BUSINESS RISK A practical guide for board members A DIRECTOR’S GUIDE

Business Risk

Dec 14, 2015

A must to read for those starting up their business.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BUSINESS RISKA practical guide for board members

BUSINESS RISK

BUSINESS RISK: A PRACTICAL GUIDE FOR BOARD MEM

BERSA DIRECTOR’S GUIDE

A practical guide for board members

In a world of increasing complexity anduncertainty, the need for companies todevelop robust risk management strategiesis greater than ever. Yet many fail to do so,either because they are overwhelmed by thesize of the task or because they are ill-equipped to tackle it.

Responsibility for business risk oversight liessquarely with board members.

This guide will help directors – both executiveand non-executive, in large and smallcompanies – to develop an effective approachto managing business risk. Key topics itcovers include:

•The board’s distinctive role in risk oversight•Aligning risk management and strategy•Establishing risk appetite and tolerance•Board composition and behaviour•Interaction with stakeholders•Directors’ personal risks

This guide is part of the Director’s Guide series,published by the Institute of Directors,providing directors with clear, practical adviceon key business issues, with real life case studies.

£9.95

A DIRECTOR’S GUIDE

Risk Cover_v6_Layout 1 29/05/2012 12:46 Page 1

BUSINESS RISKA PRACTICAL GUIDE FOR BOARD MEMBERS

Editor, Director Publications Ltd: Lysanne Currie

Consultant Editor: Tom Nash

Art Editor: Chris Rowe

Production Manager: Lisa Robertson

Head of Commercial Relations: Nicola Morris

Commercial Director: Sarah Ready

Managing Director: Andrew Main Wilson

Chairman: Simon Walker

Published for the Institute of Directors, Airmic Ltd, Chartis Europe Ltd,

PricewaterhouseCoopers LLP and Willis UK Ltd by

Director Publications Ltd, 116 Pall Mall, London SW1Y 5ED

020 7766 8910

www.iod.com

©Copyright Director Publications Ltd. June 2012

A CIP record for this book is available from the British Library

ISBN 9781904520-80-1

Printed and bound in Great Britain

Price £9.95

The Institute of Directors, Airmic Ltd, Chartis Europe Ltd,

PricewaterhouseCoopers LLP, Willis UK Ltd and Director Publications Ltd accept

no responsibility for the views expressed by contributors to this publication.

Readers should consult their advisers before acting on any issue raised.

INSTITUTE OF DIRECTORSThe IoD is the leading organisation supporting and representing business

leaders in the UK and internationally. One of its key objectives is to raise the

professional standards of directors and boards, helping them attain high levels of

expertise and effectiveness by improving their knowledge and skills.

AIRMICAirmic represents corporate risk managers and insurance buyers. Its

membership includes two-thirds of the FTSE 100, as well as many smaller

companies. The association organises training for its members, seminars,

breakfast meetings and social occasions. It regularly commissions research and

its annual conference is the leading risk management event in the UK.

CHARTISChartis is a world-leading property-casualty and general insurance organisation

serving more than 70 million clients around the world. With one of the industry’s

most extensive ranges of products and services, deep claims expertise and great

financial strength, Chartis enables its clients to manage risk with confidence.

PWCAs the UK's leading provider of integrated governance, risk and regulatory

compliance services, PwC specialises in helping businesses and their boards

create value in a turbulent world. Drawing from a global network of specialists in

risk, regulation, people, operations and technology, PwC helps its clients to

capitalise on opportunities, navigate risks and deliver lasting change through

the creation of a risk-resilient business culture.

WILLISWillis Group Holdings plc is a leading global insurance broker. Through its

subsidiaries, it develops and delivers professional insurance, reinsurance, risk

management, financial and HR consulting and actuarial services to corporations,

public entities and institutions around the world. Willis has more than 400

offices in nearly 120 countries, with a global team of some 17,000 associates.

ABOUT THE SPONSORS

2

3

PART 1: THE ISSUESChapter 1 7 A world of dangerNicolas Aubert, UK Managing Director,Chartis

Chapter 2 13 The board’s distinctive role in risk oversightDr Roger Barker, Head of CorporateGovernance, Institute of Directors

Chapter 3 19 Key challenges facing boardsin risk oversightAlpesh Shah, Actuarial Risk PracticeDirector, and Richard Sykes, Governance,Risk & Compliance UK Leader, PwC

PART 2: THE SOLUTIONSChapter 4 25 The board’s role in establishing the right corporate cultureRoger Steare, Professor of OrganisationalEthics at Cass Business School, City University

Chapter 5 33 Risk and strategyAlpesh Shah and Richard Sykes, PwC

Chapter 6 41Defining the risk appetite/risk tolerance of the organisationTom Teixeira, Practice Leader, GlobalMarkets International, Willis Group

Chapter 7 47 Board compositionSir Geoffrey Owen, Senior Fellow, The London School of Economics andPolitical Science

Chapter 8 53 The boardroom conversationAlison Hogan, Managing Partner, AnchorPartners, with Ronny Vansteenkiste, SVP,Group Head Talent Management &Organisation Development, Willis Group

Chapter 9 61 Information and the boardDavid Jackson, Company Secretary, BP

Chapter 10 67 Interaction with shareholdersDavid Pitt-Watson, Chair, Hermes FocusAsset Management

Chapter 11 73 The personal risks facing directorsGrant Merrill, Chief Underwriting Officer,Commercial Institutions, Financial Lines,Chartis

Chapter 12 79 The final wordJohn Hurrell, Chief Executive, Airmic

Case studies Lessons from major risk events arehighlighted throughout the Guide. For details, see page 12

CONTENTS

BUSINESS RISKA PRACTICAL GUIDE FOR BOARD MEMBERSIntroduction: Simon Walker, Director General, Institute of Directors

Foreword: Sir John Parker, Chairman, Anglo-American

4

BOARDS AND RISK Simon Walker, Director General, Institute of Directors

In its analysis of some of the most significant corporate disasters of recent years,

the recent study, Roads to Ruin, identifies a number of determinants of corporate

failure (see page 12). The key lesson that emerges is that the board of directors is

a crucial mechanism through which risks should be identified and managed.

Without a competent board, manageable difficulties are more likely to

escalate out of control. There is a greater chance that the organisation will

experience major losses, damage to its reputation, or disappear altogether.

It is clear from these cases – and others that emerged during the recent

financial crisis – that risk management is a core task for the board of directors or

supervisory board. Risk management cannot simply be delegated to specialist

risk managers or even the CEO. It is simply too important. Moreover, many

aspects of risk management require a strategic perspective that is beyond the

remit of the typical risk management department.

A common problem is for non-executive or supervisory board members to

face major challenges in securing adequate flows of objective information about

the performance of the business. In particular, a ‘glass ceiling’ that hinders

communication between internal monitoring departments (such as risk

management, internal audit or compliance) and the board can prove a fatal flaw.

In contrast, a well-informed and independently-minded board can play a

crucial role in defining the risk tolerance of the organisation. It is also well

positioned to spot the emerging risks that can so easily be overlooked or

discounted by managers immersed in the day-to-day operation of the enterprise.

Although this guide is particularly aimed at enhancing the effectiveness of

non-executive directors, senior executives will also benefit from a better

understanding of how their own risk management activities should interact with

the board in a manner that promotes the overall success of the organisation.

There are few aspects of a board's functioning that are as crucial to long-term

corporate success as risk management. For directors who wish to avoid the

mistakes of past corporate failures, this guide will be a valuable reference tool.

INTRODUCTION

FOREWORD

5

INSIGHT AND ADVICE Sir John Parker, Chairman, Anglo-American

Controlled risk-taking lies at the heart of all commercial activity. However,

boards can fail to manage risk for a variety of reasons.

