Almarai Company

2013 Q3 Earnings Presentation

Disclaimer

Information contained in this presentation is subject to change without further notice, its accuracy is not guaranteed and it may not contain all material information concerning the company. Neither we nor our advisors make any representation regarding, and assume no responsibility or liability for, the accuracy or completeness of, or any errors or omissions in, to any information contained herein. In addition, the information contains projections and forward-looking statements that reflect the company’s current views with respect to future events and financial performance. These views are based on current assumptions which are subject to various risks and may change over time. No assurance can be given that future events will occur, that projections will be achieved, or that the company’s assumptions are correct. Actual results may differ materially from those projected. This presentation is strictly not to be distributed without the explicit consent of Almarai Company management under any circumstances.

Almarai Company 2 2013 Q3 Earnings Presentation

Business Highlights

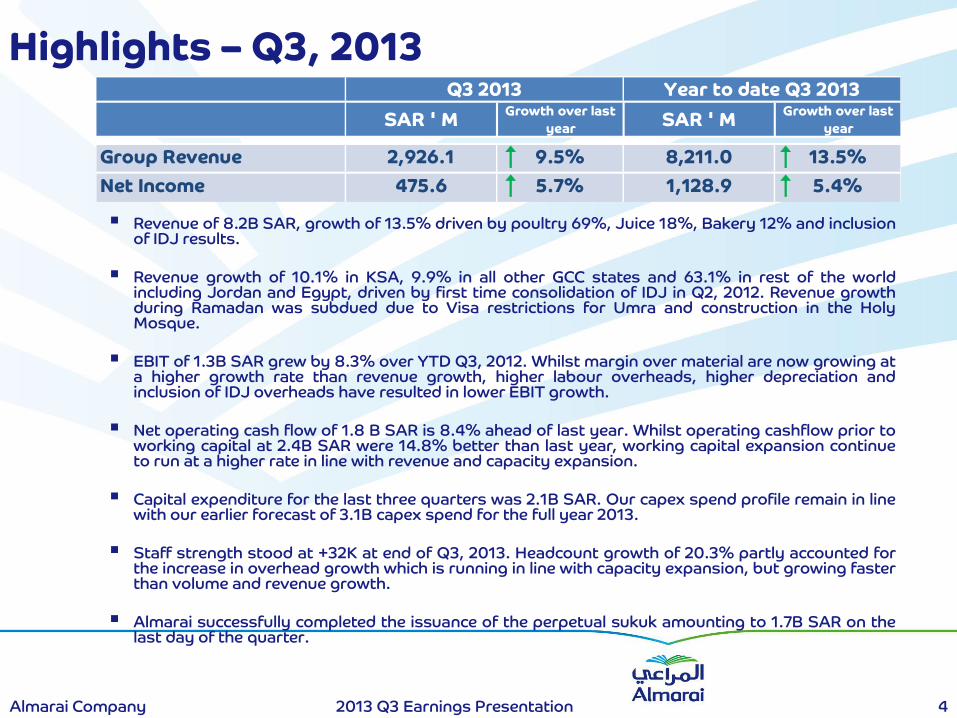

Revenue of 8.2B SAR, growth of 13.5% driven by poultry 69%, Juice 18%, Bakery 12% and inclusion of IDJ results.

Revenue growth of 10.1% in KSA, 9.9% in all other GCC states and 63.1% in rest of the world including Jordan and Egypt, driven by first time consolidation of IDJ in Q2, 2012. Revenue growth during Ramadan was subdued due to Visa restrictions for Umra and construction in the Holy Mosque.

EBIT of 1.3B SAR grew by 8.3% over YTD Q3, 2012. Whilst margin over material are now growing at a higher growth rate than revenue growth, higher labour overheads, higher depreciation and inclusion of IDJ overheads have resulted in lower EBIT growth.

Net operating cash flow of 1.8 B SAR is 8.4% ahead of last year. Whilst operating cashflow prior to working capital at 2.4B SAR were 14.8% better than last year, working capital expansion continue to run at a higher rate in line with revenue and capacity expansion.

Capital expenditure for the last three quarters was 2.1B SAR. Our capex spend profile remain in line with our earlier forecast of 3.1B capex spend for the full year 2013.

Staff strength stood at +32K at end of Q3, 2013. Headcount growth of 20.3% partly accounted for the increase in overhead growth which is running in line with capacity expansion, but growing faster than volume and revenue growth.

