© The McGraw-Hill Companies, Inc., 2008 McGraw-Hill/Irwin Chapter 4 Future Value, Present Value and Interest Rates

© The McGraw-Hill Companies, Inc., 2008 McGraw-Hill/Irwin Chapter 4 Future Value, Present Value and Interest Rates.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© The McGraw-Hill Companies, Inc., 2008McGraw-Hill/Irwin

Chapter 4

Future Value, Present Value and

Interest Rates

4-2

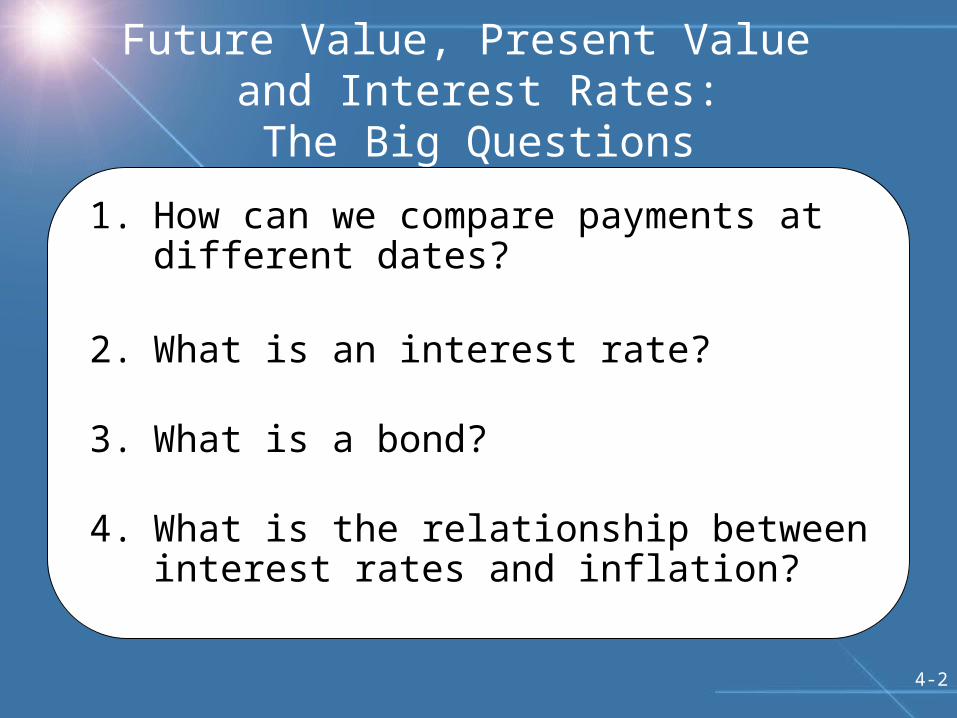

Future Value, Present Value and Interest Rates:The Big Questions

1. How can we compare payments at different dates?

2. What is an interest rate?

3. What is a bond?

4. What is the relationship between interest rates and inflation?

4-3

