Renewable Energy Projects: Maximizing

Production and Investment Tax Credits

After Newly Released IRS Guidance Navigating the Construction, Master Contracts and Transfers of Facilities Requirements

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, OCTOBER 30, 2013

Presenting a live 90-minute webinar with interactive Q&A

Gregory F. Jenner, Partner, Stoel Rives, Washington, D.C.

Kevin T. Pearson, Partner, Stoel Rives, Portland, Ore.

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-888-601-3873 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the word balloon button to send

FOR LIVE EVENT ONLY

Renewable Energy Projects October 30, 2013

4

Presented by

Gregory F. Jenner

Kevin T. Pearson

October 30, 2013

Renewable Energy Projects: Maximizing Production and Investment Tax Credits After Newly Released IRS Guidance

Renewable Energy Projects October 30, 2013

5

Overview of Available Incentives

• Production Tax Credit (“PTC”)

• Investment Tax Credit (“ITC”)

• Section 1603 Grant

• Accelerated Depreciation (“MACRS”)

• Bonus Depreciation

Renewable Energy Projects October 30, 2013

6

Production Tax Credit

• Based on amount of electricity

– Produced from qualified resource, and

– Sold to unrelated person

– During each year of credit period

• Credit rate adjusted for inflation each year –

2.3¢ per kilowatt hour for 2013

• Credit Period – 10-year period beginning

with “placed-in-service” date

Renewable Energy Projects October 30, 2013

7

Production Tax Credit

• Qualified resources include:

– Wind

– Geothermal

– Open- and closed-loop biomass

– Hydropower, marine and hydrokinetic

– Others (small irrigation, landfill gas, trash,

refined coal, Indian coal)

• Does not include solar

Renewable Energy Projects October 30, 2013

8

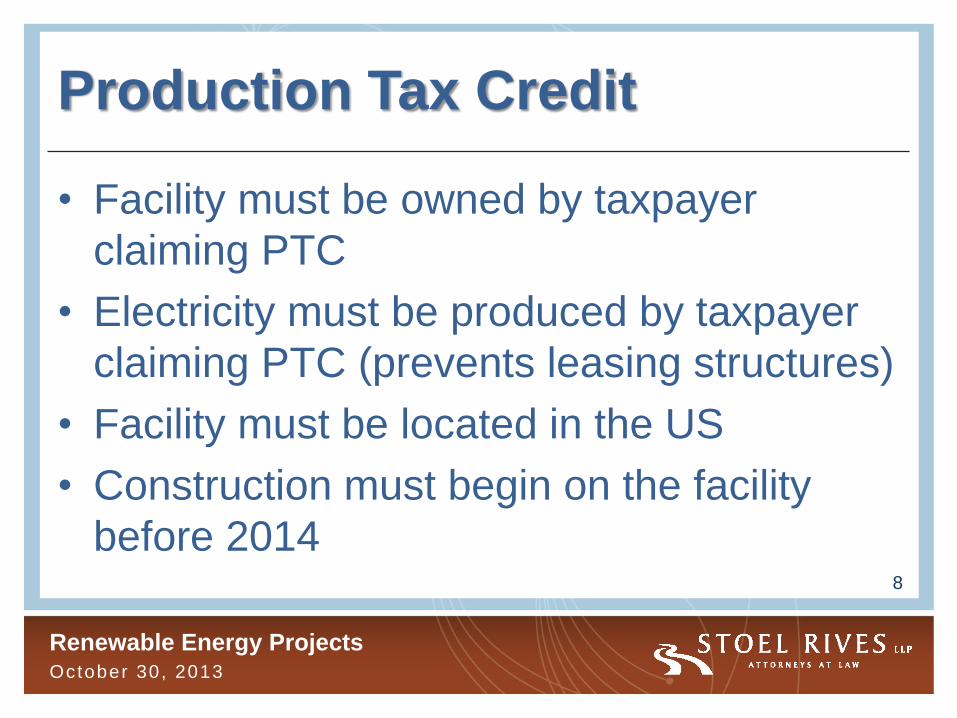

Production Tax Credit

• Facility must be owned by taxpayer

claiming PTC

• Electricity must be produced by taxpayer

claiming PTC (prevents leasing structures)

