Second Quarter 2013

NCCI C fNCCI ConferenceApril 3, 2014

Sasha WeintraubVP, Fuels & Systems Optimization

Second Quarter 2013

NCCI Coal ConferenceApril 25, 2012

Fueling Up within the “Game Changer”

S h W i t bSasha WeintraubDuke Energy

The “Game Changer” is Happening

IHS CERA (September 5, 2012)

“Unconventional gas is changing the energy world. This energy revolution is just

beginning, with the full implications still difficult to discern.”

3

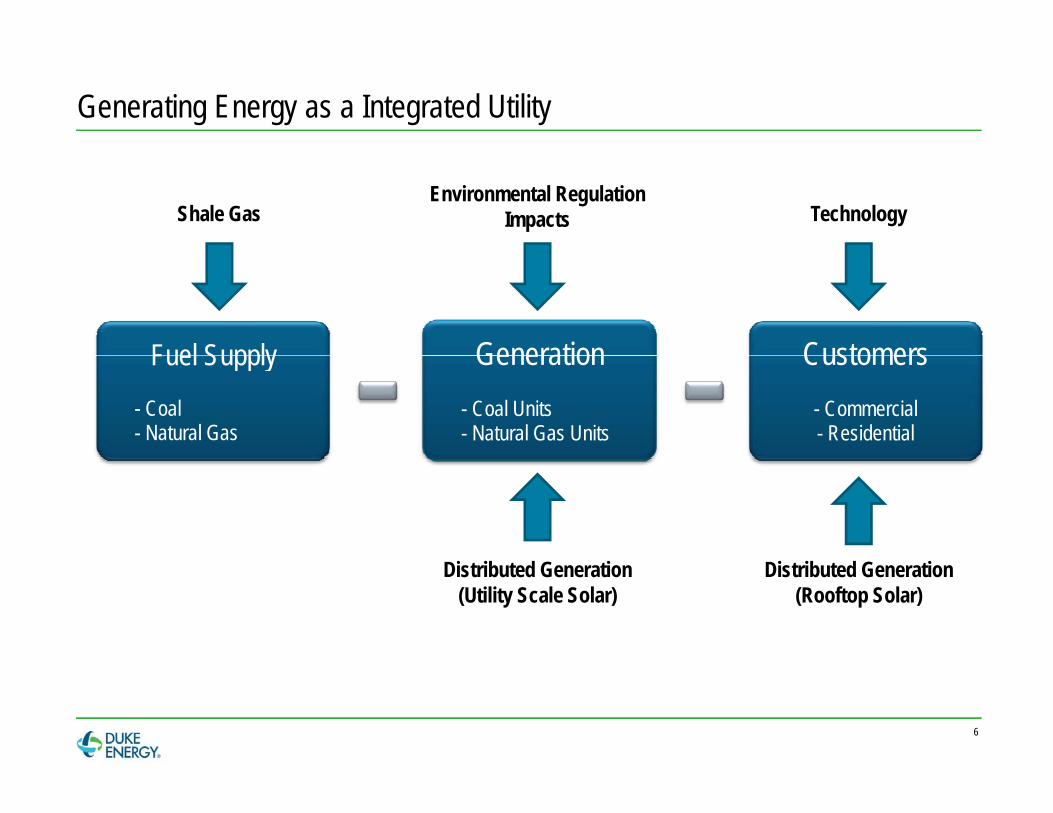

Generating Energy as a Integrated Utility

Environmental Regulation ImpactsShale Gas

Fuel Supply Generation CustomersFuel Supply- Coal - Natural Gas

Generation- Coal Units- Natural Gas Units

Customers- Commercial- Residential

4

Video

Strategic Leadership Training program at Duke Part of the program is the CEO challenge CEO challenge is a six month project Participants are asked to research and propose solutions for a complex problem Participants are asked to research and propose solutions for a complex problem This years challenge asked the following question: What is the business model for Duke Energy to be successful in the future?

5

Generating Energy as a Integrated Utility

TechnologyEnvironmental Regulation

ImpactsShale Gas

Fuel Supply Generation CustomersFuel Supply- Coal - Natural Gas

Generation- Coal Units- Natural Gas Units

Customers- Commercial- Residential

Distributed Generation(Utility Scale Solar)

Distributed Generation(Rooftop Solar)

6

Key Messages

Duke Energy supports cost-effective solar energy and recognize it as an evolution of electric generation. $3 billion already invested by Duke Energy in wind and solar $3 billion already invested by Duke Energy in wind and solar An additional $3 billion commitment in renewable energy PPAs

Distributed generation will co exist with our central station generation portfolio and integrated grid Distributed generation will co-exist with our central station generation portfolio and integrated grid. Energy policy must continue to be updated to prepare for the changing marketplace.

We look forward to working with leaders in our jurisdictions to: We look forward to working with leaders in our jurisdictions to: Make solar policies fair for all customers Encourage the use of solar energy Help us spur the economy Help us spur the economy

7

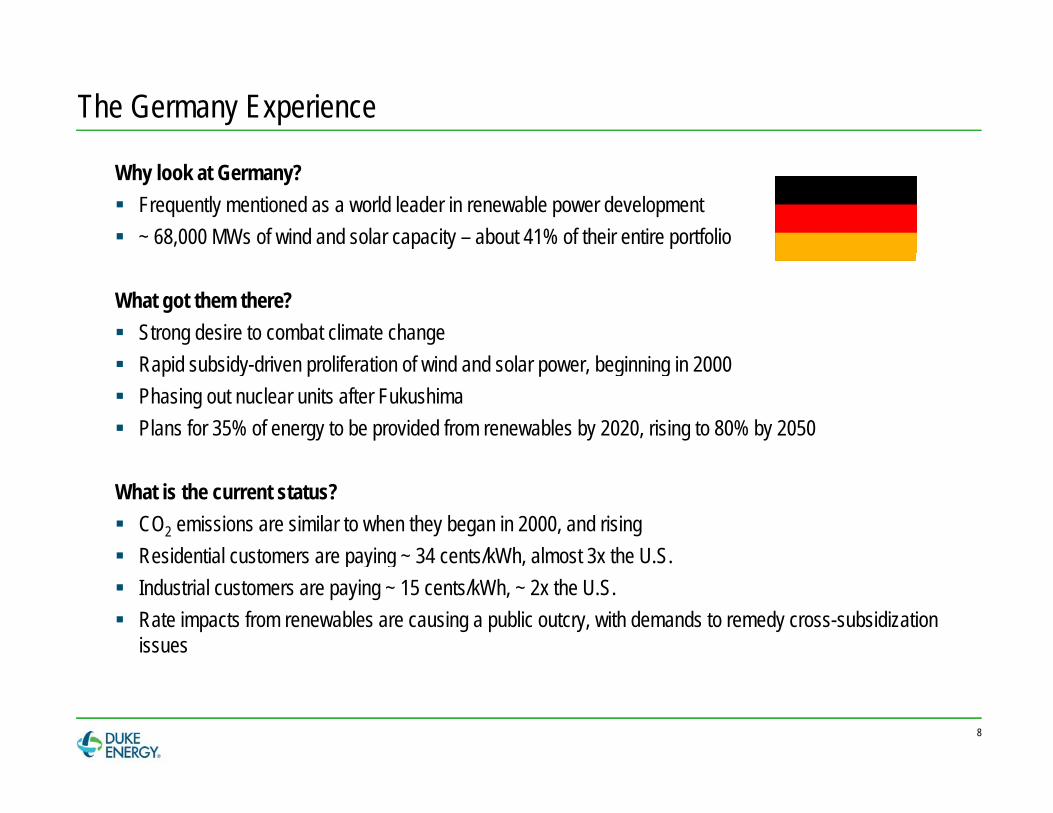

The Germany Experience

Why look at Germany? Frequently mentioned as a world leader in renewable power development ~ 68,000 MWs of wind and solar capacity – about 41% of their entire portfolio

