Shopping for an Automobile Loan

What Do I Need to Know?

Using Standard Calculators

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Automobiles

2nd most expensive purchase for most consumers

Purchased with Cash Loan / credit – very common

Automobile Loans

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Definitions Auto Loan – borrowed money to

purchase an automobile Terms of the loan will vary

Lender – a financial institution who offers loans to consumers

Credit Rating – evaluation of a person’s credit history Based on repayment patterns, prior

credit usage, credit history, length of employment

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Definitions continued Cosigner – a person who guarantees the

loan for the original borrower Responsible for paying the debt back if the

original borrower defaults• Borrower fails to make payments of principle or

interest when due and has not met other requirements of the legal contract

A cosigner may be required for a loan if the original borrower does not have a credit history or has a bad credit rating

Common for parents to cosign for young adults

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Definitions continued Secured Loan – requires a cosigner

or collateral A loan with collateral means the lender

has security interest in the property pledged as collateral

Automobile loans are secured because the automobile is typically the collateral

If the borrower fails to repay the loan, the lender can then seize the collateral by repossessing, or taking back, the property

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Lender Options Auto Dealers Commercial Banks Savings and Loans Credit Unions Online lenders Life Insurance Policies Auto Insurance Companies

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Lender Options continued

Credit Unions traditionally offer low APRs

Auto dealer financing may be easier, but not always the best deal

Remember – compare every variable to decide best option for consumer

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Consumer Rights The Truth in Lending Act - 1968

Part of the Consumer Protection Act Applies to all credit transactions

• Mortgages, credit cards, loans, etc.

Requires clear disclosure of key terms and all costs in lending agreements

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

The Truth in Lending ActThree basic rules for lenders:1. Lenders cannot advertise a good deal

which is not available to all consumers2. Advertisements must include all or none

of the terms3. If more than 4 installments are required

to pay for the good or service, the agreement must say “The cost of credit is included in the price quoted for goods and services”

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

The Truth in Lending Act continued

Lenders must disclose to consumers: Interest rate expressed as the APR Total finance charge

Allows consumers to easily compare credit offers

What’s the Real Price?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Variables of a Loan Negotiated Price

Price being paid for the automobile agreed upon by the seller and buyer

Down Payment Amount of money being paid for the

automobile at time of purchase Usually required

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Variables continued Trade-In

Amount of money received for trading in an automobile

Trade-in amount is subtracted from the negotiated price of the automobile

Principle Loan Amount Amount of the loan for the automobile after

subtracting the down payment and/or trade-in price from the negotiated price

Without interest and fees

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Variables continued Annual Percentage Rate (APR)

Measure of the cost of credit on a yearly basis expressed as a percentage

Time Period Amount of time the loan will be repaid Usually expressed in months

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Variables continued Total Cost of the Loan

Total of the principal loan amount, interest paid, and other fees

Total Purchasing Cost Total of the down payment, trade-in

value, and total loan amount

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Rules of Thumb The larger the down payment on an

automobile, the lower the principle loan amount.

The longer the time period of the loan, the smaller the payments. However, more interest is paid.

The higher the APR, the more interest is paid and the larger the total loan amount.

Calculating the Cost

Using Standard

Calculators

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Calculating the Cost Three variables are required to

calculate the cost of a loan: Principal loan amount APR Time period

Using a standard calculator does not provide exact results, just estimates

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Equations To estimate the interest paid:

Principal loan amount * APR * Time period = Interest paid

To find the total loan amount: Interest paid + Principal loan amount =

Total loan amount To find the estimated monthly

payment: Total loan amount/number of payments =

Estimated monthly payment

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Calculating the Cost

Joe has decided to purchase an automobile Negotiated price - $7,500 Down payment - $2,500 APR – 8% Time Period – 3 years

What is it really going to cost?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Calculating the Cost $7,500 - $2,500 = $5,000

(Negotiated price – Down payment = Principal loan amount)

$5,000 over 3 years at 8% APR Step 1: Estimate the Interest Paid

(Principal loan amount * APR * Time Period = Interest Paid Principal loan amount: 5,000 Time period: 3 years (3*12 = 36 payments) APR: 8% $5,000 *.08 * 3 = $1,200 Estimated interest paid: $1,200

Step 2: Find the total loan amount $1,200 + $5,000 = $6,200

(Interest paid + principal loan amount = Total loan amount)

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

What’s the Real cost? Total loan amount = $6,200 Total purchasing cost =

total loan amount + down payment $6,200+ $2,500 = $8,700

Down Payment

How does the cost

change with different

down payment amounts?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Down Payments Calculate the cost of a $7,500 car

with an 8% APR over 36 months (3 years): $1,000 down payment $2,500 down payment

What are the monthly payments? How much interest is paid? What is the total purchasing cost?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Example #1 –$1,000 Down Payment

$7,500 - $1,000 = $6,500(Negotiated price – Down payment = Principal loan amount)

$6,500 over 3 years at 8% APR Step 1: Estimate the interest paid

Principal loan amount: $6,500 Time period: 36 months (3 years) APR: 8% $6,500 * .08 * 3 = $1,560 estimated interest paid (Principal loan amount * APR * Time period = Interest Paid)

