Secular Stagnation, Financial Frictions, and Land Prices

Zhifeng Cai

Rutgers University

Federal Reserve Bank of Philadelphia, November 2019

1 / 44

Introduction

I Many works have been done on the causes of the 2008 Great Recession

I Two main channels: house price bust and financial distress

I Much less on what drives the slow recovery after the Great Recession

I Question: What role does housing and financial frictions play in driving the

“secular stagnation” after the recession?

I This paper: presents a model where large transitory financial shocks can

generate persistent slumps in outputs, house prices, and interest rates that

resemble a secular stagnation

2 / 44

Motivation House Price GDP Structual Break

-.15

-.1

-.05

0%

dev

iatio

n fr

om tr

end

0 5 10 15 20Quarters after recessions start

The Great Recession

Previous Recessions

GDP

-.4

-.3

-.2

-.1

0.1

% d

evia

tion

from

tren

d

0 5 10 15 20Quarters after recessions start

Investment-.

15-.

1-.

050

% d

evia

tion

from

tren

d

0 5 10 15 20Quarters after recessions start

Hours

-.4

-.3

-.2

-.1

0.1

% d

evia

tion

from

tren

d

0 5 10 15 20Quarters after recessions start

House Price

3 / 44

This Paper

I Key feature: Financial frictions lead to existence of multiple “regimes”

(locally stable steady states)

I Nonlinearity: Asymmetric responses to small and large negative

shocks

I large shocks → regime switch → push the economy to the bad

steady state

I The good steady state corresponds to the classic neoclassic steady

state

I The bad steady state resembles secular stagnation: low output, land

prices, and interest rates

4 / 44

How?

I Models with financial frictions typically cannot generate quantitatively

strong amplification and propagation (Kocherlakota, 2000; Cordopa and

Ripoll, 2004)

I One concern is that in these class of models the asset price volatility is too

low (Quadrini, 2011)

I This paper proposes a “land consumption channel” that addresses this

I Land has not only collateral value but also consumption value

I The consumption value of land can be highly volatile if land services

(housing) and other consumption are highly complementarity

I The high volatility of land value implies that the collateral constraint

matters quantitatively

5 / 44

The paper

I The paper consists of a theoretical part and a quantitative part

I First, embed the land consumption channel into a standard neoclassic

growth model

I Prove that the model exhibits multiple steady states if land services

and consumption are sufficiently complementarity

I Second, quantify the model and discipline this complementarity with

structural estimates.

I The resulting law of motion for capital is S-shaped with multiple

stationary points.

I At the bad steady state, firms are permanently constrained, leading to

secular stagnation

6 / 44

How Secular Stagnation Happens

I Imagine a recession that destroys certain amount of capital

I Asset (land) prices are low, constraining firms’ ability to borrow, reducing

their investment, reinforcing low capital ⇒ Bad steady state

I Why can’t the firms accumulate financial assets or simply issue equity to

grow out of the bad steady state?

1. Due to house price bust, the households experience painful

deleveraging

2. This drives down the equilibrium interest rate, making firms unwilling

to hold financial asset

3. Low consumption and tight borrowing constraint imply households

unwilling to purchase equity

I The interaction between firm-side and household-side borrowing constraints

lead to secular stagnation

7 / 44

Related Literature

I Macro models with collateral constraints (Kiyotaki and Moore, 1997)

I Role of land prices: Iacoviello (2005), Liu, Wang, & Zha (2013)

I Working capital: Mendoza (2010), Jermann and Quadrini (2012)...

I Secular Stagnation

I Shimer (2012); Fajgelbaum, Schaal, and Taschereau-Dumouchel

(2015); Schaal and Taschereau-Dumouchel (2015, 2016); Benigno and

Fornaro(2018); Eggertsson et al.(2019)...

I Empirical estimates of IES between housing and consumption

I Hanushek and Quigley(1980), Flavin and Nakagawa(2008), Siegel

(2008), Stokey(2009), Li, Liu, Yang, and Yao(2018);...

I Empirical evidence on real-estate prices and investment/employment

I Chaney, Sraer, and Thesmar (2012); Mian and Sufi (2013);

Chodorow-Reich(2014); Adelino, Schoar, and Severino (2015);

Benmelech, Bergman, Seru (2015); Giroud and Mueller (2017)...

