Model Validation across geographic

areas

Factoring in local variations to ensure accuracy of

assumptions

Nic Talbot-Jenkins

Typical Company Organisation

Global

Overview/Strategy

International US Europe

Local Markets/Affiliates/Operating Companies

To many ‘international’ companies, ‘Global’ can be

synonymous with ‘US’

Clear voice needs to be heard from the regions at

a global level

Central vs Local Forecasting

Why not forecast centrally?

Pros:

– one version of forecast & model, one keeper

– time-efficient (?)

Cons:

– miss local variation

– highly sensitive to the skill of the forecaster (errors are

amplified throughout the reach of the model)

– remote perspective

– may not reflect what is achievable in the market-place

Local vs Centralised Forecasting Why forecast locally or at a regional level?

Pros:

– closer to the market

– capture key market variations

– engage & encourage the local markets

– more robust forecast

– commercially viable/endorsed figures

Cons:

– can require extensive organisation

– time-consuming, takes time to achieve final result

The main issue - Creating a European Voice to be heard Globally………..

‘Aligned’ position needs to be fed to Global

Constant struggle for funds, resource, data etc

Understanding of EU diversity to provide robust

regional voice which represents the best business

interests for Europe

Managing Diversity Across

Europe

European Diversity

Regions & countries vary immensely

Difficult concept for Global to understand

sometimes as US is a main comparator

Diversity needs to be understood & captured in

order to provide a comprehensive view for Europe

Diabetes & the Oral Antidiabetic market as a

working example

Forecasting…………...

Forecasting is difficult enough, let alone with over

20 different markets to consider!

Patient based vs script driven

Either method needs local consideration

What needs to be considered and how can that be

managed?

Considerations - 1. Population / Patients

Epidemiology

– varies from country to country

Variances can be caused by a number of factors

– cultural variations

– demographic differences

– genetic predisposition

Different numbers of eligible patients in different

countries

Population Variance Example:

Data from UN population database (units - 000s)

0

1000

2000

3000

4000

5000

6000

7000

0-4

10-

14

20-

24

30-

34

40-

44

50-

54

60-

64

70-

74

80-

84

France

Germany

Italy

Spain

UK

Poland

Demographic Impact

Impact on disease - age-related conditions,

increase in availability of patients for treatment

Accounts for some variation in disease prevalence

Important to take into account when forecasting

across Europe

Eg. Diabetes type 2

Type 2 Diabetes:

If we took a flat rate of disease & applied to an EU

population indiscriminately…………

However, if we take a more robust process & apply

local data by age-cohort…………….

What’s Happening Demographically...

0

1000

2000

3000

4000

5000

6000

7000

8000

0-4

10-

14

20-

24

30-

34

40-

44

50-

54

60-

64

70-

74

80-

84

2001

2005

2010

2013

Data from UN population database (units - 000s). Data shown is for

Germany

Population Variance through (miss) Calculation

3500

3600

3700

3800

3900

4000

4100

4200

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Point Value

Age Mapped

Cumulative Difference ~ 2.8M

Overall

prevalence

rate of 5%

applied in

both

scenarios!!

Prevalence Calculations

Through this example we can see the benefit of

proper demographic modelling of populations.

This method should ideally be used in all countries.

Same age-cohort prevalence rates can be used in

this way, overall calculated prevalence is then tied

into the demographic map of the market.

You may find that this resolves issues with

divergent epidemiological data!

