Usiminas Presentation

2Q12

Clique para

editar o texto

mestre

Usiminas and its

Business Units

Financial

Highlights

Market

Overview

2

Agenda

Total 1,527 million tons

3 Source: World Steel

683.3

107.6 86.2 72.2 68.7 68.5 44.3 35.3 35.2 34.1

China Japan USA India Russia South Korea

Germany Ukraine Brazil Turkey

Production per Company – 2011

97.2 44.4 43.3

39.1 37.7

33.4 31.9 30.0 29.9 29.8

9.5

6.8

Arcelor Mittal

Hebei Group

Baosteel

Posco

Wuhan Group

Nippon Steel

Shagang Group

Shougang Group

JFE

Ansteel Group

36º - Techint Group

51º - Usiminas

World Production - 2011

Capacity of Crude Steel

1,988 million tons

Excess of Capacity

461 million tons

Production

1,527 million tons

Production of Crude Steel

1,527 million tons

Excess of production

149 million tons

Consumption

1,378 million tons

World - 2011

4

World Production and capacity of crude steel

78

61 68

76 83

61 57 72

35 28 29

15

21 14

12 9

17 21

18

26 41 39

7 18 18 13 9

22 22 10

39 31 32

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Steel Iron Ore Coal

5 Source: Mckinsey

Profit distribution on the steel production chain – %

Value Transfer on the Steel Chain

Production – million tons

6 Source: IABR / INDA

Inventories in the Distribution Network Flat Steel Imports – thousand tons

Apparent Consumption – million tons

3.5 3.7 3.84.1 4.0

3.7 3.8 3.73.3 3.2

3.8 3.9

3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

2.72.9

3.43.9

3.33.1 3.1 3.3 3.2 3.0

3.5 3.5

3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

0.8 0.8 0.81.0

1.2 1.2 1.2 1.21.1 1.0 1.0 1.0

2.4 2.6 2.4

3.2

3.9 4.1

3.23.6

3.0 2.9 2.8 2.8

3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

Thousand tons Monthly basis

315 283

667

790 823 865

416 415

570500 520

413

3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

Flat Steel

Brazilian Market

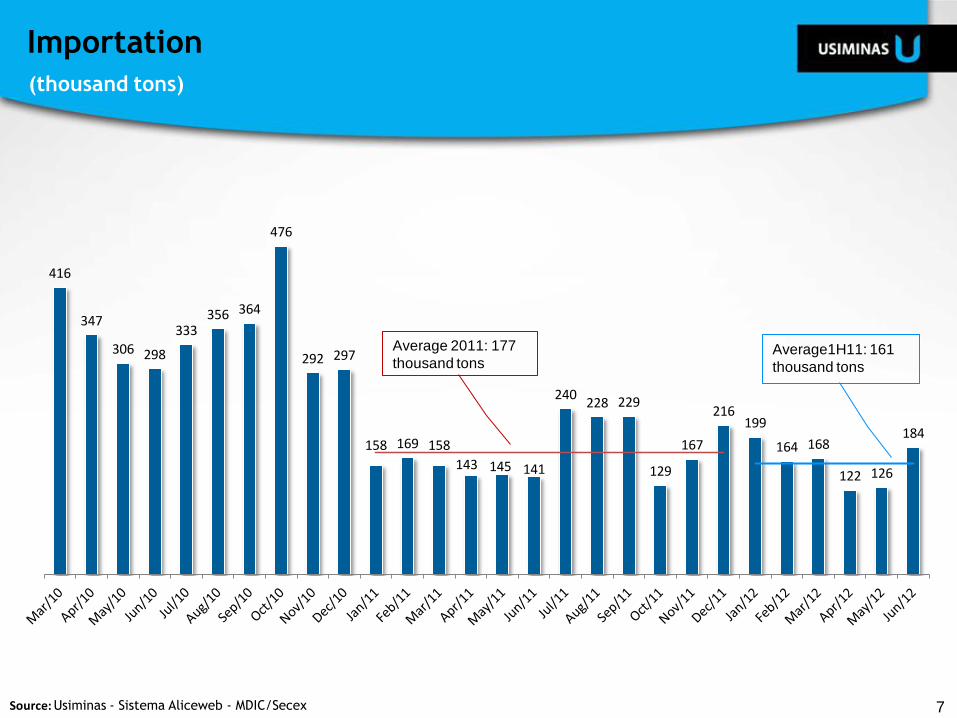

416

347

306 298

333 356 364

476

292 297

158 169 158

143 145 141

240 228 229

129

167

216 199

164 168

122 126

184

Source: Usiminas - Sistema Aliceweb - MDIC/Secex

Average 2011: 177

thousand tons Average1H11: 161

thousand tons

7

(thousand tons)

