Money Never Sleeps Presentation to the Government Investment Officers Association

David Hendler

Head of U.S. Financial Services

2

CreditSights - Fundamental Research

Topical, Strategic, Sector and Company credit research on unsecured bonds, secured bonds, CDS, loans, hybrid securities, and select equities of the major companies in the U.S. and Europe. A newly established research team in Asia is expanding our research coverage in the Asia-Pacific region.

Benefits Independence/Investor pays model

Timely

Quality of research

Unique insight

Focus/Time

Third party verification

Cost

3

CreditSights - Coverage

75 analysts covering 40 industries across 7 broadly defined sectors, plus U.S., European & Asian Credit Strategy

700 companies in core coverage, 1,400 companies with written research

US 495 Companies

European/Asian 205 Companies

High Grade 459 Companies

High Yield 241 Companies

55 Industry Outlooks to be published in early 2011

4

CreditSights - Customers

950 Institutions and 6,000 people

Mutual Funds

Insurance Companies

Investment Advisors

Hedge Funds

Dealers/Banks

Pension Funds

Government Sponsored Entities

Government Regulators

Corporations

5

Policy Time Table Update: 2011

• Financial Stability and Bank Capital Regime> Dodd-Frank Wall Street Reform/Consumer Protection Act (July ’10)

Regulatory interpretations and studies Phase-ins and follow-up regs Fed’s SCAP-2 for dividends & buybacks

> BIS III and IMF Global Financial Stability Study (August ’10) New/higher capital standards/global coordination Loss absorbency regime – write-downs/conversions/bail-ins Huge global infrastructure overlay on top of market mechanisms

• U.S. Mortgage Market Dynamics> Reforming America’s Housing Finance Market (February ‘11)

GSEs est. losses from $200B to $400B Enhanced HAMP released by Obama Administration (March ‘10) Proposed Global Servicing Settlement (Fed and State AGs)

Questions on legality/fairness/loss distribution between 1st and 2nd liens ($20B?)

Republican pushback in favor of banks

6

Dodd-Frank Wall Street Reform & Consumer Protection Act

• Revamps Twin Engines of Financial Growth Over Last 30 Years> Consumer lending business> Capital markets & financial innovation/engineering

• Restricts 3Ls: Leverage, Level 2s, Level 3s• Protects consumer borrower rights • Protects tax payers/gov’t interests, prohibits TBTF funding• Unleashes host of potential unintended consequences

> Restrictive economic/loan impacts> Credit reallocation amongst consumer/commercial spheres> Securitization market impacts> Restricts U.S. financial services global competitiveness> Banks Adaptation/Repositioning

• Congressional Republican pushback across various rulings

7

Dodd-Frank Act Deficiencies

• Credit underwriting: under emphasized, over reliance on capital/liquidity protections

• Automated credit scoring: esp. FICO scores as contributing factor to poor credit underwriting procedures

• Risk management: still needs to be empowered, improvement of credit procedures

• Public-Private Partnership: no formalized forum to debate boundaries of risk & return

8

Key Provision Comments

Fin. Stability Oversight Council (FSOC) Monitors systemic trends; sets stricter capital/liquidity rules

Orderly Liquidation AuthorityFDIC unw inds failing BHC/NBFCs*; Tsy absorbs upfront costs; after-the-fact assessment on BHCs >$50 B, other NBFCs

Consumer Financial Protection Bureau w ithin Fed: ow n budget and director

Proprietary Trading (Volcker Rule) Phase-in prop. trading ban; carve-out: 3% of capital in PE or HF

Derivatives Activities (Lincoln Amend.)IR sw aps and some CDS remain in bank; energy, metals, and ag. commodities move to sep. cap. aff iliates

Capital Regime (Collins Amend.) Tier 1 cap: phase-out Trups over 3 years, beginning in 2013

Banking Regulators OCC oversees savings banks; OTS activities eliminated

Securitizations 5% risk retention; carve-outs for low -risk mortgages

Debit Interchange (Durbin Amend.) Fed sets "reasonable/proportional" debit fees, proposed $0.12 cap