What got them there? Strong desire to combat climate change Rapid subsidy-driven proliferation of wind and solar power, beginning in 2000 Phasing out nuclear units after Fukushima Plans for 35% of energy to be provided from renewables by 2020, rising to 80% by 2050

What is the current status? CO2 emissions are similar to when they began in 2000, and rising Residential customers are paying ~ 34 cents/kWh almost 3x the U SResidential customers are paying 34 cents/kWh, almost 3x the U.S. Industrial customers are paying ~ 15 cents/kWh, ~ 2x the U.S. Rate impacts from renewables are causing a public outcry, with demands to remedy cross-subsidization

issues

8

Drivers: Technology

9.00

Solar Installation Price Trends – Utility Scale

6 00

7.00

8.00

4.00

5.00

6.00

Wac

Inst

alled

2.00

3.00

$/W

-

1.00

2008 2009 2010 2011 2012 2013 P 2014 P 2015 P 2016 P 2017 P 2018 P 2019 P 2020 P

9

Unsubsidized With Federal Tax Credits With Federal & N.C. Tax CreditsUtility Scale

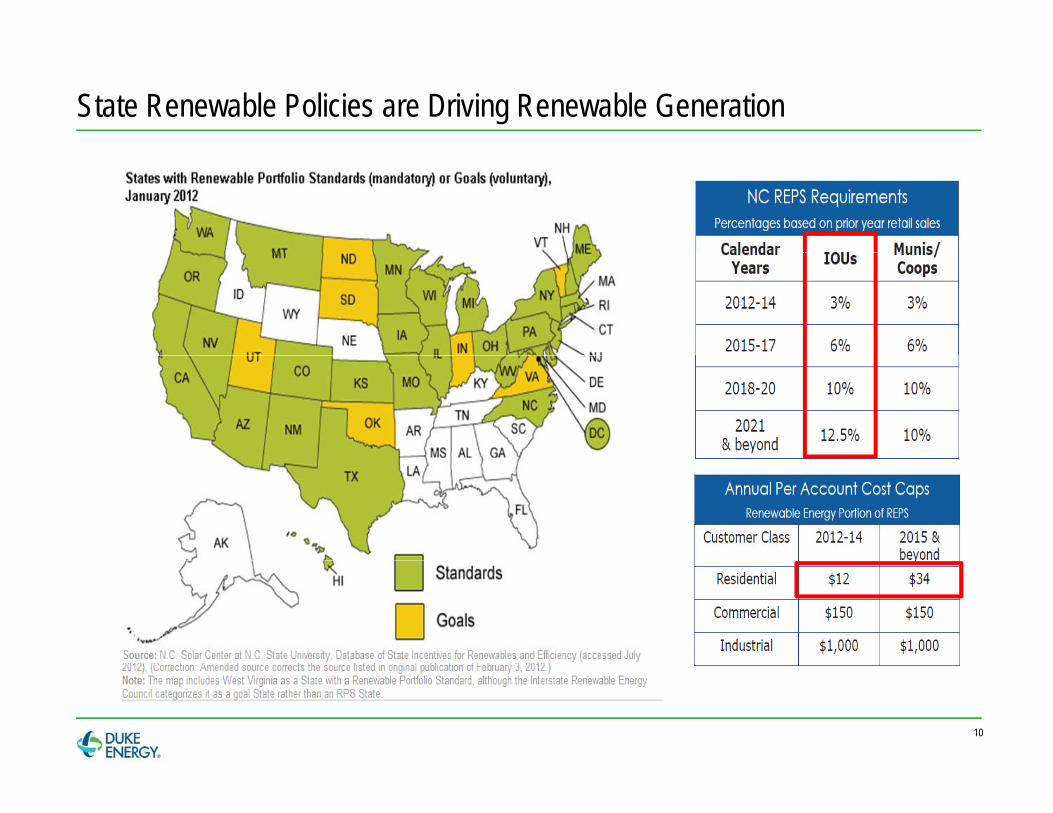

State Renewable Policies are Driving Renewable Generation

10

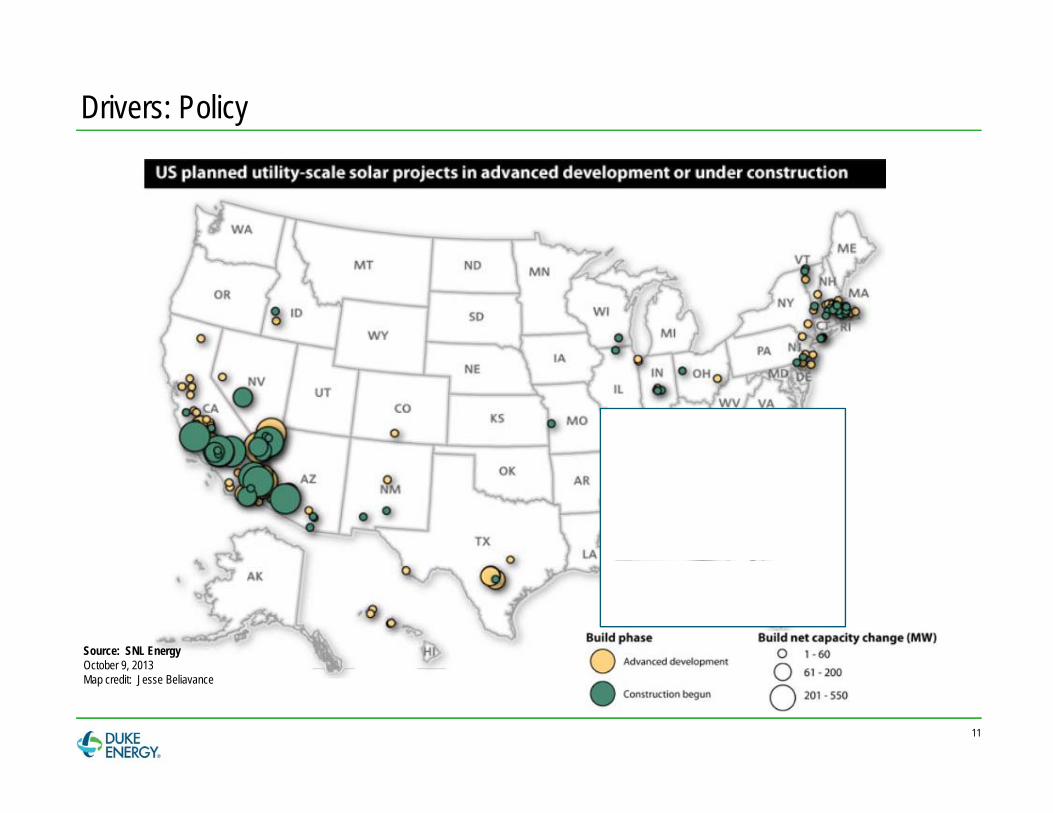

Drivers: Policy

Source: SNL EnergyOctober 9 2013October 9, 2013Map credit: Jesse Beliavance

11

Second Quarter 2013

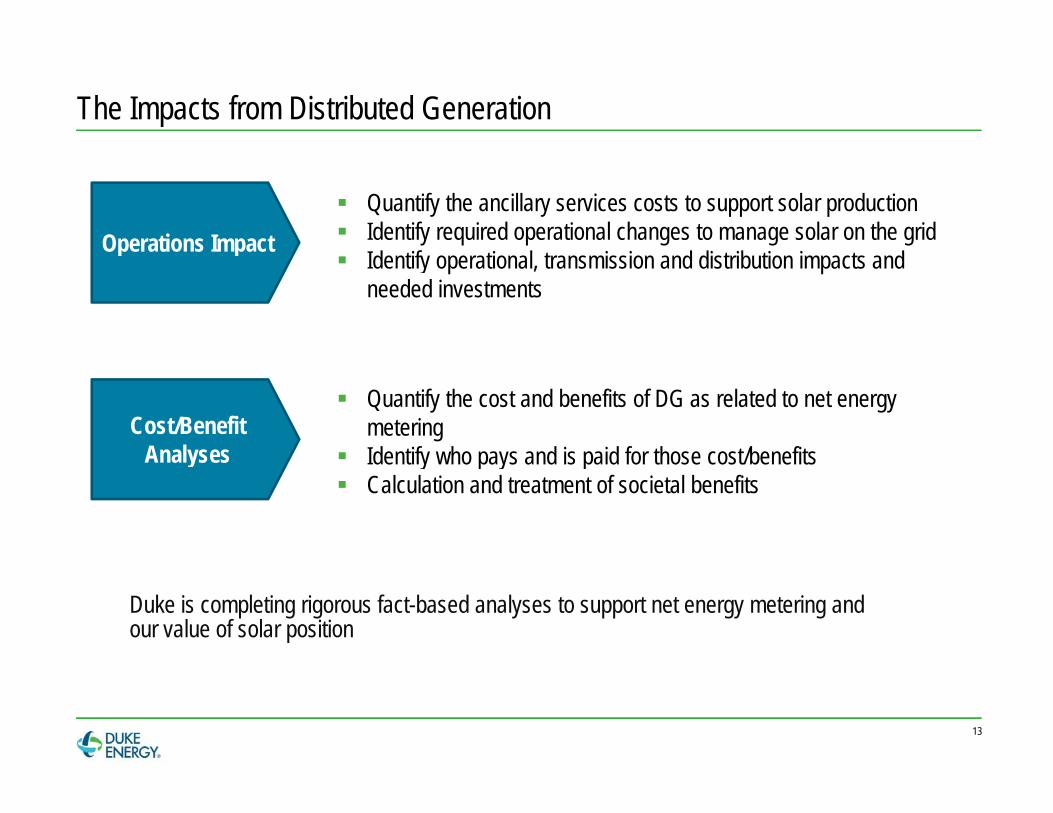

The Impacts from Distributed Generation

Operations Impact Quantify the ancillary services costs to support solar production Identify required operational changes to manage solar on the grid

Id tif ti l t i i d di t ib ti i t d p p

Identify operational, transmission and distribution impacts and needed investments

Cost/Benefit Analyses

Quantify the cost and benefits of DG as related to net energy metering

Identify who pays and is paid for those cost/benefitsAnalyses Identify who pays and is paid for those cost/benefits Calculation and treatment of societal benefits

Duke is completing rigorous fact-based analyses to support net energy metering and our value of solar position

