- 1 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Produced by:

Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Pharmaceuticals & Cosmetics

SectorPoland

January 2016

PL_3254_0013_Jan’2016_MP-NY

- 2 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Table of Contents

I. Sector Overview

1. Sector Highlights

2. Economic Importance

3. Healthcare Spending – Historical and Forecast

4. Disease Profile

5. Healthcare Resources

6. Health Perceptions and Spendings

7. Ageing Society

II. Pharmaceuticals

1. Pharmaceutical Sector Highlights

2. Pharmaceutical Market

3. Production and Investments

4. Pharmaceutical Manufacturers

5. Pharmaceutical Segments

6. Prescription vs OTC

7. Exports and Imports

8. Dietary Supplements

9. Pharmacies

10.Medicine and Supplements Use

11.Forecast

III.Cosmetics

1. Cosmetic Sector Highlights

2. Cosmetics Market Production

3. Cosmetics Market Indicators

4. Main Cosmetics Segments

5. Main Cosmetics Segments Market Shares

6. Sales

7. Exports & Imports

8. Forecast

IV.Main Players

1. M&A Activity

2. Top Ten Sector Companies

3. Pelion Healthcare Group

4. Pelion Healthcare Group (cont’d)

5. Neuca

6. Neuca (cont’d)

7. Farmacol

8. Farmacol (cont’d)

9. Glaxosmithkline

10.Rossmann

- 3 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

I. Sector Overview

- 4 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

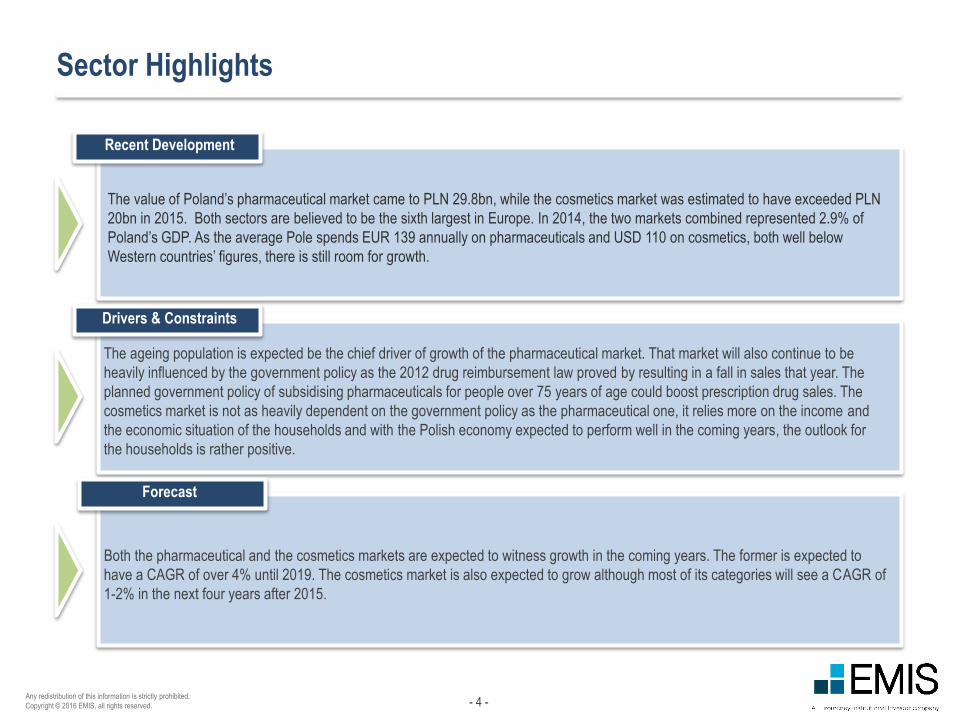

Sector Highlights

Both the pharmaceutical and the cosmetics markets are expected to witness growth in the coming years. The former is expected to

have a CAGR of over 4% until 2019. The cosmetics market is also expected to grow although most of its categories will see a CAGR of

1-2% in the next four years after 2015.

The ageing population is expected be the chief driver of growth of the pharmaceutical market. That market will also continue to be

heavily influenced by the government policy as the 2012 drug reimbursement law proved by resulting in a fall in sales that year. The

planned government policy of subsidising pharmaceuticals for people over 75 years of age could boost prescription drug sales. The

cosmetics market is not as heavily dependent on the government policy as the pharmaceutical one, it relies more on the income and

the economic situation of the households and with the Polish economy expected to perform well in the coming years, the outlook for

the households is rather positive.

The value of Poland’s pharmaceutical market came to PLN 29.8bn, while the cosmetics market was estimated to have exceeded PLN

20bn in 2015. Both sectors are believed to be the sixth largest in Europe. In 2014, the two markets combined represented 2.9% of

Poland’s GDP. As the average Pole spends EUR 139 annually on pharmaceuticals and USD 110 on cosmetics, both well below

Western countries’ figures, there is still room for growth.

Recent Development

Drivers & Constraints

Forecast

- 5 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

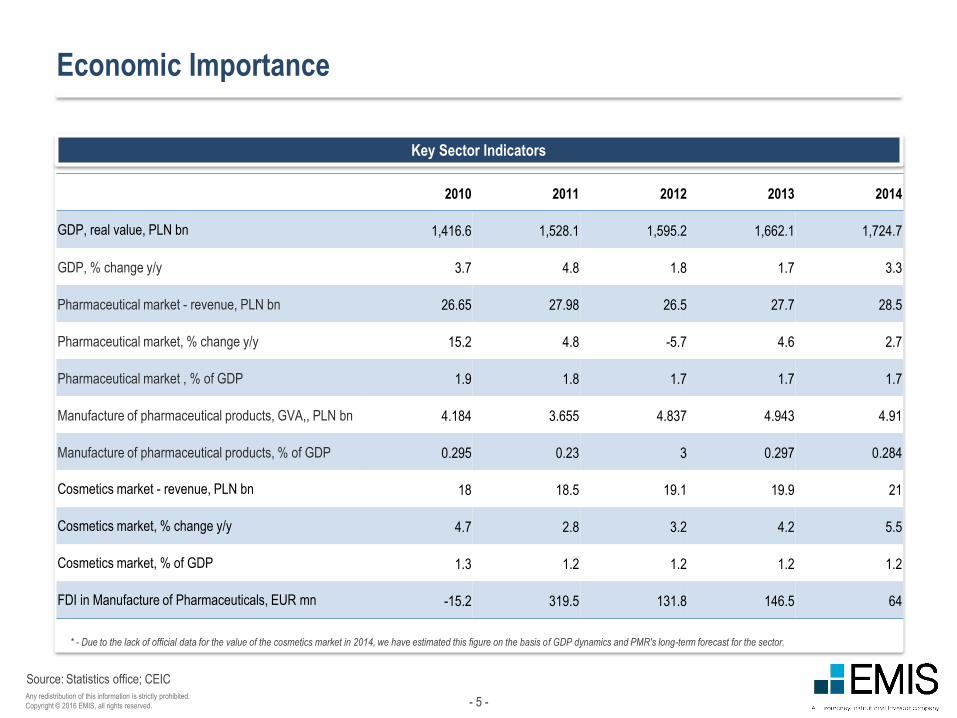

Economic Importance

Key Sector Indicators

Statistics office; CEIC

* - Due to the lack of official data for the value of the cosmetics market in 2014, we have estimated this figure on the basis of GDP dynamics and PMR's long-term forecast for the sector.

2010 2011 2012 2013 2014

GDP, real value, PLN bn 1,416.6 1,528.1 1,595.2 1,662.1 1,724.7

GDP, % change y/y 3.7 4.8 1.8 1.7 3.3

Pharmaceutical market - revenue, PLN bn 26.65 27.98 26.5 27.7 28.5

Pharmaceutical market, % change y/y 15.2 4.8 -5.7 4.6 2.7

Pharmaceutical market , % of GDP 1.9 1.8 1.7 1.7 1.7

Manufacture of pharmaceutical products, GVA,, PLN bn 4.184 3.655 4.837 4.943 4.91

Manufacture of pharmaceutical products, % of GDP 0.295 0.23 3 0.297 0.284

Cosmetics market - revenue, PLN bn 18 18.5 19.1 19.9 21

Cosmetics market, % change y/y 4.7 2.8 3.2 4.2 5.5

Cosmetics market, % of GDP 1.3 1.2 1.2 1.2 1.2

FDI in Manufacture of Pharmaceuticals, EUR mn -15.2 319.5 131.8 146.5 64

- 6 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

Healthcare Spending – Historical and Forecast

According to the latest OECD calculations, Poland’s total expenditure on health in 2013 came to 6.4% of its GDP, the third lowest among the

countries surveyed (only Mexico and Turkey had lower figures). By comparison, regional peers Czech Republic and Hungary spent 7.1% and

7.4% respectively of their GDP on healthcare. In Germany and France the figure was around 11%. Also, Poland lags behind other countries in

terms of government expenditure on healthcare, which represented 4.5% of the GDP in 2013, according to the latest available data.

Health spending (PLN bn) Health spending forecast (PLN bn)

BMI Research

80.134 84.423 89.627 95.319 101.510

35.67837.652

39.93042.483

45.353

115.811 122.074 129.556 137.803 146.854

0

20

40

60

80

100

120

140

160

2015e 2016f 2017f 2018f 2019f

Private

Government

Total

73.8 74.6 75.8 77.5

30.7 32.7 33.2 34.0

104.5 107.3 109.0 111.5

0

20

40

60

80

100

120

2011 2012 2013 2014

Private

Government

Total

- 7 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

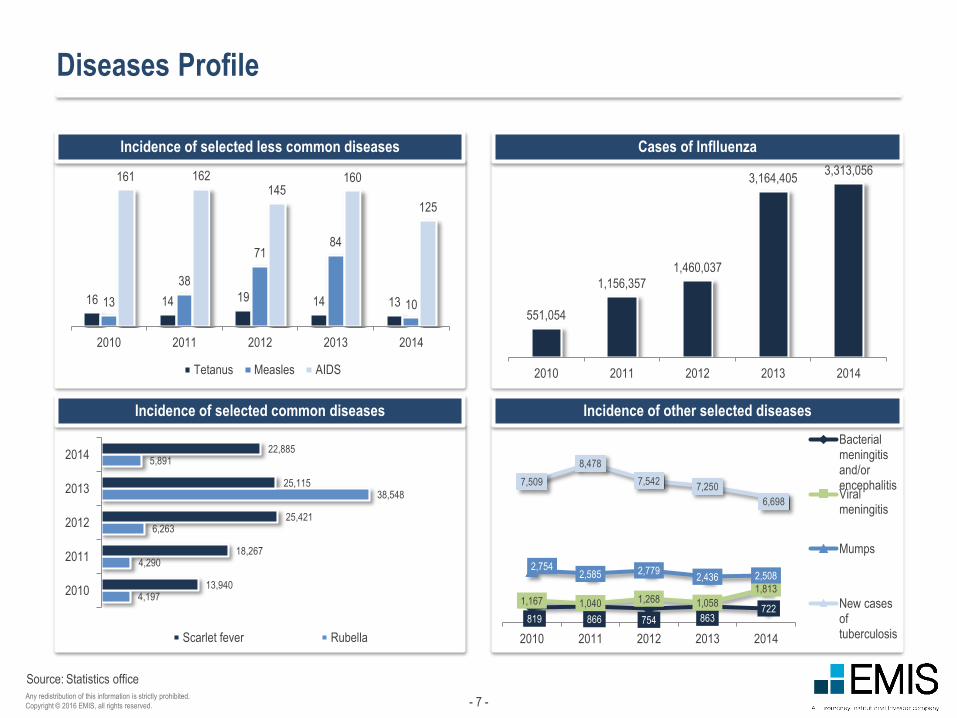

Diseases Profile

Incidence of selected less common diseases

Incidence of selected common diseases

Cases of Inflluenza

Incidence of other selected diseases

Statistics office

16 14 19 14 1313

38

7184

10

161 162145

160

125

2010 2011 2012 2013 2014

Tetanus Measles AIDS

4,197

4,290

6,263

38,548

5,891

13,940

18,267

25,421

25,115

22,885

2010

2011

2012

2013

2014

Scarlet fever Rubella

551,054

1,156,357

1,460,037

3,164,4053,313,056

2010 2011 2012 2013 2014

819 866 754 863722

1,167 1,040 1,268 1,058

1,813

2,7542,585 2,779

2,436 2,508

7,509

8,478

7,5427,250

6,698

2010 2011 2012 2013 2014

Bacterialmeningitisand/orencephalitisViralmeningitis

Mumps

New casesoftuberculosis

- 8 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

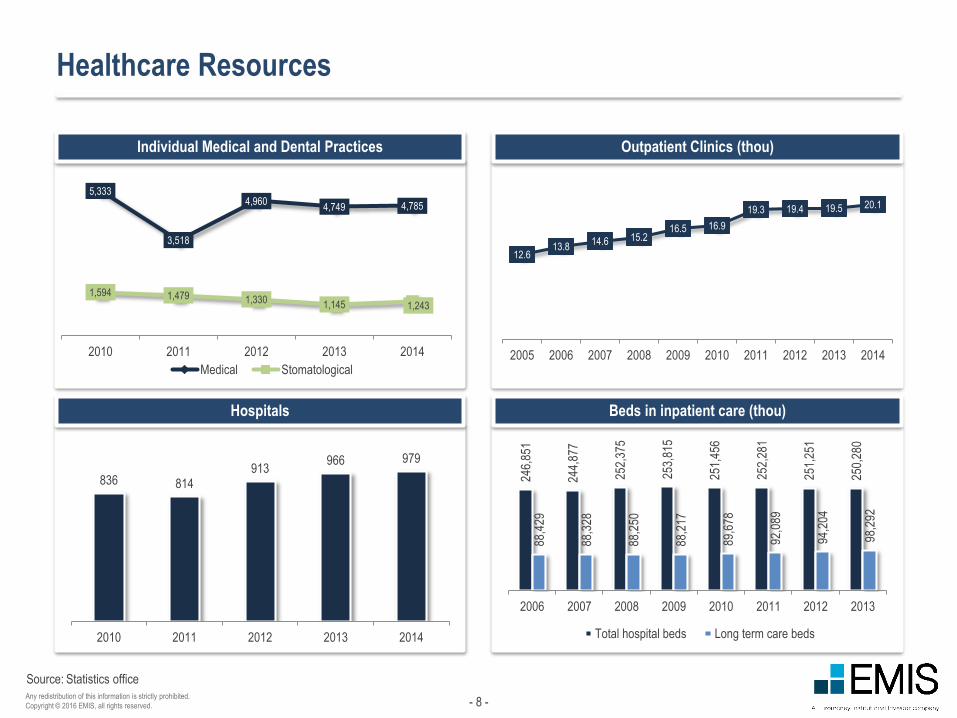

Healthcare Resources

Individual Medical and Dental Practices

Hospitals

Outpatient Clinics (thou)

Beds in inpatient care (thou)