8 / 44

Model

9 / 44

Model

I Discrete time. Infinite horizon

I Two types of agents: households and firms. Households are owners of

the firms.

I Land: of fixed supply L; can be used for consumption or production.

I Both capital and land can serve as collateral for its owner (be it

household or firm)

10 / 44

The Firms’ Problem

I Start with land l1t−1, capital kt−1, and intertemporal debt b1t−1.

I Hire labor n1t at rate wt and produce F (zt, kt−1, n1t, l1t)

I Simplifying assumption: capital is pre-determined but not land. Kills

land as a state variable.

I Isomorphic to the existence of a land rental market.

I Dividend dt is distributed after making investment decision it, debt

issuance decision b1t/Rt, and land allocation decision l1t:

b1t−1 + dt + it + pt (l1t − l1t−1) ≤ F (zt, kt−1, n1t, l1t)− wtn1t +b1tRt

I Next period capital is given by:

kt = (1− δ) kt−1 + it

11 / 44

Financial Friction

I The modeling of financial friction follows Mendoza (2010) and

Jermann and Quadrini (2012)

I Besides issuing intertemporal debt, the firm needs to raise funds with

an intra-period loan to finance working capital.

I Working capital is required to cover cash flow mismatch between

payments to various parties (workers, etc) and production revenue

I Total (inter. + intra.) borrowing is limited by a fraction of the

collateral asset:

b1tRt

+ F (zt, kt−1, n1t, l1t) ≤ ξ1tptl1t + κtkt

12 / 44

The Firms’ Problem

max{b1t,kt,l1t,it,n1t,dt} E∑∞

t=1Mtdt

b1t−1 + dt + it + pt (l1t − l1t−1) ≤ F (zt, kt−1, n1t, l1t) − wtn1t + b1tRt

b1tRt

+ F (zt, kt−1, n1t, l1t) ≤ ξ1tptl1t + κtkt

kt = (1 − δ) kt−1 + it

k0, l10, b10 given

I Constant Return to Scale Production Function:

F (z, k, n, l) = z[lγk1−γ

]αn1−α

13 / 44

The Households’ Problem

I Start period t with land holding l2t−1 and debt b2t−1.

I His income include labor income wtn2t and capital income dt.

I In each period he chooses consumption and next period land and

bond holdings subject to the following budget constraint:

b2t−1 + ct + pt (l2t − l2t−1) ≤ dt + wtn2t +b2tRt

(1)

I The household can borrow with land as collateral:

b2tRt

≤ ξ2tptl2t (2)

14 / 44

The households’ problem

max{b2t,l2t,ct,n2t} E∑∞

t=1 βtU (ct, n2t, l2t)

b2t−1 + ct + pt (l2t − l2t−1) ≤ dt + wtn2t + b2tRt

b2tRt

≤ ξ2tpl2t

n2t ≤ n, k0, l20, b20 given

15 / 44

Preference

U(ct, n2t, l2t) =

[ω(ct − χn2t

1+1/ν

1+1/ν

)1−1/σ

+ (1 − ω) l1−1/σ2t

] 1−1/η1−1/σ

1 − 1/η

I CES form of utility function where σ captures the intratemporal

elasticity of substitution between the (composite) consumption

and land

I The composite consumption term implies no wealth effect on

labor supply (GHH preference)

16 / 44

Competitive Equilibrium

DefinitionA competitive equilibrium is defined in a standard way in which the firm

and the households maximize their respective objectives given market

prices, and the markets for goods, labor, land and bonds all clear:

1. Goods: ct + it = yt

2. Labor: n1t = n2t

3. Land: l1t + l2t = L

4. Bond: b1t + b2t = 0

Lastly, the firm’s pricing kernel is equal to the household’s marginal utility:

Mt = βtUct

17 / 44

Characterization

I In the absence of equity issuance friction, household borrowing

constraint binds if and only if firm borrowing constraint binds

I Suppose otherwise, firm constraint binds but not the household one

I The firm can reduce dividend payment, and the household can

increase inter-borrowing to maintain the same level of consumption

I This relaxes the firm’s borrowing constraint and yields higher output

I Thus, the two constraints must bind at the same time

18 / 44

Characterization

I Thus, we can write the two borrowing constraints as one aggregate

constraint:

b1t + b2tRt

+ F (zt, kt−1, n1t, l1t) ≤ ξ2tptl2t + ξ1tptl1t + κtkt

I Or, with bond market clearing condition:

F (zt, kt−1, n1t, l1t) ≤ ξ2tptl2t + ξ1tptl1t + κtkt

I The bond distribution is irrelevant for equilibrium allocations

19 / 44

Isomorphism to Representative Agent

I Given that the bond distribution is irrelevant, we can aggregate

household and firm into one single agent solving:

max{l1t,l2t,ct,nt} E∑∞

t=1 βtU (ct, nt, l2t)

ct + kt − (1− δ)kt−1+∑

i=1,2 pt (lit − lit−1) ≤ F (zt, kt, l1t, nt)

F (zt, kt, n1t, l1t) ≤ ξ2tptl2t + ξ1tptl1t + κtkt

k0, l10, l20 given

I We also don’t need to keep track of the land distribution:

consumption and production take place using ex post land holdings

I The only endogenous state variable is capital accumulation

20 / 44

Steady-State Interest Rate

I The steady-state interest rate is pinned down by:

1

R= β +

λ

R

where λ is the multiplier on the collateral constraint

I Accumulating financial assets not only increases future consumption,

but also relaxes future borrowing constraint

Proposition

The steady-state interest rate is decreasing in the tightness of the collateral

constraint (measured by λ)

R =1− λβ

(3)

I If constraint binds, the gross interest rate could be less than 1

depending on how tight the collateral constraint is.

21 / 44

Steady State Multiplicity

22 / 44

Strategy

I Given any land price p, solve the representative agent problem at

steady state, and obtain the steady-state land demand (sum of

residential l1 and commercial l2 land demand)

L(p) = l1(p) + l2(p)

I Look for p such that the land market clears:

L(p) = L

I Goal: show that the L(.) function is nonmonotonic with financial

frictions

23 / 44

Land Consumption Channel

I Absence frictions, the model collapses to a standard growth model,

thus land demand L is monotonically decreasing in price p

I In the presence of financial frictions, land demand could be increasing

in price p. This nonmonotonicity comes from residential land demand:

1− ωω

(c

l2

) 1σ

︸ ︷︷ ︸Consumption benefit (MRS)

+ ξ2pλ︸︷︷︸Collateral benefit

− (1− β)p︸ ︷︷ ︸User cost

= 0

I When land price p ⇑, output increases, (composite) consumption c ⇑,

demand for residential land l2 ⇑, the magnitude depends on

substitution parameter σ

24 / 44

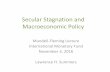

Theorem

Suppose σ (substitution in utility) and γ (land share in production)

are sufficiently small. Then for some combination of loan-to-value

ratios, there exists:

1. a unique unconstrained steady state, in which the collateral

constraint is slack and

2. at least two constrained steady states, in which the collateral

constraints are binding.

25 / 44

Graphic Illustration

Frictionless steady state A

Household demand is upward-sloping𝑙2′ 𝑝𝑠𝑠 > 0 (Lemma 3.1)

Aggregate land demand function is upward-sloping 𝐿′ 𝑝𝑠𝑠 = 𝑙1

′ 𝑝𝑠𝑠 +𝑙2′ 𝑝𝑠𝑠 > 0

Land demand 𝐿 → +∞as land price 𝑝 → 0

C B

Frictionless land demand is downward-sloping (Proposition 3.3)

𝑝1

𝐿 𝑝1 > 0

𝑝2

𝐿 𝑝2 < 0

𝑝3

𝐿 𝑝3 > 0

Figure 1: Graphical Illustration of Theorem 1

26 / 44

Remark on Interest Rate

I The interest rates of constrained steady states are lower than the

interest rate of the unconstrained steady state, due to the binding

collateral constraint.

I Transitions from good to bad steady state would entail a decline of

the interest rate

27 / 44

Quantitative Analysis

28 / 44

Calibration

Table 1: Calibration

Parameters Value Source

Discount factor β 0.99 Quarterly modelIntertemporal elasticity η 0.5 StandardDisutility of working χ 2.41 Steady state labor equal to .33Frisch Elasticity ν 4 Macro StudiesPref. weight ω 0.27 Land value/GDP= 1.06Depreciation δ 2.5% StandardCapital share α 0.35 StandardLand share αγ 0.03 Share of commer./res. land=.5Intratemporal Elasticity σ 0.487 Micro estimates (Li et al. 2016)Aggregate land stock l 1 Normalization