13

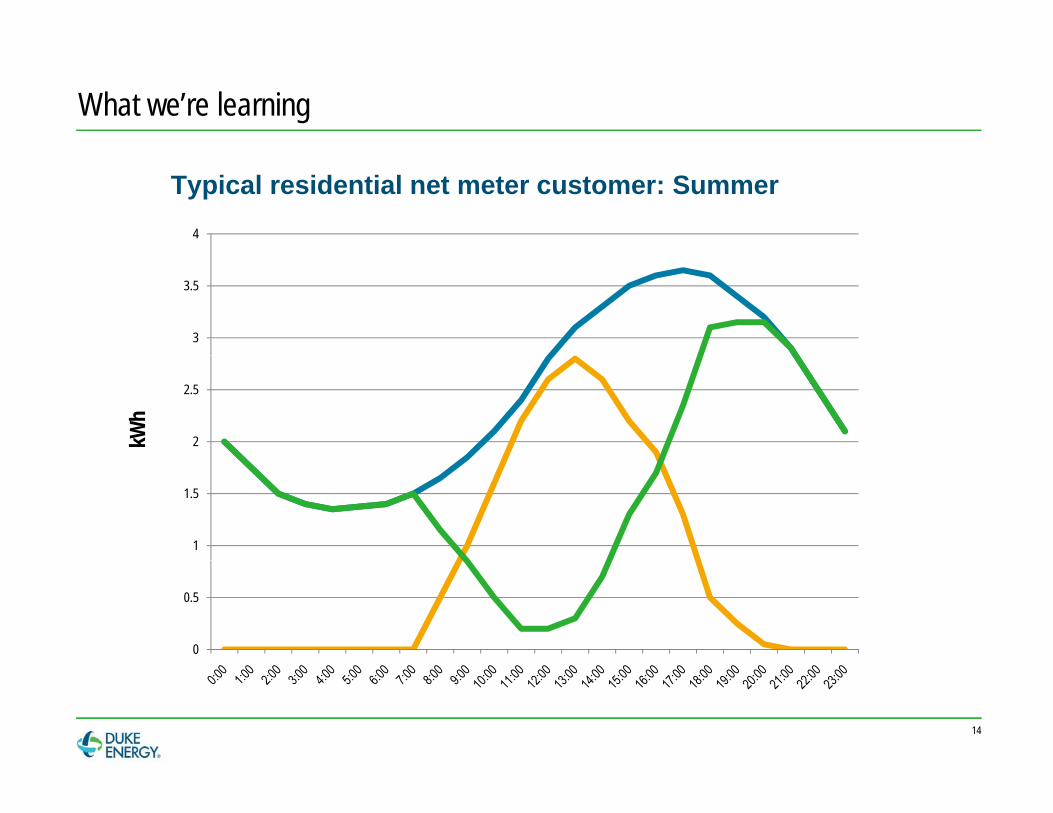

What we’re learning

Typical residential net meter customer: Summer4

3

3.5

2

2.5

kWh

1

1.5

0

0.5

14

What we’re learning

Typical residential net meter customer: Winter4

3

3.5

2

2.5

kWh

1

1.5

0

0.5

15

0

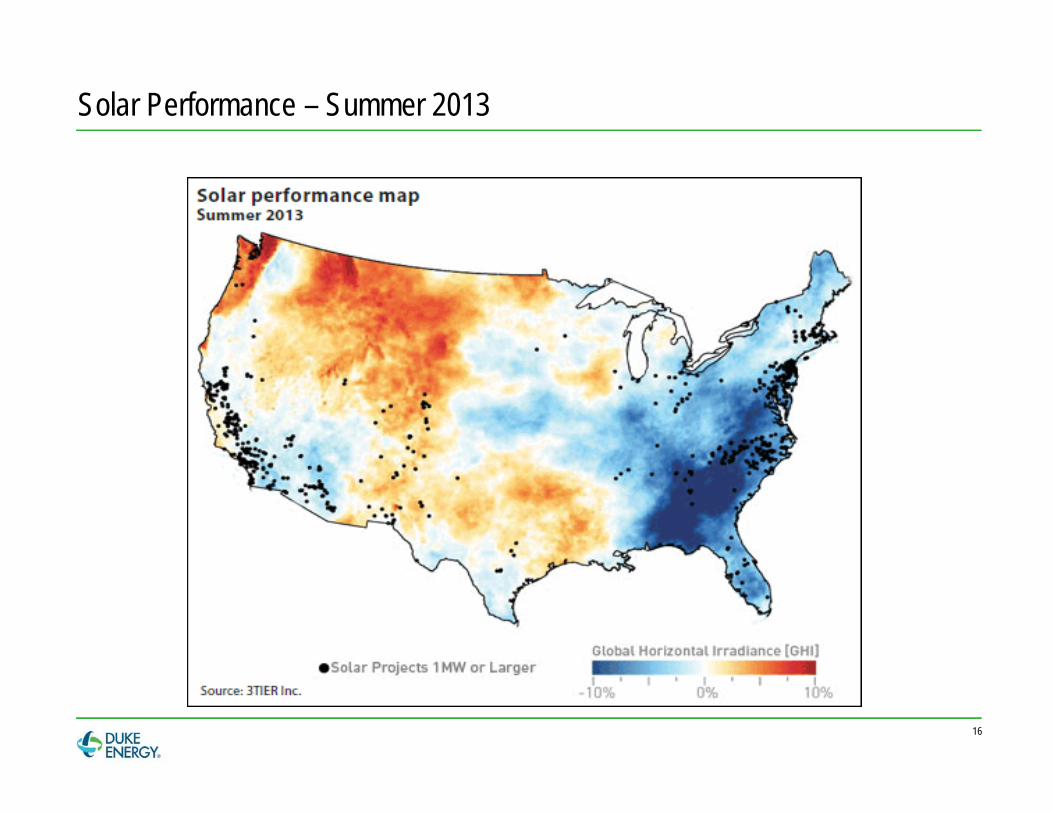

Solar Performance – Summer 2013

16

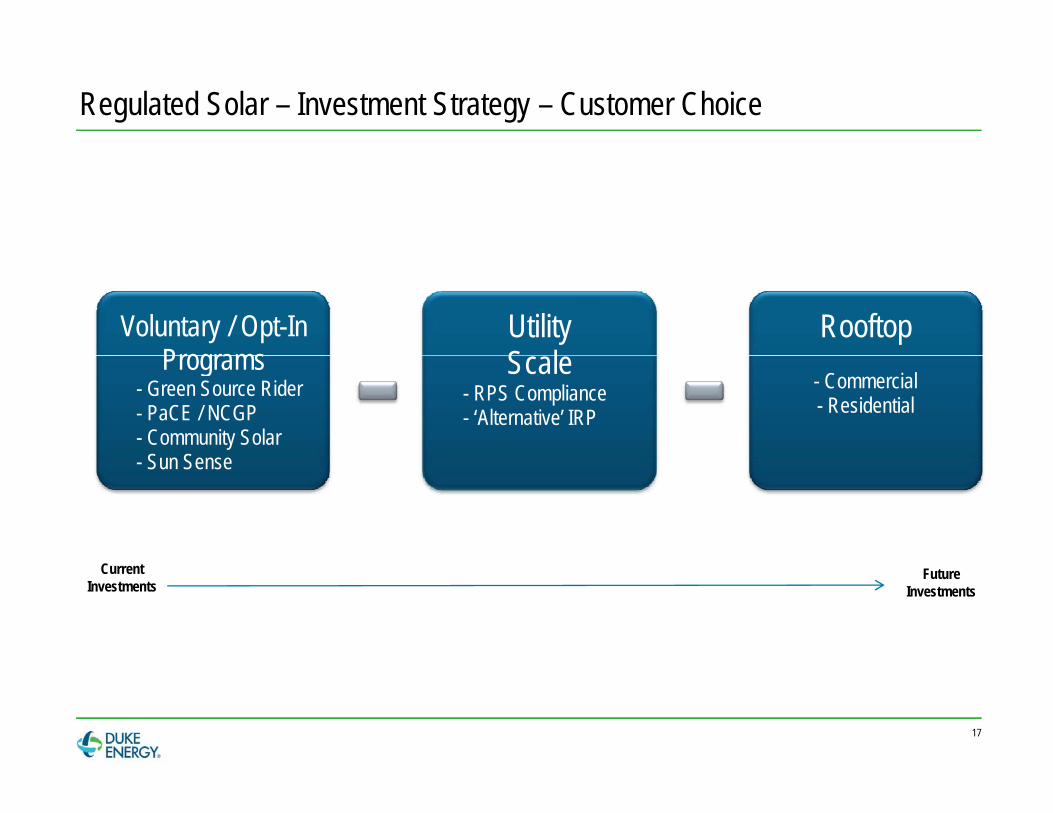

Regulated Solar – Investment Strategy – Customer Choice

Voluntary / Opt-In Programs

Utility S l

RooftopPrograms

- Green Source Rider- PaCE / NCGP - Community Solar

S n Sense

Scale - RPS Compliance- ‘Alternative’ IRP

- Commercial- Residential

- Sun Sense

Current Investments

FutureInvestments

