Value Investing PrinciplesMcDonough School of Business

Economics of Strategic BehaviorProfessor Arthur Dong

Value Investing

• Founding Fathers of Value Investing were professors Benjamin Graham and David Dodd of the Columbia Business School

• The Bibles– The Intelligent Investor– Securities Analysis

• The disciples are– Warren Buffett– Mario Gabelli– Walter Schloss

Value Investing

Value Investing

• Involves the application of strategic analysis to finance

• Rely on what is knowable not on the unknown

• It’s all about picking your races and picking your horses

Value Investing Process

SearchCheap Ugly

ObscureIgnored

ValuationAssets

Earnings Power ValueFranchise

ReviewKey Issues

Collateral EvidencePersonal Biases

Risk ManagementMargin of Safety

Some DiversificationPatience – Default Strategy

Value Investing

In the investment business everyone thinks they have an edge…

It is well established that the cheap / ugly / obscureactually outperform the market over long periods oftime……Warren Buffett

Low Market to Book Value = OutperformanceSmall and cheap stocks outperform

Avoid the expensive: want to buy boring and cheap

Systemic Biases

• Institutional Biases– Herd Mentality – to minimize deviations– Window dressing money managers– The constant hunt for blockbusters – Next Big Thing

• Individual Biases– Loss Aversion– Hindsight Bias– Lottery ticket mentality– Buying the dream and getting rich quick– People shy away from the ugly to a high degree– People have more confidence in their judgment than justified– Hindsight not adjusted very much– People have an exaggerated sense of good news

Behavioral Finance

• On the institution side, fund managers have a tendency to mimic and copy one another

• The astute investor can take advantage of institutional and individual biases and tendencies to their own benefit

• To be a good investor, you have to be good at estimating value

Traditional Approaches

• Traditional MBA Corporate Finance and DCF Model

• Estimate cash flows over five years or more (expected cash flows)• Estimate the cost of capital for the firm• Adopt a terminal growth rate • Estimate terminal cost of capital• Add it all back to derive value

• Problem: This method is highly loaded toward the terminal value

Traditional Approach

• Big Assumption – If you knew for sure the cash flows and the cost of capital into the distant future, then the DCF model will work

• But if you don’t know….then this may not be the wisest approach

DCF Limitations

• DCF takes good information and combines it with bad information to predict the future

• Add it all together and you get bad information

(+) + (-) = (-)

DCF Limitations

With the multiples or DCF method you aremaking big assumptions about the future. Plugin your numbers, turn the crank and spit out a

value for the company.

The assumptions are almost alwaysarbitrary

Differing Approaches

Traditional Approach Strategic ApproachQuestions: Questions:Profit Rate 6% Is the industry economically viable?Economically viable? Are there any competitive advantages?Cost of Capital 10% Is there “free” entry?Investment / Sales 60% Does the Firm enjoy a “sustainable”

competitive advantage?Profit Rate 9% If the competitive advantage is stable the

firm grows with the industryGrowth Rate 7%

The World According to Warren Buffett

• Know what you know, rely on your circle of competence

• Start off with the most reliable information and work toward the least reliable making adjustments along the way

• Organize value components by underlying strategic assumptions from no competitive advantage to growing competitive advantage

The Scriptures According to Benjamin Graham

• Starts with information that is normally discarded, the balance sheet

• Balance Sheet – closely evaluate the tangible assets (things you can touch and see)

• Ask yourself – is the industry viable?• If it is not viable, then value the assets at liquidation value• If the industry is viable, then value the assets at the

reproduction cost (how much to enter the business today?)• If you have inventory, what would it cost to reproduce it today?• If you have a factory, what would it cost to reproduce it today?

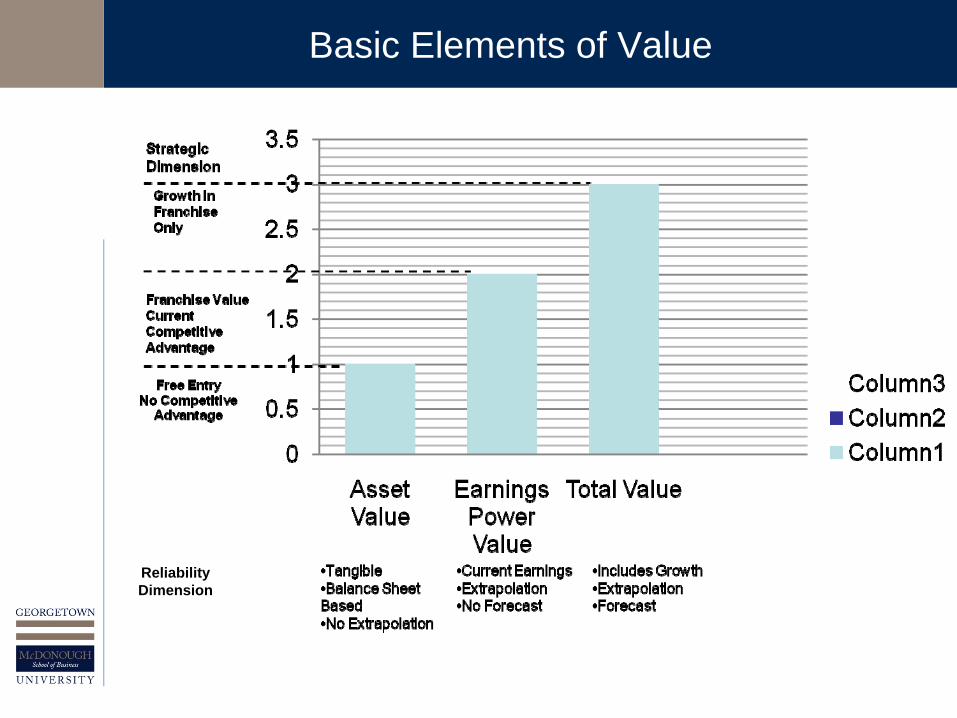

Basic Elements of Value

Reliability Dimension

Valuing the Earnings

• Next most important value component, EPV or Earnings Power Value

• EPV will reveal the average distributable earnings of the firm…this can be calculated