Almarai successfully completed the issuance of the perpetual sukuk amounting to 1.7B SAR on the last day of the quarter.

Highlights – Q3, 2013

Almarai Company 4 2013 Q3 Earnings Presentation

SAR ' MGrowth over last

yearSAR ' M

Growth over last

year

Group Revenue 2,926.1 9.5% 8,211.0 13.5%

Net Income 475.6 5.7% 1,128.9 5.4%

Q3 2013 Year to date Q3 2013

Strong pipeline of innovation continues in 2013

5 2013 Q3 Earnings Presentation Almarai Company

Sales Highlights

Sales Growth – Geography mix

Almarai Company 7 2013 Q3 Earnings Presentation

KSA

All

Others

GCC

10.1%

9.9%

63.1%

Almarai

Group 13.5%

% Growth

YTD Q3 2012

Rev in B SAR

YTD Q3 2013

Rev in B SAR

KSA65.5%

GCC25.3%

All Others9.2%

YTD Q3 2013

KSA67.5%

GCC26.1%

All Others6.4%

YTD Q3 2012

0.46

0.75

1.89

2.08

4.88

5.38

7.24

8.21

Sales Analysis by Product & Region

Almarai Company 8 2013 Q3 Earnings Presentation

Sales by Product

Participation vs Growth – YTD Q3 2013

2013 2012 % change

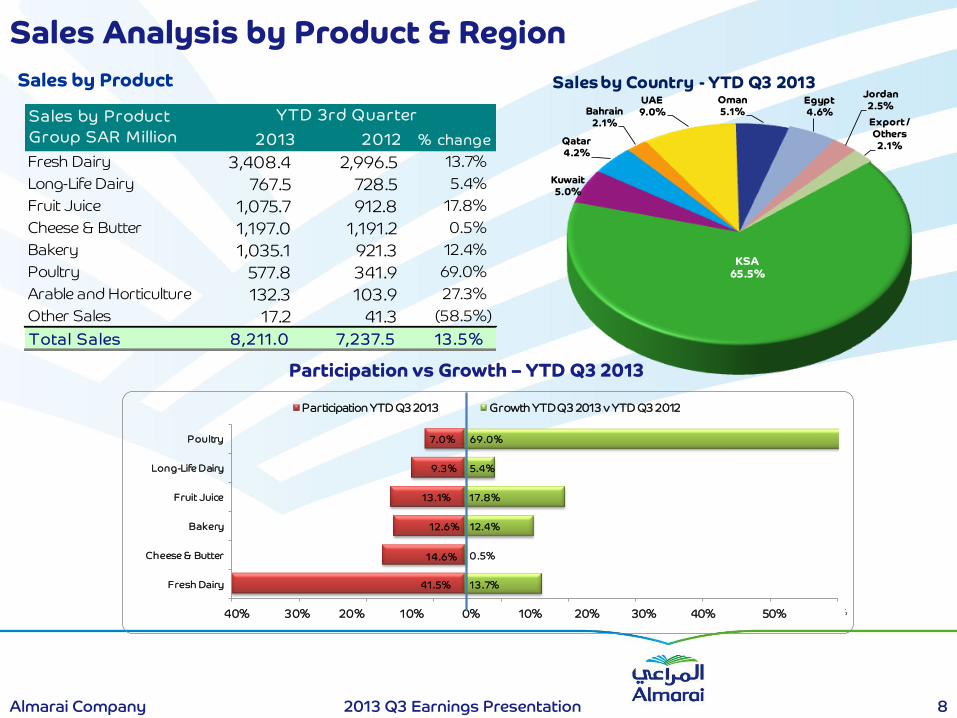

Fresh Dairy 3,408.4 2,996.5 13.7%

Long-Life Dairy 767.5 728.5 5.4%

Fruit Juice 1,075.7 912.8 17.8%

Cheese & Butter 1,197.0 1,191.2 0.5%

Bakery 1,035.1 921.3 12.4%

Poultry 577.8 341.9 69.0%

Arable and Horticulture 132.3 103.9 27.3%

Other Sales 17.2 41.3 (58.5%)

