Optimal Gradual Annuitization:Optimal Gradual Annuitization:Quantifying the Cost of Switching to Quantifying the Cost of Switching to

AnnuitiesAnnuities

by

Wolfram Horneff*, Raimond Maurer*, and Michael Stamos*

*Department of Finance, Goethe University Frankfurt, Germany

2007 IME Conference, Piraeus, Greece

Goethe University Frankfurt, Germany

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 2/19

Introduction

Increasing public awareness of longevity insurance PAYGO vs. privately funded pension system DB vs. DC

Developing a strategy for retirement is key (Retirement assets in the US: 15 Trillions)

Individuals have the role of risk managers

Main risks: (1) capital market risks(2) mortality

Building portfolios of mutual funds and life-annuities Intertemporaneous mix Contemporaneously mix Advantage: access both equity premium and longevity insurance

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 3/19

Policy/Regulatory Relevance

UK: accumulated occupational pension assets has to be annuitized by age 75

Germany’s “Riester” plans provide a tax inducement if life annuity payments begin to pay out at age 85

In the US, annuitization not compulsory for 401(k) plans Low annuity demand tax laws require minimum distributions to begin at age 70 ½

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 4/19

Annuity Mechanics I: Mortality Credit

Simple 1-period example: Alternative 1: direct bond investmentAlternative 2: invest in bonds through annuity

Real interest rate: r = 2%, survival prob.: p = 90%

Age dependent return profile

End-of-year payoff

Initial Investment Alive Dead

(1) 100 (in bond) 100(1+r)=102

100(1+r)=102

(2)

End-of-year payoff

Initial Investment Alive Dead

(1) 100 (in bond) 100(1+r)=102

100(1+r)=102

(2) 100 (in annuity) 100(1+r)/p=113.3 0

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 5/19

Annuity Mechanics II

Immediate Constant Payout Life Annuity: like a fixed coupon corporate bond (default: time of death)

Pricing:

Mortality credit is compensation for illiquidity: Once purchased annuities have to be held until deathOpportunity costs: no equity premium, lack of bequest

potential, inflexibility

T

ts

R

at

tsf

tT

tsts

f

att

t

tsf

spR

CF

R

spCFPR

11

)(1

)(

Mortality credit

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 6/19

Most Related Insurance Literature

Blake, Cairns, and Dowd, (2003), Pensionmetrics II: Stochastic pension plan design during the distribution phase, Insurance: Mathematics and Economics. Numerical derivation of complete switching time (with varying

bequest motive and annuity costs)

Milevsky and Young, 2007, Annuitization and Asset Allocation, Journal of Economic Dynamics and Control. Derived analytically optimal asset allocation and complete switching

time Also, gradual annuitization derived for restrictive case (up to solution

of ODEs) (constant force of mortality, no annuity cost) But, lack of pre-existing pension income, bequest motives

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 7/19

Contributions

Comparison of different annuitization strategies: Complete stochastic switching Partial stochastic switching Gradual annuitization

Dynamic optimization of asset allocation (stocks, bonds and annuities) and consumption

Robustness: Pre-existing pensions (e.g. public and/or occupational) Non additive utility (Epstein/Zin) Bequest motives Annuity costs

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 8/19

The Model: Capital Markets

Riskless bonds: Rf: riskless growth rate in real terms (= 1.02)

Risky stocks: Rt ~ LN(,)

: expected growthrate (= 1.06) : standard deviation (= 18 percent)

Bonds and stocks can be traded each year

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 9/19

The Model: Wealth Evolution

Contemporary budget constraint Gradual Annuitization Partial Switching Complete Switching

Wt: cash on handMt: amount invested in bonds St: amount invested in stocksPRt: amount invested in annuity Ct: consumption

Cash on hand in t + 1 conditional on survivalGradual Annuitization Partial Switching Complete Switching

Wt+1: next period cash on handLt+1: sum of annuity payments

Pt+1: annuity payoutsYt+1: public pension income.