Some downside risks may emerge from within the organisation as a result of

operational failures. But many corporate disasters occur due to the weakness of

the board itself. The board has the potential to be both a source of risk to the

organisation as well as an effective means of risk mitigation.

This practical new guide for directors is designed to ensure that your

organisation does not become the next case study in the annals of poor risk

management. Various sources of boardroom risk are addressed. In some cases,

individual directors may simply lack the necessary expertise or experience to

understand the business in all its complexity. In other instances, a charismatic or

overbearing CEO may dominate the boardroom conversation. Even a period of

corporate success can, ironically, often prove to be a source of danger. It may

make it difficult for the board to challenge or criticise the status quo. The board

may fall victim to the delusions of ‘groupthink’ or overconfidence.

It is all too easy for directors to discount the significance of these and other

boardroom pitfalls: “It will never happen to us.” History has shown, however,

that such issues can easily arise on boards, even among directors of high calibre.

The intransigence of such problems is both a reflection of the complexities of

human behaviour and an increasingly challenging business environment.

By bringing together the insights of leading experts in corporate governance

and risk management, this publication seeks to help shape the risk management

agenda of board members. In particular, it will assist chairmen and non-

executive directors to hit the ground running in their risk management role, and

rapidly ask the right questions of the CEO and the rest of the management team.

I commend this practical and insightful new publication as a significant

contribution to the risk management awareness of directors across a wide range

of organisations.

CONFIDENCE is on the agenda.

Chartis Europe Limited is authorised and regulated by the Financial Services Authority (FSA number 202628). This information can be checked by visiting the FSA website (www.fsa.gov.uk/

Pages/register<http://www.fsa.gov.uk/Pages/register>). Registered in England: company number 1486260. Registered address: The Chartis Building, 58 Fenchurch Street, London, EC3M 4AB.

Insurance solutions

from Chartis.Today’s directors and officers

and multinational clients face

more risk than ever, due to a growing

breadth of international regulations

and heightened enforcement.

Having the right coverage is critical.

At Chartis, we have an unparalleled global

network offering cutting-edge insurance

solutions built to meet the challenges of risk

today—and will keep innovating to meet the

challenges of tomorrow. Learn more at

www.chartisinsurance.com/uk

7

A WORLD OF DANGER

Nicolas Aubert, UK Managing Director, Chartis

SNAPSHOT■ New risks are constantly emerging, including the dangers of doing business in

global markets.■ Many board members fail to recognise the dangers they face personally.■ Different-sized companies face varying sizes and types of risk. ■ Managing risk is not just about buying insurance. ■ With the right approach from the board, most risks can be successfully managed

and mitigated.

BALANCING RISK AND REWARDThe balance between risk and reward is the very essence of business: without

taking risks companies cannot generate profits. But, as later chapters in this

Guide will explain, there is a world of difference between calculated risks, taken

with foresight and careful judgement, and risks taken carelessly or unwittingly.

The starting point for boards is to oversee risk in relation to their organisation’s

risk ‘appetite’ and ‘tolerance’ and to align their approach to risk with its broader

strategic aims.

In a world of increasing complexity and uncertainty, companies must build on

this foundation to manage risk more rigorously than ever.

A few fall victim to ‘black swan’ events – catastrophic external factors that are

entirely outside the company’s control – so rare and random that they challenge

the ability of organisations to plan for them. But many simply fail to understand

the extent of the dangers to which they are exposed. Board members are

particularly culpable, often underestimating the risks that their organisations

run, while also being blind to the dangers they face in a personal capacity, which

can result in financial penalties, criminal actions and ruined reputations.

(Chapter 11 of the Guide focuses specifically on the personal risks faced by

directors and officers.)

CHAPTER 1

8

RISKS IN THE REAL WORLDSome traditional risks remain common to all businesses, including risks related

to ‘bricks and mortar’, product liability and employer’s liability, among others.

Beyond these general business risks, different types and sizes of company tend to

face different sorts of risk. For example, small companies are especially

vulnerable to cashflow and credit risk, historically two of the greatest causes of

business failure when mishandled. In today’s difficult economic climate, small

firms are also more vulnerable to threats such as fraud, crime and vandalism.

The risk profile for mid-corporates too, has changed in response to tough

times. A 2010 report by Chartis, Risk and Opportunity in the Mid Corporate Sector,

concluded that companies of this size (£5m-£50m turnover) perceive the ‘post-

crisis’ world as a much more uncertain place. Over 80% think that risks now seem

more real – in terms of the seriousness of the impact they could have on their

business – compared with five to 10 years ago, while a similar majority believe

there are also more risks to worry about.

The research showed their top concerns as:

■ Safety of physical assets (30% of respondents)

■ Public liability (28%)

■ Employer’s liability (25%)

■ Debtors/bad debts (21%)

■ Professional indemnity and negligence (16%)

■ Crime and vandalism (14%)

■ Staff turnover (14%)

■ Product liability (14%)

■ Business interruption (14%)

■ Volatile global markets (12%)

EMERGING RISKSThe report also noted which of these risks have shot up the agenda as a result of

the economic downturn. They include, not surprisingly, concerns about debtors

and bad debts, and about over-reliance on a few suppliers. Similarly, professional

indemnity and negligence-related risks have become much more of a worry.

A WORLD OF DANGER

Other risks have grown in recent years, threatening companies of varying

sizes. Among the most dangerous are ‘cyber risks’. Any company dealing with

electronic data, whether on mobile devices, computers, servers or online, faces

such risks, which range from loss of information on a single laptop to the threats

posed by cloud computing. Businesses may also face issues regarding denial of

service or defacement and disruption to their web presence. According to the

Government’s Office of Cyber

Security and Information

Assurance, cyber crime – which

ranges from petty fraud to

competitor theft of intellectual

property and commercial

information – now costs UK

businesses £21bn a year.

Cyber risks are evolving and becoming more complex. Where organisations

have in the past invested in security and protection for their physical assets,

consideration now needs to focus on network and system safeguards.

INTERNATIONAL RISKSRecent years have seen the growing globalisation of business – and where

business goes, risk goes with it. Multinationals, which can include any company

with an overseas presence – not just the global giants – face a wide range of

potential dangers.

All multinationals, whatever their size, face supply chain risk. Today’s super-

efficient manufacturing practices exacerbate it, with supply chains so

streamlined that if anything goes wrong companies are very exposed. This was

highlighted by the sight of workers in the UK car industry – both in large plants

and in dependent smaller firms – being put on short time when Japan’s

earthquake and tsunami choked off component supplies. In another recent

example, supplier issues saw Marks and Spencer fall short of stock in some of its

best-selling clothing lines, causing a dent in its profits and its share price.

A worthwhile safeguard is to check out, through certification or other means,

the insurance coverage purchased by key suppliers. It is one thing to wait for

9

A WORLD OF DANGER

Multinationals, which can include any company with anoverseas presence, face a wide range ofpotential dangers

insurance payments to be made against a supplier having suffered a loss; it is

something else to have to source an unknown/untested supplier at short notice

because the incumbent isn’t insured and is unable to trade.

Trade credit risks (the risks to a company’s accounts receivables) are an issue

for a wide range of UK companies, including mid-corporates as they expand into

new territories.

In more unstable territories, political risks are always an issue to consider.

What happens if a government unilaterally cancels a contract, or even

nationalises a company – as has been seen in Argentina recently, with the state

taking control of Spanish oil company YPF Repsol. Politically motivated violence

can result in property or collateral damage for a company, and problems can

occur when equipment or currency cannot be repatriated.

There are other newly-established risks too, a prime example being

environmental liability. In line with the EU’s Environmental Liability Directive

(ELD), many European countries have recently introduced legislation that

requires companies to either buy environmental insurance or provide alternative

guarantees to fund the cost of damage to the environment that they may cause.