Dodd-Frank Act – Highlights

Source: U.S. government, CreditSights*NBFCs = Non-Bank Financial Companies

9

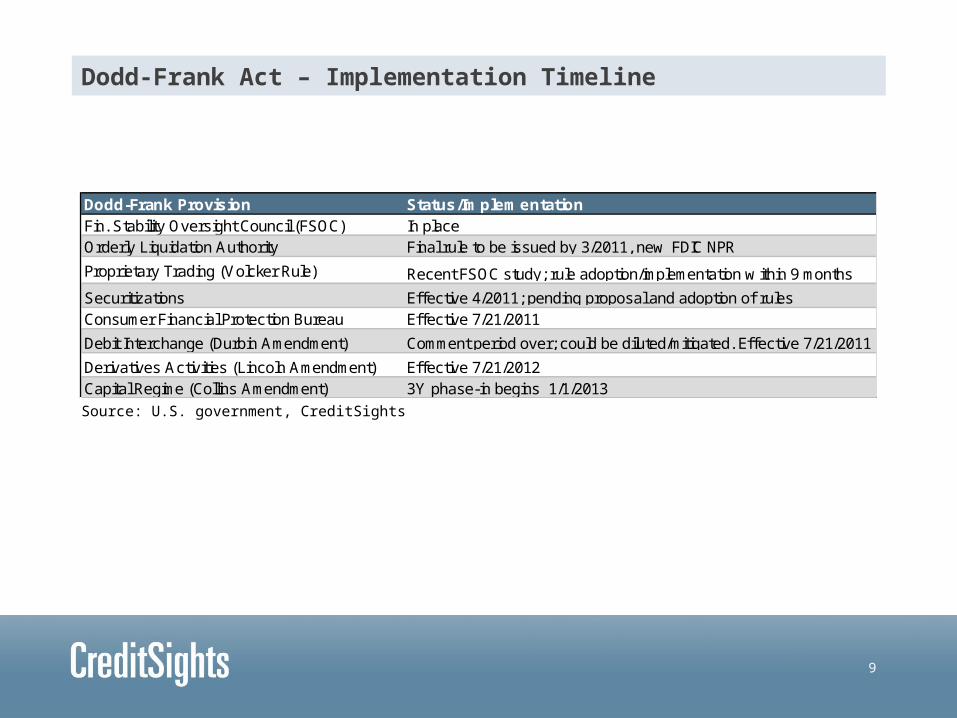

Dodd-Frank Act – Implementation Timeline

Source: U.S. government, CreditSights

Dodd-Frank Provision Status/ImplementationFin. Stability Oversight Council (FSOC) In placeOrderly Liquidation Authority Final rule to be issued by 3/2011, new FDIC NPR

Proprietary Trading (Volcker Rule) Recent FSOC study; rule adoption/implementation w ithin 9 months

Securitizations Effective 4/2011; pending proposal and adoption of rulesConsumer Financial Protection Bureau Effective 7/21/2011

Debit Interchange (Durbin Amendment) Comment period over; could be diluted/mitigated. Effective 7/21/2011

Derivatives Activities (Lincoln Amendment) Effective 7/21/2012Capital Regime (Collins Amendment) 3Y phase-in begins 1/1/2013

10

BIS III Capital StandardsCommon Equity Tier 1 Capital Total Capital

Minimum 4.5% 6.0% 8.0%Conservation Buffer 2.5% 2.5% 2.5%Minimum + Buffer 7.0% 8.5% 10.5%Countercyclical Buffer TBD TBD TBD

BIS III Capital Standards

Source: Basel Committee on Banking Supervision, CreditSights

11

BIS III Phase-in Schedule

Source: Company reports, CreditSights*Range of 0% - 2.5%. Consists of common equity or other fully loss absorbing capital, to be implemented on adiscretionary basis by local regulators when deemed that excess credit growth is resulting in a system-wide build-up of risk** Instruments that no longer qualify as non-common Tier 1 or Tier 2 capital will be phased out over a 10 year period, 1/1/13Cons. = conservation

BIS III - Phase-in Schedule2011 2012 2013 2014 2015 2016 2017 2018 2019

Min. Tier 1 Common - - 3.50% 4.00% 4.50% 4.50% 4.50% 4.50% 4.50%Conservation Buffer - - - - - 0.625% 1.25% 1.875% 2.50%Min. Tier 1 Common + Cons. Buffer - - 3.50% 4.00% 4.50% 5.125% 5.75% 6.375% 7.00%Min. Tier 1 Capital - - 4.50% 5.50% 6.00% 6.00% 6.00% 6.00% 6.00%Min. Tier 1 Capital + Cons. Buffer - - 4.50% 5.50% 6.00% 6.625% 7.25% 7.875% 8.50%Min. Total Capital - - 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00%Min. Total Capital + Cons. Buffer - - 8.00% 8.00% 8.00% 8.625% 9.25% 9.875% 10.50%Countercyclical Buffer* - -Deductions from Tier 1 Common - - - 20.00% 40.00% 60.00% 80.00% 100.00% 100.00%Recognition of capital instruments** - - 90.00% 80.00% 70.00% 60.00% 50.00% 40.00% 30.00%

Leverage ratioFinal

Adjust.Liquidity coverage ratioNet stable funding ratio Observation Period Minimum Standard

