The views expressed in this presentation do not necessarily reflect the views of AT&T.

Tom Kerber

Smart Home Market

Director, ResearchParks Associates

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Drivers and Barriers to Smart Home Adoption

The views expressed in this presentation do not necessarily reflect the views of AT&T.

62% 62%72% 69%

10% 11% 8% 9%

80%

70%

60%

50%

40%

30%

20%

10%

0%

10%

20%

Smart home services Smart home products Where to buy smarthome services

Where to buy smarthome products

Very familiar (Rating 6-7) Not familiar (Rating 1-3)%

of

Res

po

nd

ents

Barriers - Awareness

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Smart Home Familiarity (Q2/14)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

21%

26%

26%

28%

29%

29%

29%

30%

30%

31%

31%

32%

34%

34%

34%

35%

36%

39%

39%

41%

41%

43%

45%

51%

Open a pet door

Turn on/off or check the status of appliances in your laundry area

Receive a daily summary of your home's energy usage

Understand your home's energy performance

Open and close your garage door

Turn on/off or check the status of appliances

Let you know if energy use is within budget

Monitor your home's total electricity usage in real time

Identify ways of improving your home's energy efficiency

Identify if there is a problem with any major appliances

Have appliances automatically minimize electricity usage

Monitor, program, and adjust your home's thermostat

Receive alerts when energy usage is high

Use sensors to know occupancy and automatically turn off lights and appliances

Monitor indoor security cameras

Monitor outdoor security cameras

Turn on/off the lights

Lock and unlock doors

Receive alerts when motion detectors are triggered

Receive alerts when there is a water leak

Receive alerts when there is a medical emergency

Receive alerts when doors or windows are opened

Receive alerts for carbon monoxide or a gas leak

Receive alerts for smoke or fire

Barriers - No Concise Value Proposition

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Most Appealing Smart Home Use Cases (Q2/14)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Barriers - Upfront, Recurring Fees

Source: Homeowners with Broadband at Home Q2 2013 | N=4,000 U.S. Broadband Homeowners | © 2013 Parks Associates

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Barriers - Interoperability

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Importance of Interoperability (Q2/14)%

Rep

ort

ing

“Ver

y Im

po

rtan

t”(R

atin

g 6

/7 w

ith

7=

“Ext

rem

ely

Imp

ort

ant”

)

1st device purchased(n=736, ±3.61%)

51%

2nd device purchased(n=573, ±4.09%)

58%

3rd device purchased(n=520, ±4.3%)

60%

The views expressed in this presentation do not necessarily reflect the views of AT&T.

39% 38%

24% 20%

Concern over unauthorized access Concern over historical data

Concerned (Rating 5) Very concerned (Rating 6-7)

Barriers– Privacy and Security

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Smart Home Privacy Concerns (Q2/14)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Drivers - Huge Brands Entering the Market

The views expressed in this presentation do not necessarily reflect the views of AT&T.

• Complementary Product Sales

• App Sales, Upgrades

• Advertising, Lead Generation

• Data Exchange

• Energy Savings, Demand Response

• Transaction Fees

• Subsidizing Upfront Costs

Drivers - Business Innovation

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Data Collection

Display

Modeling

Notifications

Prediction

Intelligent Control

Reporting

Adapt and Learn

Drivers - Data Creating Growing Value

The views expressed in this presentation do not necessarily reflect the views of AT&T.

• Low awareness

• No concise value proposition

• Initial cost, recurring fees

• Interoperability

• Privacy and security

Market Barriers

• Big brands entering market

• New business models

• Value-added services

Market Drivers

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Smart Product Adoption

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Two Paths to Market

Products Systems

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Yes, 13%No, 83%

I’m not sure, 4%

Smart Home Product Adoption

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Adoption of Smart Home Control Products (Q2/14)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