The ELD introduces two types of liability: ‘strict’ – in respect of environmental

damage caused by operators who professionally conduct potentially hazardous

activities; and ‘fault-based’ – in respect of environmental damage to protected

species and natural habitats from all other occupational activities. The

legislative changes affect different companies in different ways, but it is

important that all companies review if and how they are affected.

A key issue is the high degree of regulation of insurance, with significant

differences in various countries. It is essential that multinational companies

meet the tax and regulatory requirements in each jurisdiction in which they

operate. A prime example would be in the rapidly growing ‘BRICs’ (Brazil, Russia,

India and China). UK-written policies are often deemed ‘non-admitted’ in the

BRICs, so UK companies need to purchase cover in the local jurisdiction.

For insurable risk it is prudent for firms to choose an insurer whose

international presence matches their own – not only now, but also in the future if

looking to expand. Local knowledge and business relationships, commonality of

languages spoken and understanding of the local markets is not to be

10

A WORLD OF DANGER

underestimated. A global broker should also be considered to bring a local

tripartite relationship together to ease the resolution of issues.

REPUTATIONAL RISKSReputational risk too has grown in importance. In a 2011 report from the

Financial Reporting Council (FRC), Boards and Risk, participants from major

companies did not consider reputational risk to be a separate category, but a

consequence of failure to manage

other risks successfully. But the

report notes that the ‘grace period’

that a company has to deal with a

problem before it becomes

reputationally – and subsequently

financially – damaging, has been

sharply reduced. Developments in

media and communications, including social networking, mean that news of

failures or problems now often has an almost instantaneous impact locally and

internationally.

RISKS CAN BE MANAGEDThe ‘bottom line’ for businesses is that all of these risks are both identifiable

and manageable. Through ‘gap analysis’ you can identify risks that need

mitigating. For those risks that you feel you cannot retain, the next step is to

consider transferring them. Some may be passed to suppliers, customers or

sub-contractors through legal and contractual arrangements, while for others

risk transfer will involve the purchase of insurance.

The need to develop robust risk management strategies is evident. Used

effectively, they enable businesses to identify many potential threats and to

implement plans for mitigation. They also help to reduce costs and insurance

premiums. By taking a systematic approach to identifying, managing and

exploiting risk, many more UK businesses can build a stable, successful future.

11

A WORLD OF DANGER

By taking a systematicapproach to managingbusiness risk, manymore UK businessescan build a stable,successful future

12

A WORLD OF DANGER

Roads to Ruin, A Study of Major Risk Events: Their Origins, Impact and Implications, a2011 report by Cass Business School on behalf of Airmic, highlights seven key risk areasthat are potentially inherent in all organisations. They can pose a real threat to any firm,whatever the size, which fails to recognise and manage them. They are:

1. Board skill and NED control: risks arising from limitations in board skills andcompetence and on the ability of the NEDs effectively to monitor and, as necessary,control the executive arm of the company;2. Board risk blindness: risks from board failure to recognise risks inherent in thebusiness, including risks to business model, reputation and ‘licence to operate’, to thesame degree that they engage with reward and opportunity;3. Inadequate leadership on ethos and culture: risks from a failure of board leadershipand implementation on ethos and culture;4. Defective internal communication: risks from the defective flow of importantinformation within the organisation, including up to board level;5. Risks from organisational complexity and change: including risks followingacquisitions;6. Risks from incentives: including effects on behaviour resulting from both explicit andimplicit incentives;7. Risk ‘glass ceiling’: risks arising from the inability of risk management and internalaudit teams to report to and discuss, with both ‘C-suite’ executives and NEDs, potentialdangers emanating from higher levels of their organisation’s hierarchy, involving forinstance, ethos, behaviour, strategy and perceptions.

Case studies from Airmic’s Roads to Ruin report, illustrating many of these seven riskareas, are highlighted on pages 32, 39, 52, 60 and 72.

ROADS TO RUIN

13

THE BOARD’S DISTINCTIVEROLE IN RISK OVERSIGHTDr Roger Barker, Head of Corporate Governance, Institute of Directors

SNAPSHOT■ A key rationale for the board is to ensure that company decision-making is

undertaken in the interests of all relevant stakeholders, not just company insiderssuch as management or dominant shareholders.

■ The board’s biggest contribution to effective risk management is likely to be its choice of chief executive. But it also plays a key role in defining the company’s risktolerance and risk culture, and in identifying major risks that may have beenoverlooked or discounted by management.

■ The board’s main ongoing task is to perform risk oversight, so it needs to satisfyitself that effective risk management is being practised at all levels of theorganisation.

WHAT IS THE POINT OF THE BOARD OF DIRECTORS?A board of directors is a legal requirement for any corporate enterprise. However,

the justification for a board of directors in a modern quoted company owes more

to considerations of risk than the need to comply with regulation or statute.

In particular, the board can be seen as a direct response to a key risk posed by

the structure of the modern public company: that decision-making becomes

dominated by company insiders – particularly the chief executive and top

management – whose interests are not necessarily aligned with those of the

company’s stakeholders (particularly its shareholders). A large number of

corporate disasters over the last two decades have highlighted the saliency of

this risk.

The board of directors exists as a distinct layer of governance, sandwiched

between management and the company’s shareholders. In most countries,

national corporate governance codes or regulations stipulate that a majority of

board members should be independent non-executive directors. In addition, it is

increasingly seen as best practice for the board to be chaired by an independent

CHAPTER 2

14

chairman whose role and responsibilities are entirely separate from those of the

chief executive. In European countries with a dual board structure (for example,

Germany, the Netherlands and Switzerland) greater board independence is

sought by removing executives from membership of the board altogether (to

form the so-called supervisory board).

The motivation behind these structural requirements is to encourage the

board to think and act as an independent body, particularly in relation to

company management but also vis-à-vis any large shareholders that might

dominate the company’s agenda. In comparison with a board dominated by

company insiders, such a board is seen as being better able to make decisions

that are in the broader interests of the company as a whole.

It has not always been like this. Thirty years ago, the boards of most large UK

and US companies were almost

entirely populated by senior

managers. And outside the UK and

US, it remains common for directors

to be delegated to the boards of

listed companies as representatives

of dominant shareholders.

However, a governance structure

without an independently-minded board creates substantial risks for the

company and its stakeholders. A much discussed problem of corporate

governance – commonly referred to as ‘the agency problem’ – arises from the

risk that the executives hired to run the company will have a different business

agenda to that of the shareholders.

The risk of simply leaving management to its own devices is particularly acute

in stockmarket-listed companies due to the ‘laissez-faire’ governance approach

of many modern institutional shareholders. In contrast to the shareholders of

privately-held firms, such investors are distant from the company. Their

investment portfolios typically consist of small percentage equity positions in

hundreds of individual stocks. As a result their incentive to actively monitor the

risk-taking activities of management is limited.

Furthermore, they typically have no appetite to step ‘inside’ the company,

THE BOARD’S DISTINCTIVE ROLE IN RISK OVERSIGHT

First and foremost, theboard’s most importantcontribution to effectiverisk management islikely to be its choice ofchief executive

and serve on boards themselves, due to the constraints that this would impose on

their ability to buy and sell the company’s shares.

Reflecting their own limitations as governance monitors, institutional

shareholders have been key proponents of more independent boards over the

last couple of decades. From their perspective, a key role of the board is to act as a

neutral arbiter of company interests. This gives them greater confidence to

invest as minority shareholders.

More generally, an independently-minded board should be a source of

reassurance to all stakeholders. It reduces the risk that company decision-

making is dominated by one group or one person. It helps ensure that the

company’s activities are subject to objective challenge and risk-analysis by a

second group of independent experts. The board provides, in essence, the

ultimate risk management mechanism at the apex of the company structure.