Considerations - 2. Market Variations - Products & Usage As well as population & cultural differences there

are vast differences across Europe in terms of

products & competitors

Germany - wide use of herbal remedies

Italy - OAD market consists of combination

products (not widely seen elsewhere in Europe)

Consideration of local competitors is key to

unlocking market potential

Has knock-on effects on product positioning &

marketing

Product Usage Variations - OAD Market

Difference in packs available in some markets

Tablet strengths

Key competitors vary

– Germany - mainstay of treatment are the SUs

– UK - Metformin becoming drug of choice first line

Strategy clearly needs to be very different to sell

against the SUs vs metformin (different modes of

action etc)

Impact on Patient Turnover

1st line therapy will affect the rate of turnover of the patient pool

SUs - not sustainable long term for 1st line use, patients will fail to be maintained quicker & progress to 2nd line

Metformin - patients maintained for far longer, slower to reach 2nd line therapy

Important for the TZD class as they are indicated as 2nd line combination therapy

Country market potential will vary hugely depending on the treatment paradigm

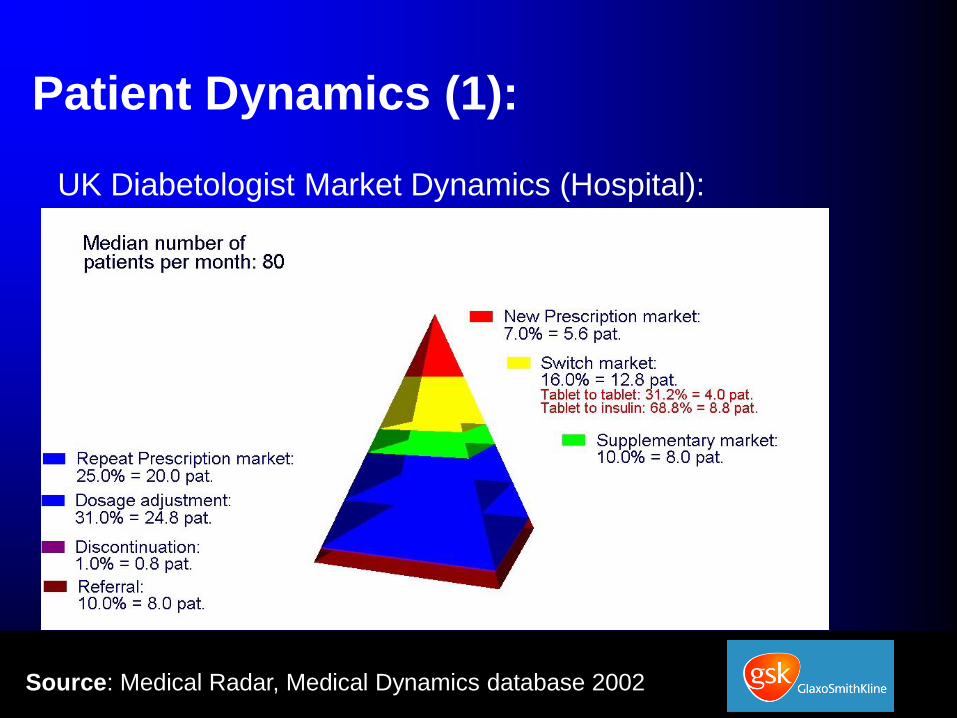

Patient Dynamics (1):

Source: Medical Radar, Medical Dynamics database 2002

UK Diabetologist Market Dynamics (Hospital):

Patient Dynamics (2):

German Diabetologist Market Dynamics (Hospital):

Considerations - 3. Healthcare Access

Very different access methods for healthcare

across Europe

France - free access to specialists & medications

UK - GP ‘gatekeepers’, patients need referral to

specialist

Reimbursement of medications - partial

reimbursement of some medications in various

markets (e.g. Sweden - % of price, Germany - 3 co-

payment bands depending on pack size)

Considerations - 4. Reimbursement

Reimbursement issues vary by market

– political (Germany - positive list - TZDs are absent,

only access to private patients)

– legal (EU legislation advises member states to take

measures to control their own healthcare spend,

Finland - no reimbursement available to products <1

on market)

– environmental (GDP in country & ability to pay for

healthcare/medications)

Considerations - 5. Pricing

Price levels - no uniform price across Europe

(although a price corridor exists)

Lower prices in Europe than in US (price often

overestimated by Global colleagues)