ttttt CPRSMW

1111 ttttftt YLRSRMW

tMSC

tPRMSCW

ttt

ttttt ,

,

t

t

t

PR

MS

CW t

tt

tt

,

,

,

0

tP

t

RMRSYW ftttt

,

,0

11

tP

tRMRS

YW

fttt

t

,

,1

1

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 10/19

The Model: Preferences

Preferences as in Epstein and Zin (1989) are described by

level of relative risk aversion (= 5)

elasticity of intertemporal substitution (= 0.2)

personal discount factor (= 0.96)

k: strength of the bequest motive ( =0)

ps: subjective survival probabilities (population average [male])

C: consumption

B: bequest

Choose Ct, Mt, St and PRt in the way that Vt is maximized

/11

1

1

/111

11

1/11 11

tstt

sttt

stt BkpVpECpV

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 11/19

The Model: Optimization Problems

Complete Switching:

Partial Switching:

Gradual Annuitization:

00

VMaxttt BSC ,,,

00

VMaxPRBSC T

ttt ,,,,

00

VMaxT

tttt PRBSC ,,,

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 12/19

The Model: Numerical Solution

Normalize all variables with public pension income

Dynamic stochastic optimization of the Bellman equation in a 3-dimensional state space: Discretize continuous state variables:

- Normalized wealth- Normalized sum of annuity payouts

Discrete state variables:- Age- Switched or not

Calculations of expectations (multiple integral): gaussian cubature integration

One period optimization: numerical constrained maximization Value function derived by piecewise bi-cubic-splines Policy function by bi-cubic splines and neighboring interpolation

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 13/19

Optimal Policies: Demand for Annuities (No Bequest)

Wealth Age

Annuity Payouts = 0

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 14/19

Value of Postponing Annuitization

VSW(PR,.) < VSW(PR=0,.)No purchase region

PR0

VSW(PR,.) ≥ VSW(PR=0,.)Purchase region

VSW(PR,.)

PRind

OpportunityCosts

VSW(PR=

VSW(PR=0,.)