17

Net metering

$ 10/kWh$.10/kWh

$.10/kWh

18

Net Metering Analogy

19

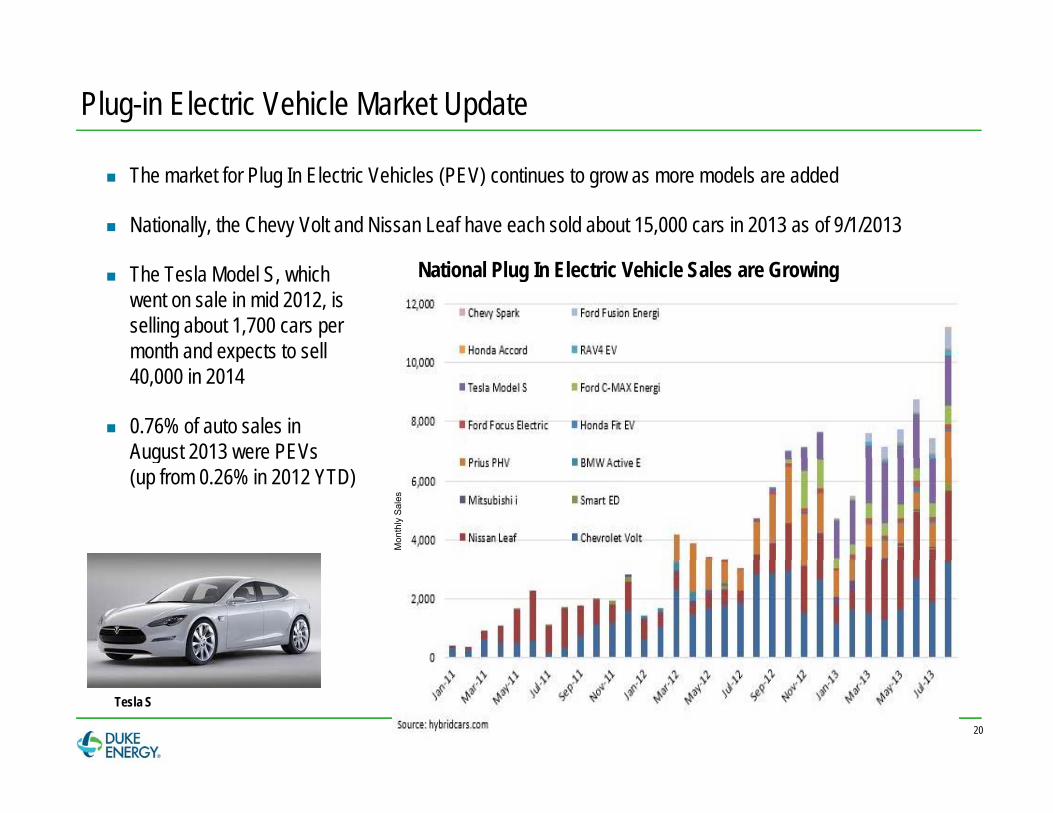

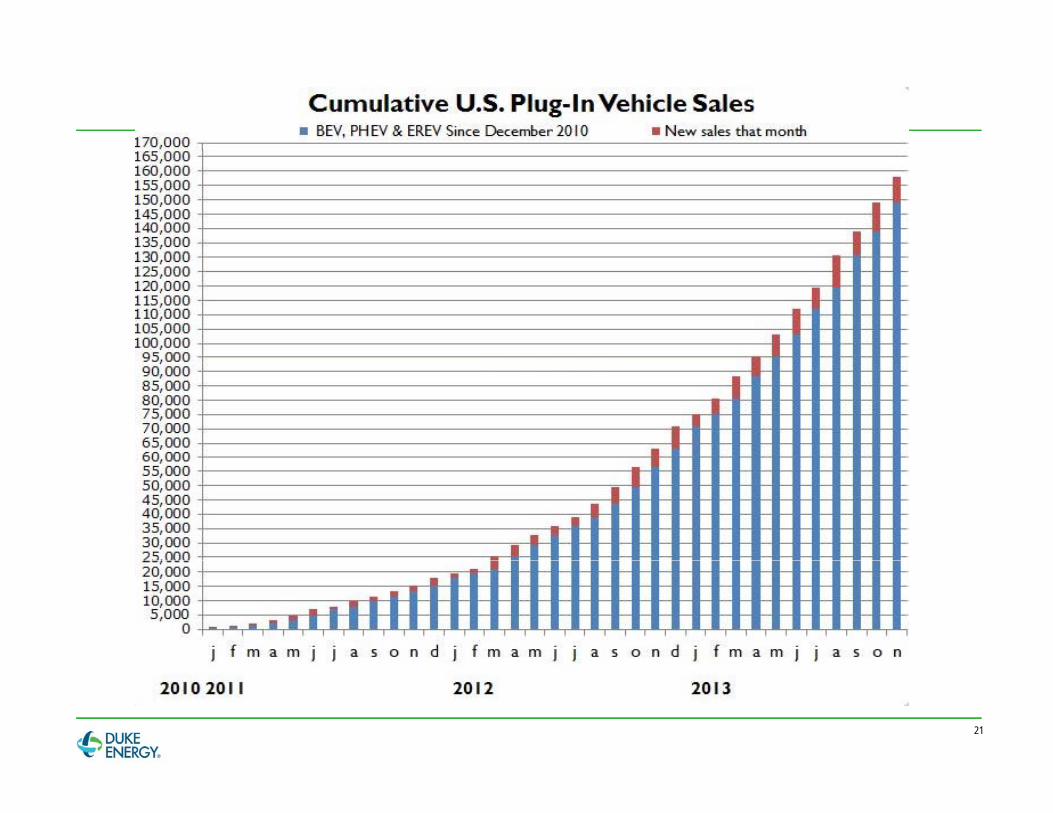

Plug-in Electric Vehicle Market Update

The market for Plug In Electric Vehicles (PEV) continues to grow as more models are added

Nationally, the Chevy Volt and Nissan Leaf have each sold about 15,000 cars in 2013 as of 9/1/2013

The Tesla Model S, whichwent on sale in mid 2012, is selling about 1,700 cars per month and expects to sell

National Plug In Electric Vehicle Sales are Growing

month and expects to sell 40,000 in 2014

0.76% of auto sales in August 2013 were PEVs August 2013 were PEVs (up from 0.26% in 2012 YTD)