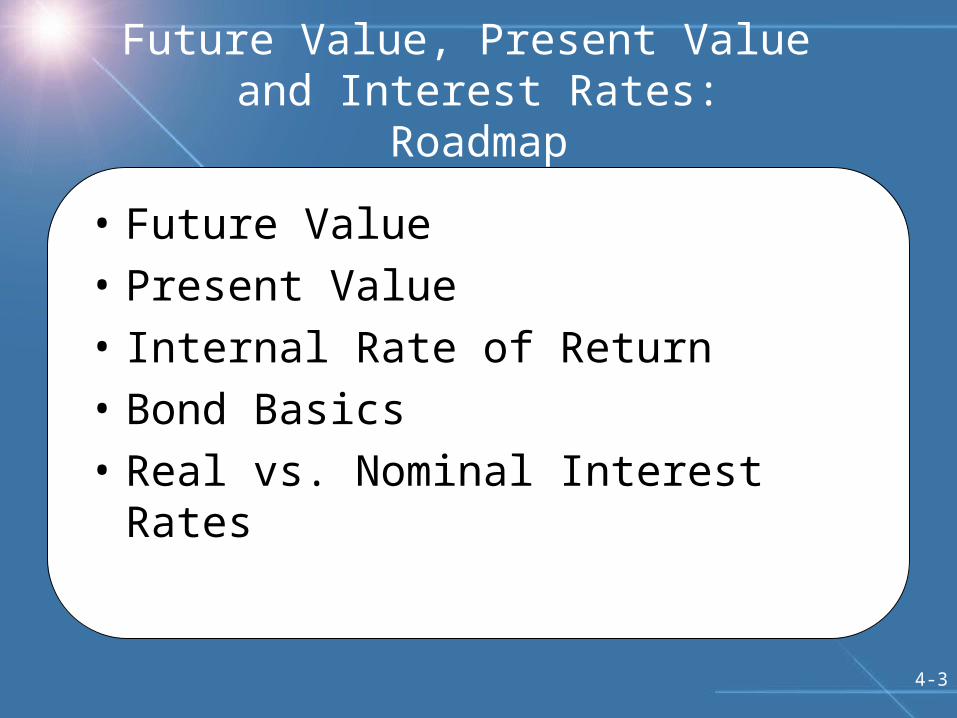

Future Value, Present Value and Interest Rates:

Roadmap

• Future Value

• Present Value

• Internal Rate of Return

• Bond Basics

• Real vs. Nominal Interest Rates

4-4

A Brief History of Lending

• Lenders despised throughout history.

• Credit is so basic that we evidence of loans going back 5 thousand years.

• Hard to imagine an economy without it.

• Yet, people still take a dim view of lenders because they charge interest

4-5

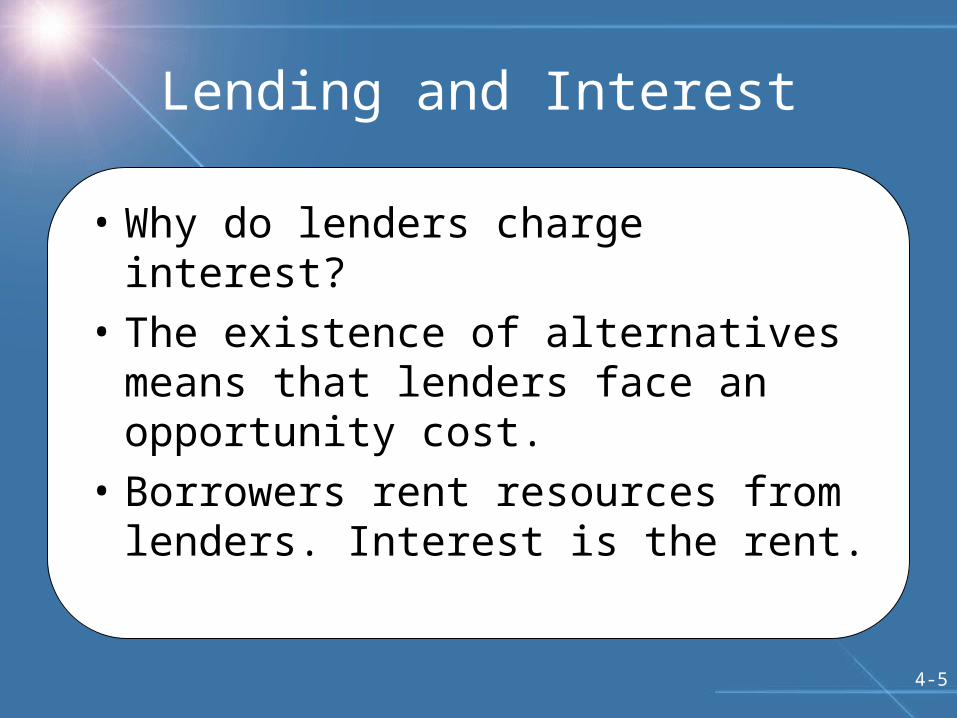

Lending and Interest

• Why do lenders charge interest?

• The existence of alternatives means that lenders face an opportunity cost.

• Borrowers rent resources from lenders. Interest is the rent.