Importation

2,822 3,051 3,075

3,382 3,406 3,455 3,591

2007 2008 2009 2010 2011 2012p 2013p

Brazilian Production of vehicles

+8% +1% +10% +1% +1%

+4%

2,186 2,445

2,652 2,855 2,775 2,897 3,024

2007 2008 2009 2010 2011 2012p 2013p

Nacional Sales

+12% +9% +8% 4% 4%

277 375

489

660

858 945

1,040

2007 2008 2009 2010 2011 2012p 2013p

Export Sales

+35% +30% +35%

+30% +10%

+10% -3%

Source: 2007 a 2011 – Anfavea; 2012 e 2013: Projeções Usiminas – Planejamento Comercial, março 2012 8

Brazil’s Production and Sale of vehicles

Investments in industry in 2012: R$17.1 billion

Investments in infrastructure in 2012: R$105.3 billion

Investments in housing during the period of 2011/2014 : R$279 billion

9

MEDIUM AND LONG TERM PROJECTS

2012-2016

~ US$ 237 Bi

2012

~ R$ 761 millions

2012

~ R$ 230 millions

Source: Valor Economico, PAC’s website, Petrobras’s website,Portal da Copa – Governo Federal

2012

~ R$ 25,6 Bi

2012

~ R$ 11.1 Bi

4.5 million tons of steel

2.7 long

1.8 flat

1.5 million tons of steel

0.9 long

0.6 flat

Benefit from the Brazilian positive outlook

Domestic Market

10

Clique para

editar o texto

mestre

Usiminas and its

Business Units

Financial

Highlights

Market

Overview

Agenda

Foundation

of Usiminas

Operation

Start Up

Privatization

Usiminas:1991

Cosipa: 1993

Listing on

Latibex

Aquisition of J.

Mendes iron ore

mines

Aquisition of

Zamprogna

Soluções

Usiminas,

con-solidation

of the

companies Rio

Negro, Dufer,

Fasal and

Zamprogna

and industrial

units Usial and

Usicort

Single CNPJ:

Cosipa is

incorporated

by Usiminas

Creation of Mineração Usiminas

Port Agreement

Mineração Usiminas and

MMX

Selling of

Ternium shares

Joint Mining

and

Cooperation

Agreement

with MMX, MBL

and Ferrous

Negociation

with J. Mendes

concluded

Acquisition of

Litigation Area

1956

1991

2005

2008

2009

2010

2011

2012

Entrance of Ternium/ Tenaris

in Usiminas’ Control Group

New shareholders

agreement singned among Niippon Group,

Ternium / Tenaris and Usiminas Pension Fund

until 2031

11

Time Line

12

Mining

Steel

Steel processing

Capital Goods

Strategically Located

13

Auto Industries

Cold Rolled and

Galvanized (EG and HDG)

Ship-Building

Heavy Plates

Pipelines

Heavy Plates and Hot

Rolled

Pressure Vessels

Heavy Plates

Agricultural

Machines

Heavy Plates and Hot

Rolled

Civil Construction

Heavy Plates, Cold and Hot

Rolled and Galvanized (EG

and HDG)

Autoparts

Hot Rolled

Household

Appliances

Cold Rolled and

Galvanized (EG and

HDG)

Everyday Steel Application

14

Voting Capital – ON

Control Group:

63.86% of Voting

Capital

Total Capital 1,013,786,190

49.84% 50.16%

ON PN

PN 508,525,506 ON 505,260,684

10 Board of Directors Members:

- Controling Shareholders: Ternium / Tenaris (3), Nippon Group (3), Usiminas Pension Fund (1) and

Employees Representative (1)

- Minority Shareholders : Previ (1) and Geração Futuro Funds (1)

Nippon Group29.45%

Ternium / Tenaris

27.66%

Usiminas Pension Fund

6.75%

Free Float36.14%

Shareholder Composition

15

Mining

Steel

Steel Processing Capital Goods

UPST

REA

M

DO

WN

ST

REA

M

* Controled by Usiminas ** Results accounted through equity income

Ipatinga

Automotiva Usiminas *

Metform and Codeme

stake **

Cubatão

Unigal Usiminas * Mineração Usiminas *

Soluções Usiminas * Usiminas Mecânica *

Complete solution of products and services

through the value chain

Total amount for 2012

R$ 2.0 billion

Strategic focus on enhancing competitiveness of current operations

Ongoing Projects

Galvanizing

Line

550,000 tons

(Unigal)

Hot Strip Mill

2.3 million tons

(Usiminas

Cubatão)

Mining

Production

Reach total

capacity of

12 million

tons in 2013.