Mon

thly

Sal

es

20

Tesla S

21

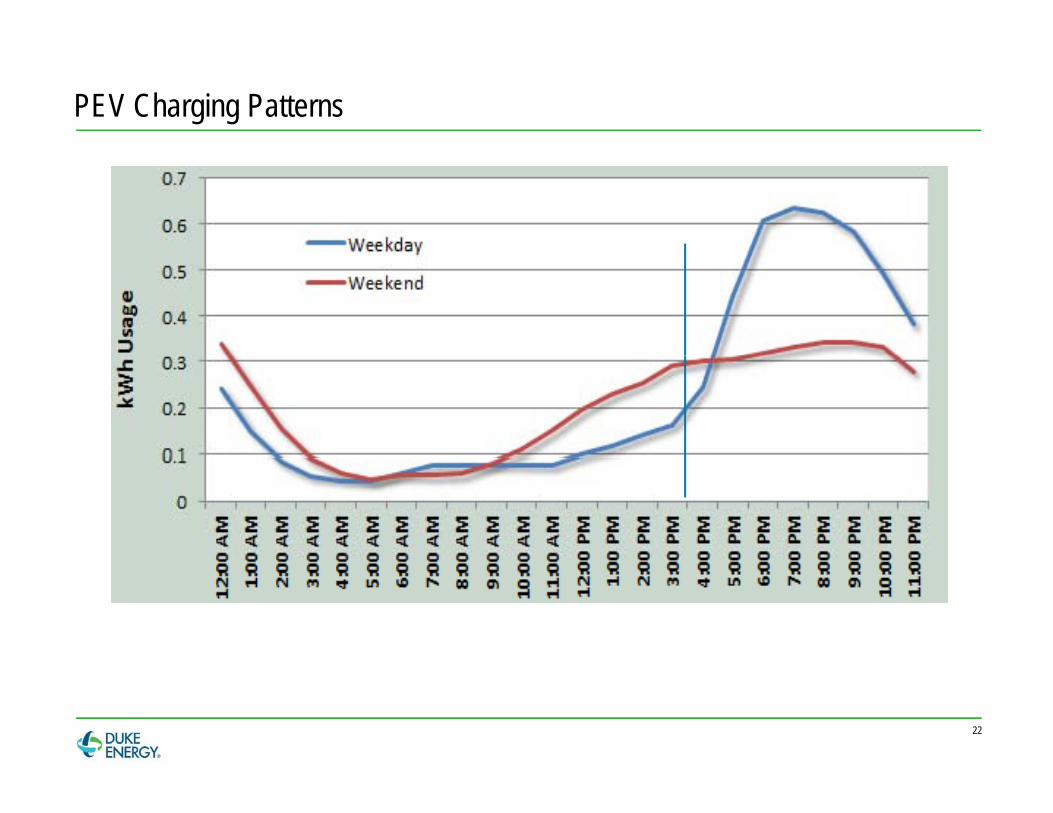

PEV Charging Patterns

22

Technology Adoption Rates Occurring Faster

Rates of Adoption of New Technologies

ds%

of U

.S. H

ouse

hold

23

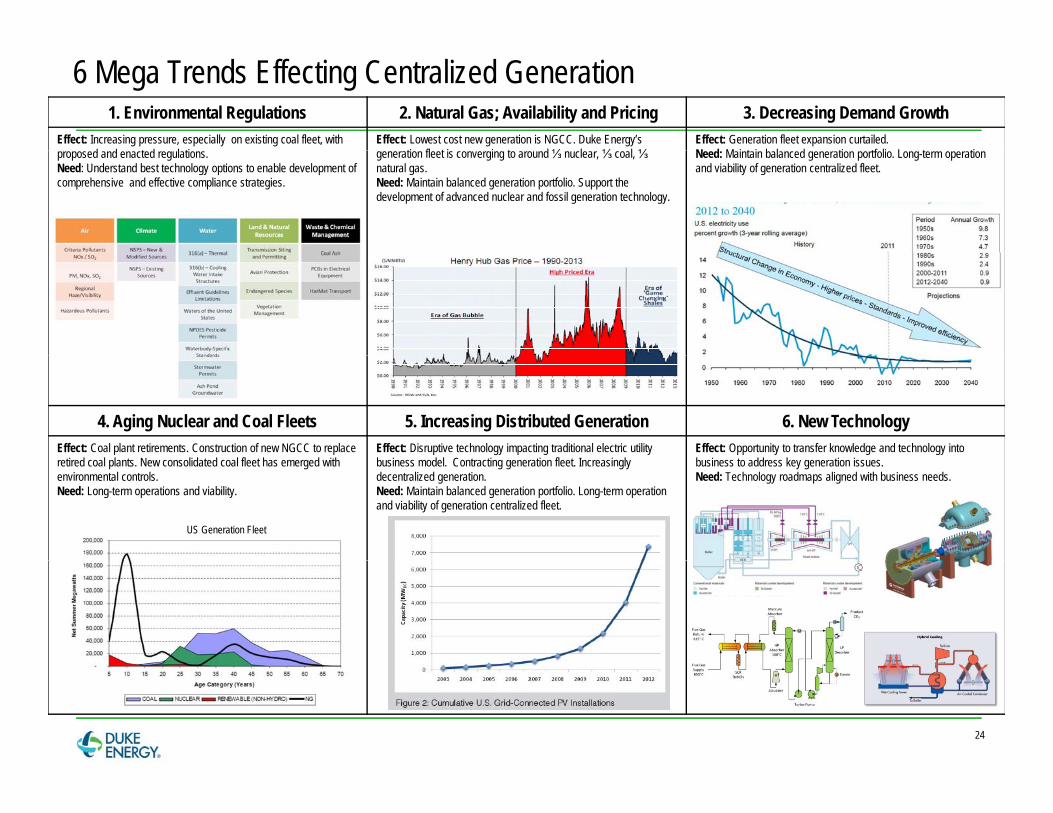

6 Mega Trends Effecting Centralized Generation1. Environmental Regulations 2. Natural Gas; Availability and Pricing 3. Decreasing Demand Growth

Effect: Increasing pressure, especially on existing coal fleet, with d d t d l ti

Effect: Lowest cost new generation is NGCC. Duke Energy’sti fl t i i t d ⅓ l ⅓ l ⅓

Effect: Generation fleet expansion curtailed. N d M i t i b l d ti tf li L t ti proposed and enacted regulations.

Need: Understand best technology options to enable development of comprehensive and effective compliance strategies.

generation fleet is converging to around ⅓ nuclear, ⅓ coal, ⅓natural gas.Need: Maintain balanced generation portfolio. Support the development of advanced nuclear and fossil generation technology.

Need: Maintain balanced generation portfolio. Long-term operation and viability of generation centralized fleet.

