Think Tank- Oil and Gas Industry

• Panel 1. Energy reform and the new tax

regime for hydrocarbon producers.

• Panel 2. Financing & Structuring Investment

in Mexico

• Panel 3. Energy Tax Hot Topics

July 10, 2014

Energy reform and the new tax regime for

hydrocarbon producers.

10 July 1014

Think Tank- Oil and Gas Industry

Page 3

Presenters

► Iván Sandrea

CEO Sierra Energy

► Stephen Landry

EY’s America Oil & Gas Tax Leader

► Richard Overton

EY ITS Partner

► Moderator: Oscar López Velarde

EY ITS Partner

Page 4

E&P contracts for public and private

companies

Independent regulators

Permits for midstream and

downstream

Pemex and CFE modernization

Oil and gas reform

Highlights of the reform

Page 5

?

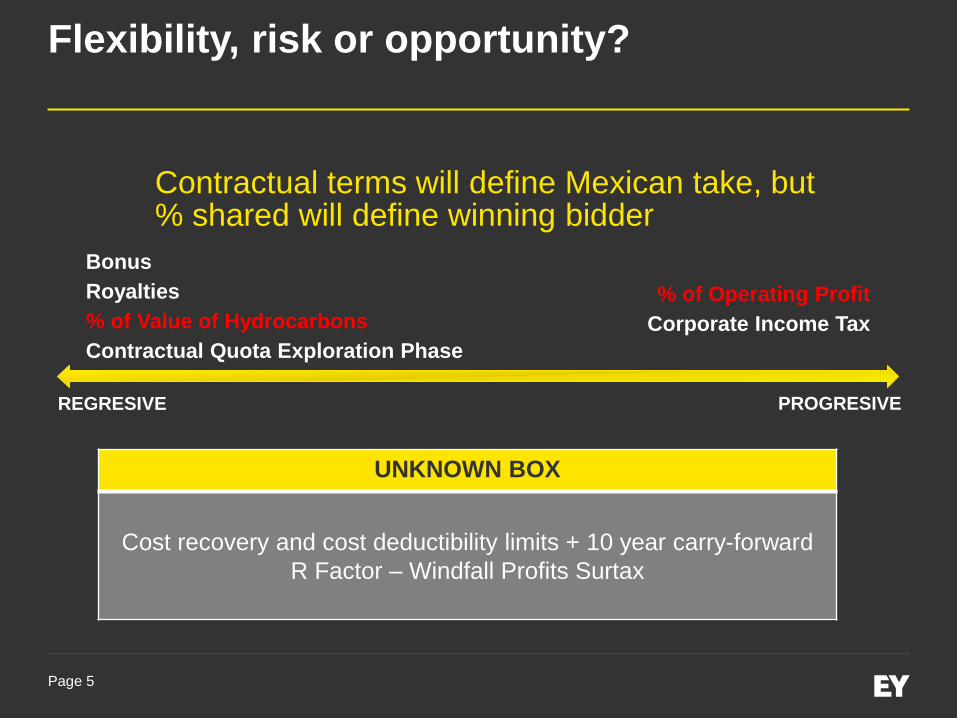

Flexibility, risk or opportunity?

UNKNOWN BOX

Cost recovery and cost deductibility limits + 10 year carry-forward

R Factor – Windfall Profits Surtax

REGRESIVE PROGRESIVE

Bonus

Royalties

% of Value of Hydrocarbons

Contractual Quota Exploration Phase

% of Operating Profit

Corporate Income Tax

Contractual terms will define Mexican take, but % shared will define winning bidder

