CPA P1 Corporate Reporting

1 © Cenit Online 2015

TOPIC 40_41 - IAS 7 STATEMENT OF CASHFLOWS

a) Overview Notes

b) Statement of Cashflows V.S Statement of profit or loss

c) Interpreting Statement of Cashflows

d) Miscellaneous Points on Statement of Cashflows

e) Consolidated Statements of Cashflow

CPA P1 Corporate Reporting

2 © Cenit Online 2015

(a) OVERVIEW NOTES

CPA P1 Corporate Reporting

3 © Cenit Online 2015

CPA P1 Corporate Reporting

4 © Cenit Online 2015

CPA P1 Corporate Reporting

5 © Cenit Online 2015

CPA P1 Corporate Reporting

6 © Cenit Online 2015

CPA P1 Corporate Reporting

7 © Cenit Online 2015

CPA P1 Corporate Reporting

8 © Cenit Online 2015

CPA P1 Corporate Reporting

9 © Cenit Online 2015

CPA P1 Corporate Reporting

10 © Cenit Online 2015

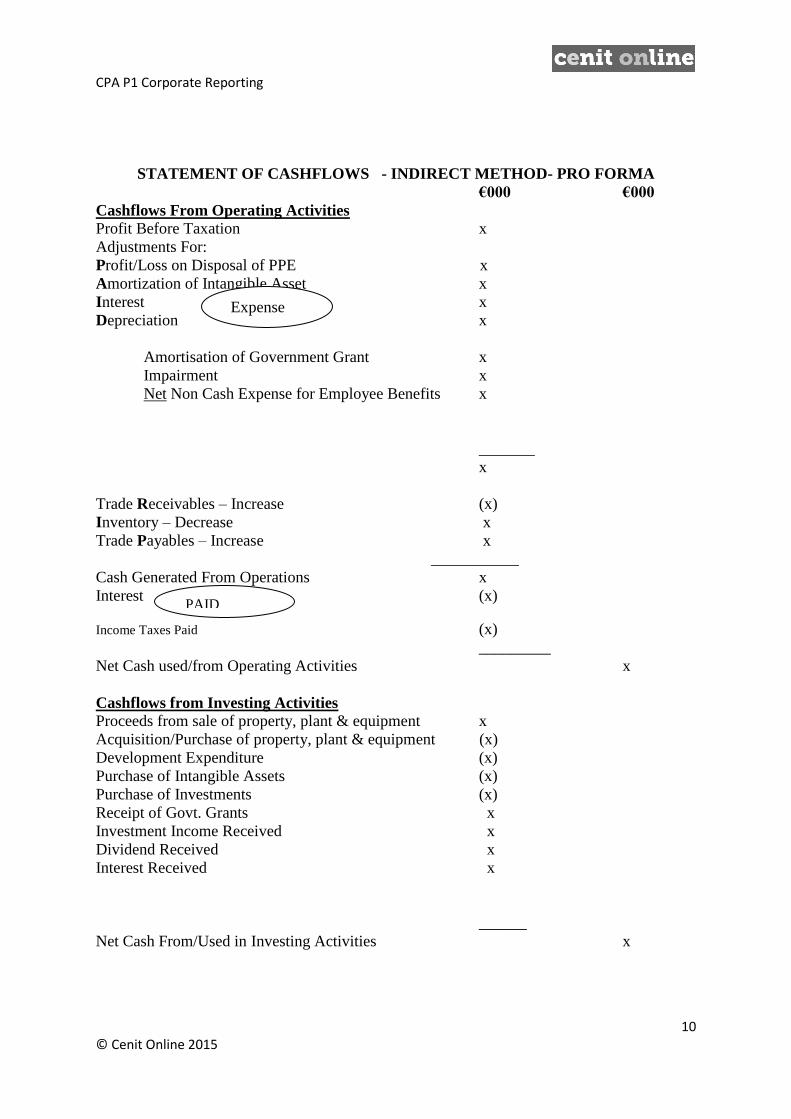

STATEMENT OF CASHFLOWS - INDIRECT METHOD- PRO FORMA

€000 €000

Cashflows From Operating Activities

Profit Before Taxation x

Adjustments For:

Profit/Loss on Disposal of PPE x

Amortization of Intangible Asset x

Interest x

Depreciation x

Amortisation of Government Grant x

Impairment x

Net Non Cash Expense for Employee Benefits x

_______

x

Trade Receivables – Increase (x)

Inventory – Decrease x

Trade Payables – Increase x

___________

Cash Generated From Operations x

Interest (x)

Income Taxes Paid (x)

_________

Net Cash used/from Operating Activities x

Cashflows from Investing Activities

Proceeds from sale of property, plant & equipment x

Acquisition/Purchase of property, plant & equipment (x)

Development Expenditure (x)

Purchase of Intangible Assets (x)

Purchase of Investments (x)

Receipt of Govt. Grants x

Investment Income Received x

Dividend Received x

Interest Received x

______

Net Cash From/Used in Investing Activities x

Expense

PAID

CPA P1 Corporate Reporting

11 © Cenit Online 2015

€000 €000

Cashflows from Financing Activities

Proceeds from Issue of Share Capital x

Proceeds from Issue of Loan/Debentures x

Repayment/Redemption of Loan/Debentures (x)

Payment of Finance Lease Obligations (Capital) (x)

Dividend Paid (x)

________

Net Cash Used/From Financing Activities x

_____________

Net Increase/Decrease in Cash & Cash Equivalents

(Derived from Info Given in Question) x

Cash & Cash Equivalents at Beginning of Period (From Question) x

_____________

Cash & Cash Equivalents at End of Period (From Question) x

CPA P1 Corporate Reporting

12 © Cenit Online 2015

(b) Statement of Cashflows VS Statement of profit or loss

“Cash is King”

an entity profit for a period differs from its cashflow because

1. Statement of profit or loss and SOFP are prepared on an accrual basis (i.e. we

match income and expense to the periods they relate to irrespective of which

they are actually paid and received).

2. Cashflows are not affected by an entity accounting policies.

Reasons Why Cashflow Information is Useful

1. Cashflows are factual and are therefore difficult to change/manipulate.

2. Cashflow Information for the current period can be used as a basis for

predicting future cashflows.

3. Cashflow is easier to understand than profit, especially for non business

people.

4. If the statement of cashflows is prepared using the indirect method, it shows

the relationship between an entity’s profit and its cash generating ability by

reconciling profit before tax to cash generated from operating activities.

Seeing this link is of benefit to users of Statement of Cashflows as it gives an

indication of the quality of the entity’s earnings (aka profits).

Limitations of Cashflow Information

1. Cash balances are measured at a specific point in time so management of a

company could arrange transactions so that the cash balance is affected as

little as possible e.g. lease an asset rather than outright purchase.

2. Management could also delay paying suppliers until after the year end to

preserve cash balances for the preparation of the Statement of Cashflows.

3. Cashflow is not the same as earnings/profits. Cash is important in the short

term, but profits are also needed for long term survival.