THE BOARD’S RISK OVERSIGHT RESPONSIBILITIESOnce it has been established, the board has a number of unique roles with respect

to risk management, which are distinct from the risk management activities of

the top executive team.

First and foremost, the board’s most important contribution to effective risk

management is likely to be its choice of chief executive. If the wrong person is

appointed to lead the company, then all of the board’s subsequent efforts to

contribute to effective risk management will be severely compromised.

In cases where the chief executive’s approach to risk is not serving the

interests of the company, the board has an equally important role in replacing

him or her with a more appropriate candidate. This may not be a pleasant task.

But it is likely to be the single most important way that the board can contribute

to effective risk management.

A second basic issue for the board involves defining the nature and extent of

the risks that the company is willing to take. This is not just a question of listing

activities that the company should undertake or avoid. It is also about defining

an attitude to risk, a ‘risk culture’, that makes sense for the company as a whole.

Establishing the risk tolerance of the company should always be regarded as a

specific board responsibility. It should not be set by management or left to

15

THE BOARD’S DISTINCTIVE ROLE IN RISK OVERSIGHT

emerge by default without explicit discussion by directors.

A third area in which the board is well-placed to play a meaningful role is in

identifying risks to the organisation that the chief executive – for a variety of

reasons – may have overlooked or discounted. In more extreme cases, they could

be risks that management is actually attempting to conceal. Success in this role

will depend on the board being able to combine an independent critical mindset

with relevant business expertise.

Beyond these distinctive board level responsibilities, it is important for

directors to recognise that most risk management activities will not – and should

not – be directly undertaken by the board. Given the board’s relatively limited

resources, this would be an impractical task. Most risk management will be

performed by the CEO, individual line managers and specialist control

departments such as internal control, compliance, risk management, internal

audit and business continuity.

However, the board does have a key role to play in the ‘oversight’ of these risk

management activities. It should regularly satisfy itself that the company has

effective risk management and control systems in place. Furthermore, directors

should take steps to establish direct communication with relevant risk

management units and external sources of information (including possible

access to whistleblowers) in order to ensure that the board does not become

insulated from the reality of the company’s situation.

Directors also have a more informal role in ‘taking the temperature’ of the

organisation in order to clarify if the board’s chosen risk culture is being reflected

in the behaviour and attitudes of managers and employees on the ground.

A practical issue for the board is whether to delegate some of its risk oversight

activities to committees of smaller sub-groups of directors. As a bare minimum,

most large companies nowadays have audit, nomination and remuneration (or

compensation) committees, which are often mandated by regulation or national

corporate governance codes.

However, other types of committee may also be established to focus on

specific risk issues, for example, health and safety, corporate social

responsibility, or environmental issues. Overall responsibility for risk oversight

should always remain with the board as a whole. However, a board committee

16

THE BOARD’S DISTINCTIVE ROLE IN RISK OVERSIGHT

may assist overall board functioning by allowing a more detailed consideration

of important categories of risk.

An issue that has arisen in recent years concerns the potential establishment

of a designated risk committee. Risk committees are now a common feature of

many financial institutions. In that context, they are typically engaged in

overseeing the forward-looking risks arising from exposure to various kinds of

financial asset. However, risk committees are viewed as less relevant to non-

financial companies. In such enterprises, forward-looking risk assessment is

normally seen as a core activity of the board as a whole.

In summary, the board exists to

ensure that the company fulfils the

interests of its key stakeholders. In

such a role, it is an intrinsic part of

the company’s overall risk

management structure. However,

the challenges facing directors in

this task are considerable. The rest

of this book provides insight into how the board can rise to these challenges, and

help ensure that the company’s mission is not derailed by the impact of

inappropriate or unforeseen risks.

17

THE BOARD’S DISTINCTIVE ROLE IN RISK OVERSIGHT

It is important fordirectors to recognisethat most riskmanagement activitieswill not – and should not– be directly undertakenby the board

www.pwc.co.uk/riskresilience

Creating value in a turbulent world.

We help our clients to align their risk and business strategies so they’re more successful. Because putting risk at the centre of your business is now more important than ever before. To fi nd out more visit www.pwc.co.uk/riskresilience

© 2012 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom), which is a member fi rm of PricewaterhouseCoopers International Limited, each member fi rm of which is a separate legal entity.

27712.indd 1 02/05/2012 12:56:01

19

KEY CHALLENGES FACINGBOARDS IN RISK OVERSIGHT

Alpesh Shah, Actuarial Risk Practice Director, and Richard Sykes, Governance, Risk & Compliance UK Leader, PwC

SNAPSHOT■ Discharging the board’s duties and responsibilities around risk oversight

presents tough challenges. These include ensuring adequate ability to understand key risks, creating the time necessary to debate properly, and having the courage to stand up to management.

■ These challenges are further compounded by the variable quality of risk information reaching the board, the increasingly complex nature of organisations leading to complicated risk issues, and management’s potential conflict between managing or reducing risk and striving for improved performance.

■ The external perception of risk is also changing with the speed of risk impacts and the contagion between operational, financial and reputational consequences demanding increased agility from the board.

BALANCING RISK AND REWARD Discharging the board’s duties and responsibilities around risk oversight is oftennot straightforward and presents a range of challenges. At the heart of these

challenges are the perceived conflicting desires between striving for improved

performance, as demanded by shareholders and compelled by competitors, and

the need to understand and manage the risks in achieving this. While executive

and senior management will often be driven to improve performance to achieve

strategic objectives, reinforced by remuneration and incentive mechanisms, the

board needs to ensure that the risks taken by management to achieve these goals

are understood and appropriately mitigated. Most organisations’ remuneration

structures are geared towards rewarding exceptional performance, looking to

align the interests of management with shareholders to create value. Whilst in a

very limited number of financial sectors we are now starting to see incentive

mechanisms that reflect the amount of risk taken to deliver performance, the

CHAPTER 3

20

lack of a risk dimension for many does not support prioritising risk

considerations within the business. This can create potential tension in the

boardroom and between the board and senior managers.

In practice, this tension can manifest itself in a number of ways. Non-

executive directors (NEDs) will often have a less detailed awareness of the key

risks within the business compared to management. The nature of the role

means they will have access to less information than management on which to

assess the risks undertaken by the organisation. Addressing this information

asymmetry can often be a challenge.

The source of information around risks will vary significantly between

organisations. Some will rely on risks being identified and reported from lower

levels in the organisation, aggregated at a companywide level by someone

responsible for risk management. Others will rely on senior or executive

management preparing a suitable summary of key risks and responses for board

consumption. Such approaches are not always founded on underlying risk

indicators from within the business and may be unduly influenced by executive

perceptions of risks and board expectations.

The key question is how much of this risk information from the business is

provided to the board? Management will naturally seek to review and potentially

sanitise this information before presentation to the board. As a result, while

board members can gain some understanding of the effectiveness of risk

management from this process, the lack of detail or focus on key or emerging risk

issues will hamper the NEDs’ ability to discharge their duties in effective risk

oversight. Many organisations struggle to prepare an appropriate summary of

the risk profile of the company for board members, which succinctly articulates

the key risk exposures, threats and emerging issues. Often such analysis is

separate from discussions around strategy and performance. This hampers the

appreciation of risk in the context of returns for shareholders through achieving

strategic objectives. Often the risks that are most material to an organisation will

be those that disrupt the business’s ability to achieve its strategic objectives.

Understanding how much risk has been taken in the pursuit of strategic

performance is one of the ways in which the board can understand if the current

risk profile is appropriate.