Page 6

Ring-fencing

• Rules yet to be defined

• JOA not available

• Lack of consolidation

• Government take

Contract Mexican

Tax

Local Content

Legal Entity

Ring-fencing

Page 7

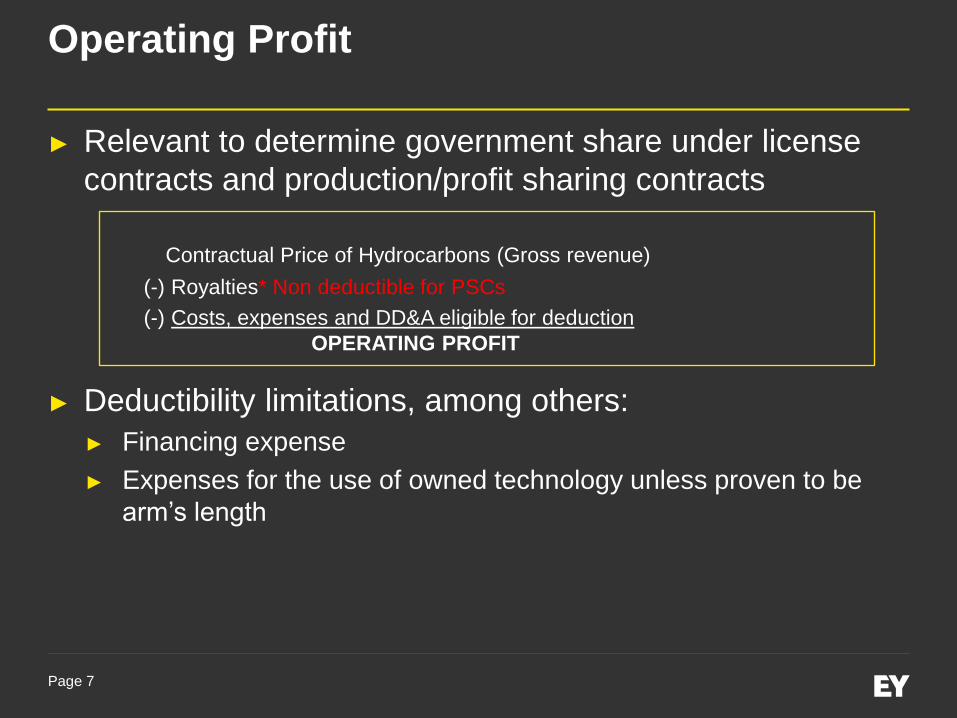

Operating Profit

► Relevant to determine government share under license

contracts and production/profit sharing contracts

Contractual Price of Hydrocarbons (Gross revenue)

(-) Royalties* Non deductible for PSCs

(-) Costs, expenses and DD&A eligible for deduction

OPERATING PROFIT

► Deductibility limitations, among others:

► Financing expense

► Expenses for the use of owned technology unless proven to be

arm’s length

Page 8

Capex depreciation

► New rates:

► Might be used also for income tax

► Upon election of the taxpayer

► Lack of clear definitions

► Tax or accounting rules?

► Only applicable to contractor

Depreciation Rate Capex Item

100%

• Exploratory phase

• Secondary recovery and improvement

• Non-capitalizable maintenance or IDC

25% • Development and production phase

10% • Storage and transport infrastructure

Page 9

Arm’s length principle

Cost oil + mark-up or margin = Contractor’s Take

Deductible and recoverable Cost Oil?