3%

3%

4%

4%

4%

4%

5%

5%

5%

5%

6%

6%

6%

6%

6%

Water leak detectors

Sprinkler system

Blinds or drapes

Combination sensor

Home or Kitchen appliances

Power strip

Door bells

Outlet/plug

Carbon monoxide detectors

Garage door openers

Door locks

Security camera

Smoke detectors

Programmable thermostat

Lights

Smart Home Product AdoptionAdoption of at Least 1 of the Listed Smart Home Devices (Q2/14)

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% | © 2014 Parks Associates

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Smart Home Product Adoption

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Smart Home Devices as System or Stand-alone Device (Q2/14)

…part of a home control system that controls multiple devices

…stand alone devices, not part of any system

…part of a home security system58% 58% 52% 48% 50% 46% 48% 42% 42% 39% 36% 37% 32%

9% 8%9% 11% 9%

10% 7%12% 10% 12%

10% 8% 13%

32% 34% 39% 41% 41% 44% 45% 47% 48% 49% 54% 55% 55%

Do

or

lock

s

Secu

rity

cam

era

Co

mb

inat

ion

sen

sor

Wat

er

leak

det

ect

ors

Car

bo

n m

on

oxi

de

det

ecto

rs

Smo

ke d

ete

cto

rs

Do

or

bel

ls

Ligh

ts

Gar

age

do

or

op

ener

s

Ou

tlet

/plu

g

Pro

gram

mab

le t

her

mo

stat

Blin

ds

or

dra

pes

Po

wer

str

ip

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Value Added Services

The views expressed in this presentation do not necessarily reflect the views of AT&T.

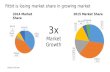

Value Added Services Command 3X Price

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

58%42%

Smart Thermostat: Preference (Q2/14)$99—A programmable thermostat that can:-Be monitored for status or controlled from a smartphone, tablet or computer

$299—A programmable thermostat that can:-Be monitored for status or controlled from a smartphone, tablet or computer

-Display the current weather forecast

-Use weather forecast to save money by running your air conditioner or furnace when it is most efficient

-Increase your home’s energy efficiency by “learning” your daily routines and temperature preferences

-Automatically make minor adjustments to save money by operating your system when electricity prices are low

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Value Added Services Command 4X Price

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

47%

53%

Smart Smoke Detector: Preference (Q2/14)

$29—A smoke detector that can:-Be monitored for status or controlled from a smartphone tablet or computer

$129—A smoke detector that can:-Be monitored for status or controlled from a smartphone, tablet or computer

-Send you alerts when the battery needs to be replaced

-Send you alerts when the alarm is triggered telling you about the event and location

-Automatically shut off the furnace or air conditioner in the event ofa fire

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Value Added Services Drive Replacement

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

While it’s still working properly,

61%

Only when it stops working properly, 39%

Advanced Smart Smoke Detector: Likelihood of Replacing Functioning Unit (Q2/14)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Bundling Services Together

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

21%

26%

26%

28%

29%

29%

29%

30%

30%

31%

31%

32%

34%

34%

34%

35%

36%

39%

39%

41%

41%

43%

45%

51%

Open a pet door

Turn on/off or check the status of appliances in your laundry area

Receive a daily summary of your home's energy usage

Understand your home's energy performance

Open and close your garage door

Turn on/off or check the status of appliances

Let you know if energy use is within budget

Monitor your home's total electricity usage in real time

Identify ways of improving your home's energy efficiency

Identify if there is a problem with any major appliances

Have appliances automatically minimize electricity usage

Monitor, program, and adjust your home's thermostat

Receive alerts when energy usage is high

Use sensors to know occupancy and automatically turn off lights and appliances

Monitor indoor security cameras

Monitor outdoor security cameras

Turn on/off the lights

Lock and unlock doors

Receive alerts when motion detectors are triggered

Receive alerts when there is a water leak

Receive alerts when there is a medical emergency

Receive alerts when doors or windows are opened

Receive alerts for carbon monoxide or a gas leak

Receive alerts for smoke or fire

Most Appealing Smart Home Use Cases (Q2/14)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

