Title: CASH HOLDING – THE SIGNAL FOR MERGERS AND ACQUISITIONS IN NON-FINANCIAL ACQUIRING FIRMS CASE: JAPAN NIKKEI 225 2018 Master’s Thesis Graduate School of Business Student ID 3 D 1 6 0 1 3 0 Name PHAN VIET HUNG Submission Date (yyyy/mm/dd) 2018 / 06 / 29 Supervisor Professor Philip Sugai

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Title:

CASH HOLDING – THE SIGNAL FOR MERGERS AND ACQUISITIONS IN

NON-FINANCIAL ACQUIRING FIRMS

CASE: JAPAN NIKKEI 225

2018 Master’s Thesis

Graduate School of Business

Student ID 3 D 1 6 0 1 3 0

Name PHAN VIET HUNG

Submission Date

(yyyy/mm/dd)

2018

/

06

/

29

Supervisor Professor Philip Sugai

DECLARATION OF ORIGINALITY OF WORK

I affirm that the attached work is entirely my own except where the words or ideas of other

writers are specifically acknowledged through the use of inverted commas and in-text

references. This assignment has not been submitted for any other subject at Doshisha

University (or other institution). I have revised, edited, and proofread this paper.

Word count: 10,123

Student signature:

I

ABSTRACT

This research empirically tests the relation between M&A and Cash holding

level in turbulent context of Japanese economies with double finance crisis in the

period of 2009-2013. The fact, that the cash holding in Japanese non-financial

firms climbed rapidly while the M&A value just fluctuated or even went down in

this period, need to be relooked by agency problem and related concepts. The

empirical evidence shows that there is no significant difference of M&A value

among the groups of Cash holding levels in the scope of Japanese Nikkei 200 non-

financial firms in this period. The research points out the absence of agency

concept in M&A value and utilizes the light of precautionary motive to cover.

CASH HOLDING – THE SIGNAL FOR MERGERS AND ACQUISITIONS IN

NON-FINANCIAL ACQUIRING FIRMS

…

CASE: JAPAN NIKKEI 225

Hung Phan Viet

June 2018

Keywords: Cash holding; Cash holding level; M&A value, agency problem.

II

DEDICATION

…

With all respect and love, to my parents,

who have supported me all things, from material to spirit,

who have sacrificed all things they have for me without recalling,

who have reminded me that I owe to the world, and my responsibility is contributing

my life to make it more beautiful,

and who I just have once in my life

…

To my dear,

who wakes up me in the dayspring to enjoy together with study and work passion,

who encourages me when I feel tired after the heavy workload,

who is my inspiration in my all works and paths I have experienced

III

ACKNOWLEDGMENT

…

I thank the Konosuke Matsushita Memorial Foundation (松下幸之助記念財団) for their vital

financial funding in the two-year period of academic life in Japan 2016-2018.

I thank the Doshisha University Graduate School of Business - Global MBA program with

excellent and enthusiastic faculty and staff for making the valuable two-year academic period.

I specially thank Professor Philip Sugai for the outstanding instruction. You make me realize

clearly how to define and solve the research issues and sharp highly my researching mindset

in the statistics section. “Standing on the giant shoulders” should be my core method I apply

to all next paths of academic and real life.

I also thank Professor Shigeru Matsumoto for the guiding of initiation in research theme of

Mergers and Acquisitions.

I thank my friends who support me to achieve the necessary database to conduct my research.

I also thank the people who share to me the knowledge, opinions, and consulting to my

research theme of Nikkei 225. Without their aids, the research will confront the issues of

sufficiency and accuracy.

Finally, I thank all my foreign friends in Japan and Vietnam, in global MBA program, in

various cities I have lived in Japan for all your loves and supports. I always cherish and keep

my whole life.

IV

TABLE OF CONTENTS

DEDICATION .................................................................................................................................. II

ACKNOWLEDGMENT ................................................................................................................... III

TABLE OF CONTENTS ................................................................................................................. IV

LIST OF TABLES ........................................................................................................................... VI

LIST OF FIGURES ......................................................................................................................... VI

LIST OF ABBREVIATIONS ......................................................................................................... VII

CHAPTER 1: INTRODUCTION ........................................................................................................1

1.1. Background ..............................................................................................................................1

1.2. Research problem .....................................................................................................................3

1.3. Research question.....................................................................................................................8

1.4. Research objectives ..................................................................................................................8

1.5. Research outline .......................................................................................................................9

CHAPTER 2: LITERATURE REVIEW ........................................................................................... 12

2.1. Theory review ........................................................................................................................ 12

2.2. Empirical evidence review ...................................................................................................... 14

CHAPTER 3: METHODOLOGY ..................................................................................................... 15

3.1. Data sample ........................................................................................................................... 15

3.2. Methodology .......................................................................................................................... 19

CHAPTER 4: FINDING & DISCUSSION ........................................................................................ 30

4.1. Finding................................................................................................................................... 30

4.1.1. Description of Cash holding & M&A ............................................................................... 30

4.1.2. The result of statistical tests ............................................................................................. 31

4.2. Discussion .............................................................................................................................. 40

CHAPTER 5: CONCLUSION .......................................................................................................... 45

V

5.1. Summary ................................................................................................................................ 45

5.2. Contribution and recommendation .......................................................................................... 47

5.2.1. Contribution .................................................................................................................... 47

5.2.2. Recommendation ............................................................................................................. 50

5.3. Limitation and future research ................................................................................................ 51

APPENDIX ...................................................................................................................................... 53

Appendix 1: The Market Cap data between Nikkei - TSE: The data in 2009- 2014 ...................... 53

Appendix 2: Why Exclude 25 Financial companies ....................................................................... 55

Appendix 3: Descriptive table about median of cash holding in whole 200 Nikkei and every

industry group in Nikkei 200 ......................................................................................................... 56

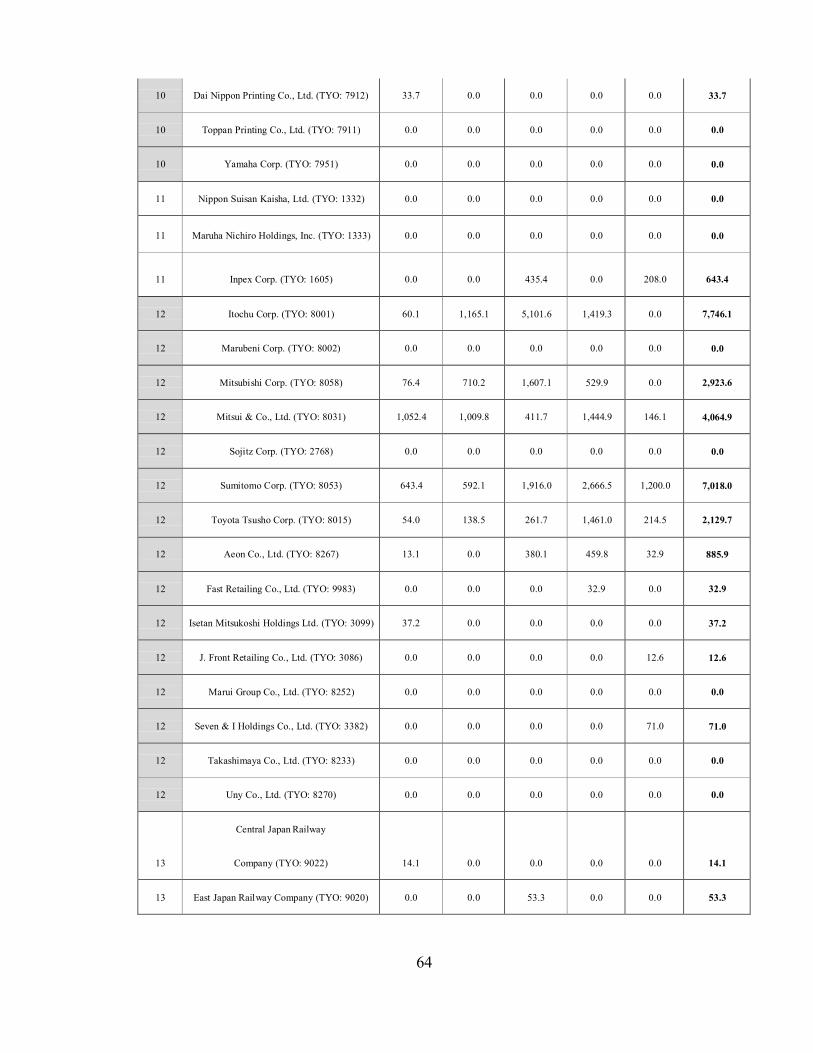

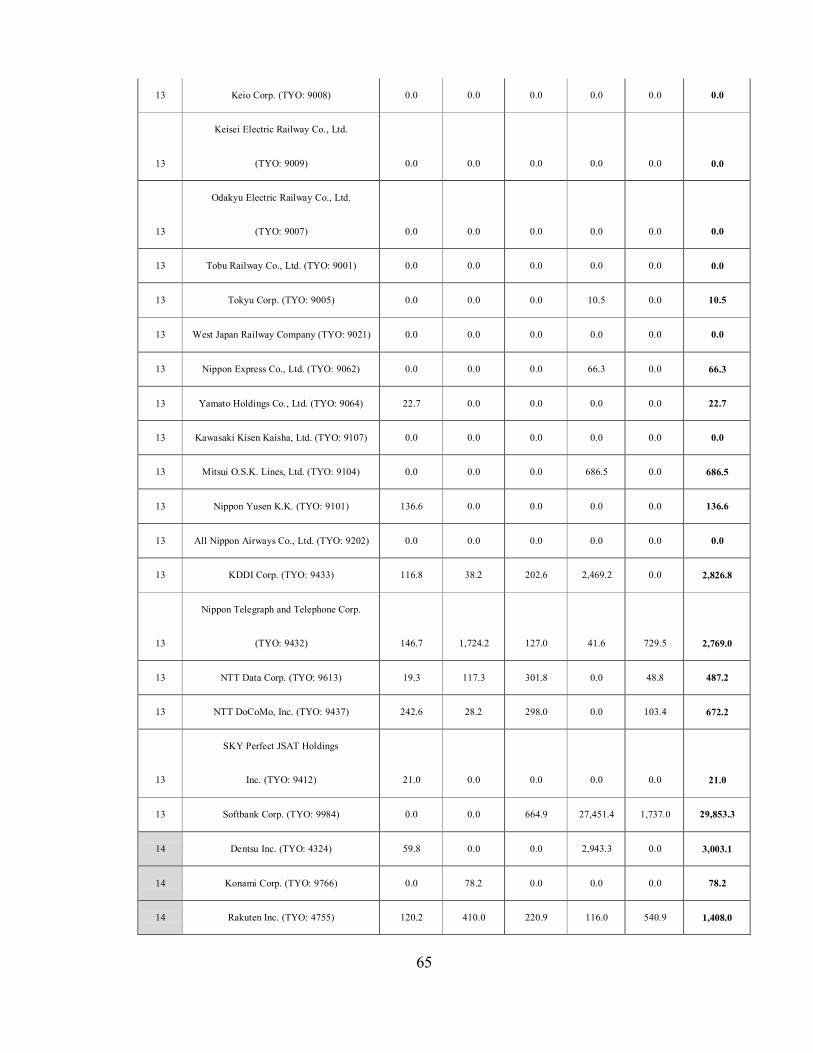

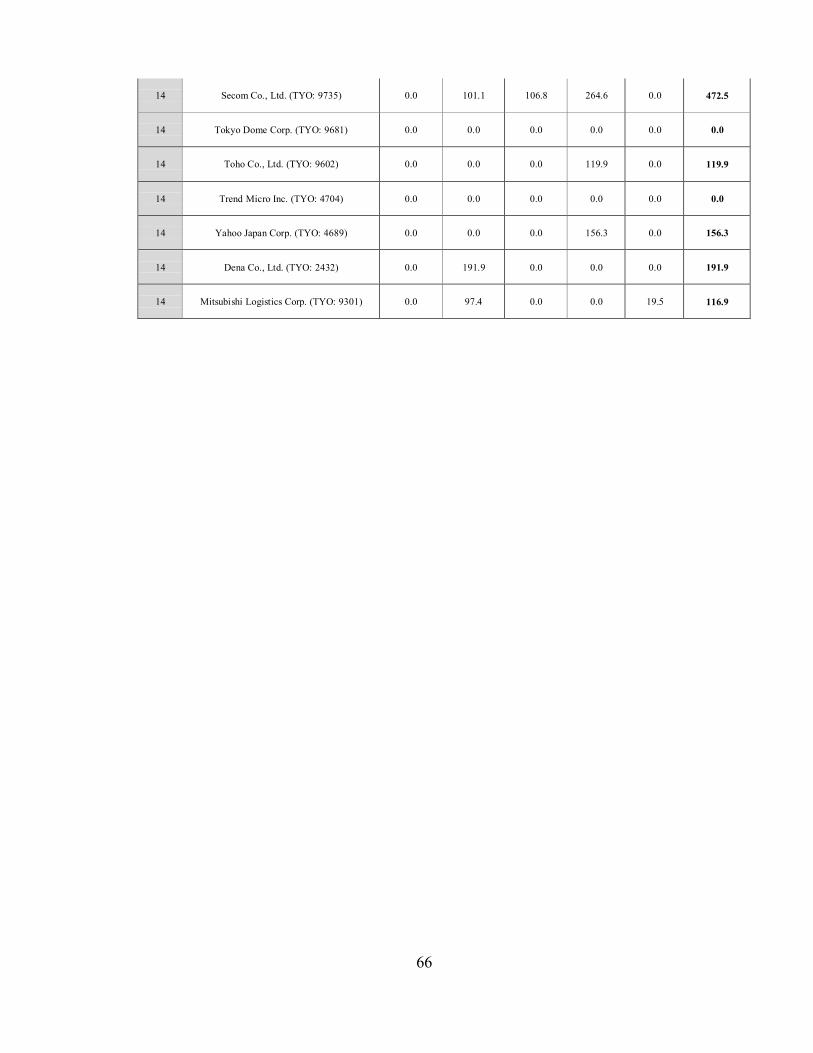

Appendix 4: Analyzed summary of M&A value of 200 Nikkei firms in the period of 2009-2014

<List of Nikkei 200 Updated in December 2017> .......................................................................... 57

REFERENCE ................................................................................................................................... 67

VI

LIST OF TABLES

Table 1 Frequency of M&As conducted by Nikkei comparing to whole Japanese

firms in 2009-2014

17

Table 2 Value of M&As conducted by Nikkei comparing to whole Japanese firms in

2009-2014

17

Table 3 Market Cap of Nikkei comparing to Tokyo Stock Exchange in 2009-2014 19

Table 4 Adjusted List of Industries- Nikkei 200 24

Table 5 The descriptive table of cash holding and M&A in Nikkei 200 in 2009-2013 31

Table 6 The result of Hypothesis (i). – descriptive summary 32

Table 7 The result of Hypothesis (i). – Kruskal-Wallis test result 33

Table 8 The result of Hypothesis (ii). – descriptive summary 34

Table 9 The result of Hypothesis (ii). – Kruskal-Wallis test result 35

Table 10 The result of Hypothesis (iii). – descriptive summary 36

Table 11 The result of Hypothesis (iii). – Kruskal-Wallis test result 37

Table 12 The result of Hypothesis (iv). – descriptive summary 39

Table 13 The result of Hypothesis (iv). – Kruskal-Wallis test result 39

LIST OF FIGURES

Figure 1 Non-financial firms’ real holding of cash assets and real aggregate investment in

Japan

5

Figure 2 The Cash-to-Asset median across non-financial firms within selected countries

in the period 2010- 2012

5

Figure 3 M&A status of Japanese firms in the period of 2009-2014 7

Figure 4 The Value of M&A deal in Nikkei & whole Japanese companies in the period of

2009-2014

18

Figure 5 Methodology process 21

VII

LIST OF ABBREVIATIONS

TSE Tokyo Stock Exchange

M&As Mergers and Acquisitions

UNCTAD United Nations Conference on Trade and Development

Nikkei 200 200 non-financial firms in Nikkei 225 (updated to Dec 2017)

C/A Cash-to-Asset

Kruskal-Wallis H test KW test

1

CHAPTER 1: INTRODUCTION

The first chapter starts by describing the background of Mergers and Acquisitions

(hereafter called M&A). In this part, the research will focus on describing the important roles

of M&A in the business entities generally and Japan, the national economic theme which the

research is conducted. Then, the research will review briefly the factors influencing the M&A,

in which cash holding is highlighted for leading to next part. In that way, the research problem

will be figured out from the clear difference between documented hypothesis and reality based

on database analyzing. Next, the research question and the research objectives will be given.

The last part covers all the structure of the whole thesis by the outline map.

1.1. Background:

Mergers and Acquisitions

According to the United Nations Conference on Trade and Development (UNCTAD),

Mergers and Acquisitions (M&As) term is defined as “situations where there is a legal operation

between two or more enterprises whereby firms legally unify assets formerly subject to separate

control”, (UNCTAD, 2017). According to Investopedia (2018), “M&As is a general term that

refers to the consolidation of companies or assets through various types of financial transactions.

M&A can include a number of different transactions, such as mergers, acquisitions,

consolidations, tender offers, purchase of assets and management acquisitions. In all cases, two

2

companies are involved.”

Important roles of M&As

In term of M&A size, according to Thomson Reuter, the global M&As in 2018 has reached

to $3 trillion for four consecutive years, that remarks the more and more important roles of

M&A in the economies. Updated to 2016, Japan-sourced acquisitions reached the value of JPY

10.4 trillion (equivalent to USD 100 billion), three times higher than domestic transactions’

value rotated within Japan (UNCTAD, 2017).

In the trend of growing economy and globalization, M&As become one of most common

shortcuts of business to get the optimum growth. According to Marks & Mirvis (1998), the core

strategy behind M&As is one plus one makes three. From the “one” of the acquiring firm’s

value and “one” of the targeting firm, the total value generated is three and more. The important

role of M&A in various aspects of business has been studied in the range of theories and

documented evidence.