KEY CHALLENGES FACING BOARDS IN RISK OVERSIGHT

Even if appropriate information is provided to the board, there is often a

hurdle for NEDs in appropriately understanding and challenging this

information. This is more acute for those NEDs who come from unrelated

industries and so may not have the same level of understanding of risks within

the industry. The responsibilities of

directors are ever-increasing and

many NEDs commonly comment

that these responsibilities need to

be discharged within significant

limitations of time and resources.

How much time does the board, and

NEDs in particular, devote to

understanding and addressing risk issues? While for many companies risk is

playing an increasing role at board discussions, the complexities of

organisations and the risk issues they face require increasing time and resources

to be fully understood.

Putting this in the context of an increasingly complex and diverse business

and risk environment compounds the problem. Today, companies are faced with

a larger range of risks from an increasing variety of sources. This changed risk

landscape has resulted in more recognition of the potential exposure to extreme

risk events that are both very hard to plan for and typically lead to significant

adverse consequences for organisations. These ‘black swan’ risks require a

broader and potentially varied risk management response from organisations

and clear direction from boards. The challenge for boards is to broaden the

nature and richness of the risk discussions they have, to ensure they give

appropriate attention to all types of risks.

In addition, the speed at which risks manifest themselves and have an impact

on the organisation is quickening. In the past, the impact of operational failures

could often be managed internally with limited reputational and external

impacts. Today, any risk event is potential headline news, resulting in

reputational and business effects on the organisation. This ‘risk contagion’,

where the impact of operational risk quickly leads to reputational and broader

business effects, demands agility of response to minimise the impact on the

21

KEY CHALLENGES FACING BOARDS IN RISK OVERSIGHT

The challenge for boards today is toensure that they andtheir companies are prepared to respondquickly to risk eventsshould they occur

organisation. Boards are often not able to respond with the speed and agility

required during and immediately after the occurrence of risk events. The

challenge for boards today is to ensure that they and their companies are

prepared to respond quickly to risk events should they occur.

Reputational impacts are becoming a more significant driver of risk

considerations. Traditional risk management approaches have often tried to

measure risk impacts financially. Understanding the reputational effect of risks

and weighing this against financial and other impacts is becoming increasingly

important and presents new challenges for both board members and companies’

risk management functions.

Organisations operate within a variety of corporate governance structures.

Within whatever framework is adopted, the need for clear risk oversight from the

board, which is distinct from management, is essential. NEDs bring valuable

insights from other companies, industries and geographies and these will

include perspectives on risks and risk management. One of the more significant

challenges to good risk management within organisations is the lack of breadth

of risk thinking. There is a danger that risk management is often focused on

health and safety, financial or operational issues that are the forefront of day-to-

day business activity. The broader perspective on a variety of risks that comes

from the diversity of the board, including exogenous hazards and strategic

threats, helps support a richer and more comprehensive risk management

process. Demonstrating the potential relevance of these external, independent

views to the organisation and getting senior management and executive buy-in

present an additional challenge for the board.

Even when boards understand risks, how well do they appreciate the reliance

placed on key risk mitigation? For some risks, insurance may provide an essential

cushion against the financial impact

of risk events. However, insurance is

a complex product and there is

increasing recognition that the risk

of insurance coverage being

misaligned with the changing risk

profile of an organisation may

22

The broader perspectiveon a variety of risks thatcomes from the diversityof the board helpssupport a morecomprehensive riskmanagement process

KEY CHALLENGES FACING BOARDS IN RISK OVERSIGHT

compromise the quality of this key mitigation tool. Given these complexities,

how can the board effectively challenge and gain comfort that insurance cover

will be in place where needed?

For other risks, key operational and other controls should help manage risk

exposures to acceptable levels. The board will often seek assurance from internal

and external audit around the effectiveness of some controls. However, many

risk management frameworks fail to appreciate the true risk exposure before

credit is taken for any controls. As such, less emphasis is placed on the value of

controls in reducing the impact and likelihood of risk events occurring. It is often

the failure of one or more of these controls that leads to a previously well-

controlled risk having a material and unexpected impact on an organisation. In

addition to understanding the underlying risks within the business, boards need

also to understand the reliance being placed on key controls.

There is often a desire for unity of thinking and opinion around the board

table. This may engender confidence in external stakeholders and internal

management that the strategic direction of the organisation is sound and

supported by all. However, the role of NEDs in challenging executives and senior

management is essential to good governance. The challenge around risk is no

exception. Appropriate risk information needs to be available to the whole

board; the board needs sufficient risk management competency to assess this

information effectively; and there needs to be an open and constructive dialogue

between executive and non-executive directors around risk issues.

KEY QUESTIONS FOR BOARD MEMBERS■ Is the quality and breadth of risk information you see on the board enough

for you really to understand the organisation’s risk profile?

■ How confident are you in your board’s ability to understand and challenge

the organisation on the effective management of risk?

■ How prepared and agile is your organisation and the board to respond to

risk situations should they arise?

23

KEY CHALLENGES FACING BOARDS IN RISK OVERSIGHT

24

The growing importance placed on corporate governance has enhanced the role ofthe company secretary. The holder of the post is now seen in many respects as theguardian of a company’s governance and an independent adviser to the board. TheFinancial Reporting Council (FRC), in its most recent revision of the UK CorporateGovernance Code, makes this point: “The company secretary should be responsible foradvising the board through the chairman on all governance matters.”

The secretary thus has a responsibility to all directors, but for practical reasons, thechairman needs to retain some control. The Code sees the secretary as a resource forthe whole board: “All directors should have access to the advice and services of thecompany secretary, who is responsible to the board for ensuring that board proceduresare complied with.”

The administrative role is crucial: “Under the direction of the chairman, the companysecretary’s responsibilities include ensuring good information flows within the boardand its committees and between senior management and non-executive directors, aswell as facilitating induction and assisting with professional development as required.”

Not only is the secretary in many ways a chief of staff to the chairman in running anefficient and effective board, but there is also a relationship with each director, whomight seek the independent view of the secretary on an area of potential dispute orcontroversy. (This is why it can be problematic if an executive director is also thecompany secretary.)

Non-executives can in particular look to the secretarial team for help and guidance intheir role and to understand fully proposals coming before the board. If they want toseek independent advice outside the company (as encouraged by the Code), that canoften be achieved through the company secretary.

Induction of new directors was an area highlighted by the 2009 Walker review as ameans of improving the effectiveness of non-executive directors, who might come totheir post with little or no knowledge of the workings of the company and its board, andpossibly little experience of its business sector. The secretary has a key role in designingand implementing an induction process that quickly and efficiently gives directors theknowledge they need to play a full part in the boardroom.

For a company secretary’s perspective on risk management information and theboard, see Chapter 9.

KEY CHALLENGES FACING BOARDS IN RISK OVERSIGHT

THE PIVOTAL ROLE OF THE COMPANY SECRETARY

Source: The Director’s Handbook, IoD/Kogan Page, 2010

25

THE BOARD’S ROLE INESTABLISHING THE RIGHT

CORPORATE CULTUREProfessor Roger Steare, Corporate Philosopher in Residence and Professor of Organisational Ethics at the Cass Business School

SNAPSHOT■ Good corporate governance is primarily dependent on board members defining a

clear moral purpose and modelling core values, sound judgement and leadershipbehaviours.

■ Having a good corporate governance structure and effective processes and systems are also important, but these exist to measure core leadership qualities.

■ The mitigation of risk begins with a clear and deep understanding of human behaviour in the workplace. Robots are designed to comply with clear instructions; human beings need inspiration.

MANAGING RISK – IT’S ABOUT PEOPLE AS WELL AS PROCEDURES“Leadership is a potent combination of strategy and character. But if you mustbe without one, be without the strategy.” General Norman Schwarzkopf

To understand how to manage risk, look at how people manage risk in extreme

environments. Managing risk in war is a great example. Strategy, planning,

training, rehearsal and operational excellence are vital. But without character,

just cause, judgement, courage, and love for country and comrade, they will lose

and they may die.

