1

Jean Laherrere 1 May 2019 Updated US primary energy in quad I have already written a first short paper on “US primary energy in quad” https://aspofrance.files.wordpress.com/2019/03/uspe2019.pdf This paper is more complete. Most of US oil and gas production data are reported in volume, but the heat content of the petroleum products varies in linear relationship with density (from 10°API to 70°API).

The heat content of oil production by country varies from 5100 to 6400 kBtu/b = 26%

y = -0,1581x + 44,314!

30!

35!

40!

45!

10! 15! 20! 25! 30! 35! 40! 45! 50! 55! 60! 65! 70!

heat

con

tent

GJ/

m3!

°API!

Canada oil products energy content vs gravity!

Jean Laherrere March 2015!

aviation gasoline!

asphalt!

heavy fuel oil!

lubricant & greases!

light fuel oil!

kerosene!diesel!

http://www.statcan.gc.ca/pub/57-601-x/2010004/appendix-appendice1-eng.htm!

heavy oil!

medium & light oil!

5000

5100

5200

5300

5400

5500

5600

5700

5800

5900

6000

6100

6200

6300

6400

6500

0 10 20 30 40 50 60 70 80

heat

con

tent

kBT

U/b

cumulative crude +condensate Mb/d

EIA 2014 crude oil +condensate heat content versus production

heat content kBtu/b

Jean Laherrere 2015

Sudan 5084

Cuba 6393

US 5800 constant since 1950!

average 5860 kBtu/bmedian 5880 kBtu/b

2

EIA was unable before 2013 to measure the density of the US crude production. In fact, EIA does not measure but guesses US oil production through a survey (EIA-914) https://www.eia.gov/petroleum/production/faqs.php With the expanded Form EIA-914 survey, EIA collects data from a sample of less than 500 out of 13,000 currently active operators of oil and natural gas wells. These operators account for about 90% of crude oil, lease condensate, and natural gas production in the Lower 48 states and a significant share of the total oil and natural gas production in each of the 15 states and the federal Gulf of Mexico for which data are individually collected.

EIA was reporting from 1950 to 2013 a constant heat content for US crude production (green at 5.8 MBtu/b) when all other products were declining except crude oil import (to compensate). This diminution of the energy of oil production by volume is due to the LTO production. The API input at refineries increases since 2008.

3

It is obvious that reporting US energy by volume is misleading and it is necessary to work on energy data. But it is obvious that US past energy data quality is poor ! EIA recognizes this fact by giving historical data only since 1949. But EIA monthly MER reports are complete and of very good quality, better than IEA or UK or Norway agencies reports. The energy unit of the SI (system international of units, which is the legal rule in every country in the world except the US, Liberia and Myanmar) is the Joule or the toe (tonne oil equivalent 1 toe = 42 GJ) One joule is about the energy to lift an apple by one meter. One man-day muscular energy (35 W for 8 hours) represents about one MJ (24 g of oil), when one horse energy represents 21 men and a 200 HP tractor represents 4300 men. OECD citizens use 0.2 GL per capita per year = 4.7 toe = 180 “energy slaves” (Didier Sornette 2019 & Euan Mearns’ site) French household, which consumes 4 MWh per year, uses in fact 50 virtual minimum salary (SMIC) men paid 1 € per month (Philippe Charlez’s book 2017) US agencies report energy by using the Btu = British thermal unit (illegal in the European Union since 1980, replaced by the Joule) 1 US quad = 1000 US trillion Btu =PBtu = 1 Btu = 1055 J and 1 quad ~ 1.06 EJ (exajoule) ~25 Mtoe SI quadrillion = million power 4 = 10E24 = Y (yotta) IEA definition:

27

28

29

30

31

32

33

3,5

4,0

4,5

5,0

5,5

6,0

6,5

1950 1960 1970 1980 1990 2000 2010 2020

°API

US

crud

e oi

l inp

ut r

efin

erie

s

MBt

u/b

year

US crude oil, petroleum products & NGPL heat content from EIA

crude oil import

crude oil prod & exportproducts import

products exportpetroleum consumption

motor gasoline consumptionNGPL prod

°API input refineries

Jean Laherrere Ap 2019

http://www.eia.gov/totalenergy/data/monthly/pdf/sec13_2.pdf

4

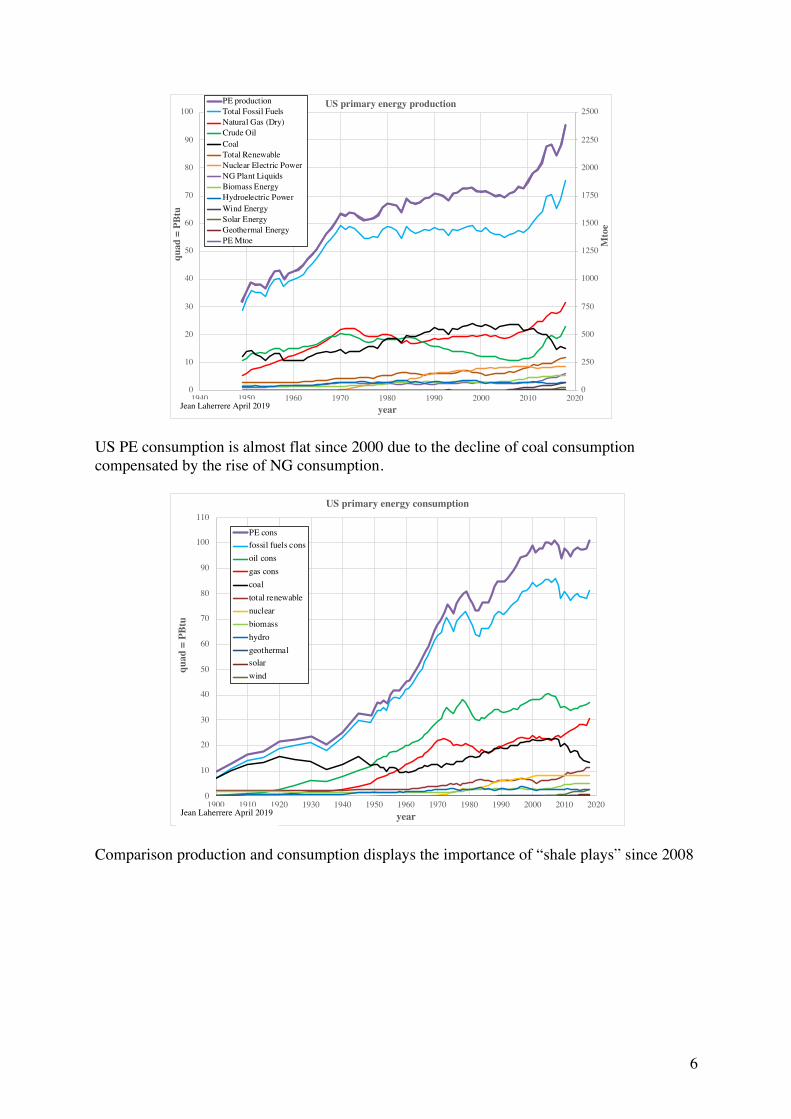

Electricity generation in TWh = 3600 TJ = 3.4 GBtu = 3.4/10E6 quad 1 quad = 293 TWh USDOE EIA MER reports each month the primary energy since 1949 -Primary energy PE consumption is flat since 2005, but production and export up and import are down.

PE production is up, mainly from crude oil and natural gas. Coal production is down since 2008 Since 1990 NG production is higher than oil production

To compare rise, log scale graph is better. Since 2011 rise of gas production is similar to the rise of the renewables. but oil rise is higher

5

Oil price down since 2012 and NG price since 2006, but residential electricity flat and three times gasoline price

US primary energy production displays the huge importance of fossil fuels and the largest production is natural gas, overpassing coal (first 1986-2010. The US PE production is up since 2008 because of oil and gas “shale plays” production

1

10

100

1940 1950 1960 1970 1980 1990 2000 2010 2020

quad

= P

Btu

log

scal

e

year

US primary energy production log scale

Natural Gas (Dry)

Crude Oil

Coal

Total Renewable

Nuclear Electric Power

Jean Laherrere April 2019

6

US PE consumption is almost flat since 2000 due to the decline of coal consumption compensated by the rise of NG consumption.