4-6

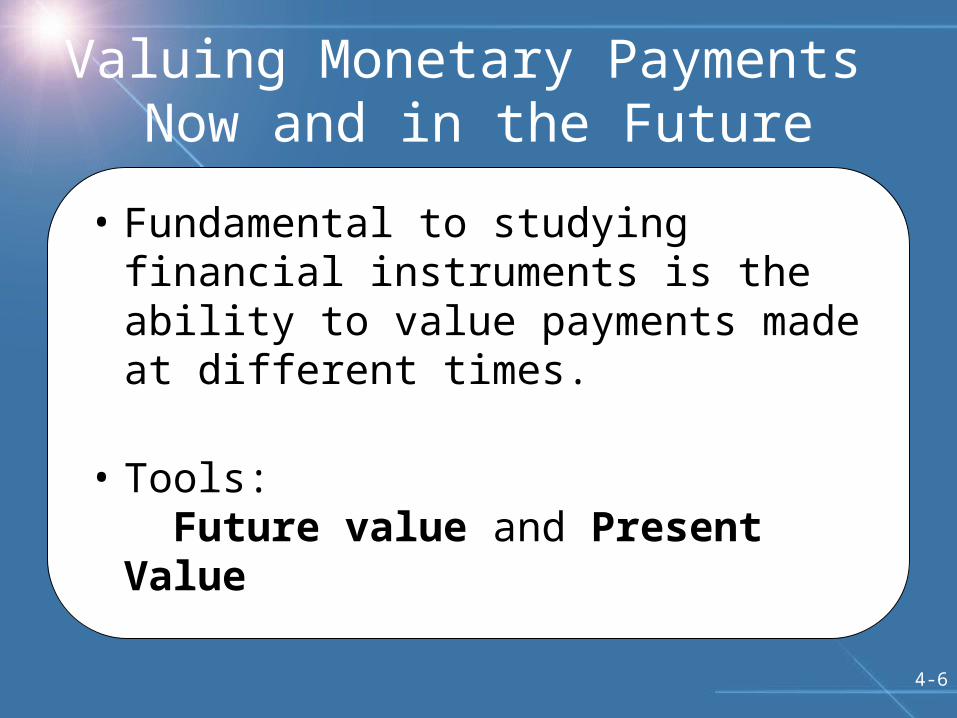

Valuing Monetary Payments Now and in the Future

• Fundamental to studying financial instruments is the ability to value payments made at different times.

• Tools: Future value and Present Value

4-7

Future Value:Definition

The value on a future date of an investment made today.

If you invest $100 today at 5 percent interest per year, in one year you will have $105.

4-8

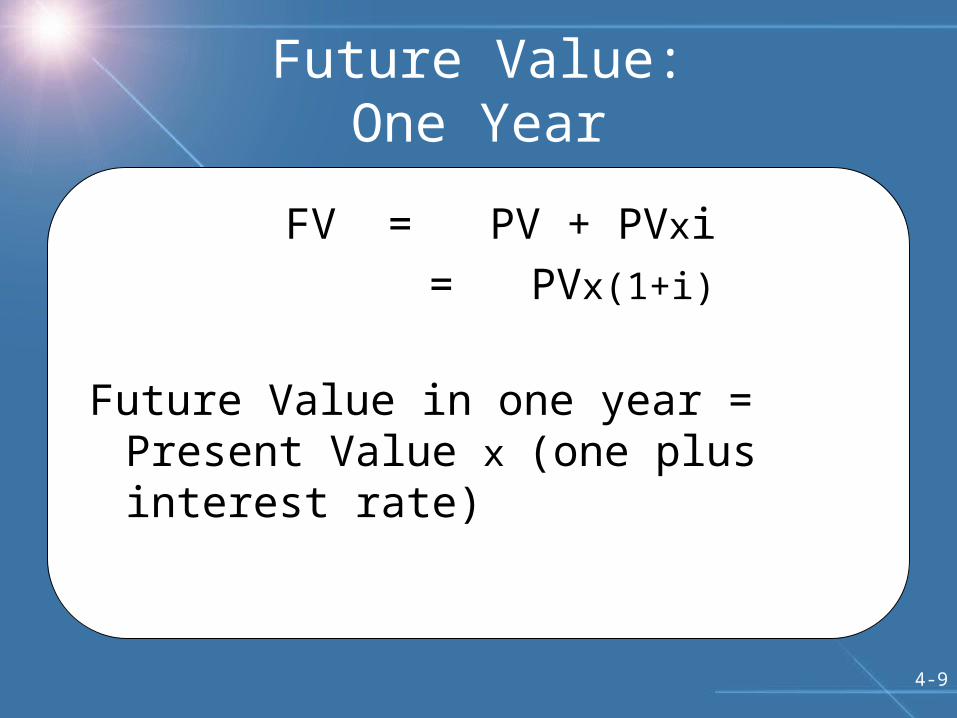

Future Value:One Year

Future Value =Present Value + Interest

FV = PV + PVxi

$105 = $100 + $100x(0.05)

4-9

Future Value:One Year

FV = PV + PVxi

= PVx(1+i)

Future Value in one year =Present Value x (one plus interest rate)