Supervisory Monitoring

Parallel run Disclosure starts Jan 1st, 2015

Pillar 1 migration

Observation Period Minimum Standard

12

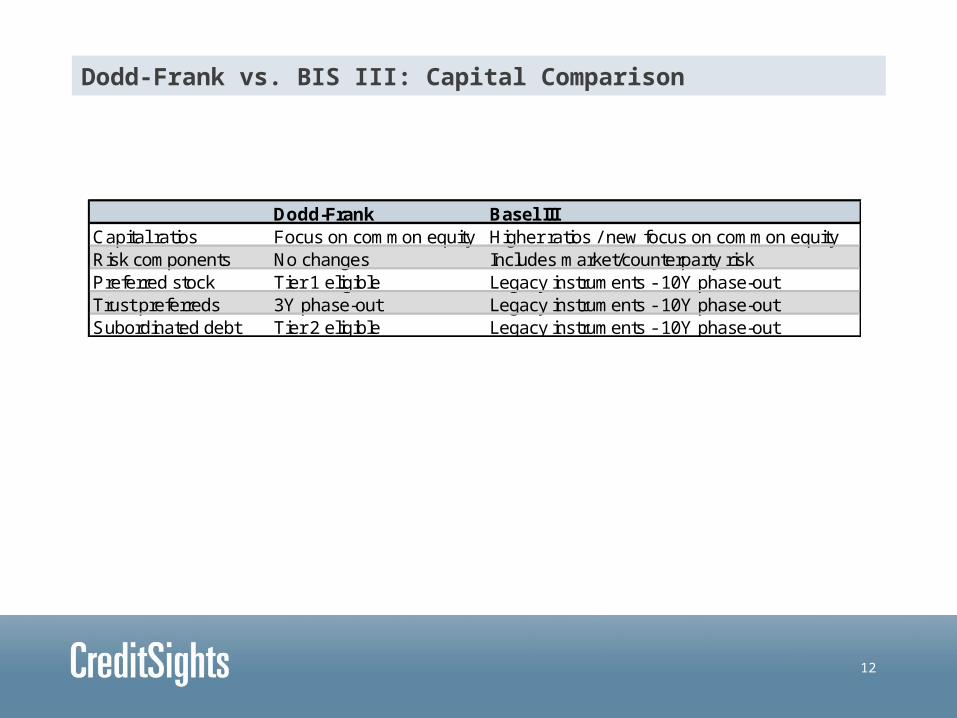

Dodd-Frank Basel IIICapital ratios Focus on common equity Higher ratios / new focus on common equityRisk components No changes Includes market/counterparty riskPreferred stock Tier 1 eligible Legacy instruments - 10Y phase-outTrust preferreds 3Y phase-out Legacy instruments - 10Y phase-outSubordinated debt Tier 2 eligible Legacy instruments - 10Y phase-out

Dodd-Frank vs. BIS III: Capital Comparison

13

0%

10%

20%

30%

40%

50%

60%G

S

MS

NT

RS

BK

ST

T C

BA

C

JP

M

KE

Y

RF

PN

C

FH

N

US

B

CO

F

CM

A

MI

ST

I

ZIO

N

WF

C

AX

P

FIT

B

HB

AN

BB

T

MT

B

U.S. Banks: Liquid Asset Ratio

Source: FFIEC, SNL, CreditSightsAs of 4Q10. Green = Strong, Orange = Borderline, Red = Weak. Bar represents median = 18%Liquid asset ratio: (cash & equivalents + securities + Fed funds & repos + trading account – pledged securities) / total assets

14

Orderly Liquidation Authority: Hope or Hostage?

• Key Takeaway: taxpayer bailout prohibited; capital structure vulnerable

• BIS proposals differ as public monies still available, broader loss sharing to subordinated debt, possibly to senior debt

• Harmonizing global regulation – BIS 3 gravitating to Dodd-Frank

• Investment bank "bail-in" plans now part of BIS proposals

• Market Discipline: priority of claims, bridge banks, loss assessments

15

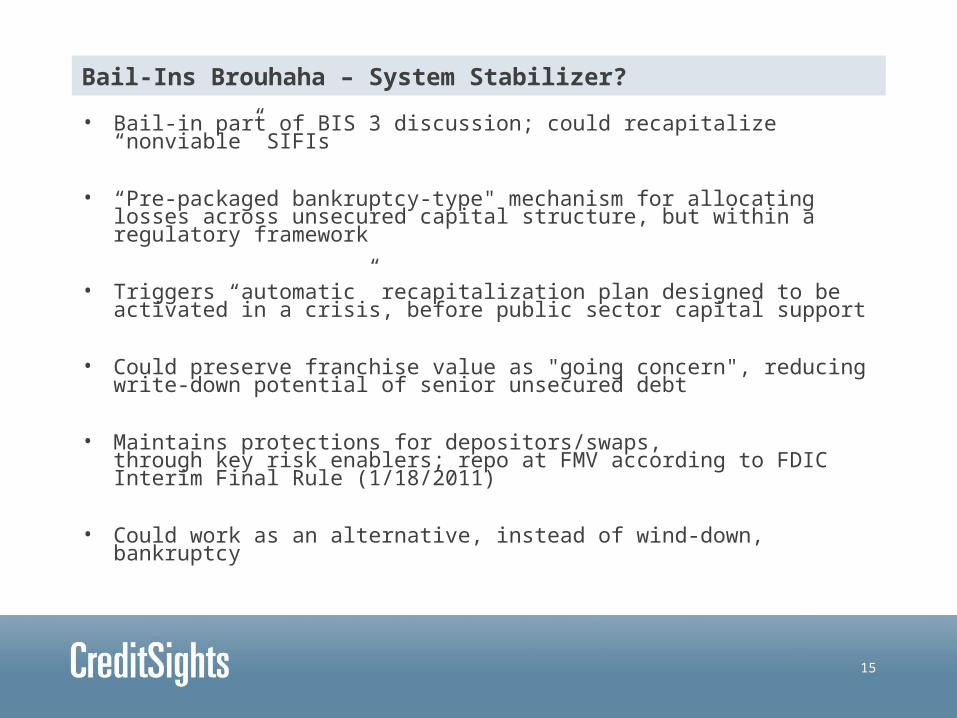

• Bail-in part of BIS 3 discussion; could recapitalize “nonviable” SIFIs

• “Pre-packaged bankruptcy-type" mechanism for allocating losses across unsecured capital structure, but within a regulatory framework