Comparison production and consumption displays the importance of “shale plays” since 2008

0

250

500

750

1000

1250

1500

1750

2000

2250

2500

0

10

20

30

40

50

60

70

80

90

100

1940 1950 1960 1970 1980 1990 2000 2010 2020

Mto

e

quad

= P

Btu

year

US primary energy productionPE productionTotal Fossil FuelsNatural Gas (Dry)Crude OilCoalTotal RenewableNuclear Electric PowerNG Plant LiquidsBiomass EnergyHydroelectric PowerWind EnergySolar EnergyGeothermal EnergyPE Mtoe

Jean Laherrere April 2019

0

10

20

30

40

50

60

70

80

90

100

110

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

quad

= P

Btu

year

US primary energy consumption

PE consfossil fuels consoil consgas conscoaltotal renewablenuclearbiomasshydrogeothermalsolarwind

Jean Laherrere April 2019

7

The plot of PE consumption and production in percentage shows roughly that for the last 20 years fossil fuels represent 80% when nuclear about 10% and renewables are about 10%, as in 1920: not much change! Renewables are far to take over!

It is interesting to compare the US percentage on energy with the world primary energy (in Mtoe) and we see the same pattern with fossil fuels at 80% for the last 20 years, nuclear is less at 5% and renewables is more at 15%. But it is obvious that fossil fuels trend at 80% will stay for a while!

0

10

20

30

40

50

60

70

80

90

100

110

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

quad

= P

Btu

year

US primary energy consumption & production

PE consPE productionfossil fuels consTotal Fossil Fuels prodoil conscrude oil + NGL prodgas consNatural Gas (Dry) prodtotal renewable constotal renewable prod

Jean Laherrere April 2019

0

10

20

30

40

50

60

70

80

90

100

1900 1920 1940 1960 1980 2000 2020

perc

enta

ge P

E %

year

US primary energy consumption & production in percentage

% fossil fuels cons% fossil fuels prod% renewables cons% renewables prod% nuclear cons% nuclear prod

Jean Laherrere April 2019

8

The fossil fuels resources are limited, and their production will peak and decline, in contrary the total renewable is assumed to be durable and their production will reach a peak and stay at this level. The nuclear primary energy is less limited by resources, more by politics. It is necessary to distinguish the renewable and the nuclear rom the total primary energy production -Nuclear production Nuclear production data depends upon the used conversion factor and this factor varies with sources, assuming the efficiency of an electric plant. The conversion toe/MWh varies between EIA, BP and France (= IEA after 2001)

PE nuclear production started in 1960 and increased sharply up to 2000 and stays flat to 2018.

0

10

20

30

40

50

60

70

80

90

100

1850 1870 1890 1910 1930 1950 1970 1990 2010 2030

%

year

World primary energy: percentage per source

% FF% renewables% nuclear

Jean Laherrere Dec 2018

0,20

0,22

0,24

0,26

0,28

0,30

1950 1960 1970 1980 1990 2000 2010 2020

toe/

MW

h

year

conversion factor in toe for nuclear electricity from EIA, BP & France

EIA US MER

France nuclear

BP Stat Rev modern power station

Jean Laherrere April 2019

9

AEO2019 forecasts a sharp decline 2019-204 and flat beyond to 2050. AEO2010 forecasted an increase. We plotted on the same graph the US electricity generation nuclear reported in TWh by IEA/WEO: both data correlate well with the equivalence 1 quad = 100 TWh, when in energy is 1 quad = 293 TWh, but the conversion factor must be applied, depending the assumed efficiency. WEO2011 forecasted an increase, WEO2018 forecasts a decrease but less than AEO2019. Our guest is the nuclear will stay flat (dotted arrow)

-Total renewable Total renewable includes biomass, hydroelectric, wind, solar and geothermal. Renewables production was about 3 quads from 1850 to 1940, 6 quads from 1980 to 2005 and rises to 11.5 quads in 2018. Renewables are assumed to go towards an asymptote and to stay there.

0

100

200

300

400

500

600

700

800

900

1000

0

1

2

3

4

5

6

7

8

9

10

1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

elac

ctri

city

gen

erat

ion

TWh

quad

US primary energy nuclear production

nuclear quad

AEO2010

AEO2019

WEO TWh

WEO2011

WEO2018

Jean Laherrere April 2019

1 quad = 293 TWh

10

The asymptote of production is estimated to be about 118 or20 quads, from the extrapolation of the bumpy annual growth versus annual production. With such asymptote at 18 quads, renewable production is estimated to be about 16 quads in 2050, which is the value forecasted by AEO2019; AEO2010 was more optimistic for renewable in 2035 than AEO2019 by 14%! AEO2019 is less optimistic on renewable than AEO2010, because with the shale plays less renewable is needed, but is it right? The plot of PE annual production growth versus annual production trends (loosely) towards 18 quads. The uncertainty is very high, but an ultimate of 20 quads

-Fossil fuels production

0

2

4

6

8

10

12

14

16

18

20

1800 1820 1840 1860 1880 1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

quad

= P

Btu

year

US primary energy total renewable production

A = 20 quadA = 18 quadAEO2010 renewableAEO2019 renewabletotal renewablebiomasshydrowindsolargeothermal

Jean Laherrere April 2019

-1

0

1

0 2 4 6 8 10 12 14 16 18 20

annu

al r

enew

able

gro

wth

qua

d

annual production quad

US annual growth vs primary energy total renewable production

an growth renew2009-2018

Jean Laherrere April 2019

11

US fossil fuels production in quad displays a large increase of 9 %/a for NGPL since 2009, of 7.5 %/a for crude oil since 2008 and only 4 %/a for natural gas since 2005. Crude oil rise for 1951-1970 was 2.3%/a and the decline for 1985-2006 2.8 %/a, pretty close. The US oil production is a good example of symmetry because the high number of oil producers acting in random. But shale plays have disturbed the trend and it was completely ignored in AEO 2010.

The same display in log scale allows to compare slopes. NGLP production is similar to NG production, except for the shale gas

If renewables and nuclear are assumed to not decline, it is not the case for the other sources of primary energy, being the fossil fuels, which will peak and decline.

0

125

250

375

500

625

750

875

1000

0

5

10

15

20

25

30

35

40

1940 1950 1960 1970 1980 1990 2000 2010 2020

Mto

e

quad

year

US fossil fuels production in quadNG + NGPLrise 5.8 %/arise 4 %/aNatural Gas (Dry)rise 2.3 %/adecline 2,8 %/arise 7.5%/aCrude OilCoalrise 5,5 %/arise 9 %/aNG Plant Liquidscrude oil Mtoe

Jean Laherrere Feb 2019

in 2018 NGPL = 19% of NGNG+NGPL = 39 % PENG+NGPL = 164 % crude oil

1

10

100

1940 1950 1960 1970 1980 1990 2000 2010 2020

quad

log

scal

e

year

US fossil fuels production in quad log scale

NG + NGPL

Natural Gas (Dry)

Crude Oil

Coal

Natural Gas Plant Liquids

Jean Laherrere Feb 2019

in 2018 NGPL = 19% of NGNG+NGPL = 39 % PENG+NGPL = 164 % crude oil

12

The HL of fossil fuels production is estimated to trend towards 6000 quads (cumulated production since 1950), being parallel to the trend of 1984-2005. Because the large uncertainty, our ultimate is taken with only one significant digit. Taking 2 or more significant digits will show that I do not understand the uncertainty of the estimate.

With such ultimate of 6000 quads, fossil fuels will peak soon and to decline sharply, as the rise.

This straight FF forecast should be compared with the forecast on page 35 being the addition of the separate forecasts for oil, gas and coal (cumulative production being different 1850 and 1950 where CP 1950 = 1000 quads).

0

1

2

3

4

0 1000 2000 3000 4000 5000 6000 7000 8000

aP/C

P%

cumulative PE -renewable production quad since 1950

US HL of primary energy fossil fuels production

aP/CP%

1984-2005

Jean Laherrere Ap 2019

0

1000

2000

3000

4000

5000

6000

0

10

20

30

40

50

60

70

80

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

annu

al q

uad

year

US primary energy fossil fuels production

fossil fuels prodU = 6000 quadCP PE-renew-nuclearU = 6 000 quad

Jean Laherrere Ap 2019

13

-Total primary energy forecast Adding fossil fuels forecast with the forecast for renewable and nuclear, the PE production in 2050 will be 53 quads, when AEO2019 forecasts 115 quads, more than the double! But AEO2010 forecast for 2035 was 24 % lower than AEO2019! In 2030 PE will be back to 2000 level at 70 quads, but beyond it is too severe, needing a lot of energy import and it is likely that nuclear will return or that renewable will improve.