29 / 44

Calibration

Elasticity of Substitution between Housing and Consumption σ

I Most micro estimates between 0.13 and 0.6

I Hanushek and Quigley(1980), Flavin and Nakagawa(2008),

Siegel (2008), Stokey(2009), Li, Liu, Yang, and Yao(2016)

I Set η = 0.487 as in the structural estimation of Li, Liu, Yang, and

Yao(2016)

Loan-to-value Ratio ξ, κ

I Constraint occasionally binding ⇒ cannot estimate using steady state

targets

I Set it so that constraint only binds in big recessions

I Set ξ = κ = 0.03: Constraint binds with about 6% drop in

output

30 / 44

Dynamics: Multiple Steady States

Current Capital 𝐾𝑡

Futu

re C

apit

al

450 𝑙𝑖𝑛𝑒

Good Steady State(unconstrained)

Bad Steady State(constrained)

Frictionless Model Model with Collateral Constraint

Middle Unstable Steady State

Region Converging to bad steady state Region Converging to good steady state

Constrained Region Unconstrained Region

Figure 2: Law of Motion for Capital

31 / 44

Transitional Dynamics

I Transitional dynamics depend on how much capital lost

during the recession

I More capital lost during the recession, slower the recovery.

32 / 44

Transitional Dynamics

10 20 30 40 50 60 70 80 90 1000.92

0.94

0.96

0.98

1Output

10 20 30 40 50 60 70 80 90 1000.92

0.94

0.96

0.98

1Labor

10 20 30 40 50 60 70 80 90 1000.92

0.94

0.96

0.98

1

1.02Investment

Small RecessionMedium RecessionLarge Recession

10 20 30 40 50 60 70 80 90 1000.8

0.85

0.9

0.95

1Land Price

33 / 44

Isolating the Collateral Channel

I Consider an alternative economy where land price is

exogenously fixed at the unconstrained steady state level

(call it fixed-p economy)

I This captures scenario where there is a severe recession but

without financial amplification through collateral constraint

I Model no longer displays slow recovery

34 / 44

Transitional Dynamics(Fixed-p Economy)

10 20 30 40 50 60 70 80 90 1000.975

0.98

0.985

0.99

0.995

1Output

10 20 30 40 50 60 70 80 90 1000.98

0.985

0.99

0.995

1Labor

10 20 30 40 50 60 70 80 90 1001

1.005

1.01

1.015

1.02Investment

10 20 30 40 50 60 70 80 90 1000.85

0.9

0.95

1Land Price

Small RecessionMedium RecessionLarge Recession

35 / 44

Accounting for the Slow Recovery

36 / 44

Narratives of the Great Recession and Aftermath

I Large swings in house demand create boom-bust in house prices

I Collapse of the financial sector lead to large financial shocks

I Productivity slow down after the Great Recession

37 / 44

Quantitative Strategy

Feed into the model:

I A sequence of housing demand shocks

I To match house prices between 2007Q4 to 2016Q1

I Not just the decline but the subsequent house price recovery

I A sequence of credit shocks

I To match output decline between 2007Q4 to 2009Q4

I Examine the model’s ability to explain subsequent stagnation

I A sequence of productivity shocks

I Independently computed as the Solow residual

38 / 44

Accounting for the Slow Recovery

2008 2009 2010 2011 2012 2013 2014 2015 2016-1

-0.5

0

% D

evia

tion

Demand (Taste) Shock

2008 2009 2010 2011 2012 2013 2014 2015 2016

-0.2

-0.1

0

0.1

% D

evia

tion Lehman Bankruptcy Credit Shock

2008 2009 2010 2011 2012 2013 2014 2015 2016

Year

-0.04

-0.02

0

0.02

0.04

% D

evia

tion

Productivity Shock

39 / 44

Accounting for the Slow Recovery

2008 2010 2012 2014 2016-0.2

-0.15

-0.1

-0.05

0

% D

evia

tion

Output

DataModel

2008 2010 2012 2014 2016-0.2

-0.15

-0.1

-0.05

0

% D

evia

tion

Hours

2008 2010 2012 2014 2016

Year

-0.5

-0.4

-0.3

-0.2

-0.1

0

% D

evia

tion

Investment

2008 2010 2012 2014 2016

Year

-0.5

-0.4

-0.3

-0.2

-0.1

0

% D

evia

tion

House Price

40 / 44

Compared to Fixed-p Model without Financial Amplification

2008 2010 2012 2014 2016-0.2

-0.15

-0.1

-0.05

0%

Dev

iatio

n

Output

DataBench ModelFixed-p Model

2008 2010 2012 2014 2016-0.2

-0.15

-0.1

-0.05

0

% D

evia

tion

Hours

2008 2010 2012 2014 2016-0.5

-0.4

-0.3

-0.2

-0.1

0Investment

2008 2010 2012 2014 2016

Year

-0.5

-0.4

-0.3

-0.2

-0.1

0

% D

evia

tion

House Prices

41 / 44

Decomposition of Output

2008 2009 2010 2011 2012 2013 2014 2015 2016-18

-16

-14

-12

-10

-8

-6

-4

-2

0

2

% D

evia

tion

Fro

m P

re-c

risis

Lev

el

-16.9

-13.5

-4.3-4.9

-3.3

DataModel (All Three Shocks)Demand Shock OnlyProd. Shock OnlyCredit Shock Only

42 / 44

Interest Rate

2008 2009 2010 2011 2012 2013 2014 2015 2016-8

-6

-4

-2

0

2

4

6

Per

cent

age

Poi

nts

%

Annualized Interest Rate

Data (Federal Funds Rate)ModelConstrained Interest Rate=0.85%

43 / 44

Conclusion

I The paper: A model to explain the slow recovery after the 2008

financial crisis

I Key feature: Multiple steady states and nonlinear dynamics

I Crucial ingredient: Dual role of land as households’ consumption and

firms’ collateral

I Quantitative discipline: Housing-consumption complementarity from

cross-sectional evidences and structural estimates

I Quantitative findings:

I The model can generate persistent recessions comparable to

post-Great Recession data

I Credit Shock, albeit short-lived, contributes non-trivially to the

slow recovery

44 / 44

Real GDP Back

8.5

99.

510

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

1 / 8

House Price Index Back

11.

52

2.5

1975 1985 1995 2005 2015Real House Price Index

Constant 2% Growth Trend

S&P/Case-Shiller U.S. National Home Price Index, deflated by GDP deflator

2 / 8

Land Price Index Back

12

34

56

1975 1985 1995 2005 2015Real Land Price Index

Constant Growth Trend

Lincoln Institute of Land Policy, Davis and Heathcote(2007)

3 / 8

Motivation Back

-.08

-.06

-.04

-.02

0.0

2%

dev

iatio

n fr

om tr

end

0 5 10 15 20Quarters after recessions start

GDP

-.4

-.3

-.2

-.1

0.1

% d

evia

tion

from

tren

d

0 5 10 15 20Quarters after recessions start

Investment

-.1

-.05

0.0

5%

dev

iatio

n fr

om tr

end

0 5 10 15 20Quarters after recessions start

Labor

-.4

-.3

-.2

-.1

0.1

% d

evia

tion

from

tren

d

0 5 10 15 20Quarters after recessions start

House Price

Detrended with a Structual Break at Year 1989

4 / 8

Cross sectional evidenceQuestion: Is there a systematic relation between the extent ofhousing price drop and pace of recovery at the MSA level?

-.2

-.15

-.1

-.05

0.0

5Lo

g D

evia

tion

Fro

m T

rend

1990 1995 2000 2005 2010 2015Employment

MSA with smallest housing price delineMSA with medium housing price delineMSA with biggest housing price deline

5 / 8

Quantity of land grows smoothly.8

.91

1.1

1.2

1.3

1.4

1.5

1975 1985 1995 2005 2015Quantity Index of Residential Land

Lincoln Institute of Land Policy, Davis and Heathcote(2007)

6 / 8

Quantity of land grows smoothlyBack

11.

21.

41.

61.

8

1950 1960 1970 1980 1990Quantity Index of Commercial Land

Lincoln Institute of Land Policy, Davis and Heathcote(2007)7 / 8

Accounting for the labor wedge Back

2004 2006 2008 2010 2012 2014 2016-0.02

0

0.02

0.04

0.06

0.08

0.1

0.12Data

2004 2006 2008 2010 2012 2014 2016-0.2

0

0.2

0.4

0.6

0.8

1

1.2Model

Labor WedgeFirm Component

8 / 8