Tota l Sa les 8,211.0 7,237.5 13.5%

Sales by Product

Group SAR Million

YTD 3rd Quarter

KSA65.5%

Kuwait5.0%

Qatar4.2%

Bahrain2.1%

UAE9.0%

Oman5.1%

Egypt4.6%

Jordan2.5%

Export / Others

2.1%

Sales by Country - YTD Q3 2013

41.5%

14.6%

12.6%

13.1%

9.3%

7.0%

13.7%

0.5%

12.4%

17.8%

5.4%

69.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Fresh Dairy

Cheese & Butter

Bakery

Fruit Juice

Long-Life Dairy

Poultry

Participation YTD Q3 2013 Growth YTD Q3 2013 v YTD Q3 2012

40% 30% 20% 10% 0% 10% 20% 30% 40% 50%

Change in growth rates and IDJ consolidation results in

higher share of poultry, juice and dairy

Almarai Company 9 2013 Q3 Earnings Presentation

39.6% 40.7% 43.4%40.3% 39.6% 39.9%

44.7%

19.4% 15.4%15.3%

15.5% 16.4% 14.4%

13.3%

14.4%

12.9%11.3%

14.0% 14.1%12.9%

11.1%

10.2%13.3% 13.8% 12.5% 11.9%

13.4%13.8%

10.5% 10.4% 9.4% 10.9% 10.7%9.1%

8.5%

4.7% 4.7% 4.8% 6.1% 6.7%7.1%

7.3%

1.3% 2.6% 2.0% 0.7% 0.5% 3.4% 1.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013

Revenue Contribution

Other Sales

Poultry

Long-Life Dairy

Fruit Juice

Bakery

Cheese & Butter

Fresh Dairy

Statement of Income

Almarai Company 10 2013 Q3 Earnings Presentation

• Margin over material has continued to show higher growth than revenue in the first three quarters. However, higher depreciation, IDJ consolidation effect from Q2 2012 and higher headcount to manage poultry roll out resulted in lower gross profit growth compared to revenue growth.

• Similarly, growth in overheads is driven by head count increase and IDJ consolidation in Q1, resulting in lower net profit growth relative to revenue growth

SAR million 2013 2012 Change 2013 2012 Change

Sales 2,926.1 2,673.0 9.5% 8,211.0 7,237.5 13.5%

Cost of sales (1,821.1) (1,660.8) 9.7% (5,243.8) (4,596.3) 14.1%

Gross Profit 1,105.0 1,012.2 9.2% 2,967.2 2,641.2 12.3%

Selling and Distribution Expenses (470.9) (418.3) 12.6% (1,378.4) (1,166.4) 18.2%

General and Administration Expenses (80.5) (85.3) (5.7%) (250.4) (239.2) 4.7%

EBIT 553.6 508.6 8.9% 1,338.4 1,235.6 8.3%

Share of Results of Associates (3.4) (3.9) (13.1%) (25.2) (21.6) 16.5%

Funding and Currency Costs (62.9) (41.3) 52.5% (159.8) (110.9) 44.1%

Income from Main Operations 487.3 463.4 5.2% 1,153.4 1,103.1 4.6%

Zakat and Income Tax (8.8) (14.6) (39.6%) (28.5) (35.6) (19.9%)

Income before Non Controlling

Interest478.5 448.8 6.6% 1,124.9 1,067.5 5.4%

Non Controlling Interest (2.9) 1.2 n.a 4.0 4.1 (2.2%)

Net Income 475.6 450.0 5.7% 1,128.9 1,071.6 5.4%

Earnings Per Share 0.80 0.75 1.89 1.79

Net Income % 16.3% 16.8% 13.7% 14.8%

3rd Quarter Year to Date 3rd Quarter

Segment Reporting

Almarai Company 11 2013 Q3 Earnings Presentation

SAR Mi l l ionDairy &

JuiceBakery Poultry

Arable and

Hort iculture

Other

Act ivi t ies

Almarai

Consol idated

Q3 YTD 2013

Sales 6,477.5 1,035.1 577.8 320.9 1.2 8,412.5

Third Party Sales 6,464.5 1,035.1 577.8 132.3 1.2 8,211.0

Depreciation (689.1) (100.6) (110.1) (54.2) (12.9) (966.9)

Income / (loss) before Non

Controlling Interest1,264.3 77.3 (212.3) 47.4 (51.7) 1,124.9

Total Assets 13,672.8 2,099.7 4,631.1 1,802.6 1,021.2 23,227.4

Total Liabilities (5,944.9) (671.4) (4,824.3) (246.7) (1,145.9) (12,833.2)