In operation

2Q11

Foundry

24,000 tons

(Usiminas

Mecânica)

4Q11 1Q12 Energy self

sufficiency

Reach total

capacity of

around 500MW

Hot Run

16

Pickling line

III (Cubatão)

Revamping of

Coke Plant II

(Ipatinga)

Investments

17

Income Statement per Business Units - Non Audited (R$ million)

Note: All transactions among the business units are made at market price. MRS results are accounted through equity on Equity

Income.

R$ million

2Q12 1Q12 2Q12 1Q12 2Q12 1Q12 2Q12 1Q12 2Q12 1Q12 2Q12 1Q12

Net Revenue 213 239 3,097 2,573 533 497 205 251 (821) (674) 3,225 2,886

Domestic Market 143 217 2,348 2,234 522 491 203 251 (811) (654) 2,405 2,539

Export Market 70 22 749 339 11 6 2 0 (10) (20) 820 347

COGS (73) (100) (3,057) (2,574) (495) (447) (225) (258) 783 666 (3,067) (2,713)

Gross Profit 140 139 39 0 37 49 (19) (7) (39) (8) 158 173

Operating Income (Expenses) (49) (36) (43) (100) (50) (51) (17) (23) 0 1 (159) (209)

EBIT 91 103 (4) (100) (13) (2) (36) (30) (39) (7) (1) (36)

EBITDA 100 111 201 100 0 11 (29) (25) (40) (7) 232 190

EBITDA Margin 47% 46% 6% 4% 0% 2% -14% -10% - - 7% 7%

Mining SteelSteel

Processing

Capital

GoodsAdjustment Consolidated

(quarter)

Results Accounted by Business Unit

18

Income Statement per Business Units - Non Audited (R$ million)

Note: All transactions among the business units are made at market price. MRS results are accounted through equity on Equity

Income.

R$ million

1H12 1H11 1H12 1H11 1H12 1H11 1H12 1H11 1H12 1H11 1H12 1H11

Net Revenue 452 479 5,670 5,485 1,029 1,102 456 681 1,497 (1,658) 6,111 6,089

Domestic Market 361 390 4,582 4,701 1,012 1,079 454 651 (1,465) (1,657) 4,944 5,194

Export Market 91 89 1,088 784 17 23 2 0 (30) 0 1,168 896

COGS (173) (123) (5,631) (5,312) (943) (993) (483) (604) 1,450 1,662 (5,780) (5,370)

Gross Profit 279 357 39 173 87 109 (27) 77 (46) 3 332 719

Operating Income (Expenses) (85) (52) (143) (131) (101) (105) (40) (51) 1 3 (368) (336)

EBIT 195 305 (104) 42 (15) 4 (66) 26 (47) 6 (37) 383

EBITDA 211 319 301 306 11 35 (54) (39) (47) 3 422 702

EBITDA Margin 47% 67% 5% 6% 1% 3% -12% 6% - - 7% 12%

Mining SteelSteel

Processing

Capital

GoodsAdjustment Consolidated

(semester)

Results Accounted by Business Unit

Cubatão

Ipatinga

19 19

Steel

Installed Nominal Capacity : 9.5 million tons / year

Slabs Hot Coils Cold Coils Heavy Plates Slab Caster EG HDG

1,950,000tons

Optmized

Rolling

Capacity

2,000,000tons 1,900,000tons 1,020,000tons 350,000tons

Cubatão Plant - 1,200,000tons - 4,400,000tons* 1,000,000tons 4,500,000tons

3,700,000tons Nominal

Capacity 8,000,000tons 2,000,000tons 9,500,000tons 1,050,000tons 360,000tons

-

Ipatinga Plant 1,050,000tons 360,000tons 2,500,000tons 3,600,000tons 1,000,000tons 5,000,000tons

20

Galvanized

* HCR mill # 2 under ramp up.

