1

TOPIC 3INTERIM FINANCIAL REPORTING

(MFRS 134)

2

LEARNING OUTCOMES

At the end of the topic, students should be

able to:1. Explain the content of interim reporting2. Explain the recognition &

measurement3. Explain the disclosure requirement

3

DEFINITION

A financial report containing either a complete set of financial statements or a set of condensed financial statements for an interim period.

Interim period is a financial reporting period shorter than a full financial year (e.g. half-yearly or quarterly)

The reports cover current period, year to date and comparatives.

THE IMPORTANCE OF INTERIM REPORTING

Investors consider that the interim financial reporting is of more value than annual financial information which enables them to analyze the actual performances and also to revise their projections.

Interim financial reports provide price-sensitive data to investors.

Timely and reliable interim financial reporting improves the ability of investors, creditors, tax authorities and others to understand an enterprise's capacity to generate earnings and cash flows and its financial condition and liquidity.

4

5

THE CONTENT OF INTERIM FINANCIAL STATEMENTS

1. The full set of financial statements, or

2. Condensed financial statements consist of:

a. A condensed statement of financial position

b. A condensed statement of comprehensive

income statement

c. A condensed statement of changes in equity

d. A condensed statement of cash flows

e. Selected explanatory notes

Reporting Period For Interim Financial Statements

Interim financial reports generally can be half-yearly or quarterly reports.

The reports cover current period, year to date and comparatives

6

7

Periods Which Interim FS Required To Be Presented

Statement of financial position as of the end of current interim period and a comparative statement of financial position as of the end of the immediately preceding financial yearStatements of comprehensive income for the current interim period and cumulatively for the current financial year to date, with comparative statements of comparative income for the comparable interim periods (current and year to date) of the immediately preceding financial year

8

Periods Which Interim FS Required To Be Presented (Con’t)

Statement showing changes in equity cumulatively for the current financial year to date, with a comparative statement for the comparable year to date period of the immediately preceding financial year.Statement of cash flow cumulatively for the current financial year to date, with a comparative statement for the comparable year to date period of the immediately preceding financial year.

9

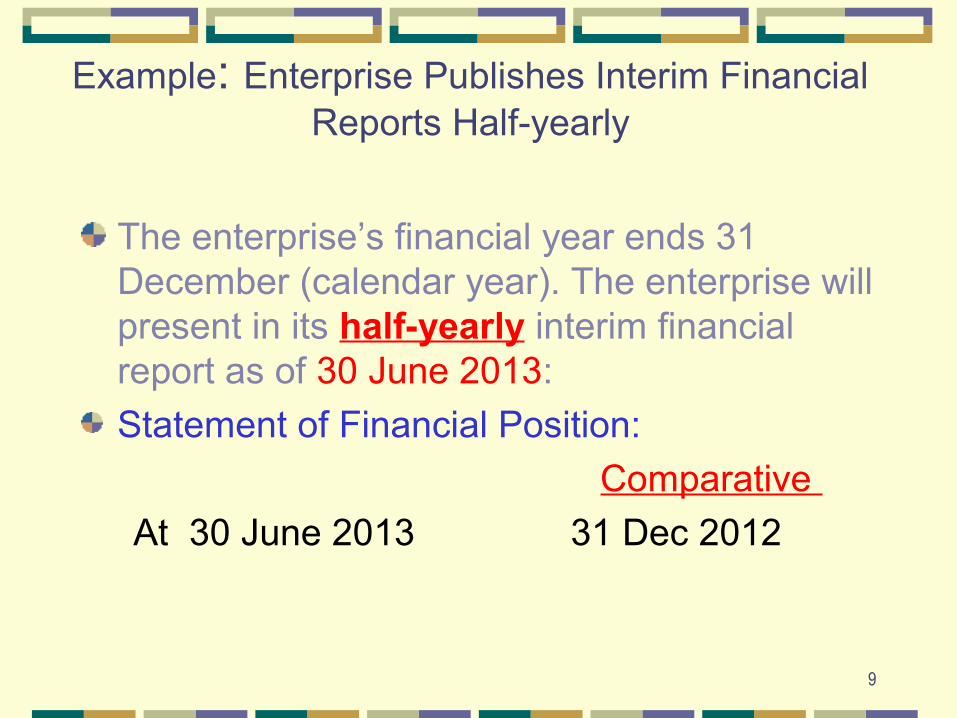

Example: Enterprise Publishes Interim Financial Reports Half-yearly

The enterprise’s financial year ends 31 December (calendar year). The enterprise will present in its half-yearly interim financial report as of 30 June 2013:

Statement of Financial Position:

Comparative

At 30 June 2013 31 Dec 2012

10

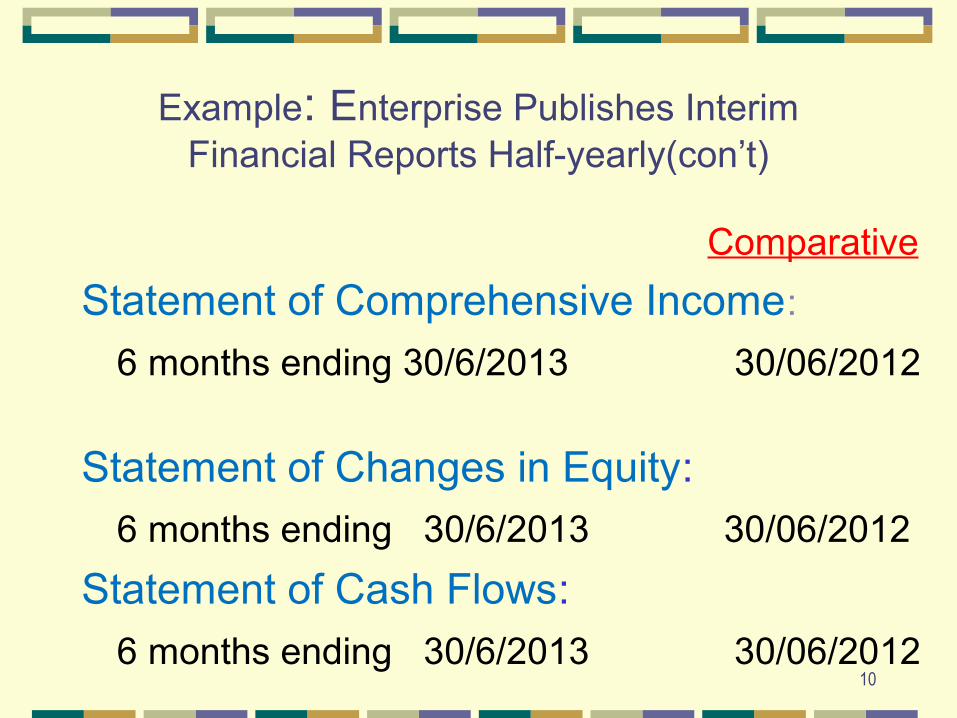

Example: Enterprise Publishes Interim Financial Reports Half-yearly(con’t)

Comparative

Statement of Comprehensive Income:

6 months ending 30/6/2013 30/06/2012

Statement of Changes in Equity:

6 months ending 30/6/2013 30/06/2012

Statement of Cash Flows:

6 months ending 30/6/2013 30/06/2012

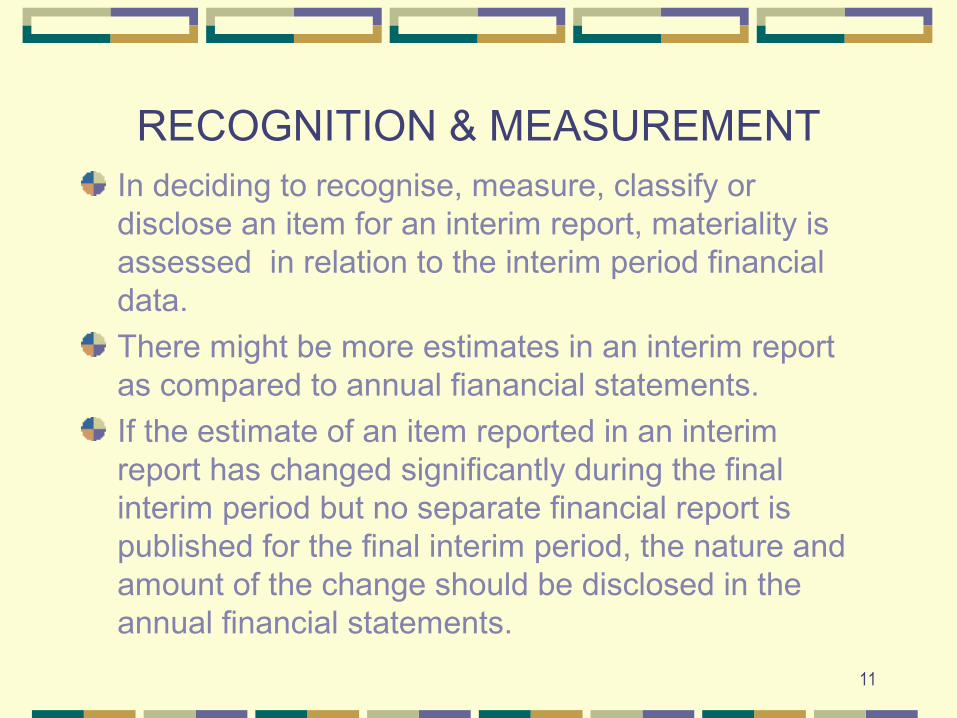

RECOGNITION & MEASUREMENTIn deciding to recognise, measure, classify or disclose an item for an interim report, materiality is assessed in relation to the interim period financial data.

There might be more estimates in an interim report as compared to annual fianancial statements.

If the estimate of an item reported in an interim report has changed significantly during the final interim period but no separate financial report is published for the final interim period, the nature and amount of the change should be disclosed in the annual financial statements.

11

12

RECOGNITION & MEASUREMENT (CON’T)

The principles for recognising assets, liabilities, income and expenses are the same as in the annual financial statements.

The frequency of interim reporting (annually, half-yearly or quarterly) should not effect the measurement of annual result, thus measurement should be made on year-to-date basis

13

1. Depreciation- is based on the asset in use during the period2. Impairment loss – is done at the end of Interim Period (IP). If

the impairment loss estimates changes in the subsequent period, the original estimate is changed. No retrospective adjustment is required.

3. R&D – The determination of capitalising development cost has to be done at the end of each IP.

4. Inventories – at the end of each IP, there is a need to determine value of inventories (often use estimates).

5. Tax Expense – The tax expense is the best estimate of the weighted average annual income tax rate expected for the full financial year. If tax rate changes, the income tax for subsequent period is adjusted. Malaysia – the tax rate is flat rate – no adjustment.