• Facility must be located in the US

• Construction must begin on the facility

before 2014

Renewable Energy Projects October 30, 2013

9

Investment Tax Credit

• Based on cost of qualifying equipment

– Generally 30% of tax basis (reduced to 10%

after 2016)

– Credit is claimed entirely in the year in which

property is placed in service

• Property generally must be placed in

service by taxpayer claiming ITC

• Property must be “energy property”

Renewable Energy Projects October 30, 2013

10

Investment Tax Credit

• “Energy property” includes

– Solar

– Geothermal

– Fuel cells

– Certain PTC-eligible facilities for which an

election is made to claim ITC rather than PTC

• Property must be eligible for depreciation

• Does not apply to transmission property

Renewable Energy Projects October 30, 2013

11

Investment Tax Credit

• PTC-eligible property must be tangible

personal property or other tangible property

(not building or structural component) used

as integral part of facility

• Basis of property reduced by 50% of ITC

• Recapture if property or interest in property

sold or ceases to be energy property within

5 years of “placed in service” date

Renewable Energy Projects October 30, 2013

12

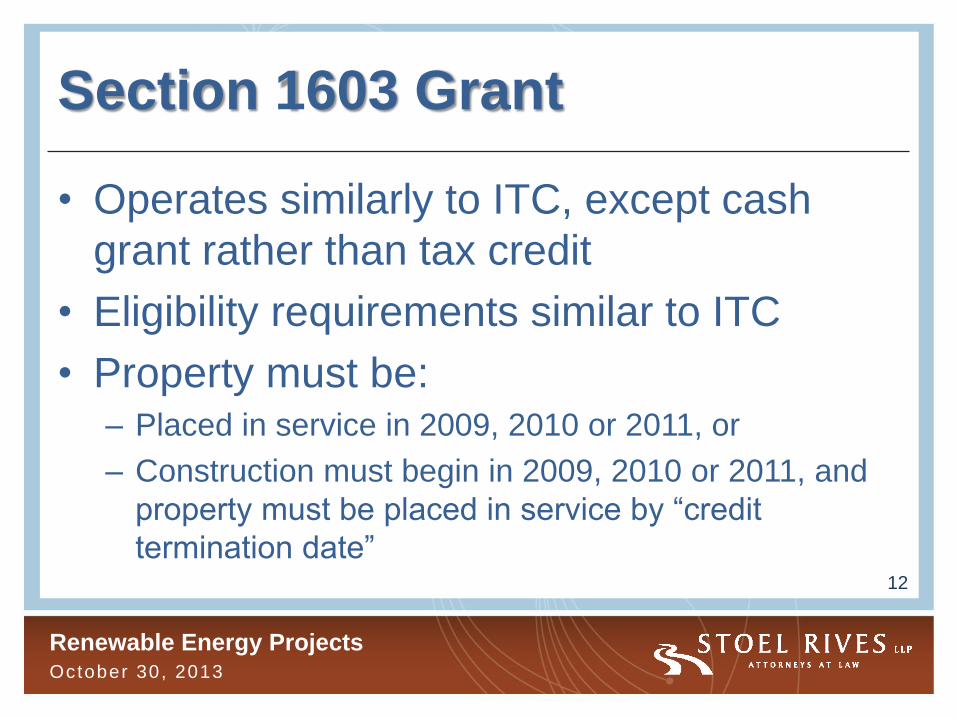

Section 1603 Grant

• Operates similarly to ITC, except cash

grant rather than tax credit

• Eligibility requirements similar to ITC

• Property must be: – Placed in service in 2009, 2010 or 2011, or

– Construction must begin in 2009, 2010 or 2011, and

property must be placed in service by “credit

termination date”

Renewable Energy Projects October 30, 2013

13

Section 1603 Grant

• Application requirements

• Recapture rules similar to ITC

• Treasury Dept. Guidance re “beginning

construction” and other issues

• Forget (mostly) everything you know about

Treasury Dept. Guidance, particularly

regarding valuation

Renewable Energy Projects October 30, 2013

14

“Placed in Service” vs.