Following the seminal papers by Jensen and Ruback (1983), Jensen (1986), the M&As market

has influenced whole economies and business. Anju. S (1990) classifies M&As into the two

main types: “value-maximizing theory” and “managerial theory”. Barney (1988) and Prahalad

and Hamel (1990) proved M&A role in the performance promotion of core competencies and

3

resources. In term of empirical evidence, Capron (1990) pointed out the effect of the long-term

acquisition on the asset divestiture and resource redeployment, or Jarell et al. (1988) and

Bradley et al. (1988) researched the M&A as a net-value-increasing deal. In the work of Steven

et al. (2013), the acquiring firms in industries are strongly proved to achieve the comparative

advantages. The efficiency and strategic motives of M&A are also emphasized in this study.

Matsumoto (2017) proves the generation of integration and synergy in the cases of failure and

success “made in Japan” in cross border M&As. A cost-saving benefit is mentioned in the work

of Hayn (1989) about the tax-shield, and of Richard et al. (2007) about the overall cost reduction

leading the buying power boost. Clearly, because of the important documented roles of M&A,

it is necessary to study the influencing factors to M&A decision. In the next section, the author

points out the research problem basing on the relation between M&A and an influencing factor-

cash holding.

1.2. Research problem:

The lesson from theory & empirical evidence

In this research, the term “Cash” refers to Cash and Cash equivalent. According to

International Accounting Standard 7 (IAS 7), Cash “comprises cash on hand and demand

deposits”. And cash equivalents are “short-term, highly liquid investments that are readily

convertible to known amounts of cash and which are subject to an insignificant risk of changes

4

in value”. The definition from Investopedia (2018) is “Cash and cash equivalents (Cash) refer

to the line item on the balance sheet that reports the value of a company’s assets that are cash

or can be converted into cash immediately. These include bank accounts, marketable securities,

commercial paper, Treasury bills and short-term government bonds with a maturity date of three

months or less.” From that way, the definition of “Cash holding” in this research refers the Cash

and Cash equivalents in the balance sheet at the end of fiscal year.

Because of the important effects of M&A, a range of previous papers study the factors which

affect M&As. In this research scope, the factor mentioned is Cash Holding.

Jensen and Meckling (1976) and Jensen (1986) note in their seminal theory of agency cost

between manager and shareholder. In the company which has the large cash holding, the

manager considers the acquisition as the primary method of spending money instead of paying

out to shareholder. Harford (1999) proves that the firm which reserves the large cash holding is

more likely than other firms to conduct acquisition and industry diversification. He also points

out in his empirical evidence that the rise of capital liquidity is the one of the most important

reasons for the increase of M&A activity in the US from the second half of the 1990s (Harford,

2005). In the work of Shleifer and Vishny (1992), cash holding is mentioned as the result of

free cash flow, in which the firm holding the large free cash can increase stock prices, that

makes the financial constraint on the acquiring firm relaxed. Consequently, the evaluated price

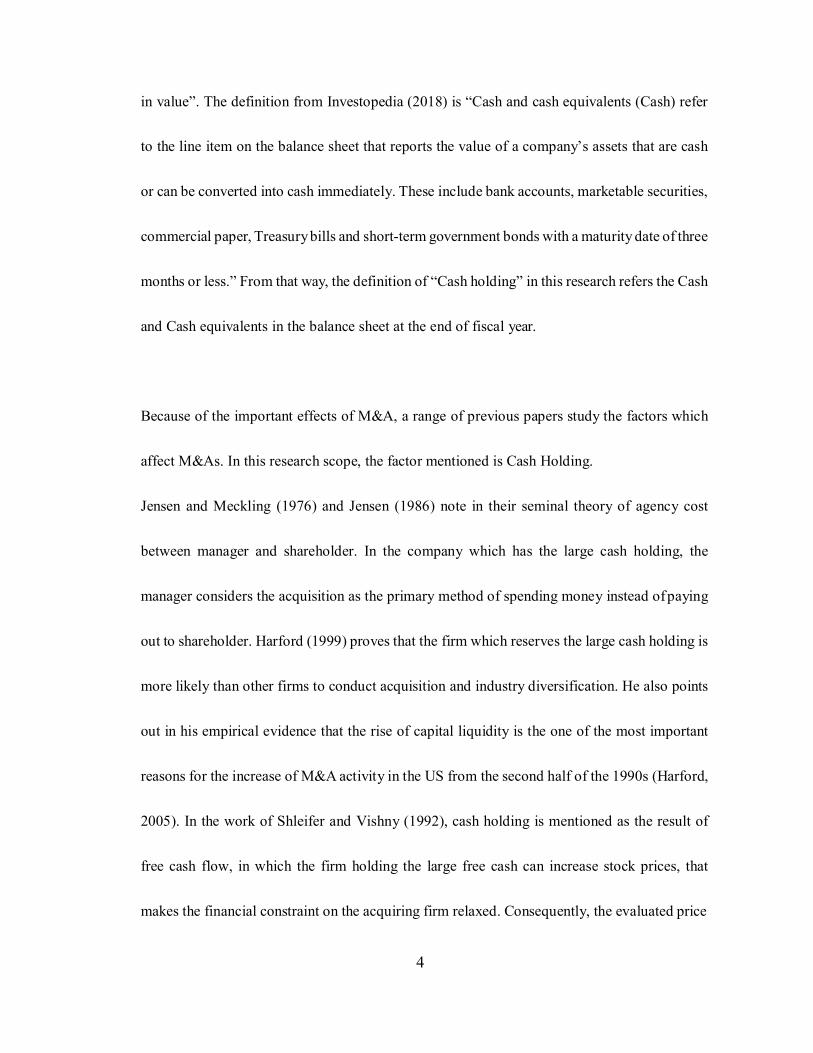

5

Figure 1: Non-financial firms’ real holding of cash assets and real aggregate investment in Japan

Source: National Account, Bank of Japan

6

Japanese non-financial firm reserved has accounted for 50 percent of nominal GDP. However,

contrary to the rapid increase of cash holding, the value of the whole Japanese aggregate

investment has just decreased since 1995 as the main trend. The big gap between these opposite

trends has occurred since the period around 2009. In the work of Naoki (2012) with the scope

of 2,200 listed Japanese stocks, the median firm’s cash-to-asset ratio just dropped to 8% in 1988,

before rising rapidly to above 10% in the period of 2009-2010. Shinada, N. (2012) also points

out the strong increase of cash holding in Japanese firms under the effects of internal and

external economies factors.

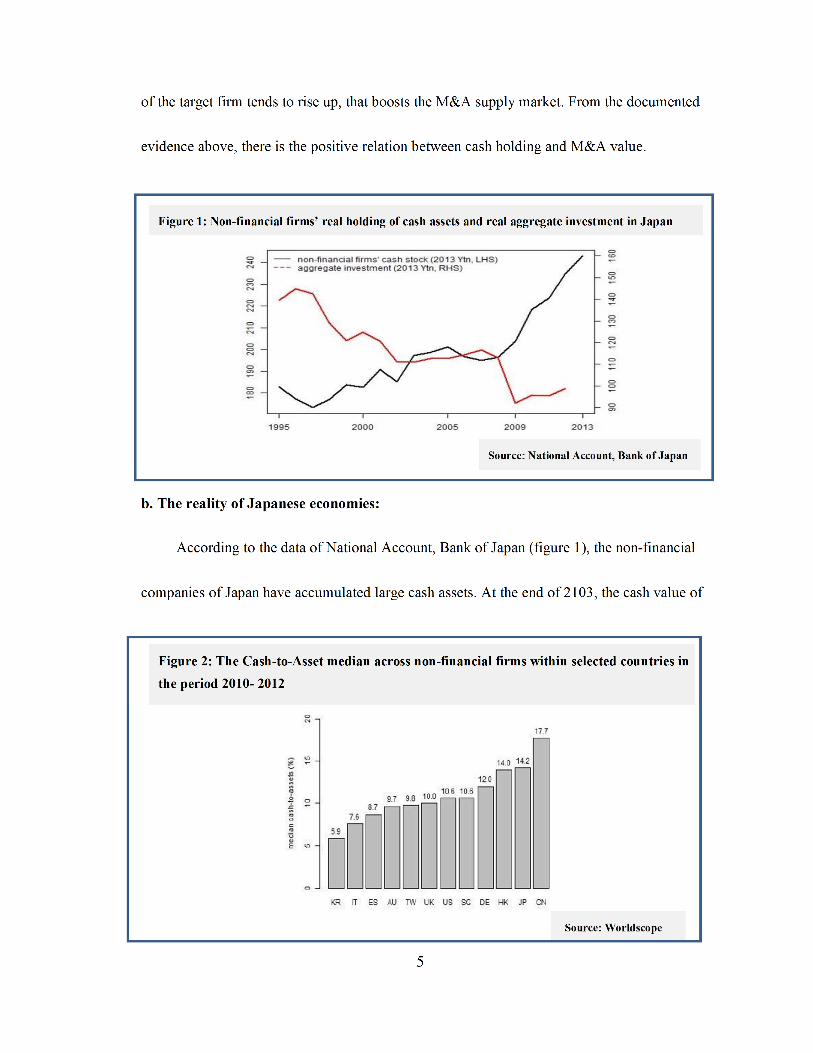

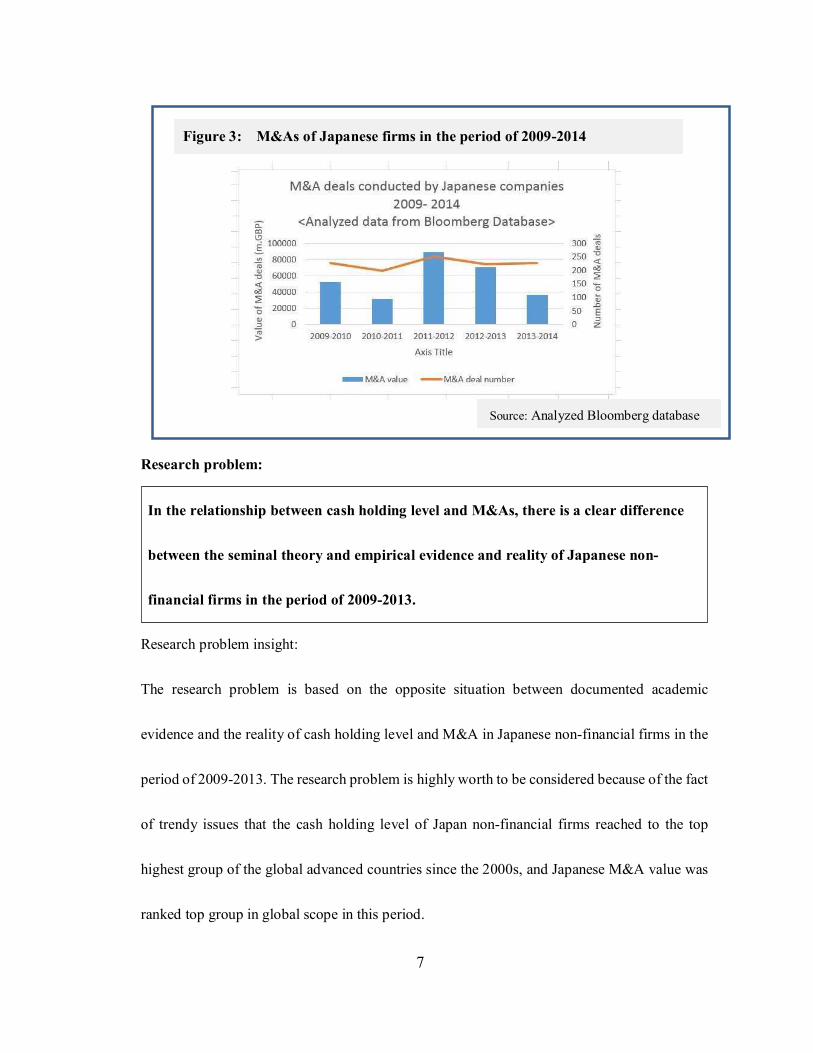

Figure 2 presents the outstandingly high cash holding of Japanese non-financial firms in

comparison with other countries. In the period of 2010-2012, the median of cash holding in

Japan is even four percent higher than in the US. Nevertheless, in this context, according to the

analyzed database from Bloomberg (figure 3), the M&A investment has just fluctuated or even

decreased sharply in the period of 2009-2014.

7

In the relationship between cash holding level and M&As, there is a clear difference

between the seminal theory and empirical evidence and reality of Japanese non-

financial firms in the period of 2009-2013.

Research problem:

Research problem insight:

The research problem is based on the opposite situation between documented academic

evidence and the reality of cash holding level and M&A in Japanese non-financial firms in the

period of 2009-2013. The research problem is highly worth to be considered because of the fact

of trendy issues that the cash holding level of Japan non-financial firms reached to the top

highest group of the global advanced countries since the 2000s, and Japanese M&A value was

ranked top group in global scope in this period.

Figure 3: M&As of Japanese firms in the period of 2009-2014

Source: Analyzed Bloomberg database

8

What is the relation between M&A and level of cash holding in Japanese non-financial

firms in the period of 2009-2013?

There is a big lack of effort or empirical evidence which study directly the relation between

cash holding and M&A investment of Japanese firms. The empirical paper which mentions

directly to agency problem in this relation of Japanese firms is also scarce.

1.3. Research question:

From this key question, the research will extend the detail questions, as follow:

Whether there is difference of the M&A value according to different levels of cash holding in

the period of 2009-2013.

Whether the M&A investment and cash holding in Japanese non-financial firms in the period

of 2009-2013 follow the concept that the higher the level of cash holding is, the more M&A

value is conducted.

1.4. Research objectives:

From the key question above, in the academic perspective, the research focuses on two

objectives:

Test the relation between the cash holding and M&A in the reality of Japanese non-financial

9

firms, then review the previous documented evidence and contribute to academic community.

This objective is considered as the most important objectives in the research.

Analyze and understand the main situation and trend of cash holding and M&A in the scope of

typical Japanese non-financial firm group in the typical period.

Respect to personal perspective, Japan really inspires the author by rich tradition value and

admirable economy achievements. To understand deeply about Japan, especially Japanese

economies, besides overcoming language barrier, studying the Japanese firms is very essential.

The research serves for the author’s personal objectives in long-term vision:

Give the chance for the author to study deeply the status of the Japan economies through the

typical and influencing firm group.

Discover the gaps or problems in Japanese firms through the process of collecting and analyzing

data not only in the theme of cash holding and M&A but also in wider economic scope. In that

way, the author can extend the scope of research in the further research path.

1.5. Research outline:

The research will go through five main chapters. In the Chapter 1, the main idea of

research will be revealed from the perspectives of documented evidence and reality of Japan

economy, the main theme utilized by the research. By figuring out the opposite arguments

10

between the theory and empirical evidence and the reality of Japan in non-financial firm term,

the research leads to research problem and research question, respectively. The research

objective in the angle of academy and individual will be explained.

Chapter 2 comprises two sections for literature reviewing. The first and second section will

present the main theories and empirical evidences respectively to describe the M&As in the

angle of cash holding.

The third chapter describe the data scope and methodology. In the section of data, the reason to

utilize the data scope will be revealed. Then, the variable of data relating to cash holding and

M&As will be also defined and explained clearly. The section of methodology helps the

audience understand how the research analyzes the data, sets up the threshold, and points out

the expected outcomes. In the last section, the set of hypothesizes will be presented, that basing

on the arguments from the research problem and research question.

Chapter 4 discloses the finding basing on analyzed data. The descriptive information and the

result of hypothesis tests will follow strictly and answer the research question. The arguments

from the chapter of literature review will be utilized to discuss this finding in multiple views.

11

In chapter 5, the research will be wrapped up by the integrated conclusion, including summary,

contribution and recommendation, limitation and further research. The summary will integrate

coherently all research content, then the section of contribution and recommendation will

highlight how the research contribute to knowledge. The last section will disclose the limitation

of research and propose the further step of studies.

12

CHAPTER 2: LITERATURE REVIEW

In this chapter, the research goes through review processing of theories and empirical

evidences that present the relation between cash holding and M&As. In the section of theory

review, the concepts of agency problem and demand for cash by firms are respectively described.

Two concept directions will be presented: agency theory suggests the positive relation between

the cash holding and M&As, while the theory of precaution and transaction cost mention the

conservative approach to hold cash for risk and cost reduction rather investment motive. Then

the section of empirical one will summary the academic evidence to support for this relation

between cash holding and M&As.

2.1. Theory review:

The agency theory

There is a range of forces drive the M&A activities, such as synergies, promotion of

economic scales, tax reduction, deregulation. In his seminal theory, Jensen (1986) suggests the

agency theory to argue as a cause of M&A activities. This theory is considered as the one of the

most influencing approach to relation between the cash holding and investment decision,

including M&As. In this theory, the manager plays a role of an agent of shareholder, however,

there are core conflicts between them because of their interest difference. When the firm

accumulates the large cash stock, the shareholders want to receive this cash as a payment.

13

However, this payment reduces the asset scale and scope controlled by managers, thereby

dwindling the power of managers in firm and forcing them to approach capital market when the

company confronts the financial shortfall. Consequently, instead of paying out for the

shareholder, the managers have the motive to expand their firm by investment decisions.

Besides, the expansion of firms also enhances the manager’s power with their controlled

resource, as well as influence their compensation with the positive increase. According to his

theory, the decision of acquisition is considered as a primary practice which the manager apply

to their firm strategy. The clear lesson from this theory is there is the positive correlation

between level of cash holding and M&A activities, in which, when the firm accumulates the

large cash holding, the manager tends to do acquisition instead of paying out to shareholder.

The theory of the demand for cash by firms:

Keynes (1936) argues that the firm holds cash for the motive of precaution and transaction

cost. In the economic context with various uncertainty, management and financial risks, or

sudden investment opportunities, the firm tends to hold more cash. With the large cash holding,

the firm can reduce the internal and external negative effects and keep the stability of financial

health. Besides, in term of transaction cost, the cash holding is beneficiary for a firm by saving

their transaction costs, which comprises: the cost of raising the external cost and the cost of

liquidating assets when needed. Following the factors of uncertainty, such as financial crisis,

14

the government or bank interference, interest rate, …, this theory can explain the demand for

cash by firms on a case-by-case basis.