14

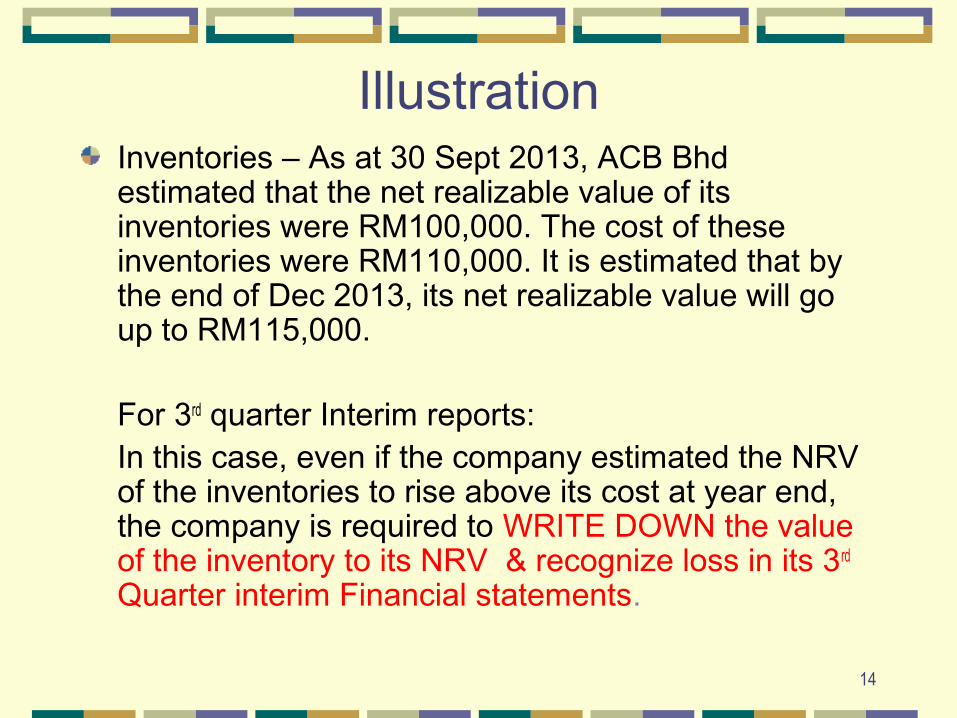

IllustrationInventories – As at 30 Sept 2013, ACB Bhd estimated that the net realizable value of its inventories were RM100,000. The cost of these inventories were RM110,000. It is estimated that by the end of Dec 2013, its net realizable value will go up to RM115,000.

For 3rd quarter Interim reports:In this case, even if the company estimated the NRV of the inventories to rise above its cost at year end, the company is required to WRITE DOWN the value of the inventory to its NRV & recognize loss in its 3rd Quarter interim Financial statements.

Accounting Policies

The accounting policies applied in the interim financial statements have to be the same as that applied in the annual financial statements.

If there are changes in the accounting policies after the date of the most recent annual statements, the new policies should be applied in the interim financial statements.

15

Revenue Received Seasonally, Cyclically Or Occasionally

Revenues that are received seasonally, cyclically or occasionally within a financial year should not be anticipated or deferred as of an interim date if anticipation or deferral would not be suitable at the end of entity’s financial year.

Examples dividend revenue, royalties and government grant-should be recognized when they occur.

16

Costs Incurred Unevenly During The Financial Year

Costs that are incurred unevenly during an entity’s financial year shall be anticipated or deferred for interim reporting purpose if, and only if, it is also suitable to anticipate or defer that type of cost at the end of financial year

17

DISCLOSURE REQUIREMENT

An entity shall include in its interim financial report an explanation of events and transactions that are significant to an understanding of the changes in financial position and performance of the entity since the end of the last annual reporting period.

Information disclosed in relation to those events and transactions shall update the relevant information presented in the most recent annual financial report.

18

DISCLOSURE REQUIREMENT (CON’T)

The following is a list of events and transactions for which disclosures would be required if they are significant: the list is not exhaustive.

(a) the write-down of inventories to net realisable value and the

reversal of such a write-down;

(b) recognition of a loss from the impairment of financial assets,

property, plant and equipment, intangible assets, or other

assets, and the reversal of such an impairment loss;

(c) the reversal of any provisions for the costs of restructuring;

(d) acquisitions and disposals of items of property, plant and

equipment;

19

DISCLOSURE REQUIREMENT (CON’T)

(e) commitments for the purchase of property, plant and equipment;

(f) litigation settlements;

(g) corrections of prior period errors;

(h) changes in the business or economic circumstances that affect

the fair value of the entity’s financial assets and financial

liabilities, whether those assets or liabilities are recognised at

fair value or amortised cost;

(i) any loan default or breach of a loan agreement that has not been

remedied on or before the end of the reporting period;

(j) related party transactions;20

DISCLOSURE REQUIREMENT(CON’T)

(k) transfers between levels of the fair value hierarchy used in

measuring the fair value of financial instruments;

(l) changes in the classification of financial assets as a result of a

change in the purpose or use of those assets; and

(m) changes in contingent liabilities or contingent assets.

21

OTHER DISCLOSURES (IN NOTES TO INTERIM FS)

a) Statement of same accounting policies and methods of computation

b) Explanatory comments about the seasonality or cyclicality of interim operations

c) The nature and amounts of items affecting assets, liabilities, equity, net income, or cash flow that unusual because of their nature, size or incidence

22

OTHER DISCLOSURES (IN NOTES TO INTERIM FS)

d) The nature and amount of changes in estimates of amounts reported in prior interim periods or prior financial years, if material

e) Issuances, cancellation, repurchases, resale and repayments of debt and securities equity

f) Dividend paid

g) Segment revenue and segment result for business segment and geographical segments

23

OTHER DISCLOSURES (IN NOTES TO INTERIM FS)

h) events after the end the interim period that have not been reflected in the FS for the interim period.

i) The effect of changes in the composition of entity during the interim period including business combination, obtaining & losing control of subsidiary, restructuring & discontinued operations.

24