Return on Sales 19.6% 7.5% (36.7%) 35.8% n.a. 13.7%

Growth versus Q3 YTD 2012

- Third Party Sales 10.1% 12.4% 69.0% 27.3% n.a. 13.5%

- Income / (loss) before Non

Controlling Interest20.5% 15.0% 231.6% 8.2% 82.1% 5.4%

Q3 2013

Sales 2,354.1 324.8 212.9 120.2 0.3 3,012.4

Third Party Sales 2,354.1 324.8 212.9 34.0 0.3 2,926.1

Depreciation (225.5) (37.1) (49.2) (18.4) (5.2) (335.4)

Income / (loss) before Non

Controlling Interest556.4 11.7 (75.1) 1.7 (16.2) 478.5

Return on Sales 23.6% 3.6% (35.3%) 5.0% n.a. 16.4%

Growth versus Q3 2012

- Third Party Sales 6.9% 7.2% 67.1% (14.3%) n.a. 9.5%

- Income / (loss) before Non

Controlling Interest29.4% (21.3%) 303.9% (94.5%) 83.1% 6.6%

Trend charts

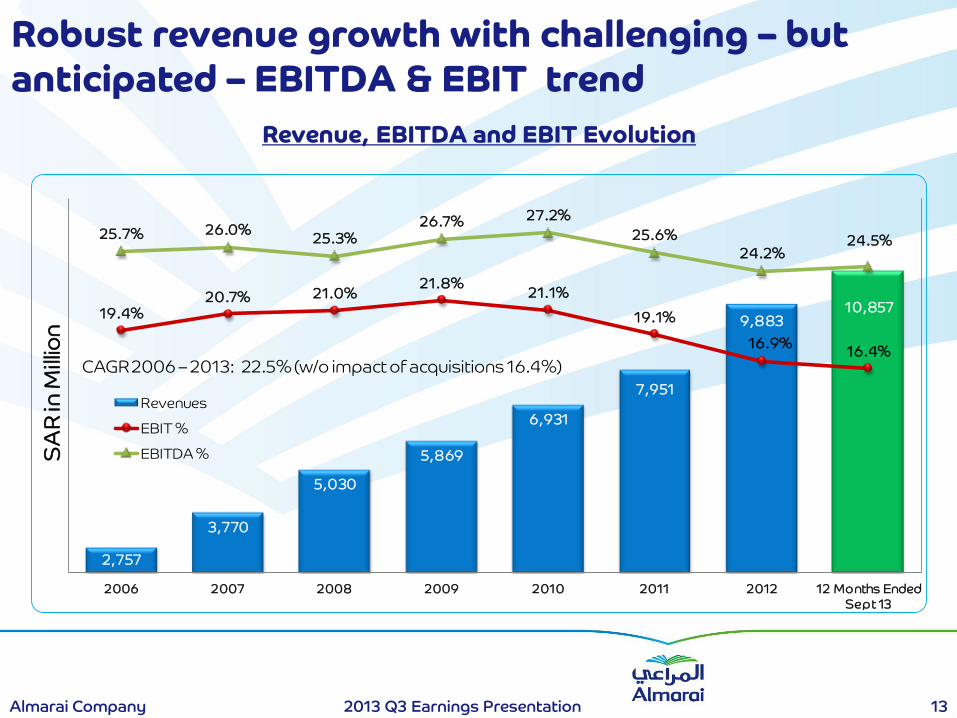

Robust revenue growth with challenging – but

anticipated – EBITDA & EBIT trend

Almarai Company 13 2013 Q3 Earnings Presentation

Revenue, EBITDA and EBIT Evolution

2,757

3,770

5,030

5,869

6,931

7,951

9,88310,85719.4%

20.7% 21.0%21.8%

21.1%

19.1%

16.9%16.4%

25.7% 26.0%25.3%

26.7% 27.2%

25.6%

24.2%24.5%

2006 2007 2008 2009 2010 2011 2012 12 Months Ended

Sept 13

SA

R in

Mill

ion

Revenues

EBIT %

EBITDA %

CAGR 2006 – 2013: 22.5% (w/o impact of acquisitions 16.4%)