Statistics office

12.613.8

14.6 15.216.5 16.9

19.3 19.4 19.5 20.1

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

246,

851

244,

877

252,

375

253,

815

251,

456

252,

281

251,

251

250,

280

88,4

29

88,3

28

88,2

50

88,2

17

89,6

78

92,0

89

94,2

04

98,2

92

2006 2007 2008 2009 2010 2011 2012 2013

Total hospital beds Long term care beds

836 814913

966 979

2010 2011 2012 2013 2014

5,333

3,518

4,9604,749 4,785

1,594 1,479 1,330 1,145 1,243

2010 2011 2012 2013 2014

Medical Stomatological

- 9 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

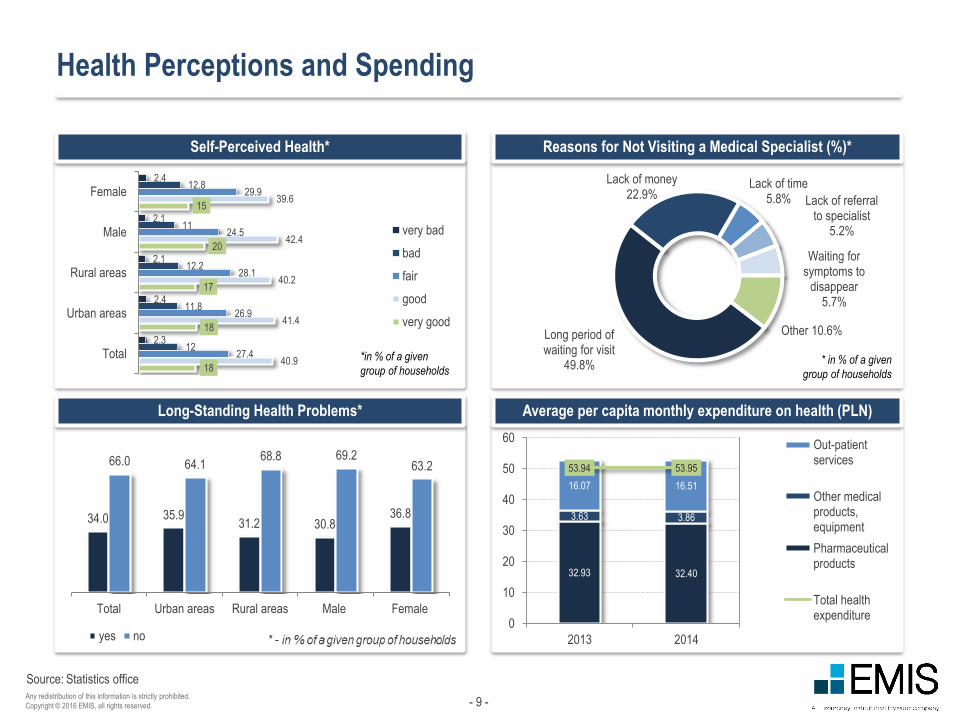

Health Perceptions and Spending

Self-Perceived Health*

Long-Standing Health Problems*

Reasons for Not Visiting a Medical Specialist (%)*

Average per capita monthly expenditure on health (PLN)

Statistics office

18

18

17

20

15

40.9

41.4

40.2

42.4

39.6

27.4

26.9

28.1

24.5

29.9

12

11.8

12.2

11

12.8

2.3

2.4

2.1

2.1

2.4

Total

Urban areas

Rural areas

Male

Female

very bad

bad

fair

good

very good

*in % of a given

group of households

34.0 35.931.2 30.8

36.8

66.0 64.168.8 69.2

63.2

Total Urban areas Rural areas Male Female

yes no

Long period of waiting for visit

49.8%

Lack of money22.9%

Lack of time5.8% Lack of referral

to specialist5.2%

Waiting for symptoms to

disappear5.7%

Other 10.6%

* in % of a given

group of households

32.93 32.40

3.63 3.86

16.07 16.51

53.94 53.95

0

10

20

30

40

50

60

2013 2014

Out-patientservices

Other medicalproducts,equipment

Pharmaceuticalproducts

Total healthexpenditure

- 10 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

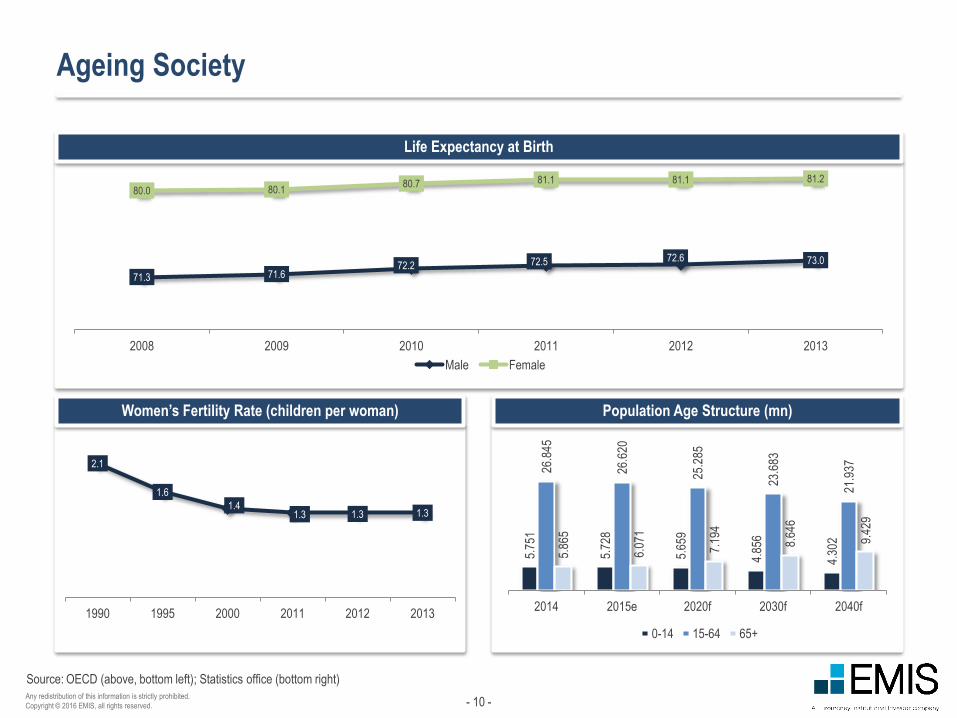

Ageing Society

Women’s Fertility Rate (children per woman)

Life Expectancy at Birth

Population Age Structure (mn)

OECD (above, bottom left); Statistics office (bottom right)

2.1

1.6

1.41.3 1.3 1.3

1990 1995 2000 2011 2012 2013

5.75

1

5.72

8

5.65

9

4.85

6

4.30

2

26.8

45

26.6

20

25.2

85

23.6

83

21.9

37

5.86

5

6.07

1

7.19

4

8.64

6

9.42

9

2014 2015e 2020f 2030f 2040f

0-14 15-64 65+

71.3 71.672.2 72.5 72.6 73.0

80.0 80.180.7 81.1 81.1 81.2

2008 2009 2010 2011 2012 2013

Male Female

- 11 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

II. Pharmaceuticals

- 12 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Pharmaceutical Highlights

Recent

Development

The value of the pharmaceutical market came to PLN 29.9mn at the end of 2015, up 4.8% y/y, according to Pharma Expert. The IMS Health latest available estimates, which are for 2013, show that the Polish market was the sixth largest one in Europe. The EUR 139 per capita annual expenditure on drugs in Poland remains one of the lowest in Europe, according to a 2015 report by DNB Bank and Deloitte. The state reimbursement for drugs in Poland is also one of the lowest in Europe. Generic drugs hold a dominant position on the market representingaround 70% of all sales as of the end of 2015, a figure that is based on various estimates. Pharmaceutical wholesalers, driven by falling margins in their business, started entering higher margin segments of the market. Prime examples of this trend are Pelion’s acquisition of the Natura drugstore chain or Neuca’s acquisitions of outpatient clinics.

Drivers &

Constraints

The increasing life expectancy in Poland (at 77 years in 2013) combined with a birth rate well below the replacement level are expected to lead to the ageing of the Polish population. The only age group that will be growing in the next decades will be the 65 plus age group. This process will be the main driver for the pharmaceutical market as it is the older age groups that use medicines most frequently. Growing wealth and health consciousness are also expected to contribute to a rise in sales. Also the planned government policy of providing free of charge pharmaceuticals for citizens over 75 years of age could increase prescription drug sales, just as the drug reimbursement policy of 2012 led to a slump in pharmaceutical and especially prescription drug sales. However, as of the beginning of 2016, forecasts by DNB Bank and Deloitte expect the pharmaceutical market growth rate to slow down manly due to a halt in pension growth, which directly affects prescription drug sales.

Government

Policy

In 2015, two amendments to the 2012 Pharmaceutical Law were introduced. One is the so-called counterfeit goods amendment, obliging wholesale units to apply a quality system determining obligations, processes and risk management regarding their operations, and the other aims at preventing the reverse distribution chain.

Also the new Polish government, created in November 2015 by the Law and Justice party, plans to put into force its election promise of providing free of charge pharmaceuticals for people over 75 years of age. The list of the free medicines will be updated every two months. The pharmaceuticals will be funded directly from the state budget and not from the National Health Fund. In 2016, PLN 495mn will be earmarked for funding the medicines for the elderly. By 2025, this figure should reach PLN 1.2bn.

Forecast

In 2016, pharmaceutical sales are expected to increase by 1.1% y/y compared to a growth of over 4% in 2014, due to an expected stagnation in prescription drug sales caused by slower pension growth. BMI Research expects the total pharmaceutical sales to grow by a CAGR of 4.6% until 2019. OTC drug sales are forecast to grow by a CAGR of 4.6 % in that period, prescription drugs by 4.8% . Also generic drugs will continue to dominate the landscape, growing by a CAGR of 4.4% until 2019. Patented drugs are expected to grow at a faster rate in 2015-2019, but their share in total pharmaceutical sales will not exceed 32% from the current around 30%.

- 13 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

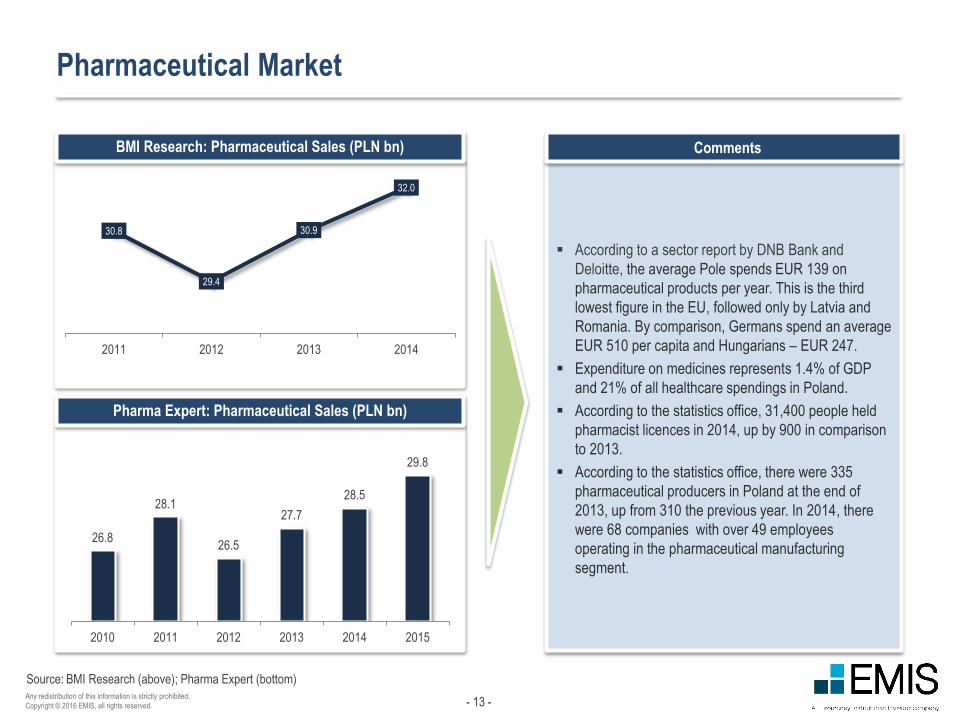

Pharmaceutical Market

BMI Research: Pharmaceutical Sales (PLN bn)

Pharma Expert: Pharmaceutical Sales (PLN bn)

According to a sector report by DNB Bank and

Deloitte, the average Pole spends EUR 139 on

pharmaceutical products per year. This is the third

lowest figure in the EU, followed only by Latvia and

Romania. By comparison, Germans spend an average

EUR 510 per capita and Hungarians – EUR 247.

Expenditure on medicines represents 1.4% of GDP

and 21% of all healthcare spendings in Poland.

According to the statistics office, 31,400 people held

pharmacist licences in 2014, up by 900 in comparison

to 2013.

According to the statistics office, there were 335

pharmaceutical producers in Poland at the end of

2013, up from 310 the previous year. In 2014, there

were 68 companies with over 49 employees

operating in the pharmaceutical manufacturing

segment.

BMI Research (above); Pharma Expert (bottom)

30.8

29.4

30.9

32.0

2011 2012 2013 2014

26.8

28.1

26.5

27.7

28.5

29.8

2010 2011 2012 2013 2014 2015

- 14 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

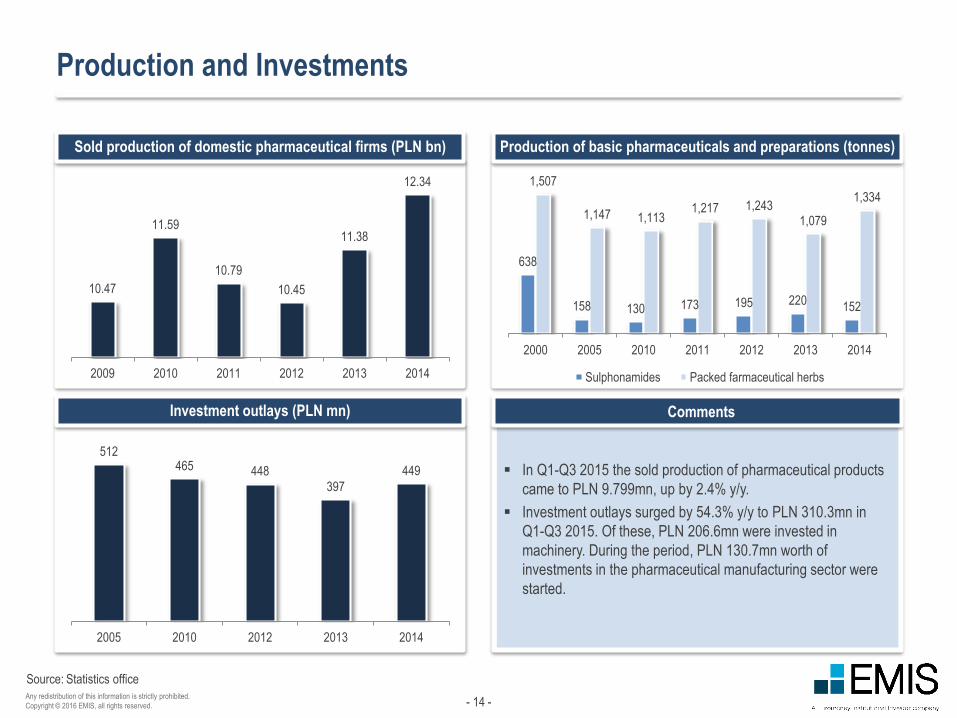

Production and Investments

Sold production of domestic pharmaceutical firms (PLN bn)

Investment outlays (PLN mn)

Production of basic pharmaceuticals and preparations (tonnes)

Statistics office

In Q1-Q3 2015 the sold production of pharmaceutical products

came to PLN 9.799mn, up by 2.4% y/y.

