DO YOU KNOW WHEN A LEASE STARTS?

www.LeaseQuery.com

FOR ACCOUNTING PURPOSE, WHAT IS THE CORRECT DATE A LEASE STARTS?

A)Lease start date B)Move in dateC)Possession date D)Commencement dateE)Execution date

WHEN DOES A LEASE START?

For accounting purposes, a lease “starts” on the date possession is passed from the landlord to the tenant

On that date, the lessee or tenant should start recording straight-line expense, even if that date is earlier than the “commencement date” specified on the lease

EVERY LEASE HAS A “START” DATE, BUT MOST PEOPLE DO NOT UNDERSTAND WHAT THAT DATE

REALLY IS.

“COMMENCEMENT DATE” Specified on the lease document

has ABSOLUTELY no bearing whatsoever on the lease start date under current (and the new) lease

accounting rules.

WHAT IS A COMMENCE-MENT DATE?

For accounting purposes, the commencement date specified on the lease may be used to determine the lease end date, as most of the time the “lease term” specified on the lease document startson the commencement date.

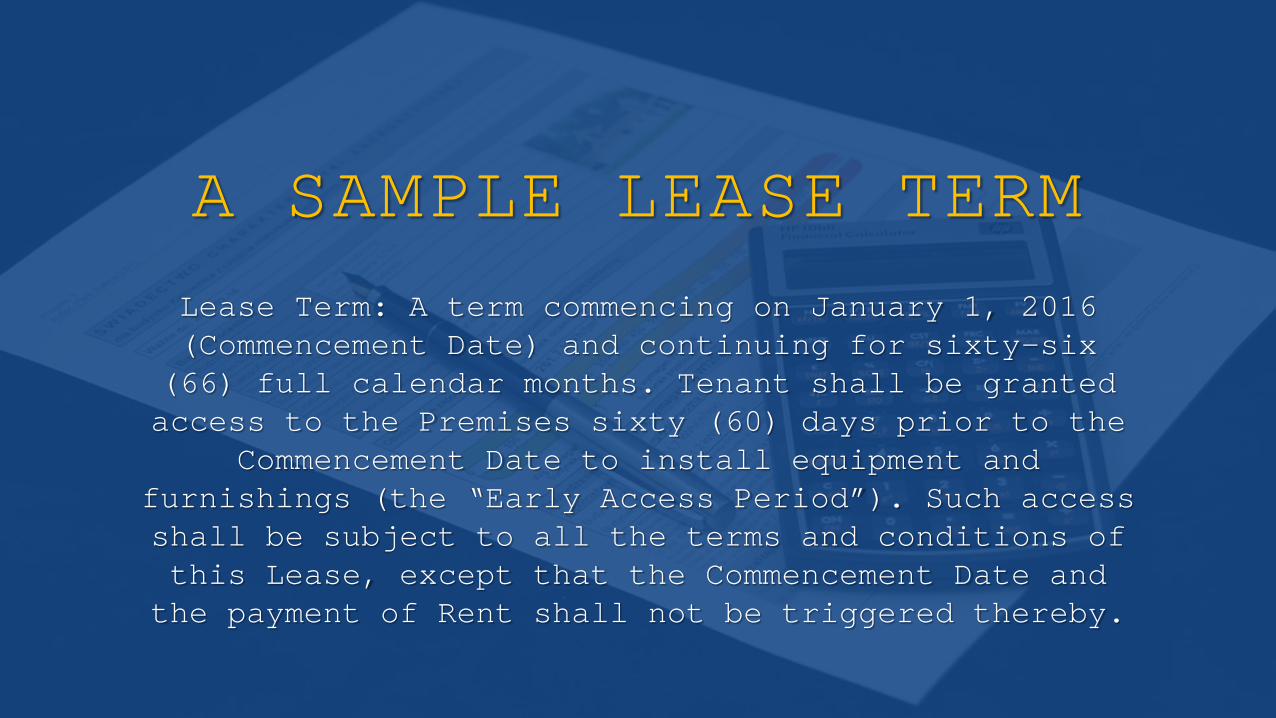

A SAMPLE LEASE TERMLease Term: A term commencing on January 1, 2016 (Commencement Date) and continuing for sixty-six (66) full calendar months. Tenant shall be granted access to the Premises sixty (60) days prior to the

Commencement Date to install equipment and furnishings (the “Early Access Period”). Such access shall be subject to all the terms and conditions of this Lease, except that the Commencement Date and

the payment of Rent shall not be triggered thereby.

Based on the language in the previous page, for accounting

purposes, the lease start date is actually November 1, 2015 (or

whenever access is granted), and the lease term is actually 68 months. The tenant would record expense in the months of November and December (the offset is to deferred rent), even though the lease explicitly asserts that the commencement date

is January 1, 2015.