• Triggers “automatic” recapitalization plan designed to be activated in a crisis, before public sector capital support

• Could preserve franchise value as "going concern", reducing write-down potential of senior unsecured debt

• Maintains protections for depositors/swaps, through key risk enablers; repo at FMV according to FDIC Interim Final Rule (1/18/2011)

• Could work as an alternative, instead of wind-down, bankruptcy

Bail-Ins Brouhaha – System Stabilizer?

16

Bail-Ins Brouhaha – System Stabilizer?

For Regulators: Enforces market

discipline with capital structure at risk of

loss upfront; minimizes systemic

risk and political fallout

For Banks: Maintains access

to regulatory capital which has been stymied by credit crisis and

investor confusion on bank

resolutions; could increase cost of

capital

For Investors: More transparent and uniform structures and bond covenants and

triggers; still may raise return hurdles and/or

exclude participation by traditional fixed income

investors - the regulatory desired

investor class

For Investment Bankers: Innovative compromise

solution; preserves largest sector for debt deal flow from global financial institutions;

major underwriting fee revenues driver and could enhance fee potential for

some instruments and overall

17

$0

$5

$10

$15

$20

$25

$30

$35

BACJP

MW

FC C GS

MS

USBPNC

STICO

FBBT

BKFIT

BRF

KEYM

TBSTT

CMANTRS

HBANZIO

N MI

FHN

Contingent Capital Notes – Potential Issuance

Source: SNL, CreditSightsRepresents 2% of risk weighted-assetsAs of 4Q10. In $ billions.

18

Ratings Agencies: Proposed Changes

Source: S&P, Moody’s, CreditSights

• S&P

Places greater emphasis on country, economics, and industry risk

Individual company analysis increases importance of capital/funding

Earnings de-emphasized

Short-term debt: brokers more vulnerable to downgrade to A2

• Moody’s

Reassesses government willingness and capacity for support

Higher likelihood of govt. sharing bailout cost with debt holders

Focused mainly on the ratings impact to bank subordinated debt

Possible negative impact to acquirers of distressed banks

19

Mega-Trends: Banks

Higher operating leverage

- Cards: Convenience vs. Credit

- Basic Capital Markets/Transactions Services

- “Nuts & Bolts Banking” vs. “Casino Royale”

High margin products- C&I Lending (small/middle/large)

- CRE Lending

- Affluent Customers

- Pre-paid cards for non-prime

- Overseas Ops.