The same data in percentage of the PE displays fossil fuels production percentage around 80 % from 1998 to 2018 for real data and staying at 80% up to 2050 for AEO2019. AEO2010 forecasted a FF percentage in decline. EIA does not forecast any significant energetic transition before 2050

In contrary my forecast expects for FF around 55% in 2050.

0

10

20

30

40

50

60

70

80

90

100

110

120

1800 1820 1840 1860 1880 1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

annu

al P

E p

rodu

ctio

n qu

ad

year

US primary energy production FF, renewable & nuclear

AEO2010AEO2019U PEPE prodU = 6000 quadfossil fuels prodA = 18 quadAEO2010 renewableAEO2019 renewabletotal renewable prodnuclear productionfuture flat

Jean Laherrere April 2019

0

10

20

30

40

50

60

70

80

90

100

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

%

year

US primary energy production FF, renewable & nuclear in percentage

% FF% FF my guess% FF AEO2019% FF AEO2010% renew% renew my guess% renew AEO2019% renew AEO2010% nuclear% nuclear my guess% nucl AEO2019% nucl AEO2010

Jean Laherrere April 2019

14

EIA/AEO evolution 1979-2019 of the PE forecast shows clearly that EIA forecasting is not good in the past and the present forecast should be about the same!

The US PE energy per capita (in red) has peaked at 310 MBtu in 1970, then declined to 235 MBtu in 2005 and is in 2018 at 290 MBtu = 53 boe (US crude oil barrel = 5,8 MBtu) My forecast for PE production per capita in 2050 will be in at 140 MBtu (which was the value in 1900), against the double for AEO2017. AEO2019 forecasts a peak for PE per capita in 2026 at 318 MBtu, against my forecast of 280 in 2020. But my forecast for 2030 is equal to AEO2010 forecast!

0

10

20

30

40

50

60

70

80

90

100

110

120

1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

PE p

rodu

ctio

n qu

ad

year

US PE production: AEO evolution 1979-2019 AEO1979AEO1982AEO1985AEO1990AEO1993AEO1994AEO1995AEO1996AEO1997AEO1998AEO1999AEO2000AEO2001AEO2002AEO2003AEO2004AEO2005AEO2006AEO2007AEO2008AEO2008AEO2009AEO2010AEO2011AEO2012AEO2013AEO2014AEO2015AEO2017AEO2018AEO2019actualactual-15%actual+15%Jean Laherrere Ap 2019

0

50

100

150

200

250

300

350

0

10

20

30

40

50

60

70

80

90

100

110

120

1800 1820 1840 1860 1880 1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

PE/c

apita

MBt

u

annu

al P

E p

rodu

ctio

n qu

ad

year

US primary energy production & per capita

AEO2010AEO2019U PEPE prodAEO201O/capAEO2019/capU PE/capPE/cap MBtu

Jean Laherrere April 2019

15

-Crude oil 1860-2100 Crude oil (including lease condensate), after a peak in 1970, in 1986 (Alaska) is presently increasing since 2008 with the LTO (light tight oil instead of the poorly called shale oil). Its ultimate is estimated at a round value of 2000 quads = 50 Gtoe = 350 Gb. Comparing to the crude oil ultimate in Gb a value of 1900 quads is closer. But a 2000 quads ultimate shows more the uncertainty of the ultimate, with only one significant digit. With such ultimate of 2000 quads, the crude oil production will be in 2035 about 15 quads when USDOE.EIA AEO 2019 forecasts the double = 30 quads.

My forecast displays a decline symmetrical with the rise and for 2035 is more than AEO2010 forecast! The HL of the crude oil is presently rising with the LTO, but its future decline will be parallel to the trend 1958-2008 and symmetrical with the rise, trending towards the rounded 2000 quads

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0

5

10

15

20

25

30

1860 1880 1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

CP

quad

aP q

uad

year

US crude oil production & forecast AEO & U = 2000 quad

increase 3%/adecline 2.5 %/aAEO2019AEO2010U = 2000 quadquad crude oilU = 2000 quadCP crude quad

Jean Laherrere Feb 2019

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

5,5

6,0

6,5

0 500 1000 1500 2000

aP/C

P%

cumulative crude oil production quad

US HL of crude oil production 1860-2018

aP/CP%1958-2008

Jean Laherrere Feb 2019

16

US producers have almost stopped making exploration, concentrated on the development of so-called shale plays.

The number of exploratory wells after a peak in 1981 at 17573 wells was only in 2017 at 847, 20 times less! The number of NFW (new field wildcats) dropped from 9151 to 450, again by 20 times. It means that the US are almost explored for oil and gas since 1859! Only few unexplored areas left offshore But the number of oil producing wells displays, after a second peak in 1985 at 646 626 (mainly due to marginal oil wells), a third peak in 2014 at 597 281, dropping in 2017 at 560 996.

US non marginal producing wells have stayed almost flat since 1992, in particular for gas wells: the shale play cannot be seen!

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

annu

al n

umbe

r of

wel

ls

year

US annual number of exploration wells

explodry exploNFWoil explogas explo

Jean Laherrere April 2019

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

num

ber

of p

rodu

cing

wel

ls

year

US number of producing wellsoilwellsmarginal oilwells DGMNmarginal oilwells <15 b/d IPAAgaswellsmarginal gaswells <90 kcf/d

Jean Laherrere Jan 2016

source EIA, IPAA, DGMN

17

EIA/AEO2011 crude oil forecast retrospective is chaotic: EIA was unable to properly forecast US oil production oil in the past and it is likely that it will be the same for the future!

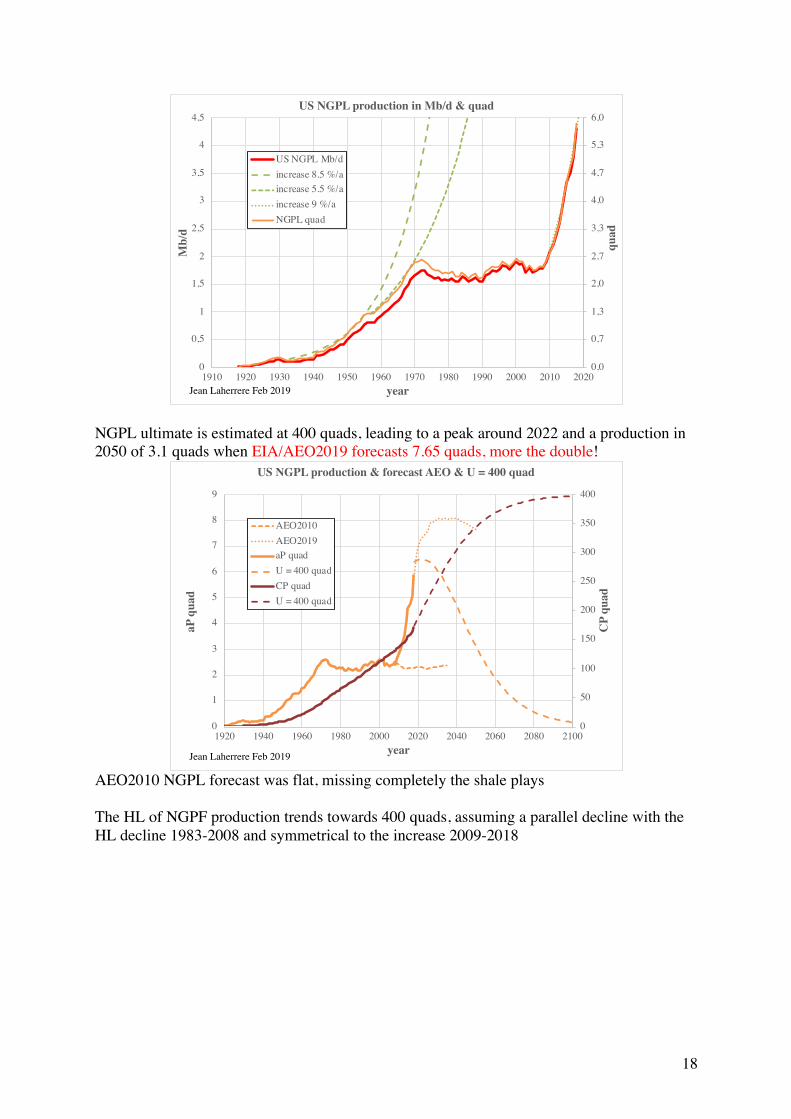

-NGPL production 1919-2100 The natural gas plant liquids production has increased since 1933 at 8.5 %/a until 1955, then at 5.5 %/a until 1970, then almost flat and from 2008 increasing at 9 %/a with the shale play, but this high rise is too high to stay long and the decline will be steep, as the rise.

