The Affordable Care Act

An American Story

John J. Sarno, Esq.

Employers Association of New Jersey

www.eanj.org

1

Patient Protection and Affordable

Care Act

March 23, 2010

A New Era for America2

U.S. Supreme court heard oral argument on the

constitutionality of the Affordable Care Act on

March 26-28, 2012

3

NFIB v. SebeliusU.S. Supreme Court (2012)

Personal Mandate exceeds Congress’ power to

regulate commerce but is a valid tax

4

U.S. Health Care Spending

About 18% of the U.S. economy (in 1950, 5%)

Estimated $2.90 trillion in 2013

Most health care spending per capita in the world

5

6

Health Care Outcomes – U.S.

33rd among developed nations in infant mortality

(6.3/1,000)

50th in life-expectancy (78-years)

7

Estimated 46 million Americans lack health

care insurance (17% of U.S. population)

The Uninsured

8

9

Employer-Plan Crisis

Premiums have grown 4-times faster than

wages since 1999.

Average employee contribution has gone up

200% since 2000.

Out-of-pocket and co-payments have gone

up 115% since 2000.

Five Pillars of Reform

Insurance Reform

Consumer Protections

Personal Mandate

Subsidized Coverage

Health Insurance Marketplace (Exchange)

10

Insurance Reform

High-risk pool created (2010)

Dependent coverage to age 26 (2010)

Children with pre-existing conditions cannot be denied coverage (2010)

No denial for pre-existing conditions eliminated (2014)

No Charge for annual wellness visit (2014)

Guaranteed issue policy (2014)

Modified community ratio (2014)

80 – 85% medical loss ratio (2014)

Long-term insurance program (2014)

No pre-existing condition exclusions (2014)

11

All Plans Must Provide

Essential Health Benefits

“Essential Health Benefits” requires minimum set of benefits, with no lifetime of annual coverage limits