Usiminas has a full range of flat steel products

Flat Steel Production

21

Sales – thousand tons

Segments Breakdown of

Sales – 2Q12

1,406 1,512

1,888

1,583

1,340

1,343 1,162 1,136

1,246 1,327

240

243 204

266

561

2Q11 3Q11 4Q11 1Q12 2Q12

Mercado Interno Mercado Externo

18%14%

4%

8%

7%

6%

26%

7%

9%

Auto Parts

Auto industries

Rolled Machinery

Small Diameter Tubes

Civil Construction/Shapes

Household Appliances

Distribuitors

Industrial Equipment

Other

Usiminas is focused on the domestic market with a product range to supply different

sectors

Domestic Market

22

US$/ton

R$ /ton

101 119

227

291236

299

420

111158

47 37 52

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 1Q12 2Q12

294 367

664 709

513 581

771

221 277

78 66 107

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 1Q12 2Q12

US$ /R$ 1.6737 1.7683 2.0455

Ebitda (millions) / ton

23

1,690

1,660

1,763

1,821

1,702

1,619

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

COGS (R$ millions) / ton

24

Belo Horizonte Itabira

IPATINGA

São

Paulo

ITAÚNA

Vitória

TUBARÃO

Port

ITAGUAÍ Port

CUBATÃO

Port

24

Mining and Logistics

25

Tubarão Port Itaguaí Port

(Ingá)

MODAL

Mineração

Usiminas

EFVM

Existing Routes

CUBATÃO Plant / Port

New Routes

TCS / TSA

Trammel

Sepetiba Port

Exports Exports Exports

40 Km

60 Km

IPATINGA Mill

Logistics

4 mining sites, acquired from J. Mendes Group in

Feb/2008

Reserves of 2.6 billion tons

Located in Serra Azul-MG, one of the richest iron

ore sites in Brazil

2Q12: production of 1.5 million tons

MRS: 20% of voting shares and part of the

Control Group

Land in Itaguaí-RJ, acquired in 2008

Production – MM ton:

3.8

5.5 6.8 6.3

3.4

2008 2009 2010 2011 1H12

26

Mining and Logistics

Current status

US$ 6.4 billion Mineração Usiminas S.A Estimated Market Value

Acquisition by Sumitomo Corporation of

30% of Mineração Usiminas S.A., through

the subscription of new shares, up to the

total amount of US$ 1.9 billion.

70.0%

30.0%

27

Mining and Logistics

Strategic partnership

28

Iron Ore Production Capacity – million tons by the end of the year

2 2 2 2 2

5 6 6 4 4

2 6

23

7 8 10

12

29

2010 2011 2012 2013

Friable Project : ongoing

Estimated Capex of R$800 million Compact Project:

under detailing phase

Expansion Plan

Mining

29

MMX Port and Joint Mining Agreements

MBL Joint Mining Agreement

New mine acquired from Mineração Ouro Negro (former

litigation area)

Conclusion of the negotiation with J. Mendes

Right of way agreement with Ferrous

Agreements

Mining

30

MBL

Arcelor Mittal

Ferrous (Santanense)

Comisa Emicon

MMX

Ferrous

MUSA Pau de Vinho

MUSA East

Minerita

MUSA Central

MUSA West

Itatiaiuçu

Igarapé São Joaquim De Bicas

Mineração Usiminas mining operation is highlighted in yellow.

Mineração Usiminas

Serra Azul

31 31

Itaguaí Port

32

Camaçari

Cachoeirinha

Porto Alegre

Campo Limpo Paulista

São Paulo Guarulhos

Taubaté

Recife

Serra

Betim

Santa Luzia

Soluções Usiminas

Steel Processing

33

11 industrial units in MG, SP, RS, ES and PE.

Processing capacity of 2 million tons/year.

2Q12 Net Revenues of R$443 million

Leadership:

Is the leader in the steel distribution

sector since 2010, according to INDA.

Soluções Usiminas

Steel Processing

Automotiva Usiminas

34

Clients 500

km

1.000

km

1.500

km

Pouso Alegre Unit

Steel Processing

35

Pouso Alegre – MG

– Close to major auto makers.

– Full service company.

2Q12 Net Revenues of R$73 million

Major Clients:

Ford, Mercedes Benz, Fiat, Volkswagen,

Volvo, General Motors, International Trucks,

Honda Toyota, PSA Peugeot Citroën, Scania.