In business, unless the board displays the same understanding of how to lead

‘hearts and minds’, then no matter how diligent its governance structure,

processes and systems, its plan will not survive contact with the reality of human

character, judgement and behaviour.

The overwhelming evidence of history is that human communities only

function and sustain themselves when people:

CHAPTER 4

26

■ Have a clear moral purpose;

■ Truly care for each other;

■ Co-operate and make good decisions about how to get the scarce resources

they need in a hostile environment;

■ Do all these things in a way that sustains their environment for

future generations.

Governments and business leaders who build a cage of laws, regulations and

internal processes become high risk, dysfunctional, mindless, fear-driven,

bureaucratic, totalitarian communities, dominated and exploited by narrow

elites. Just as we are seeing the decline of totalitarianism in the nation-state, for

example in Egypt, Libya and Syria, we are also seeing the end of the corporation

as a feudal construct. Yes, organisations need effective governance to help

mitigate risk. But without moral purpose, character, judgement and behaviour,

they will not prosper or survive.

THE MORAL PURPOSE OF BUSINESSWhy does a business exist? Perhaps it is to make money. But unless it is clearly

understood how it makes money, it will not make money for long.

The reality is that the purpose of business is to offer human beings a social

environment to co-operate and to share know-how and resources in order to

meet their needs. A business only exists when it functions as a community that

brings together investors, entrepreneurs, employees, customers, suppliers and

communities to provide goods and services to each other. Whilst making money

is an important measure of success for investors, entrepreneurs and employees,

a business will not make money for long unless its customers get quality goods

and services at a price that is fair. It will also fail to make money for long unless it

treats the members of these various stakeholder groups with empathy, fairness

and respect. This is the moral component of purpose in business.

Some good examples of well-run businesses with a clear moral purpose are

Nationwide Building Society, The Co-operative Group and The John Lewis

Partnership. These businesses have not only survived in the current economic

downturn, they have positively thrived. It is no accident that each of these

THE BOARD’S ROLE IN ESTABLISHING THE RIGHT CORPORATE CULTURE

businesses is a mutual or partnership. Mutuality is the form of association that

underpins families, friendships and the best local communities. It has been

proven over thousands of years. Corporatism, on the other hand, is good for

short-term success, but bad for risk and for sustainability.

CHARACTER, JUDGEMENT AND BEHAVIOURThe banking crisis of 2007-9 prompted several inquiries into the apparent

failures of governance that precipitated it. They included the Walker Review into

the corporate governance of banks, which for the first time addressed the

question of the ‘character’ of bank directors and senior managers.

The Financial Reporting Council (FRC) also reviewed its UK Corporate

Governance Code. I co-authored a submission to the FRC’s review with David

Phillips, Senior Corporate Reporting at PWC, which sought to address the same

issues of the character, judgement and behaviour of directors and boards. The

submission stated:

“Character, judgement and behaviour are connected stages in a process.

Character or integrity is the sum total of all our moral values and informs the

behaviour of trusted adults. Good collective judgements and decisions are made when

we consider not only legal rules and obligations (which should be regarded as the

‘letter’ of the law), but also how our values (the ‘spirit’ of the law) help us to decide

fair and reasonable outcomes for all stakeholders. We must also acknowledge that

this process will vary according to the situational context faced by boards. As a

consequence, it is critically important not only that the behaviours of organisations

are better understood, but that there are processes in place to monitor the

environments in which they operate, particularly to identify those situations when

rational human behaviour is most challenged.”

The fundamental failure of governance that precipitated the banking crisis

was not because directors failed to understand financial risk; it was because they

failed to govern with courage and integrity. This failure was not caused by a lack

of technical knowledge; it was caused by failures of character, judgement and

basic arithmetic. As we continue to pick over the wreckage of our financial

27

THE BOARD’S ROLE IN ESTABLISHING THE RIGHT CORPORATE CULTURE

system, it is clear that many post-mortems into corporate governance are fixated

by board structures, remuneration policies and risk management systems. They

do not focus in any meaningful way on the behaviour of human beings, per se.

It is baffling that boards, government and regulators seem to ignore the

powerful tools now available to measure and change human character,

judgement and behaviour. Even bus drivers are routinely given personality tests

to measure whether or not they can exercise self-control in stressful driving

conditions. So why not also test directors and senior managers to understand

their character and decision-making skills?

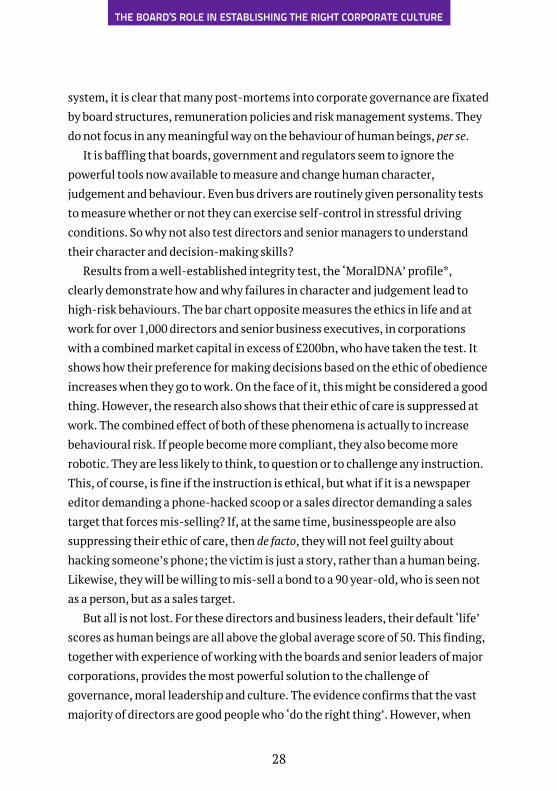

Results from a well-established integrity test, the ‘MoralDNA’ profile*,

clearly demonstrate how and why failures in character and judgement lead to

high-risk behaviours. The bar chart opposite measures the ethics in life and at

work for over 1,000 directors and senior business executives, in corporations

with a combined market capital in excess of £200bn, who have taken the test. It

shows how their preference for making decisions based on the ethic of obedience

increases when they go to work. On the face of it, this might be considered a good

thing. However, the research also shows that their ethic of care is suppressed at

work. The combined effect of both of these phenomena is actually to increase

behavioural risk. If people become more compliant, they also become more

robotic. They are less likely to think, to question or to challenge any instruction.

This, of course, is fine if the instruction is ethical, but what if it is a newspaper

editor demanding a phone-hacked scoop or a sales director demanding a sales

target that forces mis-selling? If, at the same time, businesspeople are also

suppressing their ethic of care, then de facto, they will not feel guilty about

hacking someone’s phone; the victim is just a story, rather than a human being.

Likewise, they will be willing to mis-sell a bond to a 90 year-old, who is seen not

as a person, but as a sales target.

But all is not lost. For these directors and business leaders, their default ‘life’

scores as human beings are all above the global average score of 50. This finding,

together with experience of working with the boards and senior leaders of major

corporations, provides the most powerful solution to the challenge of

governance, moral leadership and culture. The evidence confirms that the vast

majority of directors are good people who ‘do the right thing’. However, when

28

THE BOARD’S ROLE IN ESTABLISHING THE RIGHT CORPORATE CULTURE

people come to work, they suppress some of their judgement and some of their

humanity. They become thoughtless and careless. The simple but challenging

solution is to create the right environment, the right culture, for directors, for

leaders and for all employees to bring their humanity to work.