2.2. Empirical evidence review:

Harford (1999) also explains the relation between the cash holding and M&A in his study

of the U.S firms for the period from 1950 to 1994. Basing the theory of agency theory, his

empirical evidence points out that the proportion of cash-rich firm conduct the diversifying

acquisition is much higher than the proportion of the cash-poor firms. From this evidence, the

M&A activities have been potentially conducted more when the firm increase their cash

reserved to the high level. Harford (2005) also emphasizes the relation between cash holding

and M&A in his study of U.S companies in the second half of the 1990s. The crucial finding

points clearly out the capital liquidity increase affect positively to the rise of M&A activities.

Backing to the research problem of cash paradox, the theory and empirical evidence, which are

based on the agency problem for the positive relation between cash and M&As, should be

relooked in the reality of Japanese economies in the period of 2009-2013. This period was

remarkable with the turbulent economies contexts with double finance crisis with various

uncertainty. The research, in the next chapter, will test how this positive relation between cash

holding and M&As occurs in this period according to theory and empirical evidence mentioned.

15

CHAPTER 3: METHODOLOGY

To answer directly the research question, the methodology chapter presents the main

method the research is conducted. There are two sections: (1). data sample introduction and (2).

methodology to analyze this database.

3.1. Data sample:

Nikkei 225

The research utilizes the non-financial firm lists of Nikkei 225 (hereafter called Nikkei)

updated in the fiscal year 2017 as the main samples. The Nikkei stands for Japan’s Nikkei 225

Stock Average, the leading and most powerful index of Japanese stocks, which comprises 225

blue-chip firms traded on the Tokyo Stock Exchange. The key secondary source comes from

the Bloomberg and the official Tokyo Stock Exchange database. The observation period of five

years starts in 2009, the fiscal year witnessed the global financial crisis with the remarkably

opposite trend between cash holding and investment in whole Japan economy.

The financial indexes studied are divided into two groups: Cash & Cash equivalent and M&A

deals’ data. In the group of Cash & Cash equivalent, the research focuses on Cash & Cash

equivalent and Net Asset to calculate the ratio of Cash & Cash equivalent to Net Asset. Turn to

M&A, there were above 400 M&A deals conducted by these 200 Nikkei blue-chips in the period

of 2009-2013. The data collected are acquiring firms and target firms, whether they did M&A,

16

the value of each M&A and total values in each year, the frequency (the number) of M&A deals

conducted, whether they complete the M&A. The currency of database is Great British Pound

– GBP.

The representative of Nikkei 225

In term of M&As

In the total above 3600 listed firms in the Tokyo Stock Exchange update to 2018, despite

the number of non-financial firms of Nikkei just account for the modest rate at 5.5%, there are

four reasons that Nikkei can representative highly in this research field.

Being the group of 225 largest companies in Tokyo Stock Exchange, their financial indexes

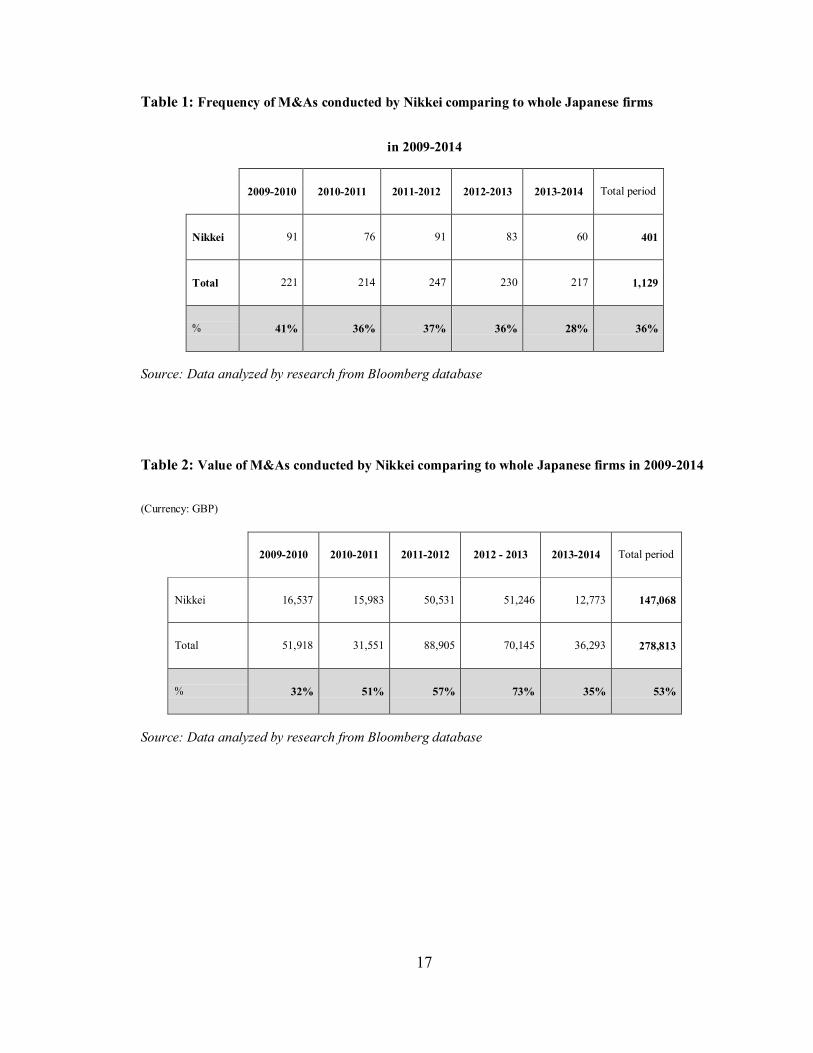

always account for high proportion in whole Japan stocks. The historical M&A database

analyzed in this research proves that Nikkei contributed the large part in value and frequency

in the M&A term. In the observation period, the frequency of M&As conducted was above 400,

that accounted for above 36% of total M&A deals conducted successfully by the whole 2300

listed companies at that time. The value of M&As accounted for above 50% of total value of

whole Japanese listed companies.

(Aggregate investment here means: Joint venture, long-term investment & M&A according to

Bloomberg database)

17

Table 1: Frequency of M&As conducted by Nikkei comparing to whole Japanese firms

in 2009-2014

2009-2010

2010-2011

2011-2012

2012-2013

2013-2014

Total period

Nikkei

91

76

91

83

60

401

Total

221

214

247

230

217

1,129

%

41%

36%

37%

36%

28%

36%

Source: Data analyzed by research from Bloomberg database

Table 2: Value of M&As conducted by Nikkei comparing to whole Japanese firms in 2009-2014

(Currency: GBP)

2009-2010

2010-2011

2011-2012

2012 - 2013

2013-2014

Total period

Nikkei

16,537

15,983

50,531

51,246

12,773

147,068

Total

51,918

31,551

88,905

70,145

36,293

278,813

%

32%

51%

57%

73%

35%

53%

Source: Data analyzed by research from Bloomberg database

18

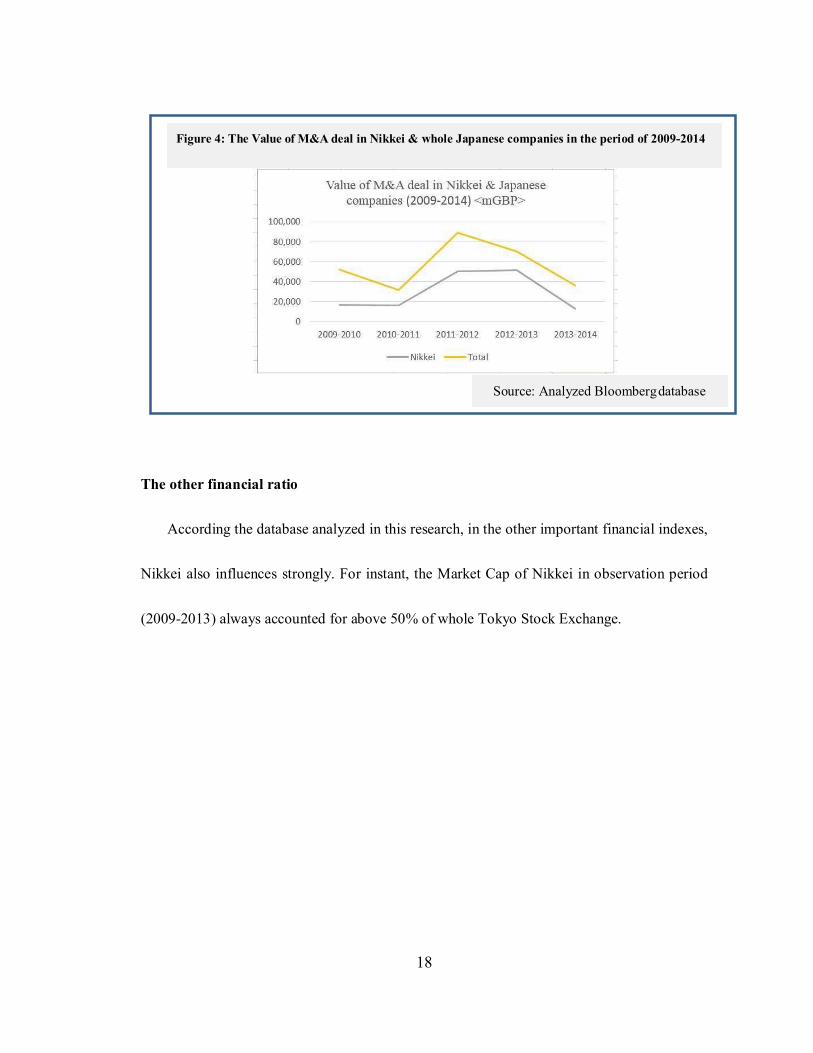

The other financial ratio

According the database analyzed in this research, in the other important financial indexes,

Nikkei also influences strongly. For instant, the Market Cap of Nikkei in observation period

(2009-2013) always accounted for above 50% of whole Tokyo Stock Exchange.

Figure 4: The Value of M&A deal in Nikkei & whole Japanese companies in the period of 2009-2014

Source: Analyzed Bloomberg database

19

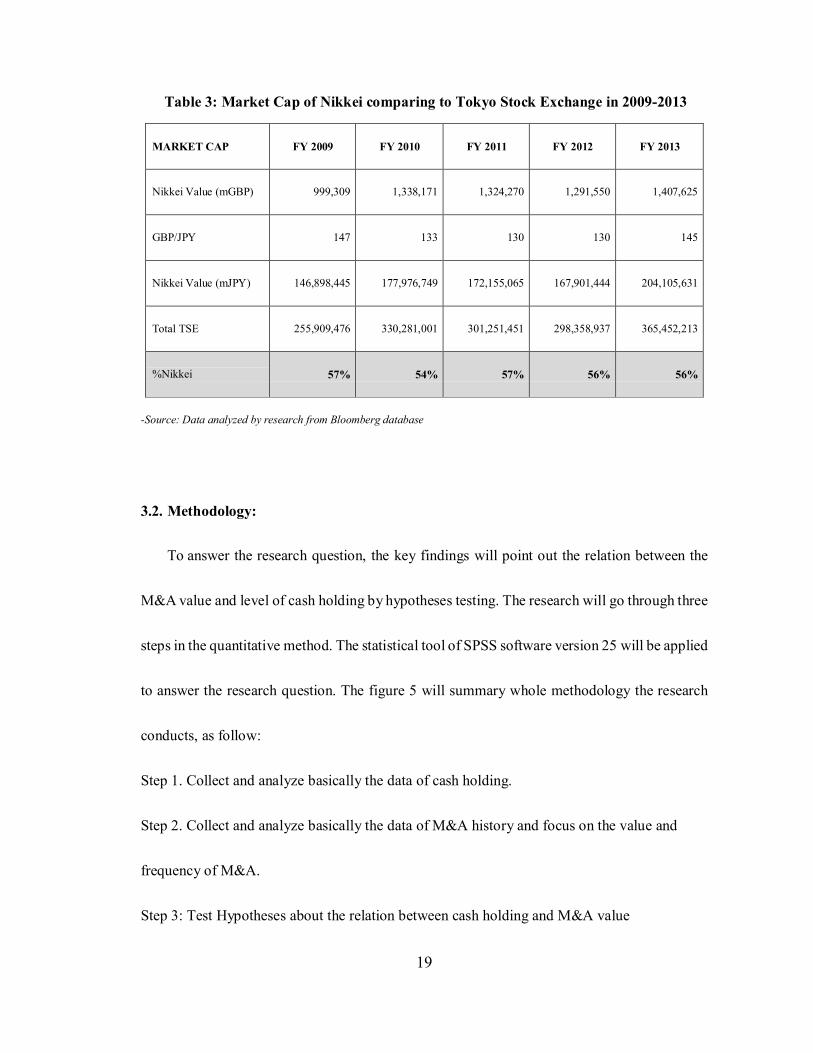

Table 3: Market Cap of Nikkei comparing to Tokyo Stock Exchange in 2009-2013

MARKET CAP

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

Nikkei Value (mGBP)

999,309

1,338,171

1,324,270

1,291,550

1,407,625

GBP/JPY

147

133

130

130

145

Nikkei Value (mJPY)

146,898,445

177,976,749

172,155,065

167,901,444

204,105,631

Total TSE

255,909,476

330,281,001

301,251,451

298,358,937

365,452,213

%Nikkei

57%

54%

57%

56%

56%

-Source: Data analyzed by research from Bloomberg database

3.2. Methodology:

To answer the research question, the key findings will point out the relation between the

M&A value and level of cash holding by hypotheses testing. The research will go through three

steps in the quantitative method. The statistical tool of SPSS software version 25 will be applied

to answer the research question. The figure 5 will summary whole methodology the research

conducts, as follow:

Step 1. Collect and analyze basically the data of cash holding.

Step 2. Collect and analyze basically the data of M&A history and focus on the value and

frequency of M&A.

Step 3: Test Hypotheses about the relation between cash holding and M&A value

20

Step 1: Collect & Analyze Cash holding:

In term of cash holding

The result of this step is the first research finding by presenting the statistical description

of cash holding in the scope of whole 200 companies and in every industry in the period of

2009-2013, and the database to conduct the relation between cash holding & M&A in the third

step.

Level of Cash holding is the main variable when tracking and testing the effect of cash holding

in the next steps. For this variable, the research bases on the ratio of Cash-to-Asset (Cash &

Cash equivalent deflated by Net Asset), hereafter marked C/A ratio. The reason to employ the

C/A ratio because it is the common ratio which is used in many reports when studying about

the level of cash holding, such as National Report, Bank of Japan. This ratio is also mentioned

in the research of Naoki (2012), Harford (1999), Harford (2005), that point out the outstanding

changes and effects of cash holding. The data source of Cash and Net Asset value is the

standardized Balance Sheet of 200 Nikkei non-financial firm annual reports from Bloomberg

database.

21

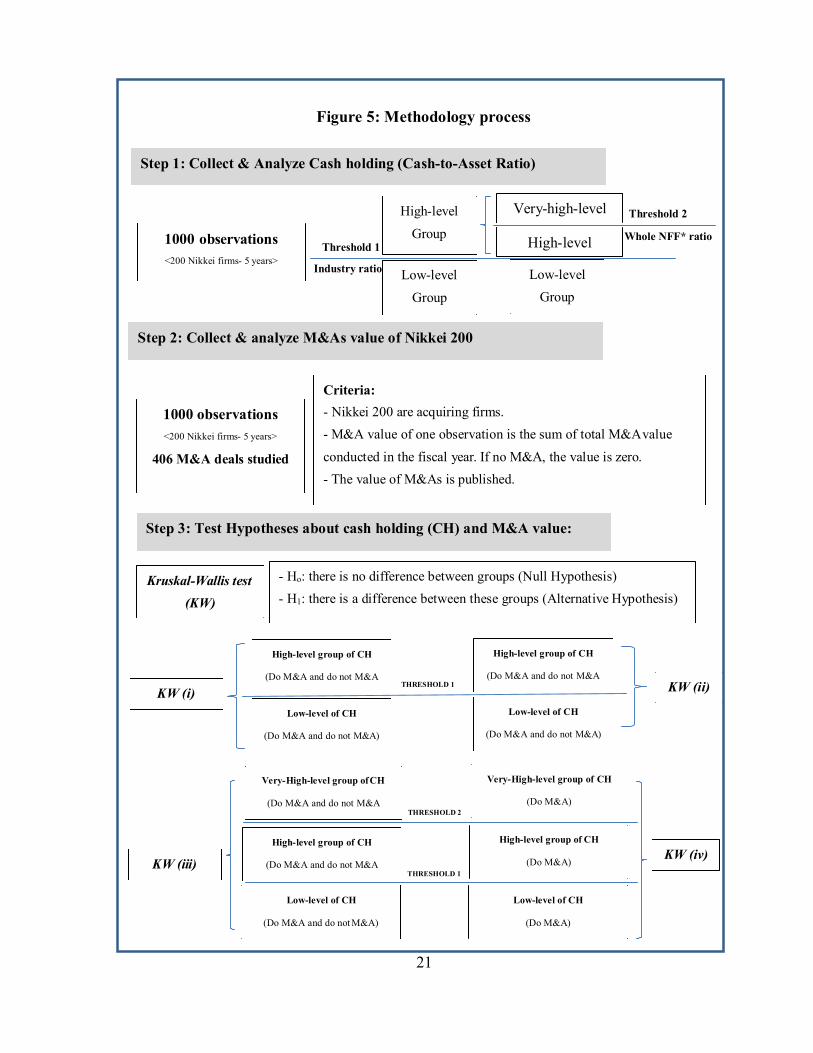

Figure 5: Methodology process

Step 1: Collect & Analyze Cash holding (Cash-to-Asset Ratio)

1000 observations

<200 Nikkei firms- 5 years>

High-level

Group Threshold 1

Industry ratio Low-level

Group

Very-high-level

High-level

Low-level

Group

Threshold 2

Whole NFF* ratio

Step 2: Collect & analyze M&As value of Nikkei 200

1000 observations

<200 Nikkei firms- 5 years>

406 M&A deals studied

Criteria:

- Nikkei 200 are acquiring firms.

- M&A value of one observation is the sum of total M&A value

conducted in the fiscal year. If no M&A, the value is zero.

- The value of M&As is published.