CPA P1 Corporate Reporting

13 © Cenit Online 2015

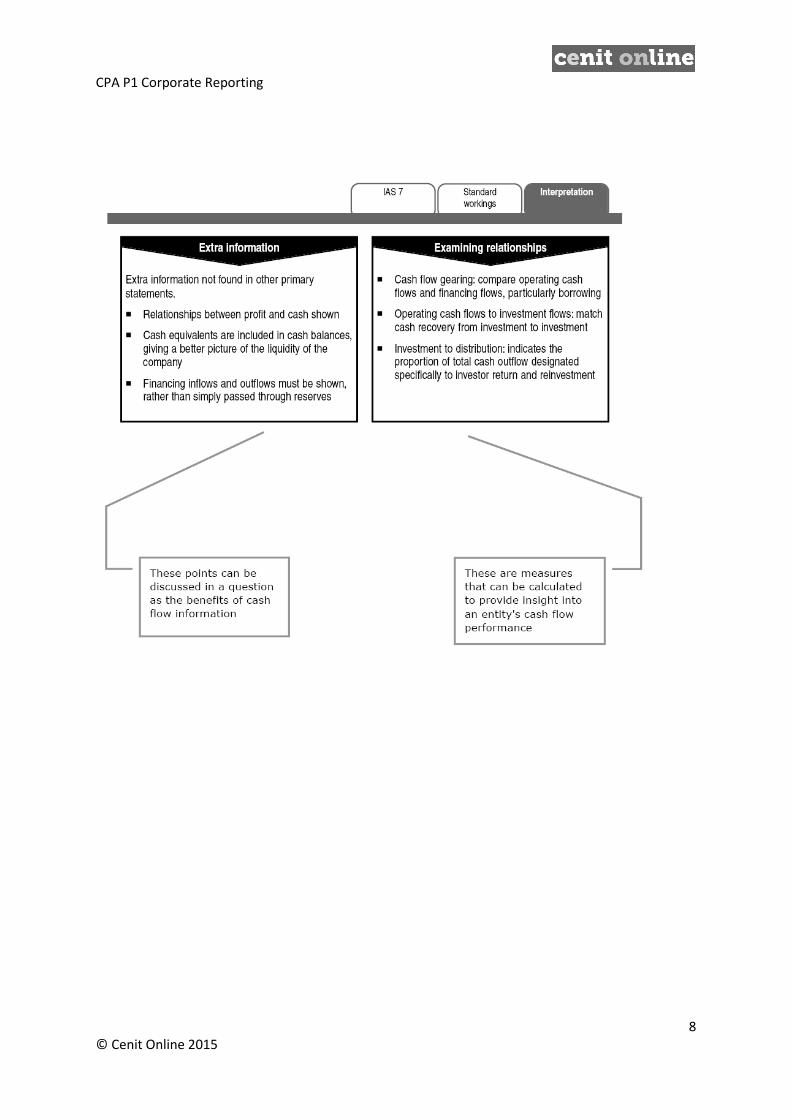

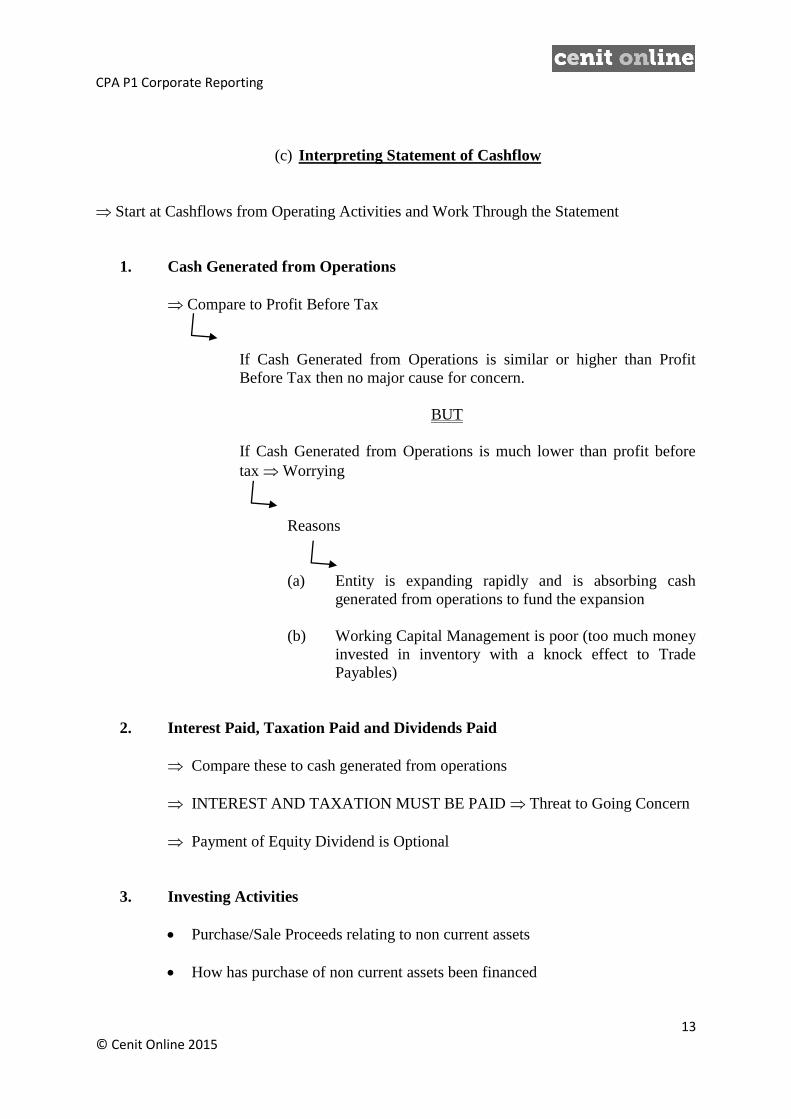

(c) Interpreting Statement of Cashflow

Start at Cashflows from Operating Activities and Work Through the Statement

1. Cash Generated from Operations

Compare to Profit Before Tax

If Cash Generated from Operations is similar or higher than Profit

Before Tax then no major cause for concern.

BUT

If Cash Generated from Operations is much lower than profit before

tax Worrying

Reasons

(a) Entity is expanding rapidly and is absorbing cash

generated from operations to fund the expansion

(b) Working Capital Management is poor (too much money

invested in inventory with a knock effect to Trade

Payables)

2. Interest Paid, Taxation Paid and Dividends Paid

Compare these to cash generated from operations

INTEREST AND TAXATION MUST BE PAID Threat to Going Concern

Payment of Equity Dividend is Optional

3. Investing Activities

Purchase/Sale Proceeds relating to non current assets

How has purchase of non current assets been financed

CPA P1 Corporate Reporting

14 © Cenit Online 2015

Cash/Share Issue/Long Term Borrowing

(Link to Financing Section of Statement of Cashflows)

A purchase of non current assets may experience a time lag before the

increased investment reaches its full beneficial effect

If an entity has financed the purchase of non current assets from a short term

source of finance (e.g. a bank overdraft) this could put a lot of strain on the

cash resources of the company and again thereafter going concern.

4. Financing Activities

If borrowings have increased, will the entity have enough cash to meet

additional interest payments in the future??

Are there any penalties for the entity if it repays borrowings early??

What is the level of gearing in the company??

5. Increase/Decrease in Cash and Cash Balances

A decrease Did the company repay a loan

An Increase Could the excess cash be invested elsewhere at a profit.

If the company has a closing overdraft, how close is it to its overdraft limit??

Does the entity have enough cash to cover

Current liabilities (tax and interest)

The current level of dividends (optional)

Any plans for expansion of the business

Any other spending commitments

Borrowings to be repaid in the next 12 months

General Points Re Answering Theory on Statement of Cashflows

BULLET POINT ANSWERS

CLEAR HANDWRITING

USE OF TERMINOLOGY/KEYWORDS

DO NOT NEGLECT THE THEORY ASPECTS

CPA P1 Corporate Reporting

15 © Cenit Online 2015

“CASHFLOWS FROM OPERATING ACTIVITIES”

Operating Activities are the Principal Revenue Generating Activities of

an Entity

e.g. Brown Thomas selling clothes and cosmetics

Fyffes cashflows earned from selling fruit

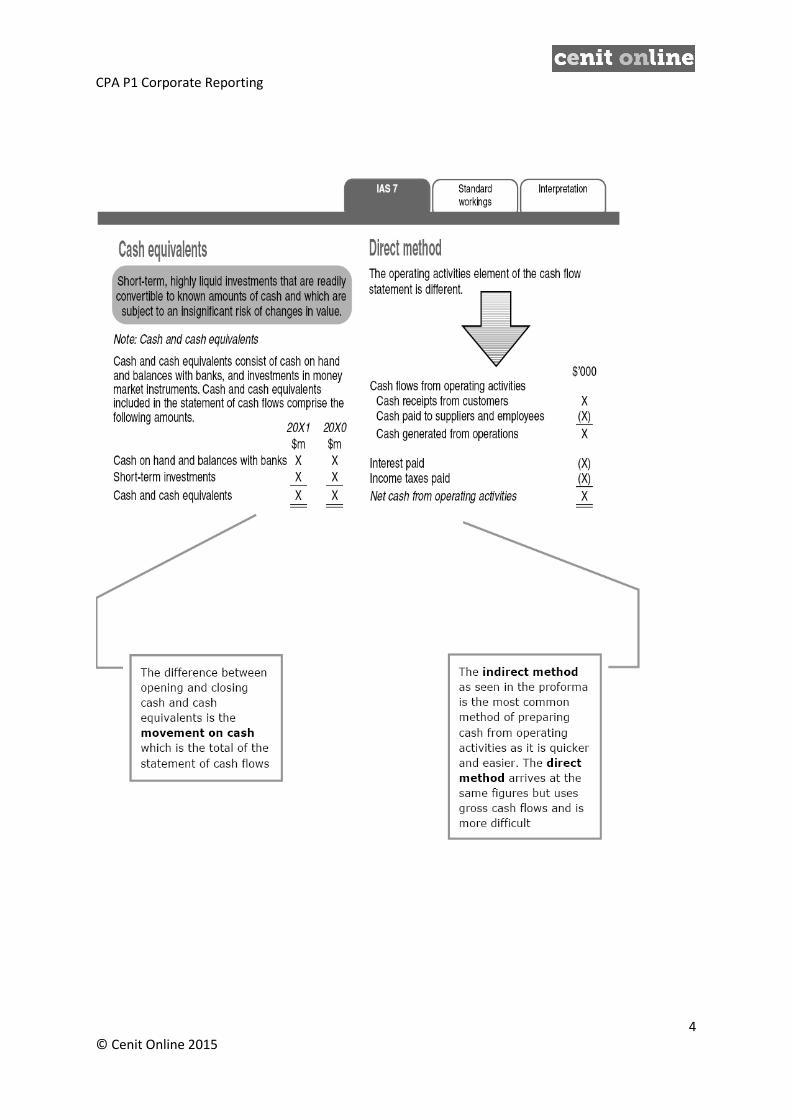

“CASH AND CASH EQUIVALENTS”

CASH: Cash in Hand, Cash in Bank and Cash Equivalents

CASH EQUIVALENTS: Include, short term highly liquid investments

that are easily convertible into cash and are subject to insignificant risk of

changes in value. (Note: Short Term Equity Investments are not cash

equivalents because they are exposed to significant changes in value i.e.

Market movements)

CPA P1 Corporate Reporting

16 © Cenit Online 2015

(d) Miscellaneous Points on Statement of Cashflows

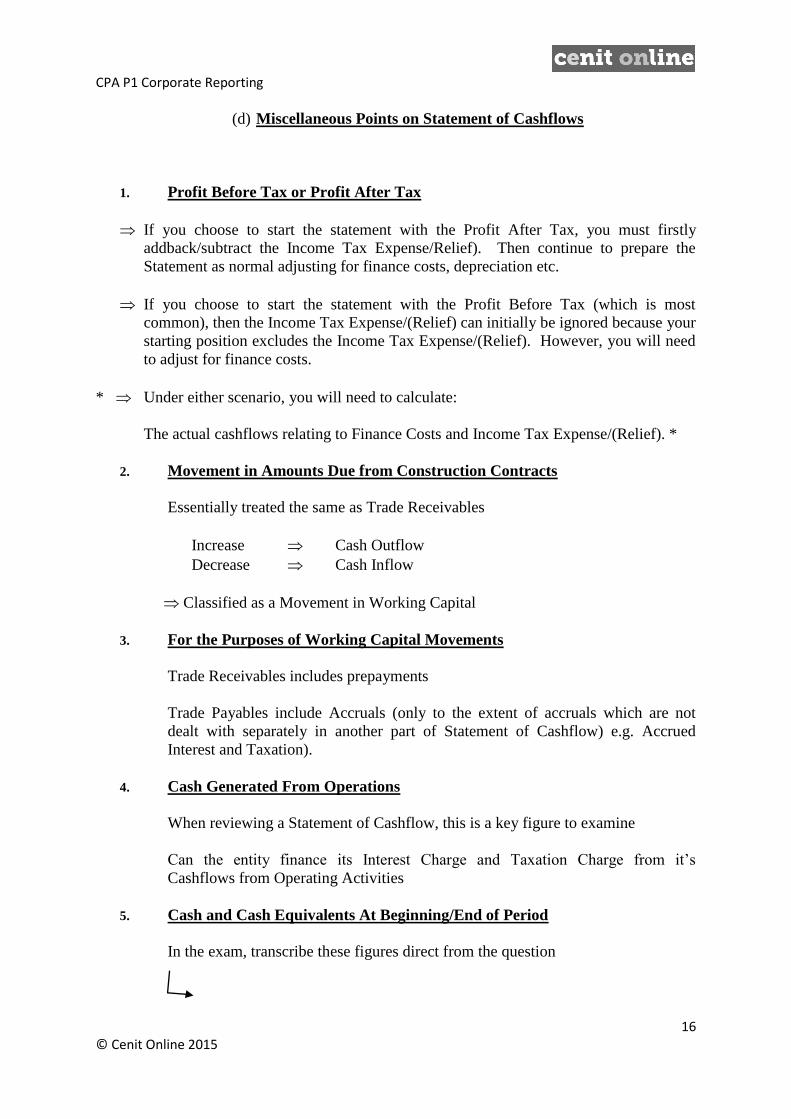

1. Profit Before Tax or Profit After Tax

If you choose to start the statement with the Profit After Tax, you must firstly

addback/subtract the Income Tax Expense/Relief). Then continue to prepare the

Statement as normal adjusting for finance costs, depreciation etc.