Investment outlays surged by 54.3% y/y to PLN 310.3mn in

Q1-Q3 2015. Of these, PLN 206.6mn were invested in

machinery. During the period, PLN 130.7mn worth of

investments in the pharmaceutical manufacturing sector were

started.

10.47

11.59

10.79

10.45

11.38

12.34

2009 2010 2011 2012 2013 2014

638

158 130 173 195 220152

1,507

1,147 1,1131,217 1,243

1,079

1,334

2000 2005 2010 2011 2012 2013 2014

Sulphonamides Packed farmaceutical herbs

512465 448

397

449

2005 2010 2012 2013 2014

- 15 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

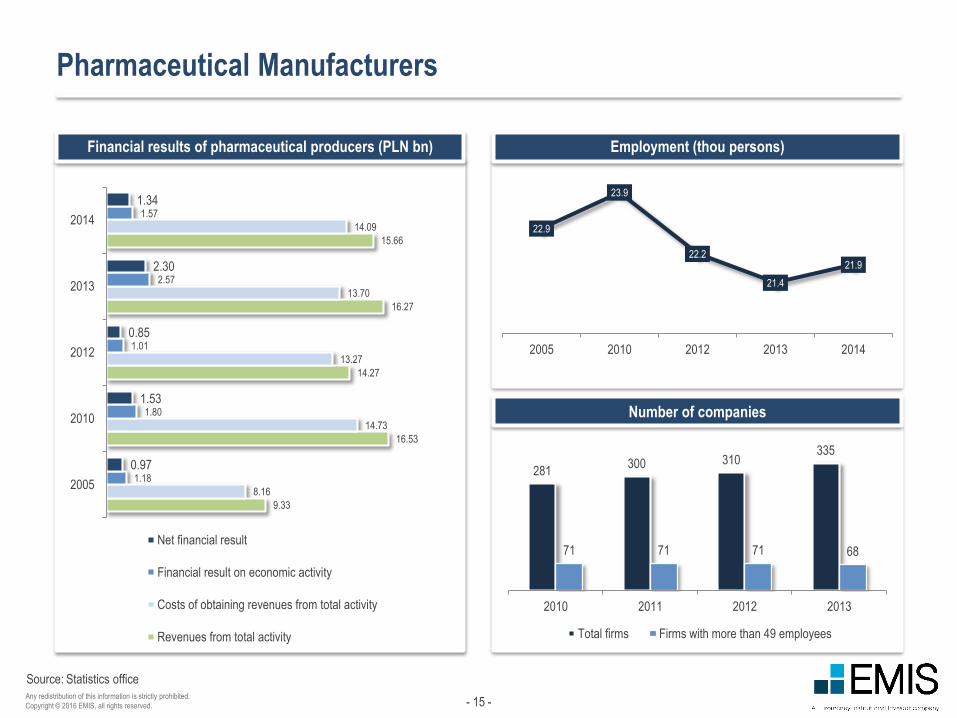

Pharmaceutical Manufacturers

Employment (thou persons)

Number of companies

Financial results of pharmaceutical producers (PLN bn)

Statistics office

9.33

16.53

14.27

16.27

15.66

8.16

14.73

13.27

13.70

14.09

1.18

1.80

1.01

2.57

1.57

0.97

1.53

0.85

2.30

1.34

2005

2010

2012

2013

2014

Net financial result

Financial result on economic activity

Costs of obtaining revenues from total activity

Revenues from total activity

22.9

23.9

22.2

21.4

21.9

2005 2010 2012 2013 2014

281300 310

335

71 71 71 68

2010 2011 2012 2013

Total firms Firms with more than 49 employees

- 16 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

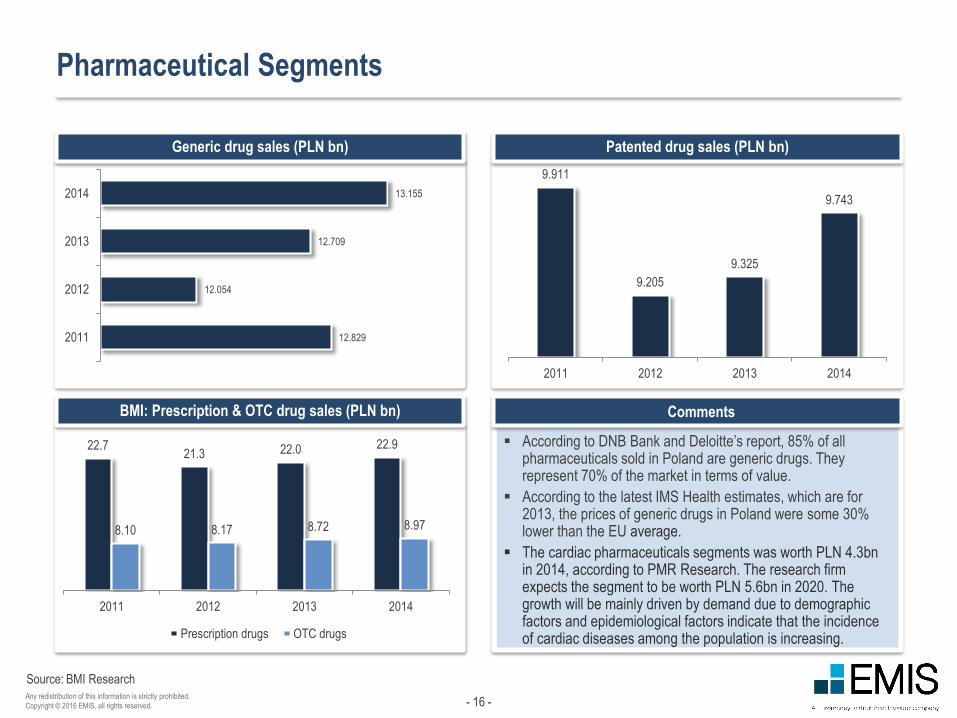

Pharmaceutical Segments

Generic drug sales (PLN bn)

BMI: Prescription & OTC drug sales (PLN bn)

Patented drug sales (PLN bn)

BMI Research

According to DNB Bank and Deloitte’s report, 85% of all pharmaceuticals sold in Poland are generic drugs. They represent 70% of the market in terms of value.

According to the latest IMS Health estimates, which are for 2013, the prices of generic drugs in Poland were some 30% lower than the EU average.

The cardiac pharmaceuticals segments was worth PLN 4.3bn in 2014, according to PMR Research. The research firm expects the segment to be worth PLN 5.6bn in 2020. The growth will be mainly driven by demand due to demographic factors and epidemiological factors indicate that the incidence of cardiac diseases among the population is increasing.

12.829

12.054

12.709

13.155

2011

2012

2013

2014

9.911

9.205

9.325

9.743

2011 2012 2013 2014

22.721.3 22.0 22.9

8.10 8.17 8.72 8.97

2011 2012 2013 2014

Prescription drugs OTC drugs

- 17 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

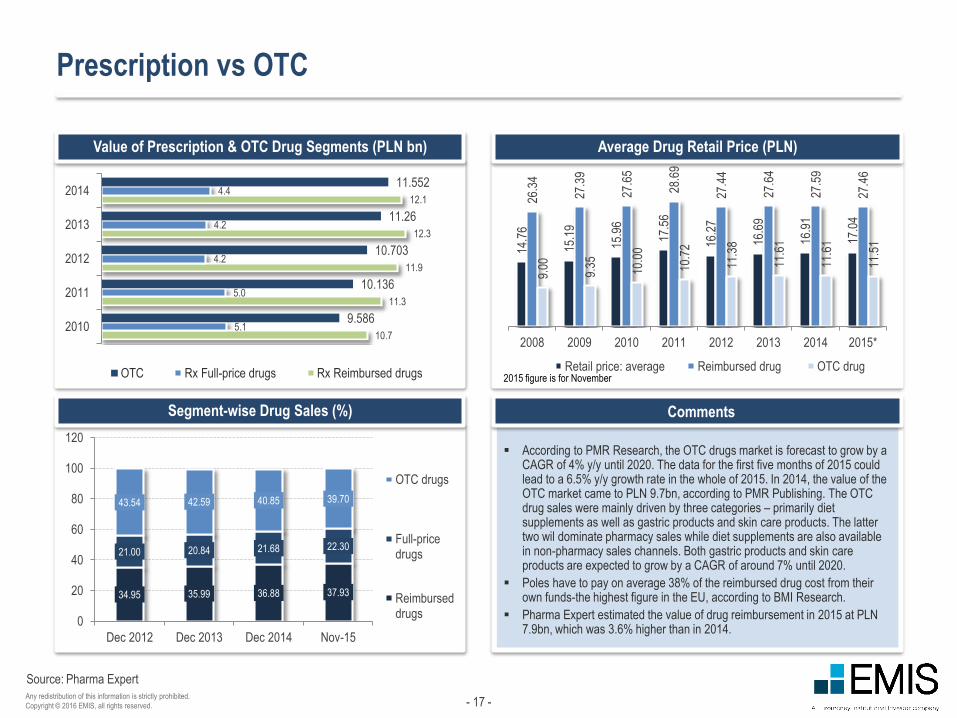

Prescription vs OTC

Value of Prescription & OTC Drug Segments (PLN bn)

Segment-wise Drug Sales (%)

Average Drug Retail Price (PLN)

Pharma Expert

According to PMR Research, the OTC drugs market is forecast to grow by a CAGR of 4% y/y until 2020. The data for the first five months of 2015 could lead to a 6.5% y/y growth rate in the whole of 2015. In 2014, the value of the OTC market came to PLN 9.7bn, according to PMR Publishing. The OTC drug sales were mainly driven by three categories – primarily diet supplements as well as gastric products and skin care products. The latter two wil dominate pharmacy sales while diet supplements are also available in non-pharmacy sales channels. Both gastric products and skin care products are expected to grow by a CAGR of around 7% until 2020.

Poles have to pay on average 38% of the reimbursed drug cost from their own funds-the highest figure in the EU, according to BMI Research.

Pharma Expert estimated the value of drug reimbursement in 2015 at PLN 7.9bn, which was 3.6% higher than in 2014.

10.7

11.3

11.9

12.3

12.1

5.1

5.0

4.2

4.2

4.4

9.586

10.136

10.703

11.26

11.552

2010

2011

2012

2013

2014

OTC Rx Full-price drugs Rx Reimbursed drugs

34.95 35.99 36.88 37.93

21.00 20.84 21.68 22.30

43.54 42.59 40.85 39.70

0

20

40

60

80

100

120

Dec 2012 Dec 2013 Dec 2014 Nov-15

OTC drugs

Full-pricedrugs

Reimburseddrugs

14.7

6

15.1

9

15.9

6

17.5

6

16.2

7

16.6

9

16.9

1

17.0

4

26.3

4

27.3

9

27.6

5

28.6

9

27.4

4

27.6

4

27.5

9

27.4

6

9.00

9.35

10.0

0

10.7

2

11.3

8

11.6

1

11.6

1

11.5

1

2008 2009 2010 2011 2012 2013 2014 2015*

Retail price: average Reimbursed drug OTC drug2015 figure is for November

- 18 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

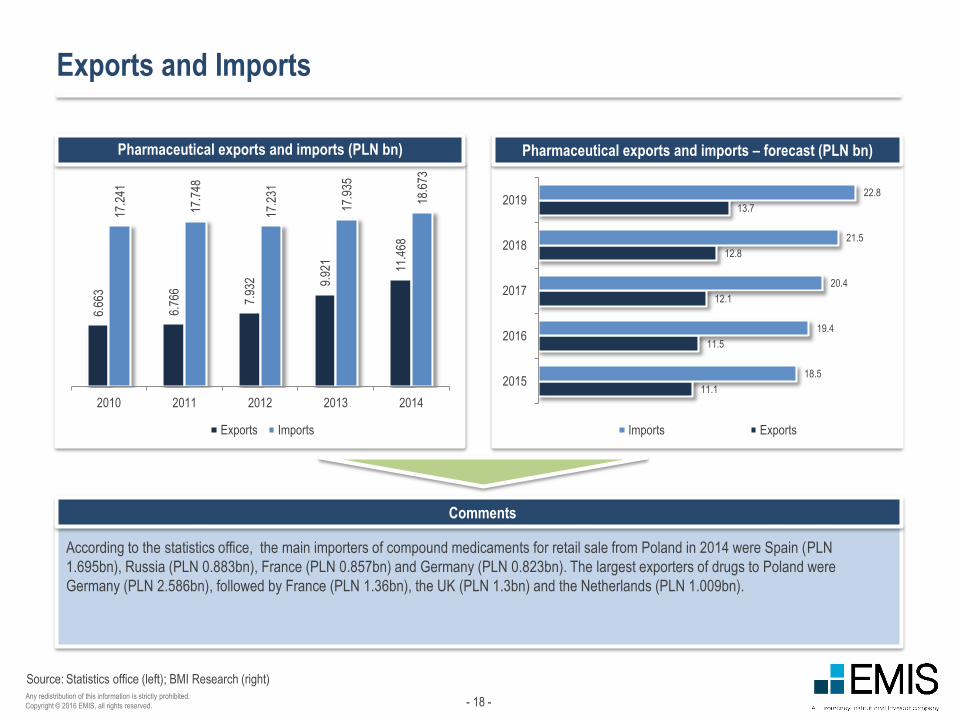

Exports and Imports

According to the statistics office, the main importers of compound medicaments for retail sale from Poland in 2014 were Spain (PLN

1.695bn), Russia (PLN 0.883bn), France (PLN 0.857bn) and Germany (PLN 0.823bn). The largest exporters of drugs to Poland were

Germany (PLN 2.586bn), followed by France (PLN 1.36bn), the UK (PLN 1.3bn) and the Netherlands (PLN 1.009bn).