Ambulatory patient services

Emergency services

Hospitalization

Maternity and newborn care

Mental health and substance abuse coverage

Prescription drugs

Rehab services and medical devices

Preventative and wellness/chronic disease management

12

“Free” Preventive Care

No Co-Pays

No Out-Of-Pockets

No Deductibles

13

Health Delivery Reforms

Research on best provider practices

Research on comparative evidence outcomes

Pilot program that pays for outcomes on flat fee

basis rather than fee for service for treatments

Medical IT

Standards for extended living arrangements

Hospice, home-health reimbursement

14

15

Community Investment

Health Care Clinics

Primary Care Training

Grants to States

Diversity and Cultural Competency

Education Curricula Development in Health Sciences

Food Labeling

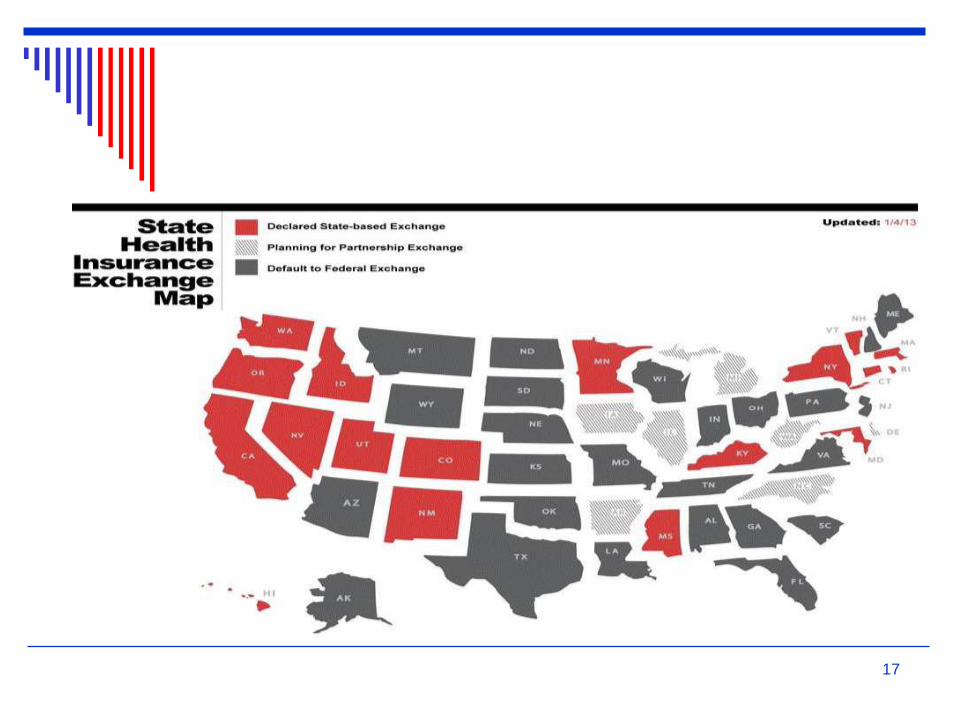

The Health Insurance Exchange

Healthcare.gov

Uninsured individuals not eligible for Medicare or Medicaid will be permitted to purchase insurance through state Exchanges (purchasing pools).

Individuals will be eligible for subsidies.

Employers with fewer than 100 employees will be permitted to enroll.

Employer eligibility may be expanded in 2017.

16

17

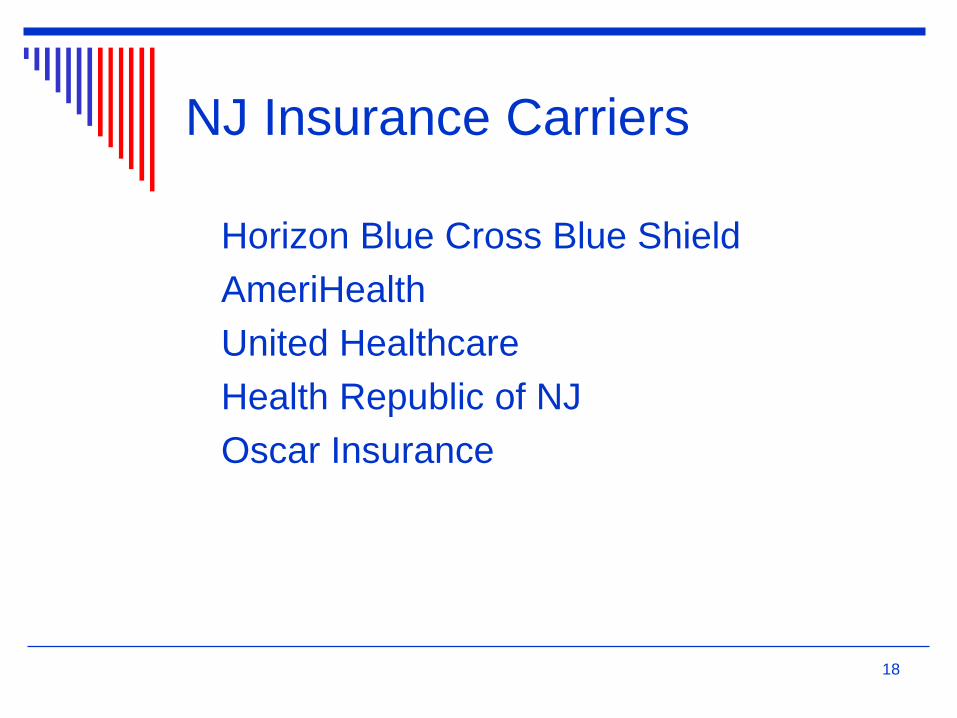

NJ Insurance Carriers

Horizon Blue Cross Blue Shield

AmeriHealth

United Healthcare

Health Republic of NJ

Oscar Insurance

18

Exchange Enrollment – N.J.