41%

40%

38%

38%

37%

36%

36%

35%

26%

28%

29%

30%

30%

31%

34%

34%

…receive a daily summary energy consumption

...understand your home’s energy performance

...let you know if energy use is within budget

…monitor your home’s total electricity usage in real time

…identify ways of improving your home’s energy efficiency

…identify problems with major appliances

…receive alerts when energy usage is high

...use sensors to automatically turn off lights and appliances when home is unoccupied

Not appealing (Rating 1-3) Very appealing (Rating 6-7)

Energy Related Use Cases

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Appeal of Smart Energy Features (Q2/14)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Source: American Broadband Households and Their Technologies Q2 2014 | N=10,000 broadband households, ±0.98% © 2014 Parks Associates

Willingness to Subscribe to Smart Energy Service (Q2/14)

Value of a Bundle of Energy Services

% o

f B

B H

Hs

“Ver

y Li

kely

” to

Su

bsc

rib

e

$9.99 per month

43%

$4.99 per month

59%

$2.99 per month

69%

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Tom KerberDirector of Research, Parks Associates

Thank You

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Bill Morelli

Consumer IoT

Director, IoT, M2M & Connectivity

IHS

Smartphones as the Passport to the IoT

The views expressed in this presentation do not necessarily reflect the views of AT&T.

• Internet of Things Overview• Definition• Evolution• Market Size

• Consumer IoT Market• Smart Home• Connected Car• Wearables

• Technology Insights

• Smartphone

Agenda

The views expressed in this presentation do not necessarily reflect the views of AT&T.

• IoT is a conceptual framework

• It’s about enabling connectivity and embedded intelligence in devices

• Some of these devices are connected today, but MANY are not

•Not strictly machine-to-machine (M2M) – also machine-to-people, people-to-machine, machine-to-objects, people-to-objects

•Creates the ability to collect data from a broad range of devices

•Data can be accessed via the cloud and analyzed using “big data” techniques

The Internet of ThingsWhat is the “Internet of Things”?

IoT can be used to provide unique value propositions and create complex information systems which are greater than the sum of the individual components.

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Industrial•Building Automation•Commercial Transportation• EFT-POS & Smartcards• Industrial Automation• Lighting•Power & Energy• Security• Test & Measurement•Other Industrial & Commercial

IoT Application SegmentsAutomotive• Infotainment•Under-the-hood

Communications•Consumer CPE• Enterprise CPE• Last-mile Access•Backbone•Mobile Handsets and Infrastructure

Computers•Desktop• Server•Portable Computing

(Netbook, Notebook & Tablet)

Medical•Consumer Medical• Imaging•Other Medical

Military & Aerospace•Commercial Aerospace•Military Equipment

Consumer•Home Appliance•Home Automation•Home Consumer Electronics•PC Peripherals & Office Equipment•Portable CE• Smart Toys• Sports and Fitness•Other Consumer

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Wired WPAN WLAN WWAN

• 2G Cellular• 3G Cellular• 4G Cellular

• 802.11a/b/g• 802.11n• 802.11ac• 802.11ad• Other 802.11• DECT ULE• Other 2.4GHz• Other Sub-GHz

• ANT+• Bluetooth –

Classic and Smart Ready

• Bluetooth Smart

W-Mesh

• ZigBee PRO• ZigBee RF4CE• ZigBee Multi-Protocol• EnOcean• ISA100.11a• WirelessHART• Z-Wave• Other 802.15.4

• Ethernet, Coax, Fiber, etc. considered as a single category

IoT Technologies

The views expressed in this presentation do not necessarily reflect the views of AT&T.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2012 2013 2014 2016 2019 2022 2025

Automotive Communications Computers Consumer

Industrial Medical Military & Aerospace Device Shipments

Source: IHS © 2014 IHS

IoT Extended Forecast - Internet Connectable Devices - Installed Base & Device Shipments

Ins

tall

ed

Ba

se

(M

)

De

vic

e S

hip

me

nts

(M

)