Pharmaceutical exports and imports (PLN bn) Pharmaceutical exports and imports – forecast (PLN bn)

Statistics office (left); BMI Research (right)

6.66

3

6.76

6

7.93

2 9.92

1

11.4

68

17.2

41

17.7

48

17.2

31

17.9

35

18.6

73

2010 2011 2012 2013 2014

Exports Imports

11.1

11.5

12.1

12.8

13.7

18.5

19.4

20.4

21.5

22.8

2015

2016

2017

2018

2019

Imports Exports

- 19 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

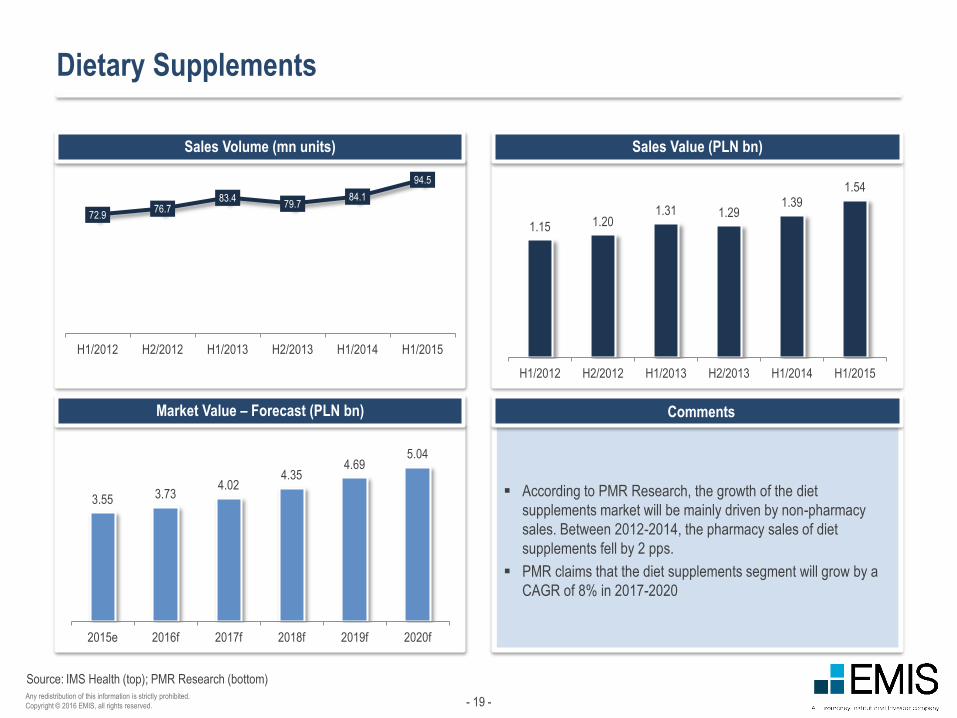

Dietary Supplements

Sales Volume (mn units)

Market Value – Forecast (PLN bn)

Sales Value (PLN bn)

IMS Health (top); PMR Research (bottom)

According to PMR Research, the growth of the diet

supplements market will be mainly driven by non-pharmacy

sales. Between 2012-2014, the pharmacy sales of diet

supplements fell by 2 pps.

PMR claims that the diet supplements segment will grow by a

CAGR of 8% in 2017-2020

72.976.7

83.479.7

84.1

94.5

H1/2012 H2/2012 H1/2013 H2/2013 H1/2014 H1/2015

1.15 1.201.31 1.29

1.391.54

H1/2012 H2/2012 H1/2013 H2/2013 H1/2014 H1/2015

3.55 3.734.02

4.354.69

5.04

2015e 2016f 2017f 2018f 2019f 2020f

- 20 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

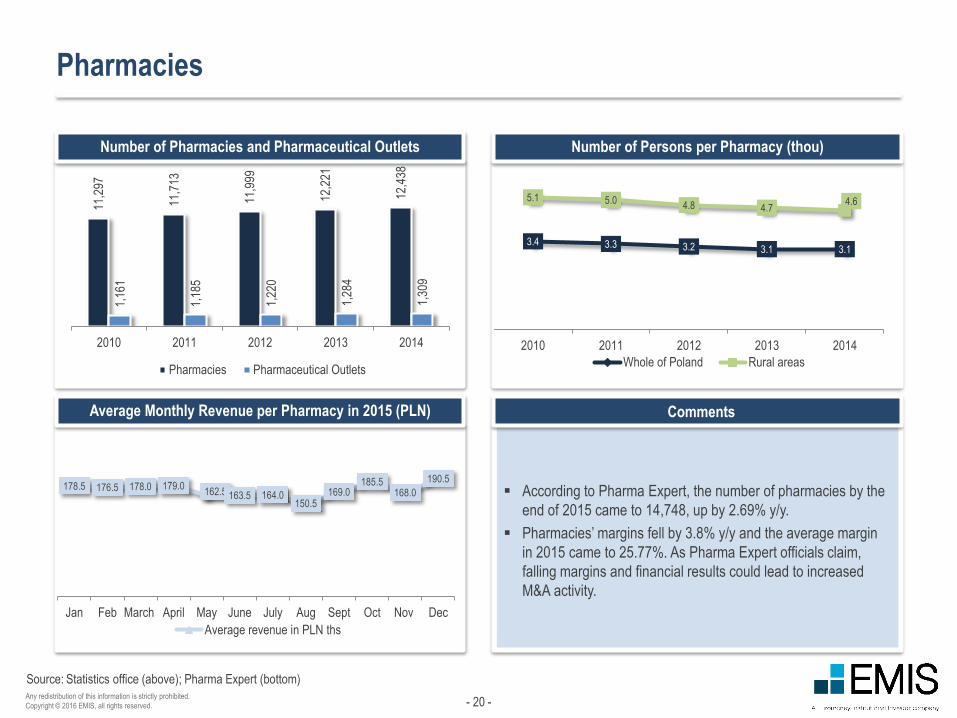

Pharmacies

Number of Pharmacies and Pharmaceutical Outlets

Average Monthly Revenue per Pharmacy in 2015 (PLN)

Number of Persons per Pharmacy (thou)

Statistics office (above); Pharma Expert (bottom)

According to Pharma Expert, the number of pharmacies by the

end of 2015 came to 14,748, up by 2.69% y/y.

Pharmacies’ margins fell by 3.8% y/y and the average margin

in 2015 came to 25.77%. As Pharma Expert officials claim,

falling margins and financial results could lead to increased

M&A activity.

11,2

97

11,7

13

11,9

99

12,2

21

12,4

38

1,16

1

1,18

5

1,22

0

1,28

4

1,30

9

2010 2011 2012 2013 2014

Pharmacies Pharmaceutical Outlets

3.4 3.3 3.2 3.1 3.1

5.1 5.04.8 4.7

4.6

2010 2011 2012 2013 2014

Whole of Poland Rural areas

178.5 176.5 178.0 179.0162.5 163.5 164.0

150.5169.0

185.5168.0

190.5

Jan Feb March April May June July Aug Sept Oct Nov Dec

Average revenue in PLN ths

- 21 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

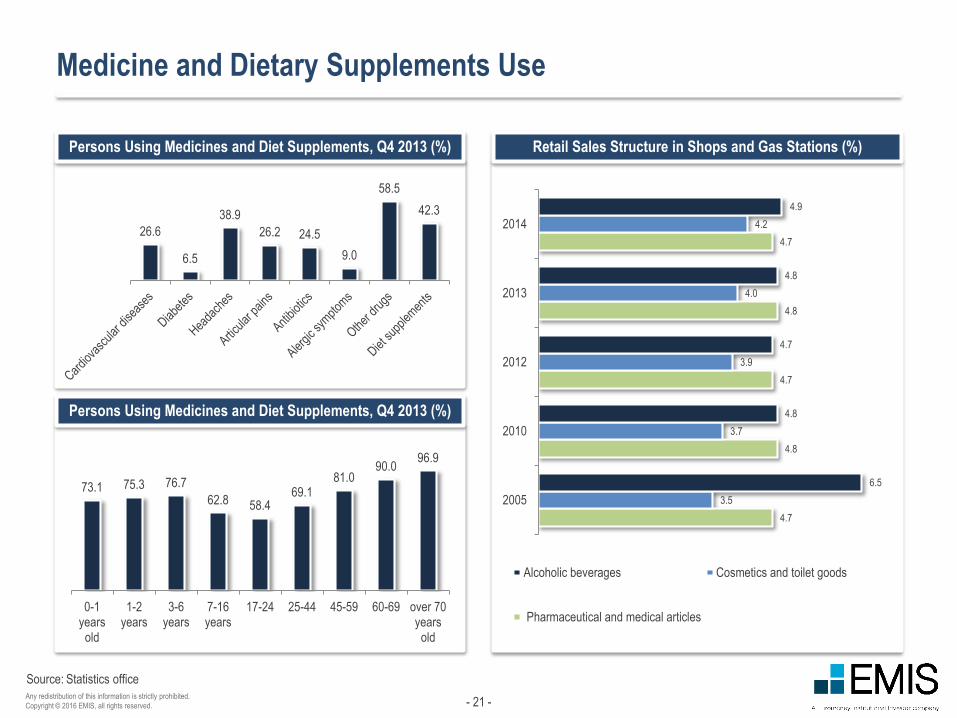

Medicine and Dietary Supplements Use

Persons Using Medicines and Diet Supplements, Q4 2013 (%)

Persons Using Medicines and Diet Supplements, Q4 2013 (%)

Retail Sales Structure in Shops and Gas Stations (%)

Statistics office

4.7

4.8

4.7

4.8

4.7

3.5

3.7

3.9

4.0

4.2

6.5

4.8

4.7

4.8

4.9

2005

2010

2012

2013

2014

Alcoholic beverages Cosmetics and toilet goods

Pharmaceutical and medical articles

26.6

6.5

38.9

26.2 24.5

9.0

58.5

42.3

73.1 75.3 76.7

62.8 58.469.1

81.090.0

96.9

0-1years

old

1-2years

3-6years

7-16years

17-24 25-44 45-59 60-69 over 70years

old

- 22 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

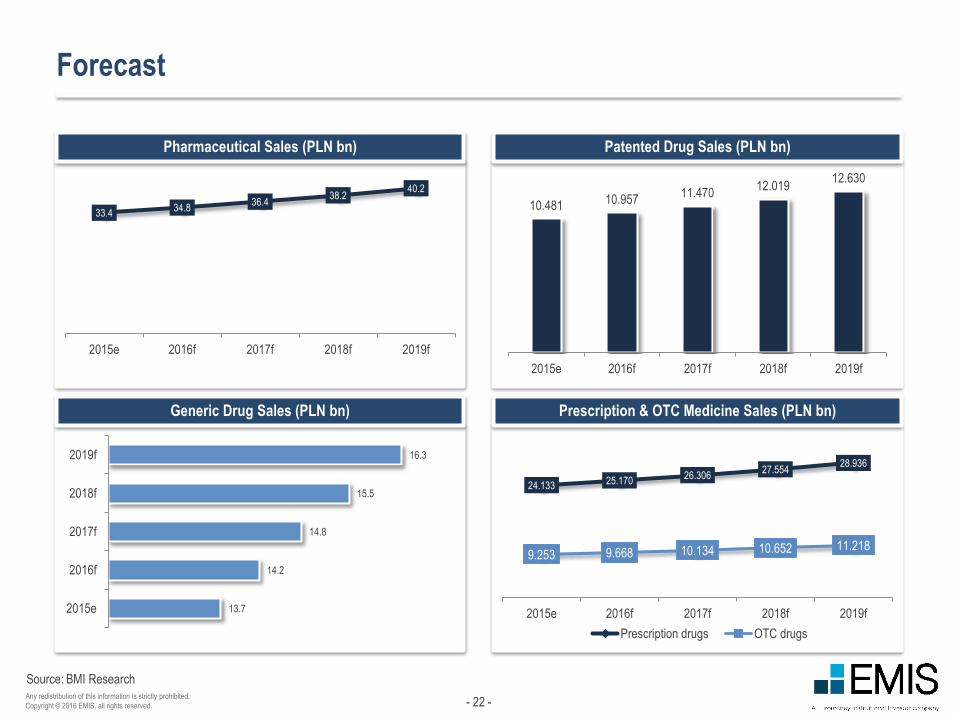

Forecast

Pharmaceutical Sales (PLN bn)

Generic Drug Sales (PLN bn)

Patented Drug Sales (PLN bn)

Prescription & OTC Medicine Sales (PLN bn)

BMI Research

33.434.8

36.438.2

40.2

2015e 2016f 2017f 2018f 2019f

13.7

14.2

14.8

15.5

16.3

2015e

2016f

2017f

2018f

2019f

24.133 25.17026.306

27.55428.936

9.253 9.668 10.134 10.652 11.218

2015e 2016f 2017f 2018f 2019f

Prescription drugs OTC drugs

10.481 10.95711.470

12.01912.630

2015e 2016f 2017f 2018f 2019f

- 23 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

III. Cosmetics

- 24 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

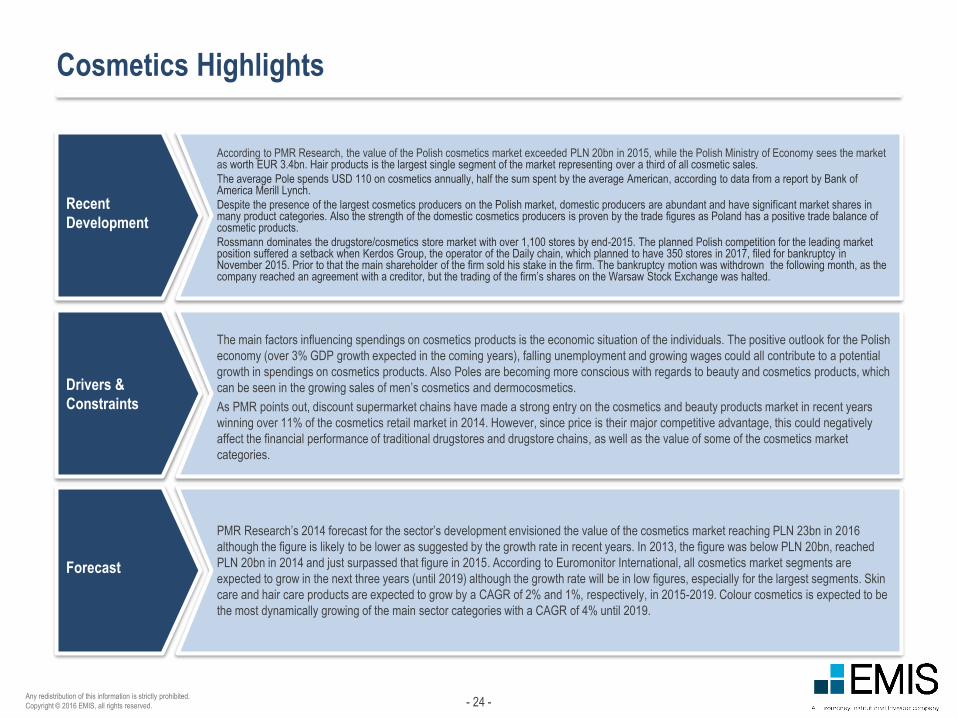

Cosmetics Highlights

Recent

Development

According to PMR Research, the value of the Polish cosmetics market exceeded PLN 20bn in 2015, while the Polish Ministry of Economy sees the market as worth EUR 3.4bn. Hair products is the largest single segment of the market representing over a third of all cosmetic sales.

The average Pole spends USD 110 on cosmetics annually, half the sum spent by the average American, according to data from a report by Bank of America Merill Lynch.

Despite the presence of the largest cosmetics producers on the Polish market, domestic producers are abundant and have significant market shares in many product categories. Also the strength of the domestic cosmetics producers is proven by the trade figures as Poland has a positive trade balance of cosmetic products.

Rossmann dominates the drugstore/cosmetics store market with over 1,100 stores by end-2015. The planned Polish competition for the leading market position suffered a setback when Kerdos Group, the operator of the Daily chain, which planned to have 350 stores in 2017, filed for bankruptcy in November 2015. Prior to that the main shareholder of the firm sold his stake in the firm. The bankruptcy motion was withdrown the following month, as the company reached an agreement with a creditor, but the trading of the firm’s shares on the Warsaw Stock Exchange was halted.