“Beginning of Construction” • Prior to 2012 “Fiscal Cliff” bill, eligibility for PTC

and ITC was based on “placed-in-service”

– Large wind projects – before 1/1/13

– Biomass, geothermal (PTC), landfill gas, trash,

hydropower – before 1/1/14

– Solar, geothermal (ITC), fuel cells, microturbines,

combined heat & power, small wind – before 1/1/17

• Fiscal cliff legislation changed requirement

for everything except third category (solar)

Renewable Energy Projects October 30, 2013

15

“Beginning of Construction”

• To qualify for PTC or ITC (by election),

construction must begin before January 1,

2014

• IRS guidance

– Notice 2013-29 – April 15

– Notice 2013-60 – September 20

• Similar, but not identical to, prior Treasury

Dept. guidance for Section 1603 Grant

Renewable Energy Projects October 30, 2013

16

“Beginning of Construction”

• Two methods for beginning construction:

– Physical work of a significant nature

– 5% safe harbor

• These are alternative methods – do not

need to satisfy both

Renewable Energy Projects October 30, 2013

17

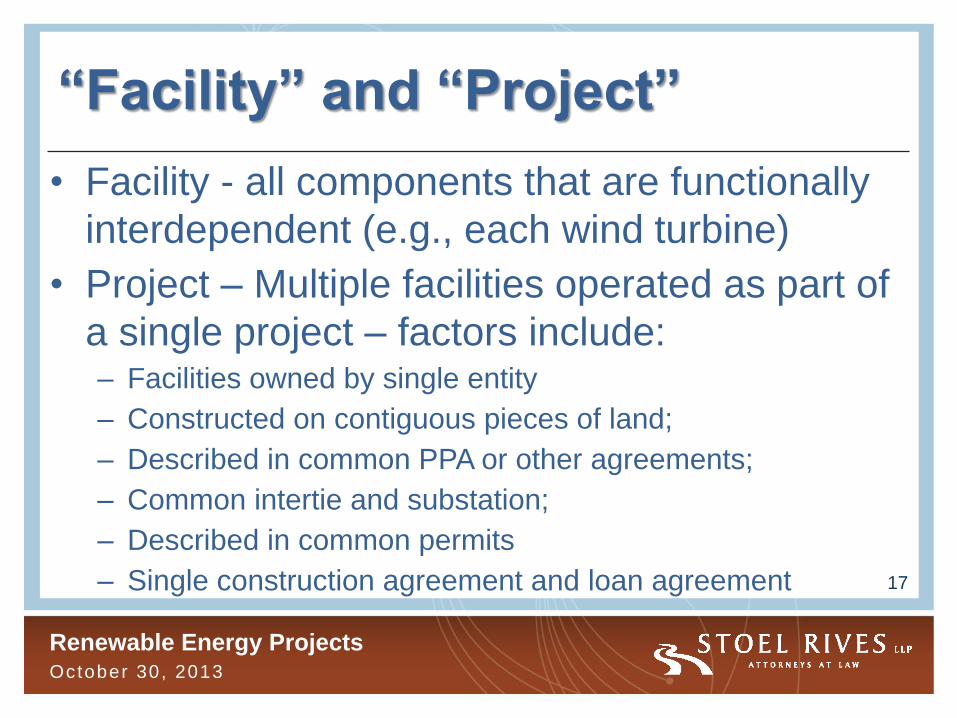

“Facility” and “Project”

• Facility - all components that are functionally

interdependent (e.g., each wind turbine)

• Project – Multiple facilities operated as part of

a single project – factors include: – Facilities owned by single entity

– Constructed on contiguous pieces of land;

– Described in common PPA or other agreements;

– Common intertie and substation;

– Described in common permits

– Single construction agreement and loan agreement

Renewable Energy Projects October 30, 2013

18

Physical Work

• May be on-site or off-site

• Must constitute “physical work of a significant

nature”

– Includes excavating for foundations, setting

anchor bolts, pouring concrete pads,

– Does not include “preliminary activities” such as

planning, designing, financing, exploring,

researching, licensing, surveys, engineering, etc.

