in last 5 years but recently its share

price has been decreased due to share market crash.

• NIBL has been very successful in utilizing good loans for generating profit. Last year

its performing loan ratio has been reached nearly 100%

NIBL has always meet the NRB’s requirement of capital adequacy ratio i.e.11%, core capital

i.e.5.5% and cash reserve ratio i.e.5%

3.3 Recommendation

From this whole analysis of performance and from the experience of working in the

organization as interns we would like to give following suggestions to NIBL:

• NIBL should focus in its operational cost to reduce it, so that it can reach to the

international top standard.

• NIBL should focus in providing more allowances and benefit to the employees to

increase their productivity to optimum level.

• NIBL should invest in developmental sectors such as- hydropower, road construction,

industrial sector etc. to contribute to the nation.

• NIBL should focus in succession planning.

28

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 29/40

BIBLIOGRAPHY

1. Management Textbooks:

• Bhandari, Dilli Raj, (2003), Principle and Practice of Banking and Insurance, Kathmandu:

Ayush Publications

• Peter S. Rose, 2003, (Fourth Edition), Commercial Bank Management

• Irwin-McGraw Hill Lawrence J. Gilman, 2006 (Ninth Edition), Principle of Managerial

Finance, Androson Welsley Longman (Singapore)

2. Websites:

• Nepal Investment Bank Ltd. http://www.nibl.com.np

• Nepal Rastra Bank www.nrb.org.np

• Google Search Engine www.google.com

3. Others:

• Nepal Rastra Bank, Banking and Financial Statistics (July 2009).

• Nepal Rastra Bank, Bank And Financial Institution Ordinance (2004).

• Annual Report (2008/2009), Nepal Investment Bank Ltd., Kathmandu.

• Nepal Rastra Bank Collection of Directives for Import/Export.

29

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 30/40

APPENDIXES

BALANCE SHEET OF 2005-2006

Capital & Liabilities Schedule Amount

1. Share Capital 590,586,000

2. Reserve & Fund 824,853,7153. Debentures and Bonds 550,000,000

4. Borrowings -

5. Deposits Liabilities 18,927,305,974

6. Bills Payable 18,820,120

7. Proposed Dividend 121,626,997

8. Income Tax Liabilities 9,318,522

9. Other Liabilities 287,626,214

Total Capital & Liabilities 21,330,137,542

Assets Schedule

1. Cash Balance 562,560,620

2. Balance with NRB 1,526,066,660

3. Balance with Banks/ Financial Institution 247,894,116

4. Money at Call and Short Notice 11 70,000,0005. Investments 5,602,868,649

6. Loan, Advances & Bills Purchased 12,776,208,037

7. Fixed Assets 343,449,635

8. Non-Banking Assets -

9. Other Assets 201,089,825

Total Assets 21,330,137,542

BALANCE SHEET OF 2006-2007

Capital & Liabilities Schedule Amount

1. Share Capital 801,352,600

2. Reserve & Fund 1,076,770,938

30

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 31/40

3. Debentures and Bonds 800,000,000

4. Borrowings -

5. Deposits Liabilities 24,488,855,696

6. Bills Payable 32,401,462

7. Proposed and Dividend payable 43,650,215

8. Income Tax Liabilities 295,150

9. Other Liabilities 347,518,664

Total capital & Liabilities 27,590,844,761

Assets Schedule .