Drivers &

Constraints

The main factors influencing spendings on cosmetics products is the economic situation of the individuals. The positive outlook for the Polish

economy (over 3% GDP growth expected in the coming years), falling unemployment and growing wages could all contribute to a potential

growth in spendings on cosmetics products. Also Poles are becoming more conscious with regards to beauty and cosmetics products, which

can be seen in the growing sales of men’s cosmetics and dermocosmetics.

As PMR points out, discount supermarket chains have made a strong entry on the cosmetics and beauty products market in recent years

winning over 11% of the cosmetics retail market in 2014. However, since price is their major competitive advantage, this could negatively

affect the financial performance of traditional drugstores and drugstore chains, as well as the value of some of the cosmetics market

categories.

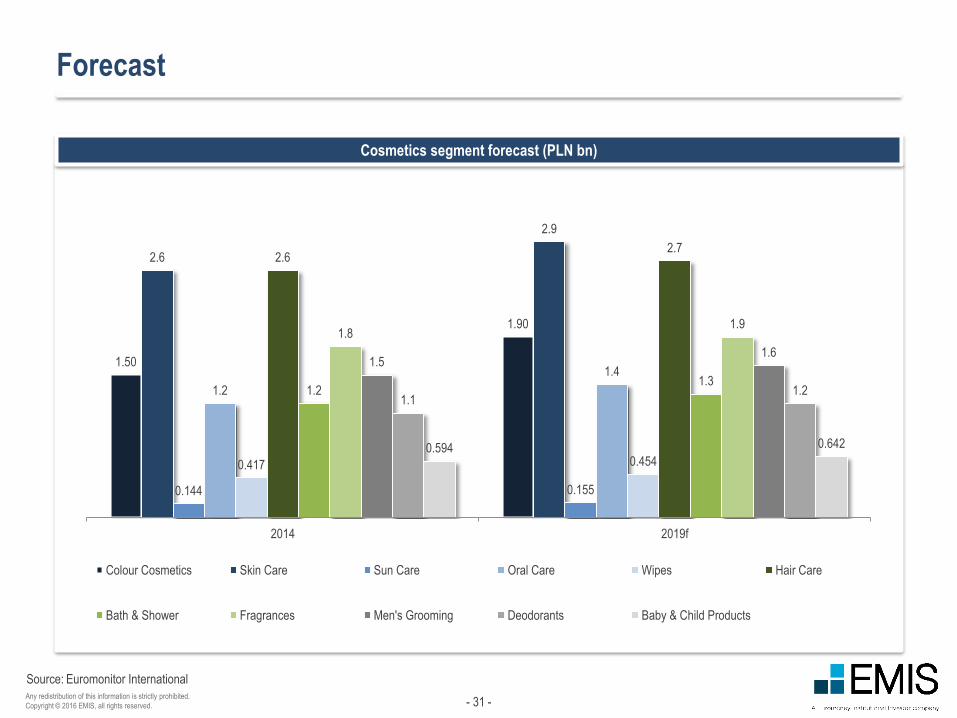

Forecast

PMR Research’s 2014 forecast for the sector’s development envisioned the value of the cosmetics market reaching PLN 23bn in 2016

although the figure is likely to be lower as suggested by the growth rate in recent years. In 2013, the figure was below PLN 20bn, reached

PLN 20bn in 2014 and just surpassed that figure in 2015. According to Euromonitor International, all cosmetics market segments are

expected to grow in the next three years (until 2019) although the growth rate will be in low figures, especially for the largest segments. Skin

care and hair care products are expected to grow by a CAGR of 2% and 1%, respectively, in 2015-2019. Colour cosmetics is expected to be

the most dynamically growing of the main sector categories with a CAGR of 4% until 2019.

- 25 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

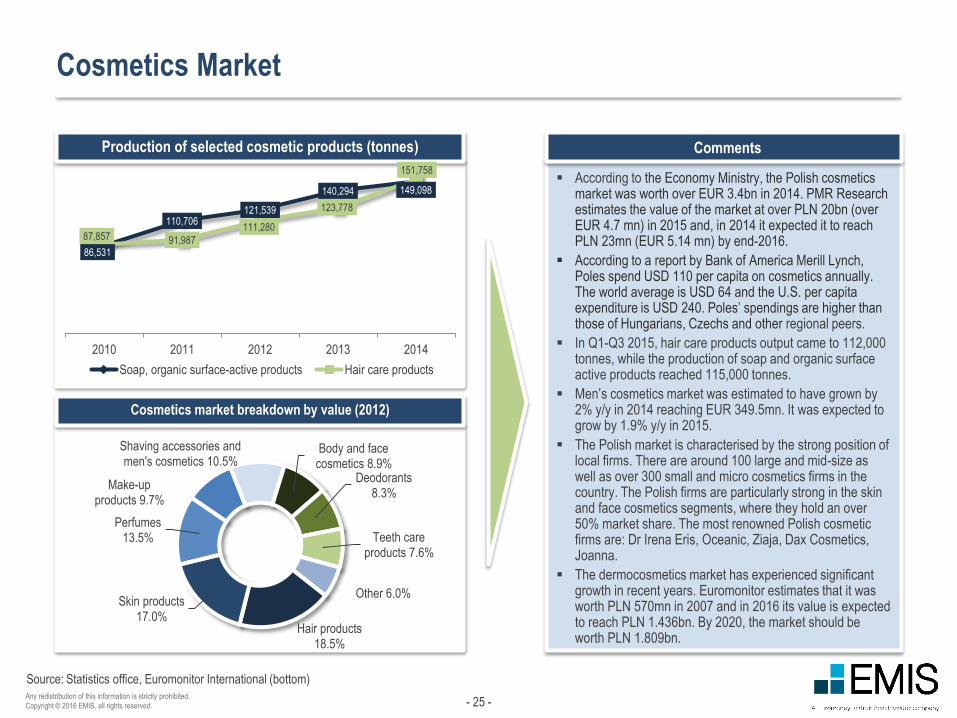

Cosmetics Market

Production of selected cosmetic products (tonnes)

Cosmetics market breakdown by value (2012)

According to the Economy Ministry, the Polish cosmetics market was worth over EUR 3.4bn in 2014. PMR Research estimates the value of the market at over PLN 20bn (over EUR 4.7 mn) in 2015 and, in 2014 it expected it to reach PLN 23mn (EUR 5.14 mn) by end-2016.

According to a report by Bank of America Merill Lynch, Poles spend USD 110 per capita on cosmetics annually. The world average is USD 64 and the U.S. per capita expenditure is USD 240. Poles’ spendings are higher than those of Hungarians, Czechs and other regional peers.

In Q1-Q3 2015, hair care products output came to 112,000 tonnes, while the production of soap and organic surface active products reached 115,000 tonnes.

Men’s cosmetics market was estimated to have grown by 2% y/y in 2014 reaching EUR 349.5mn. It was expected to grow by 1.9% y/y in 2015.

The Polish market is characterised by the strong position of local firms. There are around 100 large and mid-size as well as over 300 small and micro cosmetics firms in the country. The Polish firms are particularly strong in the skin and face cosmetics segments, where they hold an over 50% market share. The most renowned Polish cosmetic firms are: Dr Irena Eris, Oceanic, Ziaja, Dax Cosmetics, Joanna.

The dermocosmetics market has experienced significant growth in recent years. Euromonitor estimates that it was worth PLN 570mn in 2007 and in 2016 its value is expected to reach PLN 1.436bn. By 2020, the market should be worth PLN 1.809bn.

Statistics office, Euromonitor International (bottom)

86,531

110,706121,539

140,294 149,098

87,857 91,987

111,280

123,778

151,758

2010 2011 2012 2013 2014

Soap, organic surface-active products Hair care products

Hair products18.5%

Skin products 17.0%

Perfumes13.5%

Make-up products 9.7%

Shaving accessories and men's cosmetics 10.5%

Body and face cosmetics 8.9%

Deodorants8.3%

Teeth care products 7.6%

Other 6.0%

- 26 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

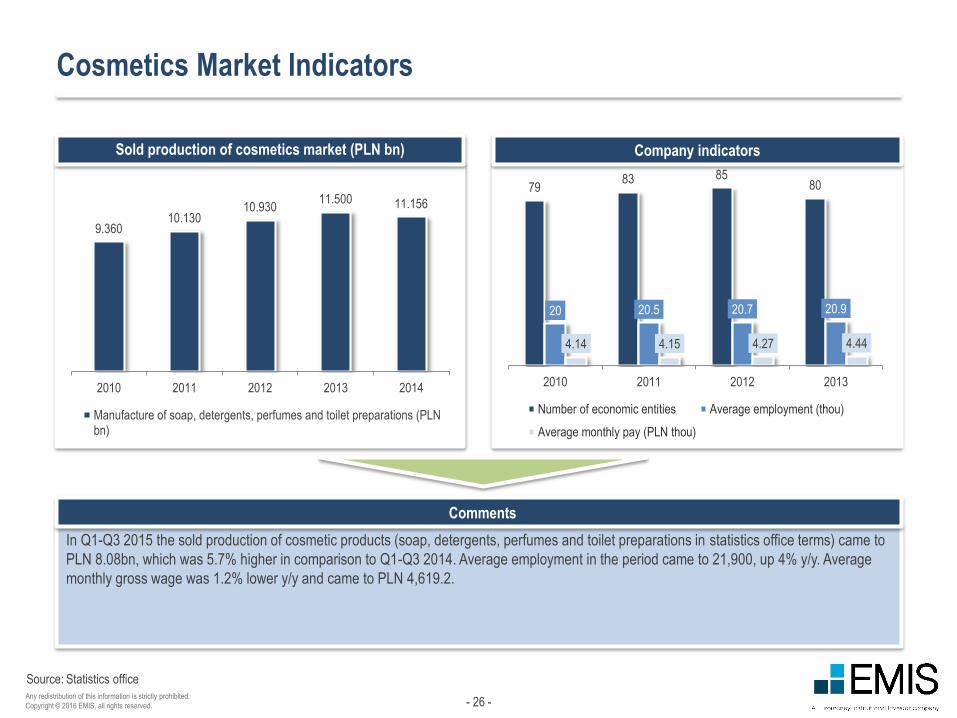

Cosmetics Market Indicators

In Q1-Q3 2015 the sold production of cosmetic products (soap, detergents, perfumes and toilet preparations in statistics office terms) came to

PLN 8.08bn, which was 5.7% higher in comparison to Q1-Q3 2014. Average employment in the period came to 21,900, up 4% y/y. Average

monthly gross wage was 1.2% lower y/y and came to PLN 4,619.2.

Sold production of cosmetics market (PLN bn) Company indicators

Statistics office

7983 85

80

20 20.5 20.7 20.9

4.14 4.15 4.27 4.44

2010 2011 2012 2013

Number of economic entities Average employment (thou)

Average monthly pay (PLN thou)

9.36010.130

10.93011.500 11.156

2010 2011 2012 2013 2014

Manufacture of soap, detergents, perfumes and toilet preparations (PLNbn)

- 27 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

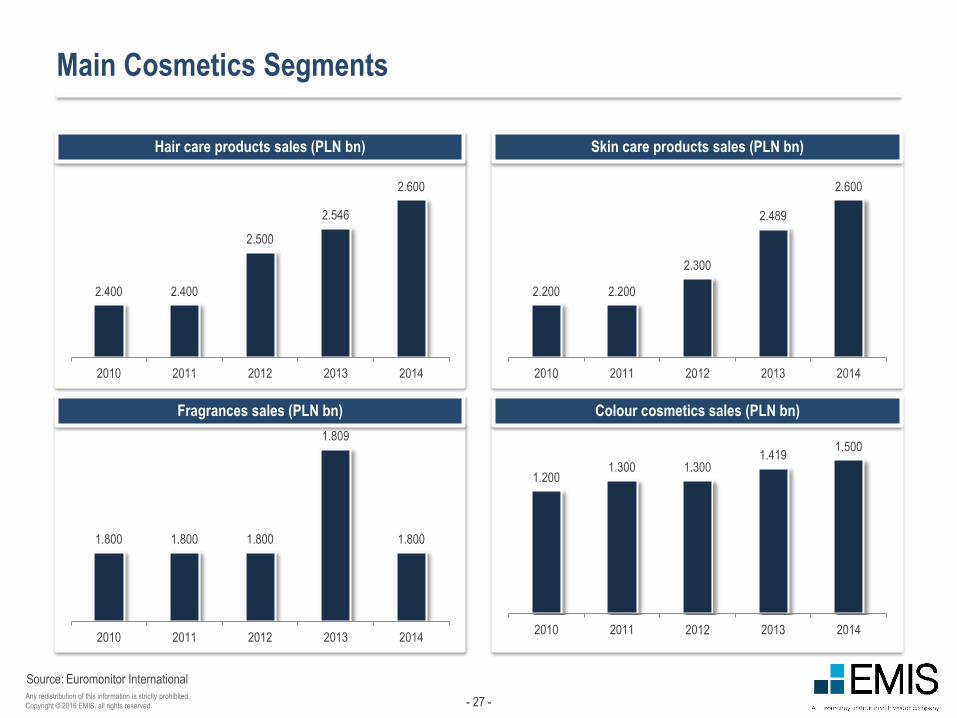

Main Cosmetics Segments

Hair care products sales (PLN bn)

Fragrances sales (PLN bn)

Skin care products sales (PLN bn)

Colour cosmetics sales (PLN bn)