Step 2: Find the total loan amount $1,560 + $6,500 = $8,060 (Interest paid + Principal loan amount = total loan amount)

Step 3: Find the estimated monthly payment $8,060 / 36 = $223 (Total loan amount / Number of payments = Estimated monthly payment)

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Example #2 –$2,500 Down Payment

$7,500 - $2,500 = $5,000 (Negotiated price – Down payment = Principal loan amount) $5,000 over 3 years at 8% APR Step 1: Estimate the interest paid

Principal loan amount: $5,000 Time period: 36 months (3 years) APR: 8% $5,000 * .08 * 3 = $1,200 estimated interest paid (Principal loan amount * APR * Time period = Interest Paid)

Step 2: Find the total loan amount $1,200 + $5,000 = $6,200 (Interest paid + Principal loan amount = total loan amount)

Step 3: Find the estimated monthly payment $6,200 / 36 = $172 (Total loan amount / Number of payments = Estimated monthly payment)

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Down Payments Example #1 - $1,000 down payment

• Principal loan amount - $6,500• Monthly payment - $223• Interest paid - $1,560• Total purchasing cost - $9,060

Example #2 - $2,500 down payment• Principal loan amount - $5,000• Monthly payment - $172• Interest paid - $1,200• Total purchasing cost - $8,700

Price Difference - $360 The higher the down payment, the lower the principal

loan amount.

Annual Percentage Rate (APR)

How does the cost

change with different

APRs?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

APRs Calculate the cost of a $7,500 car

with a $2,500 down payment over 36 months (3 years) at: 8% APR 10% APR

What are the monthly payments? How much interest is paid? What is the total purchasing cost?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

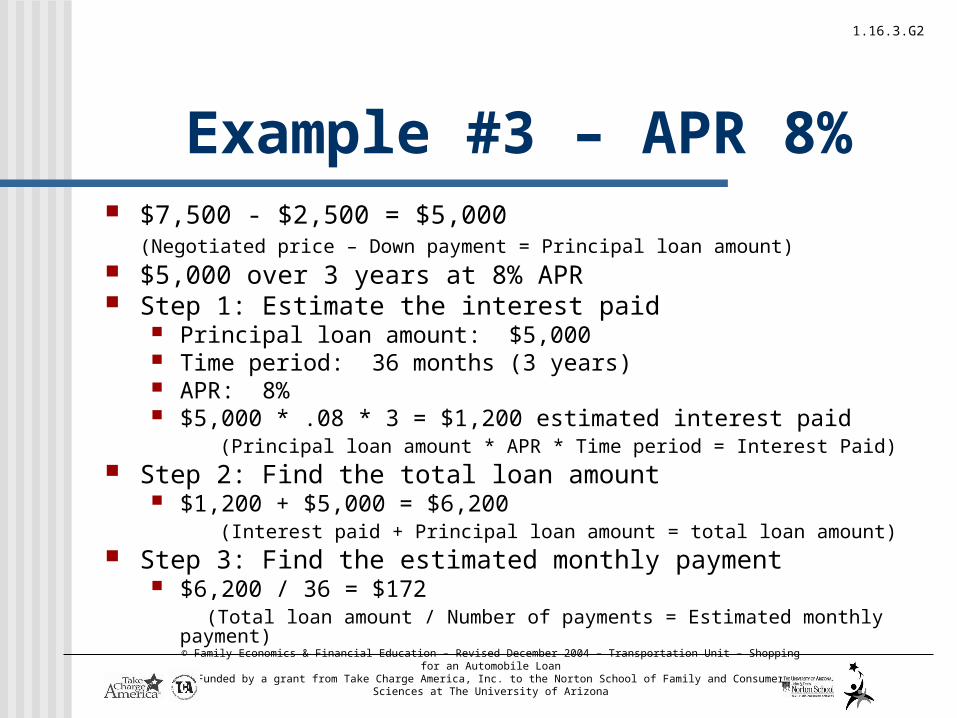

Example #3 – APR 8% $7,500 - $2,500 = $5,000

(Negotiated price – Down payment = Principal loan amount) $5,000 over 3 years at 8% APR Step 1: Estimate the interest paid

Principal loan amount: $5,000 Time period: 36 months (3 years) APR: 8% $5,000 * .08 * 3 = $1,200 estimated interest paid (Principal loan amount * APR * Time period = Interest Paid)

Step 2: Find the total loan amount $1,200 + $5,000 = $6,200 (Interest paid + Principal loan amount = total loan amount)

Step 3: Find the estimated monthly payment $6,200 / 36 = $172 (Total loan amount / Number of payments = Estimated monthly payment)