Reference pricing - markets reference internally,

externally or both to set prices for new products

– Internal - review of similar products in similar

classes to set price

– External - review of neighbouring markets to set

prices

Internal & External Reference Pricing Austria Notification of the price of the product in other EU

CountriesBelgium Notification of the price of the product in other EU

countriesDenmark Average of prices of all European Economic Area (EEA)

countries except Greece, Luxembourg, Portugal andSpain

Finland Notification of the price of the product in other EUcountries

France No external referencing

Germany No external referencing

Greece Lowest price in all EU countries

Ireland Denmark, France, Germany, Netherlands, UK

Italy Average European price

Netherlands Belgium, France, Germany, UK

Norway Average of the three lowest prices of 9 EEA countries(Austria, Belgium, Denmark, Finland, Germany, Ireland,Netherlands, Sweden and U.K.)

Portugal France, Italy, Spain

Spain Notification of the price of the product in other EUcountries

Sweden Notification of the price of the product in other EUcountries

Switzerland Denmark, Germany, The Netherlands, U.K.

U.K. No external referencing

Cost-Containment Measures by Markets

Fra

nce

Ge

rma

ny

Gre

ece

Hu

ng

ry

Ita

ly

Th

e

Ne

the

rla

nd

s

No

rwa

y

Sp

ain

Sw

ed

en

Sw

itze

rla

nd

UK

Control ex-man. Price X X X X X X X X

Ctrl reimburs. Entry X X

Cross-country comp. X X

Reference pricing X X X X X X

Payback/contracts X X X X X X

Profit control X X X X X X X X X

Promotional spent ctrl X X X X X X X X

Prescribing budgets X X X X X X X X

Pharmacoecon. Evid. X X X X X X

Fixed wholesale margin X X X

Fixed pharmacy margin

Generic substitution X X X X X

Patient co-payment X

Control of OTC price X X X X X X X X X

Control of hospital price X X X X X X X X

Product Launch Sequence

Vital in Europe to get the launch sequence right

Highest price markets should obtain a price first

Reference markets to high price markets can then

achieve the price they want (within the EU pricing

corridor)

If low price markets launch first, will mean a lower

average price for the product across Europe

Examples:

Greece - have to take the lowest average EU price

available to them at time of launch.

France - aggressive negotiations to lower new

product prices. E.g. if France launch with a low

price it will be very difficult for Germany to achieve

a higher price.

Germany & UK (so-called free price markets)

should ideally be the first countries to launch a new

product in Europe

Market Access & Impact on Launch Time

Due to market access restrictions, there is no

uniform launch date across Europe

Germany & UK tend to launch first, followed by

Spain, Italy and finally France (~12 months)

Again, this needs to be included at a country level

before forecasts can be rolled together

Considerations - 6. Patent Life/Protection Issues are coming to the fore regarding patent & data

exclusivity (Fosamax weekly in UK)

Spain - limited data exclusivity period

Large chunk of revenue may disappear due to the knock-on effects of price erosion (through reference pricing)

E.g. Fosamax weekly goes generic in UK, lowers the price of the M5B oral class

– Downward pressure in other EU markets which use external referencing, especially for Fosamax

– Any new entrants will be forced to price in a market where genericisation has occurred

– Lower prices will be awarded to new bisphosphonates in UK, as internal referencing to the M5B class

How to Practically Manage &

Forecast the Diversity

One Successful Approach……

Central template disseminated to markets - which

includes all necessary tools to assist the markets in

providing a solid, robust forecast

European initiatives

– educate markets in forecasting

– prepare & engage their focus on the product,

therapy area

– provide a European ‘owner’ to work with markets

– challenge markets on assumptions & rationale

– password-protect the Excel workbook template!!!

Or Alternatively………..

Forecast at a European level

Provide markets with a list of assumptions & a

forecast

Ask for them to validate the figures & sign off at a

local level (GM or equivalent)

Either process should end up with a robust,

validated local & regional forecast to be integrated

into the global business plans