Step 3: Test Hypotheses about cash holding (CH) and M&A value:

Kruskal-Wallis test

(KW)

- Ho: there is no difference between groups (Null Hypothesis)

- H1: there is a difference between these groups (Alternative Hypothesis)

KW (i)

High-level group of CH

(Do M&A and do not M&A

Low-level of CH

(Do M&A and do not M&A)

THRESHOLD 1

High-level group of CH

(Do M&A and do not M&A

Low-level of CH

(Do M&A and do not M&A)

KW (ii)

Very-High-level group of CH

(Do M&A and do not M&A

THRESHOLD 2

Very-High-level group of CH

(Do M&A)

KW (iii)

High-level group of CH

(Do M&A and do not M&A

THRESHOLD 1

High-level group of CH

(Do M&A)

KW (iv)

Low-level of CH

(Do M&A and do not M&A)

Low-level of CH

(Do M&A)

22

Definition of cash holding level

In the research, there are two main levels of cash holding: High-level and Low-level

groups, which are classified by the median C/A ratio of each industry as the main thresholds.

In 1000 observations from 200 Nikkei companies in 5 years, if the ratio of C/A of a Nikkei

company in any fiscal year is higher than the C/A, this observation will be ranked in high level,

and vice versa. Following the work of Berger and Ofek (1995), Harford (1999), Harford (2005),

Naoki.S. (2012), the research utilizes this median ratio of industry in every fiscal years in order

to rank the cash holding level and control the industry effect updated in every years of the period

2009-2013.

In the observations classified in High-level group, the research divides into two sub-groups:

High-level and Very-High-level group of cash holding. The threshold used is the C/A median

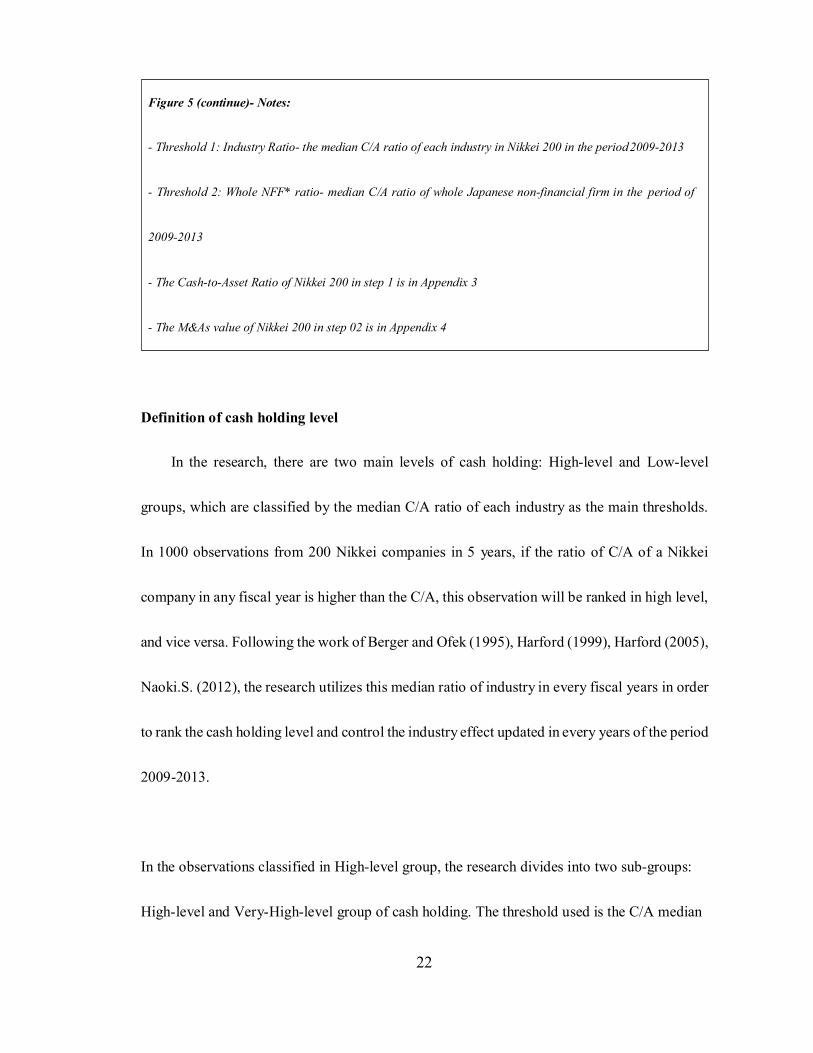

Figure 5 (continue)- Notes:

- Threshold 1: Industry Ratio- the median C/A ratio of each industry in Nikkei 200 in the period 2009-2013

- Threshold 2: Whole NFF* ratio- median C/A ratio of whole Japanese non-financial firm in the period of

2009-2013

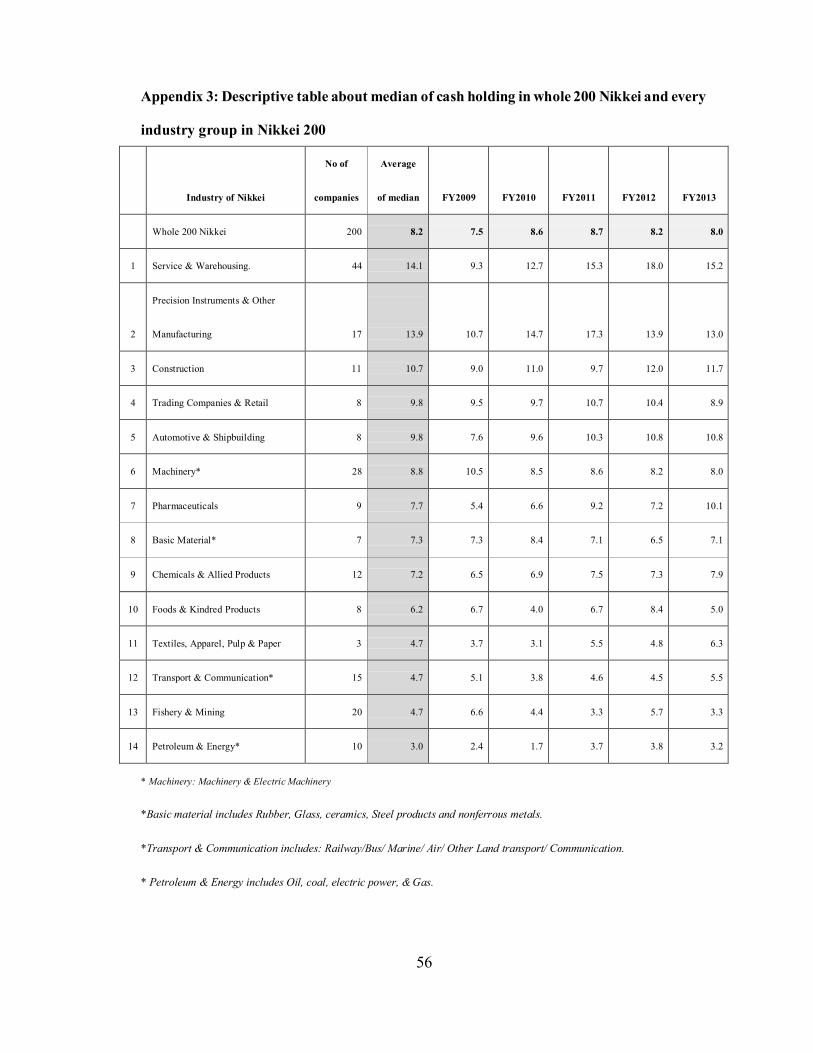

- The Cash-to-Asset Ratio of Nikkei 200 in step 1 is in Appendix 3

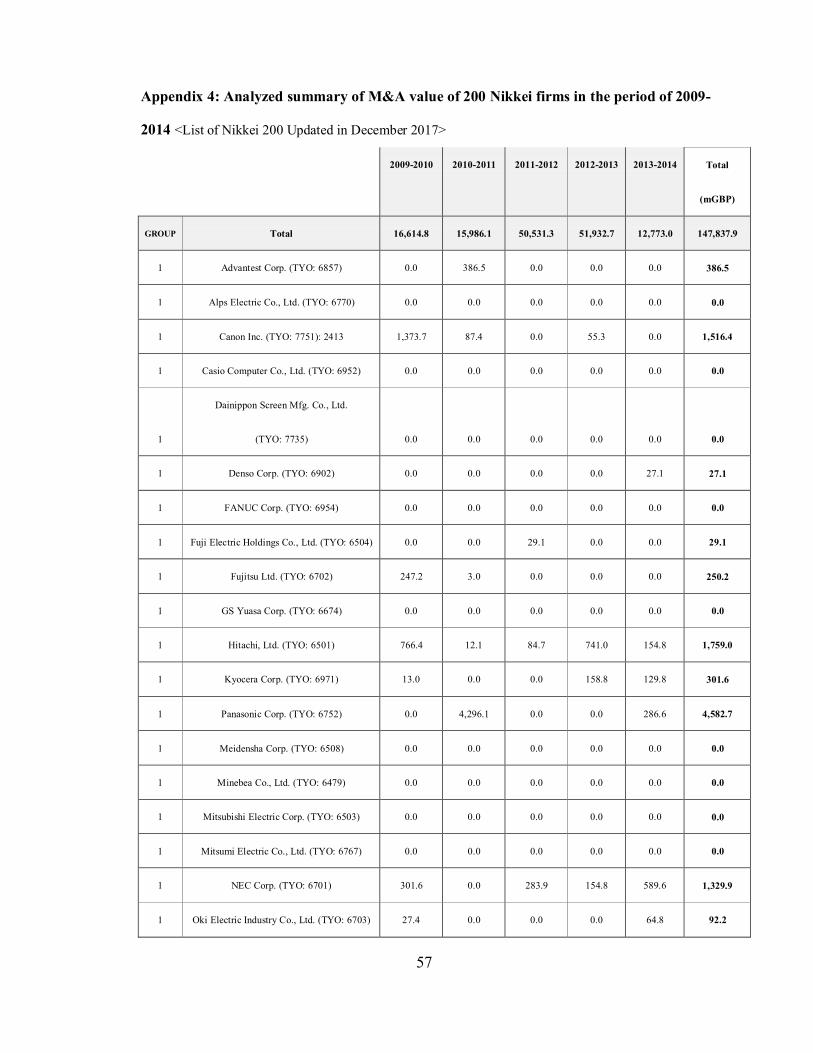

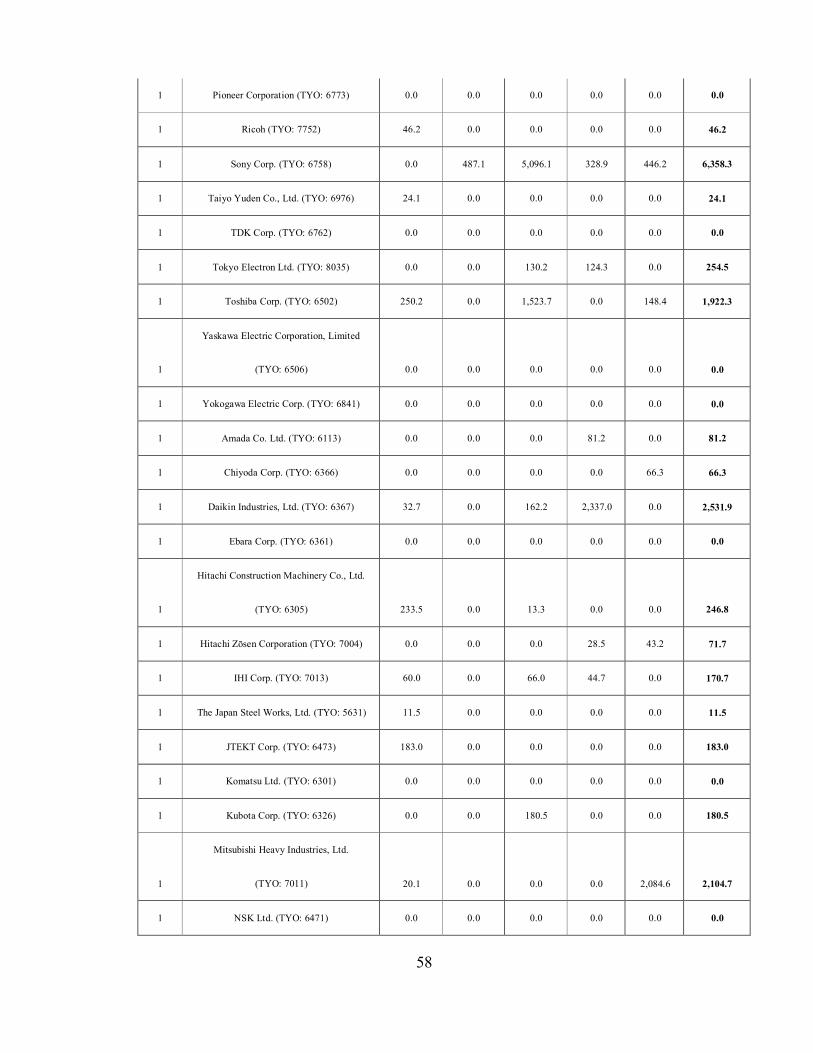

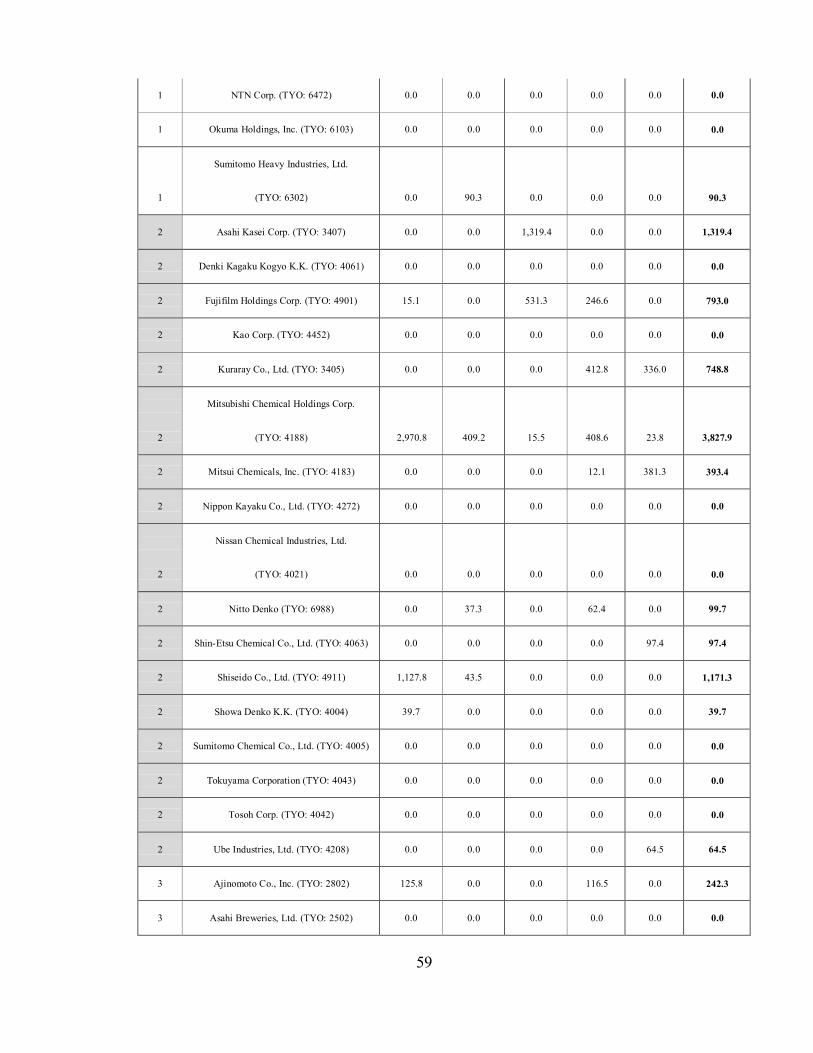

- The M&As value of Nikkei 200 in step 02 is in Appendix 4

23

of whole Japanese non-financial firms in the period of 2009-2013. This median ratio is collected

from the database of Nation Account, Bank of Japan, and readjusted suitably to the period of

2009-2013. Comparing to global advanced countries in the period of 2010-2012, the C/A

median ratio of Japanese non-financial firms has been ranked in the top highest at the rate of

about 14%. Therefore, the research utilizes this ratio as the second threshold to classify the

observations with Very-high-level of cash holding. The classification of cash holding level is

summarized in the figure 5 in the research.

