Will Mobile Payments Future be on your wrist ?

Yvon MOYSAN, Saint Germain Consulting & IESEG School of Management

EFMA Mobile Banking Advisory Council

27th of March 2015

Wearable payments: first initiative in 2011

• Nearly four years ago, U.S. Bank

launched a medical bracelet that could also make payments: it was a failure.

• But today the situation is

different

htt

p://v

isio

n.v

isa

eu

rop

e.c

om

/art

icle

/wea

rab

le-p

aym

en

ts-f

ail

ure

-in

-20

11

-su

ccess

-in

-

20

15

/80

c35

29

ce9

75

74

ffe2

3f7

defc

fb0

e2

0c

htt

p://t

hefi

na

nci

alb

ran

d.c

om

/19

20

2/u

s-b

an

k-c

on

tact

less

-pa

ym

en

t-w

rist

-ba

nd

/

“[…] when we did the test, you had to tell the merchant that you were going

to use contactless payments […]

Dominic Venturo, chief innovation officer, U.S. Bank.

Wearable payments: the situation today

• In 2015, 4.9 Billions Connected "Things" will be in use, up to 40% from 2014. By 2020, this number will reach 30 billions (1)

• The market for U.S. mobile payments will expand from $52 billion in 2014 to $142 billion by 2019 (2)

• Non-banks have built wearable payments applications such as PayPal and Walt Disney Co.

• The launch of Apple Pay and Apple Watch elevate the potential of wearable payments in consumers' minds. h

ttp

://w

ww

.pa

ym

en

tsso

urc

e.c

om

/new

s/te

chn

olo

gy/m

agic

ba

nd

s-u

sed

-by-h

alf

-of-

dis

ney-

worl

d-g

uest

s-3

01

87

43-1

.htm

l

(1): Source: Gartner (Nov.2014)

(2): Source: Forrester Research

Wearable payments: customer’s attitudes today

htt

p://w

ww

.em

ark

ete

r.co

m/A

rtic

le/W

ea

rab

les-N

ext-

Mob

ile-P

aym

en

t-D

evic

e/1

01

21

34

• Among US smartphone owners, more than 2/3 said they would prefer to use a wearable device over a mobile phone to make in-store payments.

• Mobile payments could also increase the frequency of wearables usage, as 50% of respondents said they would a wearable device more if it could make in-store payments.

• Overall, more than 40% of respondents said they would make in-store payments via wearables.

(1): Source: Stratos (Dec 2014 )

Banks and non Banks test how different wearable devices can be used in and around point of sale

terminals

Heritage Bank

htt

p://w

ww

.pa

ym

en

tsso

urc

e.c

om

/new

s/are

-wea

rab

le-p

aym

en

ts-t

he-n

ext-

dis

rup

tion

-for-

ba

nk

s-3

01

81

23

-1.h

tml

htt

p://w

ww

.ib

tim

es.

co.u

k/p

ow

er-

suit

-wea

rab

le-t

ech

-th

at-

lets

-you

-ma

ke-i

nst

an

t-p

ayw

ave-

nfc

-con

tact

less

-pa

ym

en

ts-1

44

61

16

A smart suit that lets you pay for things

by flicking your wrist.

• Made from Australian merino wool, the Japanese brand

MJ Bale suit uses Visa's payWave system to connect

to Heritage Bank's mobile wallet.

• MJ Bale, working together with the Heritage bank, have

made 11 prototype Power Suits.

• Users can top up their mobile wallet with a balance from

their bank's debit or credit card up to $1,000 and use it

to pay for items up to $100.

Main features

« Power suit »: a smart suit to pay

Heritage Bank

https://www.youtube.com/watch?v=JEuY-FHflZw

htt

p://w

ww

.sm

h.c

om

.au

/na

tion

al/

mj-

ba

les-

pa

yw

ave-p

ow

er-

suit

-giv

es-

wea

rer-

a-c

ard

-up

-

their

-sle

eve-2

01

40

42

3-3

74

he.h

tml

Barclays

htt

p://w

ww

.th

egu

ard

ian

.com

/mon

ey/2

01

4/j

ul/

05

/con

tact

less

-pa

ym

en

ts-w

rist

ba

nd

-con

nect

s-

to-b

an

k-a

ccou

nt

htt

p://w

ww

.ba

rcla

yca

rd.c

om

/new

s/b

pa

y-b

an

d-l

au

nch

es.

htm

l

htt

p://w

ww

.ba

rcla

yca

rd.c

om

/how

-we-w

ork

/in

novati

on

s/b

pa

yb

an

d.h

tml

htt

p://w

ww

.da

ilym

ail

.co.u

k/s

cien

cete

ch/a

rtic

le-2

75

80

19

/Forg

et-

Ap

ply

-Pa

y-s

oon

-ll-

pa

yin

g-

WR

IST

BA

ND

S-B

arc

layca

rd-t

ria

ls-w

ea

rab

le-c

on

tact

less

-pa

ym

en

t-L

on

don

.htm

l

‘Just imagine a typical day in the near future. You leave the house, hop on the train

and head to the gym. After your workout, you grab a coffee and go to the office.