“CULTURE EATS STRATEGY FOR BREAKFAST”This is a quote from a very senior executive responsible for safety at one of the

major oil and gas players. The point he was making is that managing risk in high-

risk businesses such as his ultimately boils down to the character, judgement and

behaviour not just of individuals, but of social groups in the workplace. This is

what we call ‘culture’. Every workplace has a culture. But it is self-evident that

many boards and senior executive teams do not properly understand the culture

of their business and then, by definition, fail to influence it in a way that not only

mitigates risk but also enhances the value of the business.

Returning to the aforementioned submission to the FRC, the following were

the recommendations on leadership and culture:

29

THE BOARD’S ROLE IN ESTABLISHING THE RIGHT CORPORATE CULTURE

MoralDNA™ Ethics in Life and at Work

Scores

58

57

56

55

54

53

52

51

50

49

48

Ethic of Obedience Ethic of Reason

Life

Work

Ethic of Care

THE BOARD’S ROLE IN ESTABLISHING THE RIGHT CORPORATE CULTURE

“Character and behaviourFurthermore, we believe the system can be further strengthened if work is undertaken

to increase boards’ understanding and awareness of the character and behavioural

mix that is more likely to support an effective governance environment. In particular

we suggest that the FRC should:

■ Conduct research and encourage market experimentation around the use of

tools and techniques that can be used to assess the character and behavioural

profile of directors and boards; and

■ Consider ways in which boards and individual directors can develop a

conscious, diligent and verifiable collective decision-making process, that

captures the essence of what is meant by the FRC in its references to ‘character’

and ‘behaviour’ throughout its July 2009 consultation document.

External reporting – exposing culture, values and behavioursIn a similar vein to the point made above, it may also be beneficial for boards to

explain the behavioural tone which is established in the way it engages with

shareholders and the management team and in the actions it takes. This can be seen

as a statement of ‘who we are’ and ‘what we stand for’. In this context, boards may

wish to explain what management style and behavioural norms they encourage and

what behaviours they will not tolerate. Here an understanding of the actions and

penalties that have been put in place to deal with such exceptions could provide

added impact.”

THE MORAL MAZEThe challenge for boards is to decide whether corporate governance can be

effective without moral leadership and culture. If the answer is ‘no’, then board

members need to understand their personal and collective character, judgement

and behaviour. This requires insight, oversight and expertise not found in

rulebooks, tick-boxes and codes of conduct, but in moral philosophy and social

psychology. In short, they need to understand who they are, how they decide

what is right, what they do and their role as leaders in meeting these challenges.

30

THE BOARD’S ROLE IN ESTABLISHING THE RIGHT CORPORATE CULTURE

KEY ACTIONS FOR BOARD MEMBERS■ Question the purpose of your business. Is it meeting the needs of all your

key stakeholders?

■ Challenge your own values, decision-making and behaviours as leaders.

Are you bringing your humanity to work?

■ Ask colleagues, customers, suppliers and local communities how they really

feel about your business. Does it inspire them? Do they love it? Why and in

what way?

■ When you have the answers to these questions ask yourself: “What are we

doing well that we need to keep doing?”, “What are we beginning to do

well, but need to do more of?” and “What are we not yet doing and need to

begin?”

CONTRIBUTORProfessor Roger Steare FRSA is ‘The Corporate Philosopher’. He is Corporate

Philosopher in Residence and Professor of Organisational Ethics at the Cass Business

School, City University London. He is a Fellow of cross-party policy think tank,

ResPublica, and consults with major corporations such as BP and HSBC, the

Financial Services Association (FSA) and the Serious Fraud office (SFO) on better

regulation and enforcement. Visit: www.TheCorporatePhilosopher.org and

www.ethicability.org

* The MoralDNA profile is a short personality test that sets out to reveal a person’s

moral values and the way they prefer to make decisions about what is right.

Developed in 2008 by Professor Steare and chartered psychologist, Pavlos

Stamboulides, the profile now measures 13 factors to describe character and

judgement and has so far been completed by more than 50,000 people from over 200

countries, many of them business leaders. The results from this research are now

being referenced by the FSA and the SFO, given their respective mandates on

mitigating financial market and corruption risks. To take the profile, visit

www.MoralDNA.com

31

THE BOARD’S ROLE IN ESTABLISHING THE RIGHT CORPORATE CULTURE

32

Mr Arthur E. Andersen, founder of Arthur Andersen, cemented his reputation when hetold a local railroad chief that there was not enough money in Chicago to persuade himto enhance reported profits by using ‘creative’ accounting. He lost the account – but therailroad firm went bankrupt soon afterwards. Mr Andersen had a clear moral compass.

By the 1980s, the firm was adopting the ‘Big Five’ auditors’ new business model:grow the business by selling consultancy on the back of the audit relationship. Andersenembraced a ‘2x’ model – bring in twice as much consultancy as audit revenue. Thosewho succeeded in doing so were rewarded, while those who did not faced sanctions.Fear of losing consultancy work must have pervaded audit teams.

Through its work for Enron, Andersen earned $25m in audit fees and $27m inconsultancy fees in 2000. Over the years, Andersen had been involved in creating andsigning off creative accounting techniques, such as aggressive revenue recognition andmark-to-market accounting, along with the creation of special purpose vehicles (SPVs)for doubtful purposes. By 2001, the firm was sufficiently concerned for 14 partners,eight from the Houston office that handled Enron, to discuss whether they retainedsufficient independence from Enron. Having observed that revenues could hit $100m,they decided to keep Enron’s account. Mr Andersen might have acted otherwise.

As news of the US Securities and Exchange Commission’s (SEC) investigation intoEnron spread to Andersen, the Houston practice manager pronounced that, while theycould not destroy documents once a lawsuit had been filed, “if [documents are]destroyed in the course of the normal [destruction] policy and the next day a suit is filed,that’s great.” In the following days, Andersen’s shredders in Houston, London andelsewhere worked overtime. This loss of moral compass was key to the firm’s collapse.

Smaller firms are far from immune to defective business culture, misalignedincentives and, as a result, inappropriate behaviour. Furniture retailer, Land of Leather,for example, focused largely on deriving profit from the peripheral activities of sellingwarranty and PPI insurance, and rewarded staff accordingly. This created the risk thatmanagement and staff would neglect key issues of safety, quality and customerservice. The firm was among retailers that subsequently sold leather furniturecontaminated by a mould-inhibiting chemical. The direct effects of the ‘toxic sofa’cases included injuries to at least 4,500 people, and some £20m of claims by themagainst the firms responsible – a major factor in Land of Leather’s collapse in 2007.

Boards should be aware that the incentives they create or encourage can distort theoutcomes they wish to achieve.

THE IMPORTANCE OF BUSINESS CULTURE, INCENTIVES AND BEHAVIOUR

33

RISK AND STRATEGY

Alpesh Shah and Richard Sykes, PwC

SNAPSHOT■ Risks can be considered to be those things that affect the ability of an organisation

to achieve its strategic objectives.■ In order to improve performance and increase value, risks must be accepted – as

the old adage goes, ‘There’s no such thing as a free lunch’. Given this, it is important that any consideration of the risks within an organisation takes place within the context of the strategy.

■ It follows that any determination of strategy should take account of the risks the organisation is exposed to. As risk and strategy are highly related, the challenge for boards is to align the risk and strategy discussion.

RISK AND REWARDGood risk management not only requires appropriate identification, assessment

and reporting of risks to the board to determine an organisation’s risk profile, but

also essential is an understanding of how much risk is acceptable and how much

the organisation can bear. All organisations need to take on some risk in order to

achieve strategic objectives and deliver returns. The key risks that an

organisation is exposed to will be those that affect its ability to achieve its

strategic or performance objectives. As such, any discussion on how much risk is

acceptable to an organisation needs to be made in the context of its strategic

objectives. The danger is that risk discussions often happen as a separate process

within the organisation and therefore fail to get an appropriate level of board and

management attention.