1. Cash Balance 763,984,320

2. Balance with NRB 1,381,351,556

3. Balance with Banks/ Financial Institution 296,178,324

4. Money at Call and Short Notice 11 362,970,000

5. Investments 6,505,679,987

6. Loan, Advances & Bills Purchased 17,286,427,389

7. Fixed Assets 759,456,336

8. Non-Banking Assets 1,125,000

9. Other Assets 233,671,849

Total Assets 27,590,844,761

BALANCE SHEET OF FISCAL YEAR 2008-2009

Capital & Liabilities Schedule Amount

1. Share Capital 2,407,068,900

2. Reserve & Fund 1,500,770,808

3. Debentures and Bonds 3 1,050,000,000

4. Borrowings 38,800,000

5. Deposits Liabilities 8,10000,065

6. Bills Payable 82,338,018

7. Proposed and Dividend Payable 485,453,507

8. Income Tax Liabilities 38,296,736

9. Other Liabilities 709,975,092

31

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 32/40

Total Liabilities 53,010,803,126

Assets Schedule

1. Cash Balance 1,833,462,494

2. Balance with NRB 4,411,133,083

3. Balance with Banks/ Financial Institution 1,673,408,313

4. Money at Call and Short Notice 11 -

5. Investments 7,399,811,700

6. Loan, Advances & Bills Purchased 36,241,206,558

7. Fixed Assets 1,060,752,482

8. Non-Banking Assets 375,000

9. Other Assets 390,653,496

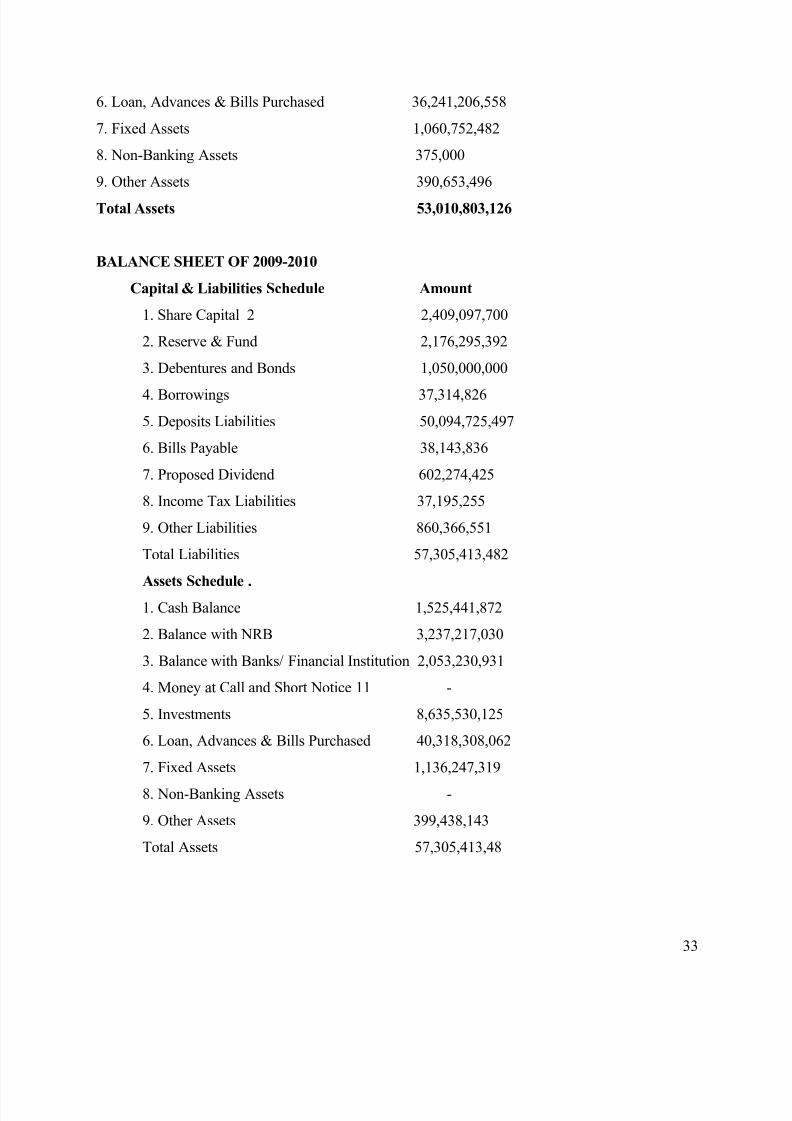

Total Assets 53,010,803,126

BALANCE SHEET OF 2008-2009

Capital & Liabilities Schedule Amount

1. Share Capital 2,407,068,900

2. Reserve & Fund 1,500,770,808

3. Debentures and Bonds 1,050,000,000

4. Borrowings 38,800,000

5. Deposits Liabilities 46,698,100,065

6. Bills Payable 82,338,018

7. Proposed Dividend 485,453,507

8. Income Tax Liabilities 38,296,736

9. Other Liabilities 709,976,092

Total capital & Liabilities 53,010,830,126

Assets Schedule .

1. Cash Balance 1,833,462,494

2. Balance with NRB 4,411,133,083

3. Balance with Banks/ Financial Institution 1,673,480,313

4. Money at Call and Short Notice 11 -

5. Investments 7,399,811,700

32

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 33/40

6. Loan, Advances & Bills Purchased 36,241,206,558

7. Fixed Assets 1,060,752,482

8. Non-Banking Assets 375,000

9. Other Assets 390,653,496

Total Assets 53,010,803,126

BALANCE SHEET OF 2009-2010

Capital & Liabilities Schedule Amount

1. Share Capital 2 2,409,097,700

2. Reserve & Fund 2,176,295,392

3. Debentures and Bonds 1,050,000,000

4. Borrowings 37,314,826

5. Deposits Liabilities 50,094,725,497

6. Bills Payable 38,143,836

7. Proposed Dividend 602,274,425

8. Income Tax Liabilities 37,195,255

9. Other Liabilities 860,366,551

Total Liabilities 57,305,413,482

Assets Schedule .