20

Mega-Trends: Possible Winners & Divestors

Bank of America

Citigroup

DIVESTORS

Bank of America

Citigroup

JPMorgan

Goldman Sachs

Morgan Stanley

ADAPTORS

FAVORS

Wells Fargo

Bigger Regional Banks

Citigroup

Processor Banks

Asset Managers

21

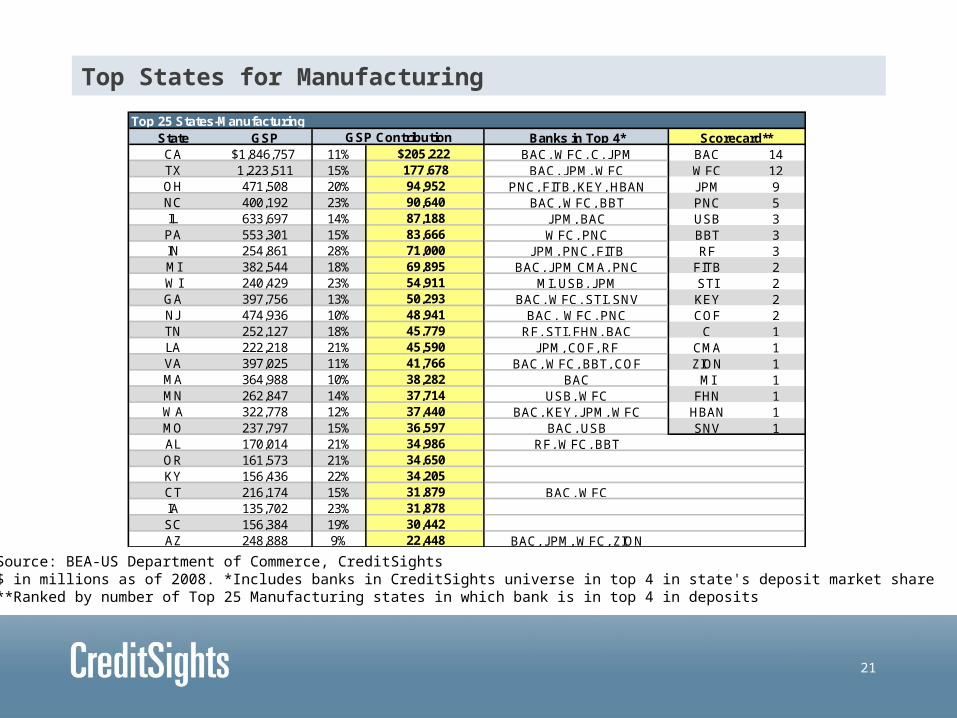

State GSP Banks in Top 4* Scorecard**CA $1,846,757 11% $205,222 BAC, WFC, C, JPM BAC 14TX 1,223,511 15% 177,678 BAC, JPM, WFC WFC 12OH 471,508 20% 94,952 PNC, FITB, KEY, HBAN JPM 9NC 400,192 23% 90,640 BAC, WFC, BBT PNC 5IL 633,697 14% 87,188 JPM, BAC USB 3PA 553,301 15% 83,666 WFC, PNC BBT 3IN 254,861 28% 71,000 JPM, PNC, FITB RF 3MI 382,544 18% 69,895 BAC, JPM CMA, PNC FITB 2WI 240,429 23% 54,911 MI, USB, JPM STI 2GA 397,756 13% 50,293 BAC, WFC, STI, SNV KEY 2NJ 474,936 10% 48,941 BAC, WFC, PNC COF 2TN 252,127 18% 45,779 RF, STI, FHN, BAC C 1LA 222,218 21% 45,590 JPM, COF, RF CMA 1VA 397,025 11% 41,766 BAC, WFC, BBT, COF ZION 1MA 364,988 10% 38,282 BAC MI 1MN 262,847 14% 37,714 USB, WFC FHN 1WA 322,778 12% 37,440 BAC, KEY, JPM, WFC HBAN 1MO 237,797 15% 36,597 BAC, USB SNV 1AL 170,014 21% 34,986 RF, WFC, BBTOR 161,573 21% 34,650KY 156,436 22% 34,205CT 216,174 15% 31,879 BAC, WFCIA 135,702 23% 31,878SC 156,384 19% 30,442AZ 248,888 9% 22,448 BAC, JPM, WFC, ZION

Top 25 States-ManufacturingGSP Contribution

Top States for Manufacturing

Source: BEA-US Department of Commerce, CreditSights$ in millions as of 2008. *Includes banks in CreditSights universe in top 4 in state's deposit market share**Ranked by number of Top 25 Manufacturing states in which bank is in top 4 in deposits

22

GSE Reform: U.S. Treasury Proposals

• Government and GSE role in housing finance likely to lessen, more private sector involvement

• Three Proposals:> Option 1: Limited govt role, privatized system of housing finance

> Option 2: Govt backstop, privatized system of housing finance

> Option 3: Govt reinsurance for MBS, privatized housing finance

• More discussion in 2011, probably punted to next Administration

23

Mortgage Mods: Response vs. Reality

• eHAMP> Obama program provides relief to indebted homeowners> Target of 7-8 million modifications> To date, 1.4 million trial modifications, 500K permanent modifications

• Potential Federal Regulators and State AGs Settlement> Force servicers to offer principal reductions if LTV>100%, subject to NPV test> May levy fines against infractions, fund programs to avoid foreclosures, etc.> Settlement costs could add up to $20B> GOP pushback against government strong arm tactics> Possible proportionate write-downs of 2nd liens

• Bank Initiated> More inclined to extend terms rather than principal reductions> Driven mostly by NPV tests

24

Reps & Warranties Risks: Estimated Capital Impact (BIS III)

Source: Company reports, CreditSightsIn $ millions. As of 3Q10. Assumes tax rate of 35%, and loss rate of 50% for first liens, 100% for second liens.

Bank of America: Estimated Tier 1 Common - 4Q12

2% 4% 6% 8% 10% 12%10% 8.8% 8.8% 8.7% 8.7% 8.7% 8.7%15% 8.8% 8.7% 8.7% 8.7% 8.6% 8.6%20% 8.8% 8.7% 8.7% 8.6% 8.6% 8.5%25% 8.7% 8.7% 8.6% 8.6% 8.5% 8.5%30% 8.7% 8.7% 8.6% 8.5% 8.5% 8.4%35% 8.7% 8.6% 8.6% 8.5% 8.4% 8.3%40% 8.7% 8.6% 8.5% 8.4% 8.3% 8.2%45% 8.7% 8.6% 8.5% 8.4% 8.3% 8.2%50% 8.7% 8.6% 8.5% 8.3% 8.2% 8.1%

Repurchase Requests as % of Remaining Loans

Acc

epta

nce

Rat

e

JPMorgan: Estimated Basel III Tier 1 Common - 4Q12

2% 4% 6% 8% 10% 12%10% 11.8% 11.7% 11.7% 11.7% 11.7% 11.7%15% 11.8% 11.7% 11.7% 11.7% 11.6% 11.6%20% 11.7% 11.7% 11.7% 11.6% 11.6% 11.5%25% 11.7% 11.7% 11.6% 11.6% 11.5% 11.5%30% 11.7% 11.7% 11.6% 11.5% 11.5% 11.4%35% 11.7% 11.6% 11.6% 11.5% 11.4% 11.3%40% 11.7% 11.6% 11.5% 11.4% 11.3% 11.3%45% 11.7% 11.6% 11.5% 11.4% 11.3% 11.2%50% 11.7% 11.6% 11.5% 11.3% 11.2% 11.1%