35

Automotiva Usiminas

Steel Processing

36

Capital Goods

Ipatinga – MG

It is one of the largest capital goods’ company in the

country.

2Q12 Net Revenues of R$205 million

Market Sectors:

– Industrial Assembly

– Structures / Metal Bridges and Blanks

– Industrial Equipment

– Industrial Erection

– Foundry and Railcars

Highlights:

– Supply of 30 thousand tons of blanks for wind towers of

Gestamp Wind Steel.

37

Usiminas Mecânica

Capital Goods

38

Ship Panel

3rd Bridge in Brasília

Ship Blocks Plant Design

Usiminas Mecânica

Capital Goods – some of its projects

Clique para

editar o texto

mestre

Usiminas and its

Business Units

Financial

Highlights

Market

Overview

39

Agenda

40

EBITDA – R$ Million

Sales – thousand tons (steel products)

Net Revenues – R$ Million

Crude Steel Production – thousand tons

1,583 1,512

1,888

2Q11 1Q12 2Q12

365

190 232

2Q11 1Q12 2Q12

3,026

2,886

3,225

2Q11 1Q12 2Q12

1,858

1,672

1,845

2Q11 1Q12 2Q12

2Q12 Consolidated Results

Highlights

41

954 1,344

1,547

2,429

3,072

5,624 5,525

4,368

5,003

6,008

1,485

2,650

1,264

422

40%

34%

32%

37% 35%

46% 42%

35% 36%

38%

14%

20%

11%

7%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 1H12

Ebitda (R$) Ebitda Margin

Ebitda / Ebitda Margin

(annualy)

42 *IFRS

337 365

343

218

190

232

11% 12%

12%

8%

7% 7%

0%

2%

4%

6%

8%

10%

12%

14%

100

150

200

250

300

350

400

450

500

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

EBITDA Ebitda Margin

Ebitda / Ebitda Margin

(quarterly)

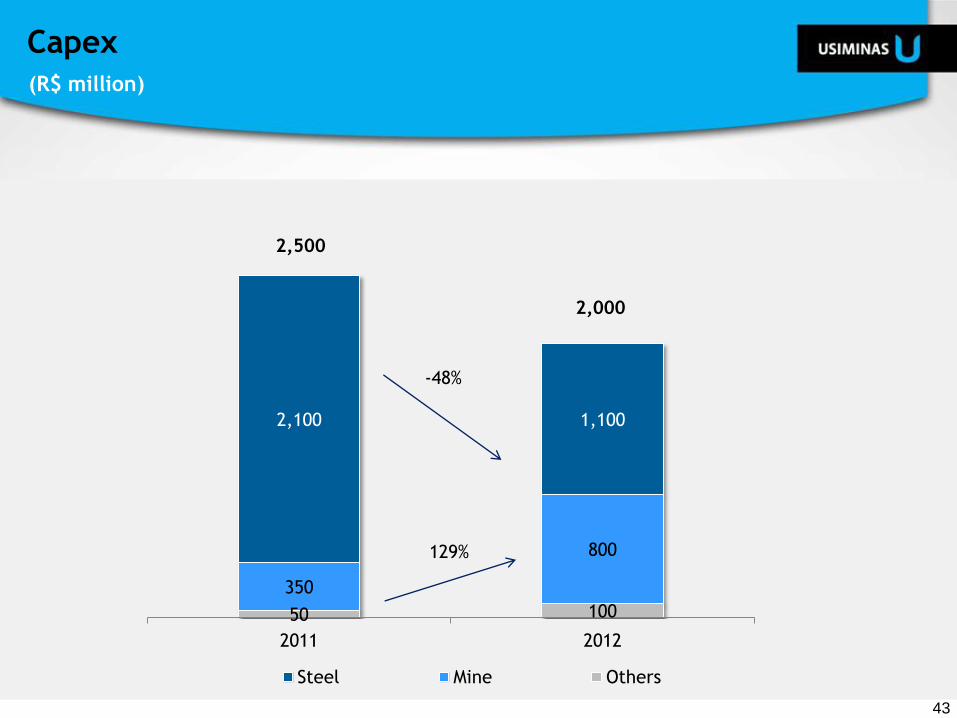

50 100

350

800

2,100 1,100

2011 2012

Steel Mine Others

2,500

2,000

129%

-48%

43

Capex

(R$ million)