The research divides 200 Nikkei companies into 14 industries. The reason for this classification

is tracking and analyzing the industry groups with the similar features of cash holding and M&A

and reducing the typical industry differences in cash holding. The original classification of

industry comes from the Tokyo Stock Exchange. This classification refers to the approaching

way of Harford (1988), Harford (2005) and Hieu V. Phan (2014), which mention to relation

between the industry groups and M&A. Table 4 presents the industry group names, as follow:

24

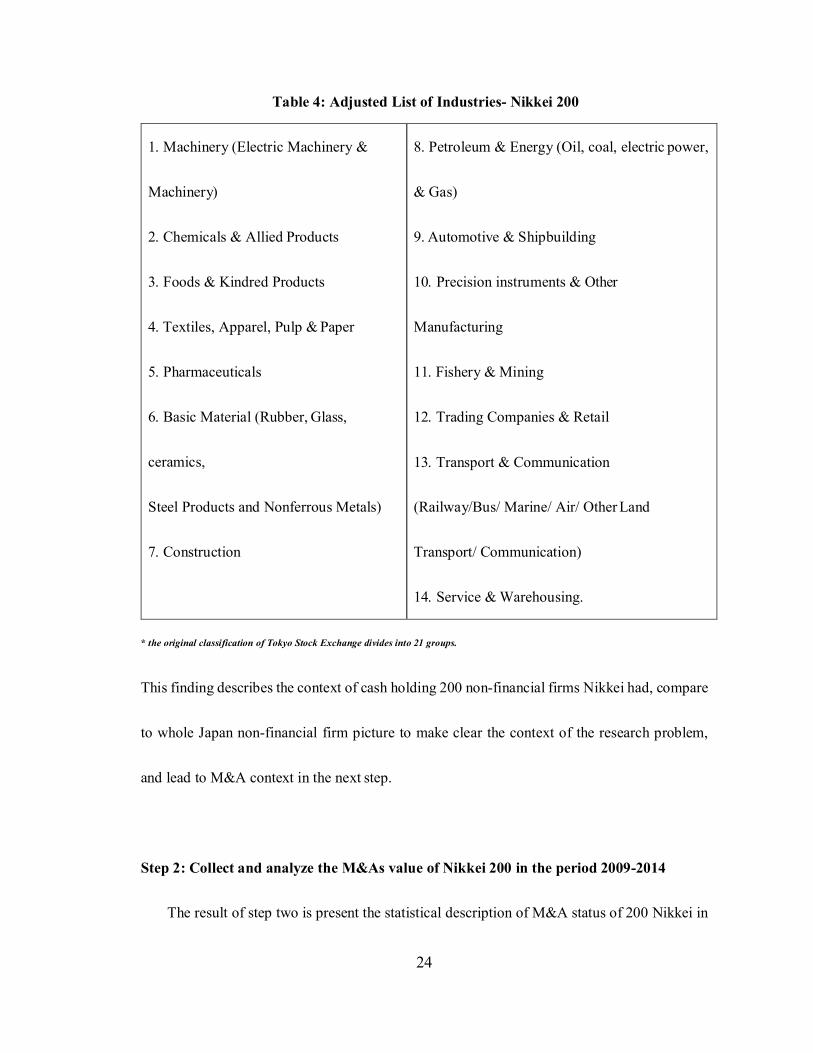

Table 4: Adjusted List of Industries- Nikkei 200

1. Machinery (Electric Machinery &

Machinery)

2. Chemicals & Allied Products

3. Foods & Kindred Products

4. Textiles, Apparel, Pulp & Paper

5. Pharmaceuticals

6. Basic Material (Rubber, Glass,

ceramics,

Steel Products and Nonferrous Metals)

7. Construction

8. Petroleum & Energy (Oil, coal, electric power,

& Gas)

9. Automotive & Shipbuilding

10. Precision instruments & Other

Manufacturing

11. Fishery & Mining

12. Trading Companies & Retail

13. Transport & Communication

(Railway/Bus/ Marine/ Air/ Other Land

Transport/ Communication)

14. Service & Warehousing.

* the original classification of Tokyo Stock Exchange divides into 21 groups.

This finding describes the context of cash holding 200 non-financial firms Nikkei had, compare

to whole Japan non-financial firm picture to make clear the context of the research problem,

and lead to M&A context in the next step.

Step 2: Collect and analyze the M&As value of Nikkei 200 in the period 2009-2014

The result of step two is present the statistical description of M&A status of 200 Nikkei in

25

the period of 2009-2014, that makes the database for the hypotheses of the relation between

cash holding and M&As in the third step. The observation will be studied for a company

between the cash holding value in ending of fiscal year X and the M&As value in the whole

next fiscal year. For instance, the observation of company A will be studied with the cash

holding value in the ending of the fiscal year 2013 (31st of March) and the M&A value in the

whole next fiscal year 2013-2014. (1st April 2013 - 31st March 2014).

The research collects all M&As conducted by Nikkei 200 companies in the period of 2009-

2014 at the number of 406 deals. All the Bloomberg database relating to M&A deal will be

collected, include acquiring firms and target firms, whether they did M&A, the value of each

M&A and total M&As value in each fiscal year, the frequency (the number) of M&A deals

conducted, whether M&A is completed with official value.

An M&A transaction is accounted as the completed deal in the period of 2009-2014 when the

following conditions occur in M&A history: acquiring firm and target firm are determined, the

acquiring firm is in the Nikkei 200 list, the price of M&A deals is announced clearly in currency

scale, and the date of M&A transaction is published in the period of 2009-2014. In term of

acquiring firms and target firms, the criteria to collect data is that the acquiring firms belong to

Nikkei 200, and the target firms is all firms acquired by that acquiring one, including the

26

domestic and global scope. The outcome of this step will be statistical description about M&As

value of 200 Nikkei companies in period of 2009-2014.

Step 3: Test Hypothesis about relation cash holding and M&A value:

The outcome of this step is to describe the relation between the level of cash holding and

M&A in Nikkei 200 non-financial firms.

The research utilizes the Kruskal-Wallis H test (hereafter called KW), a rank-based

nonparametric tool. The first reason to utilize this test because it exams the hypothesis whether

there is a statistically significant difference between two or more groups of an independent

variable. Secondly, this test can satisfy the characteristics of data. The independent variable,

which presents the value of M&As in the huge range, does not follow the normal distribution.

The Kruskal-Wallis test is a version of the independent measures (One-way) ANOVA that can

be performed on ordinal (ranked) data. The main purpose of this test is to answer the

hypothesis that is there a significant difference between two or more groups of independent

variables. The common alpha level is 0.05.

Before utilizing the KWs, data will be converted into ranked data. This test works with the

data which do not follow the normal distribution, and includes two couple of Hypothesis, as

follow:

27

- Ho: there is no difference between the tested groups (Null Hypothesis)

- H1: there is A difference between the tested groups (Alternative Hypothesis)

The Degrees of Freedom (df) is calculated by the formula: df= k-1, in which k is the number

of tested groups. For example, when testing the significant difference between two groups, k

is 2, and df is 2-1=1.

Based on the work of Kazuo et al. (2014) about the decrease of agency problem concept, and

the reality of cash paradox in the period of 2009-2013, it is predicted that there is no difference

of M&A value between the different levels of cash holding. The research will test four

hypotheses, as follow:

(i). In the whole 200 Nikkei firms with 1000 observations (including the do-M&A cases and

not-M&A cases), whether there is the difference of M&A value between two main groups:

High-level group and Low-level group of cash holding, specifically as:

- Ho: there is no difference between these two groups (Null Hypothesis)

- H1: there is a difference between these two groups (Alternative Hypothesis)

(ii). Because in 1000 observations, the huge percent at 760 observations are reported with the

M&A value of zero, that there was not M&A deal conducted. Therefore, in this hypothesis (ii),

the research just tests the observations which have M&A deals conducted to clarify 240

28

observations of “do M&A”. In the whole M&A deals conducted by Nikkei 200 in the period of

2009-2013, whether there is the difference of M&A value between High-level group and Low-

level group of Cash holding, specifically as:

- Ho: there is no difference between these two groups (Null Hypothesis)

- H1: there is a difference between these two groups (Alternative Hypothesis)

(iii). In the Nikkei 200 firms, among three groups of Cash holding level (Low, High, Very High)

in the period of 2009-2013, whether there is the difference of M&A value between these three

groups, specifically as:

- Ho: there is no difference between these three groups (Null Hypothesis)

- H1: there is a difference between these three groups (Alternative Hypothesis)

(iv). Because in 1000 observations, the huge percent at 760 observations are reported with the

M&A value of zero, that there was not M&A deal conducted. Therefore, in this hypothesis (iv),

the research just tests the observations which have M&A deals conducted to clarify 240

observations of “do M&A”. In the whole M&A deals conducted by Nikkei 200 in the period of

2009-2013, among three groups of Cash holding level (Low, High, Very High) in the period of

2009-2013, whether there is the difference of M&A value between these three groups,

specifically as:

29

- Ho: there is no difference between these three groups (Null Hypothesis)

- H1: there is a difference between these three groups (Alternative Hypothesis)

30

CHAPTER 4: FINDING & DISCUSSION

4.1. Finding:

4.1.1. Description of Cash holding & M&A:

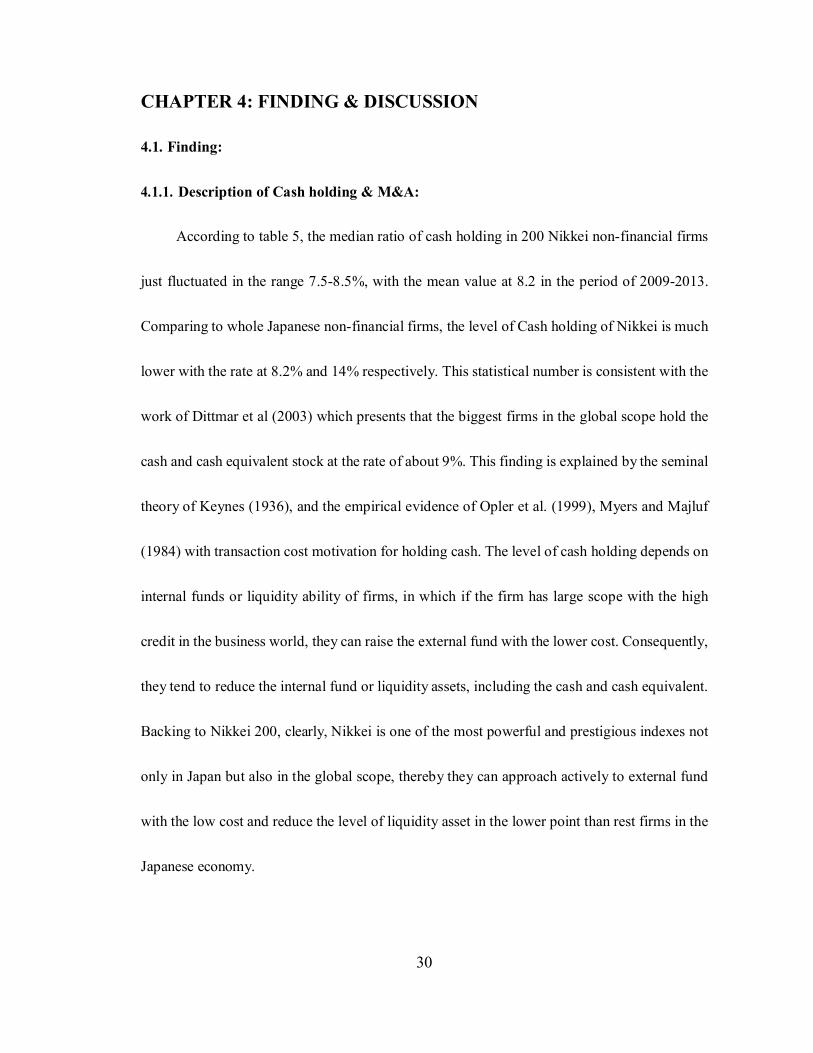

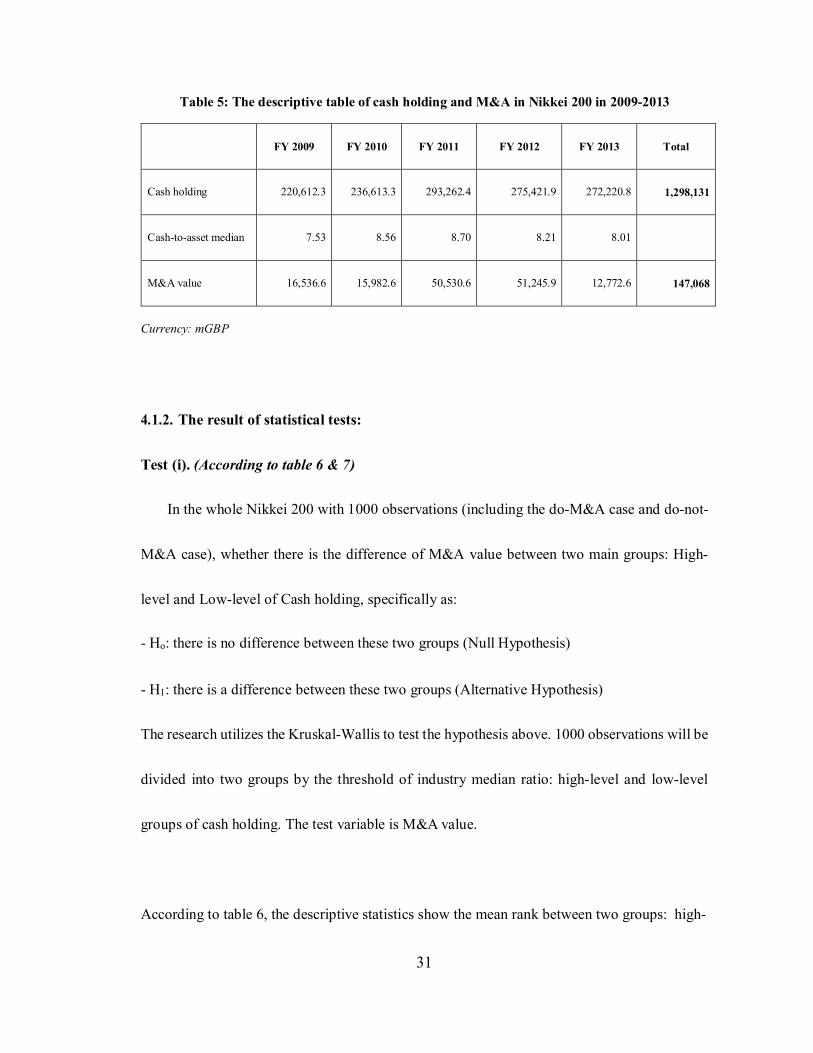

According to table 5, the median ratio of cash holding in 200 Nikkei non-financial firms

just fluctuated in the range 7.5-8.5%, with the mean value at 8.2 in the period of 2009-2013.

Comparing to whole Japanese non-financial firms, the level of Cash holding of Nikkei is much

lower with the rate at 8.2% and 14% respectively. This statistical number is consistent with the

work of Dittmar et al (2003) which presents that the biggest firms in the global scope hold the

cash and cash equivalent stock at the rate of about 9%. This finding is explained by the seminal

theory of Keynes (1936), and the empirical evidence of Opler et al. (1999), Myers and Majluf

(1984) with transaction cost motivation for holding cash. The level of cash holding depends on

internal funds or liquidity ability of firms, in which if the firm has large scope with the high

credit in the business world, they can raise the external fund with the lower cost. Consequently,

they tend to reduce the internal fund or liquidity assets, including the cash and cash equivalent.

Backing to Nikkei 200, clearly, Nikkei is one of the most powerful and prestigious indexes not

only in Japan but also in the global scope, thereby they can approach actively to external fund

with the low cost and reduce the level of liquidity asset in the lower point than rest firms in the

Japanese economy.

31

Table 5: The descriptive table of cash holding and M&A in Nikkei 200 in 2009-2013

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

Total

Cash holding

220,612.3

236,613.3

293,262.4

275,421.9

272,220.8

1,298,131

Cash-to-asset median

7.53

8.56

8.70

8.21

8.01

M&A value

16,536.6

15,982.6

50,530.6

51,245.9

12,772.6

147,068

Currency: mGBP

4.1.2. The result of statistical tests:

Test (i). (According to table 6 & 7)

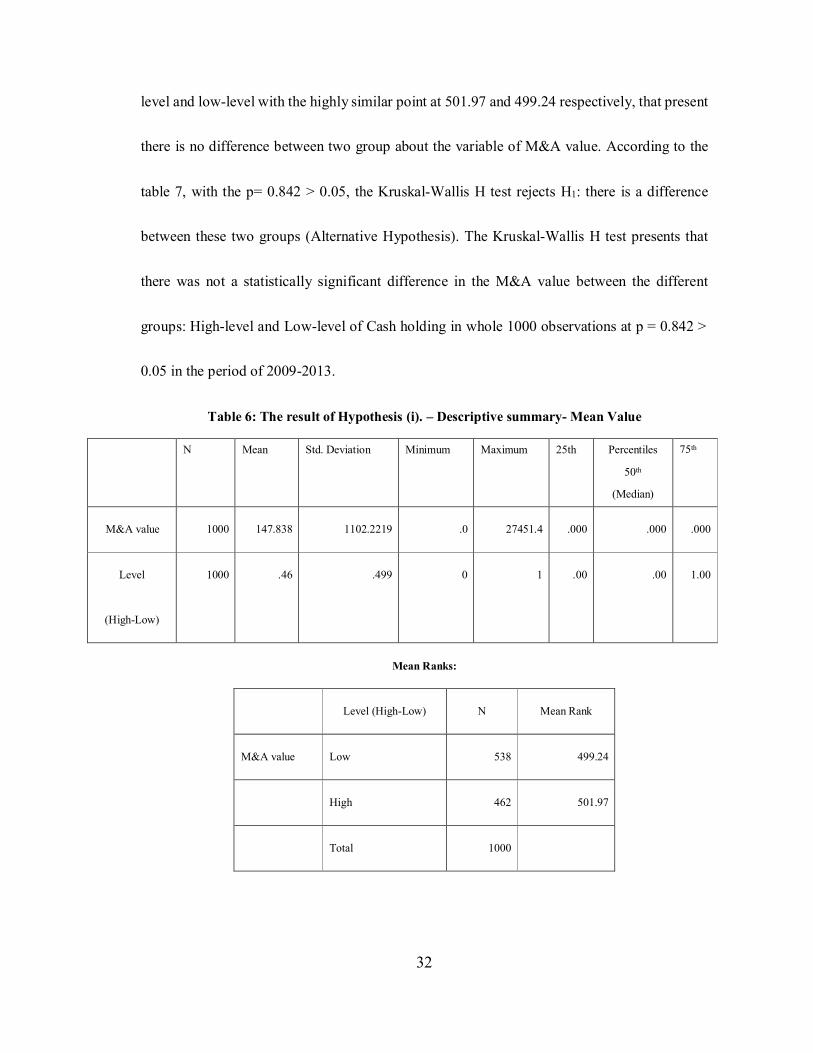

In the whole Nikkei 200 with 1000 observations (including the do-M&A case and do-not-

M&A case), whether there is the difference of M&A value between two main groups: High-

level and Low-level of Cash holding, specifically as:

- Ho: there is no difference between these two groups (Null Hypothesis)

- H1: there is a difference between these two groups (Alternative Hypothesis)

The research utilizes the Kruskal-Wallis to test the hypothesis above. 1000 observations will be

divided into two groups by the threshold of industry median ratio: high-level and low-level

groups of cash holding. The test variable is M&A value.