Repurchase Requests as % of Remaining Loans

Acc

epta

nce

Rat

e

25

Second-lien ExposuresHE Loans LTV >100% LTV >100% / HE Loans

Bank of America $137,981 $46,914 34%JPMorgan ** 88,468 40,873 46%Wells Fargo 117,744 39,086 33%Citigroup * 42,000 20,000 48%

Mortgage Modifications: Underwater Second-lien Loans

Source: Company reports, CreditSights* Estimated. Excludes Canadian, PR and LTSC HE loans'** JPM: >100% incl estimate for PCI loans from WM acquisitionAs of 4Q10. In $ millions

26

Tier 1 Common: Sensitivity to Write-Downs of HE >100% LTVBAC C JPM WFC

0% 7.8% 10.8% 10.0% 10.7%

10% 7.6% 10.7% 9.9% 10.5%

20% 7.5% 10.6% 9.7% 10.3%

30% 7.4% 10.5% 9.5% 10.1%

40% 7.2% 10.5% 9.4% 9.9%

50% 7.1% 10.4% 9.2% 9.7%

60% 7.0% 10.3% 9.1% 9.4%

70% 6.8% 10.2% 8.9% 9.2%

80% 6.7% 10.1% 8.8% 9.0%

90% 6.5% 10.0% 8.6% 8.8%

100% 6.4% 9.9% 8.4% 8.6%Wri

ted

ow

n o

f L

TV

>10

0% 2

nd

s

Mortgage Modifications: Potential Capital Impact – Second-liens

Source: Company reports, CreditSightsEst. impact: Net of estimated reserves, taxes. Includes 2 years of earnings retention.Potential capital impact of write-down of 2nd lien HE CLTV >100%As of 4Q10. Basel III Tier 1 common < 7% in red.

27

Potential Capital Impact from Mortgage Headwinds - BIS III Tier 1 CommonServicer Settlement Repurchases Home Equity Total Pro Forma

Bank of America 0.18% 0.29% 0.59% 1.06% 6.31%Citigroup 0.09% 0.05% 0.42% 0.56% 10.11%JPMorgan 0.15% 0.28% 0.70% 1.13% 8.63%Wells Fargo 0.31% 0.20% 0.95% 1.46% 8.91%Total Cost $16,000 $19,950 $58,749 $94,699

Potential Capital Impact from Mortgage Headwinds

Source: Company reports, CreditSightsEst. impact: net of estimated reserves, taxes. Includes 2 years of earnings retention.Servicer settlement: pro rata based on loans serviced.Repurchases: based on CreditSights’ estimated mid-caseHome equity: 40% write-down of 2nd lien HE CLTV >100%As of 4Q10. Basel III Tier 1 common, 7% requirement, when fully phased-in.

28

5Y CDS Range for Select Sectors

0 bps 25 bps 50 bps 75 bps 100 bps 125 bps 150 bps 175 bps

Big banks/brokers

Equip. Manufacturers

Oil and Gas

Telecos

Utilities

Consumer

Big Banks/Brokers Trade Much Cheaper than Industrials

As of 3/09/11Source: Bloomberg, CreditSightsBig Banks/brokers include: BAC, C, GS, JPM, MS, WFC

29

Bond/ CDS Recommendations

Sector Recommendation OAS* ReturnFIN. SERVICES Overweight -25 bps 1.65% U.S. Banks Overweight -25 bps 1.58% Big Banks** Overweight Regional Banks Overweight Specialty Finance Overweight -25 bps 1.43%ML U.S. Corporate Master -18 bps 1.22%

YTD 2011

Sector Recommendations: U.S. Bonds/ CDS

*YTD OAS for Merrill Lynch indices **Includes BAC, C, GS, JPM, MS, WFCAs of 3/09/11, YTD excess return represents the aggregate daily return vs. treasuries.Source: Bloomberg, CreditSights

30

Big Banks - OverweightOverweight Marketweight Underweight

Merrill Lynch Wells FargoMorgan Stanley U.S. BancorpBank of America JPMorgan

CitigroupGoldman Sachs

Regional and Mid-Sized Banks - OverweightOverweight Marketweight Underweight

Regions Fifth ThirdZions BB&T

M&T Bank PNCSunTrust Bank of New York

Marshall & IlsleyKeyCorp

HuntingtonComerica

Capital One

Specialty Finance - OverweightOverweight Marketweight UnderweightAlly Financial CIT (Shorter*) American Express

American General Finance Discover GATXCIT (Longer**) HSBC Finance H&R Block

Ford Motor Credit ResCap iStarGE CapitalSallie Mae

Credit Relative Value Recommendations

Sorted by ‘cheapest’ according to 5Y CDS relative value; *U.S. Bancorp according to 5Y cashRegionals according to 10Y cash, 5Y cash when applicable. Specialty Finance alphabetical*Shorter-dated bonds include 2013s, 2014s, 2015s. **Longer-dated bonds include 2016s, 2017s