44

2,501

288

864 922 905 735 416 302 33 155

2,343

227

1,048 628 486 723

267

1,023

2 2

Cash 2012 2013 2014 2015 2016 2017 2018 2019 2020 on

Local Currency Foreign Currency

515

4,844

1,912

1,550 1,458

683

1,325

157 35

1,391

Duration: R$: 40 months US$: 44 months

Debt Profile

(R$ million)

45

4.3 3.8

3.1 2.9

3.3

4.1

4.9

3.6

2.3 2.8

3.4

3.9 3.9 4.2

0.8 1.0 1.3 1.9 1.7 1.5 1.6 1.4

1.0 1.6

2.5 3.1

3.6 4.2

1Q09 2Q09 3Q08 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

Net Debt (R$ bi) Net Debt/EBITDA (x)

Leverage – Consolidated Basis

5.31

5.16

4.97

4.73

4.27

3.79

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

-9,7%

-11,2%

-20% = -R$938 Mi

46

Working Capital - Consolidated

(R$ billion)

128 111 113

115

79 97

242

189

210

Quarter Average 2011 1Q12 2Q12

General and Administrative Selling Total SG&A

47

SG&A - Consolidated

(R$ million)

48

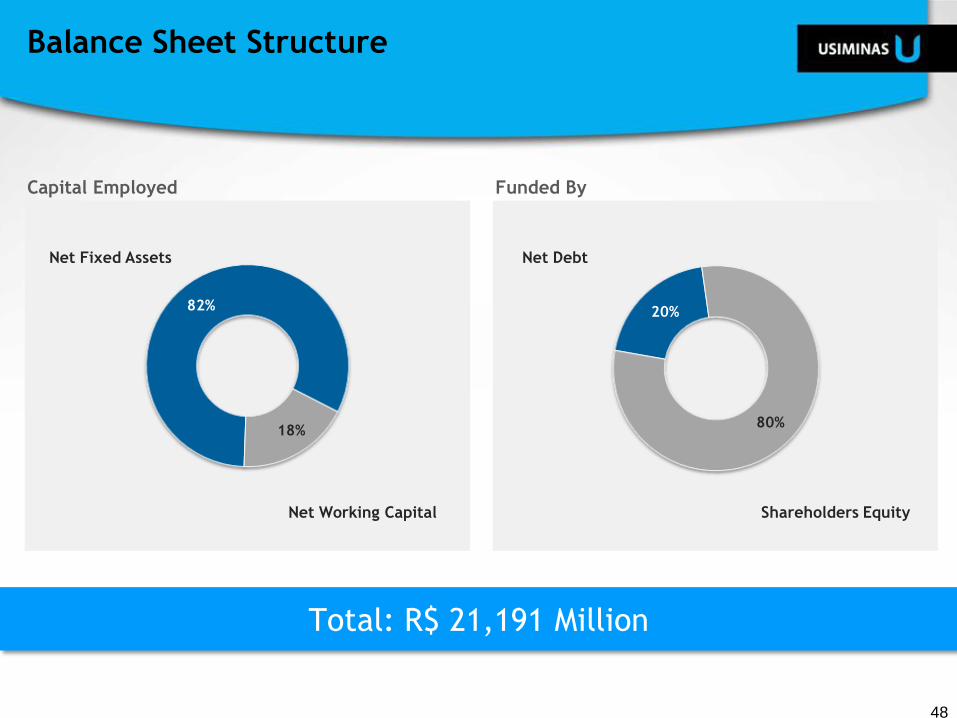

Capital Employed Funded By

Total: R$ 21,191 Million

82%

18%

20%

80%

Net Working Capital

Net Fixed Assets

Shareholders Equity

Net Debt

Balance Sheet Structure

Cristina Morgan C. Drumond Head of IR

[email protected] Phone: 55-31-3499.8772

Fax: 55-31-3499.9357

www.usiminas.com/ri

ADR

Level I

Luciana Valadares dos Santos [email protected]

Phone: 55-31-3499.8619

Leonardo Karam Rosa [email protected]

Phone: 55-31-3499.8056

Diogo Dias Gonçalves [email protected]

Phone: 55-31-3499.8710

Declarations relative to business perspectives of the Company, operating and

financial results and projections, and references to the growth of the

Company, constitute mere forecasts and were based on Management’s

expectations in relation to future performance. These expectations are highly

dependent on market behavior, on Brazil’s economic situation, on the

industry and on international markets, and are therefore subject to change.