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

180 000

200 000

1990 2000 2010 2020

annu

al n

umbe

r of

pro

duci

ng w

ells

year

US number of non marginal producing wells

non marg oil

non marg gas

Jean Laherrere Ap 2019

1700

1800

1900

2000

2100

2200

2300

2400

2500

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

annu

al p

rodu

ctio

n M

b

year

AEO 2011 retrospective of US oil production forecastAEO 1994

AEO 1995

AEO 1996

AEO 1997

AEO 1998

AEO 1999

AEO 2000

AEO 2001

AEO 2002

AEO 2003

AEO 2004

AEO 2005

AEO 2006

AEO 2007

AEO 2008

AEO 2009

AEO 2010

AEO 2011

ActualJean Laherrere Ap 2012

18

NGPL ultimate is estimated at 400 quads, leading to a peak around 2022 and a production in 2050 of 3.1 quads when EIA/AEO2019 forecasts 7.65 quads, more the double!

AEO2010 NGPL forecast was flat, missing completely the shale plays The HL of NGPF production trends towards 400 quads, assuming a parallel decline with the HL decline 1983-2008 and symmetrical to the increase 2009-2018

0,0

0,7

1,3

2,0

2,7

3,3

4,0

4,7

5,3

6,0

0

0,5

1

1,5

2

2,5

3

3,5

4

4,5

1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

quad

Mb/

d

year

US NGPL production in Mb/d & quad

US NGPL Mb/dincrease 8.5 %/aincrease 5.5 %/aincrease 9 %/aNGPL quad

Jean Laherrere Feb 2019

0

50

100

150

200

250

300

350

400

0

1

2

3

4

5

6

7

8

9

1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

CP

quad

aP q

uad

year

US NGPL production & forecast AEO & U = 400 quad

AEO2010AEO2019aP quadU = 400 quadCP quadU = 400 quad

Jean Laherrere Feb 2019

19

-crude oil & NGPL (petroleum) forecast There is very often confusion when dealing with oil production if it is crude or crude +condensate (lease condensate was in the past measured with crude) or crude +NGL. It is why it is important to plot crude +NGPL, in particular to compare with petroleum consumption.

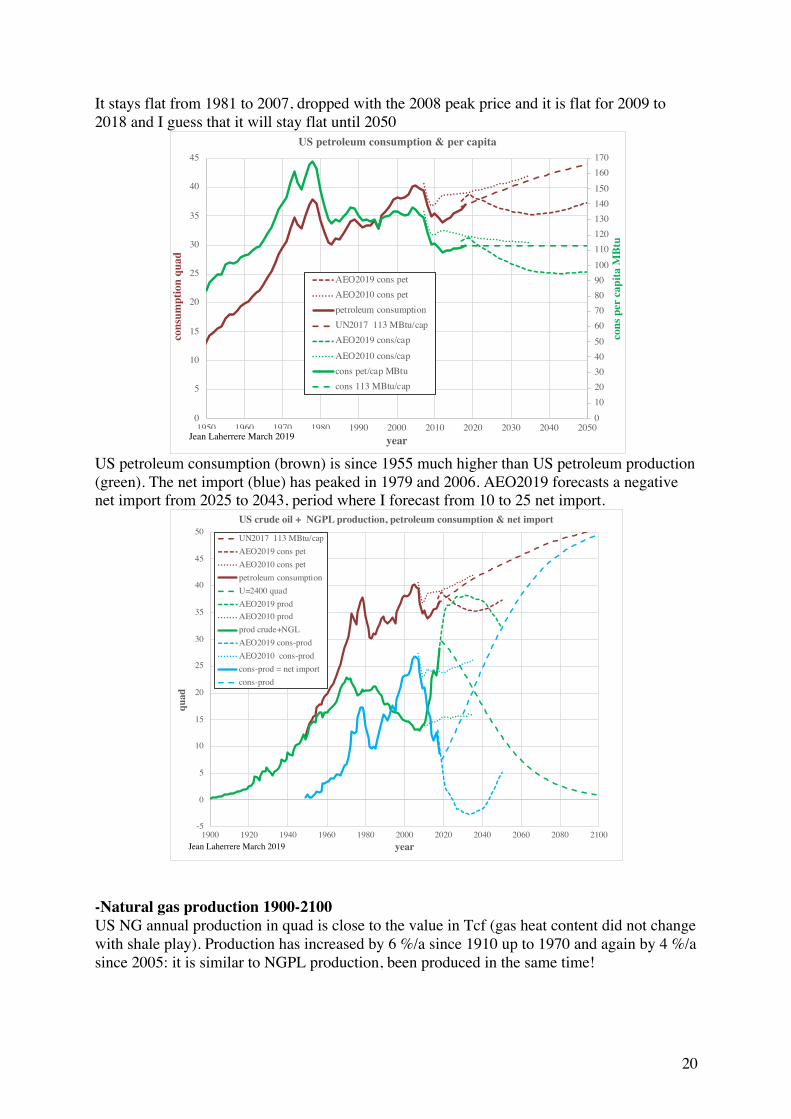

US crude oil +NGPL production is combined with crude import to feed domestic refineries which supply domestic petroleum consumption, but also petroleum exports. US petroleum consumption (brown) peaked in 1978 and 2008 (40 quads) and is presently at 37, forecasted by AEO2019 to stay at this level until 2050; AEO2010 forecasted higher values, my forecast assuming constant consumption per capita grows with population. US petroleum consumption per capita peaked in 1978 at 168 MBtu, in 2018 at 113 MBtu;

0

1

2

3

4

5

6

0 100 200 300 400

aP/C

P%

cumulative NGPL production quad

US HL of NGPL production in quad 1918-2018

aP/CP%1983-2008

Jean Laherrere Feb 2019

0

10

20

30

40

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

aP q

uad

year

US crude oil + NGPL production in quad & forecasts AEO AEO2019 prodAEO2010 prodU=2400 quadprod crude+NGLAEO2019 prodAEO2010 prodU = 2000 quadcrude oilAEO2019 prodAEO2010 prodU = 400 quadNGPL

Jean Laherrere Ap 2019

20

It stays flat from 1981 to 2007, dropped with the 2008 peak price and it is flat for 2009 to 2018 and I guess that it will stay flat until 2050

US petroleum consumption (brown) is since 1955 much higher than US petroleum production (green). The net import (blue) has peaked in 1979 and 2006. AEO2019 forecasts a negative net import from 2025 to 2043, period where I forecast from 10 to 25 net import.