‘The money or information you need for every stage of that journey will be integrated

into a single device like bPay band”

Barclaycard

• 300 000 points of sales in the UK

• Pre loaded with money (Visa or Mastercard)

• Can be automatically topped up

• Can be used for purchases of up to 20 £ (32 €)

• Available for non Barclays customers

• Free service. No commission

Main features

Bpayband, a smart wristband to pay

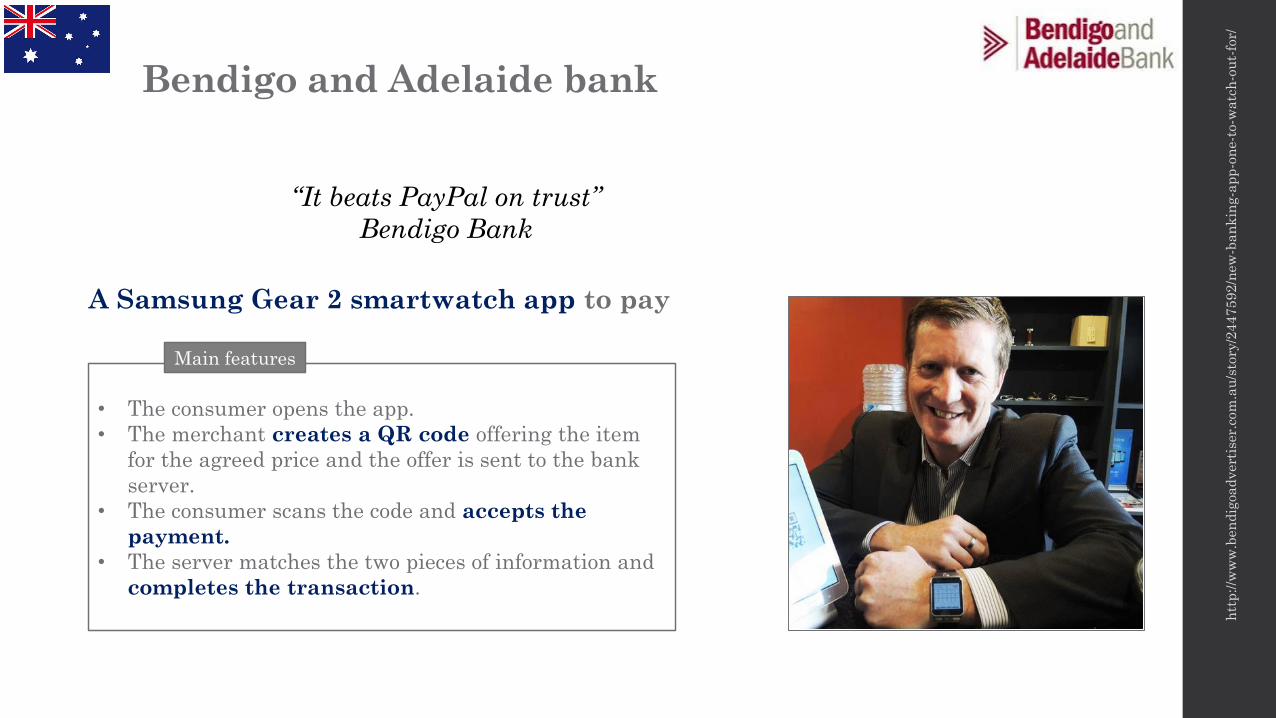

Bendigo and Adelaide bank

htt

p://w

ww

.ben

dig

oa

dvert

iser.

com

.au

/sto

ry/2

44

75

92

/new

-ba

nk

ing-a

pp

-on

e-t

o-w

atc

h-o

ut-

for/

“It beats PayPal on trust”

Bendigo Bank

• The consumer opens the app.

• The merchant creates a QR code offering the item

for the agreed price and the offer is sent to the bank

server.