• Facts and circumstances test

Renewable Energy Projects October 30, 2013

19

Physical Work (cont.)

• May be performed by taxpayer or by another

person under a binding written contract

• “Binding written contract” means

– Enforceable against taxpayer under state law

– Does not limit damages to less than 5% of contract price

• Contract must exist before work begins

• Does not include work to produce to inventory

• Privity issue – subcontractors?

Renewable Energy Projects October 30, 2013

20

Physical Work (cont.)

• “Master contract” rule – Master contract for components to be manufactured or

produced for taxpayer

– Assignment for components to “affiliated” special

purpose vehicle

• If mfg. produces components for several

facilities, “reasonable method” must be

used to associate components with facilities

Renewable Energy Projects October 30, 2013

21

Physical Work (cont.)

• Once physical work has begun, must maintain

continuous program of construction: – Facts and circumstances test

– Certain disruptions beyond taxpayer’s control permitted • Weather and natural disasters,

• Licensing and permitting delays,

• Labor stoppages or supply shortages

• Inability to obtain specialized equipment of limited availability,

• Endangered species,

• Financing delays of less than 6 months,

• Presumption if placed in service before 2016

Renewable Energy Projects October 30, 2013

22

5% Safe Harbor

• Must “pay or incur” 5% or more of total cost of

facility and make continuous efforts toward

completion thereafter

• “Pay or incur” depends on method of

accounting – “Pay” – cash method

– “Incur” – accrual method

• Total cost of facility includes depreciable basis

of facility (not land or non-integral property)

Renewable Energy Projects October 30, 2013

23

5% Safe Harbor (cont.)

• Special issue for accrual taxpayers – must

have “economic performance” – Generally occurs when property or services provided

– Special 3½ month rule

– Note - use of rule is “method of accounting”

• Property is considered “provided” when

delivered or when title is transferred

• Many taxpayers foregoing safe harbor

Renewable Energy Projects October 30, 2013

24

5% Safe Harbor (cont.)

• Look-through rule

– For property that is manufactured for taxpayer by another

person under binding written contract, costs incurred by

the other person may be taken into account

– Mfg must be able to associate costs with purchased

products – very difficult

• Master contract rule applies to safe harbor

• Cost overruns – may be able to treat individual

facilities separately to preserve 5% safe harbor

Renewable Energy Projects October 30, 2013

25

Safe Harbor (cont.)

• Continuous efforts

– Similar to physical work requirement (continuous

construction)

– Presumption if in service before 2016

– Otherwise, question of fact

• Includes paying additional costs, entering into

contracts, obtaining permits, etc.

• Certain disruptions beyond taxpayer’s

control permitted (see above)

Renewable Energy Projects October 30, 2013

26

Transfers of Facilities

• Taxpayer that begins construction need not

be the same taxpayer who places project in

service

• Any taxpayer that owns facility during PTC

period can claim PTC

• Any taxpayer that owns facility on placed in

service date can claim ITC

• Caution required re transfers

Renewable Energy Projects October 30, 2013

27

Supply Contract Drafting Issues

• Components vs. completed facilities

• Partial performance (Caltex)

• Delivery or title transfer

• 3½ month rule issues

• Preserving argument that mfg.’s physical

work can be taken into account – Not in inventory

– No production before contract executed

Renewable Energy Projects October 30, 2013

28

Supply Contract Drafting Issues

(cont.)

• Who is party to the agreement

– Developer?

– Special purpose entity?

• Identifying purchased components with

specific property

– May not be an issue if placed in service

before 2016

– May be an issue if placed in service later

Renewable Energy Projects October 30, 2013

29

Open Questions

• What if taxpayer does not know identity

and nature of project at time costs

incurred?

• What will tax equity require?

– Physical work and 5%?

– Earmarking components? When?

• Other open issues

Renewable Energy Projects October 30, 2013

30

Renewable Energy Projects October 30, 2013

31

Questions?

Gregory F. Jenner, Partner

(612) 373-8857

Kevin T. Pearson, Partner

(503) 294-9622

The materials are for informational purposes only and not for the purpose of providing legal advice or

soliciting legal business. You should contact your attorney to obtain advice with respect to any

particular issue or problem.