4-10

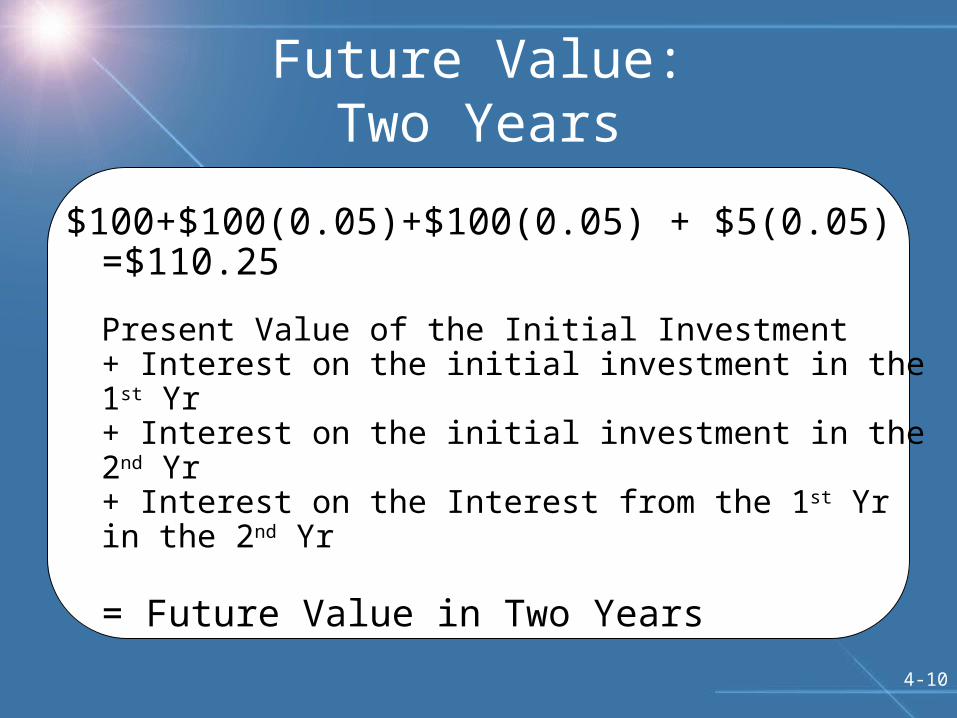

Future Value:Two Years

$100+$100(0.05)+$100(0.05) + $5(0.05) =$110.25

Present Value of the Initial Investment + Interest on the initial investment in the 1st Yr + Interest on the initial investment in the 2nd Yr+ Interest on the Interest from the 1st Yr in the 2nd Yr

= Future Value in Two Years

4-11

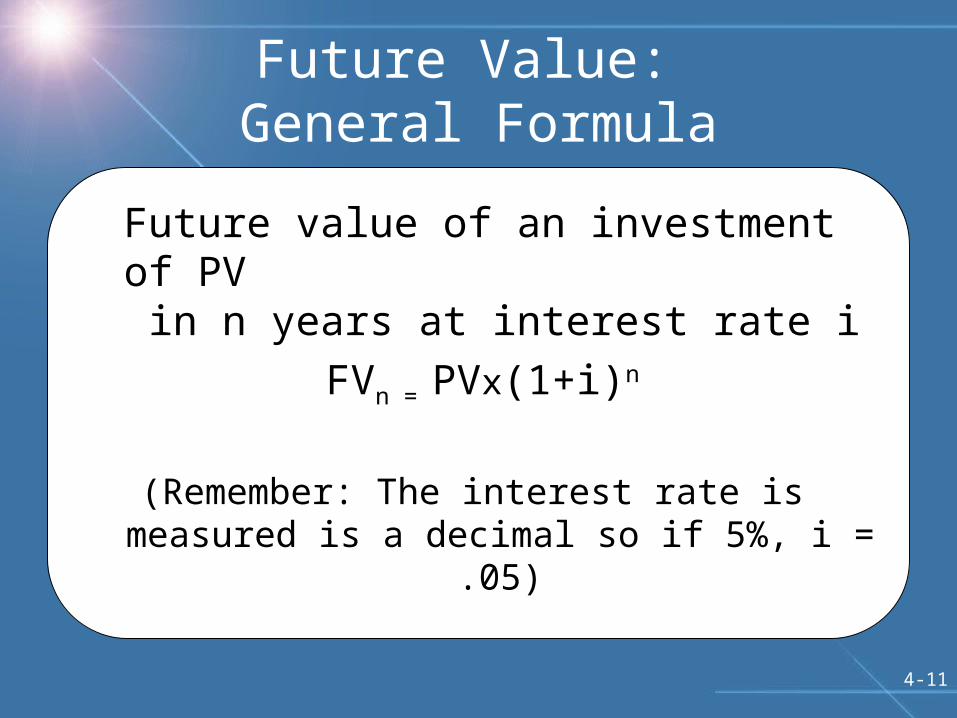

Future Value: General Formula

Future value of an investment of PV in n years at interest rate i

FVn = PVx(1+i)n

(Remember: The interest rate is measured is a decimal so if 5%, i = .05)

4-12

Future Value:$100 Investment at 5% Annual Interest

After 10 years, $100 as grown to $162.89 – that’s the initial investment of $100 plus interest of $62.89. Ignoring compounding, you would have just multiplied 5 percent times 10 years and gotten $50. The difference of $12.69 comes from compounding.