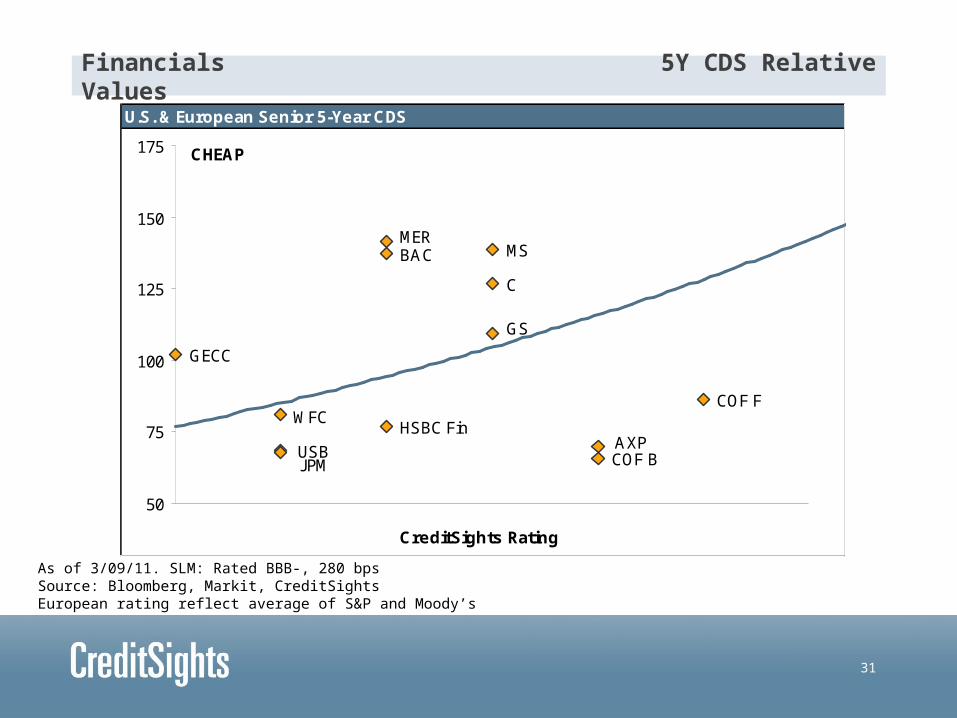

31

U.S. & European Senior 5-Year CDS

AXPHSBC Fin

GECC

COF F

COF B

MS

GS

JPM

MER

WFC

C

BAC

USB

50

75

100

125

150

175

CreditSights Rating

CHEAP

RICH

AA AA- A+ A A- BBB+ BBB

Financials 5Y CDS Relative Values

As of 3/09/11. SLM: Rated BBB-, 280 bpsSource: Bloomberg, Markit, CreditSightsEuropean rating reflect average of S&P and Moody’s

32

Ten Year Benchmark Bond Fair Value

GECCCOF

AXP

MSMER

GS

WFC

STI

RF

PNC

NCC

KEY

JPM

HBAN

FITB

C

BK

BBT

BAC

0

50

100

150

200

250

300

350

400

CreditSights Rating

Sp

read

to

10Y

Tre

asu

ry (

bp

)

RICH

CHEAP

AA AA- A+ A A- BBB+ BBB BBB- BB+

DFS

U.S. Financials 10Y Cash Relative Values

As of 3/09/11Source: MarketAxess, TRACE, CreditSights

33

Five Year Benchmark Bond Fair Value

GECC

COFAXP

MS

MER

GS

WFCUSB

STI

RF

PNCNCC

KEY

JPMFITB

CMAC

BK

BBT

BAC

0

50

100

150

200

250

300

350

400

450

CreditSights Rating

Sp

read

to

5Y

Tre

asu

ry (

bp

)

RICH

CHEAP

AA AA- A+ A A- BBB+ BBB BBB- BB+

ZION

MI

U.S. Financials 5Y Cash Relative Values

As of 3/09/11Source: MarketAxess, TRACE, CreditSights

34

Trust Preferred Securities: Select OpportunitiesCompany Coupon Price Yield Call Date STC PremiumRegions Financial 8.9% 26.55 8.4% 06/15/13 5.1% 6%Zions Bancorporation 8.0% 25.18 7.9% 09/01/07 7.0% 1%Citigroup 7.9% 26.00 7.6% 12/15/12 4.7% 4%Merrill Lynch (BofA) 7.4% 25.55 7.2% 09/15/12 5.2% 2%Bank of America 7.0% 24.97 7.0% 02/01/07 6.9% 0%Merrill Lynch (BofA) 6.5% 23.83 6.8% 06/15/12 10.1% -5%Fifth Third 7.3% 25.09 7.2% 11/15/12 6.4% 0%JPMorgan 7.0% 25.28 6.9% 01/31/02 5.5% 1%Wells Fargo 7.0% 25.32 6.9% 08/29/06 5.4% 1%

Preferred Stock: Select OpportunitiesCompany Coupon Price Yield Call Date STC PremiumZions Bancorporation 11.0% $27.33 10.1% 06/15/12 2.5% 9%Citigroup 8.5% 25.99 8.2% 06/15/13 5.8% 4%Bank of America 8.2% 26.20 7.8% 05/01/13 5.0% 5%JPMorgan 8.6% 27.74 7.8% 09/01/13 2.4% 11%PNC 8.3% 1,075.00 7.7% 05/21/13 4.3% 8%Wells Fargo 7.5% 1,030.00 7.3% NM NM 3%