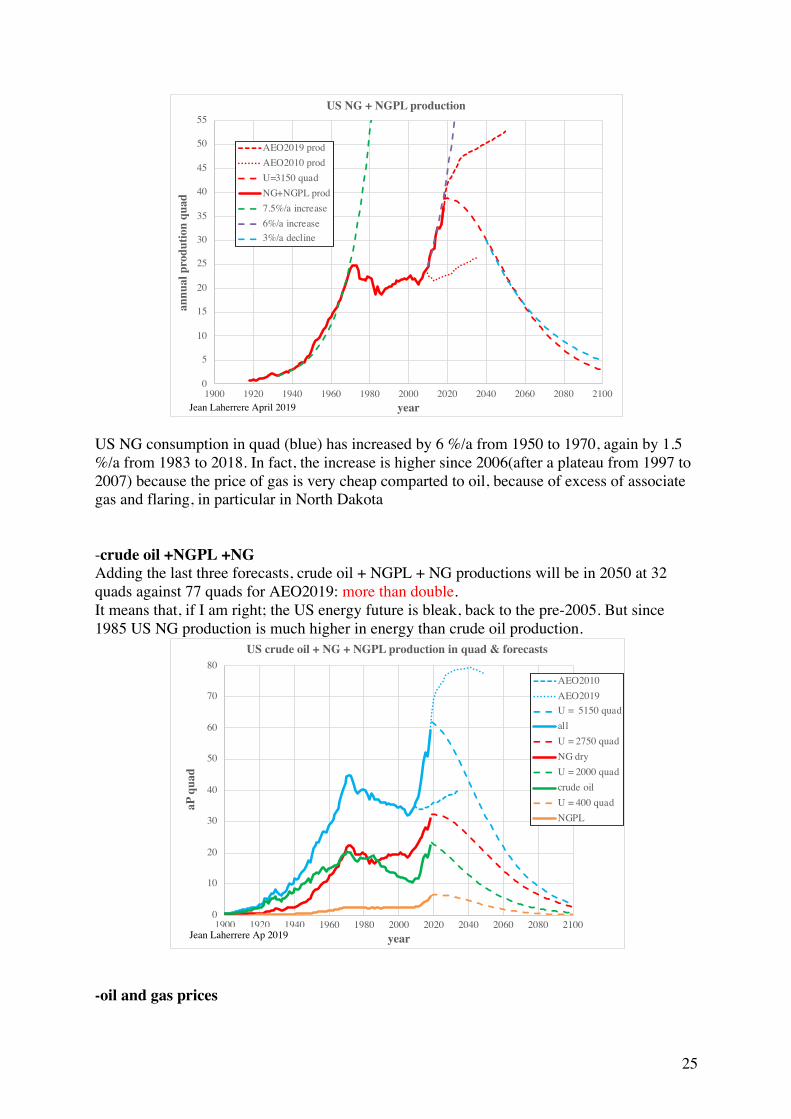

-Natural gas production 1900-2100 US NG annual production in quad is close to the value in Tcf (gas heat content did not change with shale play). Production has increased by 6 %/a since 1910 up to 1970 and again by 4 %/a since 2005: it is similar to NGPL production, been produced in the same time!

0102030405060708090100110120130140150160170

0

5

10

15

20

25

30

35

40

45

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

cons

per

cap

ita M

Btu

cons

umpt

ion

quad

year

US petroleum consumption & per capita

AEO2019 cons petAEO2010 cons petpetroleum consumptionUN2017 113 MBtu/capAEO2019 cons/capAEO2010 cons/capcons pet/cap MBtucons 113 MBtu/cap

Jean Laherrere March 2019

-5

0

5

10

15

20

25

30

35

40

45

50

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

quad

year

US crude oil + NGPL production, petroleum consumption & net import

UN2017 113 MBtu/capAEO2019 cons petAEO2010 cons petpetroleum consumptionU=2400 quadAEO2019 prodAEO2010 prodprod crude+NGLAEO2019 cons-prodAEO2010 cons-prodcons-prod = net importcons-prod

Jean Laherrere March 2019

21

US NG ultimate is estimated at 2750 quads from HL assuming parallelism with the period 1987-2005 and symmetry with the rise

US NG production will peak around 2020 and for the ultimate 2750 quads will be in 2050 at 20 quads against a forecast of AEO2019 of 45 quads: more than double

0

5

10

15

20

25

30

35

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

aP q

uad

& T

cf

year

US NG production in quad & Tcf

NG quadNG dry Tcfincrease 6 %/aincrease 6 %/aincrease 4 %/a

Jean Laherrere Feb 2019

0

0,5

1

1,5

2

2,5

3

3,5

4

4,5

5

0 500 1000 1500 2000 2500 3000

aP/C

P%

cumulative NG production quad

US HL of NG production 1900-2018

aP/CP%1987-2005

Jean Laherrere Feb 2019

22

AEO2010 NG forecast for 2035 was less than my present forecast. The NG production is compared with consumption and their difference consumption less production represents net import. AEO2019 forecasts that the negative NG import which started in 2014 will increase in 2050 to -9 quads. My forecast is that positive net import will return in 2025 and in 2050 will be 16 quads, giving a 25 quads difference with AEO2019 AEO2010 forecasted a positive NG net import in 2035 of 1.6 quad (-7 quad for AEO2019)

US NG consumption per capita (orange) peaked in 1972 at 104 MBtu and is 90 MBtu in 2018 and staying flat for AEO2019 and my forecast. AEO2010 forecasted a flat level at 70 MBtu from 2014 to 2035.

0

250

500

750

1000

1250

1500

1750

2000

2250

2500

2750

0

5

10

15

20

25

30

35

40

45

50

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

CP

quad

aP q

uad

year

US NG production & forecast AEO & U = 2750 quad

AEO2019 prodAEO2010 prodNG prod quadU = 2750 quadCP NG quadU = 2750 quad

Jean Laherrere Feb 2019

-10

-5

0

5

10

15

20

25

30

35

40

45

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

quad

year

US NG production, consumption & net import in quad U = 2750 quadAEO2019 prodAEO2010 prodNG prod quadAEO2019 consAEO2010 consNG cons quadcons93 MBtu93MBtu-2750 quadAEO2019 cons-prodAEO2010 cons-prodcons-prodNG net import

Jean Laherrere March 2019

23

US petroleum and NG consumption per capita are compared

-NG and NGPL NGPL is produced with NG and have to be compared NG and NGPL production forecasts are plotted on the same graph and it appears that AEO forecasts are flat for NGPL and rising for NG

0

10

20

30

40

50

60

70

80

90

100

110

0

5

10

15

20

25

30

35

40

45

1950 1975 2000 2025 2050

cons

/api

ta M

Btu

quad

year

US NG consumption & per capita

AEO2019 consAEO2010 consincrease 6%/aincrease 1.5%/aNG cons quadAEO2019 cons/capAEO2010 cons/capcons NG/cap

Jean Laherrere April 2019

0,8

1,0

1,2

1,4

1,6

1,8

2,0

2,2

2,4

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

ratio

pet

role

um/N

G

cons

umpt

ion

per

capi

ta M

Btu

year

US petroleum & NG consumption per capita

AEO2019 cons/capAEO2010 cons/capcons 113 MBtu/capcons pet/cap MBtuAEO2019 cons/capAEO2010 cons/capcons NG/cappetroleum/NGAEO2019

Jean Laherrere April 2019

24

The past NG and NGPL productions correlate well from 1900 to 2008 (comparison 1) with 8 quad NG = 1 quad NGPL. But from 1980 the correlation (comparison 2) differs with 3,6 quad NG = 1 quad NGPL

The shale plays produce more NGPL that the conventional gas plays Adding NG and NGL production shows that the annual growth was 7.5 %/a from 1933 to 1970, flat from 1978 to 2009, 6 %/a from 2010 to likely 2020 and a decline of 3 %/a from 2040

0

5

10

15

20

25

30

35

40

45

50

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

annu

al p

rodu

tion

quad

year

US NG & NGPL production

AEO2019 prodAEO2010 prodU = 2750 quadNG prod quadAEO2019AEO2010U = 400 quadNGPL prod quad

Jean Laherrere March 2019

0

1

2

3

4

5

6

7

8

9

0

9

18

27

36

45

54

63

72

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

NG

PLqu

ad

NG

qua

d

year

US NG & NGPL production comparison 1

AEO2019 prodAEO2010 prodU = 2750 quadNG prod quadAEO2019AEO2010U = 400 quadNGPL prod quad

Jean Laherrere April 2019

-3

-1

1

3

5

7

9

11

13

15

17

0

9

18

27

36

45

54

63

72

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100N

GPL

quad

NG

qua

d

year

US NG & NGPL production comparison 2

AEO2019 prodAEO2010 prodU = 2750 quadNG prod quadAEO2019AEO2010U = 400 quadNGPL prod quad

Jean Laherrere April 2019

25

US NG consumption in quad (blue) has increased by 6 %/a from 1950 to 1970, again by 1.5 %/a from 1983 to 2018. In fact, the increase is higher since 2006(after a plateau from 1997 to 2007) because the price of gas is very cheap comparted to oil, because of excess of associate gas and flaring, in particular in North Dakota -crude oil +NGPL +NG Adding the last three forecasts, crude oil + NGPL + NG productions will be in 2050 at 32 quads against 77 quads for AEO2019: more than double. It means that, if I am right; the US energy future is bleak, back to the pre-2005. But since 1985 US NG production is much higher in energy than crude oil production.