4. Aging Nuclear and Coal Fleets 5. Increasing Distributed Generation 6. New TechnologyEffect: Coal plant retirements. Construction of new NGCC to replace

i d l l N lid d l fl h d i h Effect: Disruptive technology impacting traditional electric utility b i d l C i i fl I i l

Effect: Opportunity to transfer knowledge and technology into b i dd k i iretired coal plants. New consolidated coal fleet has emerged with

environmental controls. Need: Long-term operations and viability.

business model. Contracting generation fleet. Increasingly decentralized generation.Need: Maintain balanced generation portfolio. Long-term operation and viability of generation centralized fleet.

business to address key generation issues.Need: Technology roadmaps aligned with business needs.

US Generation Fleet

24

U.S. DOE, Sept. 2013

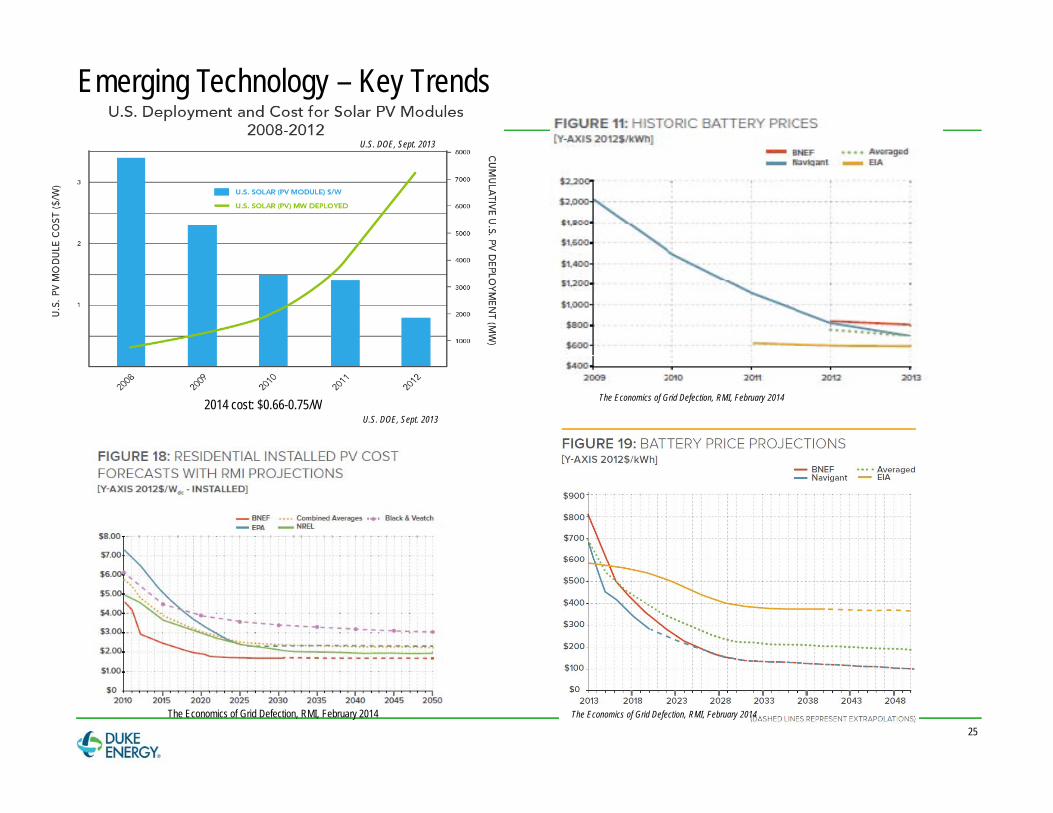

Emerging Technology – Key Trends

The Economics of Grid Defection, RMI, February 2014

U.S. DOE, Sept. 20132014 cost: $0.66-0.75/W

25The Economics of Grid Defection, RMI, February 2014 The Economics of Grid Defection, RMI, February 2014