Bank Hybrids: Trade Recommendations

Source: SNL, CreditSightsAs of February 22, 2011. Premium to par value. STC: Yield over comparable UST, based on call date.Sorted by yield/company. Most $25 par instruments, except WFC & PNC Pfds. ($1,000)

35

CreditSights’ Equity Recommendations

1Q11 2Q11 3Q11 4Q11 FY 11 Price InvestmentCompany EPS ($) EPS ($) EPS ($) EPS ($) EPS ($) Target ($) RecommendationBank of America 0.33E 0.35E 0.40E 0.45E 1.53E 15.00 MarketweightCitigroup 0.15E 0.15E 0.15E 0.15E 0.60E 5.95 OverweightGoldman Sachs 5.00E 4.75E 4.50E 5.25E 19.50E 195.00 OverweightJPMorgan Chase 1.10E 1.15E 1.20E 1.25E 4.70E 49.00 OverweightMorgan Stanley 0.75E 0.75E 0.75E 0.90E 3.15E 30.00 MarketweightU.S. Bancorp 0.48E 0.53E 0.58E 0.60E 2.19E 31.00 OverweightWells Fargo 0.65E 0.70E 0.75E 0.77E 2.87E 36.00 Overweight

36

U.S. Banks/Brokers: Key Drivers

• Bank of America> Revenue: solid capital markets, slow consumer> Manageable reps and warranties risk> Could increase dividends/repurchases in 2H11, prudent to wait until 2012> Provisions could decline to quarterly run rate of $4B, from $10B in 2009

• Citigroup> Unique international franchise, expand in BRIC+10> Strongest capital among traditional banks> Positioned to return capital, blocked by UST/FDIC TruPS until TLGP ends> Not a major mortgage originator; limited reps and warranties risk

• JPMorgan> Hoping to return capital to shareholders ASAP> Reps and warranties risk to GSEs/private labels manageable; HE overhang> Revenues driven by broad client franchise and capital markets> Expand internationally through wholesale banking strategy

37

U.S. Banks/Brokers: Key Drivers

• Wells Fargo> Reps and warranties manageable: mostly GSE; large HE run-off> Focus on cross-selling; impacted the most by debit interchange> Could look to return capital; capital somewhat lower on BIS III

• Goldman Sachs> More focused on share repurchases than dividends> Revenue helped by broad client franchise in FI, equities, and commodities> Growth strategy focused on BRIC+10

• Morgan Stanley> More work to be done to reach BIS III capital levels> Revenues hampered by underperformance in sales and trading> Asset/Wealth Management stabilizing; growth scarce

• U.S. Bancorp> Hoping to return capital to shareholders ASAP> Focus on growth of fee-generating businesses (processing, wealth mgmt)> Commercial loan growth could become key balance sheet driver

38

Strategic M&A Possibilities

Source: Bloomberg, SNL, CreditSightsRatings impact to target. Bold: Financially attractive

Strategic M&A TargetsBuyer Target EPS Accretion IRR Ratings ImpactU.S. Bancorp Fifth Third 2% 20% +3-4 notches

Regions 3% 16% +5-6 notchesSunTrust 0% 17% +3-4 notchesM&T Bank -7% 14% +2-3 notches

PNC Financial Fifth Third 0% 18% +0-1 notchesRegions 1% 14% +2-3 notchesKeyCorp -2% 11% +0-1 notchesSunTrust -4% 14% +0-1 notchesM&T -12% 11% -1-0 notches

BB&T Regions 7% 16% +4-5 notchesSunTrust 1% 17% +2-3 notches

Comerica Zions 1% 12% +5-6 notchesBMO Financial Fifth Third 7% 19% +4-5 notches

Regions 8% 15% +6-7 notchesKeyCorp 4% 12% +4-5 notches

Royal Bank of Canada

Regions 4% 18% +8-9 notches

Fifth Third 4% 23% +6-7 notchesSunTrust 3% 18% +6-7 notches

Capital One Regions 4% 13% +1-2 notchesSunTrust 0% 15% +0-1 notches

39

Copyright © 2011 CreditSights, Inc. All rights reserved. Reproduction of this report, even for internal distribution, is strictly prohibited. The information in this report has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. If you have any questions regarding the contents of this report, contact CreditSights, Inc. at (1) 212 340-3840 in the United States or (44) 20 7429 2080 in Europe. CreditSights Limited is authorised and regulated by The Financial Services Authority. This product is not intended for use in the UK by Private Customers, as defined by the Financial Services Authority.

![The Semantic Web: [You are here] Professor James Hendler hendler Director, Semantic Web and Agent Technologies Maryland Information.](https://static.cupdf.com/doc/110x72/5514e0cd550346b0338b5869/the-semantic-web-you-are-here-professor-james-hendler-httpwwwcsumdeduhendler-director-semantic-web-and-agent-technologies-maryland-information.jpg)