Quarterly Performance – Net Income

Almarai Company 14 2013 Q3 Earnings Presentation

90

.6

12

2.8

16

2.2

19

7.4

23

4.1

23

5.2

24

2.1

25

5.1

12

1.8

16

5.3

23

5.2

28

7.1

34

3.1

34

9.3

37

9.5

39

8.2

12

2.6

18

6.1

29

3.7

36

3.4

42

4.5

42

9.7

45

0.0

47

5.6

13

0.2

19

3.1

21

9.2

24

8.8

28

3.5

28

5.5

36

9.0

0

50

100

150

200

250

300

350

400

450

SA

R M

illio

n

Q2 = 4.9%

2013 versus 2012

Q1 = 5.4%

Q3 = 5.7%

Cash Flows

Cash Flow Statement (YTD Q3 2013)

Almarai Company 16 2013 Q3 Earnings Presentation

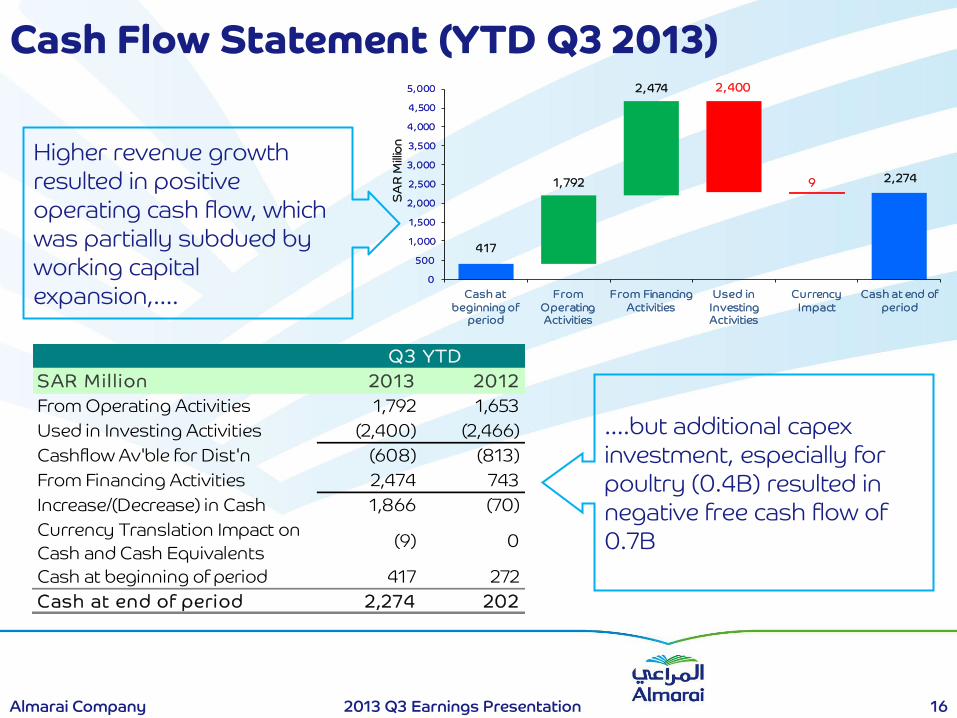

Higher revenue growth

resulted in positive

operating cash flow, which

was partially subdued by

working capital

expansion,….

….but additional capex

investment, especially for

poultry (0.4B) resulted in

negative free cash flow of

0.7B

417

1,792

2,474 2,400

9 2,274

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Cash at

beginning of period

From

Operating Activities

From Financing

Act ivities

Used in

Investing Activities

Currency

Impact

Cash at end of

period

SA

R M

illio

n

SAR Mi l l ion 2013 2012

From Operating Activities 1,792 1,653

Used in Investing Activities (2,400) (2,466)

Cashflow Av'ble for Dist'n (608) (813)

From Financing Activities 2,474 743

Increase/(Decrease) in Cash 1,866 (70)

Currency Translation Impact on

Cash and Cash Equivalents(9) 0

Cash at beginning of period 417 272

Cash at end of period 2,274 202

Q3 YTD

Cash Flow Bridge – rolling 12 months

Almarai Company 17 2013 Q3 Earnings Presentation

202

2,875

1,700

1,300 4 (3,073)

(494)