-oil and gas prices

0

5

10

15

20

25

30

35

40

45

50

55

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

annu

al p

rodu

tion

quad

year

US NG + NGPL production

AEO2019 prodAEO2010 prodU=3150 quadNG+NGPL prod7.5%/a increase6%/a increase3%/a decline

Jean Laherrere April 2019

0

10

20

30

40

50

60

70

80

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

aP q

uad

year

US crude oil + NG + NGPL production in quad & forecasts

AEO2010AEO2019U = 5150 quadallU = 2750 quadNG dryU = 2000 quadcrude oilU = 400 quadNGPL

Jean Laherrere Ap 2019

26

The oil/gas price ratio was around 6 in 1950, 1 in 2003, 6 again in 2011, down to 3 in 2018. It correlates well with the NG flaring, because when there is too much associate produced, it is flared, and NG price goes down. AEO2019 forecasts from 2020 to 2050 an oil/gas ratio of 4, meaning too much gas because LTO, which for me is wrong. AEO2010 forecasted an oil/gas ratio of about 2.5, without LTO but already too high. It is a shame to flare gas and to forecast the natural gas will be 4 times cheaper in 2050 than oil, when they were even in 2005?

EIA graph of cost of fuels to end users shows the same story: NG price is equal to residential heating oil only for the period 1987-2002

The NG prices in different countries compared to the oil price from BP 2018 shows very well that oil price and gas price correlates well except for US and Canada after 2009, which is, the start of the shale plays. In Canada NG price is lower than in <US, as flaring is higher.

0

5

10

15

20

25

30

35

40

0

1

2

3

4

5

6

7

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Alta

& N

D fl

arin

g %

oil/g

as p

rice

rat

io &

US,

Tex

as fl

arin

g %

year

US crude oil/natural gas price ratio & gas flaring

oil/gas ratioUS flared/gross %Texas flaring/gross %oil/gas AEO2019oil/gas AEO2010ND flaring %Alberta flaring %

Jean Laherrere April 2019

27

The US fossil fuels price in $/MBtu has changed drastically with time. Prices are irrational and very hard to forecast, except for gas price related to flaring.

US WTI oil price is related to the value of dollar multiplied by -1. The attempts by Saudi Arabia and Russia to reduce crude oil production to please Trump are hardly seen.

0

2

4

6

8

10

12

14

16

18

20

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

$/M

Btu

year

oil & natural gas price from BP 2018

crude oil CIFGermanyUKNetherlandsUSCanada

Jean Laherrere April 2019

0

2

4

6

8

10

12

14

16

18

20

1950 1960 1970 1980 1990 2000 2010 2020

$/M

Btu

year

US crude oil + NG + NGPL price in $/MBtu

NG Henry Hub $/MBtu

NGPL $/MBtu

WTI $/MBtu

Jean Laherrere Feb 2019

28

Also the US weekly private stocks of crude oil followed the WTI*-1 13 weeks before.

The value of the dollar is the key for WTI oil price and US crude oil stocks. This correlation is hardly mentioned in the medias. The US oil and gas production converted with such prices and using CPI inflation into $2018 and the NG production is worth much less than crude oil, despite being higher in energy. NGPL production values is presently about half NG production value.

-120

-115

-110

-105

-100

-95

-90

-85

-80

-75

0

10

20

30

40

50

60

70

80

90

100

110

120

130

2006 2008 2010 2012 2014 2016 2018 2020

broa

d do

llar

inex

*-1

oil p

rice

$/b

year

US monthly oil price & negative dollar value

WTI spot $/b

negative broad dollar index

Jean Laherrere April 2019

https://www.federalreserve.gov/releases/h10/summary/jrxwtfbc_nm.htm

-115

-105

-95

-85

-75

-65

-55

-45

-35

-25

-15

300

320

340

360

380

400

420

440

460

480

500

520

540

2012 2013 2014 2015 2016 2017 2018 2019 2020

WTI

*-1

13

wee

ks b

efor

e

US

priv

ate

stoc

ks c

rude

oil

Mb

year

US weekly private stocks crude oil & WTI *-1 shifted 13 weeks

Weekly U.S. Ending Stocks excluding SPRof Crude Oil "excluding lease stock"WTI *-1 13 weeks before

WTI $/*-1b

Jean Laherrere April 2019

oil cut Saudi Arabia-Russia

29

AEO2019 forecast of crude oil and NG prices in $2018 until 2050 is also displayed in log scale

The price ratio oil versus gas is striking: it was about 7 in 1950 declining slowly towards 1, being the equality, in 2005, but with the shale plays it jumped into 6 in 2012 , presently around 3 and forecasted to be 4 from 2020 to 2050, which is strange to me of not trending towards 1 again. Energy equality is not the goal of USDOE/EIA.

0

50

100

150

200

250

300

350

1950 1960 1970 1980 1990 2000 2010 2020

G$2

018

year

US crude oil, NG & NGPL production value in $2018

crude oil G$2018

NG G$2018

NGPL G$2018

Jean Laherrere Feb 2019

0

2

4

6

8

10

12

14

16

18

20

22

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

$201

8/M

Btu

year

US crude oil & NG price & forecasts AEO AEO2010 lowS $2008AEO2019 $2018WTI $2018AEO2010 NG Henry $2008AEO2019 $2018NG Henry Hub $2018

Jean Laherrere Ap 2019

$2018 = https://fred.stlouisfed.org/series/CPIAUCSL 1

10

100

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

$201

8/M

Btu

log

scal

e

year

US crude oil & NG price & forecastsAEO log scale

AEO2010 NG Henry $2008AEO2019 $2018NG Henry Hub $2018AEO2010 lowS $2008AEO2019 $2018WTI $2018

Jean Laherrere Ap 2019

30

In fact, gas is wasted and undervalued and flared (or vented) because often associated with oil. The US crude oil/NG price ratio correlates roughly with the US NG flaring (as Texas flaring) and since 2005 with the North Dakota flaring. It seems hard to believe that the oil/NG price ratio will stay high for the next 30 years, as forecasted by AEO2019 about 4, meaning that NG will be continued to be wasted, flared and underestimated Gas flaring is high because the lack of gas pipelines in new shale plays, as North Dakota, where Bakken oil is mainly moved by rail (explosive oil with several rail accidents). The problem is that building a pipeline needs a long term project and is shale gas a long term project? However, lack of pipelines is not obvious when looking at the US pipeline maps

There are more gas pipelines than oil pipelines Natural gas is delivered directly to the consumer at home contrary to oil going to services stations. The interstate pipeline mileage is greater for gas than for oil (OGJ 2006-2015), but steady when increasing for oil. Why is gas pipeline not increasing as oil pipeline?

0

1

2

3

4

5

6

7

8

1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

ratio

pri

ce c

rude

oil

/ NG

year

US crude oil /NG price ratio & forecasts AEO

AEO2010AEO2019oil/NG

Jean Laherrere Ap 2019

31

In 2016 the revenues of the pipeline company per mile was higher for oil than for gas. https://www.ogj.com/articles/print/volume-114/issue-9/special-report-pipeline-economics/natural-gas-pipeline-profits-construction-both-up.html

It is very hard to find any data on the cost to transport US natural gas by pipeline in $/MBtu. My search was dry! The cost to transport crude oil was about 5 $/MBtu by pipeline and 10 to 15 $/MBtu by rail. -production values & wellhead revenues IPAA reports wellhead revenues since 1992: NG production revenues were higher than crude oil before 2008 and lower after

EIA reports crude oil, NG and NGPL values in $2018 since 1950, NG value in G$2018 was lower than oil from 1960 to 1997 and from 2009 to 2018, when NG production in quad was only lower from 1950 to 1968 and from 1982 to 1988. In 2018

0

5

10

15

20

25

30

140 000

145 000

150 000

155 000

160 000

165 000

170 000

175 000

180 000

185 000

190 000

195 000

200 000

2006 2008 2010 2012 2014 2016 2018re

venu

es G

$mile

s

year

US interstate pipeline mileage and pipeline company revenues

miles gasmiles oilrevenues gas G$revenues oil G$

Jean Laherrere April 2019

https://www.ogj.com/articles/print/volume-114/issue-9/special-report-pipeline-economics/natural-gas-pipeline-profits-construction-both-up.html

60 000

65 000

70 000

75 000

80 000

85 000

90 000

95 000

100 000

105 000

110 000

115 000

120 000

125 000

130 000

135 000

140 000

2006 2008 2010 2012 2014 2016 2018

$/m

iles

year

US pipeline company revenues per mile

revenues $/mile gas

revenues $/mile oil

Jean Laherrere April 2019

https://www.ogj.com/articles/print/volume-114/issue-9/special-report-pipeline-economics/natural-gas-pipeline-profits-construction-both-up.html