According to table 6, the descriptive statistics show the mean rank between two groups: high-

32

level and low-level with the highly similar point at 501.97 and 499.24 respectively, that present

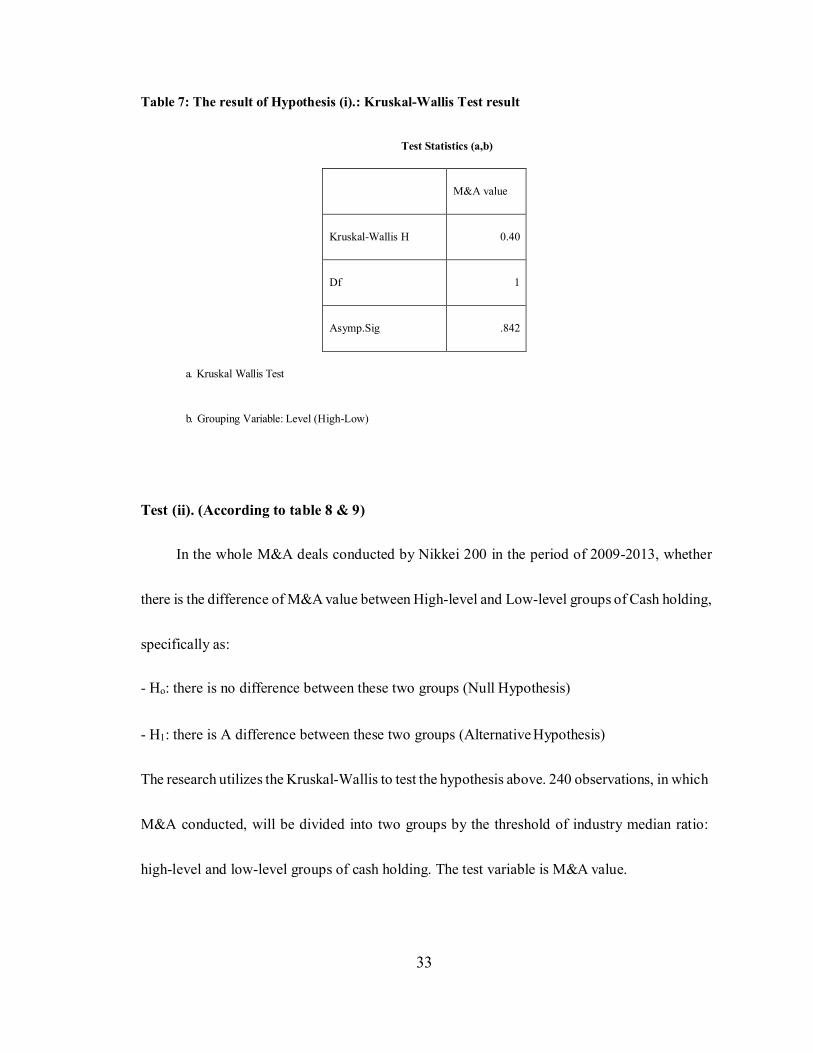

there is no difference between two group about the variable of M&A value. According to the

table 7, with the p= 0.842 > 0.05, the Kruskal-Wallis H test rejects H1: there is a difference

between these two groups (Alternative Hypothesis). The Kruskal-Wallis H test presents that

there was not a statistically significant difference in the M&A value between the different

groups: High-level and Low-level of Cash holding in whole 1000 observations at p = 0.842 >

0.05 in the period of 2009-2013.

Table 6: The result of Hypothesis (i). – Descriptive summary- Mean Value

N Mean Std. Deviation Minimum Maximum 25th Percentiles

50th

(Median)

75th

M&A value

1000

147.838

1102.2219

.0

27451.4

.000

.000

.000

Level

(High-Low)

1000

.46

.499

0

1

.00

.00

1.00

Mean Ranks:

Level (High-Low)

N

Mean Rank

M&A value

Low

538

499.24

High

462

501.97

Total

1000

33

Table 7: The result of Hypothesis (i).: Kruskal-Wallis Test result

Test Statistics (a,b)

M&A value

Kruskal-Wallis H

0.40

Df

1

Asymp.Sig

.842

a. Kruskal Wallis Test

b. Grouping Variable: Level (High-Low)

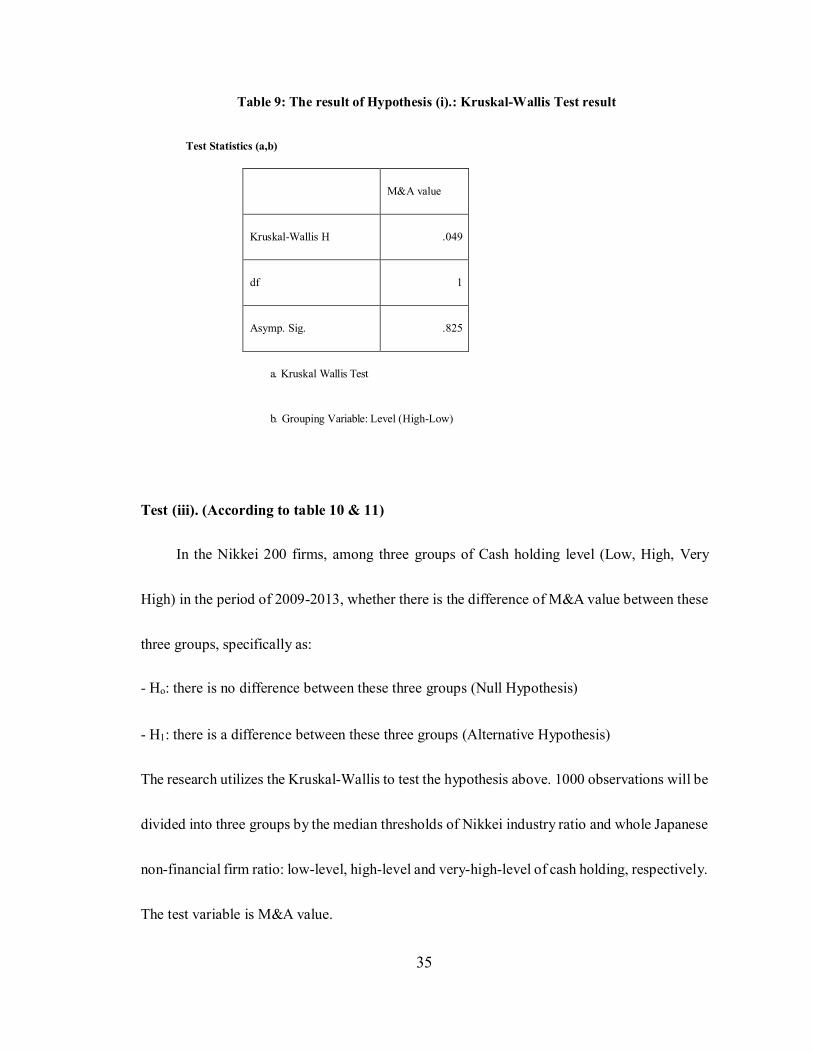

Test (ii). (According to table 8 & 9)

In the whole M&A deals conducted by Nikkei 200 in the period of 2009-2013, whether

there is the difference of M&A value between High-level and Low-level groups of Cash holding,

specifically as:

- Ho: there is no difference between these two groups (Null Hypothesis)

- H1: there is A difference between these two groups (Alternative Hypothesis)

The research utilizes the Kruskal-Wallis to test the hypothesis above. 240 observations, in which

M&A conducted, will be divided into two groups by the threshold of industry median ratio:

high-level and low-level groups of cash holding. The test variable is M&A value.

34

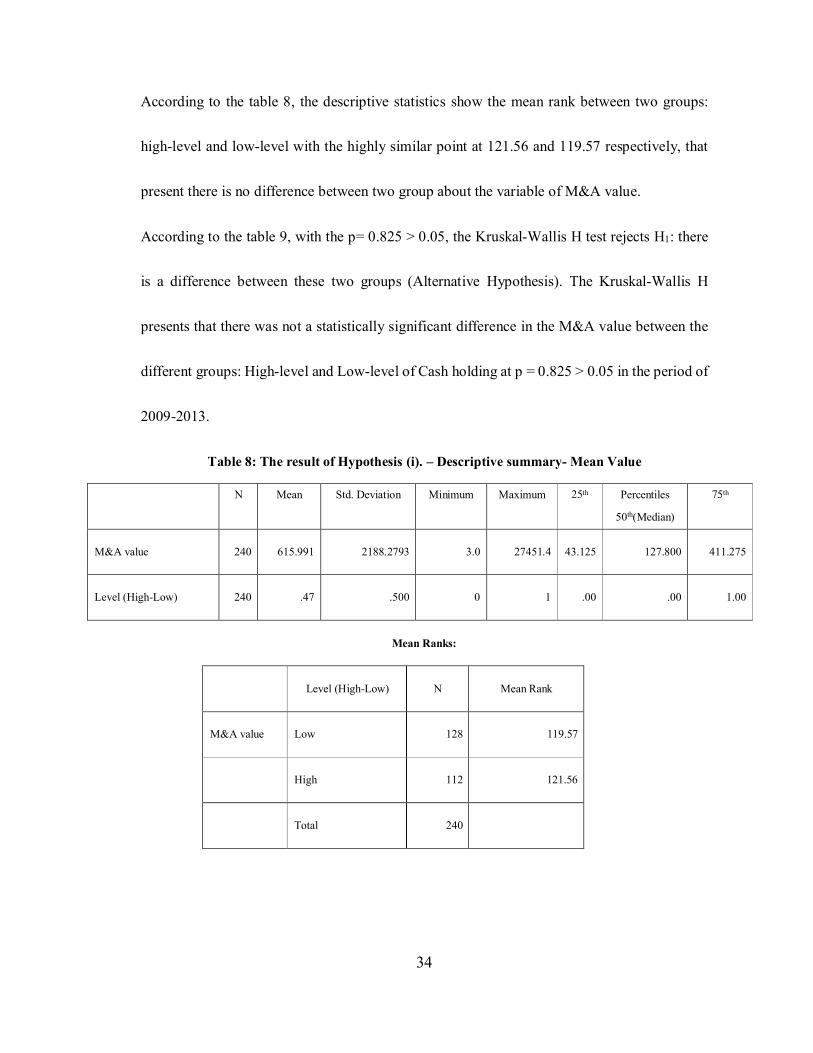

According to the table 8, the descriptive statistics show the mean rank between two groups:

high-level and low-level with the highly similar point at 121.56 and 119.57 respectively, that

present there is no difference between two group about the variable of M&A value.

According to the table 9, with the p= 0.825 > 0.05, the Kruskal-Wallis H test rejects H1: there

is a difference between these two groups (Alternative Hypothesis). The Kruskal-Wallis H

presents that there was not a statistically significant difference in the M&A value between the

different groups: High-level and Low-level of Cash holding at p = 0.825 > 0.05 in the period of

2009-2013.

Table 8: The result of Hypothesis (i). – Descriptive summary- Mean Value

N Mean Std. Deviation Minimum Maximum 25th Percentiles

50th(Median)

75th

M&A value

240

615.991

2188.2793

3.0

27451.4

43.125

127.800

411.275

Level (High-Low)

240

.47

.500

0

1

.00

.00

1.00

Mean Ranks:

Level (High-Low)

N

Mean Rank

M&A value

Low

128

119.57

High

112

121.56

Total

240

35

Table 9: The result of Hypothesis (i).: Kruskal-Wallis Test result

Test Statistics (a,b)

M&A value

Kruskal-Wallis H

.049

df

1

Asymp. Sig.

.825

a. Kruskal Wallis Test

b. Grouping Variable: Level (High-Low)

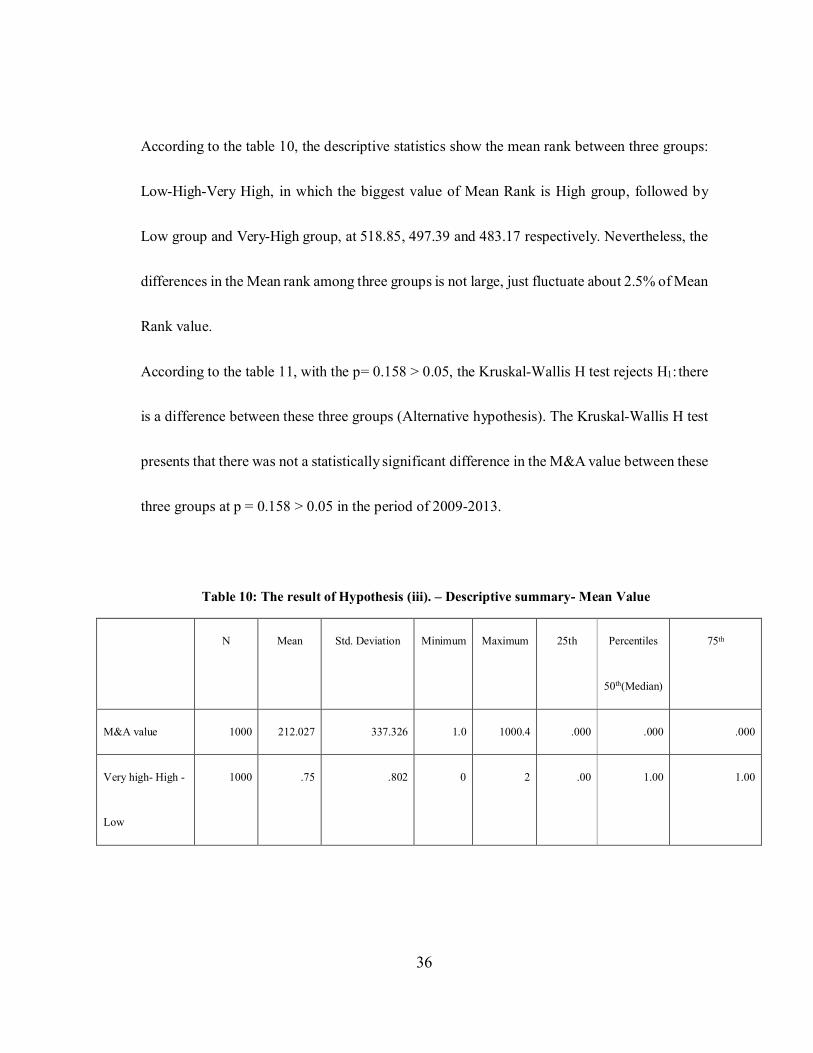

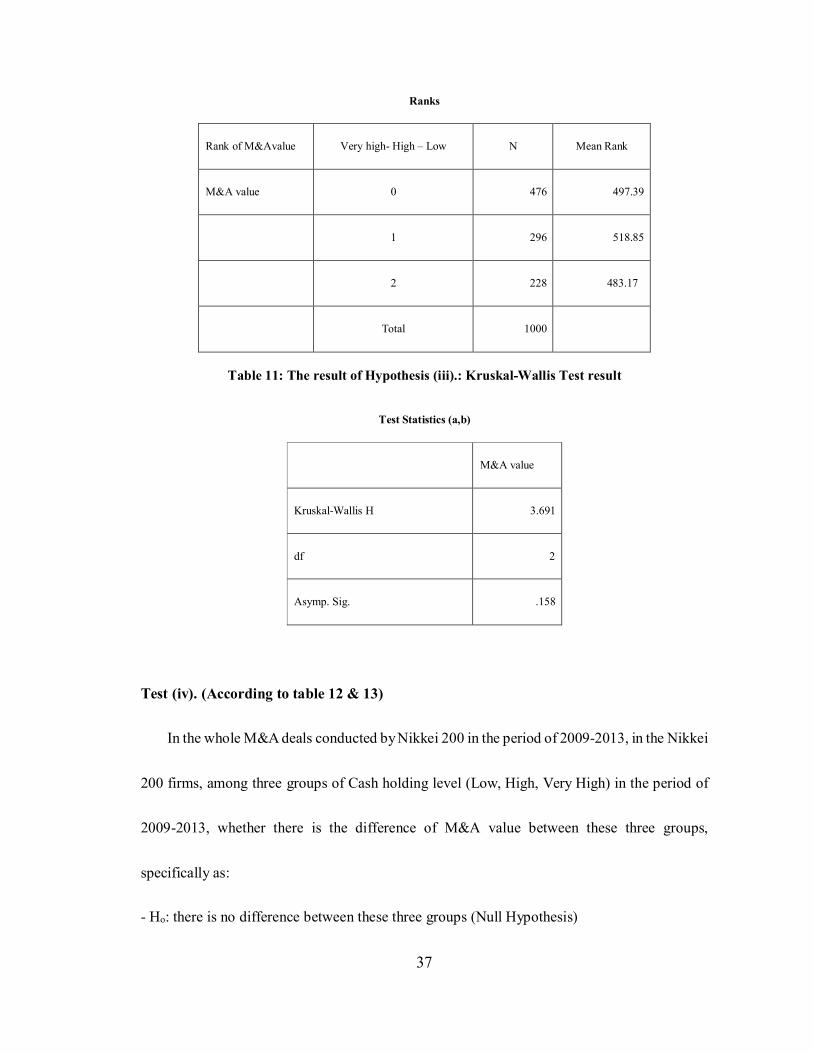

Test (iii). (According to table 10 & 11)

In the Nikkei 200 firms, among three groups of Cash holding level (Low, High, Very

High) in the period of 2009-2013, whether there is the difference of M&A value between these

three groups, specifically as:

- Ho: there is no difference between these three groups (Null Hypothesis)

- H1: there is a difference between these three groups (Alternative Hypothesis)

The research utilizes the Kruskal-Wallis to test the hypothesis above. 1000 observations will be

divided into three groups by the median thresholds of Nikkei industry ratio and whole Japanese

non-financial firm ratio: low-level, high-level and very-high-level of cash holding, respectively.

The test variable is M&A value.

36

According to the table 10, the descriptive statistics show the mean rank between three groups:

Low-High-Very High, in which the biggest value of Mean Rank is High group, followed by

Low group and Very-High group, at 518.85, 497.39 and 483.17 respectively. Nevertheless, the

differences in the Mean rank among three groups is not large, just fluctuate about 2.5% of Mean

Rank value.

According to the table 11, with the p= 0.158 > 0.05, the Kruskal-Wallis H test rejects H1: there

is a difference between these three groups (Alternative hypothesis). The Kruskal-Wallis H test

presents that there was not a statistically significant difference in the M&A value between these

three groups at p = 0.158 > 0.05 in the period of 2009-2013.