Operating Co. SPV

Contractor

Cost Plus

Mark-up

Operating Co. SPV

Contractor

Arm’s length

compensation

Royalties,

Procurement,

Financing

Eligible and not eligible costs

Page 10

License – Profit Share

Take*

$101 FMV Hydrocarbons

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$45.5 Profit Oil

$25 - 50% Government Share

$6.22 - 30% CIT

$14.28 Contractor’s Take

Operating Profit

$100 Contractual Price

$10 - Royalty

$40 - Allowed Cost Oil

$50 Operating Profit

$25 50% Government Share

* Bonus and dividend WHT not included

Corporate Income Tax

$101 FMV Hydrocarbons

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$25 - 50% Government Share

$20.75 Taxable Profit

$6.22 30% CIT

Page 11

License – Value of Hydrocarbons Share Additional royalty

Take

$101 FMV Hydrocarbons

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$45.5 Profit Oil

$25 - 25% Government Share

$6.22 - 30% CIT

$14.28 Contractor’s Take

Value of Hydrocarbons Share

$100 Contractual Price

$25 25% Government Share

* Bonus and dividend WHT not included

Corporate Income Tax

$101 FMV Hydrocarbons

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$25 - 25% Government Share

$20.75 Taxable Profit

$6.22 30% CIT

Page 12

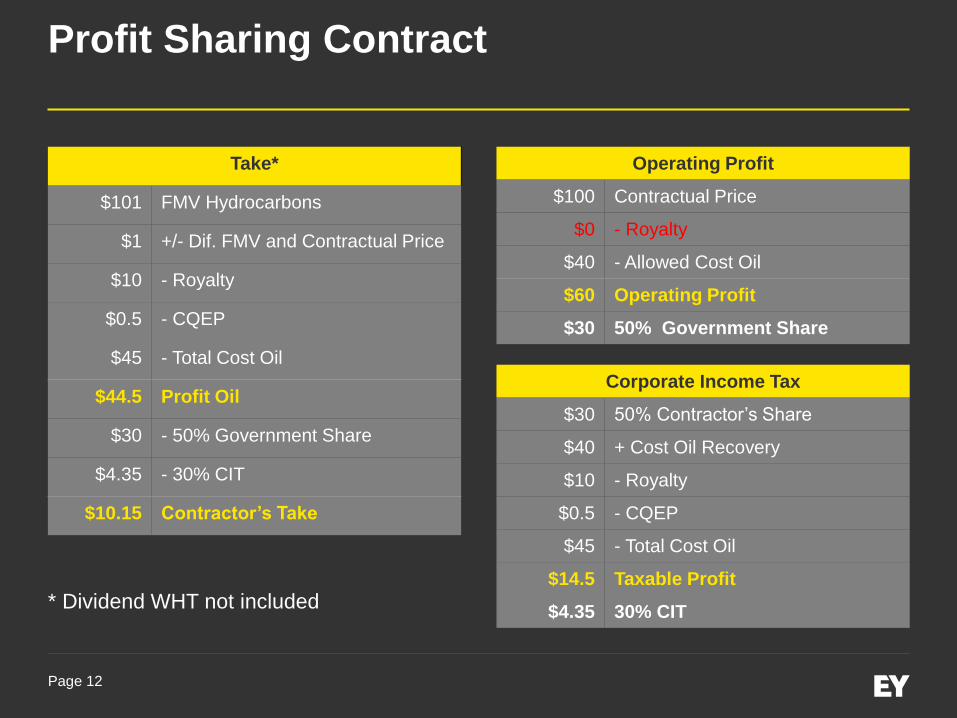

Profit Sharing Contract

Take*

$101 FMV Hydrocarbons

$1 +/- Dif. FMV and Contractual Price

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$44.5 Profit Oil

$30 - 50% Government Share

$4.35 - 30% CIT

$10.15 Contractor’s Take

Operating Profit

$100 Contractual Price

$0 - Royalty

$40 - Allowed Cost Oil

$60 Operating Profit

$30 50% Government Share

* Dividend WHT not included

Corporate Income Tax

$30 50% Contractor’s Share

$40 + Cost Oil Recovery

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$14.5 Taxable Profit

$4.35 30% CIT

Page 13

Production Sharing Contract

Take*

$101 FMV Hydrocarbons

$.3 +/- Dif. FMV and Contractual Price

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$45.2 Profit Oil

$30 - 50% Government Share

$4.56 - 30% CIT

$10.64 Contractor’s Take

Operating Profit

$100 Contractual Price

$0 - Royalty

$40 - Allowed Cost Oil

$60 Operating Profit

$30 50% Government Share