1. Cash Balance 1,525,441,872

2. Balance with NRB 3,237,217,030

3. Balance with Banks/ Financial Institution 2,053,230,931

4. Money at Call and Short Notice 11 -

5. Investments 8,635,530,125

6. Loan, Advances & Bills Purchased 40,318,308,062

7. Fixed Assets 1,136,247,319

8. Non-Banking Assets -

9. Other Assets 399,438,143

Total Assets 57,305,413,48

33

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 34/40

ANNEXURE - I

List of Licensed Commercial Banks in Nepal

ANNEXURE - IIOrganization Chart of the Management Team of NIBL

34

S.

No.

Name of bank Operation

Date (B.S.)

Location of

Head Office

Paid up Capital

( Rs. In Million)

1 Nepal Bank Limited 1937/11/15 Kathmandu 380.4

2 Rastriya Banijya Bank 1966/01/23 Kathmandu 1172.30

3 Agriculture Development Bank Ltd. 1968/01/02 Kathmandu 9278.00

4 NABIL Bank Limited 1984/07/16 Kathmandu 689.20

5 Nepal Investment Bank Limited 1986/02/27 Kathmandu 1203.00

6 Standard Chartered Bank Nepal Limited. 1987/01/30 Kathmandu 620.80

7 Himalayan Bank Limited 1993/01/18 Kathmandu 1013.50

8 Nepal SBI Bank Limited 1993/07/07 Kathmandu 874.50

9 Nepal Bangladesh Bank Limited 1993/06/05 Kathmandu 744.10

10 Everest Bank Limited 1994/10/18 Kathmandu 831.40

11 Bank of Kathmandu Limited 1995/03/12 Kathmandu 603.10

12 Nepal Credit and Commerce Bank Limited 1996/10/14 Siddharthanagar 1275.80

13 Lumbini Bank Limited 1998/07/17 Narayangadh 750.00

14 Nepal Industrial & Commercial Bank Limited 1998/07/21 Biaratnagar 792.00

15 Machhapuchhre Bank Limited 2000/10/03 Pokhara 821.70

16 Kumari Bank Limited 2001/04/03 Kathmandu 900.00

17 Laxmi Bank Limited 2002/04/03 Birgunj 732.00

18 Siddhartha Bank Limited 2002/12/24 Kathmandu 790.00

19 Global Bank Ltd. 2007/01/02 Birgunj 700.00

20 Citizens Bank International Ltd. 2007/6/21 Kathmandu 560.00

21 Prime Bank Ltd 2007/9/24 Kathmandu 700.00

22 Sunrise Bank Ltd 2007/10/12 Kathmandu 700.00

23 Bank of Asia Nepal Ltd. 2007/10/12 Kathmandu 700.00

24 Development Credit Bank Ltd. 2001/01/23 Kathmandu 301.00

25 NMB Bank Ltd. 1996/11/26 Kathmandu 1000.00

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 35/40

Chairman &

Chief Executive DirectorAudit Committee

Senior General Manager

Company SecretarySenior General Manager

Company Secretary

General Manager Deputy General

Manager

Credit/Retail

HeadInternal Audit

Audit Committee

Deputy GeneralManager

Operations

HeadHuman

Resource

Head

Legal

Shares &Company

Affairs

Assistant GeneralManager

Credit Quality

HeadLoan Admin

HeadForex/Treasury

HeadCash &

Transfer

BRANCHES

Operations

Head

General

Service

Head

R&D

Head

Remittance/

Card

Head

IT

Head

Accounts/Budgets

HeadCorporate Bank

HeadTrade Finance

HeadCredit Admin

BranchCo-ordination

HeadRetail Bank

Customer Service

Customer Finance

DepositMarketing

BRANCHES

Credit/Retail

ANNEXURE - III

Branches of NIBL

35

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 36/40

1. KATHMANDU HEAD OFFICE

Durbar Marg, P.O. Box 3412

Tel: 4228229, 4242530 (DISA)