Euromonitor International

2.200 2.200

2.300

2.489

2.600

2010 2011 2012 2013 2014

2.400 2.400

2.500

2.546

2.600

2010 2011 2012 2013 2014

1.800 1.800 1.800

1.809

1.800

2010 2011 2012 2013 2014

1.2001.300 1.300

1.4191.500

2010 2011 2012 2013 2014

- 28 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

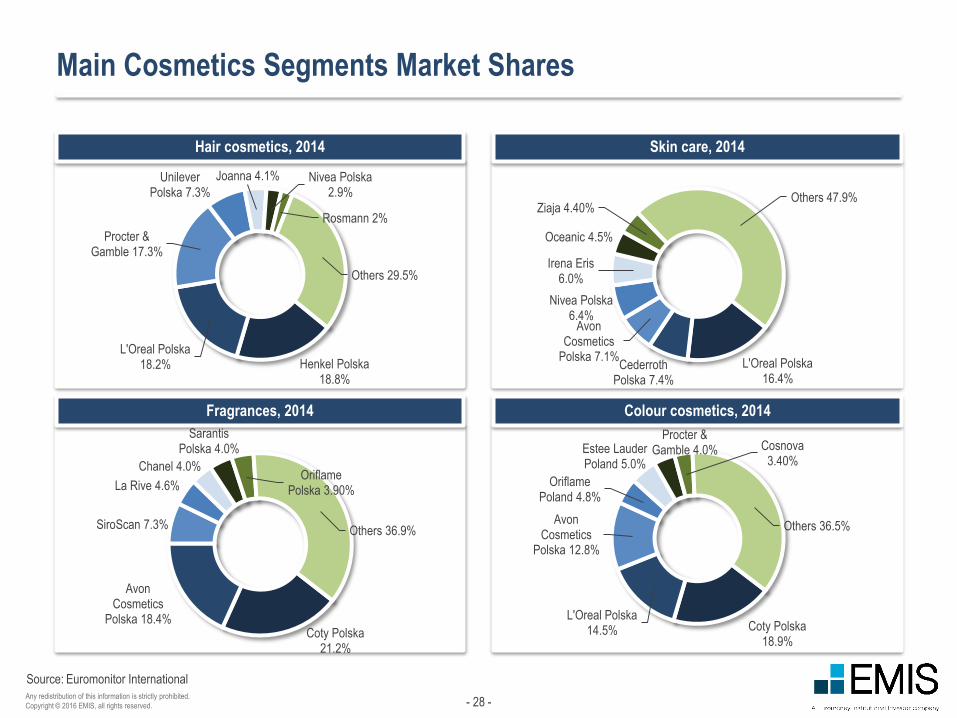

Main Cosmetics Segments Market Shares

Hair cosmetics, 2014

Fragrances, 2014

Skin care, 2014

Colour cosmetics, 2014

Euromonitor International

Henkel Polska18.8%

L'Oreal Polska18.2%

Procter & Gamble 17.3%

Unilever Polska 7.3%

Joanna 4.1% Nivea Polska2.9%

Rosmann 2%

Others 29.5%

L'Oreal Polska16.4%

Cederroth Polska 7.4%

Avon Cosmetics

Polska 7.1%

Nivea Polska6.4%

Irena Eris6.0%

Oceanic 4.5%

Ziaja 4.40%Others 47.9%

Coty Polska21.2%

Avon Cosmetics

Polska 18.4%

SiroScan 7.3%

La Rive 4.6%

Chanel 4.0%

Sarantis Polska 4.0%

Oriflame Polska 3.90%

Others 36.9%

Coty Polska18.9%

L'Oreal Polska14.5%

Avon Cosmetics

Polska 12.8%

Oriflame Poland 4.8%

Estee Lauder Poland 5.0%

Procter & Gamble 4.0% Cosnova

3.40%

Others 36.5%

- 29 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

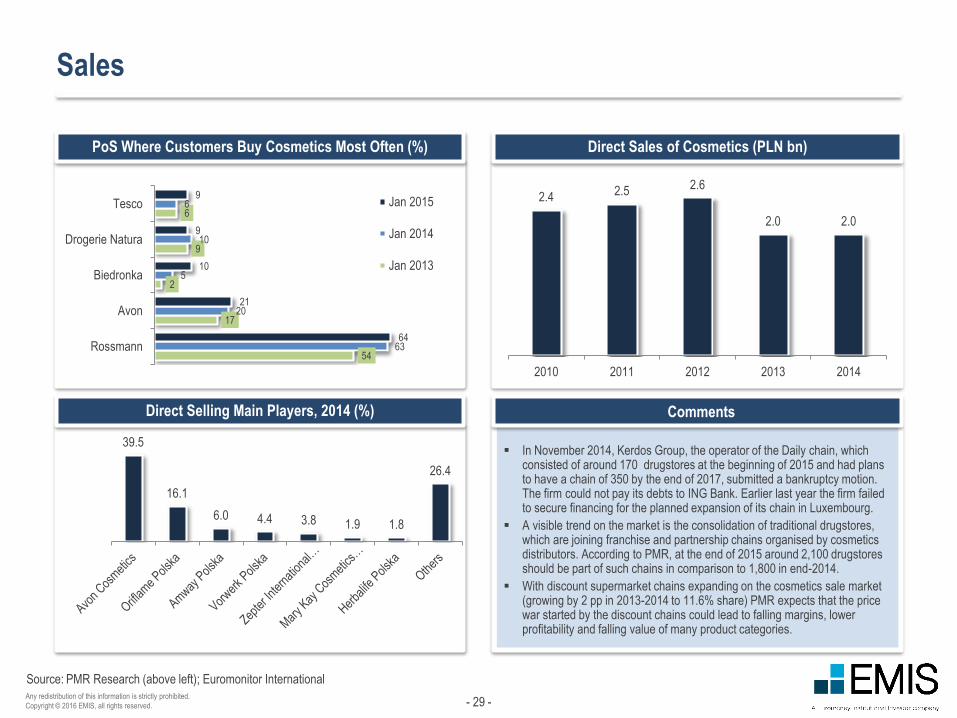

Sales

PoS Where Customers Buy Cosmetics Most Often (%)

Direct Selling Main Players, 2014 (%)

Direct Sales of Cosmetics (PLN bn)

PMR Research (above left); Euromonitor International

In November 2014, Kerdos Group, the operator of the Daily chain, which consisted of around 170 drugstores at the beginning of 2015 and had plans to have a chain of 350 by the end of 2017, submitted a bankruptcy motion. The firm could not pay its debts to ING Bank. Earlier last year the firm failed to secure financing for the planned expansion of its chain in Luxembourg.

A visible trend on the market is the consolidation of traditional drugstores, which are joining franchise and partnership chains organised by cosmetics distributors. According to PMR, at the end of 2015 around 2,100 drugstores should be part of such chains in comparison to 1,800 in end-2014.

With discount supermarket chains expanding on the cosmetics sale market (growing by 2 pp in 2013-2014 to 11.6% share) PMR expects that the price war started by the discount chains could lead to falling margins, lower profitability and falling value of many product categories.

2.4 2.5 2.6

2.0 2.0

2010 2011 2012 2013 2014

39.5

16.1

6.0 4.4 3.8 1.9 1.8

26.4

54

17

2

9

6

63

20

5

10

6

64

21

10

9

9

Rossmann

Avon

Biedronka

Drogerie Natura

Tesco Jan 2015

Jan 2014

Jan 2013

- 30 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Comments

Source:

Exports & Imports

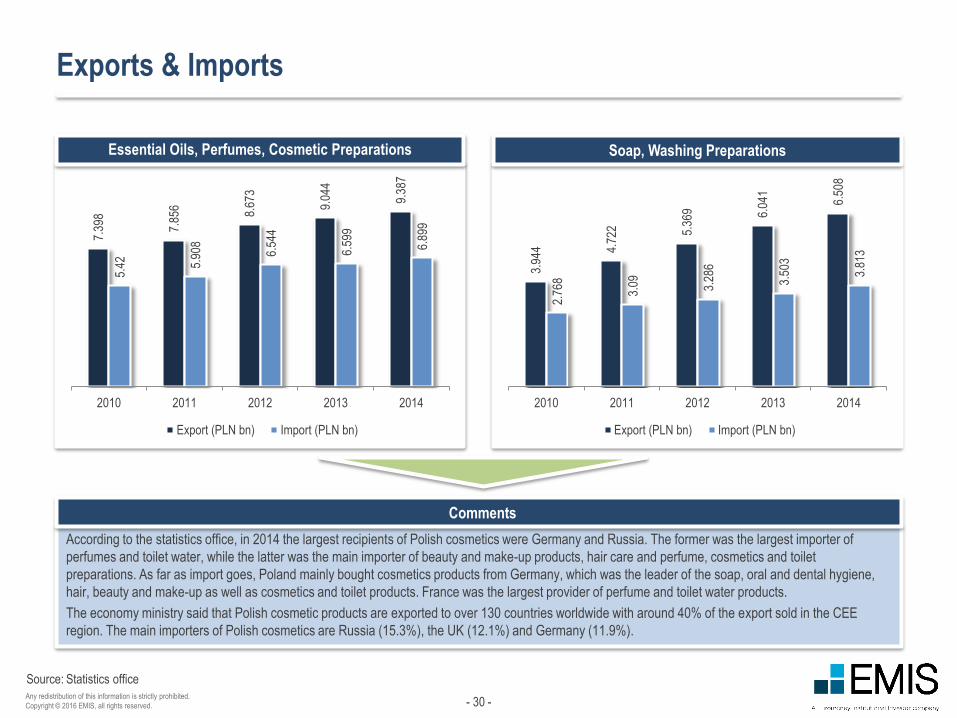

According to the statistics office, in 2014 the largest recipients of Polish cosmetics were Germany and Russia. The former was the largest importer of

perfumes and toilet water, while the latter was the main importer of beauty and make-up products, hair care and perfume, cosmetics and toilet

preparations. As far as import goes, Poland mainly bought cosmetics products from Germany, which was the leader of the soap, oral and dental hygiene,

hair, beauty and make-up as well as cosmetics and toilet products. France was the largest provider of perfume and toilet water products.

The economy ministry said that Polish cosmetic products are exported to over 130 countries worldwide with around 40% of the export sold in the CEE

region. The main importers of Polish cosmetics are Russia (15.3%), the UK (12.1%) and Germany (11.9%).

Essential Oils, Perfumes, Cosmetic Preparations Soap, Washing Preparations

Statistics office

7.39

8

7.85

6 8.67

3

9.04

4

9.38

7

5.42 5.

908

6.54

4

6.59

9

6.89

9

2010 2011 2012 2013 2014

Export (PLN bn) Import (PLN bn)

3.94

4 4.72

2 5.36

9 6.04

1

6.50

8

2.76

8

3.09 3.28

6

3.50

3

3.81

3

2010 2011 2012 2013 2014

Export (PLN bn) Import (PLN bn)

- 31 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

Forecast

Cosmetics segment forecast (PLN bn)

Euromonitor International

1.50

1.90

2.6

2.9

0.144 0.155

1.2

1.4

0.417 0.454

2.62.7

1.21.3

1.81.9

1.51.6

1.11.2

0.594 0.642

2014 2019f

Colour Cosmetics Skin Care Sun Care Oral Care Wipes Hair Care

Bath & Shower Fragrances Men's Grooming Deodorants Baby & Child Products

- 32 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

IV. Main Players

- 33 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

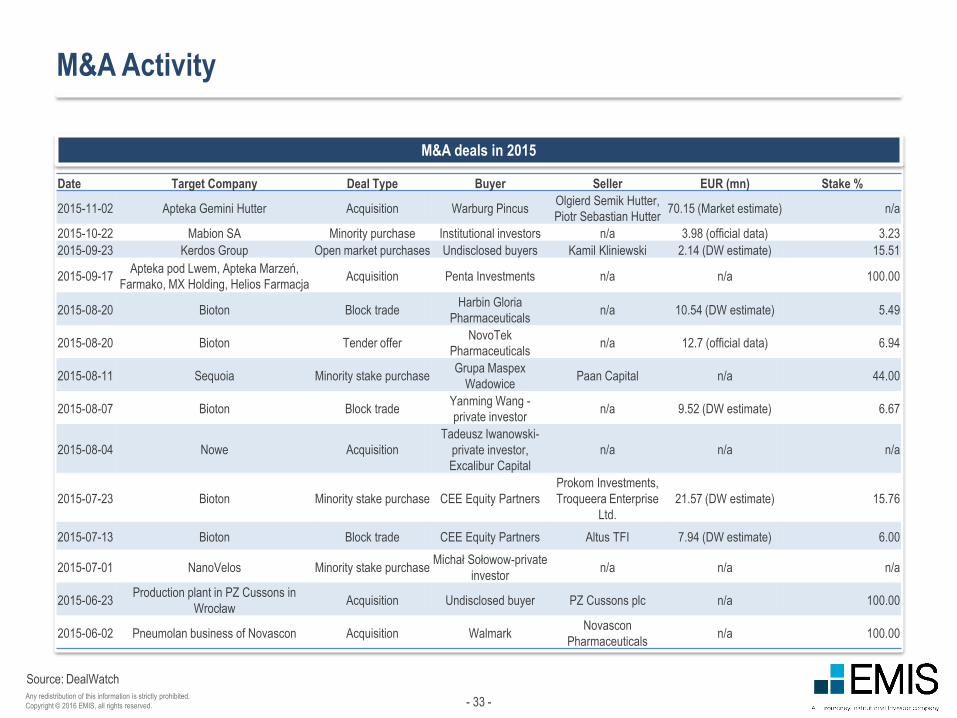

M&A Activity

M&A deals in 2015

DealWatch

Date Target Company Deal Type Buyer Seller EUR (mn) Stake %

2015-11-02 Apteka Gemini Hutter Acquisition Warburg PincusOlgierd Semik Hutter,

Piotr Sebastian Hutter70.15 (Market estimate) n/a

2015-10-22 Mabion SA Minority purchase Institutional investors n/a 3.98 (official data) 3.23

2015-09-23 Kerdos Group Open market purchases Undisclosed buyers Kamil Kliniewski 2.14 (DW estimate) 15.51

2015-09-17Apteka pod Lwem, Apteka Marzeń,

Farmako, MX Holding, Helios FarmacjaAcquisition Penta Investments n/a n/a 100.00

2015-08-20 Bioton Block tradeHarbin Gloria

Pharmaceuticalsn/a 10.54 (DW estimate) 5.49

2015-08-20 Bioton Tender offerNovoTek

Pharmaceuticalsn/a 12.7 (official data) 6.94

2015-08-11 Sequoia Minority stake purchaseGrupa Maspex

WadowicePaan Capital n/a 44.00

2015-08-07 Bioton Block tradeYanming Wang -

private investorn/a 9.52 (DW estimate) 6.67

2015-08-04 Nowe Acquisition

Tadeusz Iwanowski-

private investor,

Excalibur Capital

n/a n/a n/a

2015-07-23 Bioton Minority stake purchase CEE Equity Partners

Prokom Investments,

Troqueera Enterprise

Ltd.