Table 10: The result of Hypothesis (iii). – Descriptive summary- Mean Value

N

Mean

Std. Deviation

Minimum

Maximum

25th

Percentiles

50th(Median)

75th

M&A value

1000

212.027

337.326

1.0

1000.4

.000

.000

.000

Very high- High -

Low

1000

.75

.802

0

2

.00

1.00

1.00

37

Ranks

Rank of M&Avalue

Very high- High – Low

N

Mean Rank

M&A value

0

476

497.39

1

296

518.85

2

228

483.17

Total

1000

Table 11: The result of Hypothesis (iii).: Kruskal-Wallis Test result

Test Statistics (a,b)

M&A value

Kruskal-Wallis H

3.691

df

2

Asymp. Sig.

.158

Test (iv). (According to table 12 & 13)

In the whole M&A deals conducted by Nikkei 200 in the period of 2009-2013, in the Nikkei

200 firms, among three groups of Cash holding level (Low, High, Very High) in the period of

2009-2013, whether there is the difference of M&A value between these three groups,

specifically as:

- Ho: there is no difference between these three groups (Null Hypothesis)

38

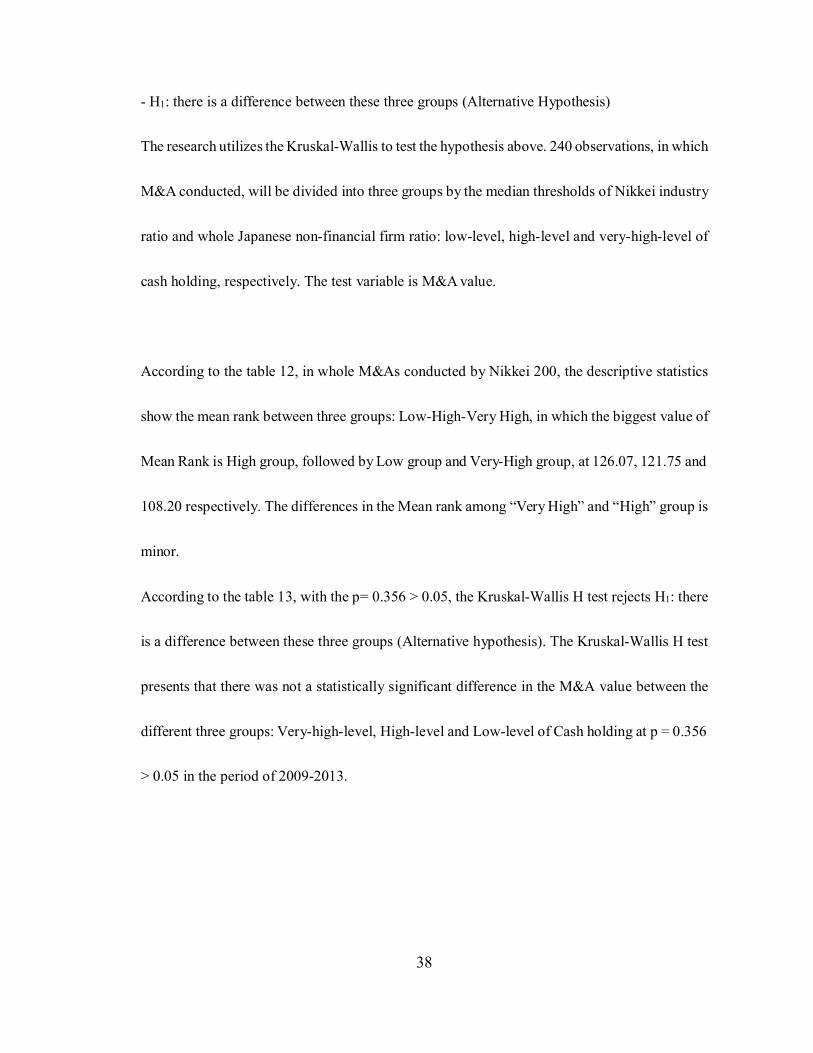

- H1: there is a difference between these three groups (Alternative Hypothesis)

The research utilizes the Kruskal-Wallis to test the hypothesis above. 240 observations, in which

M&A conducted, will be divided into three groups by the median thresholds of Nikkei industry

ratio and whole Japanese non-financial firm ratio: low-level, high-level and very-high-level of

cash holding, respectively. The test variable is M&A value.

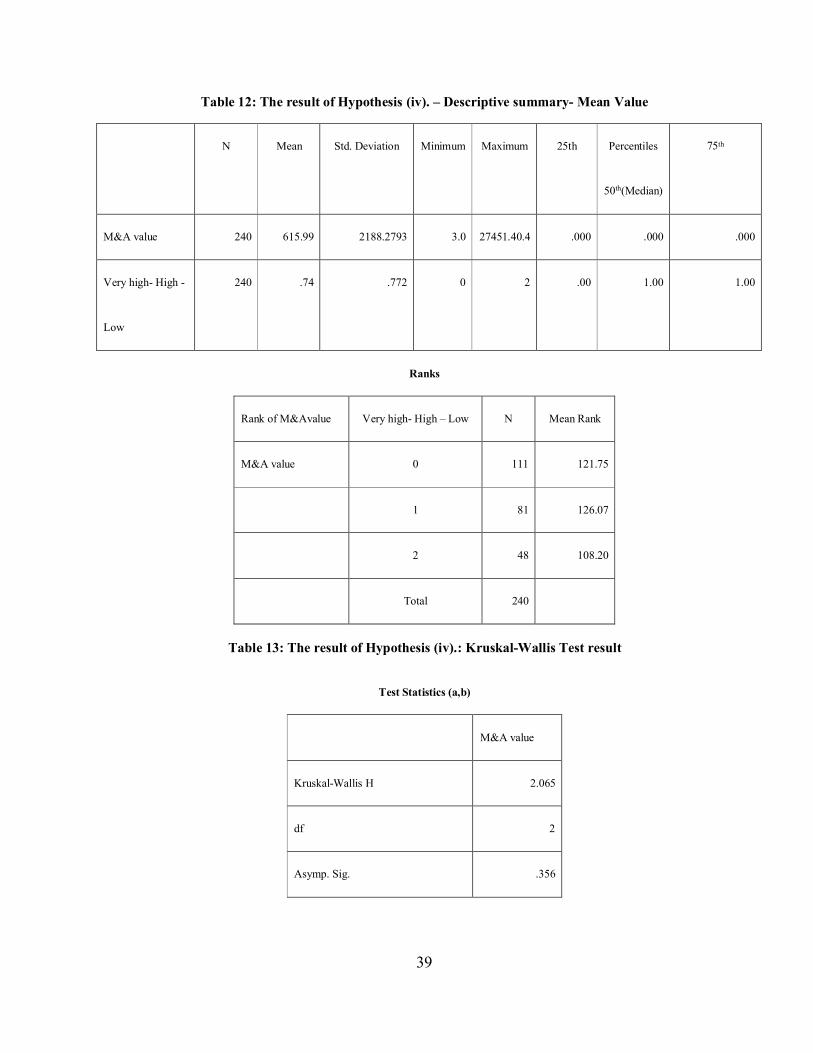

According to the table 12, in whole M&As conducted by Nikkei 200, the descriptive statistics

show the mean rank between three groups: Low-High-Very High, in which the biggest value of

Mean Rank is High group, followed by Low group and Very-High group, at 126.07, 121.75 and

108.20 respectively. The differences in the Mean rank among “Very High” and “High” group is

minor.

According to the table 13, with the p= 0.356 > 0.05, the Kruskal-Wallis H test rejects H1: there

is a difference between these three groups (Alternative hypothesis). The Kruskal-Wallis H test

presents that there was not a statistically significant difference in the M&A value between the

different three groups: Very-high-level, High-level and Low-level of Cash holding at p = 0.356

> 0.05 in the period of 2009-2013.

39

Table 12: The result of Hypothesis (iv). – Descriptive summary- Mean Value

N

Mean

Std. Deviation

Minimum

Maximum

25th

Percentiles

50th(Median)

75th

M&A value

240

615.99

2188.2793

3.0

27451.40.4

.000

.000

.000

Very high- High -

Low

240

.74

.772

0

2

.00

1.00

1.00

Ranks

Rank of M&Avalue

Very high- High – Low

N

Mean Rank

M&A value

0

111

121.75

1

81

126.07

2

48

108.20

Total

240

Table 13: The result of Hypothesis (iv).: Kruskal-Wallis Test result

Test Statistics (a,b)

M&A value

Kruskal-Wallis H

2.065

df

2

Asymp. Sig.

.356

40

4.2. Discussion:

Restate the research problem

The research problem starts from the paradox of the seminal documented evidence and the

reality of relation between Cash Holing and M&A values in the theme of Japanese non-financial

firms in the period of 2009-2013. The main idea of documented concepts is that higher level of

cash holding, the more M&As conducted. To examine comprehensively the relation between

level of cash holding and M&A value decision, the research goes through the tests with groups

of “Do M&A” and “Do not M&A”, groups of “High-level” and “Low-level” with thresholds

of industry C/A median and whole Japanese non-financial firm C/A median. Following strictly

the research question, the research findings show the main academic evidence that there was

not a statistically significant difference in the M&A value between the different groups,

specifically in high-level groups and low-level group.

The agency problem suggests that the large cash holding makes the manager tend to give more

M&A, meanwhile the research evidence shows the absence of this concept by proving that there

is not a statistically significant difference in the M&A value between the high or low level of

cash holding. Despite the cash holding in Japanese non-financial firm has rocketed to high level,

there is a huge lack of previous papers studying whether the concept of agency emerges in

Japanese economies, especially from the 2000s. This research contributes to knowledge by

41

updating the absence of this concept in the period 2009-2013 in the scope of Nikkei 200, the

most influencing firms in Japanese economies. In the limited number of paper in this theme,

the paper is consistent to the work of Kazuo et al. (2014), which points out the signal of agency

problem decrease in Japanese firms by presenting the academic evidences that these firms tend

to increase the payout to shareholders rather than hold cash for investment. The paper is also

consistent to paper of Ojo, M. (2013) with the academic evidence presenting that the bank

system of Japan has become one of the biggest investors and shareholders in Tokyo exchange

stock, therefore, in the long-term management, the bank system can boost the better

environment for communication between managers and shareholders and address the agency

problem. To interpret this situation, the research bases on two main approaching ways, as

follow:

Precautionary

In the first perspective, following the seminal theory suggested by Keynes (1936) about the

transaction cost and precautionary motive of cash in the investment decision. Basing on the

precautionary approaching, the firms tend to hold more cash to insure against to internal

financial distress and reduce future risks. The empirical work of Almeida et al. (2004) supports

this idea by proving that in financially constrained context, the firm reserves cash for the

precaution motivation as a core reason. Lins et al. (2010) argue that the firms hold

42

approximately 40% more cash than necessary to confront the financial distress and solve the

risks rather investing decision. This explaining way is more convincing in the period of 2009-

2013 when the Japanese economies suffered from double the finance crisis in 2009 and 2013.