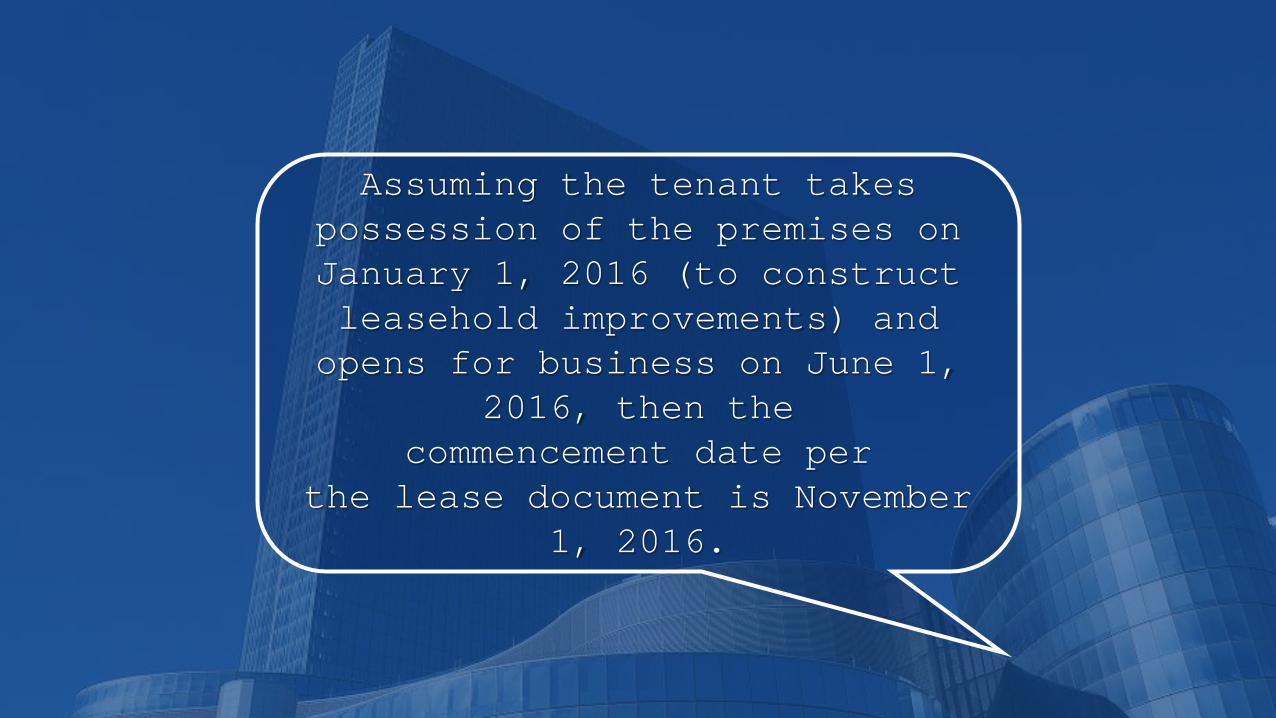

HERE’S ANOTHER EXAMPLE:The Lease Term shall be for a period of one hundred twenty (120) months commencing one hundred fifty (150) days after the date upon which Tenant Opens for business at the Demised Premises (the “Commencement Date”).

Assuming the tenant takes possession of the premises on January 1, 2016 (to construct leasehold improvements) and opens for business on June 1,

2016, then the commencement date per

the lease document is November 1, 2016.

However, for accounting purposes, the lease start date is actually January 1, 2016

(the possession date), and the tenant would have to record expense for January through October 2016, even though the

lease asserts that the commencement date is November

1, 2016

In addition, the accounting lease term is actually 130 months, as opposed to 120

months as stated in the lease.

SO THERE YOU HAVE IT; THE DIFFERENCE BETWEEN

COMMENCEMENT DATES AS STATED IN THE LEASE, AND THE COMMENCEMENT DATE FOR ACCOUNTING PURPOSES.

AS YOU ARE MAKING DECISIONS ABOUT YOUR LEASE ACCOUNTING SOFTWARE, BE SURE TO ASK IF THE SOFTWARE TRACKS BOTH THE COMMENCEMENT AND POSSESSION

DATES.

MAKE SURE THE SOFTWARE AMORTIZES RENT EXPENSE FROM THE POSSESSION DATE AND NOT

THE COMMENCEMENT DATE

LEASEQUERYDOES THIS

EFFORTLESSLY!

EASY TO USE LEASE ACCOUNTING SOFTWARE

LEASEQUERY HELPS BUSINESSES MANAGE THEIR LEASES AND AVOID

OVERPAYING RENT.

REQUEST FOR FREE TRIAL >>

IDEAL FOR OVER 30 LEASED ASSETS - BUILDINGS, EQUIPMENT OR BOTH.

REQUEST FOR FREE TRIAL >>

BENEFITS OF LEASEQUERY

Determine impact of new lease accounting rules on the lease portfolio

Instantly generate error-free lease journal entries for posting

24/7 access to lease documents and information from any location

Effectively manage and minimize financial risk associated with lease portfolios

Perform lease versus buy analyses when evaluating equipment or real estate purchases

For more information on lease, please visitwww.LeaseQuery.com