21.57 (DW estimate) 15.76

2015-07-13 Bioton Block trade CEE Equity Partners Altus TFI 7.94 (DW estimate) 6.00

2015-07-01 NanoVelos Minority stake purchaseMichał Sołowow-private

investorn/a n/a n/a

2015-06-23Production plant in PZ Cussons in

WrocławAcquisition Undisclosed buyer PZ Cussons plc n/a 100.00

2015-06-02 Pneumolan business of Novascon Acquisition WalmarkNovascon

Pharmaceuticalsn/a 100.00

- 34 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

Top 10 Sector Companies

Top Firms According to 2014 Revenue (PLN bn) Top Employers in Pharmaceutical/cosmetics Sectors

Rzeczpospolita Lista 500

Company Number of employees

Rossmann Supermarkety Drogeryjne

Polska9,389

Pelion 8,453

TZMO Group 6,296

Neuca 3,630

Farmacol2,672

(in 2013)

Avon Operations Polska 1,824

Polpharma 1,778

Sanofi Group in Poland 855

Bayer 784

GlaxoSmithKline Pharmaceuticals 608

Company Segment Sales revenue

Pelion distribution 7.699

Neuca distribution 6.569

Rossmann Supermarkety

Drogeryjne Polskaretail 5.425

Farmacol distribution 5.361

GlaxoSmithKline

Pharmaceuticalsproduction 4.218

TZMO Group production 2.529

Avon Operations Polska production/ retail 2.398

Bayer production 1.823

Grupa Sanofi Aventis production 1.8

ZF Polpharma production 1.776

- 35 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Highlights

Source:

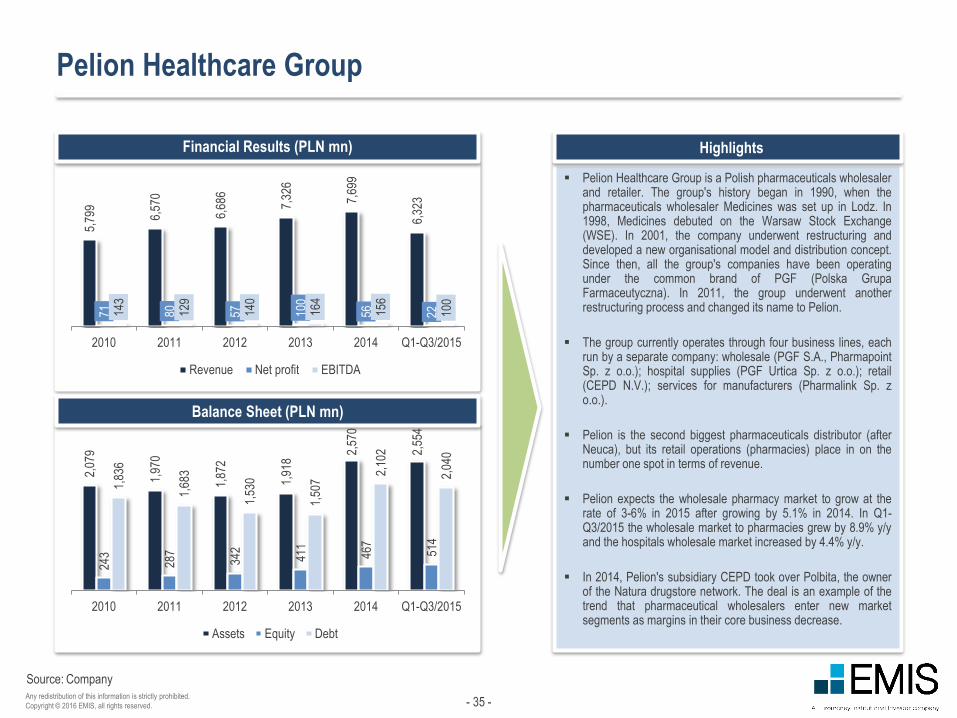

Pelion Healthcare Group

Financial Results (PLN mn)

Pelion Healthcare Group is a Polish pharmaceuticals wholesalerand retailer. The group's history began in 1990, when thepharmaceuticals wholesaler Medicines was set up in Lodz. In1998, Medicines debuted on the Warsaw Stock Exchange(WSE). In 2001, the company underwent restructuring anddeveloped a new organisational model and distribution concept.Since then, all the group's companies have been operatingunder the common brand of PGF (Polska GrupaFarmaceutyczna). In 2011, the group underwent anotherrestructuring process and changed its name to Pelion.

The group currently operates through four business lines, eachrun by a separate company: wholesale (PGF S.A., PharmapointSp. z o.o.); hospital supplies (PGF Urtica Sp. z o.o.); retail(CEPD N.V.); services for manufacturers (Pharmalink Sp. zo.o.).

Pelion is the second biggest pharmaceuticals distributor (afterNeuca), but its retail operations (pharmacies) place in on thenumber one spot in terms of revenue.

Pelion expects the wholesale pharmacy market to grow at therate of 3-6% in 2015 after growing by 5.1% in 2014. In Q1-Q3/2015 the wholesale market to pharmacies grew by 8.9% y/yand the hospitals wholesale market increased by 4.4% y/y.

In 2014, Pelion's subsidiary CEPD took over Polbita, the ownerof the Natura drugstore network. The deal is an example of thetrend that pharmaceutical wholesalers enter new marketsegments as margins in their core business decrease.

Balance Sheet (PLN mn)

Company

5,79

9

6,57

0

6,68

6

7,32

6

7,69

9

6,32

3

71 80 57 100

56 22143

129

140

164

156

100

2010 2011 2012 2013 2014 Q1-Q3/2015

Revenue Net profit EBITDA

2,07

9

1,97

0

1,87

2

1,91

8

2,57

0

2,55

4

243

287

342

411

467

514

1,83

6

1,68

3

1,53

0

1,50

7

2,10

2

2,04

0

2010 2011 2012 2013 2014 Q1-Q3/2015

Assets Equity Debt

- 36 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

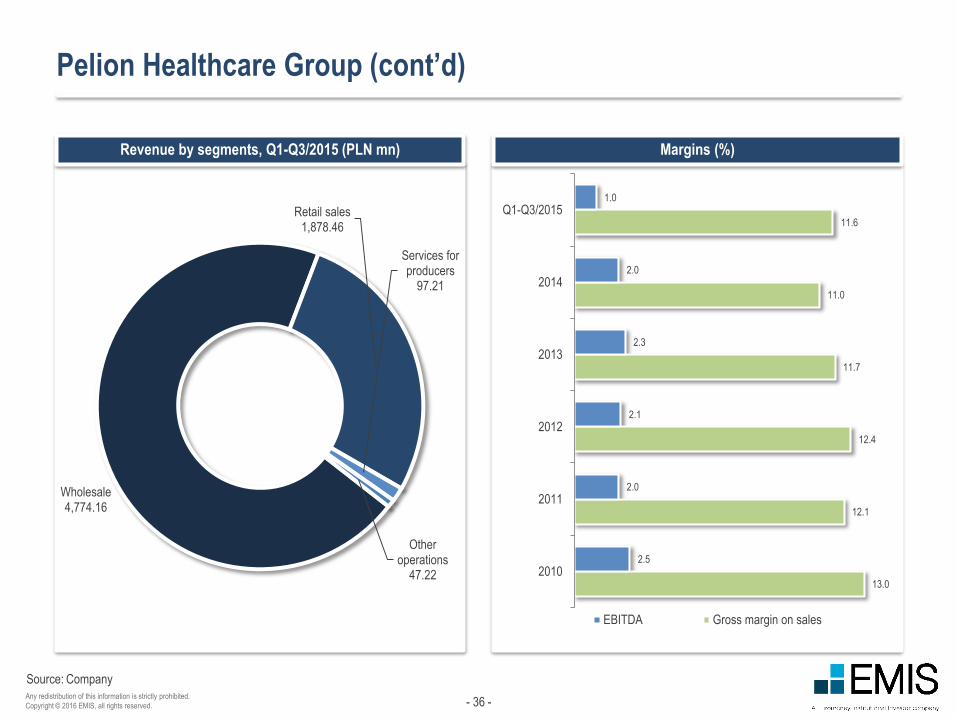

Pelion Healthcare Group (cont’d)

Revenue by segments, Q1-Q3/2015 (PLN mn) Margins (%)

Company

13.0

12.1

12.4

11.7

11.0

11.6

2.5

2.0

2.1

2.3

2.0

1.0

2010

2011

2012

2013

2014

Q1-Q3/2015

EBITDA Gross margin on sales

Wholesale4,774.16

Retail sales1,878.46

Services for producers

97.21

Other operations

47.22

- 37 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Highlights

Source:

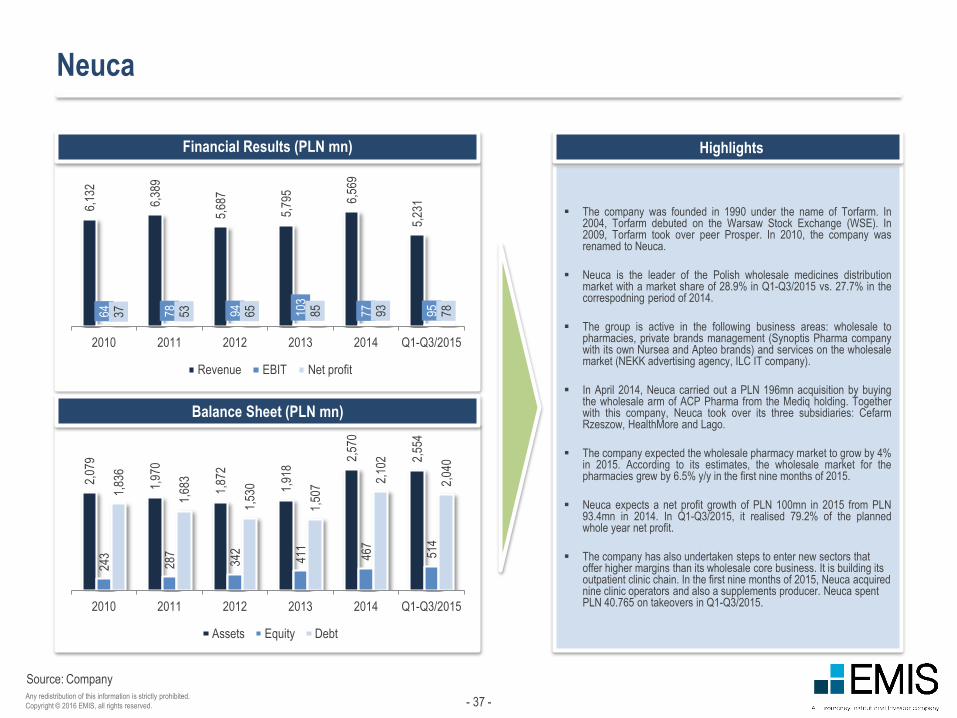

Neuca

Financial Results (PLN mn)

The company was founded in 1990 under the name of Torfarm. In2004, Torfarm debuted on the Warsaw Stock Exchange (WSE). In2009, Torfarm took over peer Prosper. In 2010, the company wasrenamed to Neuca.

Neuca is the leader of the Polish wholesale medicines distributionmarket with a market share of 28.9% in Q1-Q3/2015 vs. 27.7% in thecorrespodning period of 2014.

The group is active in the following business areas: wholesale topharmacies, private brands management (Synoptis Pharma companywith its own Nursea and Apteo brands) and services on the wholesalemarket (NEKK advertising agency, ILC IT company).

In April 2014, Neuca carried out a PLN 196mn acquisition by buyingthe wholesale arm of ACP Pharma from the Mediq holding. Togetherwith this company, Neuca took over its three subsidiaries: CefarmRzeszow, HealthMore and Lago.

The company expected the wholesale pharmacy market to grow by 4%in 2015. According to its estimates, the wholesale market for thepharmacies grew by 6.5% y/y in the first nine months of 2015.

Neuca expects a net profit growth of PLN 100mn in 2015 from PLN93.4mn in 2014. In Q1-Q3/2015, it realised 79.2% of the plannedwhole year net profit.

The company has also undertaken steps to enter new sectors that offer higher margins than its wholesale core business. It is building its outpatient clinic chain. In the first nine months of 2015, Neuca acquired nine clinic operators and also a supplements producer. Neuca spent PLN 40.765 on takeovers in Q1-Q3/2015.

Balance Sheet (PLN mn)

Company

6,13

2

6,38

9

5,68

7

5,79

5

6,56

9

5,23

1

64 78 94 103

77 9537 53 65 85 93 78

2010 2011 2012 2013 2014 Q1-Q3/2015

Revenue EBIT Net profit

2,07

9

1,97

0

1,87

2

1,91

8

2,57

0

2,55

4

243

287

342

411

467

514

1,83

6

1,68

3

1,53

0

1,50

7

2,10

2

2,04

0

2010 2011 2012 2013 2014 Q1-Q3/2015

Assets Equity Debt

- 38 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

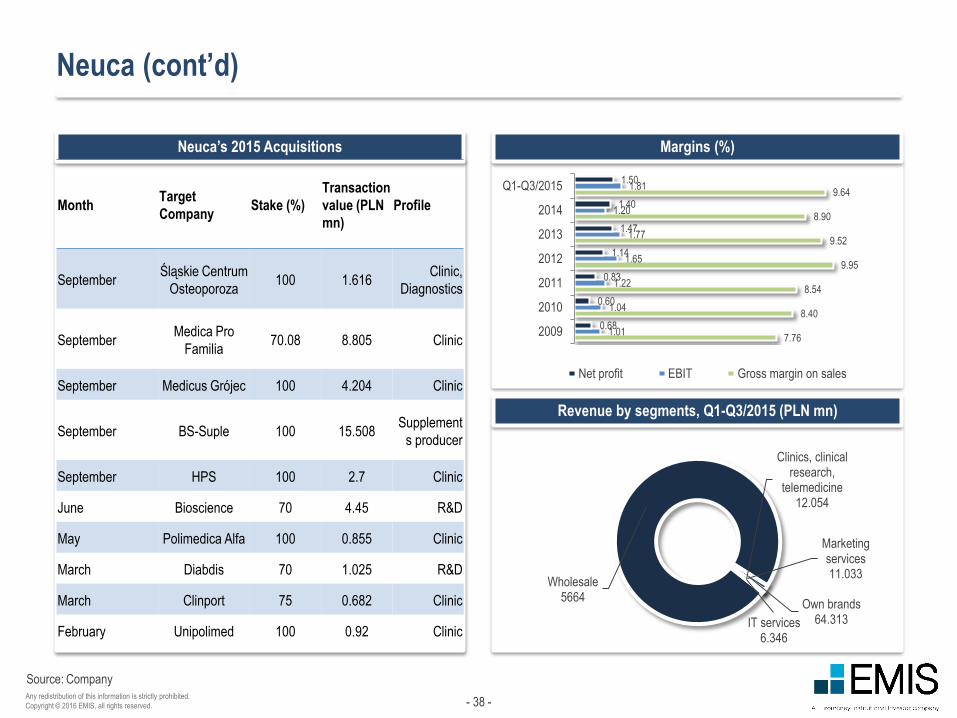

Neuca (cont’d)

Margins (%)

Revenue by segments, Q1-Q3/2015 (PLN mn)

Neuca’s 2015 Acquisitions

Company

7.76

8.40

8.54

9.95

9.52

8.90

9.64

1.01

1.04

1.22

1.65

1.77

1.20

1.81

0.68

0.60

0.83

1.14

1.47

1.40

1.50

2009

2010

2011

2012

2013

2014

Q1-Q3/2015

Net profit EBIT Gross margin on sales

Wholesale5664

Own brands64.313

Marketing services11.033

IT services6.346

Clinics, clinical research,

telemedicine12.054

MonthTarget

CompanyStake (%)

Transaction

value (PLN

mn)

Profile

SeptemberŚląskie Centrum

Osteoporoza100 1.616

Clinic,

Diagnostics

SeptemberMedica Pro

Familia70.08 8.805 Clinic

September Medicus Grójec 100 4.204 Clinic

September BS-Suple 100 15.508Supplement

s producer

September HPS 100 2.7 Clinic

June Bioscience 70 4.45 R&D

May Polimedica Alfa 100 0.855 Clinic

March Diabdis 70 1.025 R&D

March Clinport 75 0.682 Clinic

February Unipolimed 100 0.92 Clinic

- 39 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Highlights

Source:

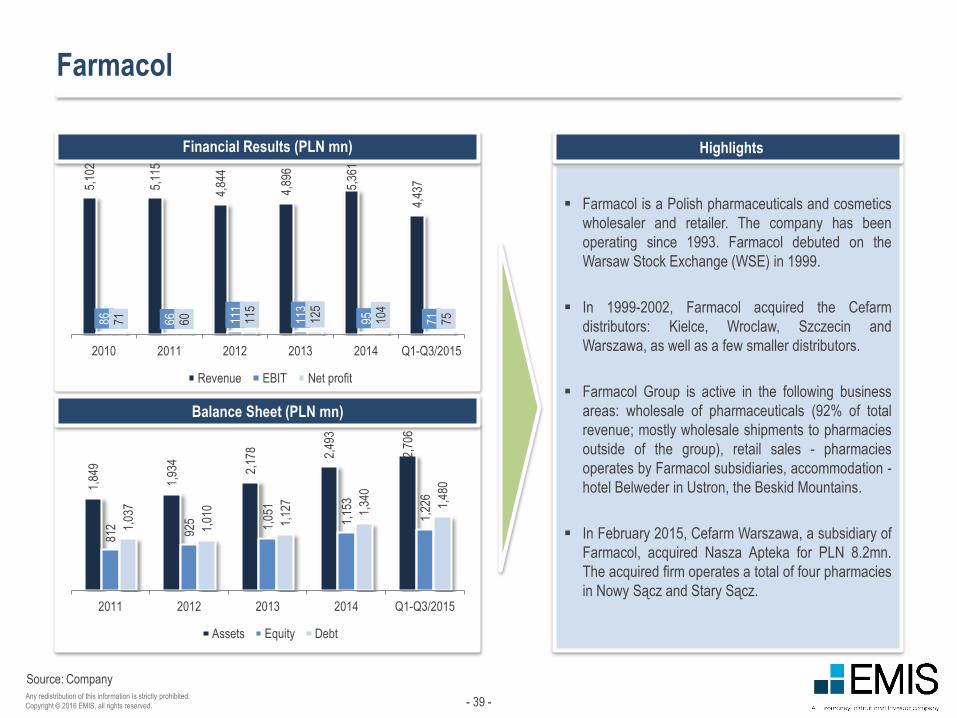

Farmacol

Financial Results (PLN mn)

Farmacol is a Polish pharmaceuticals and cosmetics

wholesaler and retailer. The company has been

operating since 1993. Farmacol debuted on the

Warsaw Stock Exchange (WSE) in 1999.