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

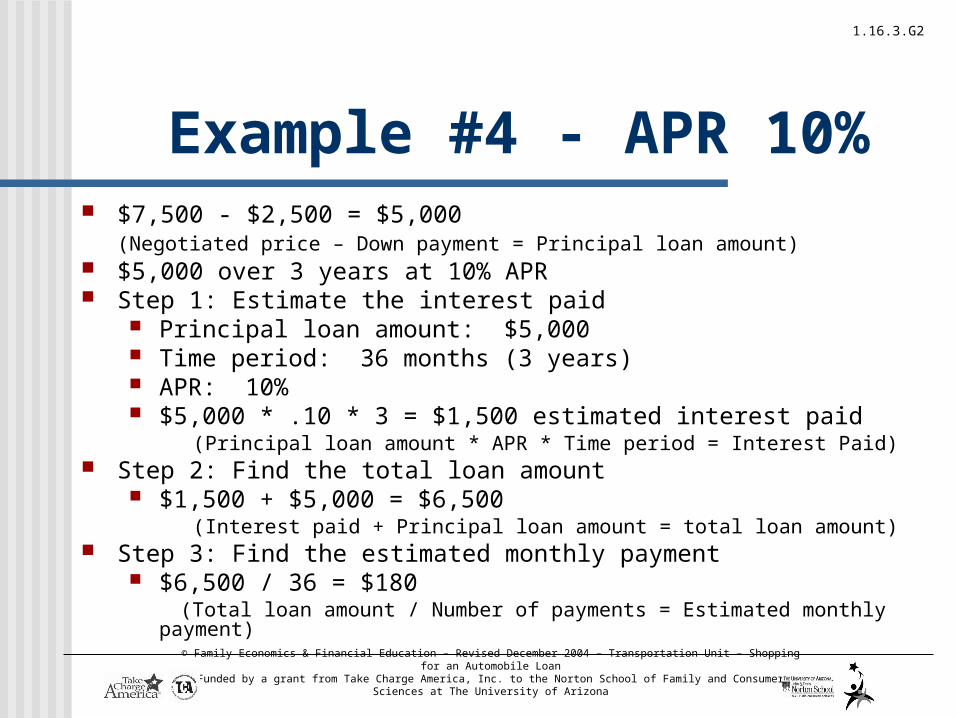

Example #4 - APR 10% $7,500 - $2,500 = $5,000

(Negotiated price – Down payment = Principal loan amount) $5,000 over 3 years at 10% APR Step 1: Estimate the interest paid

Principal loan amount: $5,000 Time period: 36 months (3 years) APR: 10% $5,000 * .10 * 3 = $1,500 estimated interest paid (Principal loan amount * APR * Time period = Interest Paid)

Step 2: Find the total loan amount $1,500 + $5,000 = $6,500 (Interest paid + Principal loan amount = total loan amount)

Step 3: Find the estimated monthly payment $6,500 / 36 = $180 (Total loan amount / Number of payments = Estimated monthly payment)

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

APRs Example #3 – 8% APR

• Monthly payments - $172• Interest paid - $1,200• Total purchasing cost - $8,700

Example #4 - 10% APR• Monthly payments - $180• Interest paid - $1,500• Total purchasing cost - $9,000

Price Difference - $300 The higher the APR, the more interest paid.

Time Period

How does the cost

change with different

time periods?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Time Periods Calculate the cost of a $7,500 car

with a $2,500 down payment with an 8% APR over: 36 months (3 years) 60 months (5 years)

What are the monthly payments? How much interest is paid? What is the total purchasing cost?

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Example #5 – 3 years $7,500 - $2,500 = $5,000

(Negotiated price – Down payment = Principal loan amount) $5,000 over 3 years at 8% APR Step 1: Estimate the interest paid

Principal loan amount: $5,000 Time period: 36 months (3 years) APR: 8% $5,000 * .08 * 3 = $1,200 estimated interest paid (Principal loan amount * APR * Time period = Interest Paid)

Step 2: Find the total loan amount $1,200 + $5,000 = $6,200 (Interest paid + Principal loan amount = total loan amount)

Step 3: Find the estimated monthly payment $6,200 / 36 = $172 (Total loan amount / Number of payments = Estimated monthly

payment)

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Example #6 – 5 years $7,500 - $2,500 = $5,000

(Negotiated price – Down payment = Principal loan amount) $5,000 over 5 years at 8% APR Step 1: Estimate the interest paid

Principal loan amount: $5,000 Time period: 60 months (5 years) APR: 8% $5,000 * .08 * 5 = $2,000 estimated interest paid (Principal loan amount * APR * Time period = Interest Paid)

Step 2: Find the total loan amount $2,000 + $5,000 = $7,000 (Interest paid + Principal loan amount = total loan amount)

Step 3: Find the estimated monthly payment $7,000 / 60 = $116 (Total loan amount / Number of payments = Estimated monthly

payment)

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Time Periods Example #5 - 3 years

• Monthly payment - $172• Interest paid - $1,200• Total purchasing cost = $8,700

Example #6 - 5 years• Monthly payment - $116• Interest paid - $2,500• Total purchasing cost - $9,500

Price Difference - $800 The longer the time period of the loan, the

smaller the payments. However, more interest is paid.

© Family Economics & Financial Education – Revised December 2004 – Transportation Unit – Shopping for an Automobile Loan

Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at The University of Arizona

1.16.3.G2

Conclusion

Compare all offers and variables before signing an agreement!

Changing a variable can either save the consumer money or he/she may end up paying much more than anticipated!