Opportunities and Challenges for SME’s in Islamic Finance

Ahmed Rostom Financial Sector Specialist

East Asia and Pacific Finance and Private Sector Development (EASFP)

The World Bank April, 18th, 2013

Objective

2

The objective of this presentation is to provide an overview of the opportunities and challenges facing SME’s Islamic Finance.

3

Road Map

• Global Islamic Finance Industry: A Brief Overview

• Structure of SME’s – Islamic Finance

• Foundations of SME’s – Islamic Finance: o Financial Inclusion o Entrepreneurship & Intermediation o Risk Sharing Friendliness

• Conclusion and Progress Discussion

Source: Central Banks, IFIS, Bloomberg, Zawya, World Islamic Insurance Directory 2012, The Banker, KFHR

Islamic Financial Assets 2011 (by Region and Financial Instrument)

Banks are dominating the seen

GCC 39%

Asia 21%

Others* 4% Sub-

Saharan Africa

1%

MENA (exc. GCC) 35%

Global Islamic Finance Industry: A Brief Overview

30%

26%

% of Banks offering sharia-compliant products

% of Banks planning tooffer sharia-compliantproducts in 12 months

Shariah Compliant Products Non-GCC MENA

4

413

15640 2 17

Murabaha Qard hassan Musharaka/Mudaraba

Salam Other

Portfolio, by type of product (USD million)

Global Shariah Compliant MSME finance: Concentrated …Lacks Instruments Diversification

And Relies Less on Investment Contracts

Source: CGAP 2010

Structure of SME’s – Islamic Finance

5

Foundations of SME’s – Islamic Finance

Financial Intermediaries

Projects

6

I – Financial Inclusion

II – Entrepreneurship & Intermediation

III – Risk Sharing Friendliness

Entrepreneurs

Savings

Direct partnership flows and revenues

Risk sharing contracts flows and revenues

Source: www.worldbank.org/globalfindex , The World Bank, April 2012

Islamic finance has a long way to go towards expanding financial inclusion

7

I - Financial Inclusion

8

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Arab World South Asia OIC Sub-SaharanAfrica

Latin America& Caribbean

Middle East &North Africa

Europe &Central Asia

East Asia &Pacific

New business density (new registrations per

1,000 people ages 18-64)

0

10

20

30

40

50

60

70

Entrepreneurial Intention

0

5

10

15

20

25

30

35

40Total early-stage Entrepreneurial Activity

II - Entrepreneurship and Intermediation

Despite the Entrepreneurial Potential … Entrepreneurial activities in OIC are Constrained…

Source: Global Entrepreneurship Monitor, 2013

Percentage of 18-64 population who are either a nascent entrepreneur or owner-manager of a new business (as defined above)

Percentage of 18-64 population (individuals involved in any stage of entrepreneurial activity excluded) who intend to start a business within three years

Moreover… access to affordable finance is a challenge for SME’s growth

Share of firms reporting cost of/access to finance (percent) 0 10 20 30 40 50 60 70

High income

East Asia & Pacific

Europe & Central Asia

Latin America & Caribbean

Middle East & North Africa

South Asia

Sub-Saharan Africa

Access to finance Cost of finance

Source: The World Bank 2008 9

II - Entrepreneurship and Intermediation

0.5% 1% 2% 2% 2% 2%

4% 4% 5%

6%

10%

13%

15% 16%

20%

24%

0%

5%

10%

15%

20%

25%

30%

SME loans/Total loans MENA countries

Source: World Bank 2011 10

II - Entrepreneurship and Intermediation

SME’ finance Gap is an opportunity …

Source: IFC 2011 11

II - Entrepreneurship and Intermediation

126 109 112 108

85 93 113 114 107 110

97 78

99 115

020406080

100120140

OPEC 2013 OIC 2013 OIC - GCC2013

MENA 2013 GCC 2013 EAP 2013 DevelopingCountries

2013DB 2013 DB 2011

44 35 38

23 15

36 31

43 40 44

20 15

40 38

0

10

20

30

40

50

OPEC 2013 OIC 2013 OIC - GCC2013

MENA 2013 GCC 2013 EAP 2013 DevelopingCountries 2013DB 2013 DB 2011

III - Risk Sharing Friendliness: Institutional Quality Starting a Business

Overall rank

Time (days)

12 Source: Doing Business Database; The World Bank 2013

Cost (% of income per capita)