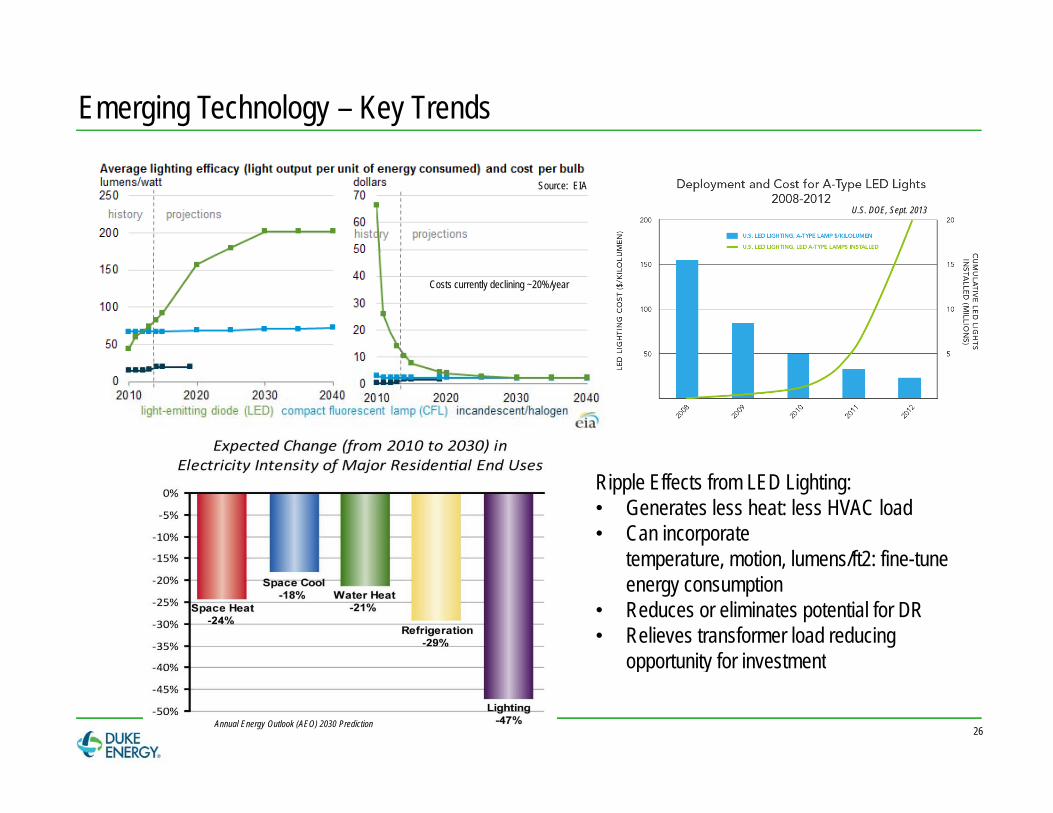

Emerging Technology – Key Trends

Source: EIA

U.S. DOE, Sept. 2013

Costs currently declining ~20%/year

Ripple Effects from LED Lighting:• Generates less heat: less HVAC load• Can incorporate

temperature motion lumens/ft2: fine-tune temperature, motion, lumens/ft2: fine-tune energy consumption

• Reduces or eliminates potential for DR• Relieves transformer load reducing

opportunity for investment

26Annual Energy Outlook (AEO) 2030 Prediction

opportunity for investment

What is the Internet of Things (IOT)?

InternetInternet

Seamless access & data exchange between all connected devices.

27

Hype Curve – Emerging Energy Technology

CO2 Capture & Sequestration

Time to Mainstream Adoption< 2 years 2- 5 years 5 – 10 years > 10 years

Small Modular Nuclear Reactors

Energy Storage (Consumer)

Thermal / Concentrating Solar

Energy Storage (Renewable Integration)

PECT

ATIO

N

Supercritical CO2 Cycles

Small Cells

Load Optimization

Big Data Analytics

Distributed Cybersecurity

Hydrogen Economy

g

Wave Power

Microgrids

Thermal Energy StorageLiquefied Natural Gas

Advanced Cooling TechnologyWater Conservation & Recycling

EXP

Integrated Gasification Fuel Cell (IGFC)

Open-Source Software

Condition-Based Maintenance

LV SST

Message Bus ProtocolsHigh-Temperature Superconductivity

Photovoltaic Generation

Tidal Power

Distributed Generation

Integrated Gasification Combined Cycle (IGCC)

Biomass Electricity GenerationVehicle-to-Grid

Energy Harvesting

Wind Generation

Municipal Waste-Derived Fuel Co-firingMV SST

g

Wireless Line Sensor

AMI IEDs

Fuel Cells

Energy Storage (UPS / Power Quality)

Combined Heat and Power

Energy Storage (Grid Support)

Geothermal Power Generation PEVs CO2 Utilization (algae-to-fuels)

Distributed Capacitor

MV PLC

IoT

OT/IT Network Management

CIM-driven StandardsPMU

HYPE CURVE Technology Trigger Peak of Inflated Expectations Trough of Disillusionment Slope of Enlightenment Plateau of

Productivity

EMERGING TECHNOLOGY Technology Screening Monitor / Development / Field Testing Technology

HYPE CURVE Technology Trigger Peak of Inflated Expectations Trough of Disillusionment Slope of Enlightenment Plateau of

Productivity

EMERGING TECHNOLOGY Technology Screening Monitor / Development / Field Testing Technology

TIME

MV PLC

TECHNOLOGY ACTION

Technology Screening Assess Initial Testing Field Testing TransferTECHNOLOGY ACTION

Technology Screening Assess Initial Testing Field Testing Transfer

28

Emerging Technology – Priority AssessmentYEARS TO MAINSTREAM ADOPTIONYEARS TO MAINSTREAM ADOPTION

< 2 years 2 – 5 years 5 – 10 years > 10 years

2014 - 2015 2016 - 2019 2020 - 2024 2024 -

EPRI Management / Technology Innovation and Partnerships

l Fuel Cells ❶❷❸ Small Modular Nuclear Reactors ❶

Tran

sfor

mat

iona

Photovoltaic Generation ❶❷❸❹Liquefied Natural Gas ❶

Small Modular Nuclear Reactors (Outside US) ❶Distributed Cybersecurity ❶

❶❷❸Energy Storage (Consumer)❶❷❸Distributed Generation ❶❷Low Voltage Solid State Transformer (LV SST) ❶❷Load Optimization ❶Distributed Cybersecurity ❶

❶Subcritical CO2 Cycles ❶Hydrogen EconomyHigh-Temperature SuperconductivityEnergy Harvesting ❶Medium Voltage Solid State Transformer (MV SST) ❶

Energy Storage (Central Generation) ❶

MPAC

THi

gh Ultra-Supercritical Coal (Outside US)❶Energy Storage (UPS / Power Quality) ❶❷❸

Advanced Sensors and Controls ❶❷❸❹Energy Storage (Grid Support) ❶❷❸Combined Heat and Power ❶CIM-Driven Standards❶❷❸Internet-of-Things (IoT) ❶❷

❶Energy Storage (Renewable Integration) ❶❷❸Integrated Gasification Combined Cycle (IGCC) ❶❹Ultra-Supercritical Coal ❶Advanced Combined Cycle ❶PEVs ❶❷❸❹Big Data Analytics ❶Message Bus Protocols ❶❷

CO2 Capture & Sequestration ❶Integrated Gasification Fuel Cell (IGFC) ❶Vehicle-to-Grid ❶Open-Source Software ❶

POTE

NTIA

L IM Medium Voltage Power Line Communications ❶❷

oder

ate On-Shore Wind Generation ❹

Sensors and Controls ❹Intelligent Electrical Devices❹

CO2 utilization (algae-to-fuels)❶❷❸OT/IT Network Management ❶❷❸

Water Conservation & Recycling ❶❷Advanced Cooling Technology ❶❷Biomass Electricity Generation ❶Off-Shore Wind Generation ❶Thermal Energy Storage ❶Thermal / Concentrating Solar ❶S ll C ll ❶Mo

g ❹AMI ❹

g ❶❷❸ Small Cells ❶Ubiquitous Condition-Based Maintenance ❶Emissions Monitoring ❶❷Ubiquitous Phasor Measurement Units ❶❷❸Microgrids ❶❷❸

w

Geothermal Power GenerationTidal Power

Emerging Technology Action❶ Monitor / Assess

29

Low Municipal Waste-Derived Fuel Co-firing ❶❷❸ Wireless Line Sensor ❶❷❸ Tidal Power