* Dividend WHT not included

Corporate Income Tax

$30 50% Contractor’s Share

$40 + Cost Oil Recovery

$.7 +/- Dif. FMV and Contractual Price

$10 - Royalty

$0.5 - CQEP

$45 - Total Cost Oil

$15.2 Taxable Profit

$4.56 30% CIT

Financing & Structuring Investment in Mexico

Think Tank- Oil and Gas Industry

Page 15

Presenters

► Deborah Byers

EY TAS Partner

► Carlos Vargas Rodriguez

BBVA Oil & Gas

► Adolfo Osorio Hernández

BBVA Oil & Gas

► Moderator: Alfredo Alvarez Laparte

EY ITS Partner

Page 16

Oil & Gas Investment Opportunities

Find it…

Get

it out…

Turn it into

something

useful…

Sell it…

Upstream Midstream Downstream

Transportation and Storage

Services & Local Supply / Construction …

Page 17

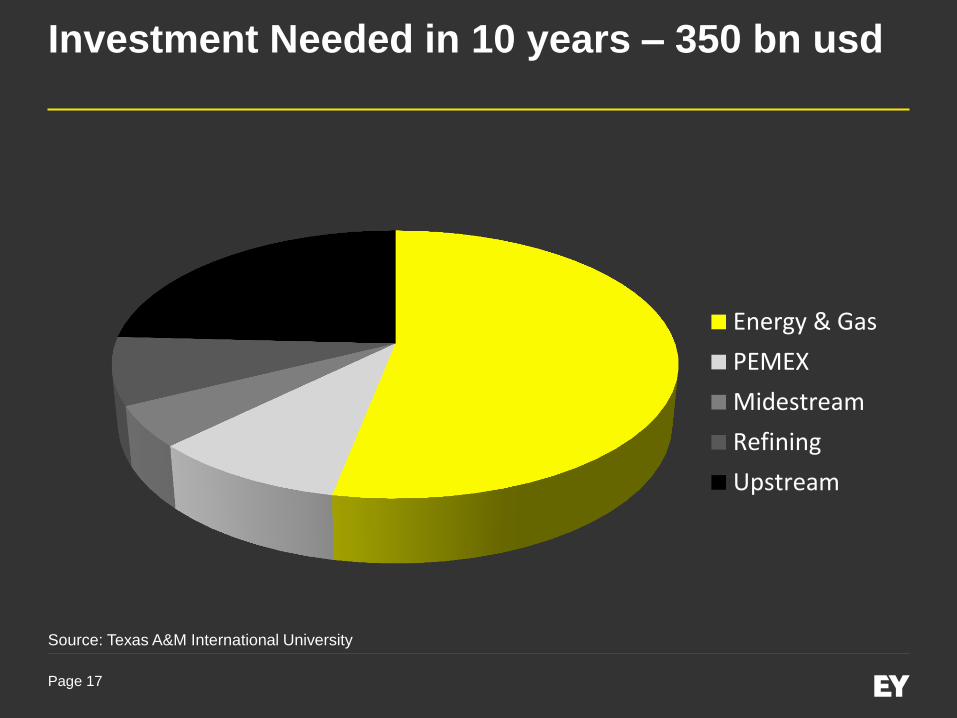

Investment Needed in 10 years – 350 bn usd

Energy & Gas

PEMEX

Midestream

Refining

Upstream

Source: Texas A&M International University

Page 18

Oil & Gas Wells – US vs Mexico

Eagle Ford Texas

Drilling Permits in 2012

US 4,143

Mexico 3

Page 19

Oil & Gas Wells – US Eagle Ford Texas

0

300

600

900

1200

1500

1800

2100

2400

Eagle Ford Bakken Permian Net other Total US

pro

du

cti

on

gain

s (

00

0 b

/d)

US crude oil production gains: last three years (Dec 2010 production vs. Dec 2013 production)

1,088

97

437

656

2,278

Page 20

Pipelines System – US vs Mexico

US – 490,000 km

Mexico – 13,000 km

Page 21

Refineries US vs Mexico

US 143 vs Mexico 6

Page 22

Resources Feeders

National &

Foreign

Corporations

Private

Equity

Banking

System

Government

Resources

Stock

Exchanges (MSE, NYSE, …)

Page 23

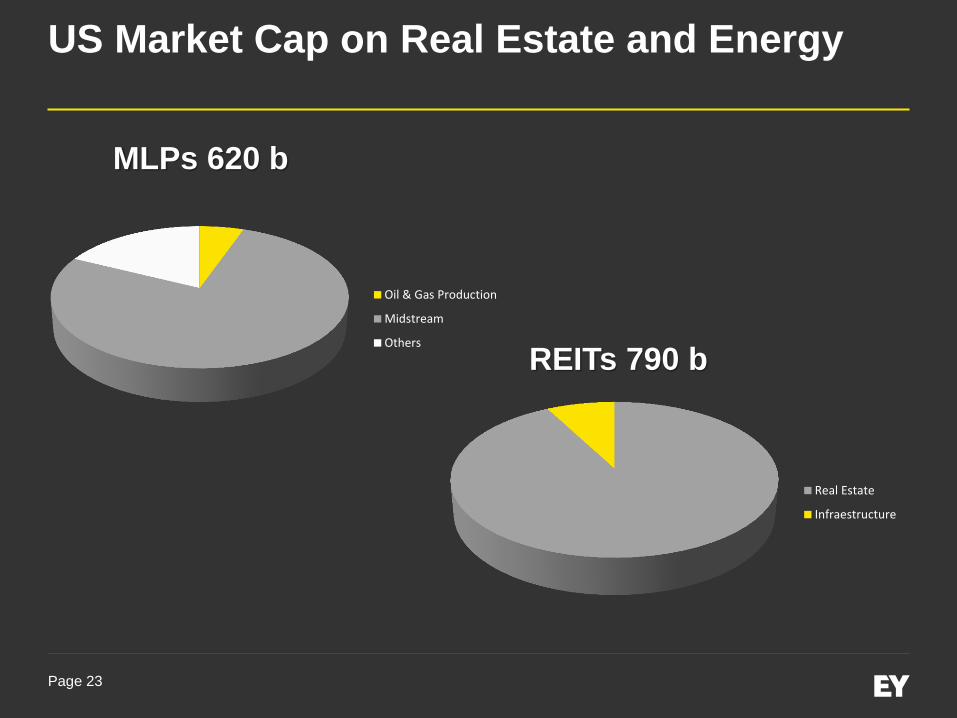

US Market Cap on Real Estate and Energy

Oil & Gas Production

Midstream

Others

MLPs 620 b

Real Estate

Infraestructure

REITs 790 b

Page 24

Mexican Market – Real Estate and Infrastructure

FIBRAS

CKDs

CKDs / FIBRAs 23 b

FIBRAS & CKDs

Others

AFORES 168 b

Page 25

MLPs for the Mexican resources need

Mexican

Subsidiary

Mexican

Subsidiary

30% Income Tax – Profits

10% dividend withholding

MLP

Holding Co

MLP

FIBRA

“Ideal Structure*”

MLP

30% Income Tax – Profits

0 - 10% dividend withholding

Financing

30% on distributions

Treaties?