0

50

100

150

200

250

300

1990 2000 2010 2020

wel

lhea

d re

venu

es G

$

year

US wellhead revenues from IPAA

crude oil

NG

Jean Laherrere April 2019

32

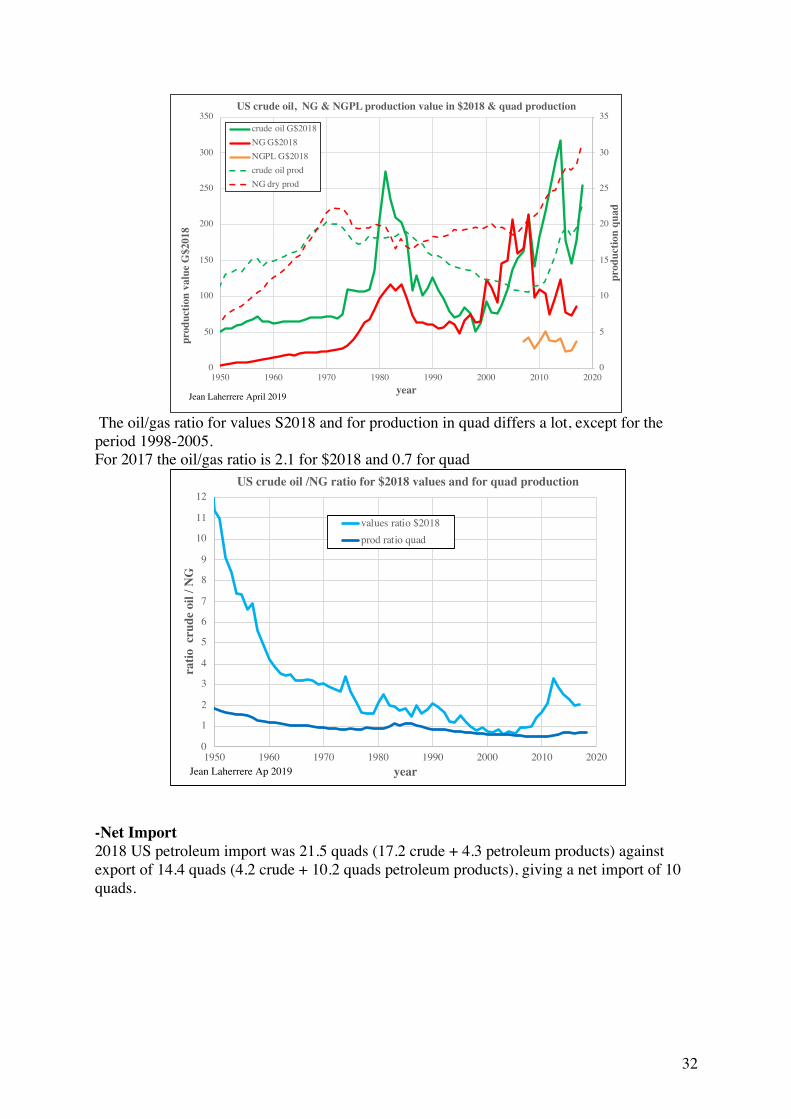

The oil/gas ratio for values S2018 and for production in quad differs a lot, except for the period 1998-2005. For 2017 the oil/gas ratio is 2.1 for $2018 and 0.7 for quad

-Net Import 2018 US petroleum import was 21.5 quads (17.2 crude + 4.3 petroleum products) against export of 14.4 quads (4.2 crude + 10.2 quads petroleum products), giving a net import of 10 quads.

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

350

1950 1960 1970 1980 1990 2000 2010 2020

prod

uctio

n qu

ad

prod

uctio

n va

lue

G$2

018

year

US crude oil, NG & NGPL production value in $2018 & quad production

crude oil G$2018NG G$2018NGPL G$2018crude oil prodNG dry prod

Jean Laherrere April 2019

0

1

2

3

4

5

6

7

8

9

10

11

12

1950 1960 1970 1980 1990 2000 2010 2020

ratio

cru

de o

il / N

G

year

US crude oil /NG ratio for $2018 values and for quad production

values ratio $2018prod ratio quad

Jean Laherrere Ap 2019

33

US NG net import was negative in 2017 and 2018.

AEO2019 forecasts that in 2021 US oil net import will be negative until 2046, with a peak of oil export in 2033 of 5 quads. AEO2010 forecasted a flat oil net import of 21 quads 2007-2035. My guess is that net oil import will resume growing from 2020 with a slope similar to 1982-2008. AEO2019 forecasts a negative NG net import growing up to 2050 at - 8 quads AEO2010 forecasted a flat NG net import around 2 quads until 2035. My guess is that NG net import will return to positive in 2035.

-15

-10

-5

0

5

10

15

20

25

30

35

1950 1960 1970 1980 1990 2000 2010 2020

net i

mpo

rt q

uad

year

US net import of oil & gas

Petroleum net mportpetroleum importpetroleum exportNG net import NGNG importNG exportcrude oil importcrude oil exportpetrol prod importpetrol prod export

Jean Laherrere April 2019

34

In 2050 AEO 2019 consumption - production = net import is forecasted at – 9 quad (meaning that US will export NG) when my forecast for U = 2750 quad and consumption per capita at 93 MBtu is + 16 quad (meaning that US will import NG) the difference is 25 quad: it is huge! EIA/MER displays US PE net imports with a peak in 1977 and 2006

-10

-5

0

5

10

15

20

25

30

35

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

net i

mpo

rt q

uad

year

US net import of oil & gas in quad & AEO2010 & AEO2019

AEO2019 oil net importAEO2010 oil net importcons-prod oil 2400 quadoilnet import quadAEO2010 NG net importAEO2019 NG net importcons-prod NG 2750 quadNG net import quad

Jean Laherrere March 2019

oilproduction = crude +NGLconsumption = crude + petroleum

35

-coal production Rutledge production data before 1950 were converted in quad using an average factor. An ultimate of 2200 quads (from 1800) is used from the HL US coal production peaked in 1998 & 2008 at 24 quads and the decline is sharp. AEO2010 forecasted for 2035 a production of 25 quads when AEO 2019 forecasts about half and my guess is half of AEO2019. The question is what environment rules will be because the resources are still large.

36

The HL for the period 2006-2018 is extrapolated towards an ultimate of 2200 quads

Adding this coal forecast for U = 2200 quads to those from crude oil, NGPL and NG (combined ultimate = 5150 quads) gives a forecast for U1800 = 7350 quads

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

0

5

10

15

20

25

30

1800 1825 1850 1875 1900 1925 1950 1975 2000 2025 2050 2075 2100

cum

ulat

ive

prod

qua

d

quad

US primary energy coal production

AEO2010

AEO2019U = 2200 quadcoal prod quadU = 2200 quadCP quad

Jean Laherrere April 2019

0

1

2

3

4

5

0 200 400 600 800 1000 1200 1400 1600 1800 2000 2200 2400

quad

cumulative production quad

US HL of primary energy coal production

aP/CP%

2006-2018

Jean Laherrere April 2019

37

This FF forecast is similar with the one page 11 using a global approach but starting from 1950 (U1950 = 6000 quads) when this one start 1800, when the cumulative FF production up to 1950 is about 1000 quads. -Population and GDP Annual population (in red) has grown from 5 M in 1800 to 327 M in 2018. UN2017 medium fertility forecasts 450 M in 2100 Annual population growth (in blue) has peaked to 3.5 M in 1992, being 2.1 M in 2018 and UN2017 forecasts 0.6 M in 2100

0

10

20

30

40

50

60

70

80

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

quad

US primary energy fossil fuels production

U = 7350 quad

FF

U = 5150 quad

crude +NGPL +NG

U = 2200 quad

coal

Jean Laherrere April 2019

CP1950 coal = 660 quadCP 1950 oil+gas = 330 quadCP 1950 FF = 1000 quad

0

0,5

1

1,5

2

2,5

3

3,5

4

0

50

100

150

200

250

300

350

400

450

1800 1825 1850 1875 1900 1925 1950 1975 2000 2025 2050 2075 2100

annu

al g

row

th M

annu

al p

opul

atio

n M

year

US population & forecast

pop MaddisonUN2017pop US EIAmedium UN2017Pm=450 MA=450 MUS pop AEO2017growth Maddisonan growth M EIAan growth M UN2017growth Pm450growth A450M

Jean Laherrere April 2019

38

US annual population growth versus population trends for the period 1992-2018 towards 450 M, being either the peak of population or the asymptote.