IoT Extended Forecast, 2011-2025Installed base

includes both active connections and

connectable devices which are

not networked

Industrial category includes a wide range on non-

consumer applications

(transportation, power and energy,

security, etc.)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

2013 2014 2015 2016 2017 2018 2019

Automotive Consumer CPE Consumer Medical Home AutomationHome CE PC Peripherals Portable & Desktop PC Portable CESmart Toys Sports & Fitness

Source: IHS © 2014 IHS

Consumer Internet Connectable Devices - Installed Base

Co

nn

ecta

ble

Devic

es (

K)

Consumer IoT Forecast, 2013-2019

Tablets, laptops and connected accessories are expected to see

continued growth

Smart Home is expected to see

significant uptake in the next 5 years

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Connect Devices

Collect Data

Access Data

Complex Analytics

Unique Value

Internet of Everything (IoE): Represents the open access to data from one or more monitoring and control systems by third-party applications to provide unique, additional value to stakeholders.

• Connectivity• Intelligence

• Sensors• Storage

• Cloud• Standards• Open APIs

• “Big Data” • Realize the true potential of a connected society…

Internet of Things Evolution

Next stage –security is key challenge!

Where we are today Ideal goal –many years away

The views expressed in this presentation do not necessarily reflect the views of AT&T.

• Three main IoT touchpoints for consumers to interact with IoT are home, car and wearables (everywhere)

• Smart Home

• Connected Car

• Wearables

Consumer IoT Market

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Consumer IoT Environments

Paradigm shift in the past decade – individuals used to access the internet at home and work.

Today, thanks to near ubiquitous wireless coverage, consumers can access the internet anywhere…

…and so can their devices.

The views expressed in this presentation do not necessarily reflect the views of AT&T.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2011 2012 2013 2014 2015 2016 2017 2018

Energy Management Hazard Detection

Healthcare or Independent Living Home Monitoring

Lighting Controls Other

Source: IHS © 2014 IHS

Smart Home Subscribers by Application

Sm

art

Ho

me S

ub

s (

K)

Smart Homes: Overview

What is a “Smart Home”?

• IHS: Low-bandwidth home network used for command or control applications

• Main application types:

• Energy Management

• Home Monitoring

• Hazard Detection

The views expressed in this presentation do not necessarily reflect the views of AT&T.

0

50,000

100,000

150,000

200,000

250,000

2012 2013 2014 2015 2016 2017 2018

Americas Asia Pacific EMEA

Source: IHS © 2014 IHS

Smart Home Device Shipments by Region

Sm

art

Ho

me

Su

bs

(K

)

Smart Homes: Forecast

• Annual smart home automation device shipments projected to grow from 25M in 2013 to 190M in 2018

• Home monitoring (safety and security) devices lead the way, driven by North American consumer requirements

• In US, service providers are forecast to see the highest growth in share; as multi-service operators like AT&T, Comcast, Time Warner and others start to penetrate mass-market households

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Key Points: Smart Home

• Diverse supplier landscape improving availability of affordable systems

• Varying consumer requirements, but security and privacy are vital

• Interoperability and user interface fragmentation

• Connected variants of smart home devices projected to slowly become the new “norm”

• Long life-cycle device OEMs look to connected devices to drive upgrades, offer value-add features and remain “current” throughout lifespan

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Key Trends Other InformationEmbedded Modem

• First telematics service• Leading telematics approach• Growth from eCall mandates

• OnStar is leading system• Through 2018• Europe, Russia and Brazil

Mobile or Smartphone

• Strong growth from Smartphone• Ford most successful system• Emerging services as apps

• Mostly a niche market earlier• Japan first: navigation services• Use Smartphone data plan

Hybrid or Both • Emerging as long-term favorite• Embedded for car-centric info• Smartphone for cloud content

• Leader after 2018• Due to higher security• Smartphone apps and data plan

Connected Car Trends

The views expressed in this presentation do not necessarily reflect the views of AT&T.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2014 2015 2016 2017 2018

Un

it S

ale

s (

#K

)

Source: IHS Automotive © 2014 IHS

Mobile Disruption in Automotive

Take-Away

• Google and Apple succeed as OEM partnerships grow

• CarPlay and Android Auto have shortened the window of opportunity for MirrorLink and increased barriers