March, 2015

254,316 enrolled

23% - 18 – 34

15% - 35 – 44

22% - 45 – 54

33% - 55 – 64

19

20

Subsidies – NJ

85% eligible for subsidies

$306 – average tax credit

$780 million in total subsidies

FamilyCare (Medicaid) – NJ

(2014)

396,000 enrollment

2.2 billion in Federal Funds

Only 40% of NJ doctors participate in the

program

21

Types of Plans

Bronze 60% of costs

Silver 70% of costs

Gold 80% of costs

Platinum 90% of costs

Most popular in NJ – Silver, mid-level

80% of enrollees pay $100 or less per

month

22

Problems

Narrow or Inadequate Provider Networks

Price (not eligible for subsidy)

“Family Glitch”

23

The Political Process:

Follow the Money

6 lobbyists for every member of

Congress

Insurance Industry - $100 million

Pharma - $110 million

Providers - $80 million

Hospitals - $90 million

Medical Device - $30 million

24

The pharmaceutical industry alone spent

over $600,000 per day in lobbying (2.3

lobbyists per member of Congress)

25

The process produced a 1,129 – page bill and

9,625 pages of regulations

26

New Revenue for Business

and Industry

$200 billion – Pharma

$205 billion – Hospitals

$102 billion – Insurance companies

$38 billion – Insurance industry

27

Taxes and Fees (10-years)

$240 billion insurance and medical

device industries

$280 billion Medicaid discounts given by

hospitals and pharma

28

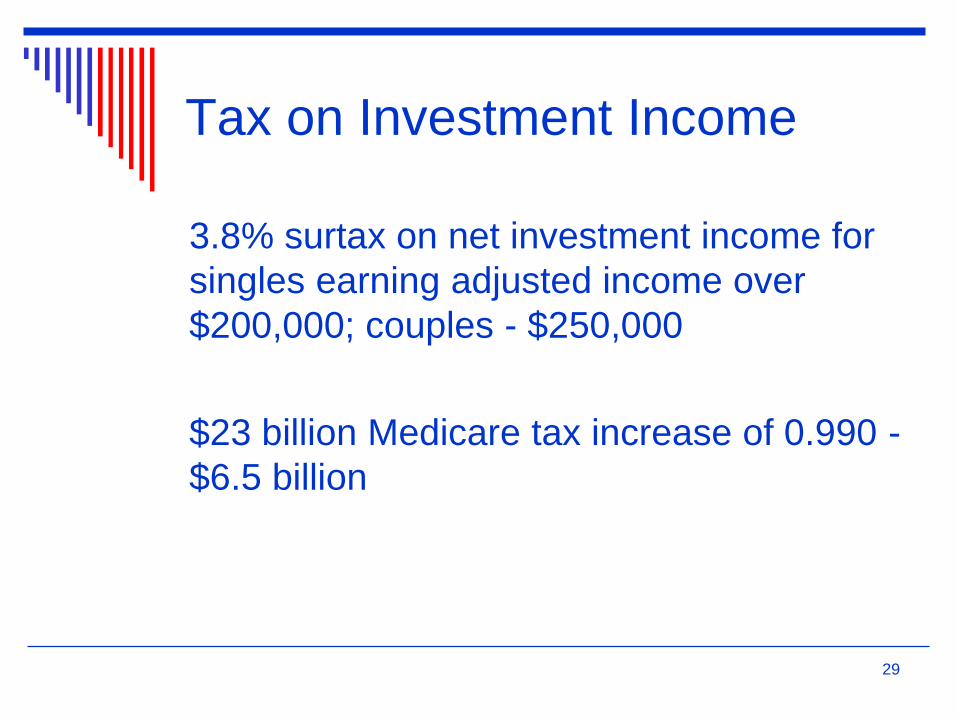

Tax on Investment Income

3.8% surtax on net investment income for

singles earning adjusted income over

$200,000; couples - $250,000

$23 billion Medicare tax increase of 0.990 -

$6.5 billion

29

Early Results

17% - uninsured before ACA

13% - 2014

16.4 million more Americans insured

3.54 billion in subsidies

30

Cost and Revenues

(estimated)

$4,600 – per person, per year in taxes,

subsidies

4,900 – new revenue for 4 major

industries

31

32

“Large” Employer Penalty

(2015)

Employers with 100 or more “full-time” employees will be penalized for not offering coverage or coverage that does not meet standards.