(240)2,274

Cash at 30 Sept 2012

Operating Cash Flow

Capex

Dividend

Others

Cash at 30 Sept 2013

+ SAR 2,072 m

Loans Issues /

Payments /

Others

Equity Issued -

Perpetual

Sukuk

Bank Loan -Sukuk

Balance Sheet

Balance Sheet

Almarai Company 19 2013 Q3 Earnings Presentation

SAR Mi l l ion 30/09/13 30/09/12

1,456 1,381

966 883

14,614 12,849

17,036 15,113

1,335 1,383

373 300

18,744 16,796

7,920 8,421

324 279

106 129

10,394 7,968

18,744 16,796

76.2% 105.7%

Total Equity

Net Capital Employed

Net Debt to Equity Ratio

Intangible Assets - Goodwill

Investment & Financial Assets, Deferred

Charges and Derivatives

Net Debt

End of Service Benefits

Deferred Tax (Net)

Net Operating Working Capital

Biological Assets

Property, Plant and Equipment

Net Operating Assets

Perpetual Sukuk

Almarai Company 20 2013 Q3 Earnings Presentation

On 24 Dhul Qadah 1434 A.H. (30 September 2013), the Company issued its first Perpetual Sukuk - Series 1 amounting to SAR 1,700.0 million at a par value of SAR 1 million each without discount or premium, bearing a return based on SIBOR plus a pre-determined margin. The Company may redeem the Perpetual Sukuk, in full or in part, at its own discretion and may defer, in full or in part, payment of any profit distribution at its own discretion. The Company is not subject to any limitation on the number of times that it may defer such payment at its own discretion and such deferral is not considered as an event of default. The Perpetual Sukuk rank in priority to all subordinated obligations and the ordinary share capital of the Company. These Sukuk do not carry the right to vote, however each sukukholder participates in the Sukuk Assets. The terms of the Sukuk entitle the Company to commingle its own assets with the Sukuk Assets. Sukuk Assets comprise the sukukholders’ share in the Mudaraba Assets and the sukukholders’ interest in the Murabaha Transaction, together with any amounts standing to the credit of the Sukuk account and the Reserve retained by the Company from the Sukuk account.

Net Debt

Almarai Company 21 2013 Q3 Earnings Presentation

1,320 2,454 3,398 3,869 4,606 6,653 8,237 7,920

70% 80%

94%

72% 74%

98% 101%

76%

1.7x 1.9x

2.3x 2.3x 2.2x

2.8x

3.1x

3.0x

0%

50%

100%

150%

200%

250%

300%

350%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2006 2007 2008 2009 2010 2011 2012 Last 12

months

Net Debt Net Debt / Equity Ratio Net Debt / EBITDA

in m

illio

nS

AR

Debt Profile highlights balanced approach for

funding….

Almarai Company 22 2013 Q3 Earnings Presentation

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

<1yr 1-2 yr 2-3yr 3-4 yr 4-5yr >5yr

SA

R B

illio

n

Debt Maturity by Age and Type

Islamic Bonds

Govt / Semi Govt Inst.

Banks

7.1, 69%0.8, 8%

2.3, 23%

Capital Expenditure

Capex spend in line with Guidance…

Almarai Company 24 2013 Q3 Earnings Presentation

Capex spend of 2.1B SAR, which is in line for with our earlier forecast of 3.1B SAR for the full year

2013.

Poultry capex spend for the first three quarter

amounted to more than 0.7B SAR. The key

highlight for the first three quarters is the

commercial start of the first line in Q1 and second

line in Q2 as previously communicated.

Sales depot and logistics expansion accounted for

~0.5B SAR for the first three quarters, resulting in

our our growing foot print across the GCC.

Manufacturing and Farming consumed capex of

~0.3B SAR each for various capacity expansion

projects

Replacement and other capex including IDJ,

accounted for another 0.3B SAR.

0%

50%

100%

150%

200%

250%

300%

Almarai TASI

Key Share Data

Almarai Company 25 2013 Q3 Earnings Presentation

Key Stat ist ics for Almarai (28 Sept 2013)

Current P/E Rat io (ttm) 22.6

Est imated P/E(12/2013) 22.2

Earnings Per Share (SAR) (ttm) 2.5

Market Cap (M SAR) 33,298

Shares Outstanding (M) 600.0

30 Day Average Volume 1,006,677

Dividend Indicated Gross Yield 1.5%

Cash Dividend (SAR) 0.8

Last Dividend 4/3/2013

5 Year Dividend Growth 11.7%

Thank you

Almarai Company

Exit 7, North Circle Road

Al Izdihar District

P.O. Box 8524

Riyadh, 11492

Saudi Arabia

Contact for investor relations matters:

Khalid M. Al Nasser

+966 11 470 00 05 ext 1280