MirrorLink Android Auto Apple CarPlay

Phone Projection Growth in Global OEM Platforms

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Key Points: Connected Car• Innovation in the connected car is occurring rapidly

outside of the “traditional” automotive supply chain

• Tech company partnerships and alliances are critical for automakers to stay relevant

• Connected car data becomes a critical component of daily operations and product development as 152 million vehicles begin transmitting 11.1PB of data by 2020

• Automakers are taking advantage of the connectivity and UX real estate offered by wearables to provide services and remote access

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Healthcare and MedicalBlood Pressure MonitorsGlucose MonitoringECG MonitorsPERS

Fitness and WellnessActivity MonitorsFitness and Heart Rate MonitorsPedometersSmart Clothing

InfotainmentBluetooth HeadsetsHead-up DisplaysImaging ProductsSmart GlassesSmart Watches

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2012 2013 2014 2015 2016 2017

World: Application store revenues ($m)

Apple App Store Google Play Other

Wearable Technology Overview• Market growing rapidly

• 2013: $10B from 105M units • 2019: $34B from 230M units (forecast)

• Service revenue to exceed $6B in 2019

• N. America and Europe account for 70% of global revenue

• Successful wearable app strategies should tie in to existing app ecosystems

The views expressed in this presentation do not necessarily reflect the views of AT&T.

44%

12%

11%

8%

7%

6%

4%2%

Health & Fitness

Lifestyle

Music

Utilities

Entertainment

Games

Sports

Photo & Video

Social Networking

Navigation

Business

Weather

Education

Health & Fitness services dominate apps for wearable

and peripheral devices

Wearable Tech AppsWearable and Peripheral Apps by Category (%)

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Key Points: Wearable Tech

• Device, service, app and OS compatibility is crucial

• So far, wearable apps and devices are an extension of smartphone ecosystems

• Health and Fitness apps dominate – but there is room for other categories

• Apps for wearables are unlikely to match smartphone and tablet app revenue success –but business models are evolving

• Advertising will play a role, with the correct data strategy

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Consumer IoT and Smartphones

• Role of the smartphone in Consumer IoT• Identity

• Security

• Data integration

• Opportunities for developers using smartphoneas entry point

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Cellular, Wi-Fi,

Bluetooth Classic, Wi-Fi, tether

Bluetooth Smart, ANT+, NFC

Smartphones

• Smartphones are the most connected device in the world based on the breadth of technologies

• Can communicate PAN, LAN, WAN

By 2017, 91% of handsets

sold will be smartphones

The views expressed in this presentation do not necessarily reflect the views of AT&T.

In 2016, smartphones will represent85% of mobile subscriptions

in the US

Smartphones: IoT Passport

• Smartphones already widely used in home

• Use in cars increasing, more integration coming

• Most wearables rely on smartphone tethering

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Smartphones are the entry point

to Consumer IoT!

Key Takeaways

• Much of the value of IoT will come from the integration of data from disparate sources

• Consumer IoT strategies should focus on interoperability, try to leverage multiple platforms

• Consumer requirements will vary based on vertical area, platform, and use case, but security and privacy are vital!!

• Don’t just solve today’s problems – look at solving future problems leveraging emerging classes of connected devices

The views expressed in this presentation do not necessarily reflect the views of AT&T.

© 2014 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be

permitted in the license agreement between client and IHS. Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information

contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted

by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information, please

contact IHS at [email protected], +1 800 IHS CARE (from North American locations), or +44 (0) 1344 328 300 (from outside North America). All products, company names or other marks

appearing in this publication are the trademarks and property of IHS or their respective owners. V2.0-29.04.14

Americas: +1.800.IHS.CARE (+1.800.447.273); [email protected]

Europe, Middle East, and Africa: +44.(0).1344.328.300; [email protected]

Asia and the Pacific Rim: +604.291.3600; [email protected]

Contact us

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Q&A

The views expressed in this presentation do not necessarily reflect the views of AT&T.

Thank You