If you choose to start the statement with the Profit Before Tax (which is most

common), then the Income Tax Expense/(Relief) can initially be ignored because your

starting position excludes the Income Tax Expense/(Relief). However, you will need

to adjust for finance costs.

* Under either scenario, you will need to calculate:

The actual cashflows relating to Finance Costs and Income Tax Expense/(Relief). *

2. Movement in Amounts Due from Construction Contracts

Essentially treated the same as Trade Receivables

Increase Cash Outflow

Decrease Cash Inflow

Classified as a Movement in Working Capital

3. For the Purposes of Working Capital Movements

Trade Receivables includes prepayments

Trade Payables include Accruals (only to the extent of accruals which are not

dealt with separately in another part of Statement of Cashflow) e.g. Accrued

Interest and Taxation).

4. Cash Generated From Operations

When reviewing a Statement of Cashflow, this is a key figure to examine

Can the entity finance its Interest Charge and Taxation Charge from it’s

Cashflows from Operating Activities

5. Cash and Cash Equivalents At Beginning/End of Period

In the exam, transcribe these figures direct from the question

CPA P1 Corporate Reporting

17 © Cenit Online 2015

i.e. Bank/Bank Overdraft Figures and any Cash Equivalents like Deposit

Accounts.

Do not depend on your Worked Solution to get the figure for “Cash and Cash

Equivalents at end of Period”.

And from doing the above, you will derive your figure for “ Net

Increase/Decrease in Cash & Cash Equivalents” (Do not depend on your

worked solution)

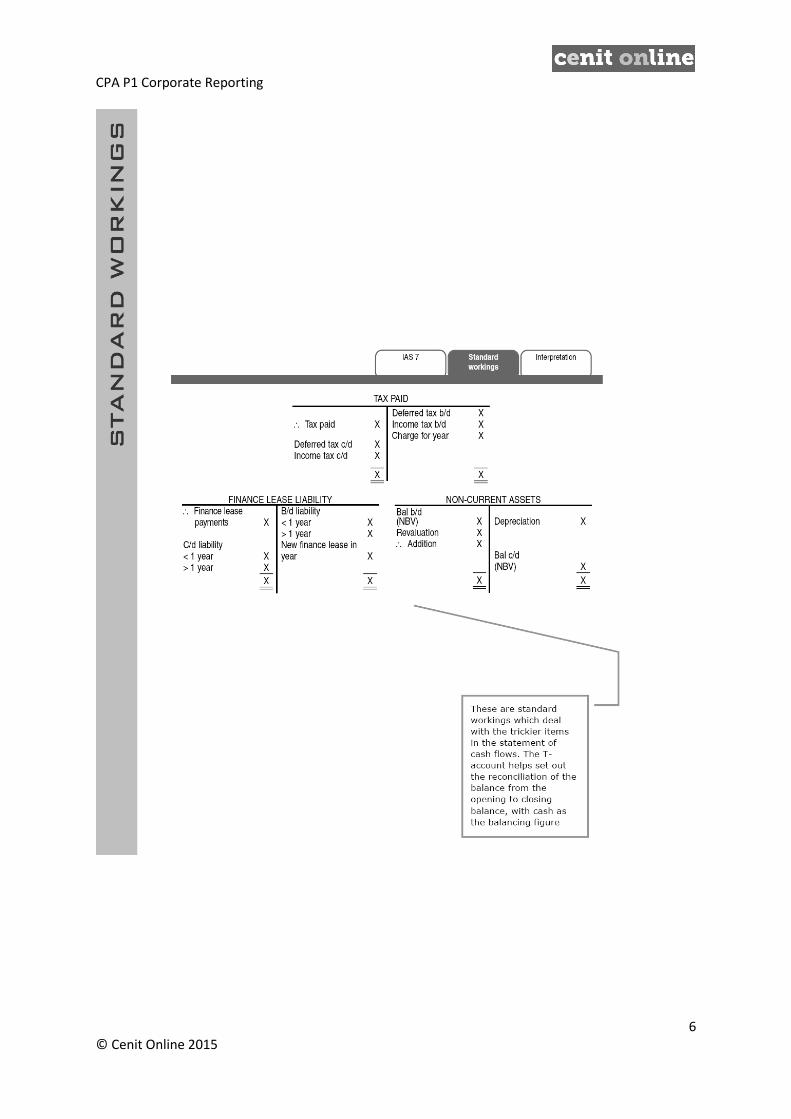

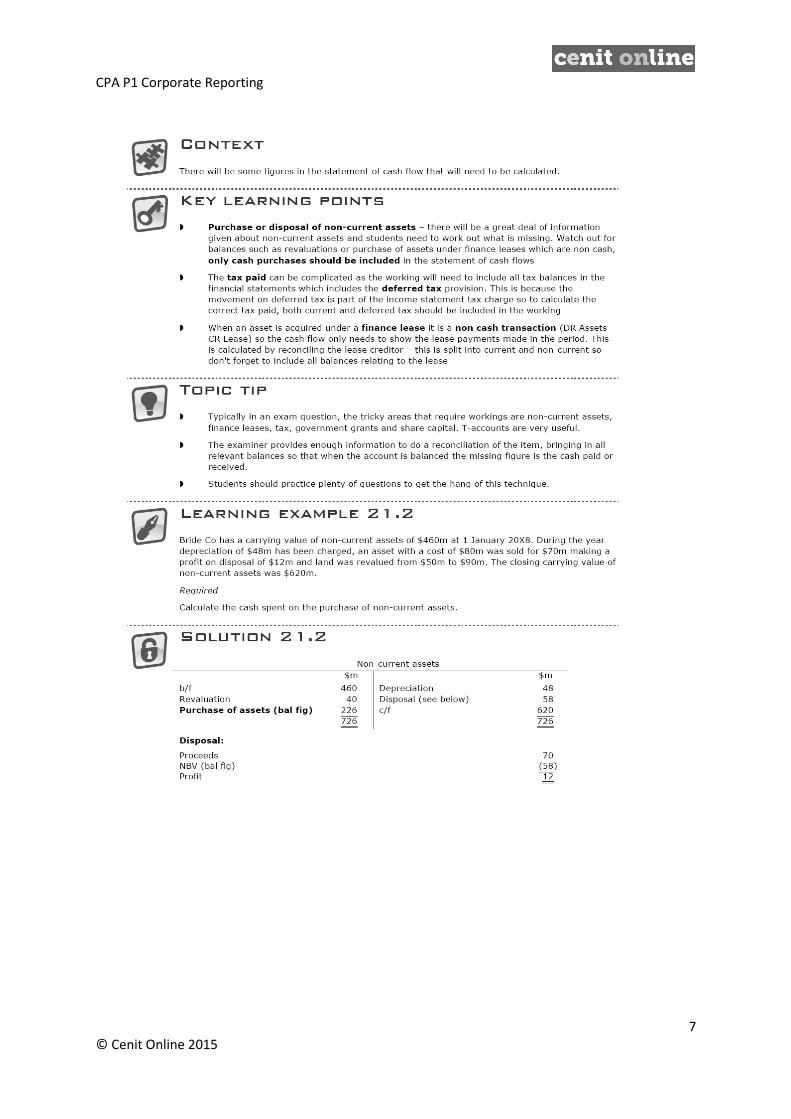

6. Finance Leases

Where the reporting entity uses an asset held under a finance lease, the

amounts to go in the statement of cash flows as financing activities are repayments of

capital only (plus any deposit paid). The interest paid will be shown under

operating activities

Finance Lease Example: The notes to the financial statements of Hayley Co show the

following in respect of obligations under finance leases

Year Ended 30 June 2005 2004

$000 $000

Amounts Payable Within 1 Year 12 8

Within 2 to 5 Years 110 66

Less: Finance Charges Allocated to

Future Periods - 14 - 8

108 66

Additions to tangible non current assets acquired under finance leases were shown in

the non current asset note at $56,000

Required: Calculate the capital repayment to be shown in the statement of cash flows