• The consumer scans the code and accepts the

payment.

• The server matches the two pieces of information and

completes the transaction.

Main features

A Samsung Gear 2 smartwatch app to pay

Bendigo and Adelaide bank

http://www.youtube.com/watch?v=5NJKjf9eyYA

BKM

htt

p://w

ww

.mob

eyfo

rum

.org

/bk

m-e

xp

ress

-th

e-f

irst

-dig

ita

l-w

all

et-

to-s

tart

-pa

ym

en

ts-

wit

h-w

ea

rab

les/

htt

p://w

ww

.mob

eyfo

rum

.org

/bk

m-e

xp

ress

-th

e-f

irst

-dig

ita

l-w

all

et-

to-s

tart

-pa

ym

en

ts-

wit

h-w

ea

rab

les/

• Customers will be able to give simple voice commands

while wearing Google Glass to shop with BKM

Express, the digital wallet selected by 16 banks in

Turkey.

Main features

A Google Glass payment application

Barclays

htt

p://w

ww

.ma

rketi

ngm

aga

zin

e.c

o.u

k/a

rtic

le/1

32

67

38

/ba

rcla

yca

rd-b

oost

s-w

ea

rab

le-t

ech

-

invest

men

t-co

nta

ctle

ss-g

loves

htt

p://w

ww

.fin

extr

a.c

om

/New

s/fu

llst

ory

.asp

x?n

ew

site

mid

=2

68

27

“In a survey of 2,000, shoppers voted gloves as the most "desired" wearable payment

item. They were popular among shoppers who wanted an easier way to pay while laden

with shopping bags. Rings and bracelets came second and third”

Barclaycard

• Embedded with a contactless chip that can be used

to pay for transactions of up to £20

• 300 000 points of sale in the UK

Main features

Contactless glove to wave and pay

Banks and non Banks test also what other financial services

should be included with payments

Logbar

htt

p://w

ww

.da

ilym

ail

.co.u

k/s

cien

cete

ch/a

rtic

le-2

57

28

20

/Th

e-B

lueto

oth

-rin

g-t

urn

s-fi

nger-

MA

GIC

-WA

ND

.htm

l

One ring to open emails, switch on lights and pay bills, all using hand gestures

• Drawing an envelope shape in mid-air opens an

• Drawing a camera opens the camera app on a

connected phone

• Drawing a musical note will start playing songs

• Switch on / off lights

• Pay bills

• Make payments with the swipe of a finger

• Receive alerts and notifications, such as new

Facebook posts

Main features

Logbar

https://www.youtube.com/watch?v=f5rH5FYd37A

Artefact

Token: A Wallet on Your Wrist

htt

ps://w

ww

.aru

co.c

om

/20

14

/06

/tok

en

-bra

cele

t-p

aie

men

t/

• A wearable bracelet connected to select payment accounts –

from checking and savings, to credit cards, digital currencies, and

PayPal account.

• A security mechanism based on a unique biometric like a thumb

print or your heart bear, a PIN or password and the device itself

• It allows to receive personalized offers from a merchant

• It allows to lend money to a friend.

• It allows to see how a purchase will impact customer’s budget

right before he pays

Main features

Royal Bank of Canada

A smart wristband for biometrically authenticated payments

htt

p://w

ww

.bio

metr

icu

pd

ate

.com

/20

14

11

/bio

nym

-rb

c-m

ast

erc

ard

-test

ing-p

aym

en

ts-u

sin

g-b

iom

etr

ic-

wri

stb

an

d

htt

p://v

en

ture

bea

t.co

m/2

01

4/1

1/0

3/m

ast

erc

ard

-an

d-b

ion

ym

-wil

l-te

st-w

rist

-ba

sed

-mob

ile-p

aym

en

ts-

no-p

hon

e-r

eq

uir

ed

/

htt

p://w

ww

.beta

kit

.com

/bio

nym

-rb

c-a

nd

-ma

sterc

ard

-an

nou

nce

-worl

ds-

firs

t-b

iom

etr

ica

lly-

au

then

tica

ted

-wea

rab

le-p

aym

en

t-te

chn

olo

gy-t

ria

l/

“We’re continuing to work to provide customers

increased choice how they pay. Once their wristband is

activated, they can leave their phone at home and

securely buy a coffee with a tap of the wrist.”

Jeremy Bornstein, head of mobile payments RBC

• The smart wristband uses

the wearer’s unique

heartbeat to verify that he

or she is the real card

holder.