Fax: 977-1-4226349, 4228927

Swift: NIBL NP KT

2. SEEPADOLE BRANCHSuryabinayak, Bhaktapur Tel: 6615617, 6612832

Fax: 6616617

3. BIRGUNJ BRANCHAdarshanagar, P.O. Box 101Tel (051) 523327, 525277

Fax: (051) 525297

4. PULCHOWK BRANCH

Pulchowk, Lalitpur

Tel: 5010188, 5010042Fax: 5010142

5. BANEPA BRANCH

Banepa, Kavre

Tel: (011) 664315,662401Fax: (011) 662402

6. JEETPUR BRANCH

Jeetpur, BaraTel: (053) 520297

Fax: (053) 520877

7. NEWROAD BRANCH

Newroad, KathmanduTel: 4242858, 4230374

Fax: 42270508. BIRATNAGAR BRANCH

Golcha Chowk, Biratnagar

Tel: (021) 534523, 534524, 534525Fax: (021) 534526

9. BUTWAL BRANCH

Traffic Chowk, Butwal

Tel: (071) 549991, 549992, 549993Fax: (071) 549888

10. BHAIRAHAWA BRANCH

Maitri Road, Bhairahawa

Tel: (071) 526991, 526992

Fax: (071) 526990

11. POKHARA BRANCH

Chiple Dunga,Pokhara

Tel: (061) 538919, 539276

Fax: (061) 538920

12. PUTALISADAK BRANCH

Putalisadak, Kathmandu

Tel: 4445302, 4445303Fax: 4445304

13. NARAYANGARH BRANCH

Pulchowk, Narayangarh

Tel: (056) 571921,571922,Fax: (056) 571925

14. JANAKPUR BRANCH

Mills Area, Janakpur

Tel: (041) 527331

Fax: (041) 527332

15. NEPALGUNJ BRANCH

Dhamboji, Nepalgunj

Tel: (081) 525978,525682

Fax: (081) 521664

16. THAMEL BRANCH

Chaksibari, Thamel

Tel: 4218431,4218434,Fax: 4218434

17. KALIMATI BRANCH

Kalimati Chowk, Kalimati

Tel: 4672493,4672494Fax: 4272612

18. BIRTAMOD BRANCH

Traffic Chowk, BirtamodTel:(023) 543810,543811

Fax: (023)543815

19. BATTISPUTALI BRANCH

Battisputali, KathmanduTel: 4471690,4471790

Fax: 4470202

20. DHANGADI BRANCH

Main Road, Dhangadi

Tel:(091) 523620,523706Fax: (091) 524090

21. GONGABU BRANCH

Gongabu Chowk, Kathmandu

Tel: 4365318,4365077Fax: 4365302

22. SURKHET BRANCH 23. JUMLA BRANCH

36

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 37/40

Neta Chowk, SurkhetTel: (083) 524330, 524331

Fax: 524332

Khalang Bazaar, JumlaTel: (087) 520132

Fax: 520304

24. BOUDHA BRANCH

Boudha, Kathmandu

Tel: 4480121,4480122Fax: 4480123

25. HETAUDA BRANCH

Bank Road, Hetauda

Tel: (057) 526001, 525946Fax: (057) 526005

26. PALPA BRANCH

Tansen,PalpaTel: (075) 520832,520833

Fax:(075)-520891

27. LUKLA BRANCH

Chaurikharka, LuklaTel:(038) 550120

Fax: (038) 550220

28. NAYA BANESHWOR BRANCH

Naya Baneshwor, Kathmandu

Tel:4785529,4782289,4782520

Fax: 4785537

29. DHUMBARAHI BRANCH

Pipalbot Chowk, Kathmandu

Tel: 4009006, 4009007

Fax: 4009009

30. BHOTAHITI BRANCH

Bhotahiti, KathmanduTel: 4230797, 4230788

Fax: 4230771

31. TULSIPUR BRANCH

Tulsipur, DangTel:(082)521613,521614

Fax: 521615

32. TRIPURESHWOR BRANCH

Tripureshwor, Kathmandu

Tel: 4259780, 4259980Fax: 4260324

33. DAMAULI BRANCH

Safasadak, Damouli

Tel:(065) 562500,562600Fax: (065) 562700

34. KRISHNANAGAR BRANCH

Krishnanagar, KapilvastuTel: (076) 520764, 520765, 520766

Fax: (076) 520354

35. GAIGHAT BRANCH

Gaighat, Udayapur Tel: (035) 420952, 420953

Fax: (035) 420954

36. LAZIMPAT BRANCHLazimpat, Kathmandu

Tel:4005058, 4005069, 4005068Fax:4005065

37. PARSA BRANCHParsa, Chitwan

Tel: (056) 583623, 583624Fax: (056) 583625

38. MAHARAJGUNJ BRANCH

Maharajgunj, KathmanduTel:4016151, 4016152

Fax:4016155

39. LALBANDHI BRANCH

Lalbandhi, SarlahiTel: (046) 501583, 501584

Fax:(046) 501585

40. LAGANKHEL BRANCH

Lagankhel, Lalitpur

Tel: 5552980

Fax: 5552990

ANNEXURE IVProducts and Services of NIBL

Products and

services PurposeTarget market

Strategies Growth

37

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 38/40

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 39/40

10. NTC

mobile bill

payment

to provide

customers

varieties of

services

all account

holders using

NTC mobile

service.

promotion of

this service to

every account

holders

medium

growth

11. ATM

services

cash withdrawl

and balanceinquiry, also has

facility of

depositing

money through

ATM machines

in some places

all account

holders

increasing

efficiency

medium

growth

12. Tele-

banking

service

to make inquiry

of account

balance and to

order statement

of account

all account

holders

focus on

reliability and

secrecy

through the

use of password

n/a

39

8/2/2019 Edited Paw An Final Report

http://slidepdf.com/reader/full/edited-paw-an-final-report 40/40

Related Documents