of Hayley Co for the year to 30 June 2005

Obligations Under Finance Lease

1.7.04 Bal Bd 66

Capital Repaid (Plug) 14

30.6.05 Additions 56

30.6.05 Bal C/d 108

122 122

CPA P1 Corporate Reporting

18 © Cenit Online 2015

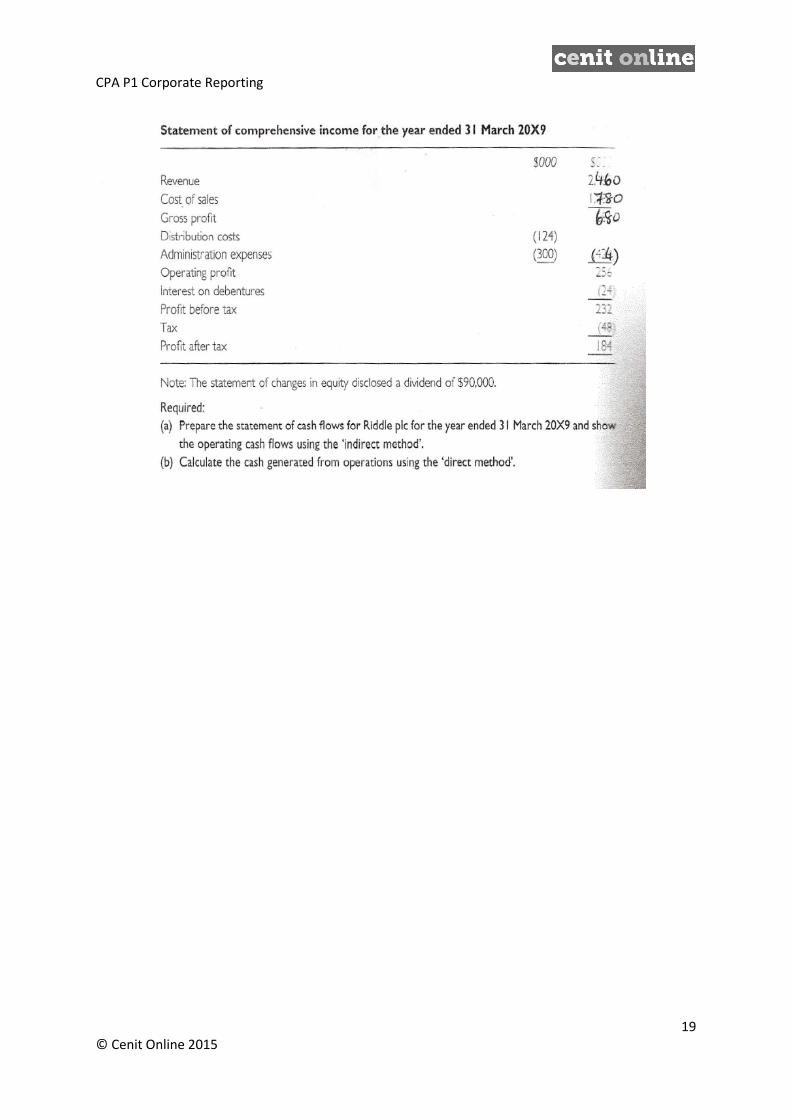

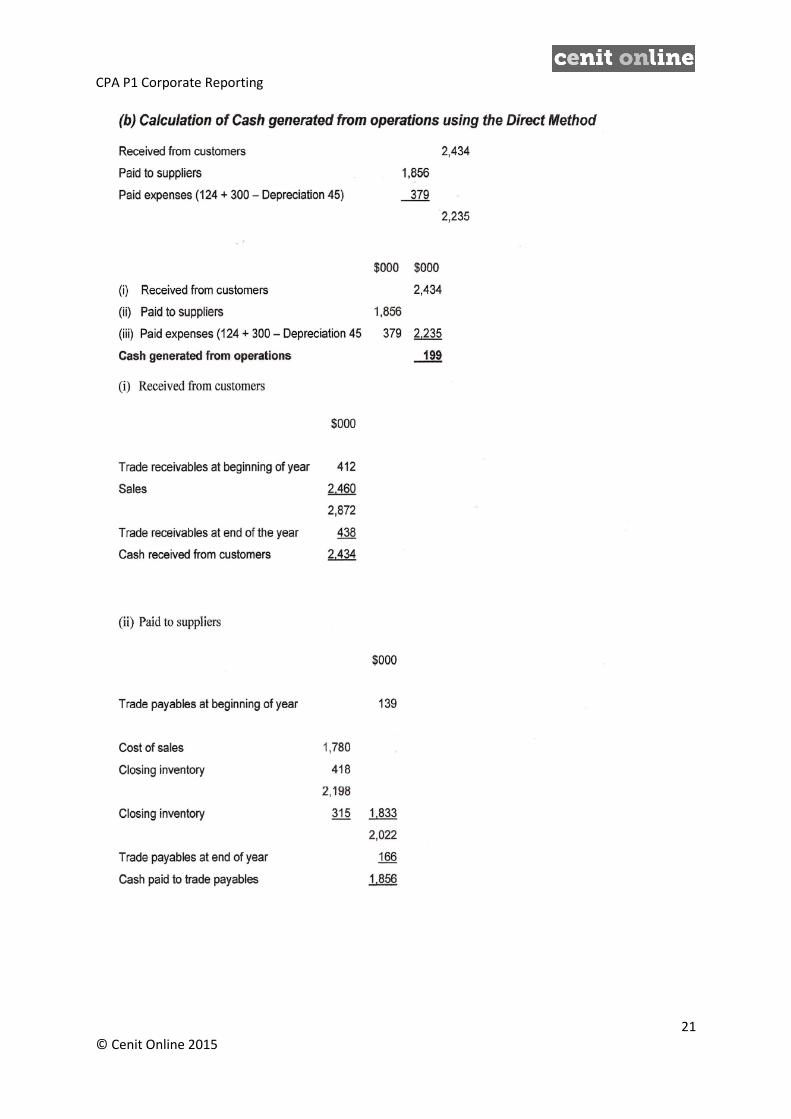

INDIRECT & DIRECT METHOD OF PRESENTING CASH GENERATED FROM

OPERATIONS – IAS 7

CPA P1 Corporate Reporting

19 © Cenit Online 2015

CPA P1 Corporate Reporting

20 © Cenit Online 2015

CPA P1 Corporate Reporting

21 © Cenit Online 2015

CPA P1 Corporate Reporting

22 © Cenit Online 2015

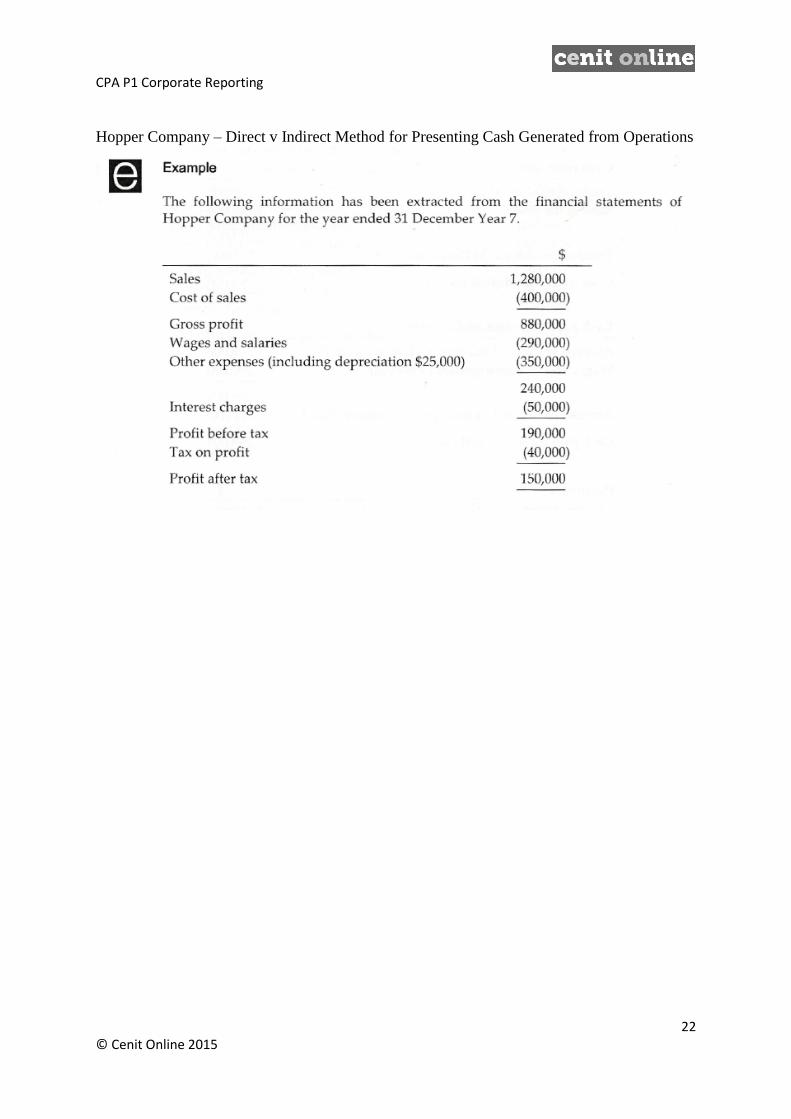

Hopper Company – Direct v Indirect Method for Presenting Cash Generated from Operations

CPA P1 Corporate Reporting

23 © Cenit Online 2015

CPA P1 Corporate Reporting

24 © Cenit Online 2015

CPA P1 Corporate Reporting

25 © Cenit Online 2015

CPA P1 Corporate Reporting

26 © Cenit Online 2015

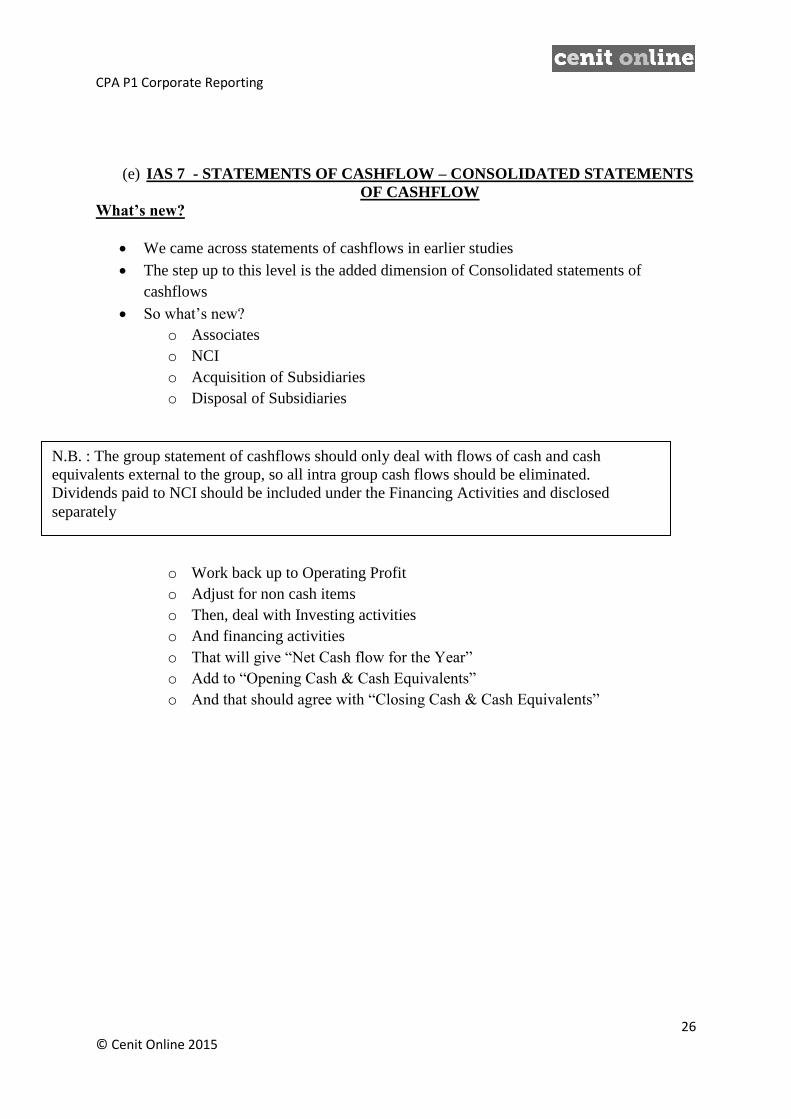

(e) IAS 7 - STATEMENTS OF CASHFLOW – CONSOLIDATED STATEMENTS

OF CASHFLOW

What’s new?