Wave PowerDistributed Capacitance ❶❷

❷ Development / Initial Testing❸ Field Testing❹ Technology Transfer

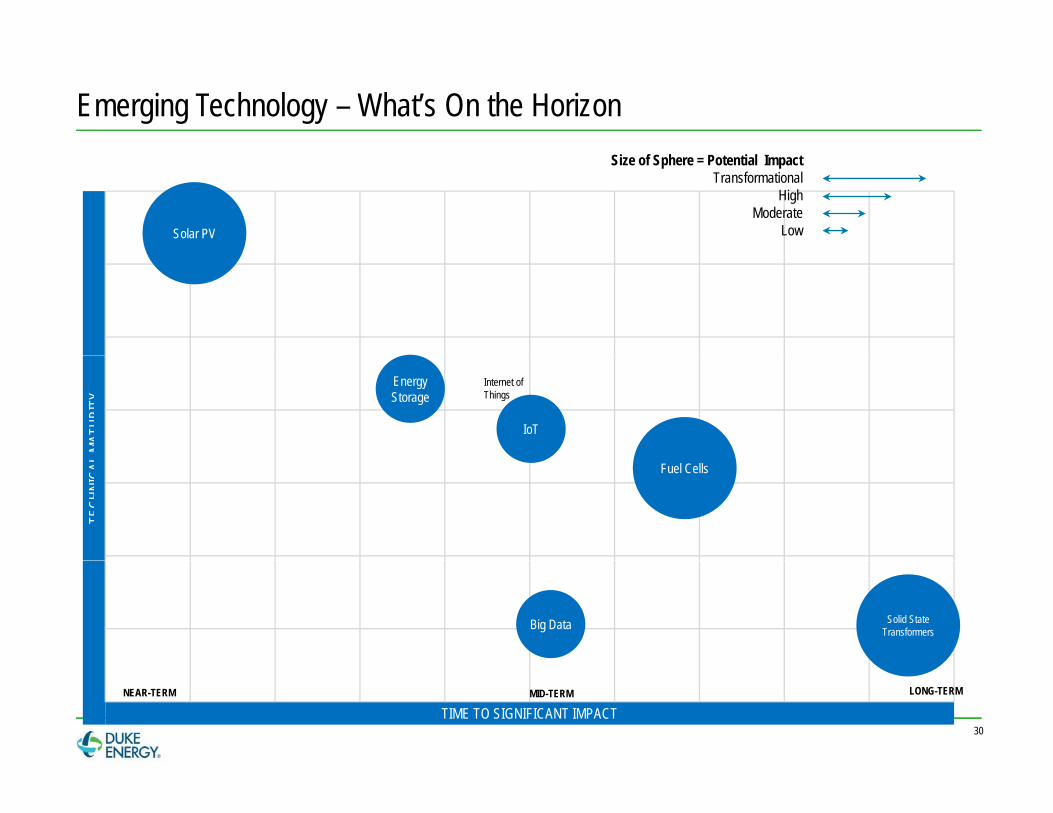

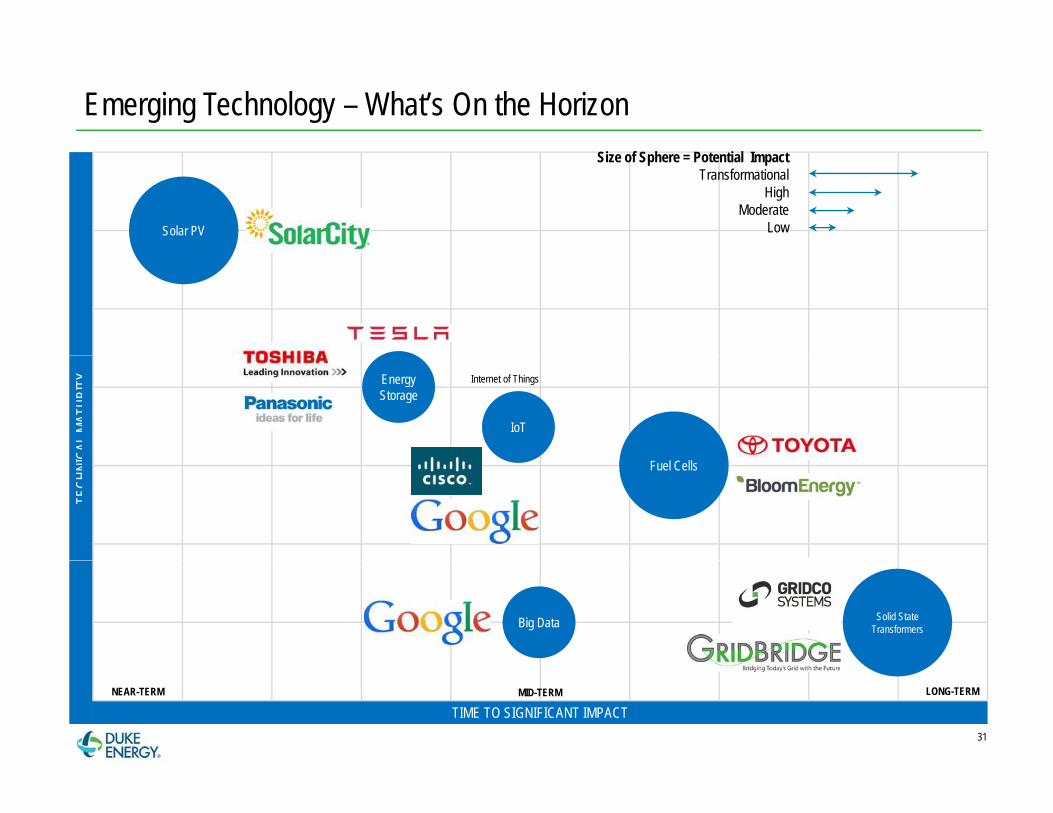

Emerging Technology – What’s On the Horizon

Solar PV

Size of Sphere = Potential ImpactTransformational

HighModerate

Low

L MAT

URIT

Y

IoT

Internet of Things

Energy Storage

TECH

NICA

L

Fuel Cells

Solid State TransformersBig Data

30TIME TO SIGNIFICANT IMPACT

NEAR-TERM LONG-TERMMID-TERM

Emerging Technology – What’s On the Horizon

Solar PV

Size of Sphere = Potential ImpactTransformational

HighModerate

Low

CAL M

ATUR

ITY

IoT

Internet of ThingsEnergy Storage

TECH

NIC

Fuel Cells

Solid State TransformersBig Data

31

TIME TO SIGNIFICANT IMPACTNEAR-TERM LONG-TERMMID-TERM

Opportunities in the New Energy Value Chain

Bulk generation Grid-scale storage

OTHER RENEWABLES FLYWHEEL BATTERYCOMPRESSED

AIRCOAL

WIND Coal

SOLARNew energy mix

GASPUMPED HYDRO

AIR

CCS

Transmission grid

L l di t ib ti id S t b ildi d h

Interconnection to super-grid

Micro-grid

Smart gridsSMART

TRANSMISSIONSMART

TRANSMISSION

Local distribution grid Smart building and home

DISTRIBUTED Multi-way flows &

PLUG-IN EV

ENERGY

SMART HVAC

SMART APPLIANCES

SMARTMICRO

SMART DISTRIBUTION

ENERGY

DISTRIBUTED STORAGE

+ - HEAT PUMPS &DISTRICT HEATING

Multi-way flows &distributed resources

Active demandside

SMART METER

MANAGEMENTSYSTEM

SMART CHARGING

ON-SITE STORAGE

MICRO-GENERATION

32

Source: Bloomberg New Energy Finance

Key Takeaways

1. Rate of technology development and adoption is accelerating.2. What happened with solar is happening with other technologies.3. Non-traditional players aggressively entering the electricity space.4. Central Generation is experiencing additional pressure.5. Internet of Things (IoT) is a key enabling technology development.g ( ) y g gy p6. Uncertainty is likely to remain with environmental and energy policy, natural gas

outlook and electricity demand.

Centralized Generation is now expected to experience decline due to Centralized Generation is now expected to experience decline due to decreasing demand growth and increasing distributed generation.

33

How Can We Operate Within This “Game Changer”

How do changing markets change procurement activities

Coal volumes are down and future coal burn projections volatileCoal volumes are down and future coal burn projections volatile

How should we buy coal? More spot purchases? Call options or put options?

V l ti i t t ? O ti f diff t i ? Volume options in contracts? Options for different regions?

How should transportation contracts be structured? Fixed? Variable?

How should contracts be priced? Fixed? Index? How can escalators be hedged?

How to create value by for centralized generation by providing flexibility

that other fuel types can not

34

The “Game Changer” is Happening

What role will Duke Energy and us play five years from now in all of this? years from now in all of this?

35