US GDP in G$ (green) and G$2012 (blue) from EIA and WB. G$2012 is 17 300 in 2018 and is forecasted to be 33 000 in 2050 by AEO2019 or by the S curve towards an asymptote of 50 000

Annual GDP growth G$2012 (red) has peaked in 1999 at 550 G$2012 and the period 1999-2017 trends towards an ultimate of 50 000.

0

1

2

3

4

0 50 100 150 200 250 300 350 400 450

annu

al p

opul

atio

n gr

owth

M

population M

US population annual growth versus population

an growth M EIA

an growth M UN2017

1992-2018

Jean Laherrere Ap 2019

0

100

200

300

400

500

600

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

annu

al g

row

th

GD

P G

$ &

G$2

012

year

US GDP from EIA & WB

US GDP G$ EIA

US GDP G$2012 EIA

US GDP G$ WB

US GDP G$2010 WB

A 50 000 G$2012

GDP AEO2017 G$2012

US GDP growth G$2012 EIA

Jean Laherrere April 2019

39

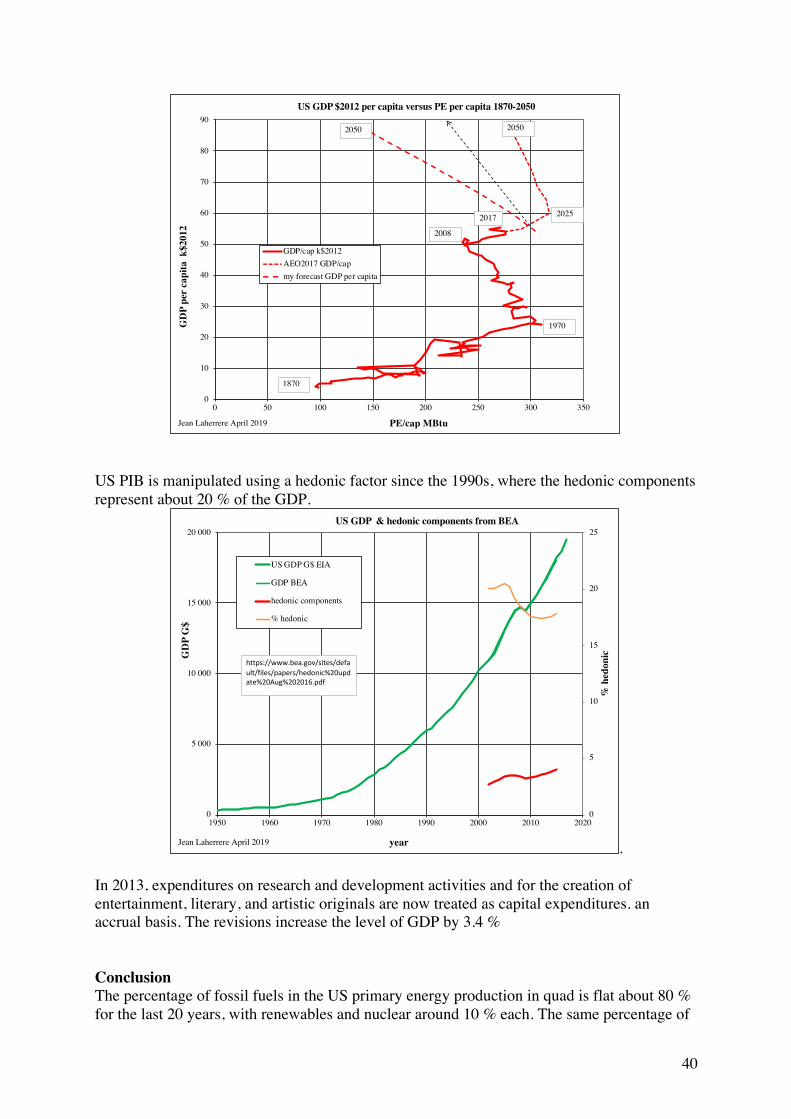

In 1880 GDP per capita was 4 k$2012 and PE per capita around 100 MBtu, in 2018 GDP/cap is 55 k$2012 and PE/cap 290 MBtu (peak at 310 in 1970) In 2050 GDP/cap will be 85 k$2012 and PE/cap 285 MBtu for AEO2018 and only 150 for my forecast! But looking at the graph I guess that PE/cap beyond 2020 will be parallel to the decline 1970-2005 as indicated by the dotted arrow, being the middle between my forecast and AEO2019!

The plot GDP/cap versus PE/cap displays different linear trends: first 1850-1970, second opposite 1970-2008 and third 2008-2020 parallel to the first trend and the fourth similar to the second trend. Again, the trend beyond 2020 could be the dotted arrow, forgetting the shale burst of 2008 and back to the post 1970 peak trend !

0

100

200

300

400

500

600

700

800

0 5 000 10 000 15 000 20 000 25 000 30 000 35 000 40 000 45 000 50 000

annu

al g

row

th G

$201

2 &

G$

GDP $2012 & G$

US GDP anual growth versus GDP

US GDP growth G$2012 EIA

1999-2017

US GDP growth G$ EIA

Jean Laherrere April 2019

0

50

100

150

200

250

300

350

0

10

20

30

40

50

60

70

80

90

100

110

120

1850 1875 1900 1925 1950 1975 2000 2025 2050 2075 2100

PE/c

ap M

Btu

GD

P pe

r ca

pita

k$2

012

year

US PE & GDP $2012 per capita

GDP/cap k$2012my forecast GDP per capitaAEO2017PE/cap MBtuU=10 000 quadAEO2017/cap

Jean Laherrere April 2019

40

US PIB is manipulated using a hedonic factor since the 1990s, where the hedonic components represent about 20 % of the GDP.

. In 2013, expenditures on research and development activities and for the creation of entertainment, literary, and artistic originals are now treated as capital expenditures. an accrual basis. The revisions increase the level of GDP by 3.4 % Conclusion The percentage of fossil fuels in the US primary energy production in quad is flat about 80 % for the last 20 years, with renewables and nuclear around 10 % each. The same percentage of

0

10

20

30

40

50

60

70

80

90

0 50 100 150 200 250 300 350

GD

P pe

r ca

pita

k$2

012

PE/cap MBtu

US GDP $2012 per capita versus PE per capita 1870-2050

GDP/cap k$2012AEO2017 GDP/capmy forecast GDP per capita

Jean Laherrere April 2019

1970

1870

2008

2017 2025

20502050

0

5

10

15

20

25

0

5 000

10 000

15 000

20 000

1950 1960 1970 1980 1990 2000 2010 2020

% h

edon

icGD

P G

$

year

US GDP & hedonic components from BEA

US GDP G$ EIA

GDP BEA

hedonic components

% hedonic

Jean Laherrere April 2019

https://www.bea.gov/sites/default/files/papers/hedonic%20update%20Aug%202016.pdf

41

80 % for fossil fuels is found for the world primary energy with 5% nuclear and 15% renewables. AEO2019 forecasts such 80% for FF until 2050, my guess is less optimistic. EIA does not forecast any energetic transition! US shale plays production forecasts are going towards the sky in AEO2019 when shale plays were ignored in AEO2010. IEA/WEO2010 considered Bakken as conventional, as shale oil was ignored, only oil shale (immature kerogen) was forecasted! The funny thing is that the term “shale oil” is wrong, because production comes from tight reservoir and “shale oil” is now called LTO = “light tight oil” Shale plays are like Uber and Tesla, lot of potential and lot of losses! It is imperative to look at production data in energy and not in volume. But the variation of price upsets the picture. Most people believe that US oil production is larger than natural gas production: it is true in value, but wrong in energy. Today US oil production is 2.1 times the gas production in value but only 0.7 times in energy (quad) US primary energy is forecasted by AEO2019 to be in 2050 44 % higher than in 2018 and it is likely to be right globally, but wrong in the components. The difference between the EIA forecasts of 2019 and 2010 is huge. It is likely that EIA 2030 forecast will display also huge difference. US NG price is three times lower than oil price and forecasted by EIA to be four times in 2050: it seems unrealistic leading to wasting natural gas and flaring. It looks unreasonable! The US shale burst will be over soon and back to reality of post 1970 oil peak. US energy independence is a fake news.