We came across statements of cashflows in earlier studies

The step up to this level is the added dimension of Consolidated statements of

cashflows

So what’s new?

o Associates

o NCI

o Acquisition of Subsidiaries

o Disposal of Subsidiaries

Remember the Layout?

o Start with profit before tax

o Work back up to Operating Profit

o Adjust for non cash items

o Then, deal with Investing activities

o And financing activities

o That will give “Net Cash flow for the Year”

o Add to “Opening Cash & Cash Equivalents”

o And that should agree with “Closing Cash & Cash Equivalents”

N.B. : The group statement of cashflows should only deal with flows of cash and cash

equivalents external to the group, so all intra group cash flows should be eliminated.

Dividends paid to NCI should be included under the Financing Activities and disclosed

separately

CPA P1 Corporate Reporting

27 © Cenit Online 2015

CONSOLIDATED STATEMENT OF CASHFLOWS - INDIRECT METHOD- PRO

FORMA

€000 €000

Cashflows From Operating Activities

Profit Before Taxation x

Adjustments For:

Profit/Loss on Disposal of PPE (x)

Amortization of Intangible Asset x

Interest x

Depreciation x

Amortisation of Government Grant x

Impairment (Consol Goodwill) x

Share of Profit (Loss) of Associate x

Gain/Loss on Disposal of Subsidary x

_______

x

Trade Receivables – Increase (x)

Inventory – Decrease x

Trade Payables – Increase x

___________

Cash Generated From Operations x

Interest (x)

Income Taxes Paid (x)

_________

Net Cash used/from Operating Activities x

Cashflows from Investing Activities

Proceeds from sale of property, plant & equipment x

Acquisition/Purchase of property, plant & equipment (x)

Development Expenditure (x)

Purchase of Intangible Assets (x)

Purchase of Investments (x)

Receipt of Govt. Grants x

Investment Income Received x

Dividend Received x

Interest Received x

Dividend from Associate x

Acquisition Cost /Disposal Proceeds of Subsidary x

______

Net Cash From/Used in Investing Activities x

Expense

Paid

CPA P1 Corporate Reporting

28 © Cenit Online 2015

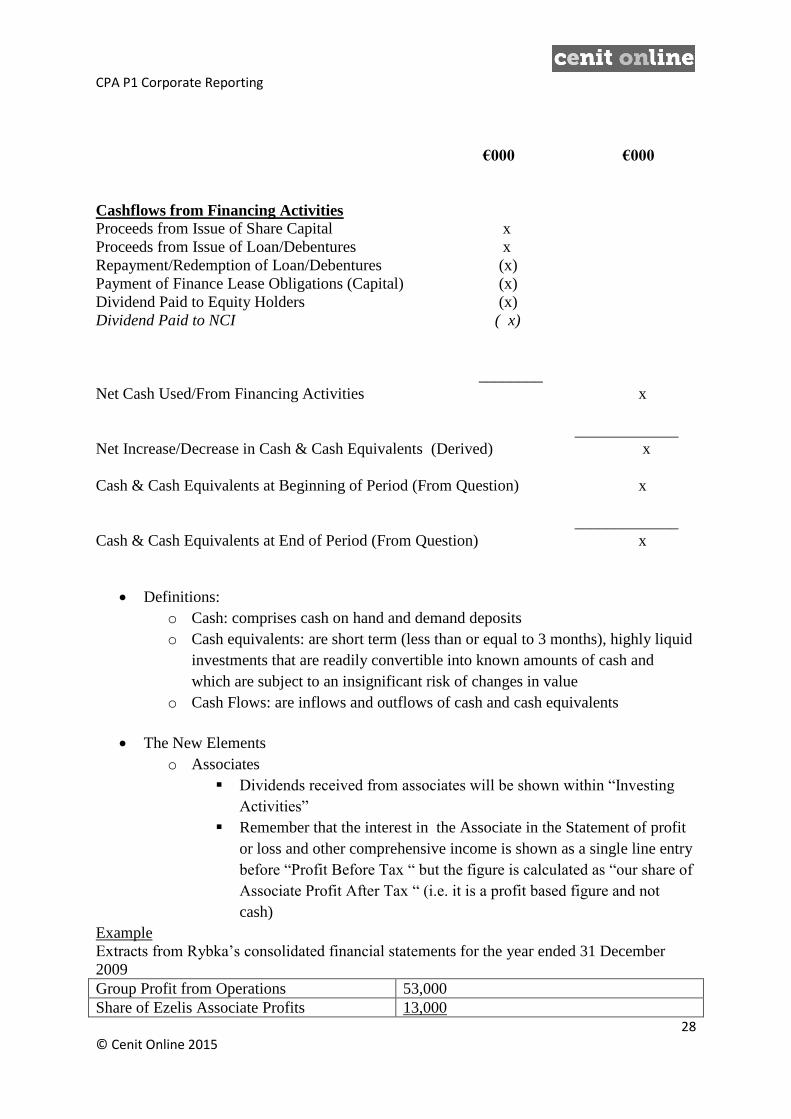

€000 €000

Cashflows from Financing Activities

Proceeds from Issue of Share Capital x

Proceeds from Issue of Loan/Debentures x

Repayment/Redemption of Loan/Debentures (x)

Payment of Finance Lease Obligations (Capital) (x)

Dividend Paid to Equity Holders (x)

Dividend Paid to NCI ( x)

________

Net Cash Used/From Financing Activities x

_____________

Net Increase/Decrease in Cash & Cash Equivalents (Derived) x

Cash & Cash Equivalents at Beginning of Period (From Question) x

_____________

Cash & Cash Equivalents at End of Period (From Question) x

Definitions:

o Cash: comprises cash on hand and demand deposits

o Cash equivalents: are short term (less than or equal to 3 months), highly liquid

investments that are readily convertible into known amounts of cash and

which are subject to an insignificant risk of changes in value

o Cash Flows: are inflows and outflows of cash and cash equivalents

The New Elements

o Associates

Dividends received from associates will be shown within “Investing

Activities”

Remember that the interest in the Associate in the Statement of profit

or loss and other comprehensive income is shown as a single line entry

before “Profit Before Tax “ but the figure is calculated as “our share of

Associate Profit After Tax “ (i.e. it is a profit based figure and not

cash)

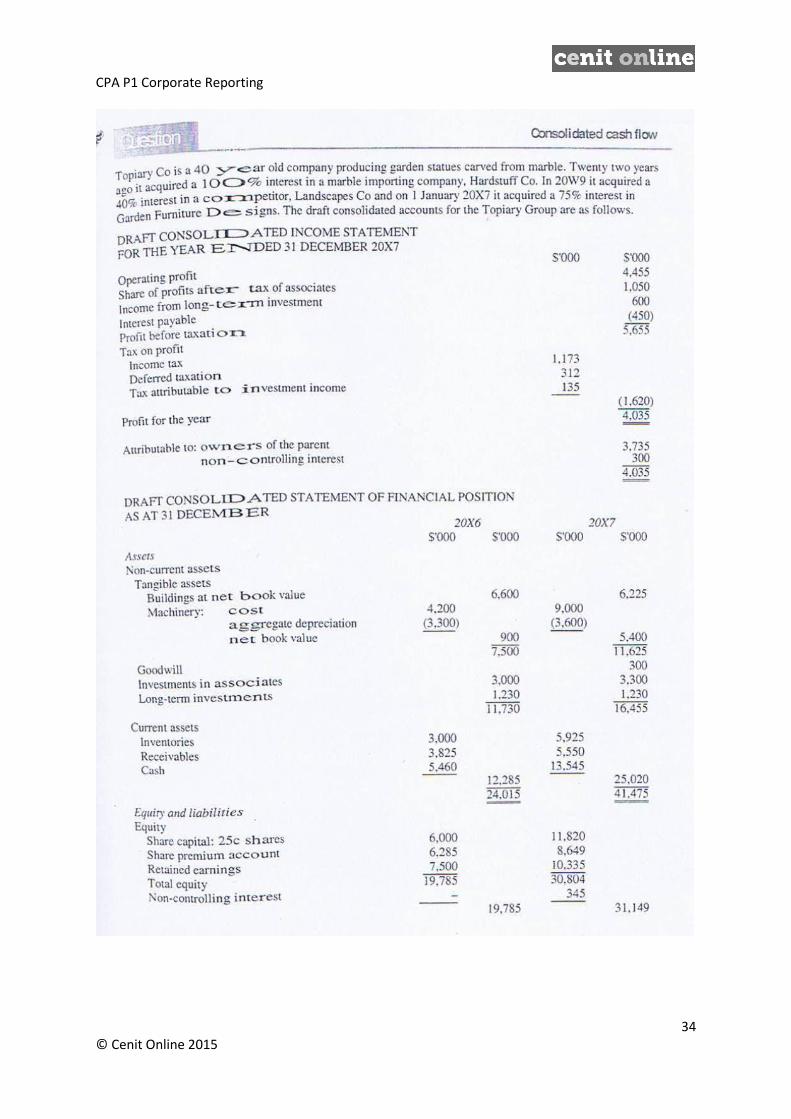

Example

Extracts from Rybka’s consolidated financial statements for the year ended 31 December

2009

Group Profit from Operations 53,000

Share of Ezelis Associate Profits 13,000

CPA P1 Corporate Reporting

29 © Cenit Online 2015

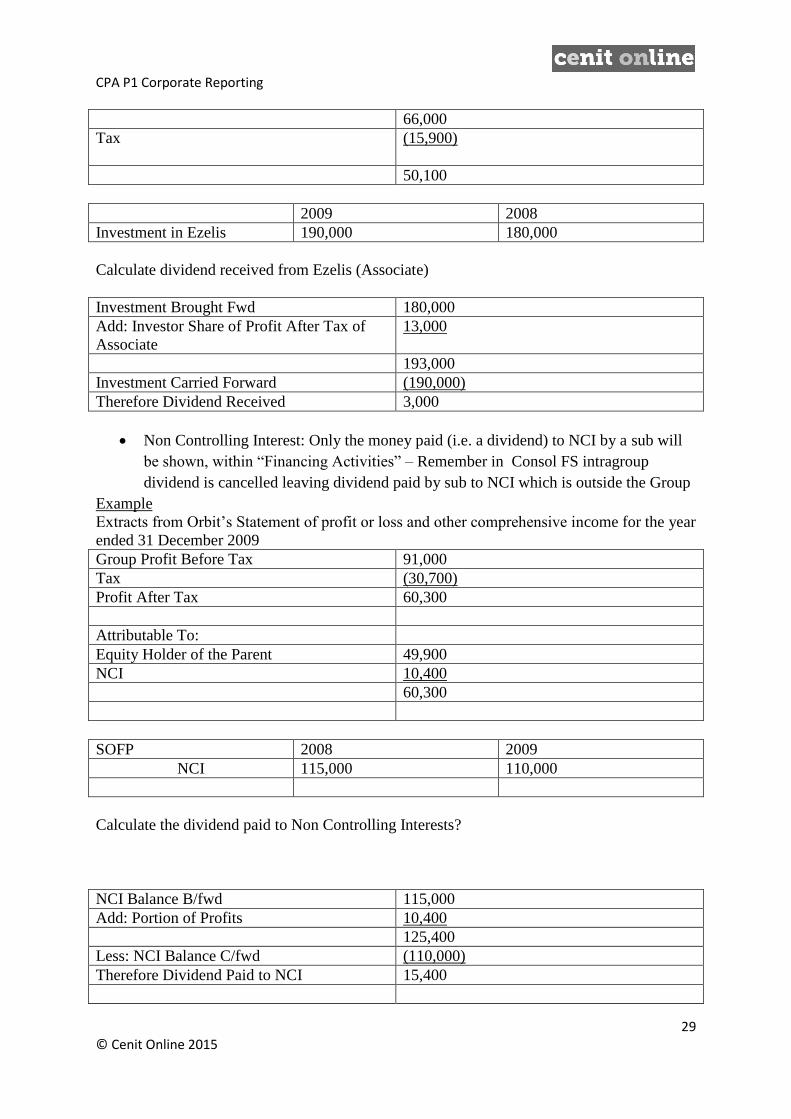

66,000

Tax (15,900)