Graham, Dodd, Buffett

• Two key determinants of value

1.Asset Value2.Earnings Power Value

On Valuing Growth

• The third component of value is growth

• For many companies, the high market price / valuations are related to future growth

• In general, value investors will not pay for growth…profitable growth is uncertain

• If growth is forecasted, there better be a moat built around that growth to protect it from potential entrants

Determining Asset Value

Asset ValueCash BookA/R Book + adjustment for uncollectiblesInventories Book + LIFO adjustmentPP&E Original Cost plus adjustment to renewProduct Portfolio Years R&D expenseCustomer Relationships Years SG&AOrganizationLicense & Franchises Present market valuesSubsidiaries Private market value

Deriving Asset Value

• Once you have completed valuing the assets, make sure you have correctly included the intangible assets as well (customer relationships, new product development, brand recognition)

• Add up the assets and subtract liabilities to come up with net asset value

Earnings Power Value

EPV = Earnings x 1 / Cost of Capital

• Start with operating earnings (EBIT)• Take earnings and subtract one time charges• Multiply average margins by sustainable revenues to derive

normalized EBIT• Multiply by the average tax rate• Add-back depreciation

This will yield normalized earnings

EPV

• EPV Business Operations = earnings power x 1 / WACC

• EPV Company = EPV Business Operations + excess net assets (cash, real estate – legacy costs)

EPV and the Value of Assets

Valuation What it meansAsset Value > EPV Value is lost due to poor management and

or industry decline. Look at the proxy statement to change management.

Asset Value = EPV Indicates company is playing on a level playing field. Free entry without substantial barriers allow entrants.

Asset Value < EPV Consequence of competitive advantage and or superior management. Powerful, sustainable competitive advantage in place. Coke has 10bb in assets, 60bb in EPV… there is a 60bb moat built around its franchise

Value of Growth

When looking at Growth…Proceed with extreme caution

• This is the least reliable value indicator and it is highly sensitive to assumptions

• Ask: does the growth have any value at all?• In practice, growth requires additional investment• The more investment, the less distributable cash flow

• The key when evaluating growth is the existence of barriers to entry and competitive advantage

Growth with no barriers = No Value to Growth

Growth Dilemma

• Crappy management is on a mission to grow – growth will kill you because it wastes valuable resources

• Competitive markets: no barriers, investment will lead to break even

• Growth has value if there are competitive barriers in place

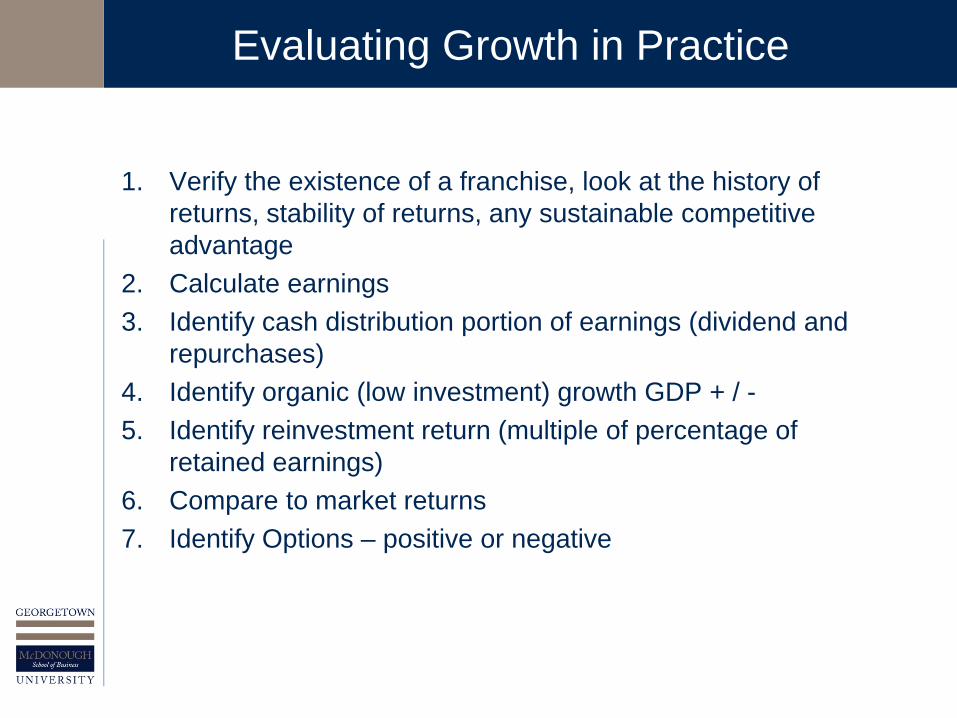

Evaluating Growth in Practice

1. Verify the existence of a franchise, look at the history of returns, stability of returns, any sustainable competitive advantage

2. Calculate earnings3. Identify cash distribution portion of earnings (dividend and

repurchases)4. Identify organic (low investment) growth GDP + / -5. Identify reinvestment return (multiple of percentage of

retained earnings)6. Compare to market returns 7. Identify Options – positive or negative