4-13

Future Value: Caution

Time (n) & interest rate (i) must be in same time units

If i is at annual rate, then n must be in years.

Future Value of $100 in 18 months at 5% annual interest rate is

FV = 100 x (1+.05)1.5

4-14

• Invest $100 at 5% annual interest

• How until you have $200?

• The Rule of 72:– Divide the annual interest rate into 72– So 72/5=14.4 years.– 1.0514.4 = 2.02

4-15

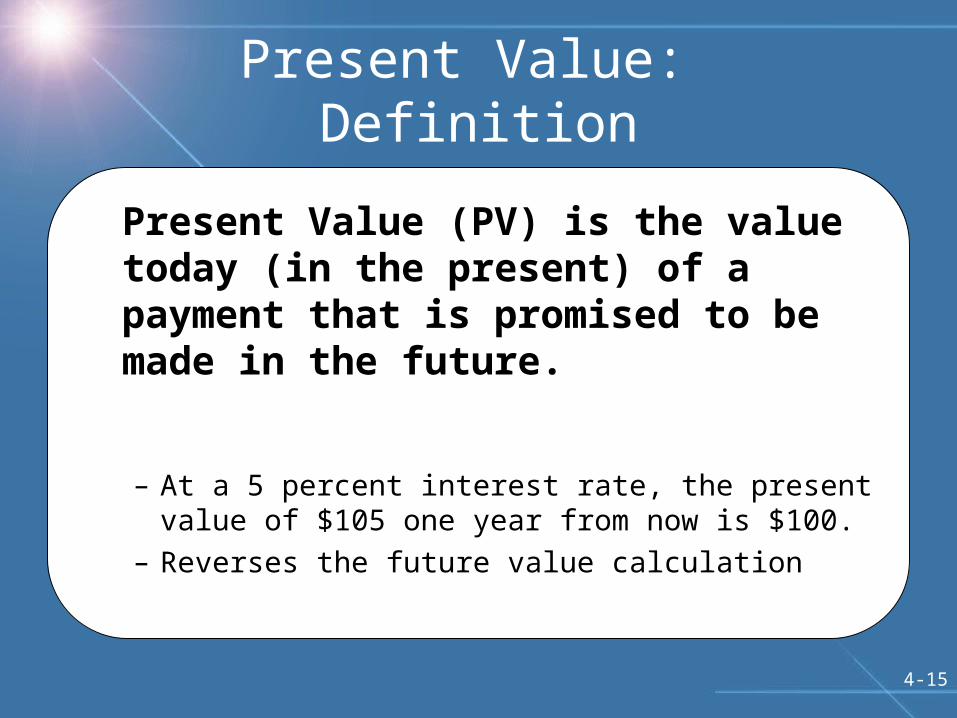

Present Value: Definition

Present Value (PV) is the value today (in the present) of a payment that is promised to be made in the future.

– At a 5 percent interest rate, the present value of $105 one year from now is $100.

– Reverses the future value calculation

4-16

Present Value:One Year

Solve the Future Value Formula for PV:

FV = PV x (1+i)so

Present Value = Future Value divided by one plus interest rate

)1( i

FVPV

4-17

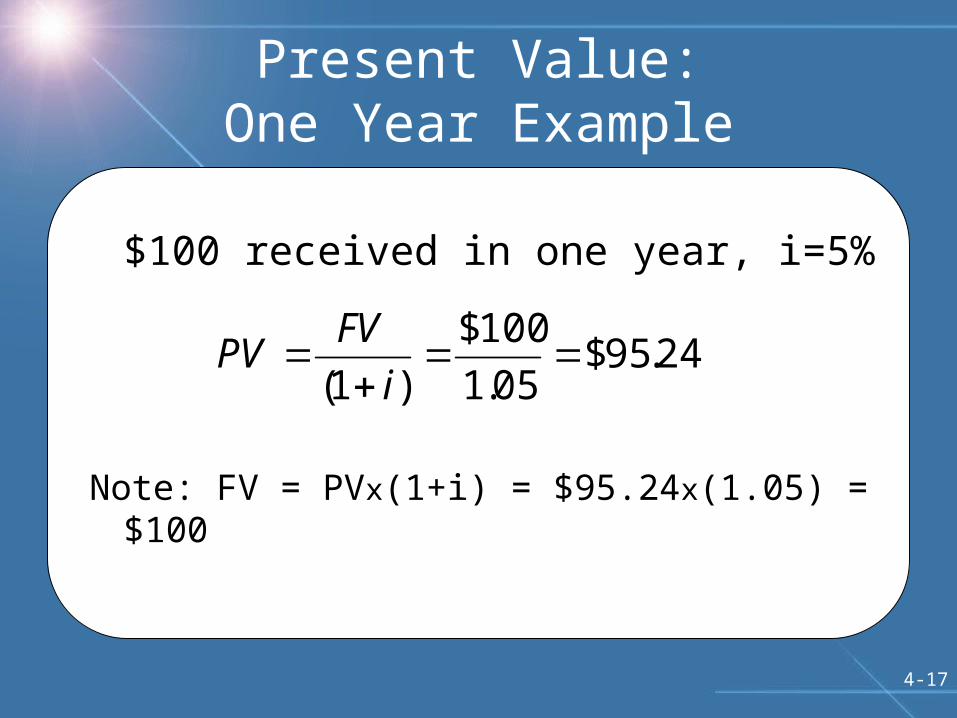

Present Value:One Year Example

$100 received in one year, i=5%

Note: FV = PVx(1+i) = $95.24x(1.05) = $100

24.95$05.1

100$

)1(

i

FVPV

4-18

Present Value:General Formula

Present Value of payment received n years in the future:

ni

FVPV

)1(

4-19

Present Value:Example

Present Value of $100 received in 2½ yrs at interest rate of 8%.

Note: FV = PVx(1+i)n=$82.50x (1.08)2.5 = $100

20.85$)08.1(

100$

)1( 5.2

ni

FVPV

4-20

Present Value:Important Properties

Present Value is higher:

1. The higher future value of the payment. (FV bigger)

2. The shorter time period until payment. (n smaller)

3. The lower the interest rate. (i smaller)

4-21

Present Value:$100 at 5% interest rate

Note rate of decline of Present Value. At a 5% interest rate, a $100 payment made in 14.4 years has a PV=$50.

4-22

Present Valueof $100 Payment

As the interest rate rises from 1% to 5%, a payment due

•1 year falls by $3.77

•10 years falls by $29.14

4-23

• Divine law of Islamic religion (Shari’a) forbids paying interest

• Banks developed alternatives.• Liabilities

– Deposit accounts: No interest– Investment accounts: Share in bank’s profits or

losses

• Assets– Profit share in exchange for loan

4-24

• Investment grows 0.5% per month• What is the compound annual rate?

FVn=PV(1+i)n = 100x(1.005)12=106.17

Compound annual rate = 6.17%(Note: 6.17 > 12x0.05=6.0)

4-25

To decide you need to compare

1. The value of the extra savings you will accumulate from waiting that allows you to purchase a more expensive care

2. The value of having the new care sooner.

4-26

Internal Rate of Return:Definition

The interest rate that equates the present value of an investment

with its cost.