50,100

2009 2008

Investment in Ezelis 190,000 180,000

Calculate dividend received from Ezelis (Associate)

Investment Brought Fwd 180,000

Add: Investor Share of Profit After Tax of

Associate

13,000

193,000

Investment Carried Forward (190,000)

Therefore Dividend Received 3,000

Non Controlling Interest: Only the money paid (i.e. a dividend) to NCI by a sub will

be shown, within “Financing Activities” – Remember in Consol FS intragroup

dividend is cancelled leaving dividend paid by sub to NCI which is outside the Group

Example

Extracts from Orbit’s Statement of profit or loss and other comprehensive income for the year

ended 31 December 2009

Group Profit Before Tax 91,000

Tax (30,700)

Profit After Tax 60,300

Attributable To:

Equity Holder of the Parent 49,900

NCI 10,400

60,300

SOFP 2008 2009

NCI 115,000 110,000

Calculate the dividend paid to Non Controlling Interests?

NCI Balance B/fwd 115,000

Add: Portion of Profits 10,400

125,400

Less: NCI Balance C/fwd (110,000)

Therefore Dividend Paid to NCI 15,400

CPA P1 Corporate Reporting

30 © Cenit Online 2015

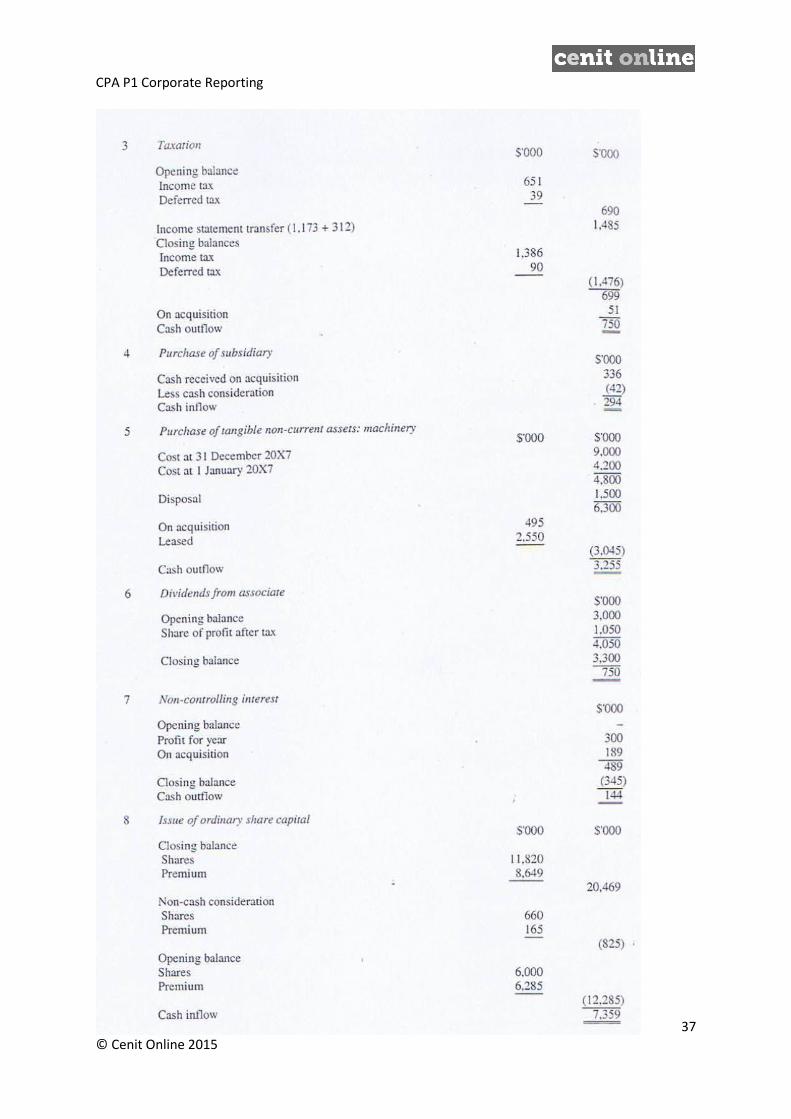

Acquisition of Subsidaries

o N.B. -The net cash paid (not shares, not loan notes – deduct cash acquired on

acquisition) in the acquisition of a subsidiary should be shown, within

Investing Activities

o A disclosure note is required showing the detail of the total purchase

consideration, and how much was actually paid in cash

o Disclosure is also needed to show the detail of assets and liabilities acquired as

well as the cash paid

Example – Acquisition of a Subsidary

When Sintija acquired 80% of the shares of Armine, on 1 January 2009, the agreed

consideration of $72,000, was settled by the issue of 15,000 Sinjita shares, valued at $4 each,

and the balance payable in cash. On the date of acquisition, Armine had prepared a SOFP as

follows

TNCA 40,000

Inventory 8,000

Receivables 16,000

Cash 18,000

Payables (6,000)

76,000

Sintija Consol Financial Statements for 2008 & 2009 were:

Statements of Financial Position as at 31 December 2009

2009 2008

INCA 10,000

TNCA 115,000 30,000

Inventory 53,000 17,000

Receivables 59,000 20,000

Cash 23,400 12,000

260,400 79,000

Shares 65,000 50,000

Premium 48,000 3,000

Retained Earnings 32,400 22,000

Revaluation Reserve 60,000

NCI 18,200

223,600 75,000

Current Liabilities

Payables 28,800 3,000

Tax 8,000 1,000

260,400 79,000

CPA P1 Corporate Reporting

31 © Cenit Online 2015

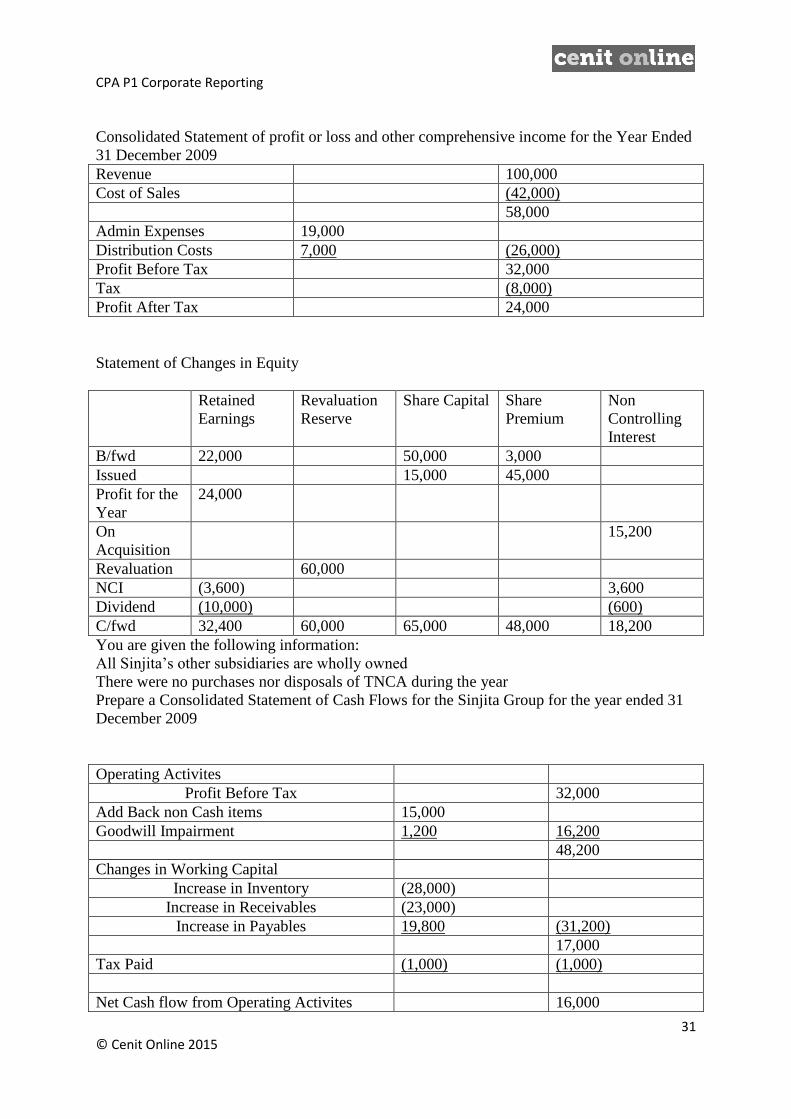

Consolidated Statement of profit or loss and other comprehensive income for the Year Ended

31 December 2009

Revenue 100,000

Cost of Sales (42,000)

58,000

Admin Expenses 19,000

Distribution Costs 7,000 (26,000)

Profit Before Tax 32,000

Tax (8,000)

Profit After Tax 24,000

Statement of Changes in Equity

Retained

Earnings

Revaluation

Reserve

Share Capital Share

Premium

Non

Controlling

Interest

B/fwd 22,000 50,000 3,000

Issued 15,000 45,000

Profit for the

Year

24,000

On

Acquisition

15,200

Revaluation 60,000

NCI (3,600) 3,600

Dividend (10,000) (600)

C/fwd 32,400 60,000 65,000 48,000 18,200

You are given the following information:

All Sinjita’s other subsidiaries are wholly owned

There were no purchases nor disposals of TNCA during the year

Prepare a Consolidated Statement of Cash Flows for the Sinjita Group for the year ended 31

December 2009

Operating Activites

Profit Before Tax 32,000

Add Back non Cash items 15,000

Goodwill Impairment 1,200 16,200

48,200

Changes in Working Capital

Increase in Inventory (28,000)

Increase in Receivables (23,000)

Increase in Payables 19,800 (31,200)

17,000

Tax Paid (1,000) (1,000)

Net Cash flow from Operating Activites 16,000

CPA P1 Corporate Reporting

32 © Cenit Online 2015

Investing Activities

Acquisition of Subsidary 6,000

- 6,000

Financing Activites -

Dividends Paid – Sinjita (10,000)

- NCI (600) (10,600)

Net Cash Flow for the Year 11,400

Cash & Cash Equivalents B/fwd 12,000

Cash & Cash Equivalents B/fwd 23,400

Note: Acqusition of Subsidary

Tangible Non Current Assets 40,000

Inventory 8,000

Receivables 16,000

Cash 18,000

Payables (6,000)

76,000

Non Controlling Interest (15,200)

60,800

Goodwill 11,200

Total Consideration 72,000

Less: Cash in Subsidary (18,000)

54,000

Less: Non Cash Consideration 60,000

Net Cash Flow on Acquisition 6,000

Note 2: Tangible Non Current Assets Acquired – During the period, Sintija revalued property

and equipment by $60,000. No property, plant and equipment was acquired neither by

Purchase nor under finance lease

Note 3: Cash and cash equivalents: Cash and cash equivalents comprise cash in hand,

balances with banks and investment in Treasury Bills. Cash and cash equivalents included in

the Statement of Cash flows

2010 2009

Balances with Banks (600) (2,000)

Cash in Hand 24,000 14,000

23,400 12,000

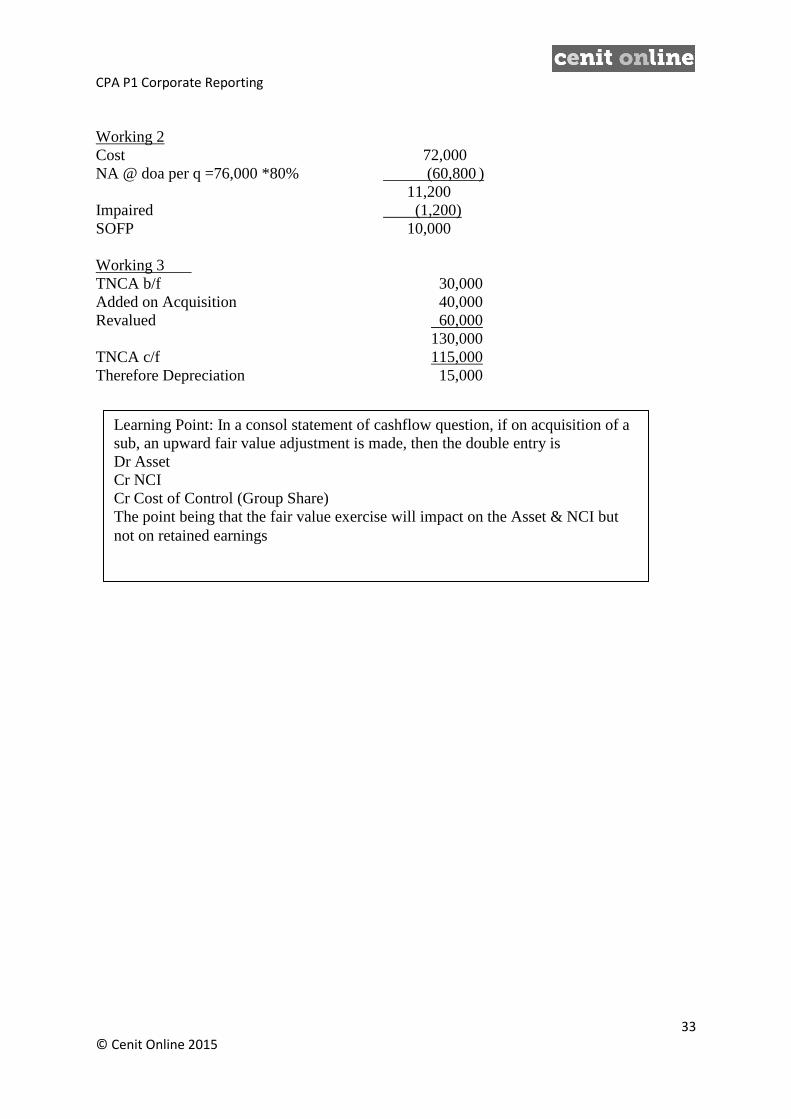

Working 1

Sinjita

80%

Armine

CPA P1 Corporate Reporting

33 © Cenit Online 2015

Working 2

Cost 72,000

NA @ doa per q =76,000 *80% (60,800 )

11,200

Impaired (1,200)

SOFP 10,000

Working 3

TNCA b/f 30,000

Added on Acquisition 40,000

Revalued 60,000

130,000

TNCA c/f 115,000

Therefore Depreciation 15,000

Learning Point: In a consol statement of cashflow question, if on acquisition of a

sub, an upward fair value adjustment is made, then the double entry is

Dr Asset

Cr NCI

Cr Cost of Control (Group Share)

The point being that the fair value exercise will impact on the Asset & NCI but

not on retained earnings

CPA P1 Corporate Reporting

34 © Cenit Online 2015

CPA P1 Corporate Reporting

35 © Cenit Online 2015

CPA P1 Corporate Reporting

36 © Cenit Online 2015

CPA P1 Corporate Reporting

37 © Cenit Online 2015

CPA P1 Corporate Reporting

38 © Cenit Online 2015

Notes:

Where a Consolidated Statement of Cashflow question includes an acquisition of a

Sub, then you will need to “Ascertain Group Structure” and calculate “Goodwill on

Acquisition” to check for a possible impairment. – Also on acquisition of a Sub, the

NCI will be credited with their share of the net assets of the Sub at the reporting date

- this will impact on calculation of dividend paid to NCI – Also only the net cash

paid on acquisition of the sub will be accounted for (i.e. Cash paid less cash and cash

equivalents acquired)

Be Careful not to double count “Share of Profit After Tax of Associate” when

calculating “Dividend Paid” in Financing Activities if applicable

Watch out for impairment of Consol Goodwill – non cash item – addback

immediately after Profit Before Tax with “Operating Activities” section – So need to

calculate Consol Goodwill on Acquisition and compare to consol goodwill at

reporting date

A Gain or Loss on Disposal of a Subsidary

o Gain: Subtract within Operating Activities

o Loss: Addback within Operating Activities

Investment Income – “Investing Activities” – account for investment income actually

received - i.e. net of tax

The figure for repayment of finance leases in “Financing Activities” is capital only –

the interest element is contained within Interest Paid in “Operating Activities”

CPA P1 Corporate Reporting

39 © Cenit Online 2015

Cash and Cash Equivalents b/f & c/f – beware of signs!!

For Acquisitions of Tangible Non Current Assets, beware of Finance Leases and

Revaluation Reserve and Fair Value Adjustments

Cash and Cash Equivalents At Beginning/End of Period

In the exam, transcribe these figures direct from the question

i.e. Bank/Bank Overdraft Figures and any Cash Equivalents like Deposit

Accounts.

Do not depend on your Worked Solution to get the figure for “Cash and Cash

Equivalents at end of Period”.

And from doing the above, you will derive your figure for “ Net

Increase/Decrease in Cash & Cash Equivalents” (Do not depend on your

worked solution)

Example – Disposal of a Subsidary

The same principles apply here as with acquisitions. Part of the changes in the

Statement of Financial Position figures are accounted for by the disposal of the

subsidiary’s assets and liabilities

Autis sold his entire shareholding of Lokys on 28 February 2009 for $800,000. He had held

the shares for 10 years since the incorporation of Lokys

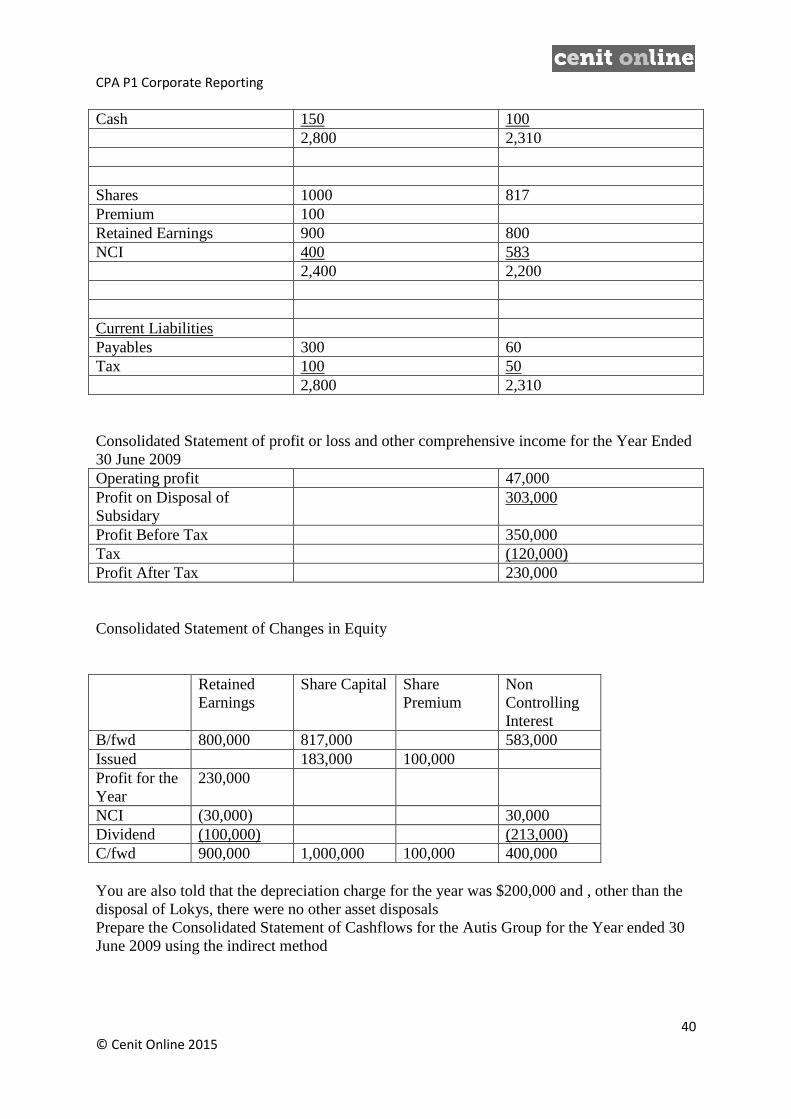

At the date of disposal, the Lokys Statement of Financial Position was

TNCA 500,000

Inventory 150,000

Receivables 100,000

Cash 50,000

Payables (75,000)