* Regulations need to be adapted

Infrastructure RIETS?

Regulatory?

Mexican

Stock Ex

“Oil & Gas Hot Topics”

Think Tank- Oil and Gas Industry

Page 27

Presenters

► Rodrigo Ochoa

EY ITS Partner

► Jorge Libreros

EY Controversy Partner

► Moderator: Koen Vant Hek Koot

EY ITS Partner

Page 28

Bareboat Charter (BBA)

Main Considerations

Income Tax Law

Use or enjoyment of goods

Royalties

Chartering (Fletamiento)

Tax Treaties:

Royalties?

Industrial Equipment?

Deductibility for Income tax purposes

Overview

Requirements

2. Fee 1. Bareboat

(BBA)

Treaty Co.

Mex Co.

Page 29

Bareboat Charter (BBA)

Main Considerations

Double Income tax withholding?

Beneficial ownership

3. Fee

2. Bareboat

(BBA)

Treaty Co.

Mex Co.

REFIPRE (*)

(*) Owner of the equipment

4. Fee

1. Bareboat

(BBA)

Page 30

Time Charter

2. Fee 1. Time

Charter

Treaty Co.

Mex Co.

Main Considerations

Business Profits

Permanent Establishment

Page 31

Financial Lease Agreement (FLA)

Temas actuales de la Industria Petrolera “Hot Topics”

2. Interest +

principal payment

1. Financial

Lease

Treaty Co.

Mex Co.

Main Considerations

Characterization for tax purposes

Tax Depreciation

Construction equipment?

Vessel / Boat ?

Other kind of asset?

Accelerated depreciation

Temporary importation

FLA vs. BBA

Page 32

Mexican tax authorities (SAT) Audits

► Deductibility of services

► Service entities (employees)

► Permanent establishment

► Prorate expenses

► Beneficial ownership

► Base Erosion and Profit Sharing (BEPS)

Page 33

Thank you

Ernst & Young

Auditoría | Asesoría de Negocios | Fiscal-Legal | Fusiones y Adquisiciones

Acerca de Ernst & Young

Ernst & Young es líder global en servicios de auditoría, asesoría de negocios,

fiscal-legal y fusiones y adquisiciones. A nivel mundial, nuestros 152,000 profesionales están

unidos por los mismos valores y un compromiso sólido con la calidad. Marcamos la

diferencia al ayudar a nuestra gente, clientes y comunidades a lograr su potencial.

Para mayor información por favor visite www.ey.com/mx

© 2013 Mancera, S.C.

Integrante Ernst & Young Global

Derechos reservados

Ernst & Young se refiere a la organización global de firmas miembro conocida como Ernst & Young Global Limited, en la que cada

una de ellas actúa como una entidad legal separada. Ernst & Young Global Limited no provee servicios a clientes.

NUESTRAS OFICINAS

AGUASCALIENTES

CANCÚN

CHIHUAHUA

CIUDAD JUÁREZ

CIUDAD OBREGÓN

CULIACÁN

GUADALAJARA

HERMOSILLO

LEÓN

LOS MOCHIS

MÉRIDA

NUESTRAS OFICINAS

MEXICALI

MÉXICO, D.F.

MONTERREY

NAVOJOA

PUEBLA

QUERÉTARO

REYNOSA

SAN LUIS POTOSÍ

TIJUANA

TORREÓN

VERACRUZ

CLAVE

449

998

614

656

644

667

33

662

477

668

999

TELÉFONO

912-82-01

884-98-75

425-35-70

648-16-10

413-32-30

714-90-88

3884-61-00

260-83-60

717-70-62

818-40-33

926-14-50

CLAVE

686

55

81

642

222

442

899

444

664

871

229

TELÉFONO

568-45-53

5283-13-00

8152-18-00

422-70-77

237-99-22

216-64-29

929-57-07

825-72-75

681-78-44

713-89-01

922-57-55