4-27

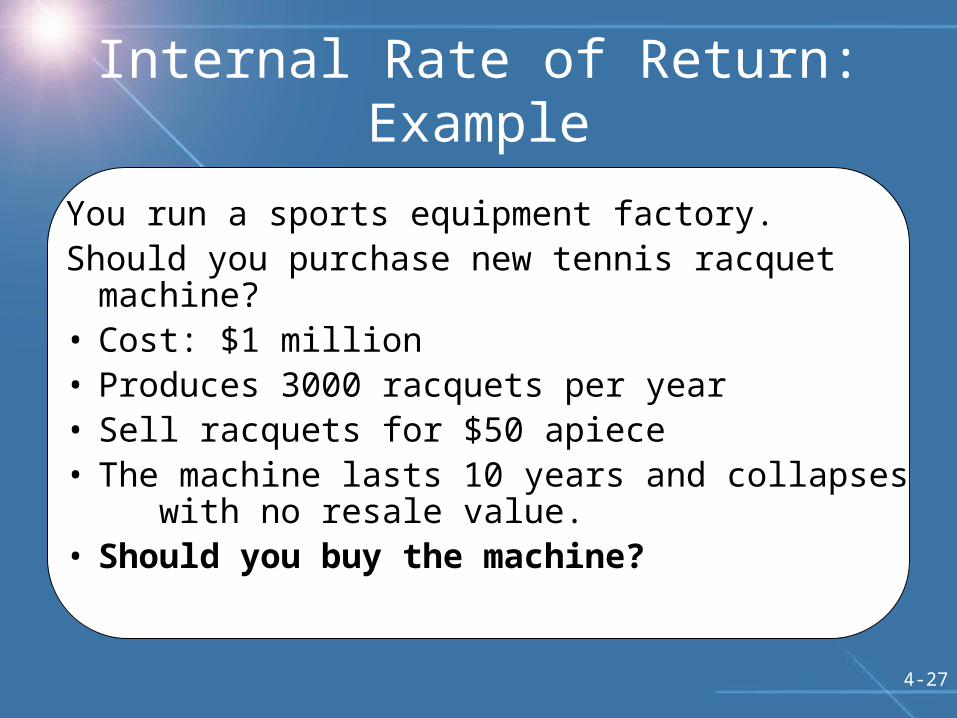

Internal Rate of Return:Example

You run a sports equipment factory.Should you purchase new tennis racquet machine?• Cost: $1 million• Produces 3000 racquets per year • Sell racquets for $50 apiece• The machine lasts 10 years and collapses

with no resale value.• Should you buy the machine?

4-28

Internal Rate of Return:Example

• Balance the cost of the machine against the revenue

• $1 million today vs. $150,000 a year for ten years.

• Is the $150,000 revenue enough to make payments on a $1 million loan?

4-29

Internal Rate of Return:Example

Solve for i:

$1,000,000

10321 )1(

000,150$......

)1(

000,150$

)1(

000,150$

)1(

000,150$

iiii

Solving for i, i=.0814 or 8.14%

4-30

Can you retire when you’re 40?

• Assume– Live to 85– Interest rate = 4%– Want to have $100,000 per year

• You will need004,072,2$

)04.1(

000,100$

)04.1(

000,100$

)04.1(

000,100$

)04.1(

000,100$

)04.1(

000,100$4544321

4-31

Bond Basics

• Bond: A promise to make a series of payments on specific future date

• Bond Price = Present Value of payments

4-32

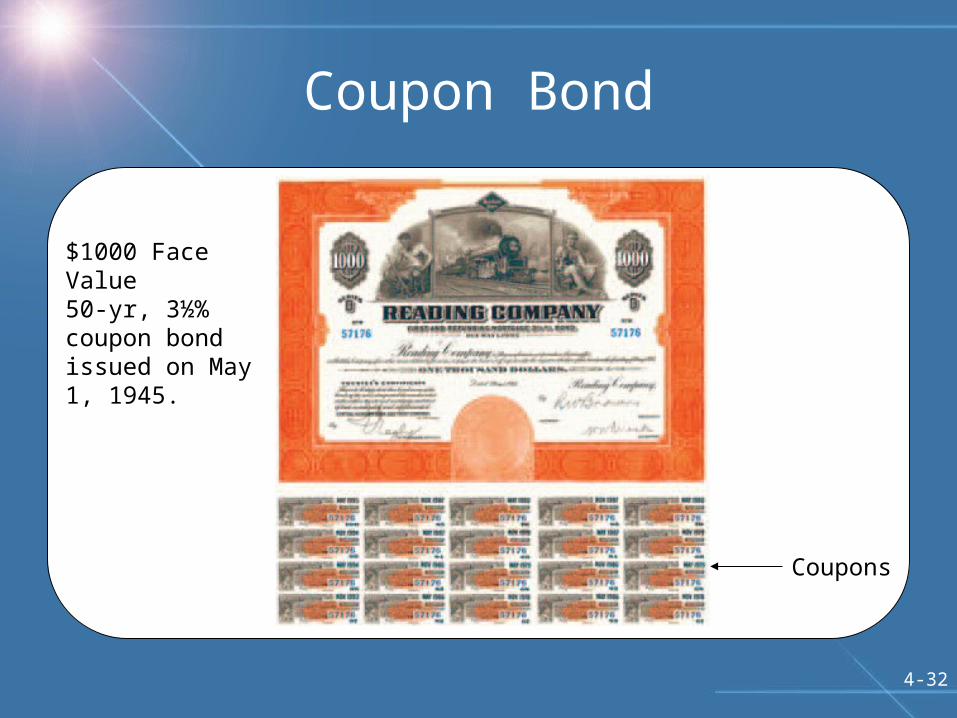

Coupon Bond

Coupons

$1000 Face Value50-yr, 3½% coupon bond issued on May 1, 1945.