All employees counted in a calendar month (part-time, temporary, seasonal).

“Full-time” employee is someone who is employed to perform services on average of 30-hrs per week or 120 hrs/month.

Part-time employees are grouped together to create “full-time” equivalents.

Aggregate number of hours worked by part-time workers in any month and divide by 120 to determine number of full-time equivalents.

33

Penalty for not offering insurance or to

less than 70% of full-time employees and

at least one FTE receives a subsidy to pay

for insurance on the Exchange

$2,000 per full-time employee after first 80 employees

34

Affordability

Full-time employee cannot pay more than 9.5% of household income for his/her share of premium for single coverage. Lowest cost plan.

Safeharbor: Employer may use W-2 income for employee. (Box 1)

Rate of Pay Safeharbor – Hourly rate multiplied by 130 hrs/month. Determine affordability using monthly premium based on monthly wage. For salaried employee, monthly wage can be used. Does not apply where wages were reduced during the year.

35

Auditing and Enforcement

U.S. Department of Treasury (IRS)

U.S. Department of HHS

U.S. Department of Labor

Combined databases – Form W-2, Form

5500, Social Security Administration

database.

36

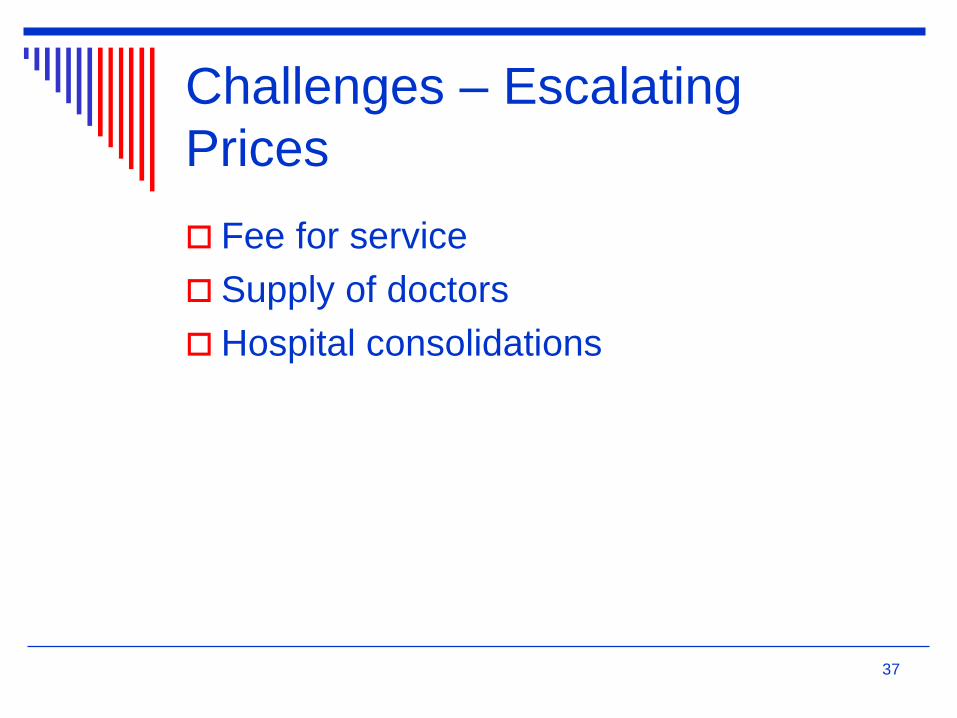

Challenges – Escalating

Prices

Fee for service

Supply of doctors

Hospital consolidations

37

Potential Solution

Accountable Care Organization (ACO)

38

The Wildcard

King v. Burwell

Argued March 3, 2015

Expected decision: June 30, 2015

39

Questions?

40

Thank You

![The Patient Protection and Affordable Care Act [PPACA = ACA]](https://static.cupdf.com/doc/110x72/56813484550346895d9b6444/the-patient-protection-and-affordable-care-act-ppaca-aca.jpg)