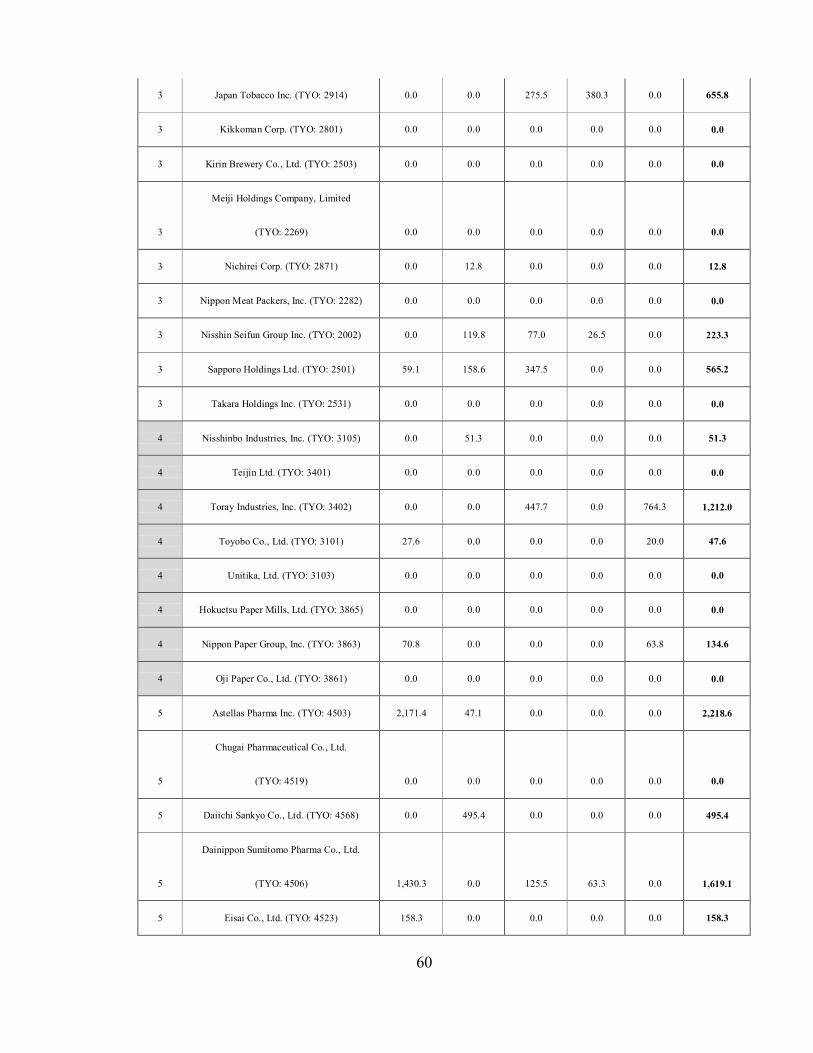

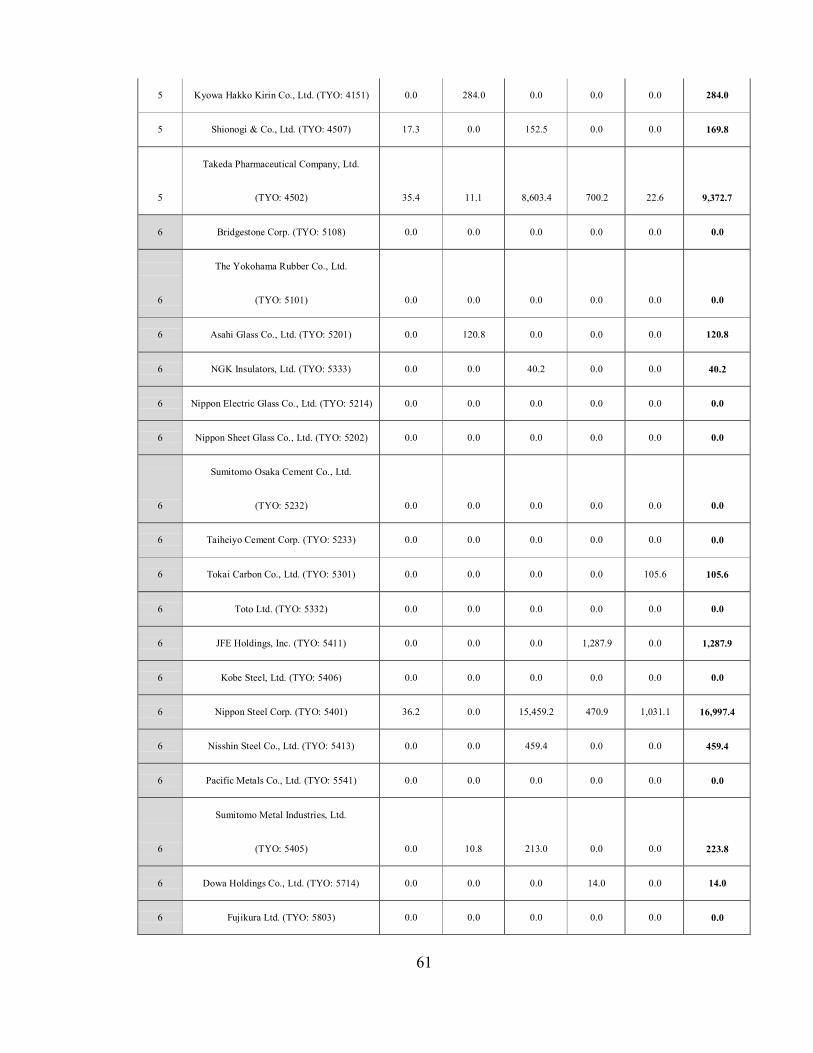

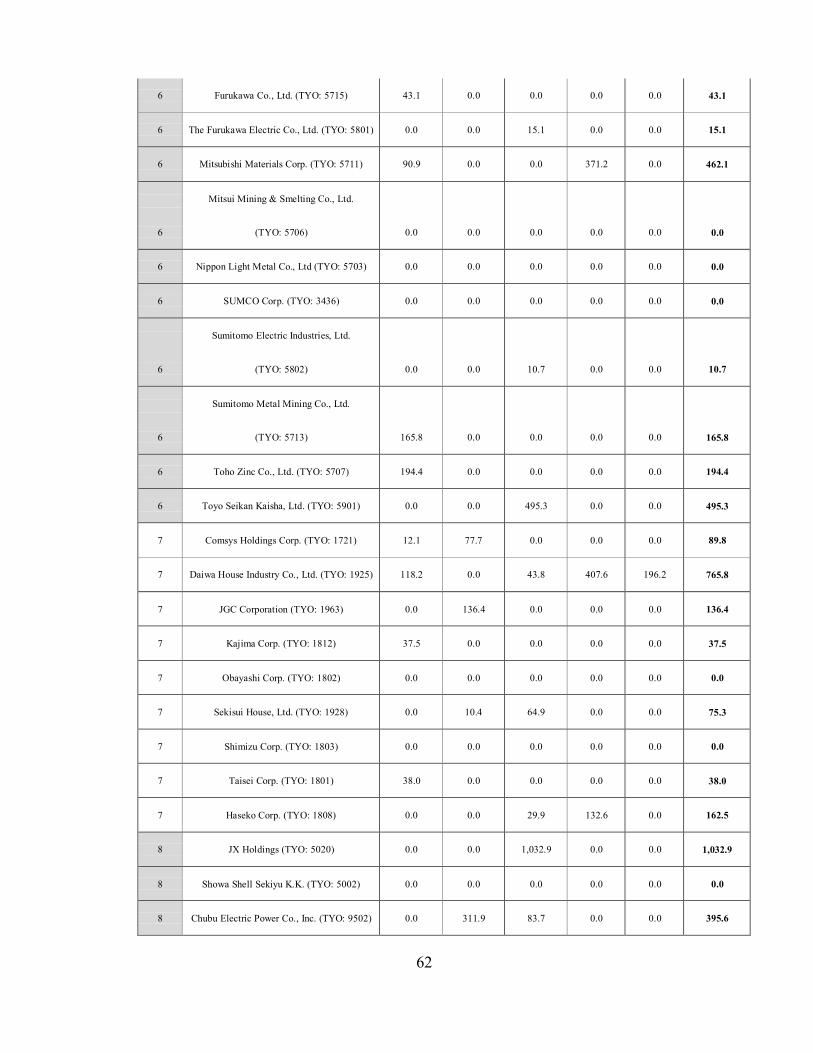

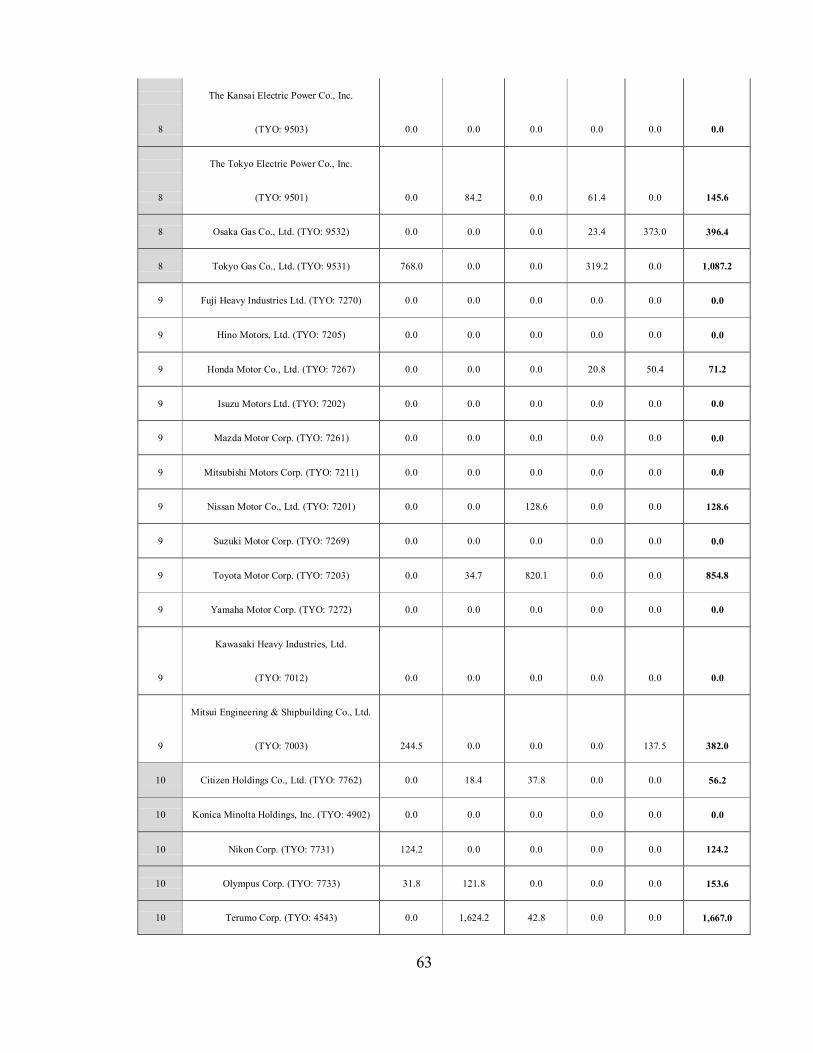

The work of Kawai et. al (2009) suggests that the deeply negative effect on the whole Japan

economies in the finance crisis 2008-2009, or Sommer (2009) proves that the financial crisis

had a greatly negative influence on the demand for high-tech manufacturing industry (car,

electric machinery, information technology) in not only Japan domestic but also global scope.

These authors’ arguments are consistent strongly to the research data scope of Nikkei 200.

Because Nikkei 200 are the biggest companies in Japan with the huge number of top firms in

the manufacturing industry, therefore, the double finance crisis clearly had the very strong

influence on their decision of cash holding or investment spending in the precautionary

approaching. Sommer (2009) also emphasizes that the financial crisis resulted in the strong

decline the business investment of Japanese firms, that is also very consistent to the research

finding in the precautionary approaching. In the other word, in such context above, the firms

tend to hold more cash for precautionary but for investment spending with agency approaching.

The characteristics of Nikkei 200

Because Nikkei 225 are the biggest firms in Japan, besides cash holding, they can approach

to capital market or bank loan actively and easily when conducting investment decision, such

43

as M&As. The first descriptive finding supports strongly to this explanation by showing that

the ratio of cash holding level in Nikkei 200 just fluctuated around 8.2%, which is much lower

than the ratio of cash holding in whole Japanese non-financial firms peaked to over 12%. This

finding is consistent to work of Dittmar et. al (2003) that suggests the largest firms in global

scope hold the cash ratio at 9% of book value. One of the main reasons for this low ratio will

be explained by the advantages of firm size and prestige. When the firms in Nikkei 200 tend to

do investment, such as M&As, they can raise fun with a number of resources: debts, stocks,

that reduce their dependence on Cash holding. Additional, according to the descriptive finding,

the average M&A value of Nikkei 200 just accounted for the relatively small at 11.3% of the

value of Cash holding. These ratios support the argument that the decision of M&A value does

not account for the big enough in preparation of cash holding in Nikkei 200.

From these arguments above, the reality of Cash paradox in the research should be considered

in the multiple perspectives by combining the theories and empirical evidence. The research

just limits at pointing out the indifference of M&A values in the different group of cash holding

and need more evidence to explain that in further empirical evidence. Despite the research

figure out the gap between the theory of agency problem and reality, the scope of research just

be wrapped in the Nikkei 200 of non-financial firms, the finding relating to financial firms, the

rest Japanese firms in the period of 2009-2013 still need to be interpreted. From that way, the

44

research suggests the further studying directions in the following steps: how to update the theory

of agency problem in the reality of typical period with variety of events and unexpected

variables, how to integrate multiple theories and empirical evidences of cash holding and

M&As deal to reflect more accurately the reality of economies.

45

CHAPTER 5: CONCLUSION

The chapter five will point out the integrated conclusions of the research with the main

contents: summary of whole research contents, contribution and recommendation, and

limitation and future research. The summary section will describe whole research flow in the

highlighted content. Then the section of contribution and recommendation will explain the

important role in academic term and real investment implication as well as suggest the direction

for related parties in the research theme. The last section makes clear the limitation of research,

give the lesson and reveal the further step of research.

5.1. Summary:

The research is conducted in the outstanding context of Japanese economies, in which the

cash holding of non-financial firms climbed rapidly to the top level comparing to other

advanced countries in global scope in the period of 2009-2013. The research theme is built in

the relation between cash holding and M&As, the investment type which has become one of

the biggest and most influencing financial activities in the global scope. The research problem

and question, respectively, are proposed basing on the paradox between the well-known

documented evidence and reality of Japanese non-financial firms in the period 2009-2013.

According to theories and empirical evidence, with the large cash holding, the firm tends to

conduct more M&A, nevertheless, the real number of whole Japanese non-financial firms

46

shows the different context between the increase of cash holding value and fluctuation or even

decrease of M&A values. The expected answer is to describe the relation between the level of

cash holding and M&A decision.

To answer this question, the research utilizes the sample of 200 non-financial firms in Nikkei

225 as the scope of research. The reasons to use this sample are: the Nikkei 200 stands for the

biggest and most influencing firms in Japan economies, that can reflect the financial health of

Japanese economies strictly, and the financial ratio relating to M&A events accounted for the

huge part in total Japanese M&A value in this period. In the term of cash holding, the research

calculates the cash ratio basing on the value of Cash and Cash equivalent in balance sheet of

fiscal year. Comparing to the thresholds of cash holding level, the cash ratio median of industry

and whole economies, 1000 observations of 200 firms in 5 years are classified into different

levels of cash holding. In the term of M&As, the most important related financial ratios are

collected and analyzed, as follow: the acquiring and acquired firms, the M&A value, the

frequency of M&A, whether M&A is completed.

By the main test of Kruskal-Wallis H in SPSS tools, the research points out the main result that

there was not a statistically significant difference in the M&A value between the different levels

of cash holding. The theory of precautionary motive in the context of Japanese economies in

47

the period 2009-2014 and the characteristics of Nikkei 200 should be the crucial explanation

for these findings.

5.2. Contribution and recommendation:

5.2.1. Contribution:

The research contributes two key points to knowledge: (i). update the agency problem and

combine the explanation from related theory in the trending issues, and (ii). fill the gap of

research about the relation between cash holding and M&As value in the typical period.

Update the agency problem and combine the explanation of the related theory in the

trending issues

The rapid increase of cash holding has been known clearly as the outstanding phenomenon

of not only in Japanese non-financial firms but also in whole Japanese economies. The relation

between the cash holding and M&A investment has been documented in the range of theories

and empirical evidence, in which the key idea is that with the large cash holding, the firm tends

to do more M&A. The agency problem is considered as the sufficient explanation for this

concept. By giving the academic evidences that there is no significant difference in M&A value

between the levels of cash holding, the research can update this concept in the reality of

Japanese context. The research contributes to knowledge by giving the academic evidence to

48

prove the absence of agency problem in the period of 2009-2013. The finding is consistent to

the work of Kazuo et al. (2014), which points out the signal of agency problem decrease in

Japanese firms by presenting the academic evidence that these firms tend to increase payout to

shareholders rather than hold cash for investment. The paper is also consistent to paper of Ojo,

M. (2013) with the academic evidences presenting that the bank system of Japan become one

of the biggest investors and shareholders in Tokyo exchange stock, therefore, in the long-term

management, the bank system can boost the better environment for communication between

managers and shareholders and address the agency problem.

The value of research also bases on the scope of research. The research focuses on the strongest

and most representative index in Japanese economies, 200 Nikkei non-financial firms, with the

Nikkei 200’s M&A value accounting for above 53% of whole Japanese economies’ one in

average. Besides, the period of research witnessed the clear paradox between the cash holding’s

rapid increase and slight fluctuation or even decrease of M&A value in 2009-2014. The research

also supports for seminal concepts of precautionary that Japanese non-financial firms increase

the cash holding level for risk and cost reduction under the effects of turbulent macro external

factors, such as financial crisis 2009 and 2011, or micro factors, such as characteristics of the

typical firm group, Nikkei.

49

The lack of efforts to address the academic problem about Japanese firms

There is a huge lack of efforts to make clear the relation between the cash holding and

M&A events in Japanese economies in the period since 2009. With both the level of cash

holding in Japanese non-financial firms and value of Japanese M&As ranked in the global top

group of the advanced countries, this relation is worth to investigate by the deep research.

Despite there is a number of previous papers which mention about the determinants for cash

holding of Japanese firms, the relation between cash holding and M&A values of Japanese firms

still have big academic gaps to fill. This research contributes to this knowledge gap by focusing

the M&A value in the angle of cash holding levels in 2009-2013, the period witnessed the cash

paradox, and the many important economics events not only in Japan, but also in the global.

Moreover, there is very modest number of papers which study about the concept of agency

problem in Japanese non-financial firms, therefore, this research contributes to knowledge by

updating and reviewing this concept.

Last but not least, in the context that there is the shortage of academic literature, which studies

the Nikkei 225 index, the most influencing index of Japanese economies, the research

contributes to knowledge by giving the description of 200 Nikkei non-financial firms in Cash

holding and M&A ratio in whole Nikkei 200 and every industry scope.

50

5.2.2. Recommendation:

To academic understanding of this issue

From the finding of research, the recommendation focuses on the updating of the agency

problem and related concept about cash holding and M&A. The agency problem should be the

primary concept to develop and apply, nevertheless, it will be bias if not referencing related

ones: precautionary motive in the trade-off theory, or macro and micro factors related. The

Japanese economies should be the outstanding sample system in this concept reviewing because

the typical status of cash holding and M&A value in the period of 2009-2013.

To practitioners who may be investing in Japan or regulating Japanese business:

When investing on Japanese firms, it is apparent that the Nikkei 225 is always one of the

most outstanding and attractive options for investor community because of their prestige and

influences. Every investment decision of these giant Nikkei firms can affect considerably to

whole investing value of whole economies in short and long term. Specifically, the fact that the

level of cash holding has climbed up to top level comparing to global scope since the 2000s,

emerges the consideration and worries of investing and observing parties about the

effectiveness of cash flow and capital expenditure. The agency concept contributes to this

problem as a main reason. From the finding, the research supports the absence of agency

problem in the investment of cash holding, that suggests the light of healthy environment in

51

cash policy of manager.

5.3. Limitation and future research:

The section of limitation and future research will review the gaps of this research in theory

application, data scope analyzation, lack of controlling related factors. Then, the research

suggests the further direction of research to fill these blanks and figure out the comprehensive

knowledge about the relation of cash holding and M&As.

Update the theory relating to Cash holding and M&As

The research focuses on the concept of positive relation between cash holding and M&A

documented by the academic evidence relating to agency problem. This problem occurs in the

firms in variety of approaching way, such as cash or debt (Jensen, 1986). The research focuses

on cash holding as a main direction, and needs to extend in debt in further step. In addition,

despite this concept is well documented in the academic world, it will be more reasonable and

effective in answering the reality of economics when combining with another related theories.

In the further steps, the research suggests the combination of the integrated theories and

hypothesis to investigate deeply and convincingly this research theme.

Scope of research

Despite 200 non-financial firms in Nikkei 225 have the largest size and most influencing

52

roles in Japanese economies, they are just the part of whole big Japanese economies. The

research needs to extend the scope size to clearly describe the trendy issues of Cash holding

and M&As in whole Japanese economies. The research problem and question about this theme

is still the gaps in the rest parts of Japanese economies in the period of 2009-2013 and later.

Therefore, for next steps, the extension of data scope is a clear direction to achieve the valuable

paper.

Additional variables in the relation between cash holding and M&As

Clearly, cash is the one of the most important factors which the acquiring firm conducts

M&A. According to data analyzed of research, just below 7.3% of whole M&A transactions

conducted by another tools, such as debt or stock, nevertheless, the research does not mention

effects of these tools. This suggests the further steps with the integration of tools to conduct

research comprehensively. The other internal factors from the target firms should be also

considered, such as strategy section, competitive advantage or financial health to give the result

more accurately.

53

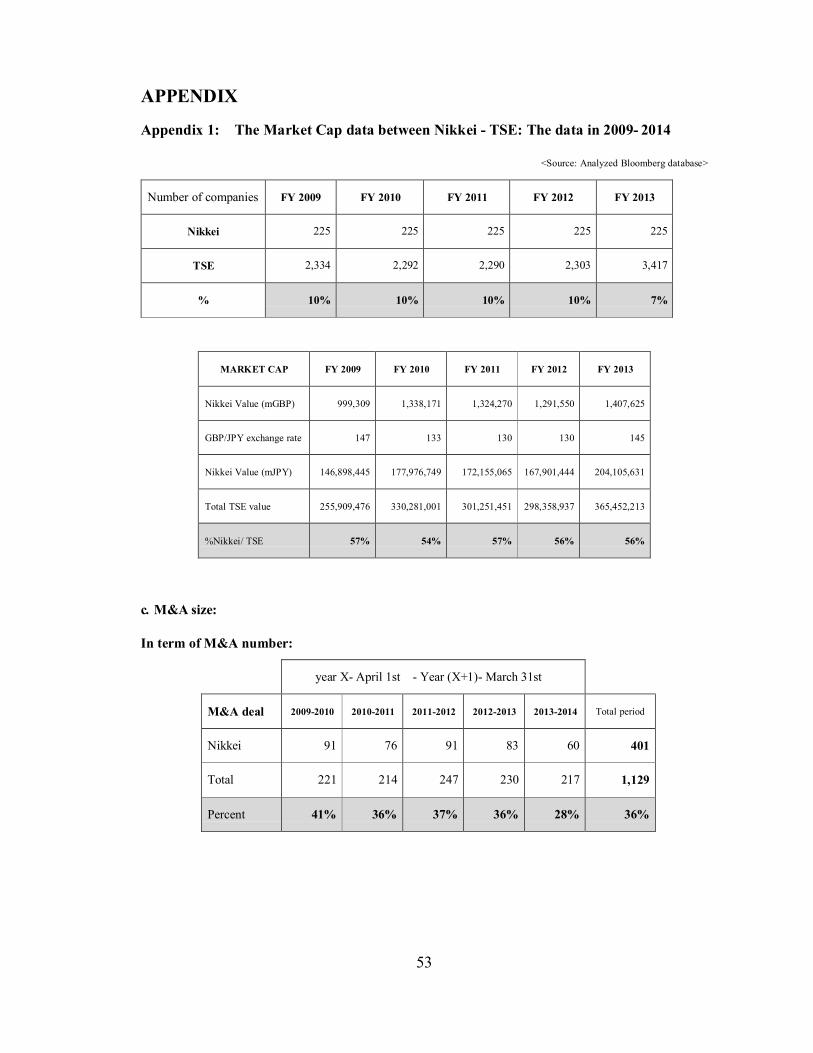

APPENDIX

Appendix 1: The Market Cap data between Nikkei - TSE: The data in 2009- 2014

<Source: Analyzed Bloomberg database>

Number of companies FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

Nikkei 225 225 225 225 225

TSE 2,334 2,292 2,290 2,303 3,417

% 10% 10% 10% 10% 7%

MARKET CAP

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

Nikkei Value (mGBP)

999,309

1,338,171

1,324,270

1,291,550

1,407,625

GBP/JPY exchange rate

147

133

130

130

145

Nikkei Value (mJPY)

146,898,445

177,976,749

172,155,065

167,901,444

204,105,631

Total TSE value

255,909,476

330,281,001

301,251,451

298,358,937

365,452,213

%Nikkei/ TSE

57%

54%

57%

56%

56%

c. M&A size:

In term of M&A number:

year X- April 1st - Year (X+1)- March 31st

M&A deal

2009-2010

2010-2011

2011-2012

2012-2013

2013-2014

Total period