4-33

Coupon Bond

• A type of loan:– Interest paid during the life of the loan– Loan repaid at maturity

• Coupon Rate: the annual interest the borrower pays (ic)

• Maturity Date: when the payments stop and the loan is repaid (n)

• Principal: the final payment (F)

4-34

Coupon Bond:Valuing the Principal

nnBP ii

FP

)1(

100$

)1(

Present value of Bond Principal = Payment divided by one plus the interest rate raised to n

4-35

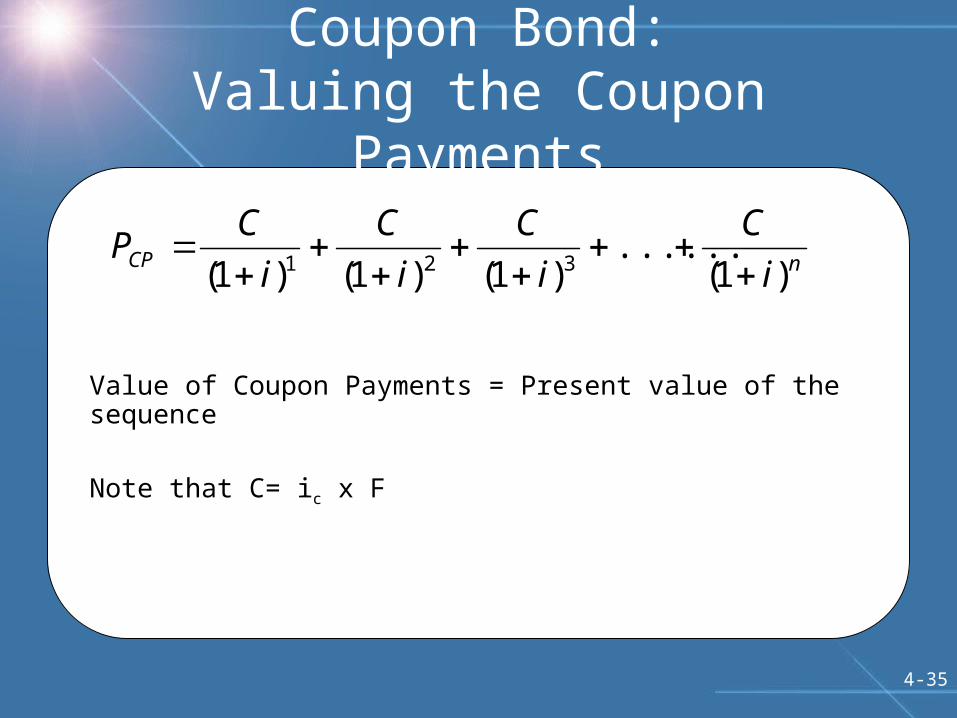

Coupon Bond:Valuing the Coupon Payments

nCP i

C

i

C

i

C

i

CP

)1(......

)1()1()1( 321

Value of Coupon Payments = Present value of the sequence

Note that C= ic x F

4-36

Price of Coupon Bond:Principal + Coupons

Price of Coupon Bond (PCB) =

Present value of Coupon Payments (PCP) + Present Value of the Principal (PBP)

nnBPCPCB i

F

i

C

i

C

i

C

i

CPPP

)1()1(......

)1()1()1( 321

4-37

Bond Pricing:Important Property

The price of a bond (PCB) and the interest rate (i) are inversely related:

i PCB

4-38

• Credit cards are useful.

• But lenders charge high interest rates.

• Pay off your balance as fast as you can.

4-39

Real and Nominal Interest Rates

• Borrowers care about the resources required to repay.

• Lenders care about the purchasing power of the payments they received.

• Neither cares solely about the number of dollars, they care about what the dollars buy.

4-40

Real and Nominal Interest Rates

Nominal Interest Rates (i)

Interest Rates expressed in current dollar terms.

Real Interest Rates (r)

Nominal Interest Rate adjusted for inflation.

4-41

Real and Nominal Interest Rates

Nominal interest rate = Real Interest Rate + Expected Inflation

i = r + e (This is called the “Fisher Equation”)

4-42

Nominal Interest Rate, Inflation Rate and Real Interest Rate

Nominal Interest Rate = Real Interest Rate + Expected Inflation

4-43

Real and Nominal Interest Rates

Countries with high nominal interest rates have high inflation:

i

© The McGraw-Hill Companies, Inc., 2008McGraw-Hill/Irwin

Chapter 4

End of Chapter

Related Documents