Discussions in the boardroom will often focus on setting and achieving key

strategic objectives that are intended to support or enhance the business value

chain and so protect or improve the organisation’s value to its stakeholders. This

will be measured as performance and reflected in management incentives and

board remuneration. Implicit within any organisation’s value chain, however, is

CHAPTER 5

34

exposure to a variety of risks. Collectively this can be referred to as the

organisation’s risk profile. Any changes to the business value chain, through the

implementation of strategy for example, will affect the risk profile. So, an

understanding of the value-adding benefits of strategic options should also

consider the implications for the risk exposures of the organisation. The desired

balance between risk and value is often referred to as ‘risk appetite’.

The determination of risk appetite will be driven by a range of external

influences, including shareholders, analysts, regulators, rating agencies,

competitors and customers. Risk appetite is essentially an articulation of the

amount of risk that the organisation will take in order to achieve its strategic

objectives. It is a tool with which the board can try to capture the expectations of

these external stakeholders, coupled with management’s and their own

expectations. Chapter 5 discusses how boards can articulate risk appetite.

Boards can improve their focus on risk and risk management by integrating

risk into the board strategic debate. Board members will often dedicate a

reasonable amount of their time to understanding, reviewing and challenging an

organisation’s strategy. Board strategy awaydays and dedicated planning

sessions are not uncommon and will be familiar to many. But how much does risk

form a key part of these discussions?

Understanding the key risks to the business, either from internal sources or

the environment in which it operates, should be a major influence of strategic

direction. These may be different and distinct from the risks to achieving

strategic objectives, which will focus on the key assumptions made in setting the

RISK AND STRATEGY

Risk Management Actions

RiskAppetite

Value

Risk

Performance

Risk Profile

Business Value ChainStrategicobjectives

expected outcome of the strategy. While there is often focus by boards on the

risks involved in achieving strategic objectives, there is often a lack of

appreciation of the breadth of key risks that accompany the business, and within

which the strategy needs to deliver.

Boards should ensure that any discussion around strategy considers the full

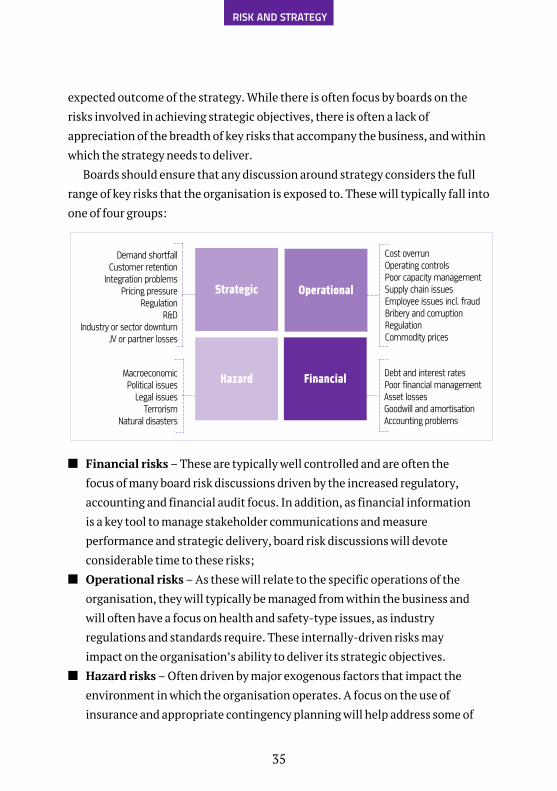

range of key risks that the organisation is exposed to. These will typically fall into

one of four groups:

■ Financial risks– These are typically well controlled and are often the focus of many board risk discussions driven by the increased regulatory,

accounting and financial audit focus. In addition, as financial information

is a key tool to manage stakeholder communications and measure

performance and strategic delivery, board risk discussions will devote

considerable time to these risks;

■ Operational risks– As these will relate to the specific operations of the organisation, they will typically be managed from within the business and

will often have a focus on health and safety-type issues, as industry

regulations and standards require. These internally-driven risks may

impact on the organisation’s ability to deliver its strategic objectives.

■ Hazard risks– Often driven by major exogenous factors that impact the

environment in which the organisation operates. A focus on the use of

insurance and appropriate contingency planning will help address some of

35

RISK AND STRATEGY

Strategic

Hazard Financial

Operational

Demand shortfallCustomer retention

Integration problemsPricing pressure

RegulationR&D

Industry or sector downturnJV or partner losses

MacroeconomicPolitical issues

Legal issuesTerrorism

Natural disasters

Cost overrunOperating controlsPoor capacity managementSupply chain issuesEmployee issues incl. fraudBribery and corruptionRegulationCommodity prices

Debt and interest ratesPoor financial managementAsset lossesGoodwill and amortisationAccounting problems

these. However, there is often a danger that as many of these risks cannot

be controlled, boards and senior management will not reflect these in their

strategic thinking. The mindset that strategy is focused on controllable

factors creates the danger of not appropriately reflecting these risk drivers.

■ Strategic risks– These include risk factors that are typically external or impact the most senior management decisions and, as such, are often

missed from many risk registers. It is incumbent upon boards to ensure all

these types of risks are included in the strategic discussion.

The external viewpoint that non-executive directors (NEDs) can bring to the

boardroom will play an essential part in ensuring this breadth of risk thinking

enhances the development of strategic thinking. The challenge for boards is to

ensure the processes followed to review and approve strategy can be flexed to

include an appropriate consideration of risk. There is a range of approaches that

may be considered.

A well-defined understanding of what risk means relative to strategy is

essential. The achievement of strategic objectives will often be expressed as one

or more key strategic intents or visions. Examples include: “Increasing revenue

by £Xm in the next year; increasing market share in core markets by Y%;

improving customer churn rates/satisfaction metrics by X”. In setting these

strategic objectives, it is the intent of the board and senior management that, in

achieving them, the value of the organisation will increase or be protected for its

shareholders (or for key

stakeholders for non-profit

organisations).

The impact of risk events can be

expressed as an acceptable variation

in these strategic goals that

management is prepared to accept

to achieve them (for example, 2%

growth with virtual certainty, or 10% growth with increasing risk of losses).

While not all risks can be mapped back to a defined impact on strategic outcome

metrics, the discipline of considering risks in this context will help boards to

36

RISK AND STRATEGY

The challenge for boardsis to ensure theprocesses followed toreview and approvestrategy can be flexed toinclude an appropriateconsideration of risk

understand the potential impact of these risks and prioritise management effort

to manage them accordingly.

SOME OF THE KEY QUESTIONS THAT BOARDS SHOULD ASK AROUND STRATEGY AND RISK ARE:How well is my strategy actually defined?A good understanding of the key risks to strategic intent and the value of the

organisation require a good understanding of the strategy itself. A robust

articulation of the key elements of strategy (strategic intent, strategic

drivers/actions, the context within which the strategy will be delivered etc.) will

allow boards to isolate and identify how the strategy will interact with the risks

faced by the business. A lack of clarity around the strategy will encourage risk

and strategy to continue as two separate processes within the organisation.

Bringing these processes together will help align risk management to the

strategic delivery plan.

How broad are the risks we are considering?Strategy needs to be defined in the context of the risk environment in which the

business operates. The broader the consideration of the types of risks the

business faces, the better the strategy can be developed to respond to or navigate

these risks. Bringing together the internal risk information from the business

with an understanding of exogenous risk exposures as highlighted by senior

management and NEDs in particular, should be a key focus of the board.

What risk scenarios have we considered to test our plans?It is often not easy to identify all potential risk exposures and their causes. Those

risks that are going to be of most interest to the board will often be defined by the

potential impact of the consequences of the risk manifesting. Scenario analysis,