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 15/19

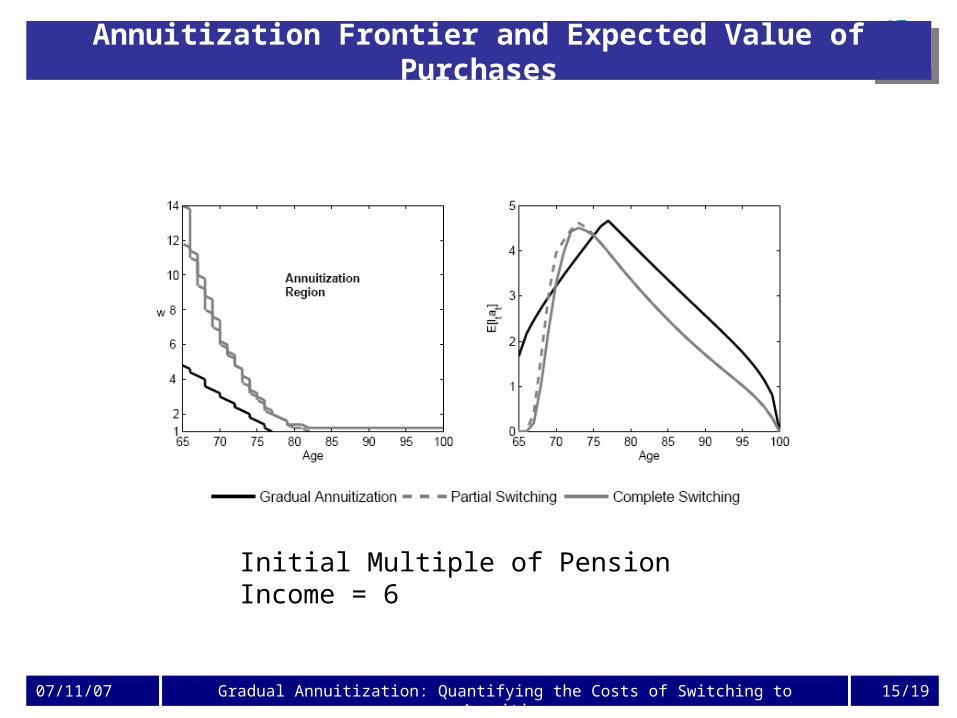

Annuitization Frontier and Expected Value of Purchases

Initial Multiple of Pension Income = 6

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 16/19

Optimal Expected Annuity Stock Fraction for Various CRRA

Initial Multiple of Pension Income = 6

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 17/19

The Impact of IES on

Initial Multiple of Pension Income = 6

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 18/19

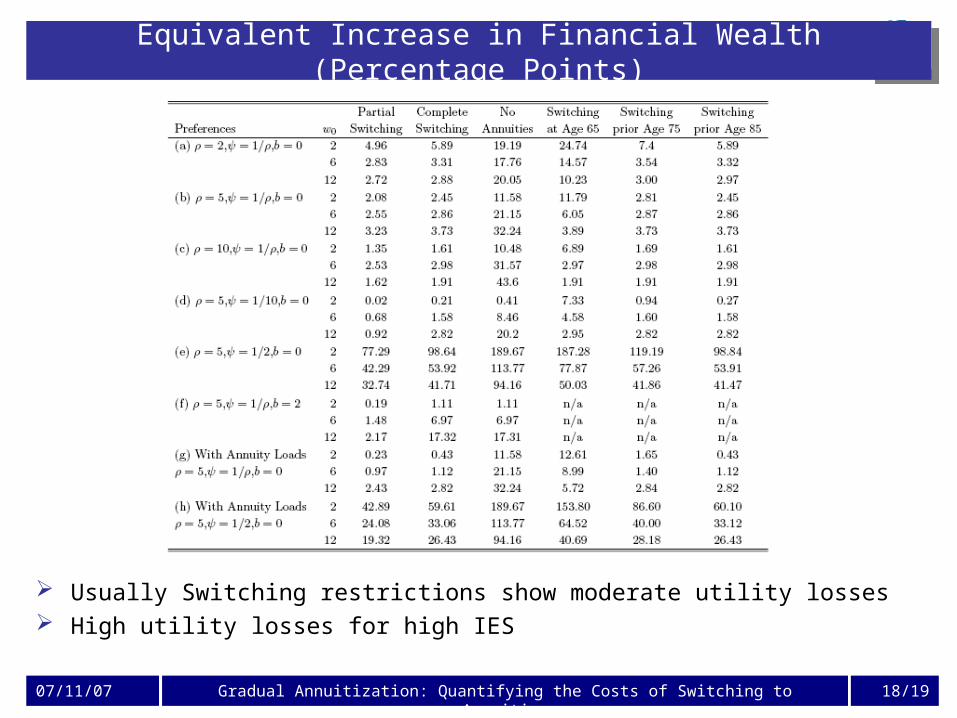

Equivalent Increase in Financial Wealth (Percentage Points)

Usually Switching restrictions show moderate utility losses High utility losses for high IES

07/11/07 Gradual Annuitization: Quantifying the Costs of Switching to Annuities 19/19

Conclusions

Hedging longevity risk is valuable for the retiree

Trade offs: Age effect: (1) increasing mortality credit (mortality risk),

(2) decreasing human capital/pension wealth Wealth effect: the higher wealth on hand compared to bond-like human

capital, the lower is the stock demand

Switching restrictions: annuitization postponed: wait until mortality credit high enough to

compensate higher opportunity costs High welfare losses for (1) Switching at 65 and (2) High IES

Future work: Interest rate risk and inflation risk Alternative longevity insurance Implications of Taxes and Housing (Reverse Mortgage)