Main features

• RBC expects that this device

will be used as a unique

identification device that could

be a substitute for computer’s

password, car’s keys and also

a way to check in to hotels

room.

In progress

Payment option or not on your wrist ?

Only 12,2 % of smartphone owners cited making payments and tracking payment history as the primary way they

used or would be interested in using wearable devices.

Instead, wearables owners and potential users were most interested in tracking fitness and health.

Banks and non Banks shouldn’t bank on selling wearables based on their mobile payment options. Mobile payment options are

a nice-to-have wearables feature, not a must-have.

ss

(1): Source: Stratos (Dec 2014 )

American Express as an ideal combination ?

The Jawbone UP4: it does everything the UP3 does, and you can buy things with it.

htt

p://t

ech

cru

nch

.com

/20

15

/04

/15/j

aw

bon

es-

new

-20

0-u

p4

-dou

ble

s-a

s-a

n-a

meri

can

-exp

ress

-

card

/

• The UP4 can act as an AmEx card at hundreds of

thousands of NFC-enabled merchants in the US

• The idea: add an AmEx card to the UP4 through

Jawbone’s UP app. Then just tap the UP4 against an

NFC-enabled card reader, and Purchase is made!

• Fitness and health trackers: Bio impedance sensors,

heart rate, hydration levels, track sleep (“light sleep” vs

“deep sleep”) etc.

Main features

Extract from the survey:

Internet of Things:International Banking and Insurance wearable apps

- More than 150 slides- More than 70 initiatives analysed in more than 20 countries

- For more information, visit our website:http://www.saintgermainconsulting.com/en/etudes

Saint Germain Consulting

Yvon MOYSAN

Tél: 06 62 84 71 00

www.saintgermainconsulting.com

Questions and Answers ?

Internet of Things: international Banking and Insurance wearable apps

• Glasses, watches, wristbands, virtual reality headset, iBeacon or even wearable suits… Which bank or insurer have already launched a wearable app and why? What are the features of these apps dedicated to customers or employees? What are customers’ needs and expectations? What are customers’ fears? What are primary customers’ uses ? What are the app features that banks and insurers have already abandoned? What are the future app features or devices that banks and insurers expect to focus on? What are the Internet of Things key figures and projected trends?

• This study includes more than 150 slides and covers the major wearables app that banks and insurers have developed so far. More than 70 of them are indeed analyzed. The objectives of the bank or the insurer are presented and illustrated by CEO or Digital Marketing Director verbatim, the main current and future features of the app and first customers’ feedbacks are detailed. In addition, the study includes several relevant links to press articles and videos illustrating the bank or insurer wearable app.

Sa

int

Germ

ain

Con

su

ltin

g : 3

7 r

ue S

ain

t A

nd

ré d

es

Art

s 7

50

06

Pa

ris

Tél

: 0

6 6

2 8

4 7

1 0

0 –

Em

ail

: y

von

.moysa

n@

sain

tgerm

ain

con

sult

ing.c

om

For more information regarding this study, please send an e- mail to [email protected]

PURCHASE ORDERPlease send it by e-mail to [email protected] or by mail to

Saint Germain Consulting Yvon MOYSAN 37, Rue Saint André des Arts 75006 Paris France

Internet of Things: international Banking and Insurance wearable apps. January 2015. (PDF version)

790 €

Option for shipping in PowerPoint format 120 €

Name:…………………………………………………… First name:……………………………………....

Company:………………………………………………………………………………………………………...

Job title:………………………………………………………………………………………………………….

Address:…..……………………………………………………………………………………………………..

ZIP Code:……………………………………….............. City:…………………………………...................

Country:………………………………………………………………………………………………………….

Phone number:.……………………………………….... Mobile:.……………………………….................

e-mail:….……………………………………..............................................................................................

Date:.………………………………………………………… Signature:.…………………………...............

The study will be sent by e-mail after the reception of the payment by transfer to this checking account number:

Code banque 30003 Code guichet 03082 N° Compte 00050786145 Clé RIB 35

IBAN : FR76 3000 3030 8200 0507 8614 535 BIC-ADRESSE SWIFT : SOGEFRPP

Number Total

Sa

int

Germ

ain

Con

su

ltin

g : 3

7 r

ue S

ain

t A

nd

ré d

es

Art

s 7

50

06

Pa

ris

Tél

: 0

6 6

2 8

4 7

1 0

0 –

Em

ail

: y

von

.moysa

n@

sain

tgerm

ain

con

sult

ing.c

om