Tax (15,000)

Net Assets 710,000

The consolidated statement of financial position of the Autis Group as at 30 June 2009 and

2008 were

2009 2008

$000 $000

INCA

TNCA 1300 900

Inventory 750 800

Receivables 600 510

CPA P1 Corporate Reporting

40 © Cenit Online 2015

Cash 150 100

2,800 2,310

Shares 1000 817

Premium 100

Retained Earnings 900 800

NCI 400 583

2,400 2,200

Current Liabilities

Payables 300 60

Tax 100 50

2,800 2,310

Consolidated Statement of profit or loss and other comprehensive income for the Year Ended

30 June 2009

Operating profit 47,000

Profit on Disposal of

Subsidary

303,000

Profit Before Tax 350,000

Tax (120,000)

Profit After Tax 230,000

Consolidated Statement of Changes in Equity

Retained

Earnings

Share Capital Share

Premium

Non

Controlling

Interest

B/fwd 800,000 817,000 583,000

Issued 183,000 100,000

Profit for the

Year

230,000

NCI (30,000) 30,000

Dividend (100,000) (213,000)

C/fwd 900,000 1,000,000 100,000 400,000

You are also told that the depreciation charge for the year was $200,000 and , other than the

disposal of Lokys, there were no other asset disposals

Prepare the Consolidated Statement of Cashflows for the Autis Group for the Year ended 30

June 2009 using the indirect method

CPA P1 Corporate Reporting

41 © Cenit Online 2015

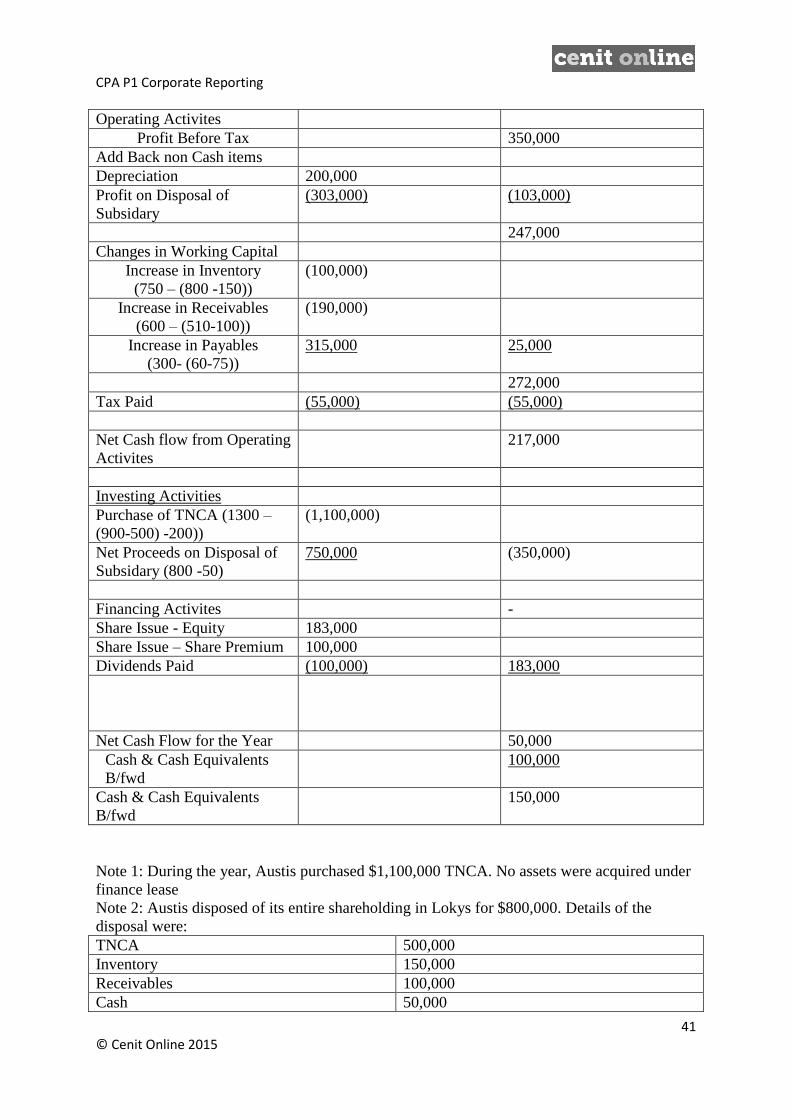

Operating Activites

Profit Before Tax 350,000

Add Back non Cash items

Depreciation 200,000

Profit on Disposal of

Subsidary

(303,000) (103,000)

247,000

Changes in Working Capital

Increase in Inventory

(750 – (800 -150))

(100,000)

Increase in Receivables

(600 – (510-100))

(190,000)

Increase in Payables

(300- (60-75))

315,000 25,000

272,000

Tax Paid (55,000) (55,000)

Net Cash flow from Operating

Activites

217,000

Investing Activities

Purchase of TNCA (1300 –

(900-500) -200))

(1,100,000)

Net Proceeds on Disposal of

Subsidary (800 -50)

750,000 (350,000)

Financing Activites -

Share Issue - Equity 183,000

Share Issue – Share Premium 100,000

Dividends Paid (100,000) 183,000

Net Cash Flow for the Year 50,000

Cash & Cash Equivalents

B/fwd

100,000

Cash & Cash Equivalents

B/fwd

150,000

Note 1: During the year, Austis purchased $1,100,000 TNCA. No assets were acquired under

finance lease

Note 2: Austis disposed of its entire shareholding in Lokys for $800,000. Details of the

disposal were:

TNCA 500,000

Inventory 150,000

Receivables 100,000

Cash 50,000

CPA P1 Corporate Reporting

42 © Cenit Online 2015

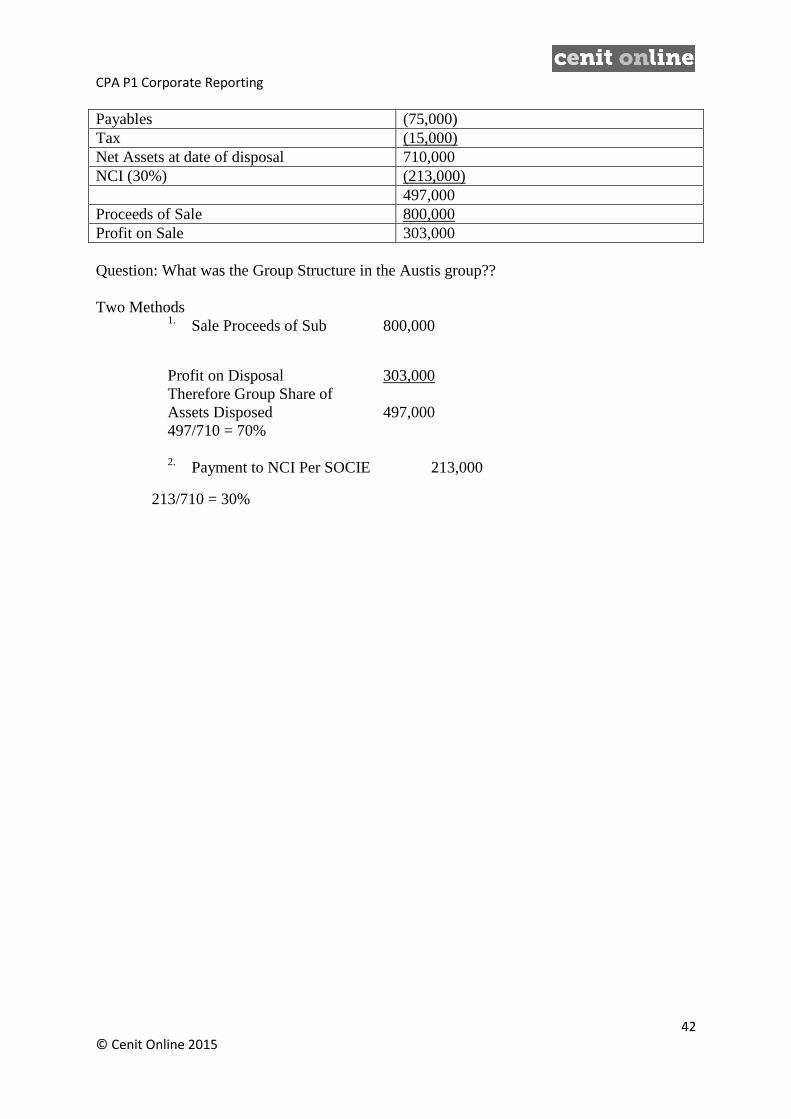

Payables (75,000)

Tax (15,000)

Net Assets at date of disposal 710,000

NCI (30%) (213,000)

497,000

Proceeds of Sale 800,000

Profit on Sale 303,000

Question: What was the Group Structure in the Austis group??

Two Methods 1. Sale Proceeds of Sub 800,000

Profit on Disposal 303,000

Therefore Group Share of

Assets Disposed 497,000

497/710 = 70%

2. Payment to NCI Per SOCIE 213,000

213/710 = 30%

CPA P1 Corporate Reporting

43 © Cenit Online 2015

APPROACH TO CSOCF/SOCF

Layout Proforma – One Page for Operating Activities and One Page for Investing

Activities & Financing Activities

Calculate Opening Cash & Cash Equivalents, Closing Cash & Cash Equivalents and

Increase/Decrease in Cash & Cash Equivalents Directly from Question

Begin with Profit Before Tax – then “PAID IS” (Non Cash Items)

o Profit/Loss on Disposal of NCA

o Amortisation

o Impairment

o Depreciaition

o Interest Expense

o Share of Profit of Associate

o then RIP (Movements in Working Capital)

o Calculate Interest Paid & Taxation Paid

Investing Activities

Financing Activities

Aim is to deal with each line item in the SOFP/CSOFP to identify cash movement if

applicable. Tick of each line item as you go.

Total CSOCF/SOCF if time allows

Past Exam Questions – IAS 7

Q3 (8) August 2013

Q2 April 13 (Single Company SOCF)

Q1 Aug 2011 (Consol. Statement of Cashflow)

Q3 Aug 11

Q3 Apr 11

![Chap18[1] the Statement of Cashflows](https://static.cupdf.com/doc/110x72/55cf9942550346d0339c7445/chap181-the-statement-of-cashflows.jpg)