In 1999-2002, Farmacol acquired the Cefarm

distributors: Kielce, Wroclaw, Szczecin and

Warszawa, as well as a few smaller distributors.

Farmacol Group is active in the following business

areas: wholesale of pharmaceuticals (92% of total

revenue; mostly wholesale shipments to pharmacies

outside of the group), retail sales - pharmacies

operates by Farmacol subsidiaries, accommodation -

hotel Belweder in Ustron, the Beskid Mountains.

In February 2015, Cefarm Warszawa, a subsidiary of

Farmacol, acquired Nasza Apteka for PLN 8.2mn.

The acquired firm operates a total of four pharmacies

in Nowy Sącz and Stary Sącz.

Balance Sheet (PLN mn)

Company

5,10

2

5,11

5

4,84

4

4,89

6

5,36

1

4,43

7

86 66 111

113

95 7171 60 115

125

104

75

2010 2011 2012 2013 2014 Q1-Q3/2015

Revenue EBIT Net profit

1,84

9

1,93

4

2,17

8 2,49

3

2,70

6

812

925 1,05

1

1,15

3

1,22

6

1,03

7

1,01

0

1,12

7

1,34

0

1,48

0

2011 2012 2013 2014 Q1-Q3/2015

Assets Equity Debt

- 40 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Source:

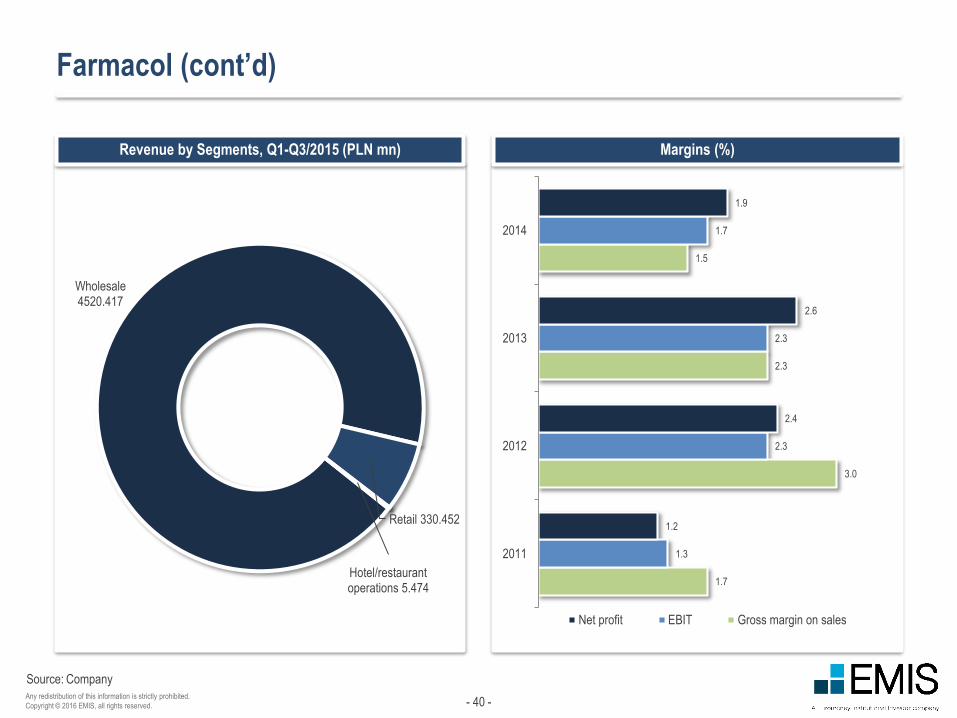

Farmacol (cont’d)

Revenue by Segments, Q1-Q3/2015 (PLN mn) Margins (%)

Company

1.7

3.0

2.3

1.5

1.3

2.3

2.3

1.7

1.2

2.4

2.6

1.9

2011

2012

2013

2014

Net profit EBIT Gross margin on sales

Wholesale4520.417

Retail 330.452

Hotel/restaurant operations 5.474

- 41 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Highlights

Source:

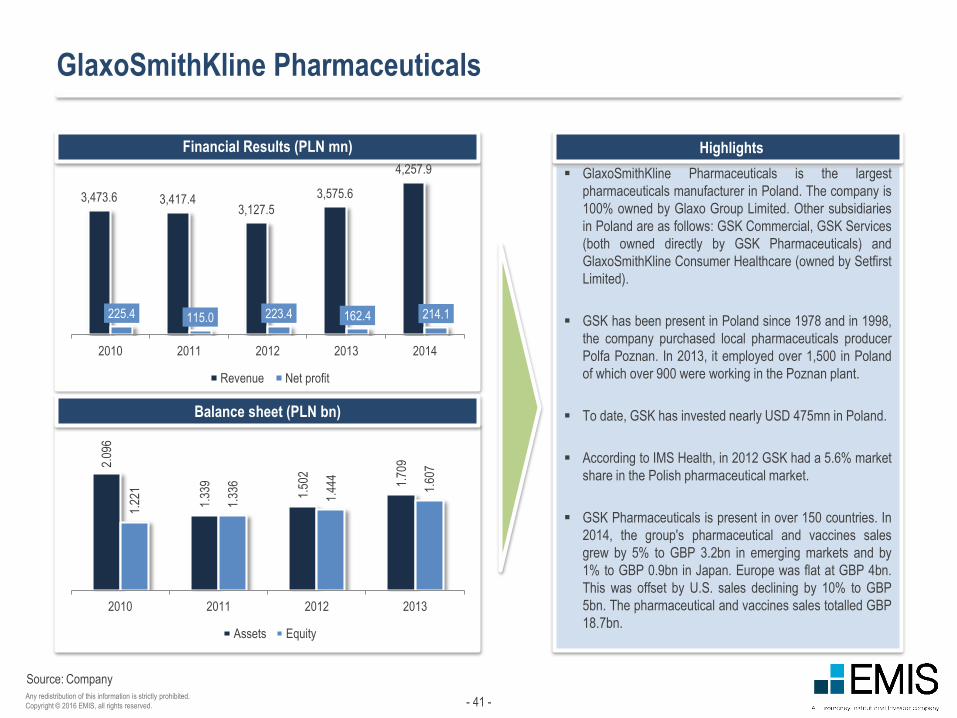

GlaxoSmithKline Pharmaceuticals

Financial Results (PLN mn)

GlaxoSmithKline Pharmaceuticals is the largest

pharmaceuticals manufacturer in Poland. The company is

100% owned by Glaxo Group Limited. Other subsidiaries

in Poland are as follows: GSK Commercial, GSK Services

(both owned directly by GSK Pharmaceuticals) and

GlaxoSmithKline Consumer Healthcare (owned by Setfirst

Limited).

GSK has been present in Poland since 1978 and in 1998,

the company purchased local pharmaceuticals producer

Polfa Poznan. In 2013, it employed over 1,500 in Poland

of which over 900 were working in the Poznan plant.

To date, GSK has invested nearly USD 475mn in Poland.

According to IMS Health, in 2012 GSK had a 5.6% market

share in the Polish pharmaceutical market.

GSK Pharmaceuticals is present in over 150 countries. In

2014, the group's pharmaceutical and vaccines sales

grew by 5% to GBP 3.2bn in emerging markets and by

1% to GBP 0.9bn in Japan. Europe was flat at GBP 4bn.

This was offset by U.S. sales declining by 10% to GBP

5bn. The pharmaceutical and vaccines sales totalled GBP

18.7bn.

Balance sheet (PLN bn)

Company

3,473.6 3,417.43,127.5

3,575.6

4,257.9

225.4 115.0 223.4 162.4 214.1

2010 2011 2012 2013 2014

Revenue Net profit

2.09

6

1.33

9

1.50

2

1.70

9

1.22

1

1.33

6

1.44

4

1.60

7

2010 2011 2012 2013

Assets Equity

- 42 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Highlights

Source:

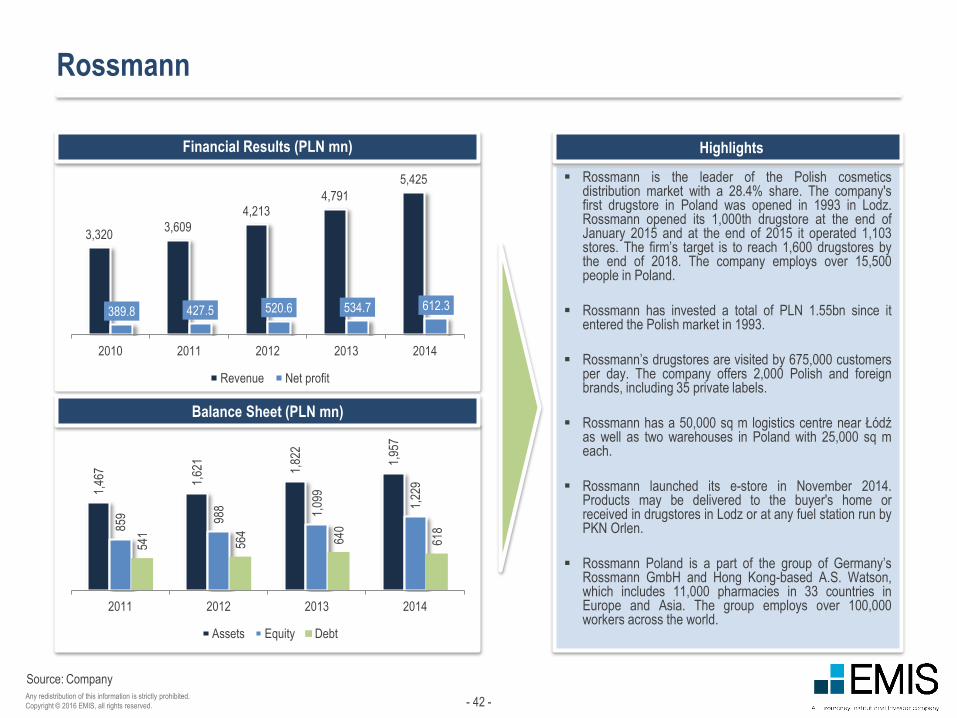

Rossmann

Financial Results (PLN mn)

Rossmann is the leader of the Polish cosmeticsdistribution market with a 28.4% share. The company'sfirst drugstore in Poland was opened in 1993 in Lodz.Rossmann opened its 1,000th drugstore at the end ofJanuary 2015 and at the end of 2015 it operated 1,103stores. The firm’s target is to reach 1,600 drugstores bythe end of 2018. The company employs over 15,500people in Poland.

Rossmann has invested a total of PLN 1.55bn since itentered the Polish market in 1993.

Rossmann’s drugstores are visited by 675,000 customersper day. The company offers 2,000 Polish and foreignbrands, including 35 private labels.

Rossmann has a 50,000 sq m logistics centre near Łódźas well as two warehouses in Poland with 25,000 sq meach.

Rossmann launched its e-store in November 2014.Products may be delivered to the buyer's home orreceived in drugstores in Lodz or at any fuel station run byPKN Orlen.

Rossmann Poland is a part of the group of Germany’sRossmann GmbH and Hong Kong-based A.S. Watson,which includes 11,000 pharmacies in 33 countries inEurope and Asia. The group employs over 100,000workers across the world.

Balance Sheet (PLN mn)

Company

3,3203,609

4,2134,791

5,425

389.8 427.5 520.6 534.7 612.3

2010 2011 2012 2013 2014

Revenue Net profit

1,46

7

1,62

1

1,82

2

1,95

7

859 98

8 1,09

9

1,22

9

541

564

640

618

2011 2012 2013 2014

Assets Equity Debt

- 43 -Any redistribution of this information is strictly prohibited.

Copyright © 2016 EMIS, all rights reserved.

Contact:

Corporate Headquarters

6-8 Bouverie Street

London EC4Y 8DD

UK

Voice: +44 20 7779 8100

Fax: +44 20 7779 8224

Americas Headquarters

225 Park Avenue South

New York, New York 10003

US

Voice: +1 212 610 2900

Fax: +1 212 610 2950

Asia Headquarters

Eucharistic Congress Bldg. No. III

4th Floor, 5 Convent Street

Mumbai 400 001

India

Voice: +91 22 22881123

Fax: +91 22 22881137

Disclaimer:

The material is based on sources which we believe are reliable, but no warranty, either expressed or implied, is provided in relation to the accuracy or completeness

of the information. The views expressed are our best judgment as of the date of issue and are subject to change without notice. EMIS and Euromoney Institutional

Investor PLC take no responsibility for decisions made on the basis of these opinions.

Any redistribution of this information is strictly prohibited. Copyright © 2016 EMIS, all rights reserved. A Euromoney Institutional Investor company.

About EMIS Insight

EMIS Insight is a unit of EMIS that produces proprietary strategic research and analysis. The service features market overviews, industry trend analysis, legislation

and profiles of the leading sector companies provided by locally-based analysts.

About EMIS

Founded in 1994, EMIS (formerly known as ISI Emerging Markets) was acquired by Euromoney Institutional Investor PLC in 1999. EMIS works from over 15 offices

around the world to deliver electronic information products, by subscription, to institutional customers globally. EMIS provides hard-to-get information covering more

than 100 emerging markets. Its flagship products are EMIS Intelligence and EMIS Professional.

EMIS clients include top investment banks, corporations, law firms, consultants, investment and insurance companies, universities and libraries, multilateral

organisations, and others.