4.2

2.6 2.3

3.6

4.5

2.4 2.5 2.8 2.3 2.1

3.3 3.8

2.0 2.0

0

1

2

3

4

5

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountriesDB 2013 DB 2011

102 115 118 124

93 91 104 110 117 120 116

94 94 108

020406080

100120140

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountries

DB 2013 DB 2011

Getting Credit Overall rank

Strength of legal rights index

3.9 4.9 5.0 3.0

4.2 6.5 5.6

3.9 4.1 4.1 3.0

4.0 6.0

4.9

02468

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountriesDB 2013 DB 2011

Source: Doing Business Database; The World Bank 2013 13

Depth of credit information

III - Risk Sharing Friendliness: Institutional Quality

111 116 116 113 110 87

115 114 116 116 115 117 88

113

020406080

100120140

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountries

DB 2013 DB 2011

592 671 682 652

588 522

654 594 667 677 664

590 547 649

0100200300400500600700800

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountries

DB 2013 DB 2011

43 41 40 44 47 37 40

28

39 41

24 20

47 47

0

10

20

30

40

50

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountriesDB 2013 DB 2011

Enforcing Contracts Overall rank

Time

Procedures (number)

14 Source: Doing Business Database; The World Bank 2013

III - Risk Sharing Friendliness: Institutional Quality

3.4 3.3 3.3 3.0 3.3 2.5

2.9 3.4 3.1 3.1 2.9

3.3 2.5

3.0

0

1

2

3

4

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountries

DB 2013 DB 2011

17.3 16.1 16.3

11.9 14.7

18.9 18.5 17.3 15.2 15.3

11.4 14.7

18.9 18.5

0

5

10

15

20

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountriesDB 2013 DB 2011

24.5 28.6 26.8 30.1

41.2

30.4 20.6 23.9 26.3 24.6 27.9

39.9 30.2

20.3

01020304050

OPEC OIC 2013 OIC - GCC MENA GCC EAP 2013 DevelopingCountriesDB 2013 DB 2011

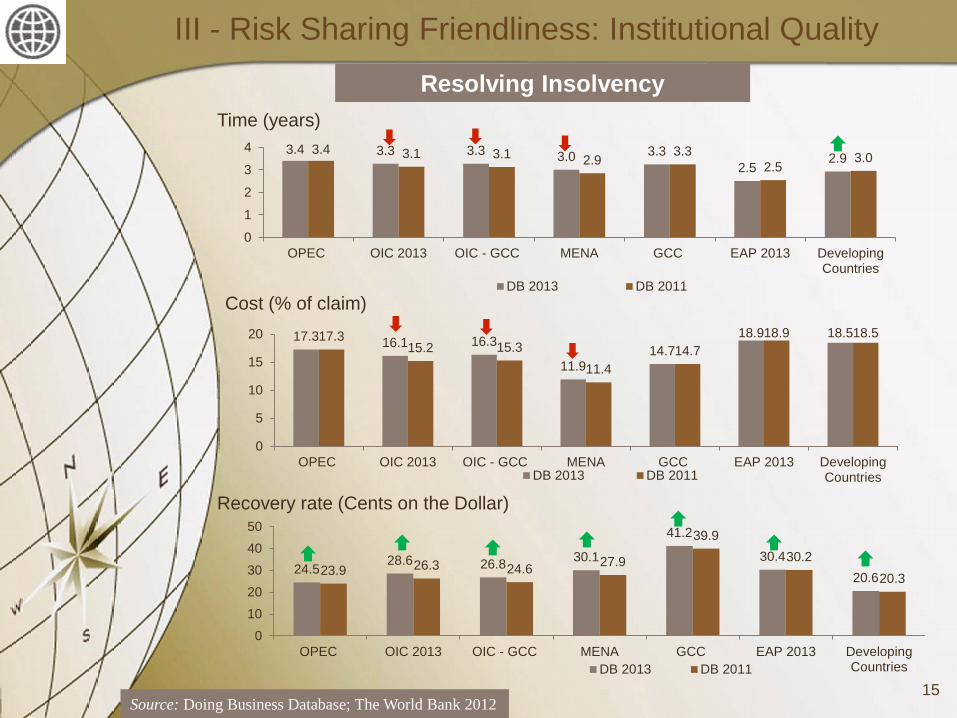

Resolving Insolvency Time (years)

Cost (% of claim)

Recovery rate (Cents on the Dollar)

Source: Doing Business Database; The World Bank 2012 15

III - Risk Sharing Friendliness: Institutional Quality

• Extending outreach of Islamic financial services will foster financial inclusion and ensures liquidity and healthy growth of the industry.

• The entrepreneurial potential in OIC countries can galvanize growth and development through risk sharing inherent in Islamic finance.

• Islamic finance have a large potential to fill a portion of global - around USD 0.5 trillion - SME’s financing gap.

• Risk sharing friendliness is a function of a conducive business environment.

Conclusion and Progress Discussion

16